Ultrasound Gel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

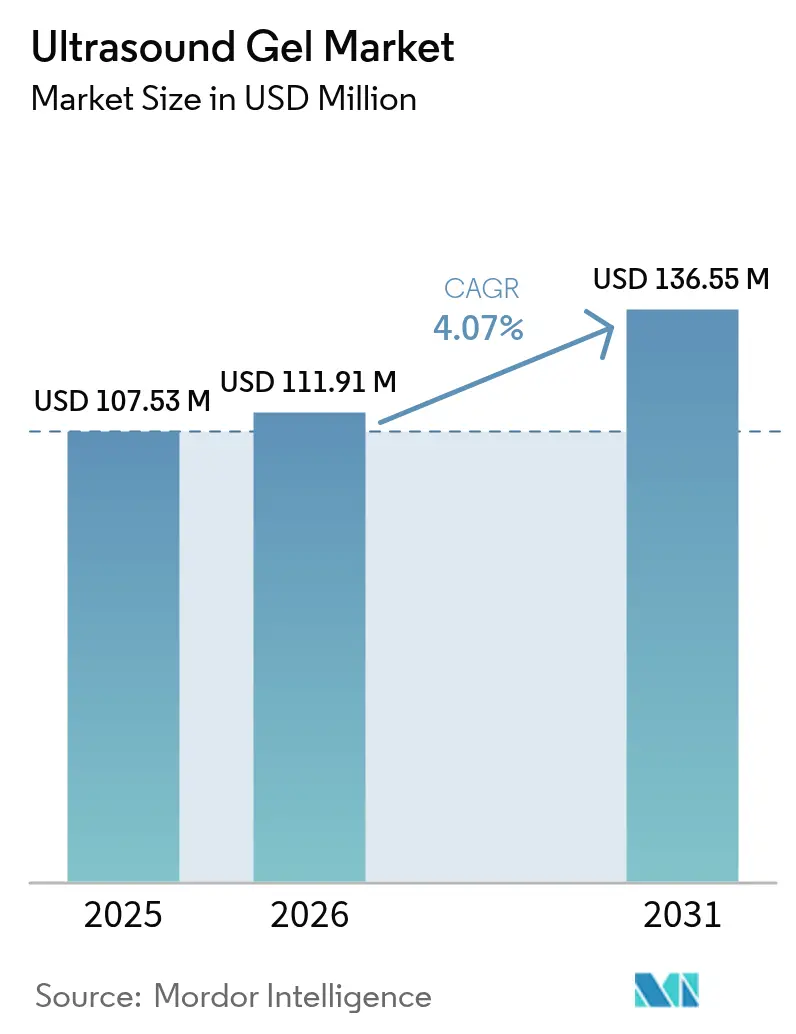

| Market Size (2026) | USD 111.91 Million |

| Market Size (2031) | USD 136.55 Million |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

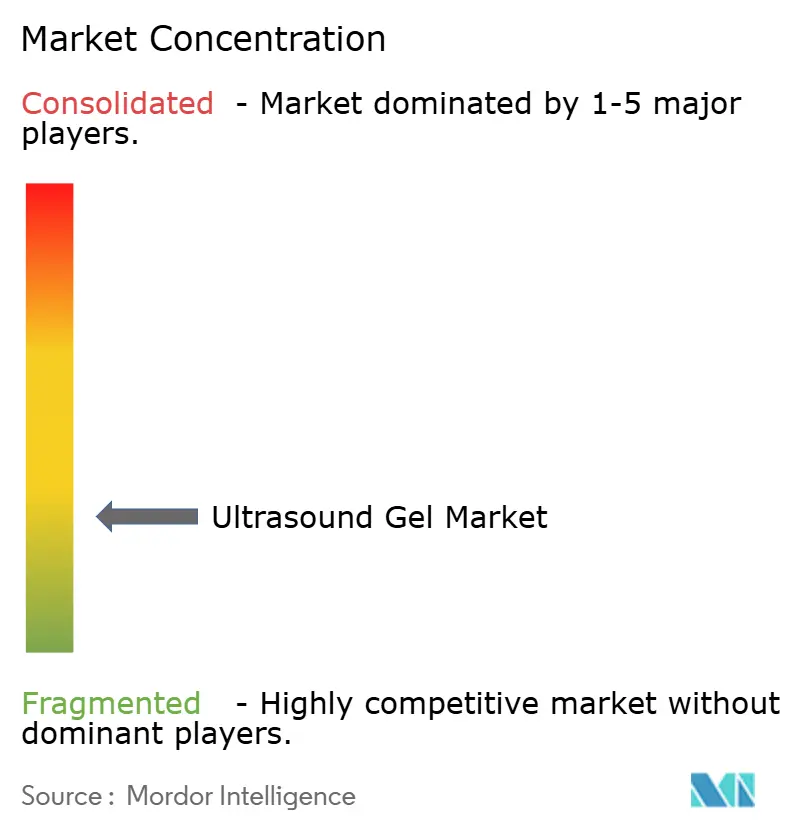

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasound Gel Market Analysis by Mordor Intelligence

The Ultrasound Gel market size is expected to grow from USD 107.53 million in 2025 to USD 111.91 million in 2026 and is forecast to reach USD 136.55 million by 2031 at 4.07% CAGR over 2026-2031.

The baseline growth reflects increasing procedure volumes across diagnostic imaging, physiotherapy, and emerging aesthetic segments. Miniaturization of ultrasound systems for point-of-care use, coupled with rising demand for high-frequency transducers, is reshaping purchasing patterns and product specifications. Supply chains are adapting to single-use, sterile packettes that align with infection-control standards in emergency and critical-care environments. At the same time, retail e-commerce channels are gaining importance as home-based physiotherapy and dermatology treatments proliferate. Competition remains moderate, with global brands defending share against agile regional players that offer specialized formulations tuned to local clinical preferences.

Key Report Takeaways

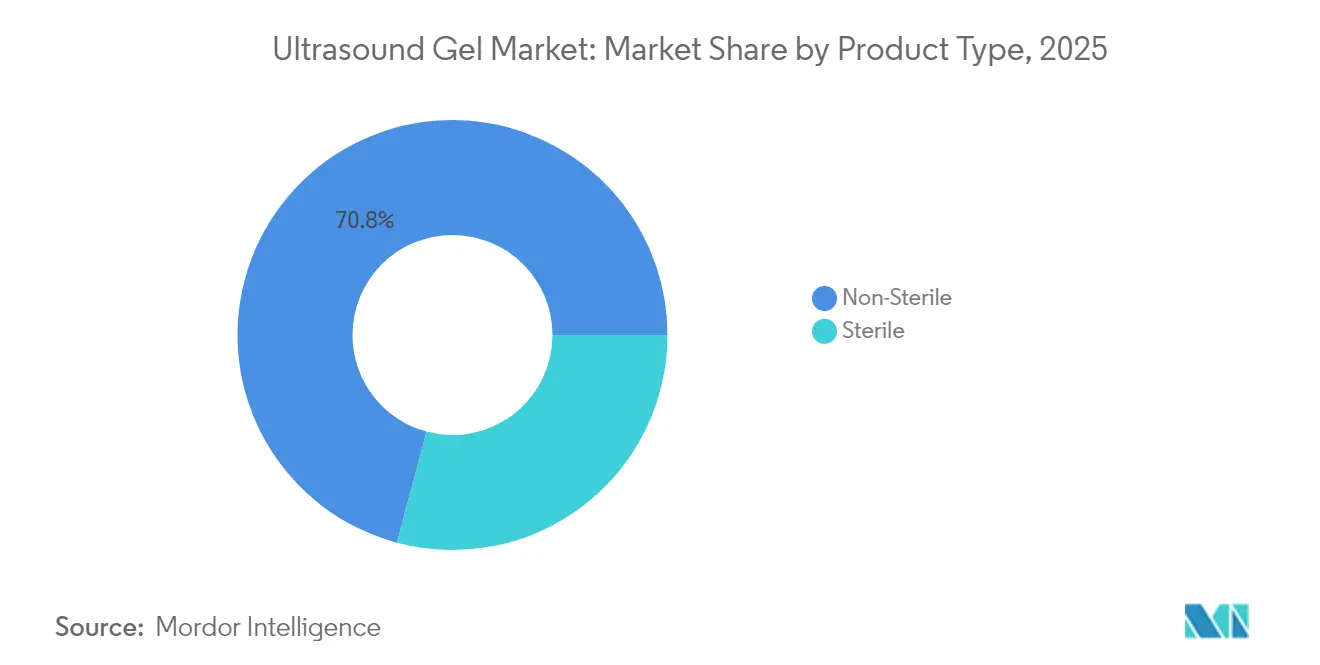

- By product type, non-sterile formulations led with a 70.84% revenue share in 2025, while sterile gels are expanding at an 8.18% CAGR through 2031.

- By application, diagnostic imaging accounted for 86.95% of the ultrasound gel market share in 2025, whereas aesthetic and dermatology procedures are advancing at an 10.94% CAGR to 2031.

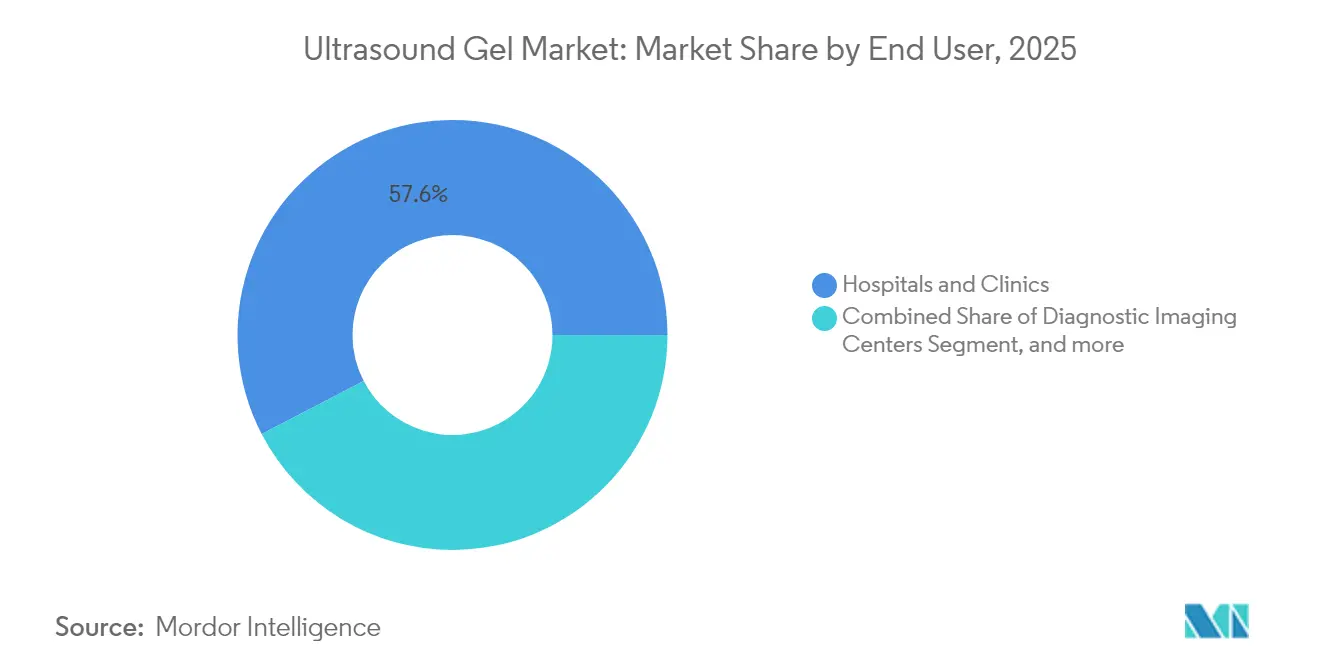

- By end user, hospitals and clinics held 57.62% of the ultrasound gel market size in 2025, and the home-care and retail segment is forecast to grow at a 12.11% CAGR between 2026 and 2031.

- By geography, North America commanded 38.92% of global revenue in 2025, while Asia-Pacific is set to expand at an 8.54% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultrasound Gel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of POCUS in emergency & primary care | +1.2% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Rapid procedure growth in obstetric & gynecologic ultrasound | +0.8% | Global, higher impact in Asia-Pacific | Medium term (2-4 years) |

| Shift toward high-frequency linear transducers needing low-viscosity, air-bubble-free gels | +0.7% | North America, Europe, advanced Asian markets | Medium term (2-4 years) |

| Expansion of home-based physiotherapy & aesthetic ultrasound treatments | +1.4% | North America, Europe, urban Asia | Short term (≤ 2 years) |

| Proliferation of handheld & wireless ultrasound devices | +0.6% | Global | Short term (≤ 2 years) |

| Growing use of ultrasound in sports medicine | +0.5% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Point-of-Care Ultrasound (POCUS) in Emergency & Primary Care

POCUS devices are moving routine imaging from radiology suites to triage rooms and community clinics, sharply widening the user base for single-use gels. WONCA formally recognized POCUS as a core diagnostic tool for family physicians in 2024, validating demand among primary-care providers.[1]WONCA, “Position Statement on Point-of-Care Ultrasound in Primary Care,” CAMBRIDGE.ORG Market penetration of handheld probes such as Vscan Air, Mindray TE Air, Lumify, and Butterfly iQ+ demonstrates a clear link between portable hardware and incremental gel consumption. Sterile packettes minimize cross-contamination when devices travel between patients, aligning with infection-control protocols. As POCUS becomes routine in ambulances and telehealth visits, manufacturers are developing pocket-sized sachets designed for quick disposal. This adoption trend is expected to lift baseline unit volumes even in mature hospital markets.

Rapid Procedure Growth in Obstetric & Gynecologic Ultrasound

Medical schools are incorporating simulator-based training programs that accelerate proficiency in obstetric and gynecologic scanning.[2]A. L. Papenburg et al., “Simulator-Based Training in Obstetric Ultrasound,” FRONTIERSIN.ORG Higher graduation rates of skilled sonographers translate into more scans per facility, raising steady-state gel demand. Procedure volumes are also expanding in private fertility clinics and midwifery practices, where ultrasound confirms fetal well-being without radiation exposure. Asia-Pacific markets, especially India and China, show steep growth in ante-natal screening programs, reinforcing regional consumption of cost-efficient non-sterile bottles. Product innovations now include color-tinted gels that improve visualization during chorionic-villus sampling, underscoring the need for niche formulations.

Shift Toward High-Frequency Linear Transducers Requiring Low-Viscosity, Air-Bubble-Free Gels

High-frequency ultrasound systems operating at 10 MHz-20 MHz are standard in dermatology and vascular imaging, but acoustic energy dissipates rapidly if air pockets exist between probe and skin. Clinical studies confirm that optimized coupling media maintain image resolution and diagnostic accuracy at 20 MHz, resolving superficial lesions in 87.9% of cases.[3]J. S. Kim et al., “High-Frequency Ultrasound for Dermatology,” MDPI.COM Gel suppliers therefore reformulate viscosity, wetting agents, and preservative loads to meet narrower acoustic impedance ranges. Specialist clinics purchase premium micro-bubble-free variants despite price premiums, signaling a value-over-volume strategy in this submarket. Regulatory clearance timelines remain manageable because base ingredients are well understood, enabling rapid commercial rollout.

Expansion of Home-Based Physiotherapy & Aesthetic Ultrasound Treatments

Consumer-grade therapy devices now target musculoskeletal pain relief, cellulite reduction, and collagen stimulation. Retail chains and e-commerce channels stock branded packets in 60 mL-100 mL sizes compatible with home applicators. TridentCare’s partnership with Essence Healthcare offers in-home ultrasound diagnostics to 60,000 Medicare Advantage members from January 2025, broadening clinical exposure to single-use gels. Aesthetic brands such as CellSound promote sound-wave devices for non-invasive fat reduction, each session consuming fresh gel sachets. Manufacturers are refining fragrance-free, hypoallergenic formulas to reduce skin reactions in non-clinical settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emergence of gel-free dry transducer & membrane-coupling technologies | -0.9% | North America and Europe | Long term (≥ 4 years) |

| Regulatory scrutiny of preservatives elevating reformulation costs | -0.4% | Europe with spill-over to North America and Asia | Medium term (2-4 years) |

| Disposal challenges for single-use plastic sachets in sustainability-focused regions | -0.7% | Europe, growing impact in North America and Japan | Medium term (2-4 years) |

| Temperature sensitivity & patient discomfort | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Emergence of Gel-Free Dry Transducer & Membrane-Coupling Technologies

Research groups have demonstrated conformable ultrasound patches that create cavitation pockets without coupling gel, achieving 26.2-fold transdermal delivery of active ingredients in pre-clinical trials. Dermatology practices also experiment with water-filled gloves and disposable membranes as quick alternatives to gel coatings. While commercialization remains early, institutional buyers may pivot once dry interfaces reach cost parity, posing a structural threat to long-range volume growth. Gel suppliers are responding with hybrid products that pair thin hydrogel layers with disposable membranes, aiming to slow adoption of fully gel-free systems.

Regulatory Scrutiny of Preservatives Elevating Reformulation Costs

The European Commission now limits methylparaben levels to 0.4% in single-agent use and 0.8% in blends, forcing companies to reformulate legacy SKUs. Reformulation demands extensive stability and microbiology testing, lengthening time-to-market and raising R&D spend. Natural antimicrobial systems using organic acids or plant extracts are under evaluation, yet they can accelerate oxidation of water-soluble polymers. Temporary supply gaps or price hikes may follow as firms exhaust existing inventories, particularly in European distribution hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Sterile Dominance with Sterile Surge Continues

Non-sterile gels retained a 70.84% revenue share in 2025, driven by routine radiology and physiotherapy sessions that collectively absorb high daily volumes. The ultrasound gel market size for non-sterile bottles is projected to grow steadily despite increasing unit conversion to sterile packettes. Hospitals remain primary buyers, but sports-medicine clinics and academic labs constitute a stable secondary channel. Vendors emphasize pump-style packaging that limits backflow contamination during high-throughput scanning days.

Sterile formulations, although smaller in absolute terms, are projected to post an 8.18% CAGR through 2031, the fastest within product segmentation. Stringent infection-control protocols in interventional radiology suites and intensive-care units underpin this trajectory. The ultrasound gel market share for sterile packettes is expected to climb as disposable sachets replace bulk bottles in invasive procedures. Manufacturers are leveraging gamma-irradiation and e-beam sterilization to preserve rheology while achieving validated sterility assurance levels.

By Application: Diagnostic Imaging Anchors Revenue while Aesthetic Use Accelerates

Diagnostic imaging maintained an 86.95% share of 2025 consumption. The ultrasound gel market size for this segment fueled by ongoing deployments of general-purpose carts in public hospitals. Cost containment efforts favor multi-liter jugs and refillable dispensers, underpinning supplier volumes. End-user education on bottle hygiene mitigates contamination risk without incurring the premium of sterile packettes.

Aesthetic and dermatology treatments recorded an 10.94% CAGR, the fastest across all uses. High-frequency systems for wrinkle reduction and scar assessment require gels with precise acoustic impedance and low drying rates. Sofwave’s SUPERB platform and similar devices recommend proprietary coupling media that command price premiums two to three times higher than standard gels. Tight-margin retail therapy brands still opt for private-label formulations, creating a bifurcated pricing structure within the niche.

By End User: Hospitals Lead while Home-Care Disrupts

Hospitals and clinics captured 57.62% of 2025 volumes. This share stems from broad procedural coverage abdominal, cardiac, obstetric, vascular and 24/7 operating patterns that necessitate bulk supplies. Purchasing consortia secure multi-year contracts, locking in favorable unit prices and stable supply.

The home-care and retail segment, forecast to deliver a 12.11% CAGR, is reshaping distribution. Direct-to-consumer e-commerce now offers pre-measured packettes positioned alongside handheld ultrasound gadgets. Parker Laboratories markets hypoallergenic Sound Enhancing gel in 100 mL tubes that fit consumer medicine cabinets. Subscription models bundle gel refills with replacement adhesive patches, signaling a pivot to consumables-plus-device revenue streams.

Geography Analysis

North America accounted for 38.92% of global revenue in 2025. High procedure density, favorable reimbursement, and early adoption of POCUS underpin this leadership. Hospitals increasingly standardize on sterile packettes for invasive use, bolstering premium segment growth. Providers also pilot gel-free patches, illustrating the region’s dual role as volume anchor and innovation testbed. Academic grants fund biodegradable-packaging research, opening doors for suppliers offering plant-based sachets.

Asia-Pacific is the fastest-growing territory with an 8.54% CAGR. Expanding health-insurance coverage enables mid-tier city hospitals in China and India to procure portable ultrasound carts, thereby uplifting annual scan counts. Local manufacturers penetrate price-sensitive markets with cost-optimized non-sterile gels, but multinationals still dominate specialty sterile products. Urban consumers increasingly seek at-home aesthetic treatments, feeding retail demand. Government screening campaigns for maternal-fetal health further propel volume.

Europe maintains a sizeable footprint, although growth is modest relative to Asia-Pacific. Strict preservative guidelines compel continuous reformulation, raising compliance costs but also differentiating premium offerings. Sustainability mandates spur experimentation with PLA and PHA sachet materials, with pilot programs underway in Germany and the Nordics. Hospitals embrace tele-ultrasound services for geriatric care, indirectly boosting single-use packette consumption.

Middle East & Africa and South America contribute smaller but rising shares. GCC nations invest in high-end diagnostic centers, favoring sterile packettes that complement imported ultrasound consoles. Brazilian obstetric practices ramp up routine prenatal scans, while Argentina’s private clinics adopt aesthetic ultrasound in metropolitan areas. Local distributors form exclusive agreements with Parker Laboratories, HR Pharmaceuticals, and Medline to secure supply continuity.

Regulatory Landscape

Ultrasound gel is regulated as a medical device in major markets, with classification and evidence expectations that shape labeling, claims, and documentation. In the United States, ultrasound gel is commonly handled under FDA Class II device requirements tied to 21 CFR 892.1570 (product code MUI). This drives Quality System Regulation compliance (21 CFR 820) and predicate-based 510(k) pathways for market access. In Europe, conductive gels used externally are generally treated as non-invasive devices under the EU Medical Device Regulation (MDR 2017/745), and the MDCG 2021-24 guidance is used to interpret borderline cases and classification principles that affect conformity assessment activities.

Across regions, biocompatibility and risk management are central anchors for formulation changes and new SKUs. ISO 10993-1 (latest 2025 edition) is used for biological evaluation planning based on contact type and duration, increasing the need for structured risk-management evidence when preservatives, fragrances, dyes, or other additives are adjusted. Infection-prevention guidance also influences product format decisions: the UK Health Security Agency has published good infection prevention practice for ultrasound gel use, reinforcing the separation between sterile single-use gel for higher-risk procedures and non-sterile formats for intact skin applications. That separation supports the shift toward sterile packettes in acute and interventional settings.

Competitive Landscape

The global field is fragmented wherein Parker Laboratories, HR Pharmaceuticals, and Medline Industries lead through extensive distribution, trusted brand equity, and diversified portfolios. Parker’s Aquasonic line retains broad clinical acceptance, while its precision-flow packettes address contamination concerns in vascular labs. HR Pharmaceuticals targets procedure-specific niches with bacteriostatic formulas and color-coding for easy identification. Medline leverages hospital supply contracts to cross-sell gels alongside disposable drapes and ancillary supplies.

Regional challengers in China and India develop low-viscosity blends tailored for portable devices, often pricing 15%-20% below global brands. Some players co-develop hydrogel sheets with device makers to secure design-win positions in emerging gel-free systems. Sustainability has become a competitive axis; Elkem’s PURESIL ORG elastomer gels, derived from sugar-cane feedstock, appeal to European buyers focused on carbon reduction.

Product adjacencies bolster loyalty. Parker’s Thermasonic gel warmer allows clinicians to set temperatures between 97 F and 109 F for patient comfort, reinforcing brand preference when bundled with Aquasonic bottles. Strategic acquisitions in logistics matter too. UPS acquired Frigo-Trans and BPL in January 2025 to expand temperature-controlled warehousing, ensuring stable supply for heat-sensitive gels in Europe.

Ultrasound Gel Industry Leaders

Compass Health Brands

National Therapy Products Inc.

HR Pharmaceuticals, Inc.

Medline Industries LP

OJI Group (SONOFAX Sdn)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities in ultrasound gel are increasingly tied to infection control and the operational shift to point-of-care scanning, where gel is used alongside portable devices across patient locations. Professional and clinical guidance that emphasizes safe gel handling and sterile, single-use packets for higher-risk or non-intact skin procedures supports premiumization of sterile packettes and smaller-format packaging for emergency, ICU, and home-visit workflows. The report context also highlights market pull from in-home diagnostics, including TridentCare working with Essence Healthcare to deliver portable ultrasound diagnostics to more than 60,000 Medicare Advantage members, which creates a practical channel for single-use and easy-disposal formats.

Another area of differentiation is reformulation and compliance-led positioning as preservative scrutiny increases and facilities standardize procurement around documented quality systems. Manufacturers that can demonstrate biocompatibility planning aligned to ISO 10993-1 and validated sterilization approaches (where applicable) can expand within sterile and procedure-specific segments, including dye-free and hypoallergenic variants for dermatology and high-frequency imaging workflows. Broader distribution capabilities also support scale in retail and home-care presence, including Drive Medicals agreement to acquire Compass Health Brands, which includes consumer medical product lines spanning ultrasound gels and can be pushed through established durable medical equipment channels.

Recent Industry Developments

- January 2026: Drive Medical signed a definitive agreement to acquire Compass Health Brands, expanding its branded and private-label portfolio that includes TheraMed ultrasound gels. The deal integrates a gel consumable line into a larger home medical equipment platform, strengthening cross-selling into retail and home-care channels where smaller-pack formats are gaining traction.

- July 2025: TridentCare and Essence Healthcare partnered to deliver portable ultrasound diagnostics to more than 60,000 Medicare Advantage members homes across five US states. The program expands point-of-care and in-home scanning volume, supporting demand for single-use gel packettes aligned with infection-control requirements during mobile workflows.

- January 2025: UPS completed its acquisition of Frigo-Trans and BPL, expanding temperature-controlled logistics capabilities across Europe. Broader cold-chain and controlled-warehouse coverage improves service levels for medical consumables distribution, supporting more consistent regional supply for gels and other procedure-adjacent items ordered through hospital procurement networks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues from ultrasound gel used as a coupling medium between an ultrasound transducer and patient skin, across healthcare and procedure settings where ultrasound imaging or therapy is performed.

Scope exclusions: It excludes ultrasound devices and probes, ultrasound contrast agents, disinfectants, and non-gel coupling substitutes such as dry pads or tapes.

Segmentation Overview

- By Product Type

- Non-Sterile

- Sterile

- By Application

- Diagnostic Imaging

- Therapeutic Ultrasound & Physiotherapy

- Aesthetic & Dermatology Procedures

- By End User

- Hospitals & Clinics

- Diagnostic Imaging Centers

- Physiotherapy/Sports Medicine Centers

- Home-Care & Retail Consumers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To ground the model, we map the demand pool that drives gel consumption, then check it against public, non-paywalled indicators. Sources such as the US FDA product databases and safety communications, the US CDC healthcare utilization statistics, OECD health statistics, and WHO health system indicators help validate procedure intensity and the care-setting mix by country.

We also review published clinical practice materials and peer-reviewed journals to understand typical gel use patterns by modality and setting, for example diagnostic imaging versus physiotherapy. On the supply side, we use company filings, investor presentations, product catalogs, tender notices, and reputable press coverage to interpret packaging formats and channel pricing. Where available, paid subscriptions are used for company financials and for import and export shipment-level checks to cross-verify the direction of volumes. These desk research sources are illustrative, and many additional public documents were reviewed to collect, validate, and clarify the inputs.

Primary Interviews and Surveys

Primary work is used to stress-test the desk view with practical inputs that are not captured in a single public dataset, especially around sterile versus non-sterile usage, purchasing cycles, and the role of distributors in smaller facilities. We speak with manufacturers, distributors, and large and mid-sized care providers across APAC, EMEA, and the Americas, and then adjust assumptions only when multiple respondents confirm the same direction.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 49% |

| Mid tier: 50% | Functional/Unit leaders: 31% | EMEA: 31% |

| Smaller Players: 14% | Managers: 56% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand build that reconstructs gel consumption from the procedure base, then converts values using typical pack sizes and average selling prices by channel. The model is corroborated with selective bottom-up approximations, including supplier revenue roll-ups for a tracked set of brands, distributor channel checks, and sampled ASP multiplied by estimated unit volumes. This helps correct for gaps where reporting is limited.

Key inputs used include ultrasound procedure volumes by care setting, the sterile versus non-sterile mix, including sterile single-use packets in infection-sensitive use cases, average gel usage per procedure, pack-size trends (bottles versus sachets), and price dispersion across hospitals, imaging centers, and retail. When local procedure statistics are thin, we bridge gaps using proxy indicators such as imaging equipment density and outpatient visit trends, and then recheck the implied per-procedure gel intensity with interview feedback.

For forecasting, we use scenario analysis supported by variable-level views from primary experts, so growth is linked to procedure growth, outpatient shift, and sterile adoption rather than a single straight-line CAGR. Pricing is handled with a simple inflation and mix approach, then reconciled to observed tender pricing and distributor quotes so the revenue curve remains realistic.

Data Validation & Update Cycle

Validation is done through several passes that compare the market output against independent signals, such as implied gel units per ultrasound procedure, trade flows where relevant, and consistency across adjacent care settings. If an anomaly is seen, such as an unusually high per-procedure value or a sudden regional jump, we reopen the assumptions behind volume, mix, or pricing and check again.

Before sign-off, the work is reviewed by another analyst, and any large variances versus prior editions trigger re-contact with selected respondents. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery scan is completed so clients receive the most current view.

Mordor Intelligence's Ultrasound Gel Market Estimate Compared With Other Published Estimates

Published market sizes for ultrasound gel can look far apart because the counted products and the assumed usage intensity are not always aligned across sources. The year and currency timing can also differ. We summarize two common estimate styles below so readers can see where the gaps tend to come from.

Ultrasound contrast agents are outside Mordor Intelligence's scope, which is one reason some wider imaging consumables totals come out higher even when the end users look similar. Differences also show up when one estimate uses a simple percentage of the broader ultrasound devices market, or when sterile single-use packs are priced as a premium across all settings without checking real purchasing behavior in imaging centers and outpatient clinics.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 111.91 M (2026) | |

| Regional Consultancy A | USD 115.54 M (2024) | Uses an earlier base year and appears to apply broad average pricing with limited visibility into pack-size mix, which can shift revenue even if volumes are similar. |

| Trade Journal B | USD 101.23 M (2023) | Anchors sizing on a narrower set of care settings and a lower implied gel use per procedure, and it may understate sterile packet penetration in higher compliance environments. |

Overall, the spread is mainly explained by what is counted with gel, which year is used, and how pricing and pack-size mix are treated across end users. By tying the total back to procedure-linked demand drivers and then checking volumes and ASP logic with interviews and public signals, the resulting number stays traceable and repeatable for planning.

Key Questions Answered in the Report

What is the current ultrasound gel market size?

The ultrasound gel market size is USD 111.91 million in 2026, with a forecast value of USD 136.55 million by 2031.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region, expected to post an 8.54% CAGR between 2026 and 2031.

Why are sterile gels gaining traction?

Heightened infection-control protocols in interventional and critical-care procedures are driving an 8.18% CAGR for sterile packettes through 2031.

How will gel-free technologies affect the market?

Dry transducer and membrane-coupling systems could trim long-term growth by an estimated 0.9 percentage points as they reach commercial maturity.

Which application is expanding the quickest?

Aesthetic and dermatology procedures are advancing at an 10.94% CAGR, the highest among all application segments.

What drives home-care demand?

The rise of handheld devices and tele-health services, exemplified by TridentCare’s 2025 initiative, is fueling a 12.11% CAGR in home-care gel consumption.

Page last updated on: