Cart-based Conventional Breast Ultrasound Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 337.30 Million |

| Market Size (2030) | USD 470.90 Million |

| Growth Rate (2025 - 2030) | 5.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

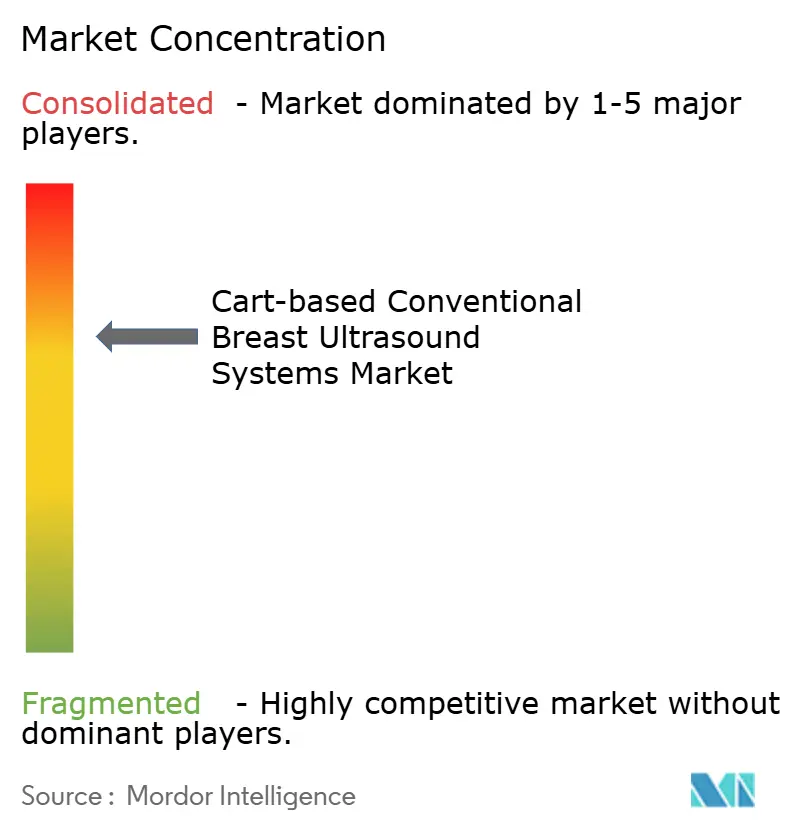

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cart-based Conventional Breast Ultrasound Systems Market Analysis by Mordor Intelligence

The cart-based conventional breast ultrasound systems market size stood at USD 337.3 million in 2024 and is forecast to reach USD 470.9 million by 2030, advancing at a 5.7% CAGR over the period. Regulatory catalysts, expanding reimbursement, and rapid AI integration are repositioning these platforms from point-solution scanners to connected diagnostic hubs. Hospitals continue to invest because cart platforms outperform handheld devices on image fidelity and elastography accuracy, while mobile screening units extend reach into rural areas. Vendors are accelerating acquisitions to embed workflow automation that offsets the sonographer shortage and enables higher daily scan volumes. Asia Pacific’s infrastructural upgrades, alongside dense-breast mandates in the United States, shape a two-speed adoption curve that balances mature-market replacement demand with developing-market first-time purchases.

Key Report Takeaways

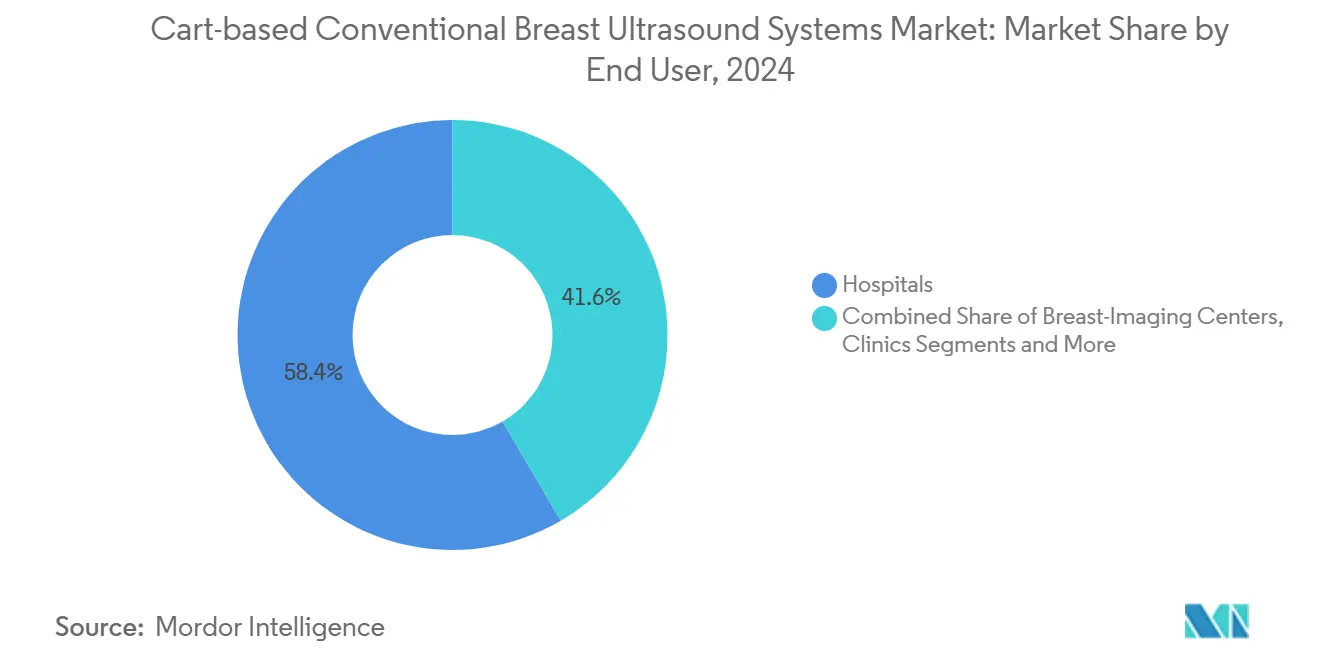

- By end user, hospitals held 58.4% of the cart-based conventional breast ultrasound systems market share in 2024. Mobile screening units are expanding at a 6.7% CAGR to 2030.

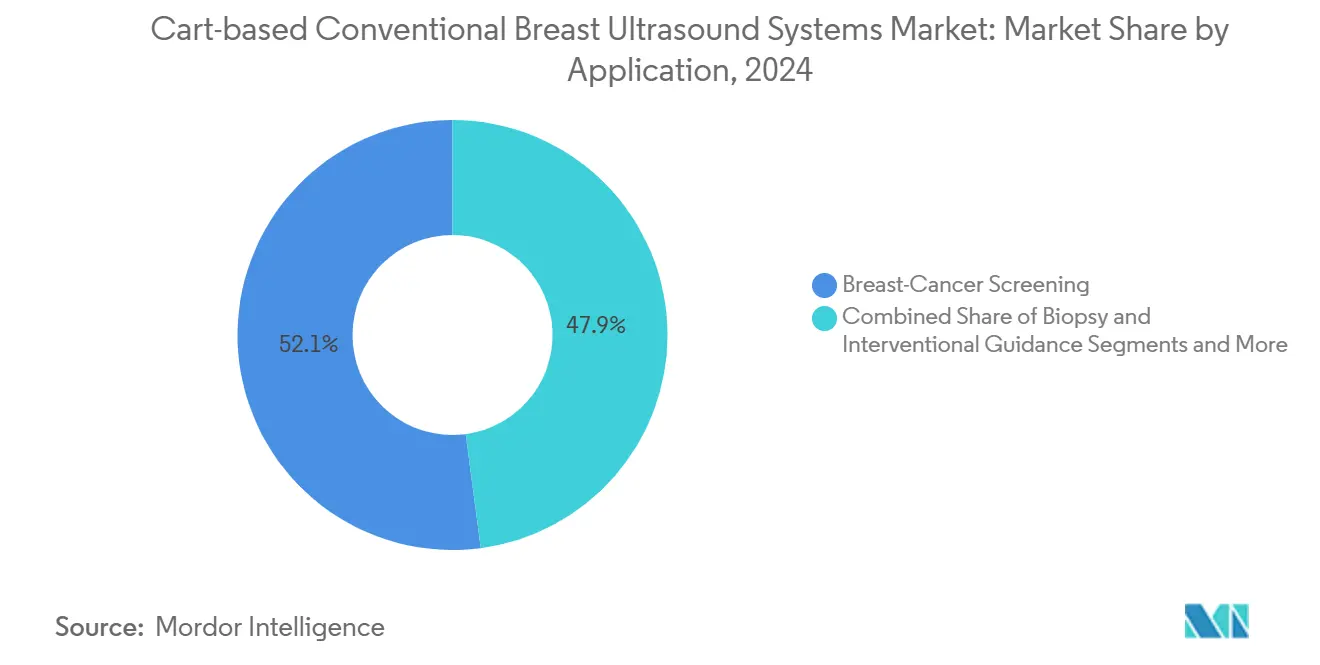

- By application, biopsy and interventional guidance contributed the fastest segment growth at 7.3% CAGR through 2030.

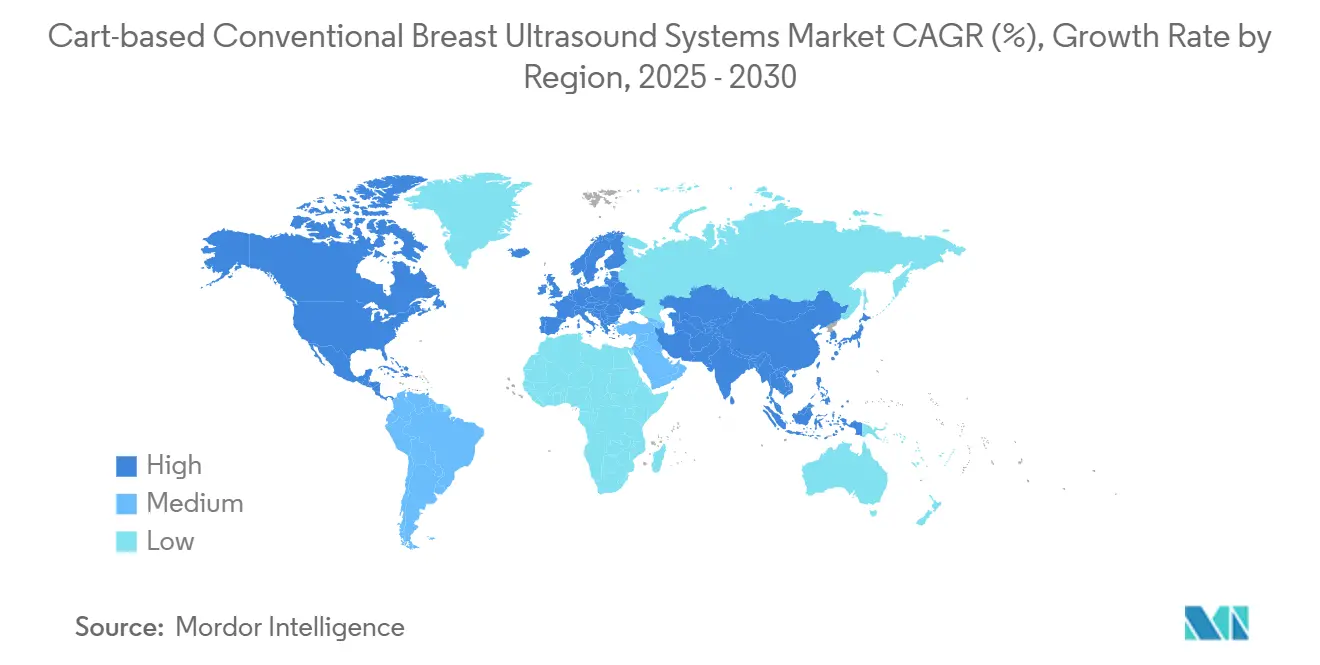

- By geography, North America captured 45.8% revenue in 2024; Asia Pacific is projected to lead regional growth at a 6.2% CAGR through 2030.

Global Cart-based Conventional Breast Ultrasound Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Breast Cancer | +1.20% | Global, with higher impact in North America & Europe | Long term (≥ 4 years) |

| Supplemental Screening Mandates For Dense Breasts | +1.80% | North America primary, EU secondary adoption | Medium term (2-4 years) |

| Technological Improvements In Image Quality & Elastography | +1.10% | Global, led by developed markets | Medium term (2-4 years) |

| Expansion Of Reimbursement Frameworks | +0.90% | North America & select EU markets | Medium term (2-4 years) |

| AI-Guided Workflow Optimisation Boosts Scan Throughput | +1.30% | Global, accelerated in high-volume centers | Short term (≤ 2 years) |

| Tele-Ultrasound Adoption In Rural Clinics | +0.60% | APAC core, spill-over to rural Americas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Breast Cancer

Cart platforms remain pivotal for early-stage detection because their elastography modules quantify tissue stiffness more reliably than portable heads. One in seven Australian women faced the disease in 2024, a prevalence echoed in Europe and the United States.[1]North Metropolitan Health Service, “New Mobile Van to Screen for Breast Cancer in WA Women,” NMHS, nmhs.health.wa.gov.au Facilities adopting shear-wave elastography report stronger lesion-to-fat contrast, shortening diagnostic pathways, and reinforcing the role of the cart-based conventional breast ultrasound systems market in precision oncology.

Supplemental Screening Mandates for Dense Breasts

The FDA’s September 2024 density-notification rule formalizes onward referral from mammography to ultrasound, anchoring a structural demand uplift for the cart-based conventional breast ultrasound systems market. Standardized language on four density categories removes variability and fuels protocol-driven ordering, making ultrasound a reimbursable next step despite Medicare copays now averaging USD 250 for density-only findings.

Technological Improvements in Image Quality & Elastography

Transparent relaxor-ferroelectric crystals have pushed transducer bandwidth to 78% at 28.5 MHz, lifting signal-to-noise ratios by 13 dB and supporting multi-angle shear-wave analysis.[2]Fei Li, “Transparent Ultrasonic Transducers Based on Relaxor Ferroelectric Crystals,” Nature Communications, nature.com When automated breast-volume scanning is layered onto elastography, malignancy sensitivity has reached 91%, reinforcing the cart-based conventional breast ultrasound systems market as the platform of choice for complex lesion assessment.[3]Lamei Zhang et al., “Innovative Integration of Automated Breast Volume Scan and Ultrasound Elastography for Enhanced Differentiation of Benign and Malignant Breast Lesions,” Scientific Reports, doi.org

AI-Guided Workflow Optimization Boosts Scan Throughput

GE HealthCare’s USD 51 million purchase of Intelligent Ultrasound brings ScanNav Assist AI into mainstream obstetric and breast workflows, cutting manual measurements and harmonizing operator performance. Similar tie-ups, such as Siemens Healthineers with DeepHealth, enable remote guidance and real-time image quality feedback, expanding exam capacity without proportional staffing increases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Costs Of Cart Systems | -1.40% | Global, more pronounced in price-sensitive markets | Medium term (2-4 years) |

| Shortage Of Skilled Breast-Sonography Professionals | -1.10% | Global, acute in rural and developing regions | Long term (≥ 4 years) |

| Supply-Chain Volatility For Piezoelectric Transducers | -0.80% | Global, with higher impact in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Price Pressure From Low-Cost Handheld Competitors | -1.00% | North America & Europe primary, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs of Cart Systems

Acquisition prices span USD 10,000–120,000, and service contracts often double ownership cost within five years. Meanwhile Butterfly Network’s USD 3,899 iQ3 reinforces a value narrative that pressurizes cart vendors to defend premium pricing through tangible diagnostic advantages. As cost-effectiveness reviews proliferate, proof of revenue uplift via additional billable procedures becomes the linchpin for procurement approvals.

Shortage of Skilled Breast-Sonography Professionals

Training pipelines lag demand, especially for niche breast-focused certifications. In Canada and rural U.S. counties, vacancy rates topped 12% in 2025, capping scan volumes regardless of equipment inventories. To sustain the cart-based conventional breast ultrasound systems market, manufacturers now bundle cloud-based simulation modules and modular certification curricula with new installs, aligning education with device features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Hospitals Drive Volume While Mobile Units Accelerate Growth

Hospitals accounted for 58.4% of the cart-based conventional breast ultrasound systems market size in 2024, supported by integrated PACS connectivity and comprehensive diagnostic protocols. These facilities depend on high-resolution elastography and AI-guided lesion scoring, reinforcing cart preference over handheld alternatives. Independent imaging centers and academic labs follow, bolstered by teaching imperatives and trial workloads.

Mobile screening units registered the fastest 6.7% CAGR, demonstrating how cart-based conventional breast ultrasound systems market adoption extends beyond fixed sites. Programs such as UC Davis MobileMammo+ plan to screen 5,000 women annually and rely on cart-mounted scanners co-located with mammography to provide same-visit supplemental imaging. By converting parking lots into temporary clinics, providers mitigate geographic inequities and build patient pipelines for centralized treatment centers.

By Application: Screening Dominance Shifts Toward Interventional Growth

Screening retained 52.1% of the cart-based conventional breast ultrasound systems market size in 2024, thanks to density-focused referrals. Diagnostic work-ups remained essential for lesion characterization, but biopsy and interventional guidance applications delivered 7.3% CAGR, the segment's high-water mark.

AI-assisted high-frequency probes now achieve AUC 0.94 when differentiating sclerosing adenosis from early malignancy, making precision-guided biopsies more efficient and reducing repeat procedures. As value-based payment models reward complication avoidance, interventional-grade elasticity mapping creates defensible demand for cart systems.

Geography Analysis

North America contributed 45.8% of 2024 revenues, reflecting mature reimbursement and the September 2024 density-notification rule that institutionalized ultrasound referrals. Copays averaging USD 250 triggered payer scrutiny yet also drove facilities to favor premium scanners that shorten diagnostic cycles. Mobile outreach, such as British Columbia’s three-unit fleet, adds incremental volumes by serving rural and Indigenous communities.

Asia Pacific is projected to post the quickest 6.2% CAGR as China scales national screening and Japan upgrades geriatric oncology capacity. Local production in South Korea compresses delivery lead times, while Australia’s statewide mobile fleets showcase hybrid deployment models that integrate cart ultrasounds for point-of-care triage.

Europe sees steady replacement demand, particularly for AI-ready devices that align with digital-health funding programs. Gulf states invest in Western-standard cancer centers, and Brazilian oncology networks procure multivendor fleets to cover rising breast-cancer incidence. Tailored financing packages and pay-per-scan contracts emerge across Latin America and Africa, where capital constraints would otherwise choke adoption.

Competitive Landscape

GE HealthCare led with roughly 30% of the cart-based conventional breast ultrasound systems market share in 2024, leveraging ScanNav Assist AI to offset labor bottlenecks and lock in service revenues. Siemens Healthineers, Philips, and Canon Medical contest the premium tier through continuous engine upgrades and localized R&D spending. Philips’ USD 150 million U.S. expansion underscores an arms-race for domestic manufacturing resiliency amid component shocks.

Butterfly Network intensifies price pressure with its sub-USD 4,000 iQ3, but durability, cooling tolerance, and advanced elastography still tilt complex cases toward carts. White-space opportunities cluster around tele-ultrasound: Siemens-DeepHealth SmartSonography allows off-site experts to steer scans, while Samsung Medison’s Z20 uses Live ViewAssist to pre-label planes for novice operators. Vendors that unify AI, ergonomics, and remote capability are best positioned to widen performance gaps over budget handhelds.

Cart-based Conventional Breast Ultrasound Systems Industry Leaders

GE HealthCare

Siemens Healthineers

Koninklijke Philips N.V.

Canon Medical Systems Corp.

Hologic Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Philips committed USD 150 million to expand Reedsville manufacturing and AI ultrasound R&D, adding 120 positions.

- November 2024: Mindray unveiled Resona A20 with Acoustic Intelligence Technology targeting breast workflows

- September 2024: Samsung Medison allied with Sonio after FDA clearance for OB/GYN ultrasound AI solutions.

Global Cart-based Conventional Breast Ultrasound Systems Market Report Scope

| Hospitals |

| Breast-Imaging Centers & Diagnostic Clinics |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| Mobile Screening Units |

| Breast-Cancer Screening |

| Diagnostic Work-up |

| Biopsy & Interventional Guidance |

| Treatment-Response Monitoring |

| Others (e.g., Intra-operative) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By End User | Hospitals | |

| Breast-Imaging Centers & Diagnostic Clinics | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| Mobile Screening Units | ||

| By Application | Breast-Cancer Screening | |

| Diagnostic Work-up | ||

| Biopsy & Interventional Guidance | ||

| Treatment-Response Monitoring | ||

| Others (e.g., Intra-operative) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2024 value of the cart-based conventional breast ultrasound systems market?

The cart-based conventional breast ultrasound systems market size reached USD 337.3 million in 2024.

How quickly is revenue expected to grow?

Revenue is projected to expand at a 5.7% CAGR, taking the total to USD 470.9 million by 2030.

Which region will add the most incremental demand by 2030?

Asia Pacific is forecast to record the fastest 6.2% CAGR as screening programs and infrastructure investments scale.

Why are mobile screening units important to vendors?

Mobile units show a 6.7% CAGR because they extend services into underserved areas, creating fresh equipment orders and recurring scan volumes.

How is AI changing purchasing criteria?

Hospitals now prioritize systems with embedded workflow automation that offset sonographer shortages and raise daily throughput, strengthening the case for cart platforms despite higher capital costs.

Which application segment is expanding fastest?

Biopsy and interventional guidance leads growth at 7.3% CAGR due to rising demand for real-time imaging during minimally invasive procedures.

Page last updated on: