3D Ultrasound Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

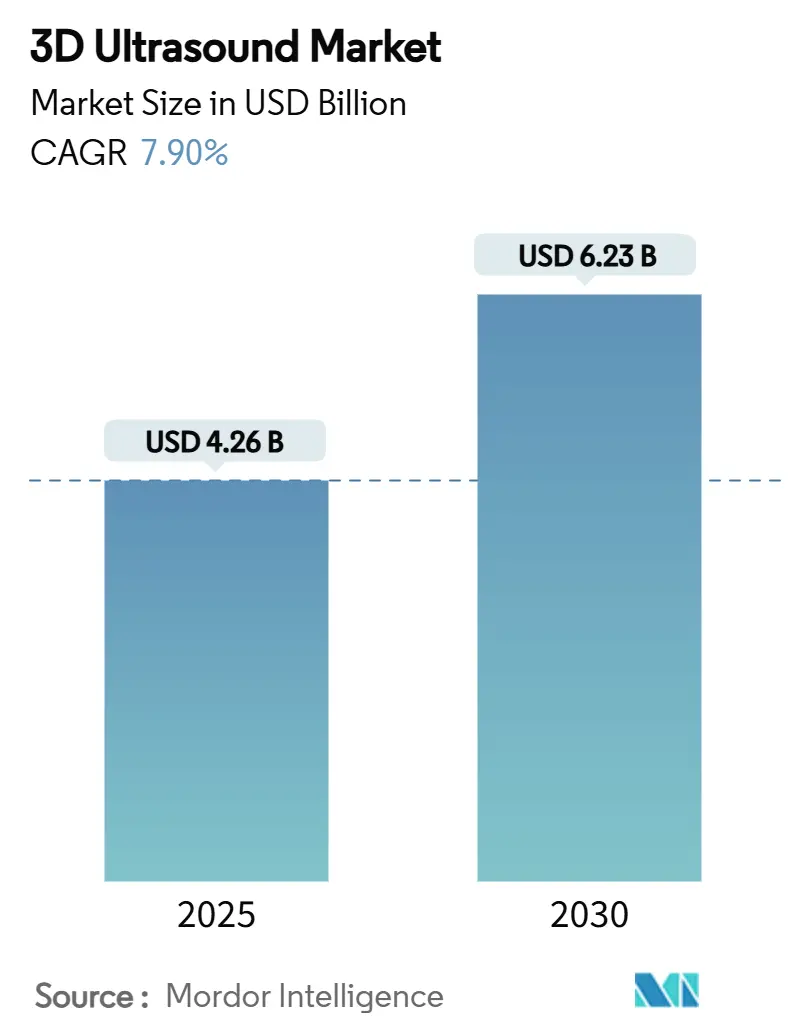

| Market Size (2025) | USD 4.26 Billion |

| Market Size (2030) | USD 6.23 Billion |

| Growth Rate (2025 - 2030) | 7.90% CAGR |

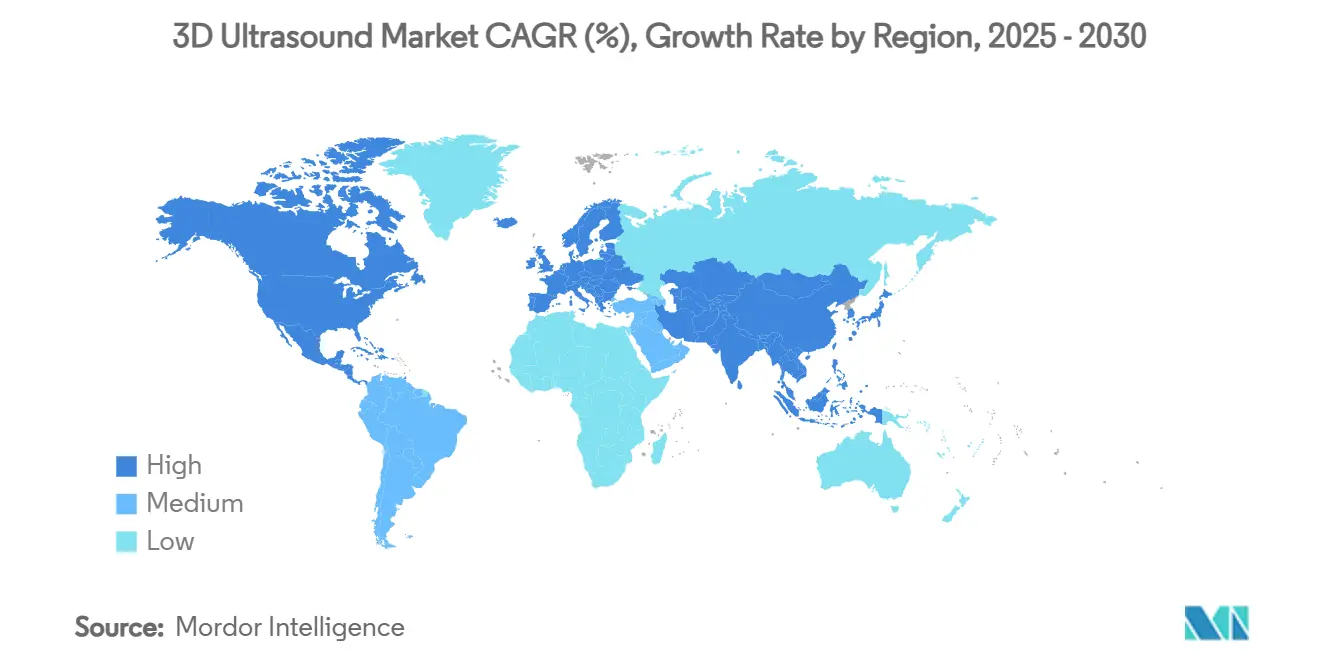

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

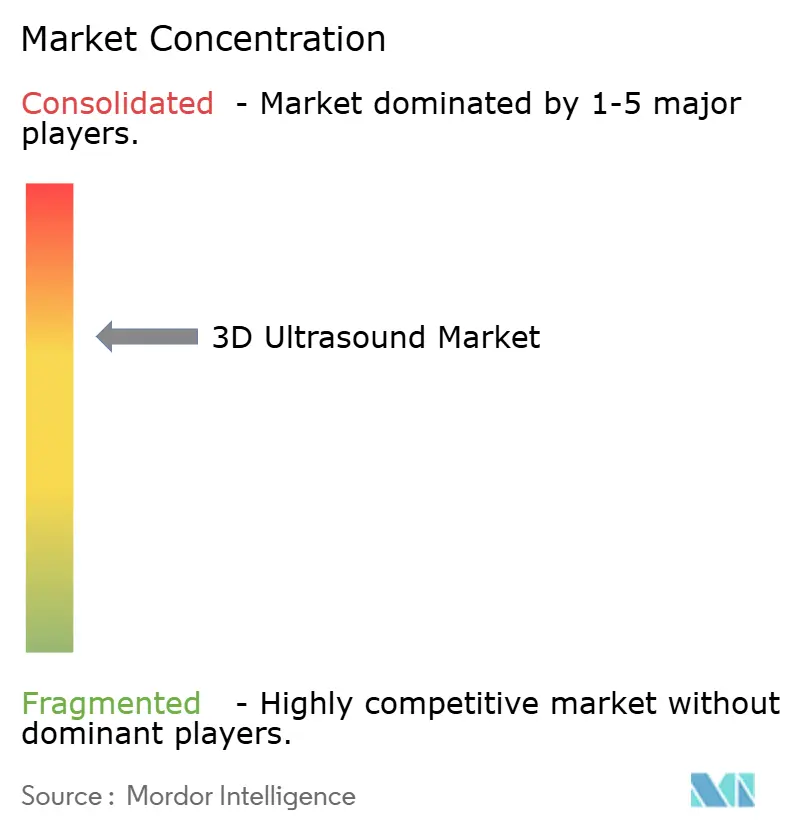

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Ultrasound Market Analysis by Mordor Intelligence

The global 3D ultrasound market size stands at USD 4.26 billion in 2025 and is projected to reach USD 6.23 billion by 2030, reflecting a 7.9% CAGR over the forecast period. Momentum is fueled by the convergence of artificial-intelligence-enabled workflow automation, demographic trends toward advanced maternal age, and a decisive shift from 2-D scans to volumetric visualization across cardiology, obstetrics, and emergency care. Handheld probes are rapidly gaining acceptance because they deliver real-time diagnostics without tethering clinicians to fixed imaging suites, thereby widening access at critical-care bedsides and in ambulatory settings. Industry leaders are advancing beyond incremental image-quality gains to cloud-connected fleets that deliver secure remote support, tele-operation, and fleet analytics—features that resonate with health systems seeking enterprise-level standardization. Capital investment cycles increasingly favor platforms that can be field-upgraded through software and AI modules, allowing providers to protect budgets while staying current with diagnostic innovations.

Key Report Takeaways

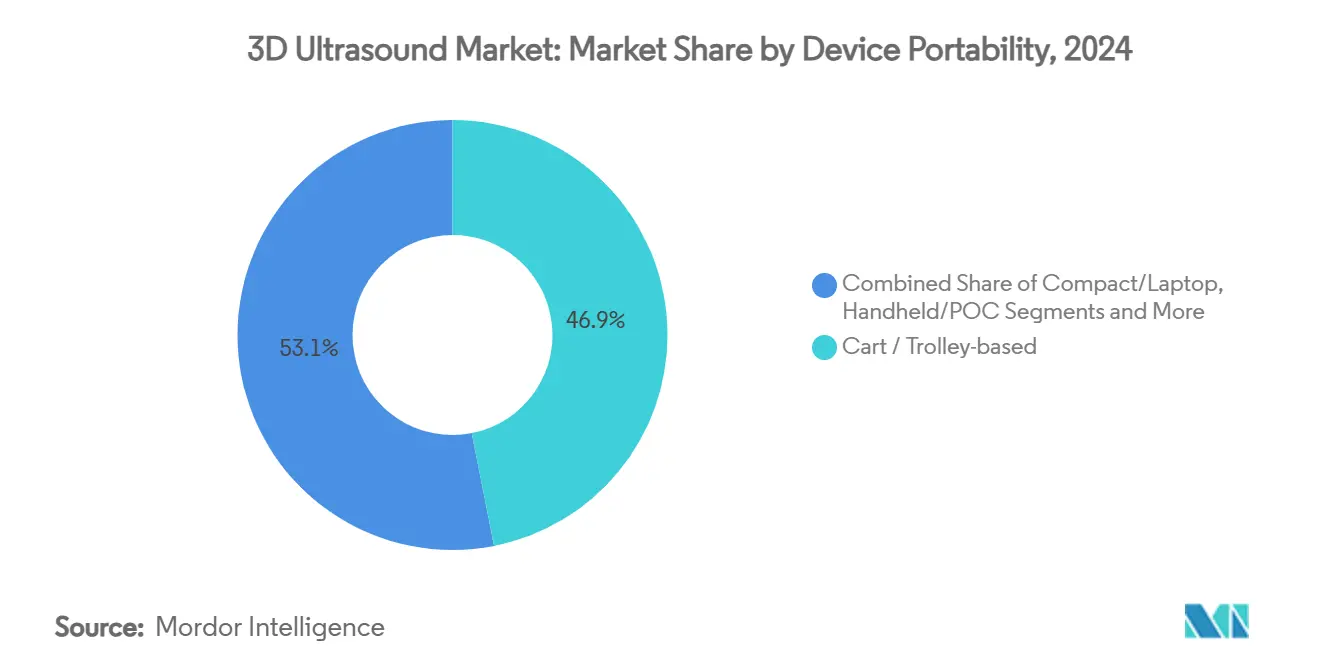

- By device portability, cart/trolley systems led with 46.9% revenue share in 2024, while handheld/point-of-care units posted the fastest 12.1% CAGR to 2030.

- By application, obstetrics & gynecology captured 38.4% of the 3D ultrasound market share in 2024, whereas cardiology is expanding at an 8.4% CAGR through 2030.

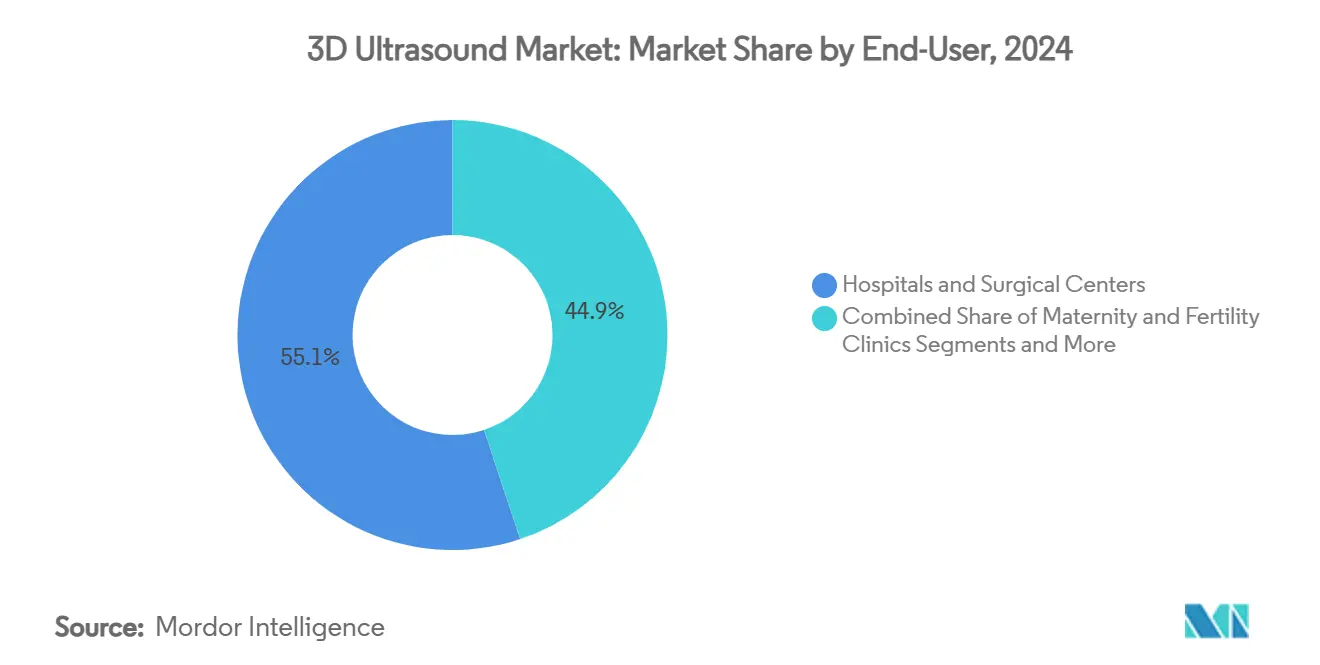

- By end-user, hospitals and surgical centers dominated with a 55.1% share in 2024, yet ambulatory surgery centers are advancing at an 8.9% CAGR to 2030.

- By transducer, curved/convex arrays accounted for 40.2% of the 3D ultrasound market size in 2024, while matrix arrays recorded a 9.5% CAGR through 2030.

- By region, North America led with a 29.8% share in 2024, and Asia-Pacific is projected to deliver the fastest 6.8% CAGR during the forecast horizon.

Global 3D Ultrasound Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven workflow automation in 3D OB/GYN imaging | +1.80% | North America, EU | Medium term (2-4 years) |

| Rising adoption of handheld 3D probes in emergency care | +1.50% | APAC, emerging markets | Short term (≤ 2 years) |

| Reimbursement expansion for volumetric breast screening (ABUS) | +1.20% | North America, EU | Long term (≥ 4 years) |

| Growing maternal age boosting fetal anomaly scans | +1.00% | Developed markets | Medium term (2-4 years) |

| Deployment of cloud-connected ultrasound fleets | +0.80% | Global | Medium term (2-4 years) |

| Rapid replacement of 2-D echo by 3-D TEE in structural heart disease | +0.70% | Global cardiac centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Workflow Automation in 3D OB/GYN Imaging

Integrating artificial intelligence into obstetric and gynecological scanning is reducing operator dependency and standardizing volumetric protocols. GE HealthCare’s 2024 acquisition of Intelligent Ultrasound’s ScanNav platform embeds automated anatomical recognition, slashing exam times by 25% while improving measurement consistency. Samsung’s USD 92.4 million takeover of Sonio strengthens real-time abnormality detection, a capability already cleared by the FDA for fetal applications. Research from the University of Ottawa confirms AI can flag cystic hygroma earlier and more accurately than manual review. The UltraGauss framework further accelerates 3-D reconstruction without sacrificing resolution, an advance that supports real-time clinical decision-making.[1]Eid Mark, “UltraGauss Reconstruction,” arxiv.orgCollectively, these technologies ease the burden on a shrinking sonographer workforce and heighten diagnostic reliability across varied skill levels.

Rising Adoption of Handheld 3D Probes in Emergency Care

Handheld 3-D ultrasound has evolved from a niche gadget to an indispensable emergency-department resource thanks to semiconductor miniaturization and on-device AI. The handheld segment is forecast to top USD 500 million in revenue by 2026, expanding 24.7% annually as clinicians increasingly rely on bedside imaging to expedite triage. GE HealthCare’s Vscan Air CL combines dual-probe versatility with wireless convenience, helping trauma teams pivot swiftly between superficial and deep structures during golden-hour assessment. Butterfly Network’s iQ3 shows how a single semiconductor chip can generate full-body 3-D scans and feed images to cloud analytics, reducing interpretation delays and democratizing expertise.

Reimbursement Expansion for Volumetric Breast Screening (ABUS)

Payers are recognizing that automated breast ultrasound improves cancer detection in dense tissue where mammography often underperforms. UnitedHealthcare’s 2025 policy update now covers ABUS exams as an adjunct to X-ray screening, signaling mainstream payer confidence. The Medicare fee schedule lists dedicated CPT codes that incentivize radiology practices to adopt ABUS workflows, while Philips’ economic analyses demonstrate exam-time reductions that offset capital costs. Hologic’s USD 350 million acquisition of Gynesonics showcases how therapeutic applications anchored in ultrasound guidance can also secure favorable reimbursement, broadening the economic case for volumetric imaging.

Growing Maternal Age Boosting Fetal Anomaly Scans

Women are delaying childbirth throughout developed economies, and maternal age 35 years or older is correlated with higher chromosomal-abnormality risk.[2]Line Elmerdahl Frederiksen, “Maternal Age and the Risk of Fetal Aneuploidy: A Nationwide Cohort Study of More Than 500,000 Singleton Pregnancies in Denmark from 2008 to 2017,” Acta Obstetricia et Gynecologica Scandinavica, obgyn.onlinelibrary.wiley.comFirst-trimester 3-D ultrasound now identifies roughly half of structural anomalies, helping clinicians recommend precision prenatal interventions. When combined with cell-free-DNA screening, volumetric imaging boosts detection sensitivity for trisomy 21 to 95.24% and achieves perfect detection for trisomies 18 and 13. These diagnostic gains reassure expectant parents and guide perinatal care decisions without invasive sampling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive matrix array transducers | -1.50% | Emerging markets | Medium term (2-4 years) |

| Shortage of sonographers trained on 3-D navigation | -1.20% | Developed markets | Long term (≥ 4 years) |

| MRI-ultrasound fusion in prostate imaging | -0.80% | North America, EU | Long term (≥ 4 years) |

| Import tariffs on electronics in price-sensitive markets | -0.50% | Bilateral trade corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Matrix Array Transducers

Matrix arrays deliver real-time volumes by firing thousands of elements simultaneously, yet this sophistication comes at a premium. Engineering innovations such as helicoid layouts for intracardiac catheters illustrate the intricacies that elevate manufacturing costs.[3] IEEE Transactions on Ultrasonics, “Helicoid Array Transducers,” ieee.org Researchers are experimenting with embossed polymer films to build large-area flexible arrays that can bend to patient contours and may eventually cut unit prices. Until cost curves decline, budget-constrained facilities will continue to deploy 2-D probes or low-element-count 3-D arrays, creating a two-tier adoption landscape.

Shortage of Sonographers Trained on 3-D Volume Navigation

Australia reports a 3,000-person shortfall, while 12% of National Health Service sonographer posts remain unfilled, reflecting an aging workforce that retires earlier than national averages. Transitioning from 2-D plane steering to 3-D volume manipulation requires extended fellowship programs, yet universities struggle to secure sufficient clinical placements. AI-driven automation may eventually ease the skills gap, but near-term shortages limit the pace at which providers can scale advanced modalities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Portability: Handheld Growth Redefines Point-of-Care

Cart systems continue to anchor tertiary-care imaging suites and represented 46.9% of the 3D ultrasound market in 2024. Still, handheld devices are sprinting ahead at 12.1% CAGR thanks to zero-footprint workflows that decouple exams from radiology departments. The handheld boom reflects semiconductor-on-probe designs that shrink beamforming electronics onto a single chip, enabling full-volume acquisition without bulky consoles. Philips Lumify and GE Vscan capitalize on app-based interfaces that stream DICOM studies into electronic records as soon as scans end, eliminating USB transfers. AI toolkits onboard these pocket devices provide real-time view-quality scoring, guiding novice users toward diagnostic frames. Public health agencies in APAC deploy handheld fleets for prenatal outreach in rural counties, underscoring how portability intersects with equity goals. Cart platforms fight back by incorporating multi-mode capabilities such as elastography and contrast imaging that handhelds cannot yet match, and by offering field-upgradeable GPUs to accelerate AI algorithms. Despite mobility gains, infection-control protocols still favor cart or compact systems in intensive-care units where probe sterilization and battery swaps remain logistical hurdles.

Compact laptops occupy a middle tier, serving anesthesia and interventional suites where horizontal mobility rather than pocket portability is required. Automated breast ultrasound scanners stand apart as specialized fixed stations optimized for prone positioning and high-density transducer arrays. Wearable patches hint at an ultramobile future; prototypes from UC San Diego have demonstrated continuous muscle-oxygen monitoring during rehabilitation, foreshadowing remote postop surveillance for orthopedic patients. As device spectra widen, procurement teams evaluate the lifetime cost of ownership, software-upgrade pathways, and cross-department usage rather than initial purchase price alone. These criteria further differentiate cart platforms—still the workhorses of cross-sectional imaging—from niche disruptors chasing decentralized care.

By Application: Cardiology Sprints Ahead

Obstetrics retains 38.4% of the 3D ultrasound market share due to entrenched screening protocols, yet cardiology is the headline growth story with an 8.4% CAGR as interventionalists demand volumetric TEE guidance for structural repairs. The expansion mirrors procedure mix trends—transcatheter mitral repair, left-atrial appendage closure, and hypertrophic-septal ablation all require intra-procedural 3-D roadmaps. AI quantification removes manual tracing variability, giving cardiologists immediate ejection-fraction numbers. OB/GYN practice still benefits from demographic tailwinds such as delayed childbearing and increased need for anomaly detection, but reimbursement upgrades for cardiac ultrasound create fresh revenue incentives. General radiology leverages 3-D scans for liver lesion characterization and multiplanar musculoskeletal reconstructions, broadening ultrasound’s reach into modalities once dominated by CT. Oncology research applies 3-D elastography to differentiate malignant thyroid nodules with high specificity, signaling another use case that could convert into mainstream protocols once broader validation is completed.

Electrophysiologists favor 3-D ICE catheters that display real-time atrial geometry during pulmonary-vein isolation, a capability that trims fluoroscopy dose. Pediatric cardiology is adopting 3-D fetal-heart mapping to counsel families pre-delivery, compressing the diagnostic-to-intervention timeline for congenital anomalies. Meanwhile, urology practices leverage 3-D kidney scans to guide percutaneous nephrolithotomy and measure stone burden volumetrically. Across the board, software add-ons that segment tissue types or flag hemodynamic anomalies underpin subscription models that generate recurring revenue streams beyond probe sales.

By End-User: ASC Momentum Builds

Hospitals and surgical centers purchased 55.1% of 3-D systems in 2024, a reflection of their procedural diversity and access to capital budgets. Ambulatory surgery centers, however, are growing 8.9% annually as payers push elective interventions to lower-cost sites and patients favor same-day recovery. ASCs integrate compact ultrasound into procedure suites for needle guidance, reducing reliance on fluoroscopy and accelerating turnover. Diagnostic imaging centers position 3-D ultrasound as an edge on competing MRI shops, marketing radiation-free vascular studies and same-visit results.

Fertility clinics employ 3-D follicular tracking to fine-tune stimulation protocols and improve oocyte retrieval timing. Primary-care physicians now adopt handheld probes for quick abdominal exams that can obviate emergency-department referrals, especially in underserved communities where imaging bottlenecks delay care. Tele-ultrasound oversight further enables nurse practitioners to perform standardized screening under remote expert supervision, widening effective access without expanding sonographer headcount.

By Transducer Type: Matrix Arrays Advance

Curved/convex arrays remain the staple for abdominal and prenatal scans at 40.2% share, yet matrix arrays grow 9.5% CAGR as vendors overcome manufacturing yield issues and refine beam-forming ASICs. Full-matrix TEE probes deliver single-beat left-ventricular volumes, eliminating ECG-gated stitching artifacts that plague multi-beat acquisitions. Transparent polymer arrays co-registered with optical fibers now enable hybrid photoacoustic imaging, opening dual-modality vistas for oncology. Linear arrays focus on carotid plaque and musculoskeletal tendon assessments, where high frequency and superficial penetration matter. Phased arrays dominate intercostal cardiac windows, while endocavitary probes deliver neonatal neurosonography and prostate biopsies with sweeping 3-D volumes that reduce sampling error.

Research labs pursue Hadamard-encoded row-column designs that slash channel counts without sacrificing resolution, promising future cost relief and lighter cables. As element counts climb, backend computing transitions to GPU clusters that render real-time cubes, reinforcing the symbiosis between hardware and AI.

Geography Analysis

North America commands 29.8% of the 3D ultrasound market thanks to mature reimbursement policies, early AI adoption, and a robust installed base that steers continual replacement cycles. Federal incentives for telehealth and cloud security accreditation further strengthen vendor pipelines as health systems modernize imaging fleets. Academic-industry collaborations funnel breakthroughs rapidly into clinical trials, and FDA clearance pathways for AI software remain predictable. Yet the region faces headwinds from a shrinking sonographer workforce and import tariffs on electronics components that inflate system prices.

Asia-Pacific delivers the fastest 6.8% CAGR through 2030 as China upgrades rural hospitals and India launches insurance schemes that reimburse point-of-care ultrasound. Revised Class III ultrasound guidelines streamline approvals, giving multinationals more apparent timelines for advanced probes. Local manufacturers leverage cost advantages to supply entry-level consoles, while global firms carve premium niches with AI and matrix-array tech. The region’s demographic profile—ageing populations and rising maternal age—adds sustained demand for cardiology and prenatal imaging.

Europe maintains steady uptake, buoyed by government screening programs and broad adherence to guidelines that encourage volumetric TEE in valvular work-ups. National health services negotiate volume-based pricing, nudging vendors to craft modular platforms that unlock advanced features via software keys. Middle East & Africa exhibit growing appetite for cloud-enabled ultrasound that mitigates specialist shortages; ministries pilot tele-ultrasound for obstetric outreach in remote deserts. South America eyes continuous-care models that tie handheld devices to primary-health campaigns, although currency volatility constrains high-end imports, pushing clinics toward refurbished consoles.

Competitive Landscape

The 3D ultrasound market shows moderate consolidation in which incumbents leverage AI, acquisitions, and cloud ecosystems to defend their share. GE HealthCare remains the largest player after absorbing Intelligent Ultrasound’s clinical AI unit for USD 53 million and partnering with NVIDIA to embed autonomous scan features. Siemens Healthineers counters with Acuson Sequoia 3.5, the first console to label abdominal organs automatically and adjust presets to patient habitus in real time. Samsung’s purchase of Sonio underscores a wider strategy to integrate specialized OB/GYN AI via the HERA platform, tightening its grip on women’s health.

Butterfly Network and other semiconductor entrants differentiate on probe-as-a-platform economics, offering subscription bundles that include unlimited software updates and cloud storage. Academic labs contribute disruptive prototypes—such as transparent arrays—that incumbents may license or acquire. Patent filings in 3-D image-reconstruction algorithms, elastography, and intravascular arrays illustrate a vibrant R&D race. International regulatory convergence, particularly China’s streamlined pathway for AI-embedded devices, lowers entry barriers for regional challengers who can tailor price-performance for domestic markets. Vendor success hinges on balancing hardware innovation with evidence-backed AI that wins clinician trust and payer reimbursement.

3D Ultrasound Industry Leaders

GE HealthCare

Siemens Healthineers

Philips

Canon Medical Systems

Samsung Medison

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Canon Healthcare USA acquired a Cleveland research facility to anchor its North American imaging headquarters and accelerate ultrasound, MRI, and CT innovation.

- January 2025: Hologic closed its USD 350 million purchase of Gynesonics, adding the Sonata System for incision-free fibroid therapy under ultrasound guidance.

- October 2024: GE HealthCare finalized its USD 53 million takeover of Intelligent Ultrasound’s clinical AI business.

- September 2024: Samsung sealed a USD 92.4 million deal for Sonio, adding FDA-cleared real-time fetal-imaging AI to its OB/GYN portfolio.

Global 3D Ultrasound Market Report Scope

| Cart / Trolley-based Systems |

| Compact / Laptop Systems |

| Handheld / POC Systems |

| Automated Breast Ultrasound Systems (ABUS) |

| Wearable / Patch Ultrasound |

| Obstetrics & Gynecology |

| Cardiology |

| Radiology / General Imaging |

| Urology & Kidney |

| Musculoskeletal & Vascular |

| Hospitals & Surgical Centers |

| Diagnostic Imaging Centers |

| Ambulatory Surgery Centers |

| Maternity & Fertility Clinics |

| Primary / Point-of-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Portability | Cart / Trolley-based Systems | |

| Compact / Laptop Systems | ||

| Handheld / POC Systems | ||

| Automated Breast Ultrasound Systems (ABUS) | ||

| Wearable / Patch Ultrasound | ||

| By Application | Obstetrics & Gynecology | |

| Cardiology | ||

| Radiology / General Imaging | ||

| Urology & Kidney | ||

| Musculoskeletal & Vascular | ||

| By End-User | Hospitals & Surgical Centers | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgery Centers | ||

| Maternity & Fertility Clinics | ||

| Primary / Point-of-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the 3D ultrasound market?

The 3D ultrasound market size is USD 4.26 billion in 2025 and is forecast to reach USD 6.23 billion by 2030.

Which segment is growing fastest?

Handheld or point-of-care devices are expanding at a 12.1% CAGR as emergency departments and ambulatory clinics adopt portable diagnostics.

Why is cardiology a high-growth application?

Structural-heart interventions increasingly rely on real-time 3-D TEE guidance, driving an 8.4% CAGR in cardiology adoption through 2030.

How are tariffs affecting the market?

A 26% US reciprocal tariff on Indian medical devices raises component costs in price-sensitive regions, trimming forecast CAGR by 0.5%.

What role does AI play in ultrasound workflows?

AI automates anatomical labeling, reduces scan times, and compensates for the sonographer shortage, adding up to 1.8% to forecast market CAGR.

Which region is expected to lead growth?

Asia-Pacific will record the fastest 6.8% CAGR owing to expanding healthcare coverage, regulatory streamlining, and growing maternal-age-related demand.

Page last updated on: