Saudi Arabia Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

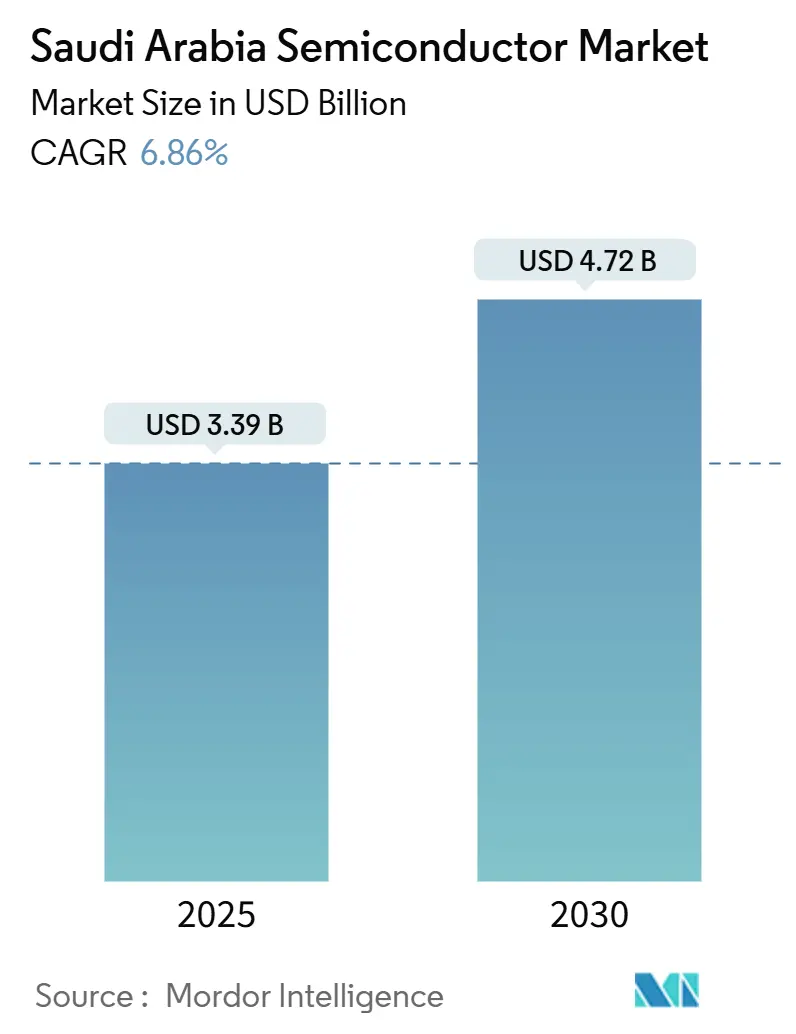

| Market Size (2025) | USD 3.39 Billion |

| Market Size (2030) | USD 4.72 Billion |

| Growth Rate (2025 - 2030) | 6.86% CAGR |

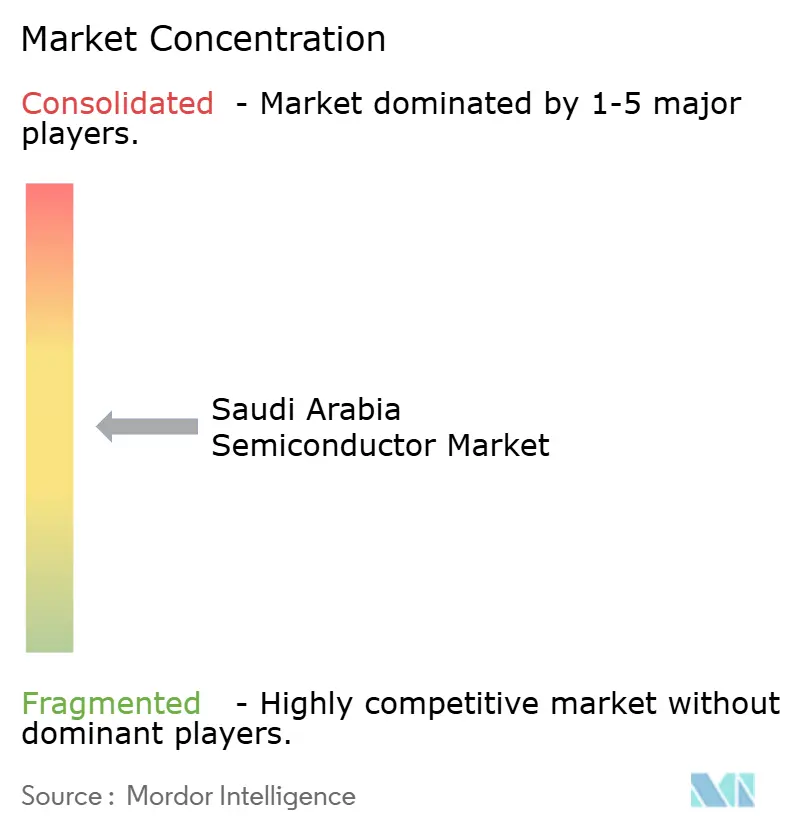

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Semiconductor Market Analysis by Mordor Intelligence

The Saudi Arabian semiconductor market size reached USD 3.39 billion in 2025 and is expected to expand to USD 4.72 billion by 2030, reflecting a 6.86% CAGR over the forecast period. Vision 2030’s mandate for technological sovereignty, the SAR 1 billion government-backed investment fund, and a plan to attract more than 50 fabless design houses continue to shape a favorable growth environment. Recent accords with the United States have removed earlier export restrictions and opened direct access to advanced AI chips from Nvidia and AMD, a development that strengthens domestic data-center capabilities and reduces supply-chain uncertainty. [1]Bloomberg, “US to Boost Saudi Access to AI Chips Even as China Issues Linger,” bloomberg.com The Kingdom’s abundant renewable‐energy resources, with wind and solar projects delivering electricity at 1.57-1.70 cents per kilowatt-hour, provide a structural operating-cost advantage for semiconductor manufacturing and packaging activities when compared with traditional hubs in East Asia and North America. Large-scale initiatives such as Alat’s USD 100 billion capital commitment, Qualcomm’s new design center, and Groq’s USD 1.5 billion AI-infrastructure program underscore a partnership-driven competitive landscape that prioritizes rapid capability transfer and ecosystem maturation.

Key Report Takeaways

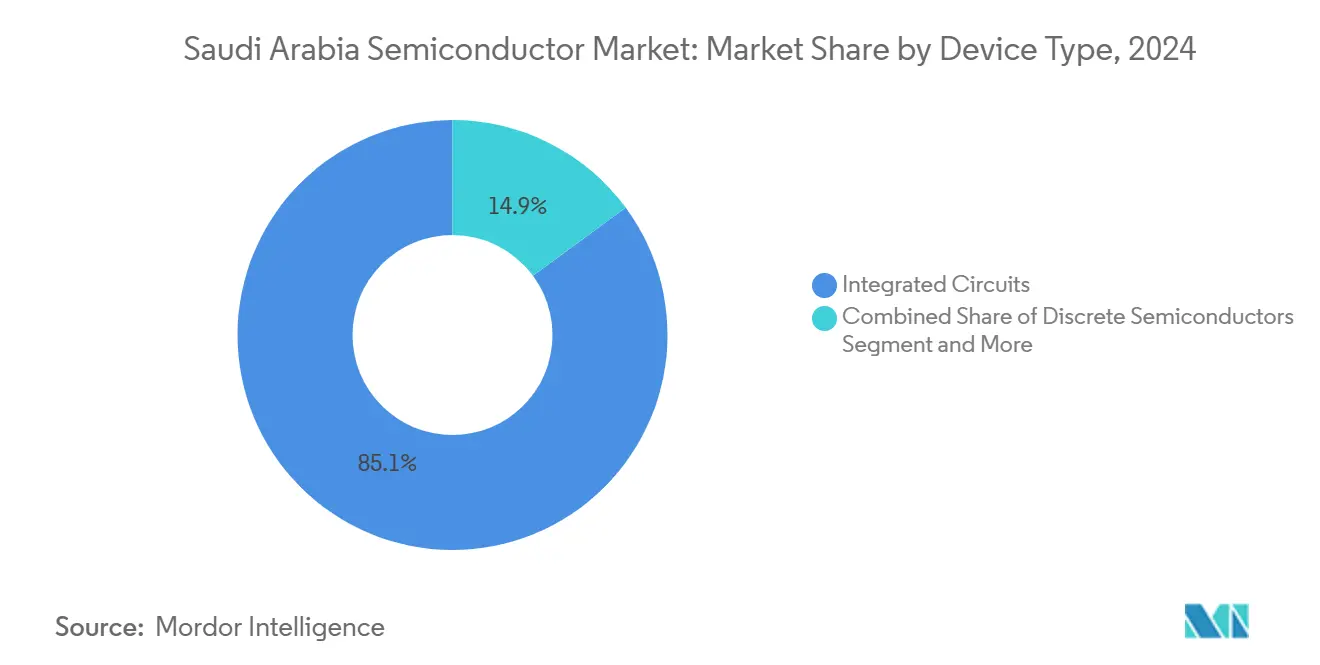

- By device type, Integrated Circuits led with 85.1% of the Saudi Arabian semiconductor market share in 2024, while Sensors and MEMS are projected to register the fastest 8.3% CAGR through 2030.

- By business model, the Integrated Device Manufacturer segment held 57.3% share of the Saudi Arabia semiconductor market size in 2024, whereas Design/Fabless Vendors are anticipated to post an 8.0% CAGR to 2030.

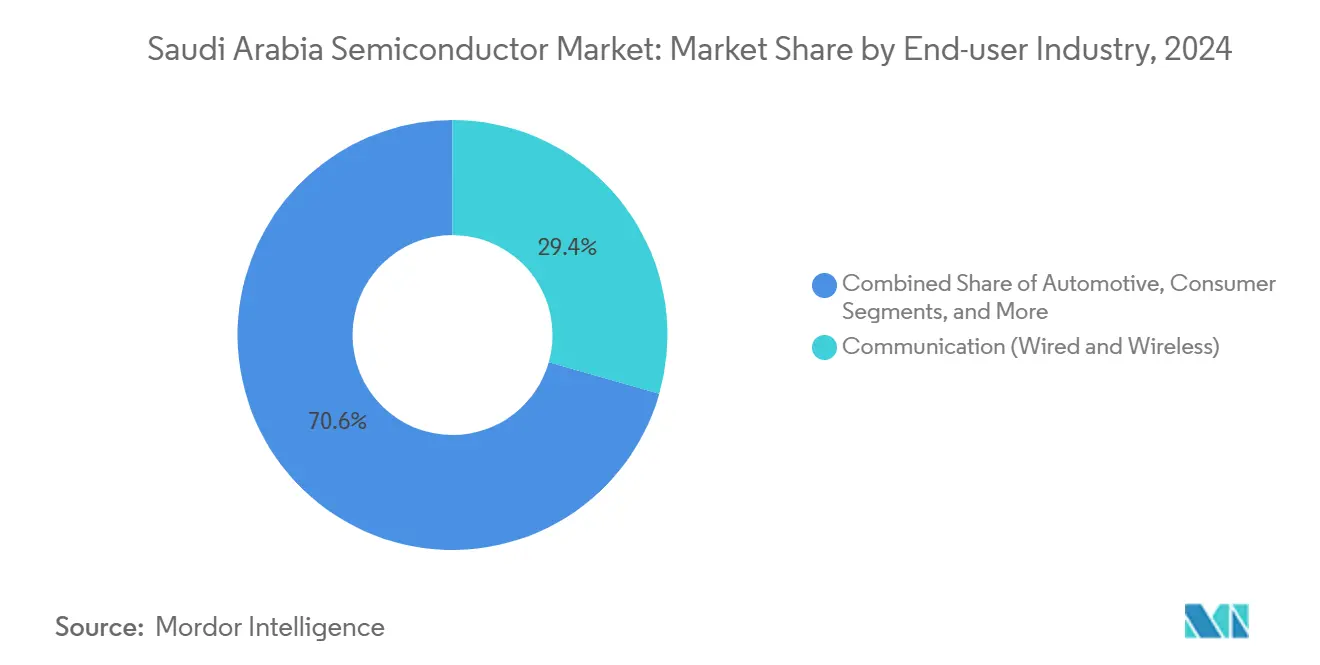

- By end-user industry, Communication applications accounted for 29.41% of the Saudi Arabian semiconductor market share in 2024; Artificial Intelligence end-use is set to expand at an 8.5% CAGR over 2025-2030.

Saudi Arabia Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed SAR 1 billion semiconductor investment fund | +1.2% | National (Riyadh, NEOM) | Medium term (2-4 years) |

| Vision 2030 incentives attracting 50+ fabless design houses | +0.9% | National (Riyadh, Jeddah, Dammam) | Long term (≥ 4 years) |

| Rising domestic demand for AI-centric datacenter chips | +1.5% | National; regional spill-over | Short term (≤ 2 years) |

| EV manufacturing roadmap boosting automotive IC uptake | +0.8% | King Abdullah Economic City | Medium term (2-4 years) |

| Abundant low-cost renewable energy lowering fab OPEX | +0.7% | NEOM and renewable zones | Long term (≥ 4 years) |

| Public–private quantum-foundry initiatives | +0.4% | KAUST and Aramco sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-backed SAR 1 billion semiconductor investment fund

The dedicated SAR 1 billion (USD 266 million) deep-tech fund supplies seed capital, salary subsidies, and relocation support to new and incoming chip-design enterprises, aiming to host 50 local design companies by 2030. Through the National Semiconductor Hub, three confirmed firms and ten prospects have already begun license and facility negotiations. [2]Quartz, “Saudi Arabia is getting into semiconductors, but it's not trying to beat Nvidia—yet,” qz.com The fund intentionally targets mature-node and application-specific devices, allowing Saudi Arabia semiconductor market participants to avoid head-to-head competition with leading-edge powerhouses such as TSMC and Intel. Structured incentives include locally benchmarked salary top-ups for Saudi engineers, soft-landing packages, and expedited incorporation procedures, thereby addressing both capital availability and human-resource shortages that commonly impede new semiconductor clusters.

Vision 2030 incentives create comprehensive fabless design ecosystem

A suite of regulatory and fiscal measures under Vision 2030 extends beyond venture capital. The Regional Headquarters program grants qualified multinationals 0% corporate tax on eligible income together with relaxed Saudization quotas, sharply lowering the cost of establishing a design presence within the Saudi Arabia semiconductor market corridors. A coordinated training pipeline, driven by King Abdulaziz City for Science and Technology and 16 partner universities, has already developed more than 400 microchip designers and fabrication researchers. Intellectual-property support services embedded in the program mitigate perceived legal-risk barriers, further enhancing the attractiveness of the Saudi Arabian semiconductor market for international design houses.

Rising domestic demand for AI-centric datacenter chips drives market expansion

The Public Investment Fund’s allocation of USD 40 billion to artificial-intelligence technology and HUMAIN’s multiyear supply contracts for several hundred-thousand high-end GPUs establish guaranteed near-term offtake for advanced semiconductors. Datacenter projects such as DataVolt’s USD 5 billion net-zero AI factory at NEOM create anchor customers that elevate national demand for processors, memory, and high-speed interconnect ICs. The goal of managing 7% of global AI model-training workloads by 2030 implies sustained silicon consumption well above current domestic output, reinforcing the strategic importance of expanding the Saudi Arabian semiconductor market.

EV manufacturing roadmap boosts automotive semiconductor opportunities

Lucid Motors’ 155,000-unit facility and Ceer’s planned 240,000-unit plant underpin a rising domestic need for power-management ICs, sensor suites, and advanced driver assistance system processors. Electric vehicles require USD 600-800 worth of semiconductors per unit, exceeding the USD 400 content in internal-combustion cars and translating into a multi-hundred-million-dollar uplift for the Saudi Arabian semiconductor market by mid-decade. Ceer’s commitment to reach 45% local-content sourcing intensifies supplier-qualification opportunities for design and packaging providers operating within the Kingdom.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited local technical talent and chip-design skill-gap | -0.8% | Nationwide | Medium term (2-4 years) |

| Absence of advanced-node fabs (< 7 nm) in the Kingdom | -1.1% | Nationwide | Long term (≥ 4 years) |

| Geopolitical export-license restrictions on leading-edge AI GPUs | -0.6% | Nationwide | Short term (≤ 2 years) |

| High capital-equipment import tariffs | -0.4% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited local technical talent constrains advanced semiconductor development

Despite a 24% rise in Saudi AI-talent availability during 2024, competition for engineers with experience in sub-10 nm lithography, advanced packaging, and machine-learning accelerators remains intense. KAUST’s Center of Excellence for Generative AI and new semiconductor curricula are medium-term solutions; for 2025-2027, many Saudi Arabian semiconductor market participants still rely on expatriate specialists or cross-border design collaborations. Worker-cost differentials with the finance and energy sectors further complicate recruitment.

Absence of advanced-node fabs limits high-value semiconductor production

Saudi Arabia has prioritized mature-node outsourced manufacturing, resulting in limited domestic capacity for sub-7 nm wafers vital to AI accelerators and flagship mobile processors. Dependence on distant foundries exposes supply chains to geopolitical tension and capacity-allocation risk, capping value capture for the Saudi Arabia semiconductor market. While this constraint avoids capital-intensive fab construction, it also postpones participation in the highest-margin product layers of the global semiconductor value chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Dominate Amid Sensors Growth

Integrated Circuits contributed 85.1% of 2024 revenue, securing the leading position within the Saudi Arabian semiconductor market. [3]Argaam, “Saudi Arabia launches SAR 1B fund…,” argaam.com Domestic hyperscale datacenter expansion and cloud-computing rollouts have kept demand elevated for server-class CPUs, GPUs, and memory. Logic ICs are increasingly customized for natural-language processing and large-language-model inference workloads ordered by HUMAIN and Datavolt clients. The Saudi Arabian semiconductor market size for Integrated Circuits is projected to grow in parallel with the overall sector trajectory, driven by AI, telecom, and automotive use cases.

Sensors and MEMS, though accounting for a smaller base, are forecast to register the fastest 8.3% CAGR to 2030. Electric-vehicle programs at Lucid and Ceer amplify uptake for inertial, pressure, and powertrain sensors, while nationwide smart-city deployments underpin demand for environmental and structural-health monitoring components. Industry 4.0 upgrades at Aramco and SABIC sites create incremental volumes for industrial MEMS, further widening the addressable opportunity set. As IoT connections proliferate across NEOM’s hydrogen valley, sensor fusion and edge analytics chips are poised for accelerated shipment growth inside the Saudi Arabian semiconductor market.

By Business Model: IDM Leadership Faces Fabless Challenge

Integrated Device Manufacturers maintained 57.3% revenue leadership in 2024 by leveraging global fabrication networks and established automotive-grade quality systems for clients like Lucid Motors and Ceer. Multinational IDMs—Samsung, STMicroelectronics, Infineon—pair overseas process technologies with Saudi channel partners to service industrial and energy customers, reinforcing trust-based procurement patterns.

Design/Fabless Vendors, however, are advancing at an 8.0% CAGR, supported by the National Semiconductor Hub’s subsidies and fast-track licensing. Qualcomm’s Riyadh design center and Groq’s neural-network coprocessor development epitomize an IP-centric entry mode that suits the Kingdom’s capital-light strategy. As localization targets raise pressure on automotive and AI supply chains, the Saudi Arabian semiconductor market share of fabless firms is expected to climb steadily, creating parallel domestic design-service demand for verification, testing, and advanced packaging.

By End-user Industry: Communication Leadership Challenged by AI Surge

Telecommunication infrastructure maintained a 29.41% slice of 2024 revenue, anchored by 5G macro-cell deployments, submarine-cable gateways, and metro ethernet backbones that utilize RF front-end modules, network processors, and optical transceivers. Operators such as STC and Zain continued multi-year RAN upgrades, reinforcing steady chip demand for the Saudi Arabian semiconductor market.

Artificial Intelligence workloads, however, represent the fastest-growing application with 8.5% CAGR through 2030, powered by Public Investment Fund’s USD 40 billion AI allocation and Groq’s USD 1.5 billion compute buildout. Cloud-to-edge architectures require high-bandwidth memory, AI accelerators, and low-latency switching ASICs, enlarging silicon volume potential. Automotive electronics round out key growth pockets: powertrain inverters, ADAS radar chips, and battery-management ICs are scaling in tandem with Lucid and Ceer production milestones.

Geography Analysis

Riyadh forms the nucleus of design, headquarters, and venture all-rainbow functions inside the Saudi Arabian semiconductor market, thanks to its close proximity to policy-makers and the broader financial ecosystem. The National Semiconductor Hub’s campus in the capital hosts pilot production labs, EDA tool suites, and a new chip-testing center sponsored by Alat.

NEOM stands out as a dual role zone: clean-energy powered manufacturing base and demand center for IoT sensors, vision processors, and quantum-ready computing. Datavolt’s net-zero factory and Samsung C&T’s SAR 1.3 billion robotics JV together create a greenfield environment to showcase semiconductor-enabled smart infrastructure.

King Abdullah Economic City serves as the automotive semiconductor cluster. Lucid’s and Ceer’s plants anchor a growing ecosystem of power-electronics packaging houses and tier-1 module integrators. Dammam’s proximity to Saudi Aramco and King Salman Energy Park stimulates the adoption of industrial automation ASICs and instrumentation sensors at Emerson’s new manufacturing hub.

Thuwal’s KAUST campus completes the geographic mosaic with advanced R&D assets for quantum computing and photonics. Aramco–Pasqal collaboration to build the region’s first quantum computer relies on cryogenic control chips, shaping a frontier-technology niche within the Saudi Arabia semiconductor market.

Competitive Landscape

The Saudi Arabian semiconductor market demonstrates moderated rivalry due to government-directed alignment of participants’ interests. Alat’s USD 100 billion pledge functions as both an investment vehicle and a cluster orchestrator, promoting joint ventures over zero-sum competition. Multinationals adopt partnership entry strategies—Qualcomm with HUMAIN, Groq with local AI start-ups—mitigating channel conflicts and accelerating knowledge transfer. [4]Qualcomm, “Qualcomm and HUMAIN to develop state-of-the-art AI data centers,” qualcomm.com

White-space arenas include automotive MCU packaging, renewable-energy inverter semiconductors, and specialty MEMS for harsh-environment oil-and-gas applications. Local firms that master reliability standards and localized reference designs can carve sustainable niches. Aramco’s Pasqal initiative signals demand beyond classic logic or memory, broadening competitive parameters to quantum and neuromorphic hardware.

Saudi Arabia Semiconductor Industry Leaders

-

Alat Company

-

STMicroelectronics N.V.

-

Infineon Technologies AG

-

NXP Semiconductors N.V.

-

Qualcomm Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Qualcomm and HUMAIN signed a memorandum to develop AI data centers and launch a Qualcomm Design Center in Saudi Arabia.

- May 2025: The United States approved expanded exports of Nvidia and AMD chips to Saudi customers, easing prior restrictions.

- April 2025: Groq unveiled a USD 1.5 billion AI-compute expansion program targeting Saudi sites.

- February 2025: Datavolt partnered with NEOM to build a USD 5 billion net-zero AI factory set for 2028 operation.

- February 2025: Ceer inked SAR 5.5 billion (USD 1.4 billion) supplier contracts for its 240,000-unit EV plant.

- January 2025: Lucid Motors joined the “Made in Saudi” program supporting industrial GDP expansion.

Saudi Arabia Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design/Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Centre |

| Artificial Intelligence |

| Government (Aerospace and Defence) |

| Other End-user Industries |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design/Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Centre | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defence) | ||||

| Other End-user Industries | ||||

Key Questions Answered in the Report

What is the revenue forecast for Saudi semiconductor suppliers by 2030?

Market revenue is expected to reach USD 4.72 billion in 2030, climbing from USD 3.39 billion in 2025.

Which device category captures most local semiconductor revenue?

Integrated Circuits held 85.1% of 2024 revenue, dominating national sales.

How fast are AI-related chip applications expanding?

AI end-use applications are projected to grow at an 8.5% CAGR between 2025 and 2030.

Where is the primary automotive-IC manufacturing cluster located?

King Abdullah Economic City hosts Lucid’s and Ceer’s EV plants, anchoring automotive IC demand.

What policy tool attracts foreign fabless design houses?

Vision 2030’s Regional Headquarters program offers 0% corporate tax and relaxed Saudization rules, encouraging multinational design centers.

Which megaproject provides the strongest renewable-energy advantage?

NEOM supplies wind and solar electricity at 1.57-1.70 cents per kWh, lowering fab operating costs.

Page last updated on: