Cardiovascular Ultrasound System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 3.29% CAGR |

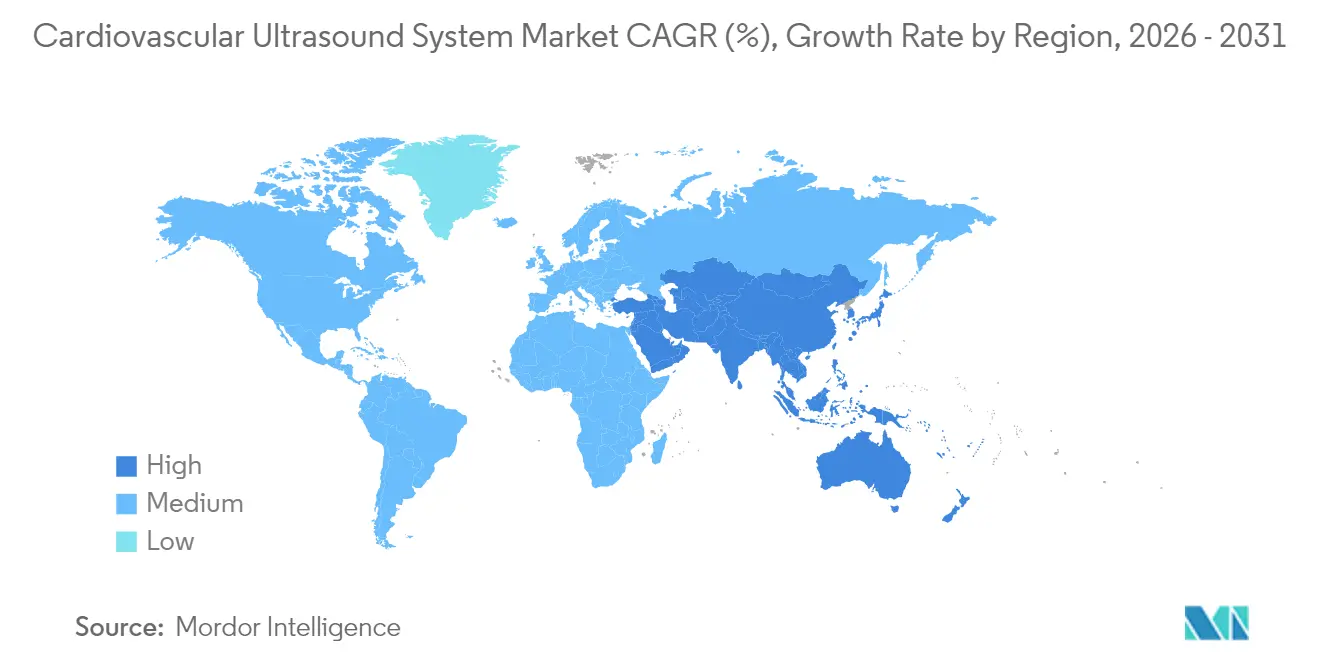

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

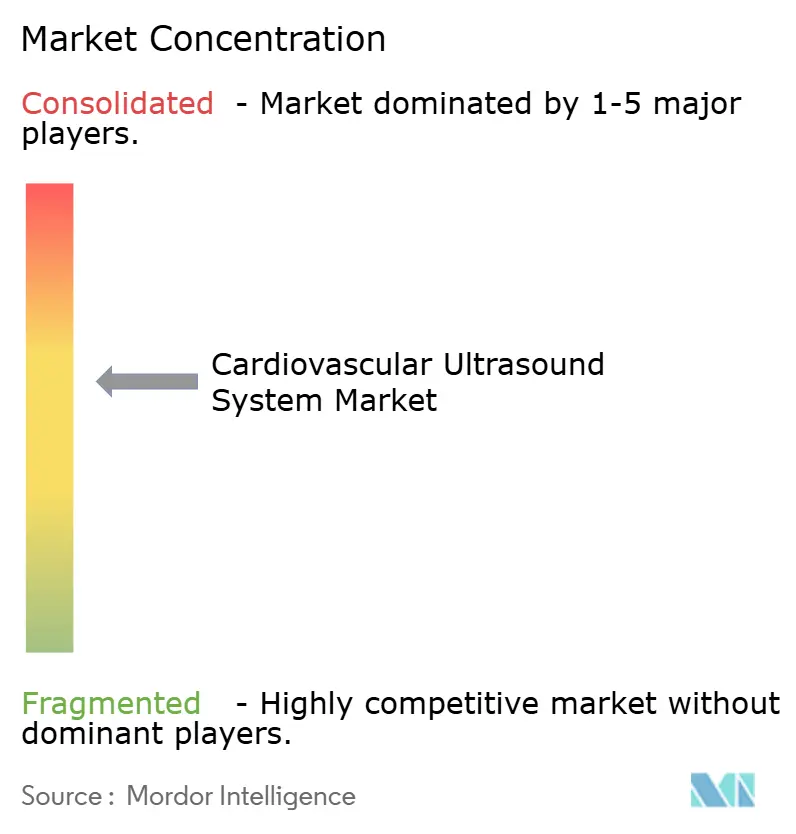

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiovascular Ultrasound System Market Analysis by Mordor Intelligence

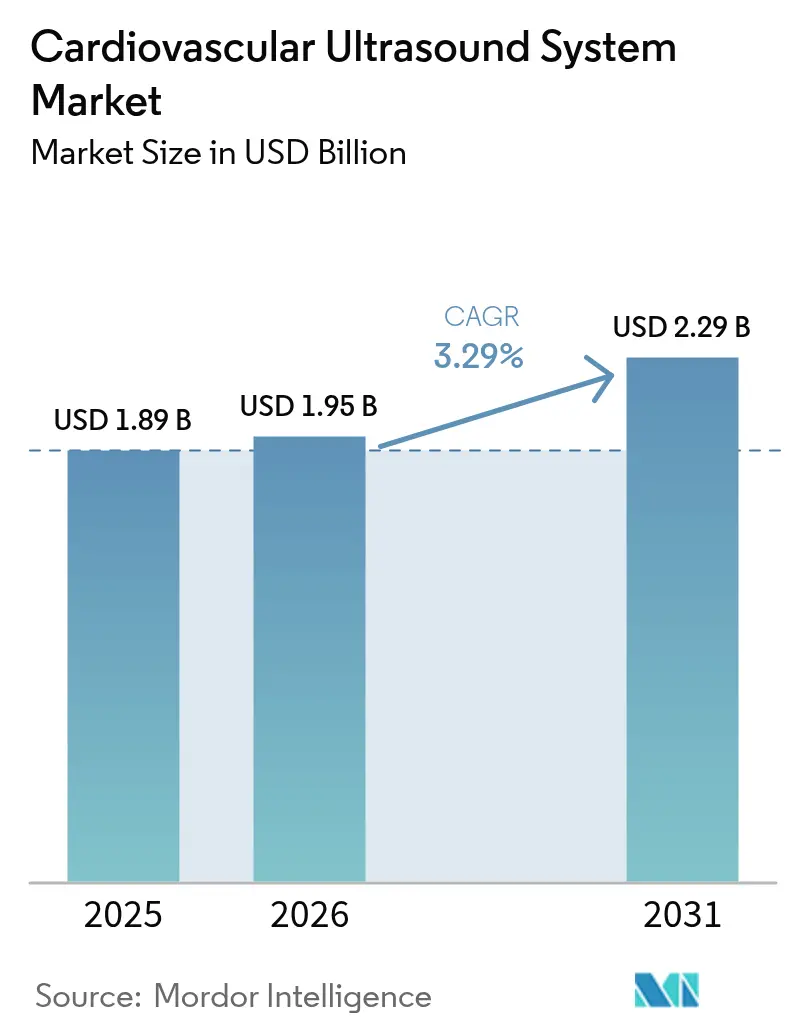

The Cardiovascular Ultrasound System Market size was valued at USD 1.89 billion in 2025 and estimated to grow from USD 1.95 billion in 2026 to reach USD 2.29 billion by 2031, at a CAGR of 3.29% during the forecast period (2026-2031).

Advances in artificial intelligence, broader adoption of handheld scanners and increasing use in emergency care are reshaping clinical workflows within the cardiovascular ultrasound system market. Regulatory support is solidifying, as shown by the FDA clearance given to UltraSight’s AI-guided cardiac ultrasound software in 2023, signaling a permissive stance toward innovation. Growing cardiovascular disease prevalence, the need for cost-effective non-invasive diagnostics and expanding point-of-care deployment are enabling mid-single-digit growth despite ongoing reimbursement pressure. Competitive activity is intense; large vendors are adding AI assets through acquisitions while start-ups pursue disruptive, cloud-centric models to serve the cardiovascular ultrasound system market.

Key Report Takeaways

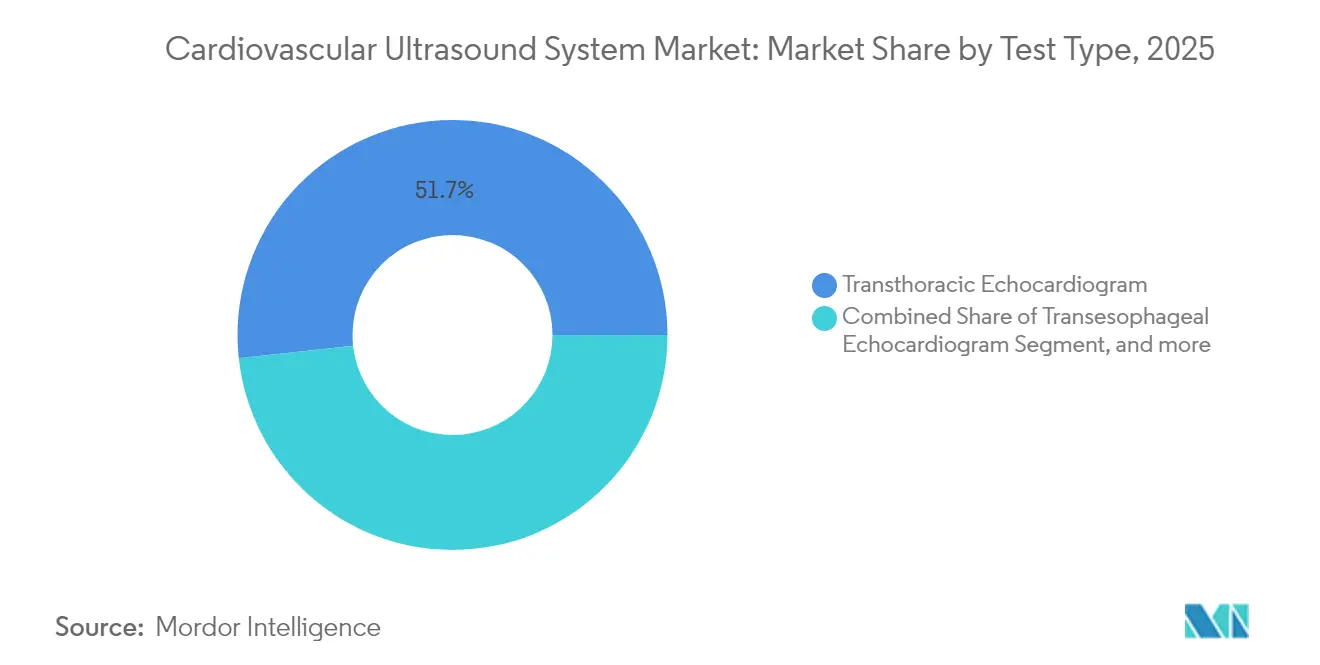

- By test type, transthoracic echocardiography commanded 51.73% of cardiovascular ultrasound system market share in 2025, while stress echocardiography is projected to expand at an 8.31% CAGR to 2031.

- By technology, 2-D platforms led with 42.74% of the cardiovascular ultrasound system market size in 2025, whereas 3-D & 4-D imaging is forecast to grow at a 9.02% CAGR through 2031.

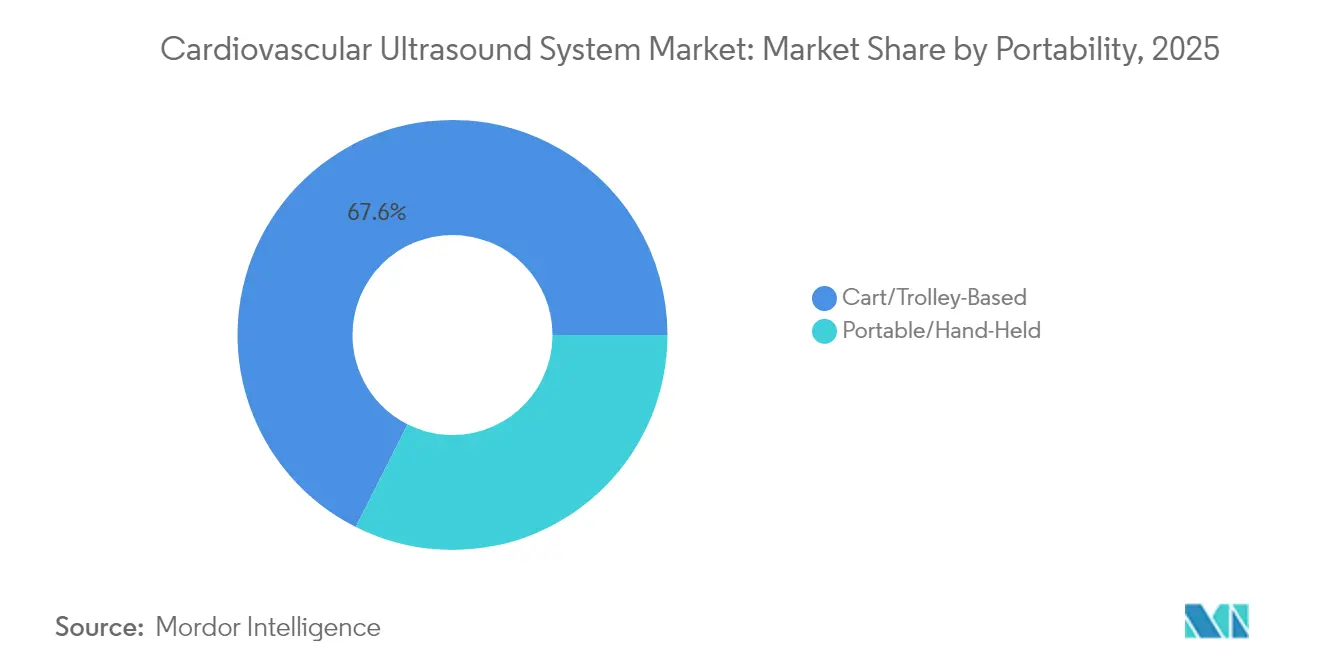

- By portability, cart-based systems held 67.58% of the cardiovascular ultrasound system market size in 2025 and handheld devices are advancing at a 12.47% CAGR over 2026-2031.

- By display type, color systems captured 83.68% share in 2025 as premium color units are set to rise at a 7.03% CAGR to 2031.

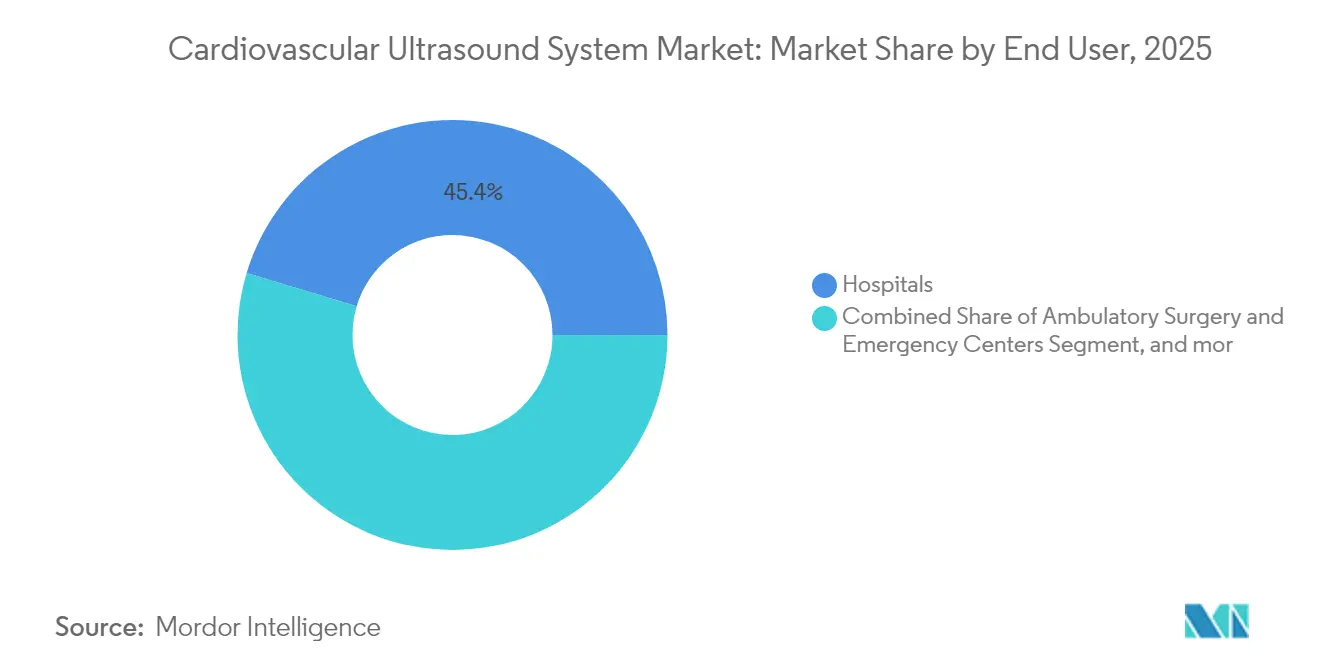

- By end user, hospitals accounted for 45.35% of cardiovascular ultrasound system market share in 2025, while ambulatory surgery and emergency centers are on track for a 10.05% CAGR in the same period.

- By geography, North America dominated with 32.12% share in 2025 and Asia-Pacific is poised to expand at an 8.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiovascular Ultrasound System Market Trends and Insights

Drivers Impact Analysis*

| Market Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cardiovascular disease burden and aging demographics | +1.2% | Global, stronger in North America and Europe | Long term (≥ 4 years) |

| AI-driven quantification, 3-D/4-D imaging and miniaturisation | +1.5% | Global, earliest uptake in North America and Europe | Medium term (2–4 years) |

| Expansion of point-of-care and emergency-department ultrasound | +0.8% | Global, pronounced in emerging markets | Medium term (2–4 years) |

| Shift from invasive diagnostics toward non-invasive ultrasound | +0.7% | Global, higher in developed markets | Medium term (2–4 years) |

| Growing emphasis on early diagnosis and preventive cardiology | +0.5% | Global | Long term (≥ 4 years) |

| Integration of AI and cloud-based imaging platforms | +0.4% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Prevalence of Cardiovascular Diseases and Aging Demographics

Cardiovascular diseases remained the leading cause of hospital admissions in England, recording 1.5 million inpatient episodes in 2022-23.[1]British Heart Foundation, “Heart and Circulatory Disease Statistics 2024,” bhf.org.ukSimilar upward trends are evident across Asia and North America, propelled by sedentary lifestyles, dietary changes and population aging. Point-of-care echocardiography has become integral to early detection strategies, supporting routine screening in ambulatory settings. Research published in 2025 demonstrated that trained clinicians can use cardiac POCUS to identify hypertrophic cardiomyopathy, diastolic dysfunction and tamponade with high accuracy.[2]Mathew D. Zimmerman, “Advanced Cardiac POCUS,” Medical Clinics of North America, sciencedirect.com As older adults require more frequent cardiac monitoring, demand for repeatable radiation-free imaging rises, anchoring long-run growth in the cardiovascular ultrasound system market.

Technological Advancements: AI-Driven Quantification, 3-D/4-D Imaging and Miniaturisation

Deep-learning algorithms now automate chamber delineation, wall-motion scoring and valvular quantification, bringing interpretation times down by up to 40% compared with manual review. FDA-cleared 3-D quantification of mitral regurgitation allows volumetric assessment that was unattainable with 2-D imaging. Miniaturised probes fit in a pocket yet deliver diagnostic image quality, permitting exams at the bedside, in ambulances and even at home. These capabilities democratise access, widen the referral base and reinforce technology refresh cycles throughout the cardiovascular ultrasound system market.

Expansion of Point-of-Care & Emergency-Department Ultrasound Applications

Bedside echocardiography accelerates triage for tamponade, shock and heart failure, reducing time-to-treatment in emergency departments. AI guidance tools embedded in handheld devices now coach novice users on probe positioning, image capture and common measurements. This lowers operator dependency and enables broader practitioner adoption, opening new revenue streams in primary care and remote clinics. The flexibility of point-of-care exams aligns with value-based reimbursement models that reward care delivered in low-cost settings.

Shift from Invasive Cardiac Diagnostics toward Non-Invasive Ultrasound Modalities

Stress echo and contrast-enhanced studies supply functional insight without catheterisation risks or radiation exposure. A comparative review showed non-invasive ultrasound achieves diagnostic yields comparable to invasive angiography for selected coronary assessments. Hospitals therefore redirect budgets to non-invasive suites, fostering steady replacement demand for premium cardiovascular ultrasound systems.

Restraints Impact Analysis*

| Market Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of premium cardiovascular ultrasound platforms | −0.9% | Emerging markets, notably Asia-Pacific and Africa | Short term (≤ 2 years) |

| Reimbursement pressure and budget constraints in developed markets | −0.8% | North America and Europe | Medium term (2–4 years) |

| Shortage of skilled sonographers and advanced echo interpreters | −0.6% | Global, acute in rural zones | Long term (≥ 4 years) |

| Limited access in low-income and rural settings | −0.5% | Sub-Saharan Africa and parts of South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Premium Cardiovascular Ultrasound Platforms

Top-tier scanners with 3-D capabilities can exceed USD 250,000, pricing out smaller providers and prolonging replacement cycles. Total cost of ownership further rises with service contracts and software upgrades. Tiered product lines and refurbished systems offer partial relief, but the cost gap between entry and premium remains large, restraining penetration in budget-constrained markets.

Reimbursement Pressure and Budget Constraints in Developed Markets

Medicare pays USD 198.58 for a complete transthoracic study with Doppler in 2025, a 12% real decline from 2021 levels. Hospitals must justify capital outlay with demonstrable outcome improvements rather than procedure volume. This financial squeeze moderates unit demand, especially for high-specification devices, within the cardiovascular ultrasound system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: TTE Holds Leadership while Stress Echo Gains Speed

Transthoracic echocardiography delivered 51.73% of 2025 revenues, underpinning its role as a routine, non-invasive cornerstone across all care settings. Its broad clinical utility secures replacement demand and ensures the cardiovascular ultrasound system market size tied to TTE remains substantial. Stress echocardiography is expanding fastest at an 8.31% CAGR to 2031 because it reveals inducible ischemia without radiation and fits preventive cardiology protocols. Rapid case throughput and reimbursements aligned with functional assessments further spur adoption.

TEE retains importance for valve evaluation and structural heart interventions. With 4-D probes now offering real-time volumetric guidance during transcatheter procedures, the segment sustains steady growth. Niche applications such as fetal and pediatric echocardiography drive technology tailoring, creating opportunities for compact, high-frequency transducers.

By Technology: 2-D Dominates yet 3-D & 4-D Accelerate

Two-dimensional imaging continues to generate 42.74% of cardiovascular ultrasound system market size due to mature workflows, familiarity and cost advantages. Diagnostic confidence from 2-D plus color Doppler remains sufficient for most routine exams. However, 3-D & 4-D imaging is on a 9.02% CAGR trajectory as interventional cardiologists demand volumetric guidance for valve repair and congenital corrections. Automated 3-D quantification of regurgitation severity adds reproducibility and shortens reporting time.

Enhanced Doppler modes such as vector flow mapping and micro-vascular imaging extend functional insights, anchoring 2-D-centric systems in everyday practice. Vendors leverage shared hardware to offer modular upgrades, smoothing the transition toward advanced modalities without full platform replacement, sustaining the cardiovascular ultrasound system market.

By Portability: Handheld Devices Redefine Access

Cart platforms still account for 67.58% of revenue thanks to premium performance, transducer versatility and integrated measurement suites. They remain indispensable in echo labs and tertiary care centers for comprehensive studies. Yet handheld units clock a 12.47% CAGR, proving that portability coupled with AI assistance can satisfy many frontline needs. The ability to disinfect, transport and deploy in seconds gained prominence during the COVID-19 surge and continues to influence procurement criteria.

Vendor strategies now blend handheld probes with cloud dashboards, enabling enterprise-wide fleet management and remote over-read. Hospitals pairing carts with handhelds achieve workflow flexibility, highlighting complementary rather than cannibalistic dynamics inside the cardiovascular ultrasound system market.

By Display Type: Color Imaging Prevails

Color systems captured 83.68% share in 2025 because flow visualisation is indispensable for valvular pathology, shunts and hemodynamic assessment. Premium color units are rising at 7.03% CAGR as OLED and high-dynamic-range panels deliver finer detail and reduced eye fatigue. Innovation in pseudo-color overlay on B-mode images helps identify subtle tissue changes and supports AI-driven tissue classification.

Black-and-white displays survive in ultra-portable probes aimed at rapid structural checks where flow data is secondary. Battery savings and lower price points keep these devices attractive in austere settings yet color-capable options are rapidly narrowing the cost gap, reinforcing the color-dominant future of the cardiovascular ultrasound system market.

By End User: Hospitals Anchor Demand while Ambulatory Centers Surge

Hospitals generated 45.35% of 2025 revenue because complex cases, interventional support and critical care continue to cluster in institutional environments. Integrated cardiology departments leverage full-feature carts and dedicated sonography teams, ensuring high study volumes. Ambulatory surgery and emergency centers will grow at 10.05% CAGR as outpatient pathways shift diagnostics closer to the patient.

Reimbursement adjustments that favor same-day discharge and the embrace of AI-guided handheld probes broaden use among non-cardiology clinicians. Diagnostic imaging centers complement hospital networks by handling follow-up exams and overflow, sustaining balanced demand across sites in the cardiovascular ultrasound system market.

Geography Analysis

North America contributed 32.12% of global revenue in 2025, backed by advanced infrastructure and quick uptake of AI-enabled upgrades. Workforce shortages persist; 46.3% of U.S. counties have no resident cardiologist, affecting 22 million people. Vendors market workflow automation and remote reading to mitigate staffing gaps.

Asia-Pacific is the fastest-growing territory at an 8.62% CAGR through 2031. China’s volume-based procurement and local manufacturing incentives foster competitive domestic suppliers, while India’s tier-2 cities add echo capacity through private hospital chains. Portable, battery-powered systems resonate in rural clinics, driving breadth of adoption across socioeconomic tiers.

Europe maintains a balanced profile with strong reimbursement for non-invasive imaging and a large aging population. Middle East & Africa and South America are smaller yet expanding as governments prioritise cardiovascular disease management. Brazil leads regional uptake through private insurance penetration and growing elective procedure volumes. Collectively, geographic trends underscore the need for scalable solutions that range from premium carts to ultra-portable probes within the cardiovascular ultrasound system market.

Competitive Landscape

Market concentration is moderate; GE HealthCare, Philips and Siemens Healthineers continue to dominate premium tiers through broad portfolios and service ecosystems. GE HealthCare’s USD 51 million purchase of Intelligent Ultrasound in 2024 bolstered real-time AI analytics capabilities. Philips focuses on integrated workflow suites that combine echo, CT and MR data in structural heart programs, while Siemens Healthineers leverages AcuNav 4-D ICE to strengthen its interventional presence.

Disruptors such as Butterfly Network and Clarius Mobile Health accelerate portability at sub-USD 3,000 price points, targeting primary care and low-resource environments. Cloud-first newcomers offer software-as-a-service packages with algorithm updates, challenging traditional capital-equipment economics. Chinese vendors advance in price-sensitive regions, expanding global footprints as domestic policies encourage export.

Strategic partnerships with pharma companies emerge to support disease-specific AI tools, as seen in Ultromics and Pfizer’s collaboration on EchoGo for amyloidosis detection. Vendors that align AI, workflow efficiency and outcome-focused metrics are positioned to gain advantage as health systems migrate toward value-based purchasing, shaping future competition within the cardiovascular ultrasound system market.

Cardiovascular Ultrasound System Industry Leaders

Canon Medical Systems Corporation

Esaote SpA

GE Healthcare

Siemens Healthcare GmbH

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: GE HealthCare partnered with Medis Medical Imaging to enhance non-invasive coronary assessments through the integration of Medis Quantitative Flow Ratio into GE's Allia Platform, aiming to improve the assessment of coronary physiology without invasive procedures.

- May 2024: Samsung Medison announced the acquisition of Sonio, a French startup specializing in AI for ultrasound, for USD 92 million, signaling Samsung's strategic investment in enhancing its ultrasound capabilities through artificial intelligence integration.

- April 2024: Us2.ai received FDA clearance for its Us2.v2 software, which automates the analysis of echocardiographic DICOM images with 45 automated echo parameters including strain analysis, significantly enhancing diagnostic review and reporting efficiency.

- April 2024: GE HealthCare secured CE marks for its Vscan Air SL wireless handheld ultrasound system, now enhanced with Caption AI.

Global Cardiovascular Ultrasound System Market Report Scope

As per the scope of this report, cardiovascular ultrasound systems use the ultrasound imaging technique to provide images of the heart. The cardiovascular ultrasound system market is segmented by test type (transthoracic echocardiogram, transesophageal echocardiogram, stress echocardiogram, and other test types), technology (2D, 3D, and 4D, and Doppler imaging), device display (color display and black and white (b/w) display), end user (hospitals, ambulatory centers, and other end users), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above-mentioned segments.

| Transthoracic Echocardiogram (TTE) |

| Transesophageal Echocardiogram (TEE) |

| Stress Echocardiogram |

| Other Test Types |

| 2-D |

| 3-D & 4-D |

| Doppler Imaging |

| Cart/Trolley-Based |

| Portable/Hand-Held |

| Color Display |

| Black & White (B/W) Display |

| Hospitals |

| Ambulatory Surgery & Emergency Centers |

| Diagnostic Imaging Centers & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Transthoracic Echocardiogram (TTE) | |

| Transesophageal Echocardiogram (TEE) | ||

| Stress Echocardiogram | ||

| Other Test Types | ||

| By Technology | 2-D | |

| 3-D & 4-D | ||

| Doppler Imaging | ||

| By Portability | Cart/Trolley-Based | |

| Portable/Hand-Held | ||

| By Device Display | Color Display | |

| Black & White (B/W) Display | ||

| By End User | Hospitals | |

| Ambulatory Surgery & Emergency Centers | ||

| Diagnostic Imaging Centers & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the cardiovascular ultrasound system market?

The cardiovascular ultrasound system market size stands at USD 1.95 billion in 2026.

How fast is the market expected to grow?

The market is forecast to post a 3.29% CAGR, reaching USD 2.29 billion by 2031.

Which technology segment is expanding most rapidly?

3-D & 4-D imaging is the fastest-growing technology, projected at a 9.02% CAGR over 2026-2031.

Why are handheld ultrasound devices gaining traction?

Handheld units support point-of-care exams, reduce infection risk and integrate AI guidance, leading to a 12.47% CAGR.

What is the biggest restraint on market growth?

High capital cost of premium platforms remains the strongest brake, subtracting an estimated 0.9 percentage points from the forecast CAGR.

Which region will record the fastest growth?

Asia-Pacific is expected to grow at an 8.62% CAGR owing to rising healthcare investment and cardiovascular disease prevalence.

Page last updated on: