Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Consumer Electronics Semiconductor Market Report is Segmented by Device Type (Discrete Semiconductors, Optoelectronics, Sensors and MEMS, and Integrated Circuits), Business Model (IDM and Design/Fabless Vendor), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

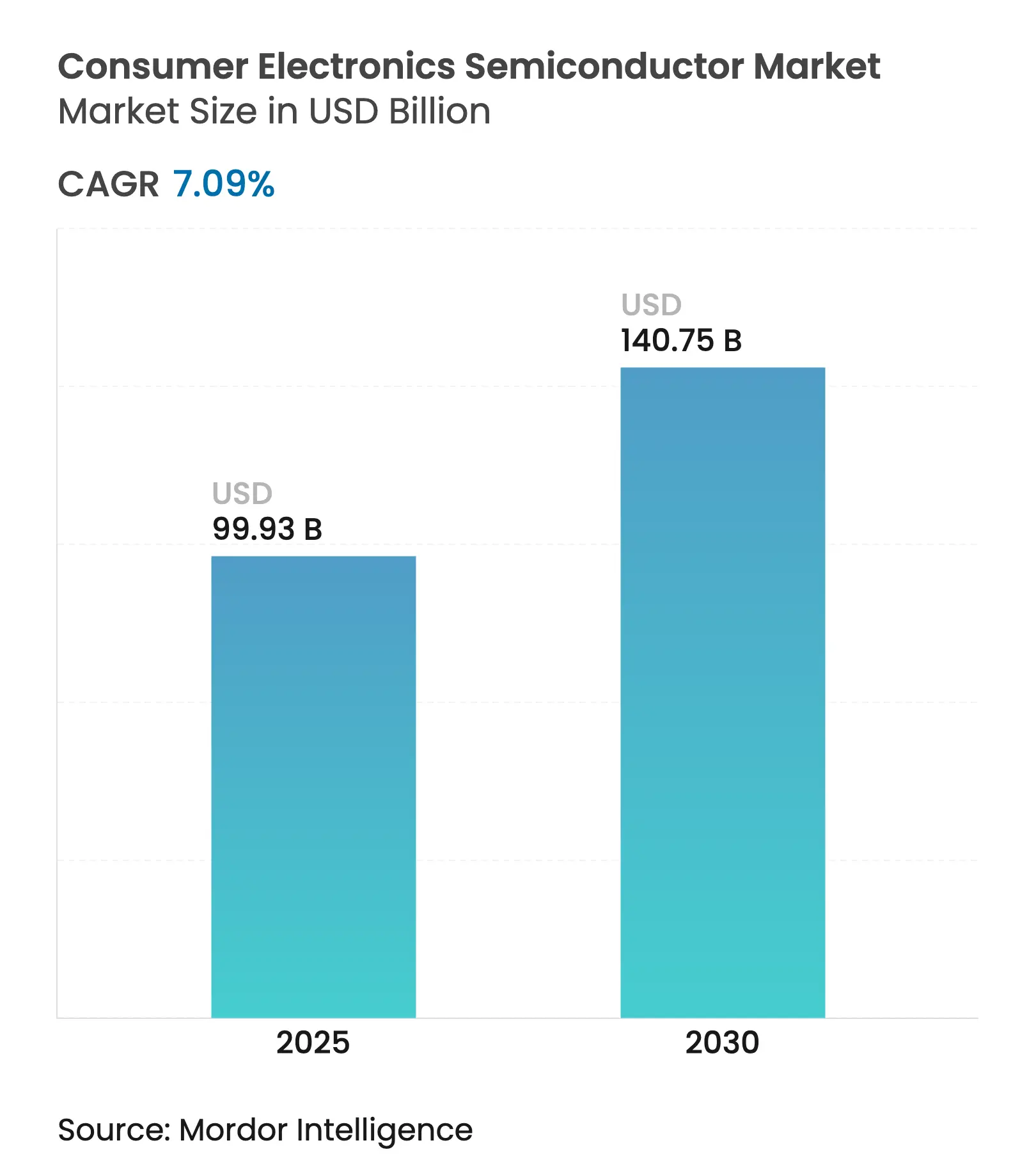

| Market Size (2025) | USD 99.93 Billion |

| Market Size (2030) | USD 140.75 Billion |

| Growth Rate (2025 - 2030) | 7.09 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

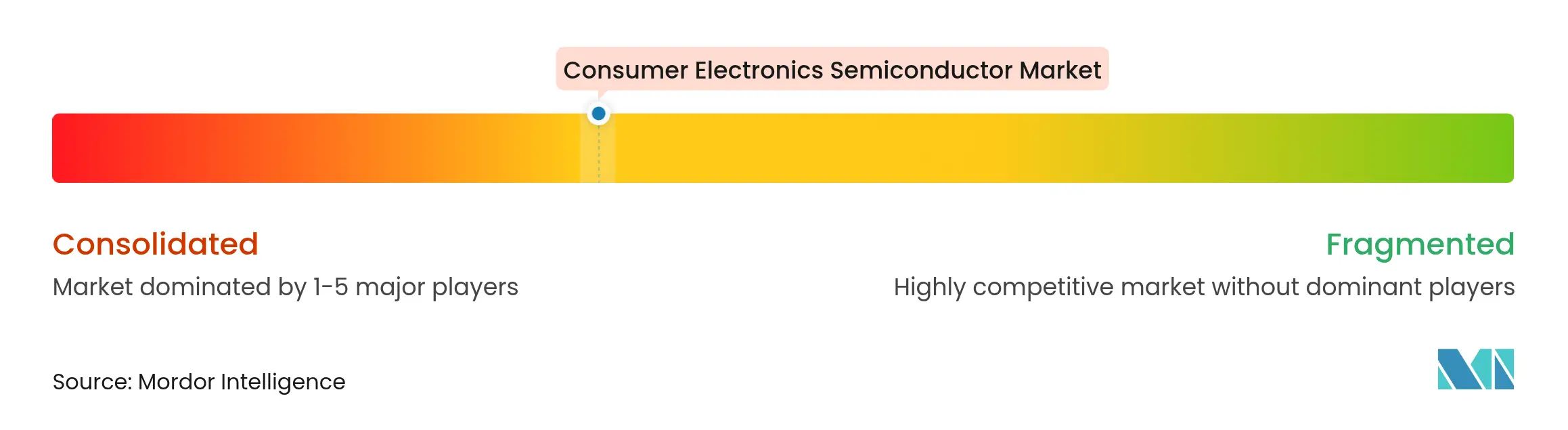

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The consumer electronics semiconductor market size stands at USD 99.93 billion in 2025 and is forecast to reach USD 140.75 billion by 2030, advancing at a 7.09% CAGR. The expansion reflects resilient end-user demand, accelerated integration of artificial intelligence, and rapid 5G uptake that together sustain high silicon content per device. Persistent supply–demand mismatches at leading-edge nodes below 7 nm, combined with government-funded capacity build-outs in the United States and Europe, have elevated strategic interest in geographic diversification. Edge-AI inferencing in connected appliances, the mainstreaming of OLED and mini-LED displays, and a legislative shift toward right-to-repair all widen the application field and encourage modular chip design. At the same time, inflationary pressures on bills of materials, coupled with tightening sustainability regulations, compel manufacturers to refine cost structures and energy footprints while defending market position. [1]Supply Chain 247, “Impact of Inflation on Electronics Components,” supplychain247.com

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising consumer demand for smart connected devices and IoT wearables Rising consumer demand for smart connected devices and IoT wearables | +1.8% | Global; early North America, Asia-Pacific core | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:+1.8% |

Geographic Relevance

:Global; early North America, Asia-Pacific core |

Impact Timeline

:Medium term (2-4 years) |

Rapid 5G smartphone penetration driving advanced SoC volumes Rapid 5G smartphone penetration driving advanced SoC volumes | +2.1% | Global; spill-over to emerging markets | Short term (≤ 2 years) | |||

Continuing miniaturization enabling higher functionality per device Continuing miniaturization enabling higher functionality per device | +1.5% | Global; led by Taiwan and South Korea | Long term (≥ 4 years) | |||

Growing adoption of OLED/mini-LED displays requiring specialized drivers and image sensors Growing adoption of OLED/mini-LED displays requiring specialized drivers and image sensors | +1.2% | Asia-Pacific core; expanding to North America and EU | Medium term (2-4 years) | |||

Expansion of edge-AI inferencing in home appliances propelling demand for dedicated NPUs Expansion of edge-AI inferencing in home appliances propelling demand for dedicated NPUs | +1.9% | North America and EU early; APAC manufacturing | Medium term (2-4 years) | |||

Increased right-to-repair legislation fostering demand for modular semiconductor sub-assemblies Increased right-to-repair legislation fostering demand for modular semiconductor sub-assemblies | +0.8% | EU leadership; North America following | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid 5G Smartphone Penetration Driving Advanced SoC Volumes

By mid-2025, more than half of new smartphones shipped will embed 5G modems, lifting wafer demand for 3 nm and 4 nm system-on-chips, especially those integrating on-die AI accelerators. Qualcomm’s handset-chip revenue reached USD 6.93 billion in Q2 2025, up 12% year-on-year, as Chinese brands upgraded flagship models. [2]CNBC Staff, “Qualcomm Tops Estimates but Guides Lower,” cnbc.com MediaTek’s Q1 2025 sales rose 14.9% year-on-year, reflecting momentum for high-performance Dimensity processors with integrated Wi-Fi 7 and on-device AI engines. Apple’s reported in-house baseband roadmap reinforces vertical integration trends and signals future shifts in supplier mix that could reshape contract-foundry allocations over the forecast period. The acceleration of chiplet-based SoC architectures further amplifies design complexity while trimming time-to-market, favoring specialist EDA and substrate suppliers.

Expansion of Edge-AI Inferencing in Home Appliances Propelling Demand for Dedicated NPUs

Edge-AI revenue for household appliances is moving from pilot stage to volume production as embedded neural-processing units migrate from mobile to large-form-factor devices. Samsung enlarged its NPU design team by 200 engineers in 2025, while the NPU market is set to reach USD 117 billion by 2030. [3]KED Global Reporters, “Samsung Ramps Up NPU R&D,” kedglobal.com The Exynos 2400 shows a 14.7-fold performance jump over the prior generation, highlighting iterative gains in tera-ops per watt critical for always-on voice and vision workloads. Qualcomm’s Snapdragon 8 Gen 3 delivers a 98% uplift in NPU throughput, enabling real-time image enhancement without cloud latency. Microcontrollers embedding low-power NPU cores from vendors such as Alif Semiconductor make AI cost-effective for white-goods OEMs. Hybrid edge–cloud frameworks, profiled in the 2025 Edge AI Technology Report, emphasize workload orchestration that balances privacy with compute efficiency.

Growing Adoption of OLED/Mini-LED Displays Requiring Specialized Drivers and Image Sensors

Mini-LED TV shipments are projected at 6.42 million units in 2024, up 59% on the previous year, edging past OLED volumes for the first time. Automotive cockpit digitization accelerates uptake; display panel shipments for vehicles are forecast at 257 million units by 2028, demanding driver ICs that manage high-contrast local dimming zones. OLED-on-silicon microdisplays, prized for augmented-reality lenses, need precision voltage-driving pixel circuits that widen programming ranges by more than fivefold versus legacy methods. Image sensor vendors benefit from the shift toward high dynamic-range cameras that optimize contrast behind transparent OLED panels. Asian foundries with legacy 28 nm capacity repurposed for driver IC production gain new utilization paths, mitigating dependency on smartphone silicon cycles.

Increased Right-to-Repair Legislation Fostering Demand for Modular Semiconductor Sub-Assemblies

The EU Right to Repair Directive, effective July 2024, obliges suppliers to provide spare parts and repair documentation for displays and smartphones for at least seven years, cutting material waste and saving consumers an estimated EUR 176 million over 15 years. Semiconductor vendors are responding with socket-friendly board designs and chiplet-based sub-assemblies that allow partial upgrades without full product replacement. Framework’s modular laptop blueprint and Apple’s expanding trade-in ecosystem illustrate commercial paths to compliance. Analysts estimate 30% of smartphones and 15% of laptops sold in 2025 will feature modular components that facilitate refurbishing yet raise reverse-logistics complexity. Circular-economy incentives are prompting deeper partnerships between chip makers, recyclers, and retailers, with blockchain pilots tracking critical minerals to validate secondary-use loops.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Supply–demand imbalances and capacity constraints at leading-edge nodes Supply–demand imbalances and capacity constraints at leading-edge nodes | −1.4% | Global; concentrated in Taiwan and South Korea | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:−1.4% |

Geographic Relevance

:Global; concentrated in Taiwan and South Korea |

Impact Timeline

:Short term (≤ 2 years) |

Geopolitical trade restrictions on semiconductor technology flows Geopolitical trade restrictions on semiconductor technology flows | −1.1% | U.S.–China tensions; global supply chain impacts | Medium term (2-4 years) | |||

Rising bill-of-materials inflation pushing OEMs toward SKU consolidation Rising bill-of-materials inflation pushing OEMs toward SKU consolidation | −0.9% | Global; acute in cost-sensitive segments | Short term (≤ 2 years) | |||

Energy intensity of advanced fabs conflicting with corporate net-zero targets Energy intensity of advanced fabs conflicting with corporate net-zero targets | −0.7% | Global; EU regulations and voluntary commitments elsewhere | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Supply–Demand Imbalances and Capacity Constraints at Leading-Edge Nodes

Foundry scheduling remains tight despite cyclical corrections. By late 2024, TSMC’s 5 nm utilization dipped during smartphone order pauses, yet 3 nm and pilot 2 nm allocations rapidly oversubscribed as AI accelerator orders surged. Samsung aims to start 2 nm risk production in late 2025, while Intel targets 100,000 wafers per month of sub-5 nm capacity by 2027, aided by prospective TSMC joint-venture operations. Analysts foresee a structural gap in sub-11 nm supply after 2026, even as mature-node capacity loosens, compelling OEMs to negotiate pre-payments and longer binding supply agreements. These bottlenecks curb near-term growth potential for the consumer electronics semiconductor market, though they also galvanize multiregional fab investments that diversify risk.

Rising Bill-of-Materials Inflation Pushing OEMs Toward SKU Consolidation

Component price inflation of 20-30% since 2024, driven by energy costs and lingering logistics disruptions, pushes device brands to streamline product portfolios. DRAM illustrates the squeeze: DDR4 16 GB chips hit USD 12 in July 2025 after Micron curtailed output to favor DDR5, adding cost pressure for mid-tier smartphones. Foundries pass through utility-price surcharges and wage inflation, lifting average die costs; a next-generation fab can now exceed USD 30 billion in capex, intensifying scrutiny over pricing transparency. To defend margins, OEMs rationalize SKUs, double-source critical components, and redesign boards for cross-platform compatibility, tactics that modulate wafer demand patterns in the consumer electronics semiconductor market.

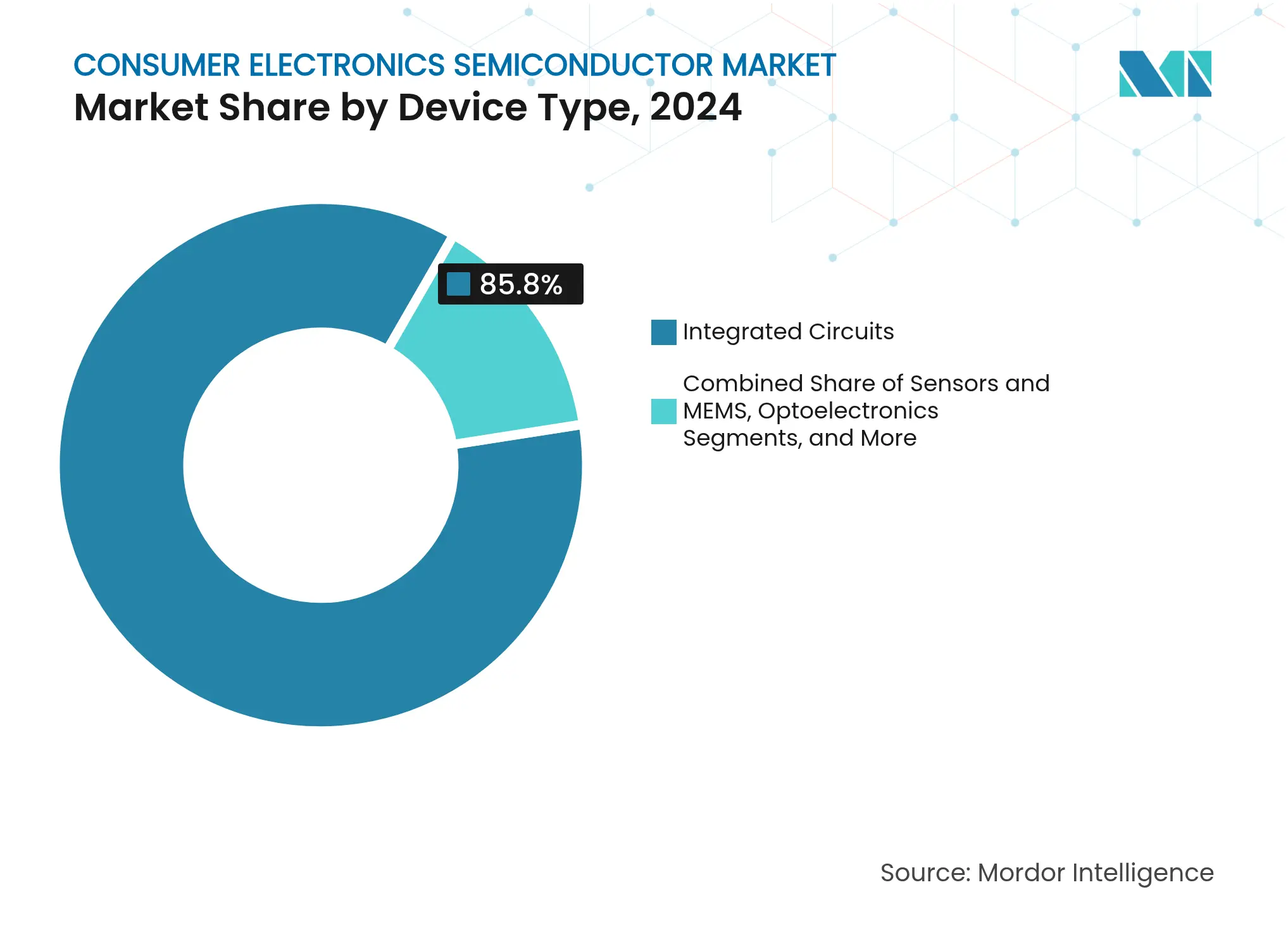

By Device Type: Integrated Circuits Anchor Market While Sensors Drive Innovation

Integrated circuits account for an 85.8% revenue slice of the consumer electronics semiconductor market in 2024. This dominance stems from the high silicon content of flagship smartphones, tablets, wearables, and smart-TV SoCs that adopt chiplet architectures to merge CPU clusters with AI engines and modem blocks. The consumer electronics semiconductor market size for integrated circuits is forecast to expand steadily through 2030 as vendors migrate high-volume parts from 7 nm to 4 nm to attain energy-efficiency targets without fully abandoning mature back-end intellectual property. Growth remains tempered by rising photomask costs and the need for EUV lithography tooling that only a handful of foundries can afford. Even so, architectural breakthroughs such as heterogeneous in-package stacking allow performance gains without node shrinks, enabling mid-range devices to capture premium-tier features and extending IC relevance across price points.

Sensor and MEMS shipments, while representing a smaller absolute value base, deliver the fastest segment growth at 8.6% CAGR. Demand surges from automotive pressure and inertial units, environmental sensing in health-focused wearables, and periscope camera modules in smartphones. The consumer electronics semiconductor market share for sensors rises in tandem with ultra-wideband positioning and radar-on-a-chip solutions that enable spatial-computing headsets. MEMS micromirror arrays for laser-beam scanning bolster AR glasses, while barometric pressure sensors help smartphones deliver centimeter-level indoor location accuracy, unlocking new app ecosystems. Foundries with 8-inch MEMS capacity capitalize on this uplift, offsetting weaker demand for legacy analog devices and diversifying revenue streams beyond volatile handset cycles.

Note: Segment shares of all individual segments available upon report purchase

By Business Model: Design Houses Challenge IDM Dominance Through Specialization

IDM enterprises retain 66.8% of the consumer electronics semiconductor market revenue in 2024. Their vertically integrated model confers process optimization control, captive capacity allocation, and deep co-design with OEMs. Yet that scale also embeds higher fixed costs and slower pivot speed when end-use trends shift. Over the forecast horizon, leading IDMs channel capex primarily toward power-efficient logic and advanced packaging to maintain competitiveness against asset-light rivals. Partnerships with design-tool vendors expedite internal IP reuse, lowering the effective cost per tape-out.

The fabless cohort, capturing the remaining 33.2% share but growing at an 8.2% CAGR, exemplifies agility. Qualcomm’s strategy to repurpose smartphone modem know-how into connected-vehicle telematics and mixed-reality chips underscores the leverage enjoyed by design-centric firms. Apple’s in-house silicon expansion and Google’s Tensor roadmap validate the premise that software-defined differentiation rests on custom silicon, accelerating demand for third-party foundry services. The consumer electronics semiconductor market size attributed to fabless players is expected to crest USD 60 billion by 2030, provided capacity access remains stable. However, dependence on a narrow set of leading-edge fabs exposes these vendors to allocation risk, spurring exploration of multichiplet partitioning that can distribute dies across mature nodes to hedge shortages.

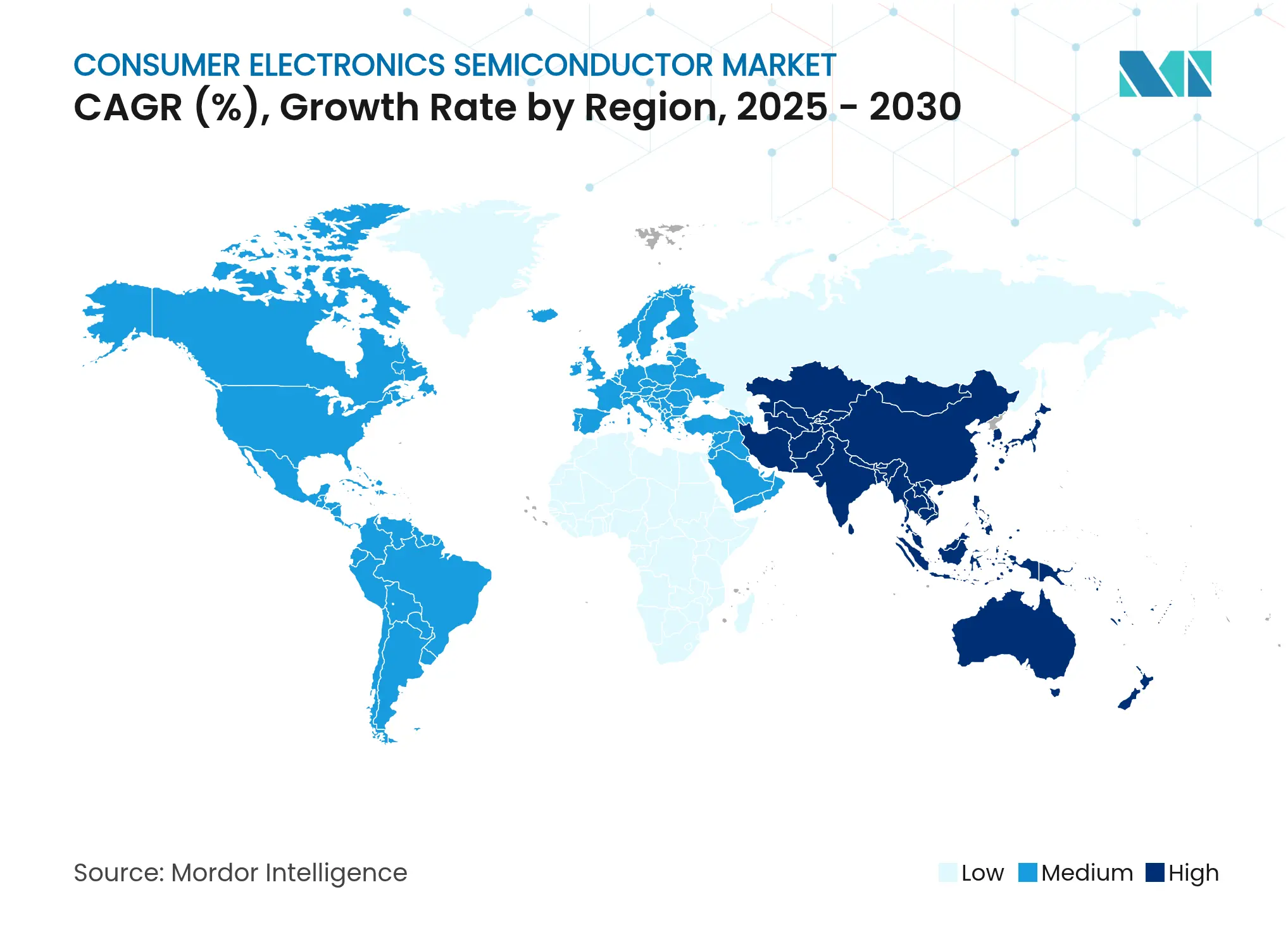

Asia-Pacific generated 51.2% of global revenue for the consumer electronics semiconductor market in 2024, supported by Taiwan’s 66% share of advanced contract-manufacturing capacity and China’s aggressive domestic subsidy programs. Regional growth is projected at an 8.1% CAGR through 2030 as local brands upgrade camera, display, and AI functionality to stand out in intensely competitive handset and TV segments. China’s share could climb to 31% by 2027 as foundries in Shenzhen and Shanghai add 28 nm and 14 nm lines, reducing reliance on imported chips. South Korea remains the memory epicenter, yet redirecting capital into U.S. fabs to secure CHIPS Act incentives may dilute local investment, opening white-space for Japanese and Taiwanese specialty material suppliers to capture value.

North America commands 19% of the consumer electronics semiconductor market and is the fastest-growing geography with an 8.5% CAGR forecast through 2030. The CHIPS Act’s USD 52 billion funding package, augmented by state-level tax abatements, underwrites fabs in Arizona, Ohio, and New York designed for sub-4 nm production. TSMC’s USD 40 billion Phoenix campus targets 20,000 wafers per month by 2026, while Intel’s foundry reorganization seeks to reclaim technology leadership via joint-venture models that blend external customer volume with internal CPU output. These facilities prioritize AI accelerators and high-speed connectivity dies, diversifying regional product mixes beyond legacy automotive nodes and lifting the consumer electronics semiconductor market size in the region.

Europe holds 9% of the consumer electronics semiconductor market. Although its share trails Asia-Pacific and North America, the EU aims to double capacity by 2030 via an incentive pool exceeding EUR 43 billion. Germany’s approval of subsidies for a 3 nm fab and France’s initiative for sovereign packaging competency illustrate policy vigor. Yet talent scarcity and longer environmental permit cycles slow groundbreaks, tempering short-term output growth. Still, Europe excels in wafer equipment, analog power devices, and gallium-nitride RF solutions, sectors with high margins and strategic value. Collaborative platforms such as the European Semiconductor Regions Alliance facilitate cross-border R&D, bolstering technology sovereignty ambitions without dislocating existing supply chains.

Market Concentration

Global foundry concentration remains high: TSMC commands 61.7% share, Samsung follows at 17%, and GlobalFoundries, UMC, and SMIC make up much of the balance. [4]Macrowise Brief, “Global Foundry Share 2024,” macrowise.substack.com TSMC’s early-mover advantage in 3 nm yields attracts AI chip providers who crave transistor-density gains for transformer models that push bandwidth limits. Samsung leverages in-house EUV clusters to synchronize memory and logic roadmaps, while Intel seeks a turnaround via process node acceleration and external customer acquisition. Within the consumer electronics semiconductor market, vertical integration intensifies as Apple, Amazon, and Google craft custom SoCs that embed proprietary AI engines, shortening feedback loops between software features and silicon capabilities.

Strategic alliances around advanced packaging have become a differentiator as Moore’s law deceleration elevates substrate design importance. TSMC is expanding its CoWoS capacity by 80% between 2024 and 2026, specifically to host AI GPUs demanding >1 TB/s package bandwidth. Samsung and Amkor invest in fan-out panel-level packaging that can lower the cost per square millimeter for large-area die-stacks targeting tablets and foldables. Materials suppliers such as 3M, which joined the US-JOINT Consortium in 2025, introduce thermally conductive adhesives that dissipate heat from vertically stacked dielets, solving a chronic thermal bottleneck in thin consumer devices.

Emerging disruptors chase geopolitical white-space. Shanghai-based SMIC is progressing on deep-UV-only 5 nm line development, aiming to circumvent export license constraints. Will Semiconductor, a leading CMOS-sensor vendor, benefits from robust domestic smartphone replacement cycles, posting double-digit growth despite global handset softness. In the United States, SkyWater’s acquisition of Infineon’s Austin fab unlocks mature-node supply for automotive and defense customers, supporting regulatory calls for trusted local production. The competitive dialogue now places equal weight on carbon-reduction roadmaps; leading players pledge 100% renewable electricity by 2030, rewarding fabs located near low-carbon grids and catalyzing new partnerships with utility providers.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

A semiconductor device is an electronic component made from semiconductor materials like silicon. It exhibits variable electrical conductivity, enabling control and manipulation of electrical currents. Common semiconductor devices include transistors, diodes, and integrated circuits. These devices are fundamental in modern electronics, serving functions like signal amplification, switching, and signal processing. They form the core of microchips, enabling the operation of computers, smartphones, and countless other electronic devices, making them integral to the functioning of our technologically driven world.

The semiconductor device market in the consumer industry is divided into various segments, including discrete semiconductors, optoelectronics, sensors, and integrated circuits (analog, logic, memory, and micro (microprocessors, microcontrollers, and digital signal processors)). This market analysis encompasses regions such as the United States, Europe, Japan, China, Korea, Taiwan, and the Rest of the World.

Market sizes and future predictions are expressed in terms of monetary value (USD) for each of these segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.