Breast Cancer Core Needle Biopsy Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

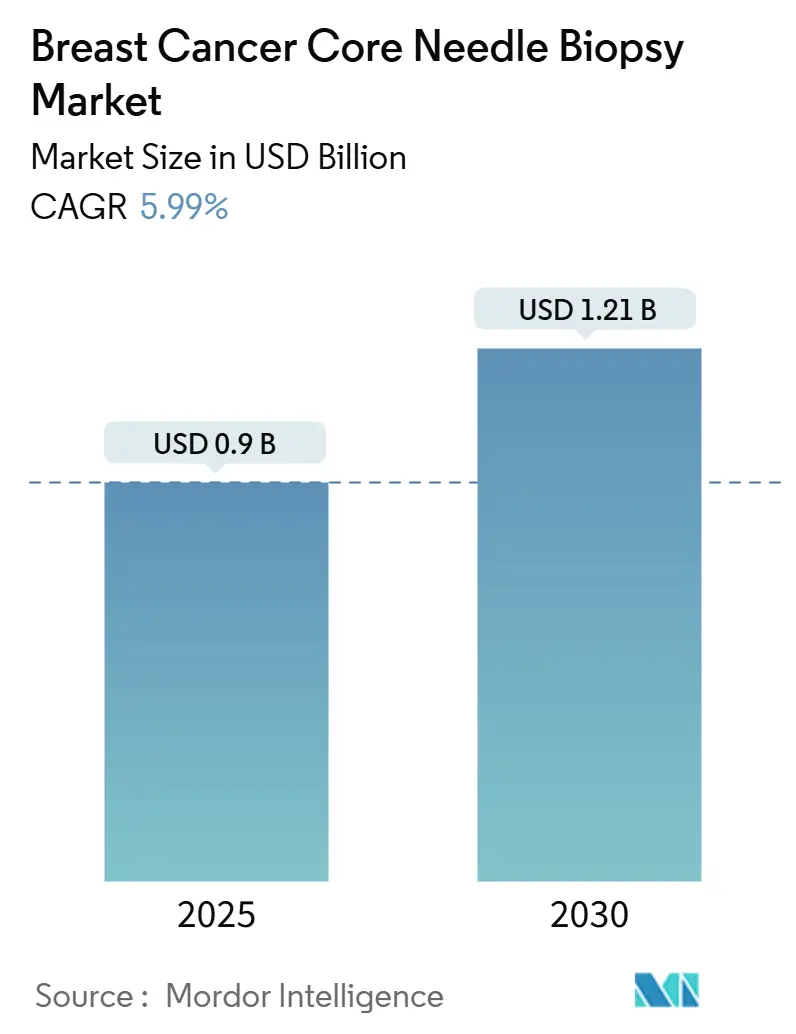

| Market Size (2025) | USD 0.9 Billion |

| Market Size (2030) | USD 1.21 Billion |

| Growth Rate (2025 - 2030) | 5.99% CAGR |

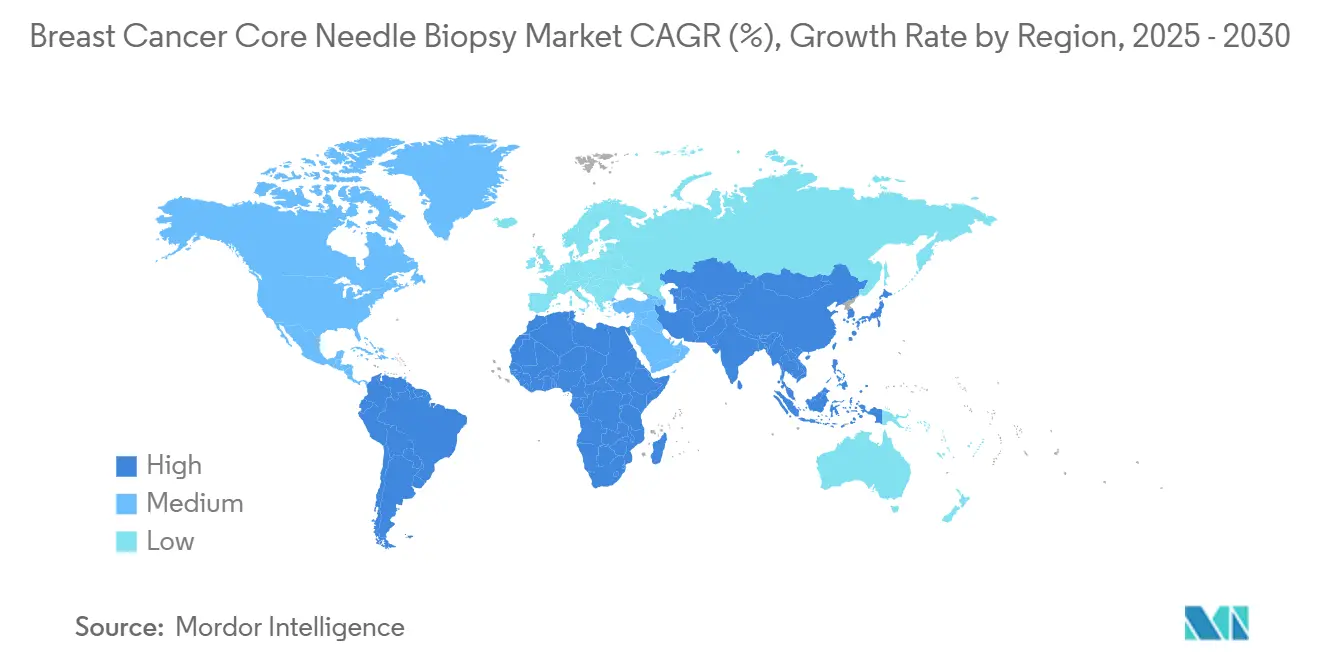

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Cancer Core Needle Biopsy Market Analysis by Mordor Intelligence

The breast cancer core needle biopsy market size is USD 0.903 billion in 2025 and is projected to reach USD 1.21 billion by 2030, advancing at a 5.99% CAGR over the period. Rising global breast-cancer incidence, earlier screening guidelines, and consistent payer support keep procedural volumes climbing. Providers favor vacuum-assisted systems that collect larger tissue cores through a single entry point, while AI-enabled imaging platforms cut procedure time and upgrade diagnostic confidence. Same-day ambulatory workflows lower readmissions and operating costs, further accelerating uptake in both mature and emerging health-care systems. Supply-chain exposure in specialty nickel alloys and ongoing concerns over false-negative results in resource-constrained settings temper the near-term growth outlook.

Key Report Takeaways

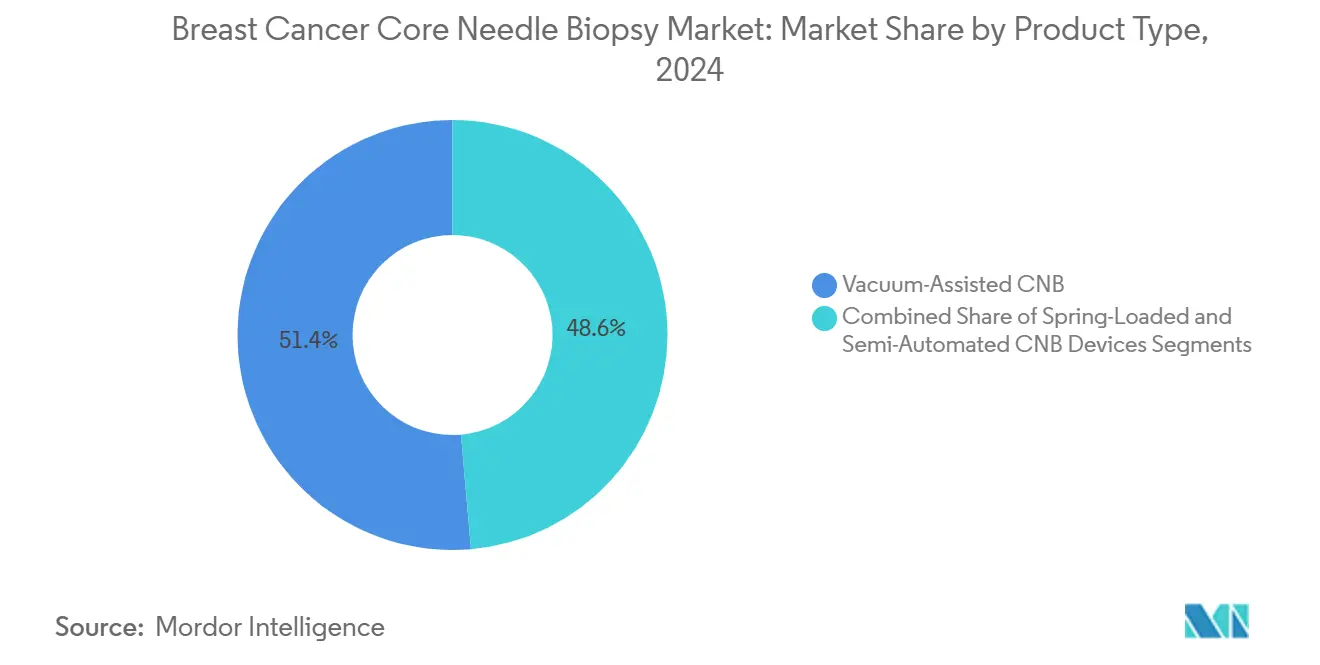

- By product type, vacuum-assisted devices accounted for 51.37% of the 2024 breast cancer core needle biopsy market share and are expanding at a 9.46% CAGR to 2030.

- By guidance technology, ultrasound led with 53.48% revenue share in 2024; MRI guidance is on track for a 10.23% CAGR through 2030.

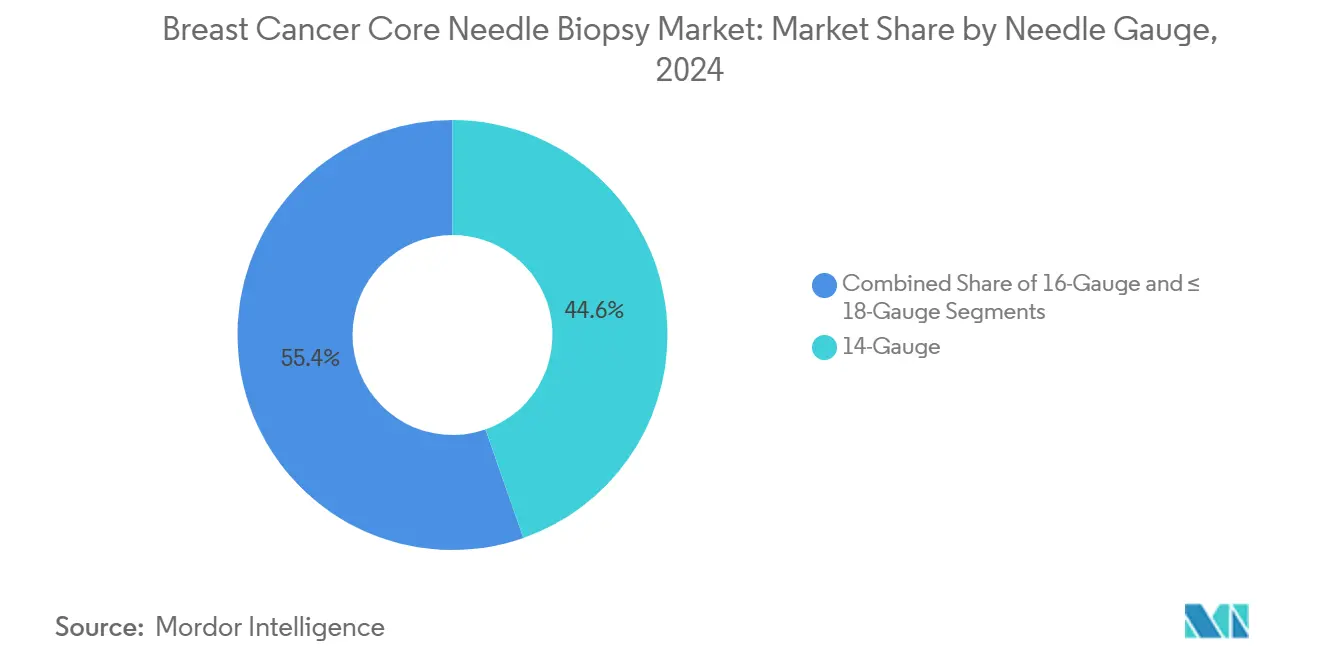

- By needle gauge, 14-gauge devices held 44.64% of the 2024 breast cancer core needle biopsy market size, while ≤18-gauge systems are the fastest-growing at 8.13% CAGR.

- By end user, hospitals performed 58.63% of total procedures in 2024, yet ambulatory surgical centers are growing the quickest at 8.94% CAGR.

- By geography, North America captured 37.44% of global revenue in 2024, whereas Asia-Pacific posts the highest regional growth at 8.21% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Breast Cancer Core Needle Biopsy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global breast-cancer incidence & screening uptake | +1.8% | Global; strongest in Asia-Pacific & North America | Long term (≥ 4 years) |

| Shift toward minimally invasive biopsies vs. open surgery | +1.2% | Global; pronounced in developed markets | Medium term (2-4 years) |

| Advances in image-guided core-needle accuracy | +0.9% | North America & Europe; spreading to Asia-Pacific | Medium term (2-4 years) |

| Favorable reimbursement in developed markets | +0.7% | North America & Europe | Short term (≤ 2 years) |

| AI-driven lesion targeting improves diagnostic yield | +0.6% | North America & Europe; early uptake in urban Asia-Pacific | Long term (≥ 4 years) |

| Same-day ambulatory diagnosis demand | +0.5% | Global; strongest in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Breast-Cancer Incidence & Screening Uptake

Rising incidence reshapes the breast cancer core needle biopsy market as screening programs widen. Asia reported 985,400 new cases in 2022 and is projected to reach 1.4 million by 2050, a pattern echoed across emerging economies.[1]Mengxia Fu, “Current and Future Burden of Breast Cancer in Asia: A GLOBOCAN Data Analysis for 2022 and 2050,” BMC Cancer, biomedcentral.comU.S. guidelines now advise biennial mammography from age 40, adding roughly 20 million screening-eligible women and lifting biopsy demand.[2]U.S. Preventive Services Task Force Panel, “Screening for Breast Cancer,” JAMA, jamanetwork.com China logged 385,837 new diagnoses in 2024, with peak rates a decade earlier than in Western cohorts, forcing rapid expansion of diagnostic capacity. Demographic aging, growing urban lifestyles, and better awareness make screening uptake outpace population growth. Disparities persist—Black women record 40% higher mortality in the United States—reinforcing the need for equitable, high-accuracy biopsy access.

Shift Toward Minimally Invasive Biopsies vs. Open Surgery

Health-care systems replace surgical excision with core needle approaches to cut costs and improve recovery. Outpatient modified radical mastectomy studies show readmission rates of 1.7% versus 2.5% for inpatient care, while costs fall from USD 113,878 to USD 94,463.[3]Ava Ferguson Bryan, “Value of Ambulatory Modified Radical Mastectomy,” Annals of Surgical Oncology, springer.com Vacuum-assisted devices generate tissue volumes adequate for receptor analysis and spare patients general anesthesia, shortening return-to-work times. Early-stage cryoablation using ProSense has delivered 96.3% local control at five years, hinting at therapeutic biopsy-plus-ablation workflows supported by regulators. Digital breast tomosynthesis guidance halves procedure time and lowers radiation dose, streamlining high-throughput ambulatory centers. Patient surveys consistently rank comfort and scar minimization over surgical completeness, steering physicians toward less invasive tools.

Advances in Image-Guided Core-Needle Accuracy

MRI/ultrasound fusion now detects 84% of lesions invisible on second-look ultrasound, permitting ultrasound-based sampling of MRI-found targets.[4]Kimberly Badal, “National Yearly Cost of Breast Cancer Screening in the USA and Projected Cost of Advocated Guidelines,” BMJ Open, bmj.comContrast-enhanced mammography guidance extends sampling to vascular patterns linked with invasive disease, while wide-angle tomosynthesis improves depth resolution. AI elevates needle tracking on ultrasound, boosting real-time placement accuracy and lowering repeat-biopsy risk. The FDA has cleared optical coherence tomography cores with AI morphology scoring, giving radiologists immediate adequacy feedback. As these tools migrate to mid-income markets, false negatives are expected to fall and procedure confidence to rise, fueling the breast cancer core needle biopsy market.

Favorable Reimbursement in Developed Markets

The 2025 Medicare Physician Fee Schedule keeps image-guided biopsy codes intact, sustaining provider margins. U.S. screening costs stand at USD 11 billion annually, yet biopsies remain among the least expensive pathways to definitive diagnosis. Inflation-adjusted payment erosion for breast surgery from 2003-2023 pushes hospitals toward outpatient core needle techniques. Europe’s DRG reforms reward procedures that combine accuracy with minimal repeats, advantaging vacuum-assisted systems. Proposed CY 2026 rule changes tie practice-expense values to device complexity, likely nudging centers toward integrated, AI-enabled platforms that justify higher reimbursement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| False-negative repeat-biopsy concerns | –0.8% | Global; highest in emerging markets | Medium term (2-4 years) |

| Procedure-related pain & anxiety | –0.6% | Asia-Pacific, Middle East & Africa, South America | Short term (≤ 2 years) |

| High device cost in low-income settings | –0.5% | Sub-Saharan Africa, rural Asia-Pacific, parts of South America | Long term (≥ 4 years) |

| Nickel-alloy needle supply disruptions | –0.3% | Global; acute in specialty manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

False-Negative Repeat-Biopsy Concerns

Up to 51% of atypical ductal hyperplasia biopsies upgrade to malignancy at excision, eroding clinician and patient trust. European studies cite interpretation errors and subtle lesion characteristics as leading causes of misses. Lesions under 1 cm and those without hypervascularity drive false-negatives on MRI, leading to delayed care. Deep-learning tools lift sensitivity but remain limited in specificity, keeping repeat interventions commonplace. Infrastructure gaps in emerging markets magnify sampling errors, stalling wider adoption of core needle techniques.

Procedure-Related Pain & Anxiety in Emerging Regions

Limited access to modern anesthesia and cultural apprehension restrict uptake where breast-cancer stigma persists. Studies confirm sufentanil pre-emptive analgesia combined with counseling significantly lowers postoperative pain, yet many facilities lack trained staff. Tumescent local anesthesia and serratus anterior plane blocks improve comfort but require consumables and skill sets absent in rural clinics. Patient anxiety prompts some clinicians to default to open biopsies perceived as definitive, dragging on procedure conversion rates and dampening the breast cancer core needle biopsy market in lower-resource geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vacuum-Assisted Systems Drive Diagnostic Evolution

Vacuum-assisted devices held the largest slice of the breast cancer core needle biopsy market share at 51.37% in 2024 and are scaling at 9.46% CAGR. The segment benefits from single-pass large-volume sampling that satisfies molecular-profile demands, lowering re-biopsy rates. Hospitals value integrated marker placement and automated tissue retrieval, which keep table time under 15 minutes. As reimbursement aligns with procedural complexity, investment shifts from spring-loaded guns to vacuum-assisted consoles. In price-sensitive regions spring-loaded devices remain a fallback, yet pilots show conversion once local payer policies recognize reduced false-negative costs. Semi-automated systems serve niche settings that need more control than spring mechanisms but cannot fund full vacuum platforms. The trajectory indicates gradual consolidation toward vacuum solutions, aided by marker innovations such as hydrogel tags that ease follow-up imaging.

Second-generation vacuum platforms now bundle AI-based depth control and ultrasound-visible tips, driving both efficiency and training ease. Studies report high patient satisfaction despite residual benign lesion tissue, hinting at therapeutic uses like vacuum-assisted excision. Manufacturers are marketing disposable hand-pieces to lower cross-contamination risk and align with infection-control mandates. As health-systems standardize device fleets, servicing contracts and software upgrades become differentiators, reinforcing scale advantages for incumbents and expanding the breast cancer core needle biopsy market size.

By Guidance Technology: MRI Integration Reshapes Precision Targeting

Ultrasound guidance retained 53.48% revenue share in 2024, yet MRI-guided procedures post the fastest 10.23% CAGR. MRI offers superior contrast for non-palpable lesions, but cost and access limit volumes primarily to tertiary centers. Fusion imaging that overlays MRI data onto live ultrasound screens bridges the gap, enabling community radiologists to sample occult lesions without full MRI suites, thereby widening addressable procedure counts. Stereotactic mammography remains the standard for calcifications, although upright tomosynthesis guidance improves ergonomics and trims radiation exposure. Tomosynthesis adoption is rising where 3D mammography has already displaced 2D screening, creating workflow continuity. AI-enhanced needle-tracking modules further increase hit rates, reducing the learning curve for newly credentialed operators.

In Japan, regulatory clearance for ultrasound-AI guidance systems accelerates hospital procurement, signaling forthcoming adoption in Korea, Singapore, and urban China. European value-based frameworks tie reimbursement to first-time diagnostic accuracy, favoring centers that bundle MRI simulation with ultrasound execution. Vendors offering multimodality workstations see higher attach rates for their biopsy probes, creating ecosystem lock-in and bolstering the breast cancer core needle biopsy market.

By Needle Gauge: Balancing Tissue Yield and Comfort

The 14-gauge category controlled 44.64% of global revenue in 2024 owing to its ability to procure robust cores for receptor assays. Larger gauges raise pain perception, yet modern anesthetic protocols offset discomfort, maintaining acceptance. 16-gauge systems serve patients with dense or fibrotic breast tissue where maneuverability is crucial. Interest in ≤18-gauge needles grows at 8.13% CAGR as ambulatory centers emphasize quick turnaround and minimal soreness. Lateral arm approaches allow stereotactic samples in small breasts, avoiding skin folds and lowering repeat imaging.

Personalized oncology increases pressure to secure enough tissue for multigene panels, nudging practitioners toward larger gauges. Concurrently, ultrasound-guided nerve blocks enable nearly pain-free sampling, reducing historical trade-offs between yield and comfort. Manufacturers innovate with echogenic coatings that boost visibility across all gauges, driving procedural confidence and sustaining expansion of the breast cancer core needle biopsy market size at segment level.

By End User: Ambulatory Hubs Capture Share

Hospitals still perform 58.63% of procedures, leveraging full pathology labs and surgical back-up. Yet ambulatory surgical centers post the strongest growth at 8.94% CAGR as payers favor lower facility fees. Dedicated breast clinics combine imaging, biopsy, and counseling under one roof, delivering same-day diagnosis that cuts patient anxiety. Diagnostic imaging centers offer cost-effective access for routine sampling where radiologist capacity exists.

Integrated health systems pilot hub-and-spoke models where downtown hospitals tackle complex MRI-guided cases, while suburban ambulatory nodes handle ultrasound and tomosynthesis biopsies. Capital-light mobile units equipped with vacuum-assisted consoles extend reach into rural pockets, particularly in India and China, enlarging the overall breast cancer core needle biopsy market.

Geography Analysis

North America leads the breast cancer core needle biopsy market with 37.44% revenue in 2024 thanks to entrenched screening programs, favorable reimbursement, and widespread AI pilot studies. Market maturity tempers growth to mid-single digits, yet replacement cycles and cryoablation adjuncts sustain vendor pipelines. Europe follows with steady demand shaped by country-specific DRG structures rewarding high diagnostic accuracy. Western European centers adopt fusion imaging fastest, while Eastern nations catch up via EU funding initiatives.

Asia-Pacific drives volume growth at an 8.21% CAGR as urban populations swell and governments underwrite national screening. China’s prevalence surge and earlier disease onset create urgency for scalable biopsy infrastructure. India’s mix of public-private partnerships funds regional breast centers, though rural access gaps persist. Japan pioneers AI ultrasound guidance, influencing neighboring health authorities.

The Middle East and Africa remain nascent yet promising; oil-rich Gulf states import cutting-edge suites, whereas Sub-Saharan clinics seek cost-contained spring-loaded options. South America grows gradually; Brazil and Argentina spearhead vacuum-assisted adoption amid economic swings. Overall, geographic diversification cushions suppliers against policy shocks, broadening the breast cancer core needle biopsy market footprint.

Competitive Landscape

The market is moderately fragmented. Hologic, BD, Danaher’s Leica, and B. Braun anchor the top tier, leveraging broad portfolios and service networks. Hologic’s USD 350 million purchase of Gynesonics extends ultrasound-based intervention capability, signifying convergence between diagnostic and therapeutic assets. BD’s planned separation of Biosciences and Diagnostic Solutions concentrates focus on core tools while freeing capital for AI collaborations.

Mid-size innovators push niche advantages: IceCure positions cryoablation as a lumpectomy alternative approved in Europe, with U.S. clearance anticipated in 2025. Clairity’s AI risk model received De Novo authorization, opening a software front that device vendors may license. Contract manufacturers race to secure nickel-alloy feedstock amid geopolitical pressures, spurring joint ventures in Southeast Asia.

Strategic focus has shifted from hardware specs to workflow performance. Vendors bundle imaging consoles, vacuum hand-pieces, and tracking software into subscription models that mirror radiology PACS arrangements. This bundling boosts switching costs and locks in consumable revenue streams, raising entry barriers for start-ups and providing a stabilizing influence on the breast cancer core needle biopsy industry.

Breast Cancer Core Needle Biopsy Industry Leaders

Becton, Dickinson & Co.

Hologic Inc.

Argon Medical Devices

Cook Medical LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The FDA issued De Novo authorization for CLAIRITY BREAST, an AI platform that predicts five-year breast-cancer risk from routine mammograms.

- January 2025: Hologic finalized the USD 350 million acquisition of Gynesonics, maker of the Sonata System, to broaden its women’s-health ultrasound portfolio.

Global Breast Cancer Core Needle Biopsy Market Report Scope

| Spring-Loaded CNB Devices |

| Vacuum-Assisted CNB Devices |

| Semi-Automated CNB Devices |

| Ultrasound-Guided |

| Stereotactic (Mammography)-Guided |

| MRI-Guided |

| Tomosynthesis-Guided |

| 14-Gauge |

| 16-Gauge |

| ≤18-Gauge |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Breast Clinics |

| Diagnostic Imaging Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Spring-Loaded CNB Devices | |

| Vacuum-Assisted CNB Devices | ||

| Semi-Automated CNB Devices | ||

| By Guidance Technology | Ultrasound-Guided | |

| Stereotactic (Mammography)-Guided | ||

| MRI-Guided | ||

| Tomosynthesis-Guided | ||

| By Needle Gauge | 14-Gauge | |

| 16-Gauge | ||

| ≤18-Gauge | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Breast Clinics | ||

| Diagnostic Imaging Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the breast cancer core needle biopsy market in 2025?

The breast cancer core needle biopsy market size stands at USD 0.903 billion in 2025, advancing toward USD 1.21 billion by 2030.

What is the projected growth rate through 2030?

The market is forecast to expand at a steady 5.99% CAGR over the 2025-2030 period.

Which product segment grows the fastest?

Vacuum-assisted devices post the strongest momentum, recording a 9.46% CAGR through 2030.

Why is MRI guidance gaining traction?

MRI’s superior soft-tissue contrast helps locate lesions that conventional imaging misses, driving a 10.23% CAGR in MRI-guided procedures.

Where will future demand rise most rapidly?

Asia-Pacific leads regional growth at an 8.21% CAGR as screening programs expand across China and India.

Are ambulatory centers overtaking hospitals?

Ambulatory surgical centers remain the fastest-growing end-user class, adding procedures at an 8.94% CAGR thanks to same-day diagnostic workflows.

Page last updated on: