Mexico Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.02 Billion |

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Heat Pump Market Analysis by Mordor Intelligence

The Mexico heat pump market size is projected to expand from USD 1.02 billion in 2025 and USD 1.08 billion in 2026 to USD 1.38 billion by 2031, registering a CAGR of 5.02% between 2026 to 2031. Uptake is accelerating as longer, hotter summers raise cooling loads, while recent regulations drive replacement of low-efficiency rooftop units with inverter-based systems. Falling prices for distributed solar have also improved the business case for hybrid photovoltaic-heat-pump projects that cut grid purchases and hedge against tariff volatility. Multinational manufacturers are localizing production of R32 and R454B models, shortening lead times and lowering import costs. However, grid bottlenecks in the Yucatán Peninsula and limited residential incentives temper near-term penetration.

Key Report Takeaways

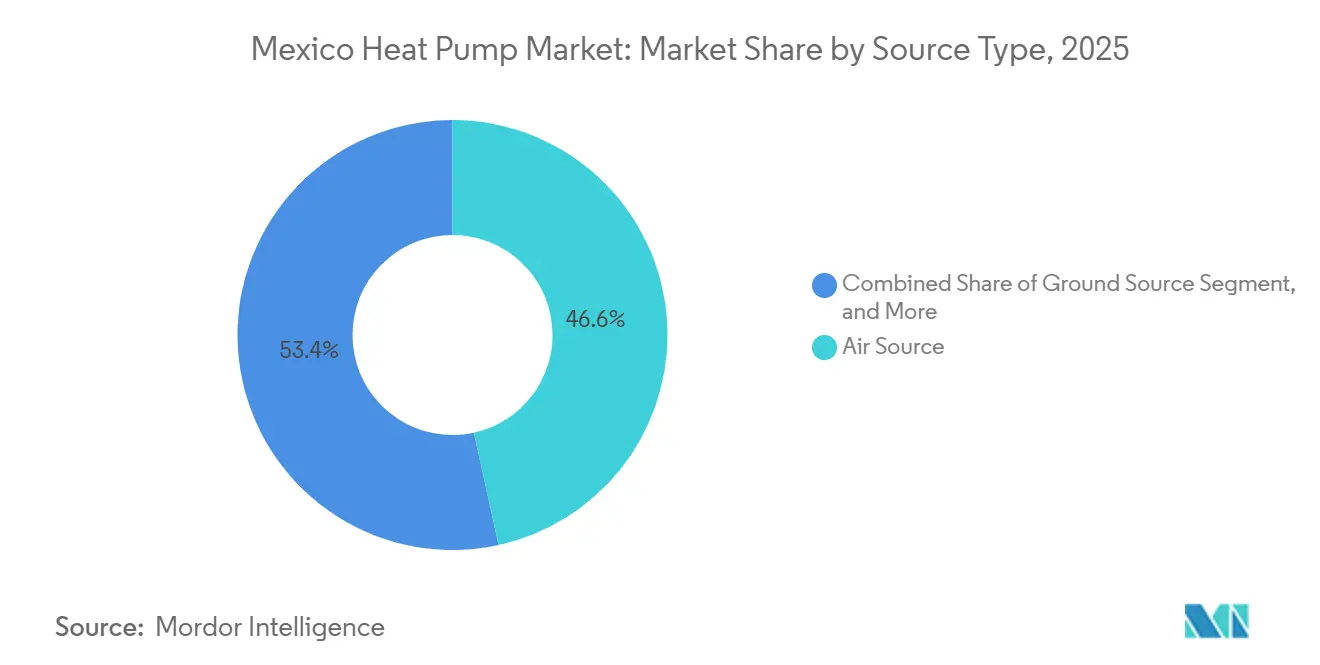

- By source type, air source systems led with 46.57% of Mexico heat pump market share in 2025, while hybrid configurations are forecast to expand at a 6.18% CAGR to 2031.

- By technology, air-to-air units held 52.03% share in 2025, whereas ground-to-water solutions are projected to grow at a 5.93% CAGR through 2031.

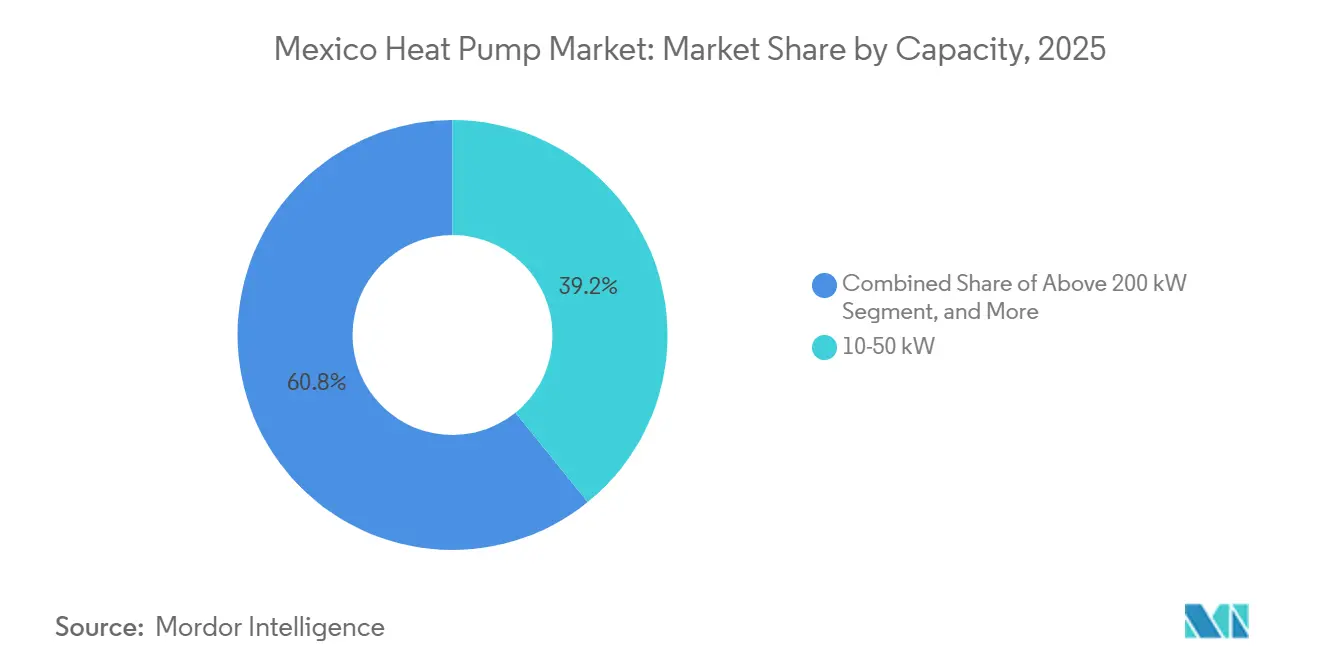

- By capacity, the 10–50 kW band accounted for 39.16% share in 2025, yet units above 200 kW are expected to post the fastest 5.57% CAGR to 2031.

- By application, space cooling commanded 43.82% share in 2025; industrial and process heating is positioned to expand at a 5.82% CAGR over the same horizon.

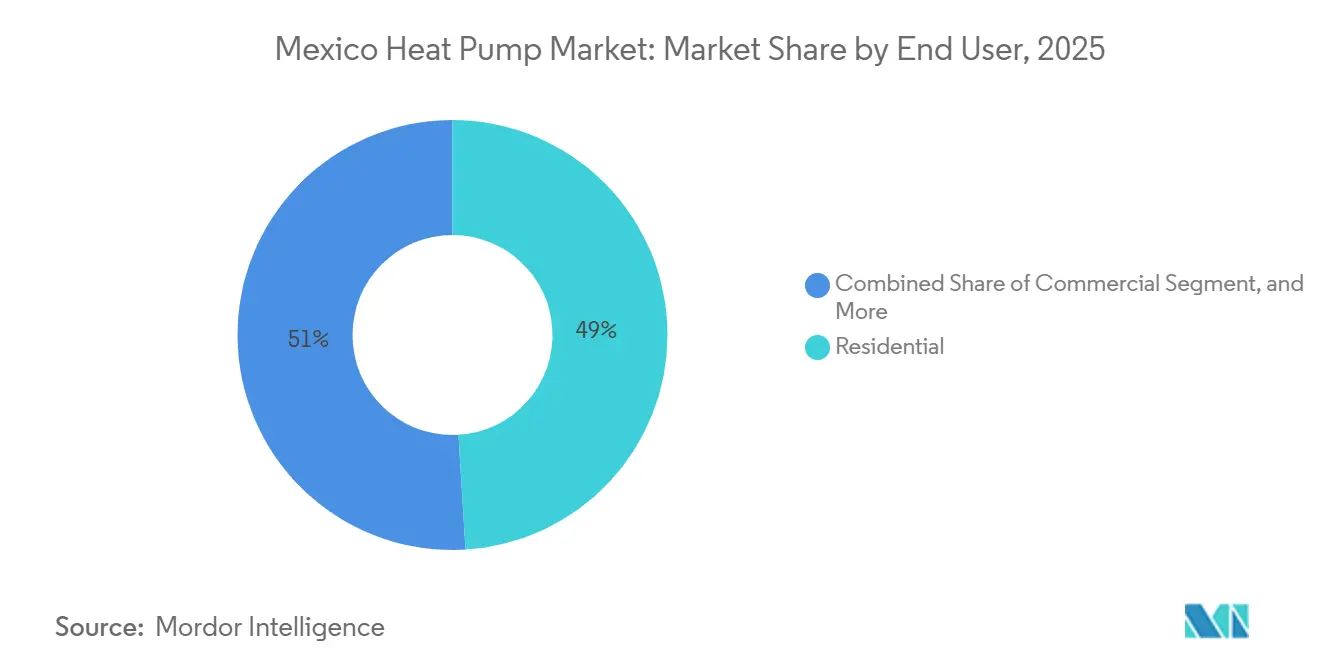

- By end user, residential installations captured 49.04% share in 2025, while commercial deployments are projected to rise at a 5.28% CAGR through 2031.

- By installation type, retrofit projects dominated with 61.43% share in 2025, whereas new-construction installations are set to increase at a 5.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cooling-Degree Days Increasing Demand for Reversible Systems | +1.2% | National, highest in Tabasco, Chiapas, northern Plateau | Medium term (2-4 years) |

| Government Incentives and Rebates for Electrification of Space Heating | +0.8% | National, federal programs and selective state pilots | Short term (≤2 years) |

| Phase-Out Timelines for Fossil-Fuel Boilers and Furnaces | +0.7% | National, aligned with Kigali HFC phase-down | Long term (≥4 years) |

| Stringent Building Energy-Efficiency Codes in Mexico | +0.6% | National, early enforcement in Mexico City, Monterrey, Guadalajara | Medium term (2-4 years) |

| Rapid Efficiency Gains in Inverter Compressors and Low-GWP Refrigerants | +0.5% | Global standards adopted via NOM alignment | Medium term (2-4 years) |

| Surge in Rooftop Solar PV Enabling Hybrid Heat Pump-PV Self-Consumption | +0.4% | National, strongest in high-irradiance northern and central states | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Cooling-Degree Days Increasing Demand for Reversible Systems

Mexico’s mean temperature climbed 1.6 °C between 2001 and 2024, and cooling-degree days are projected to increase up to 86% by the 2080s, while heating-degree days decline sharply. This climatic shift is most pronounced in Chihuahua, Tabasco, and Chiapas, where urban heat islands add as much as 6 °C to nighttime temperatures, transforming cooling from a seasonal need to a year-round baseline. Building owners therefore favor reversible air-source units that can satisfy both loads and qualify for higher efficiency rebates.[1]World Bank, “Climate Change Knowledge Portal: Mexico,” climateknowledgeportal.worldbank.org Industrial corridors adopting 24-hour production schedules find that inverter-driven heat pumps modulate capacity during extreme events, maintaining process stability. As a result, the Mexico heat pump market is benefiting from climate adaptation budgets rather than discretionary HVAC spending. The trend is expected to intensify once updated weather files are incorporated into building-energy models that underpin loan covenants and insurance underwriting.

Government Incentives and Rebates for Electrification of Space Heating

In December 2025 the National Commission for the Efficient Use of Energy earmarked dedicated efficiency funds, while the May 2025 Energy Planning and Transition Law authorized certificates that defray up-front costs in public buildings.[2]Comisión Nacional para el Uso Eficiente de la Energía, "Energy Planning and Transition Law," conuee.gob.mx Though smaller than programs in the United States, these federal grants mandate heat pumps in facilities larger than 800 m², creating predictable order flow for commercial installers. State pilots in Nuevo León and Jalisco add on-bill financing that shortens payback for mid-size offices. Limited consumer rebates keep residential volumes muted, but developers of social housing leverage bulk procurement to secure unit prices 9% below retail averages. The incentive landscape therefore tilts demand toward institutional and commercial buyers that can navigate the paperwork and aggregate projects.

Phase-Out Timelines for Fossil-Fuel Boilers and Furnaces

Mexico’s Kigali roadmap freezes hydrofluorocarbon consumption by 2024 and phases out high-GWP refrigerants by 2030, pushing manufacturers to R32 and R454B lines.[3]Energy and Commerce, “SENER Publica Nuevas Normas de Eficiencia Energética,” energyandcommerce.com.mx Parallel clean-electricity targets raise renewable penetration to 45% by 2030, reducing grid-emissions intensity. These policies erode the lifecycle cost advantage of gas boilers, especially for hotels and food processors that can capture waste heat. Grupo Solmar’s Los Cabos properties already cut LPG use by 50%, underscoring real-world savings. As carbon-pricing pilots expand, fossil systems face rising compliance costs, accelerating the pivot toward high-temperature heat pumps in industrial campuses.

Stringent Building Energy-Efficiency Codes in Mexico

NOM-035-ENER-2025 lifts the minimum integrated energy-efficiency ratio for rooftop units above 19.05 kW, with enforcement from February 2027.[4]Comisión Nacional para el Uso Eficiente de la Energía, “NORMA Oficial Mexicana NOM-035-ENER-2025,” diariooficial.gob.mx NOM-011-ENER-2025 similarly tightens seasonal efficiency for reversible ducted systems. Designers are responding by specifying variable-speed compressors, microchannel heat exchangers, and advanced controls to comply without oversizing. Early adopters in Mexico City’s premium office towers report 11% lower annual energy bills after switching to compliant equipment. As codes cascade to secondary cities, compliance deadlines will bring a replacement surge that sustains the Mexico heat pump market through the late-2020s upgrade cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Equipment and Installation Costs | -0.9% | National, acute in residential and small-commercial | Short term (≤2 years) |

| Cultural Preference for LPG and Natural Gas Heating Appliances | -0.7% | National, strongest in central and northern homes | Long term (≥4 years) |

| Limited Pool of Trained Installers and After-Sales Technicians | -0.6% | Secondary cities and rural areas | Medium term (2-4 years) |

| Electrical Grid Capacity Constraints in Peak-Load Zones | -0.5% | Yucatán Peninsula, Baja California Sur, summer peaks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Equipment and Installation Costs

Residential minisplit heat pumps remain 18% to 25% more expensive than comparable cooling-only units, and many homes require electrical-panel upgrades that add USD 1,000-3,000 per project. Financing options are limited, and interest rates above 12% negate much of the operating-cost advantage. Subsidized LPG caps shield households from full fuel costs, elongating payback periods. Consequently, many buyers in the Mexico heat pump market defer replacement until existing units fail, dampening near-term volumes. Bulk procurement by developers offers partial relief but does not yet reach the fragmented self-build sector.

Cultural Preference for LPG and Natural Gas Heating Appliances

Decades of subsidized fossil-fuel supply have entrenched gas heaters as the default choice in central and northern states. Even after commercial LPG caps were lifted in 2026, residential users still enjoy price ceilings that cushion monthly bills.[5]Comisión Nacional de Energía, “Commercial LPG Price Cap Removal,” cne.gob.mx Tenant-landlord splits further discourage electrification in multi-family properties, where owners do not recover energy savings. Installer familiarity tilts recommendations toward legacy equipment, and consumer perception of heat pumps as “cool-climate” technology persists. Overcoming this inertia will require sustained public-awareness campaigns and a larger pool of technicians trained in low-GWP refrigerant handling, objectives now addressed only in pilot form.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Leads, Hybrid Configurations Accelerate

Air source systems captured 46.57% of Mexico heat pump market share in 2025, maintaining the largest slice of demand thanks to straightforward rooftop or split-unit installations that fit legacy ductwork. Hybrid designs combining air-source equipment with auxiliary electric resistance strips or gas furnaces are forecast to advance at a 6.18% CAGR through 2031, giving the Mexico heat pump market new momentum among hotels and supermarkets that prize redundancy during grid disruptions. Daikin’s R32-based rooftop platform, assembled in San Luis Potosí, highlights how local production slashes freight costs and keeps price premiums below 12% over cooling-only models.[6]Daikin Latin America, “Daikin Inaugura Campus en San Luis Potosí,” daikin-latinoamerica.com Many industrial buyers still favor air source units in mild coastal climates because ambient temperatures rarely fall below 10 °C, letting systems hold seasonal coefficients of performance above 3.5.

Hybrid adoption is further buoyed by the 39% compound annual expansion of distributed solar, which widens the economic gap between inverter heat pumps and constant-speed chillers. Shifting utility tariffs that reward demand-response capacity add another revenue stream, prompting cold-storage warehouses to specify hybrids that stage electric resistance coils only during curtailment calls. Water source and ground source options remain niche, yet resorts with seawater intake rights or geothermal leases have issued tenders for 5-10 MW central plants, hinting at a future diversification of the Mexico heat pump market.

By Technology: Air-to-Air Dominates, Ground-to-Water Rises

Air-to-air units held 52.03% of 2025 demand, reflecting their popularity in single-family retrofits and strip-mall tenant improvements that require no hydronic loops. Ground-to-water systems are on course for a 5.93% CAGR through 2031, and early adopters in food processing have documented process-steam savings that shorten payback to six years. Air-to-water variants gain traction in high-rise condominiums where domestic hot-water loads are significant, while mixed-use campuses deploy them in tandem with thermal-storage tanks to flatten peak power draws.

Cold-climate algorithm upgrades have improved frost defrost cycles by 15%, making air-to-air viable in Chihuahua’s winter nights when temperatures occasionally dip to -5 °C. Nevertheless, breweries and textile mills continue to prefer ground-to-water units for 24-hour operations because soil temperatures stay within a narrow band, ensuring steady coefficients of performance. As inverter compressors and plate heat exchangers reach mass scale, pricing for entry-level ground-to-water kits is projected to fall 8% between 2026 and 2028, further enlarging the addressable slice of the Mexico heat pump market.

By Capacity: Mid-Range Largest, High-Capacity Fastest

Systems rated 10–50 kW accounted for 39.16% of Mexico heat pump market size in 2025, aligning with strip malls, clinics, and multifamily towers that dominate new building permits. Equipment above 200 kW is forecast to climb at a 5.57% CAGR, led by data centers in Querétaro and manufacturing campuses in Nuevo León that must decarbonize process cooling. Daikin’s planned centrifugal-chiller line, capable of 400 units a year, directly targets this tier and will supply both domestic and export orders under United States-Mexico-Canada Agreement content rules.

Installation cost advantages explain the mid-range dominance: contractors routinely split 40 kW rooftop packages into two 20 kW stages, simplifying crane logistics and preserving redundancy. Large units, in contrast, need structural steel upgrades and harmonic filters, adding 9% to 14% to installed cost. Even so, hospitals that run sterilization autoclaves 24x7 consider the lifecycle savings compelling, and the Mexico heat pump industry reports order backlogs of more than eight months for 250 kW and above machines.

By Application: Cooling Prevails, Industrial Heating Accelerates

Space cooling generated 43.82% of 2025 turnover, reflecting Mexico’s long cooling seasons and the marketing focus of minisplit distributors. Industrial and process heating is projected to expand at a 5.82% CAGR through 2031, reshaping the Mexico heat pump market as breweries, dairies, and textile dyeing plants electrify steam generation up to 90 °C. Grupo Solmar’s 50% liquefied-petroleum-gas cut in Los Cabos hotels remains the most-quoted reference project, proving that heat-recovery chillers can pay for themselves in under four years.

Domestic hot-water supply in coastal resorts is another bright spot because occupancy stays high year-round, yielding load factors above 4,000 hours. In commercial offices, dual-purpose systems now integrate with building-management software that pre-cools at midday solar peaks, raising self-consumption of rooftop arrays to 42%. Consequently, process-heating share of the Mexico heat pump market could soon overtake space heating, even though absolute cooling tonnage will keep leading unit counts.

By End User: Residential Still Biggest, Commercial Gains the Lead in Growth

The residential channel delivered 49.04% of 2025 shipments but is growing more slowly than commercial and institutional segments. Retail chains and logistics parks are committing to net-zero targets that require phasing out gas-fired packaged units, thus pushing the Mexico heat pump market toward centralized plant rooms with digital twins for predictive maintenance. Samsung’s Nuevo León training academy is already graduating 300 technicians a year, alleviating the skills bottleneck that once deterred electronics retailers from stocking high-end variable-refrigerant-flow models.[7]Samsung Electronics, “Samsung Opens HVAC Training Center in Nuevo León,” samsung.com

High-rise developers in Mexico City advertise “gas-free” amenities to differentiate units, and on-bill financing pilots in Jalisco have reduced upfront pain points for office landlords. Industrial users remain cautious, citing downtime risk during hydraulic interface retrofits, yet positive outcomes at pulp-and-paper mills in Veracruz signal a turning point. As blended-power tariffs add time-of-use surcharges for weekday evenings, commercial buyers will likely surpass homeowners in incremental volume from 2027 onward.

By Installation: Retrofit Dominates, New-Build Momentum Builds

Retrofit activity represented 61.43% of 2025 installs, as aging R410A rooftop units approach obsolescence ahead of the 2027 NOM-035 compliance deadline. New construction is poised for a 5.46% CAGR, because updated zoning codes in Mexico City require seasonal energy-efficiency ratios that most cooling-only chillers cannot meet. Builders therefore specify reversible units from the outset, allowing duct layout and electrical risers to be optimized around higher starting amperage, reducing future change-order risk.

Existing-building retrofits benefit from utility rebates that cover up to 20% of compressor costs if energy savings are independently measured. Where electric-service upgrades prove necessary, small-business owners often coordinate with solar installers to add 25-100 kW rooftop arrays, bundling permits under the streamlined 0.7 MW rule. This turnkey model, already well established in Monterrey, is spreading to Puebla and León, broadening the geographical footprint of the Mexico heat pump market.

Geography Analysis

Northern and central states together generated an estimated 57% of Mexico heat pump market revenue in 2025, and their combined demand is advancing at a projected 5.4% CAGR to 2031. Nuevo León, Chihuahua, and Sonora experience both winter heating-degree and summer cooling-degree requirements, making reversible systems the logical one-device solution. Manufacturers anchor production in the Bajío corridor, leveraging proximity to automotive supply chains and to the United States Interstate rail crossings that streamline component imports.[8]Comisión Federal de Electricidad, “Transmission and Distribution Investment Plan 2025-2030,” cfe.gob.mx

The Yucatán Peninsula holds just 7% of 2025 shipments but remains the headline risk zone because peak demand exceeds local generation by roughly 600 MW. Frequent load-shedding has pushed hotel operators in Cancún and Mérida to pair 200-500 kW air-to-water units with battery storage, an arrangement that raises installed cost yet maintains air quality during blackouts. Baja California Sur shows the fastest regional growth, albeit from a small base, because elevated LPG delivery charges tilt lifecycle economics in favor of 20-60 kW air-to-water packages that serve boutique resorts off the main grid.

Mexico City, Guadalajara, and Querétaro together commanded 28% of Mexico heat pump market size in 2025, driven by corporate campuses, data centers, and medical complexes. Upcoming FIFA-related infrastructure deadlines have accelerated chiller upgrades in stadiums and training facilities, a move that sets durable benchmarks for future public-private tenders. Solar irradiance in these high-altitude basins averages 5.4 kWh kWp⁻¹ day⁻¹, letting hybrid installations reach seasonal performance factors above 5.2 and trimming project payback by nine months compared with stand-alone units.[9]Emmi, “Autoconsumo Fotovoltaico con Baterías,” emmi.mx

Competitive Landscape

The Mexico heat pump market features a cluster of global incumbents, Daikin, Bosch, Carrier, Mitsubishi Electric, LG, Samsung, and Danfoss, supplemented by Chinese brands that focus on entry-level minisplits. Combined, the top five suppliers controlled roughly 63% of 2025 shipments, indicating moderate concentration with ample room for challenger offerings. Localization plays dominate investment headlines: Daikin’s San Luis Potosí campus now hosts inverter-compressor R and D and will produce 400 water-cooled centrifugal chillers a year from 2026, while Danfoss doubled Monterrey capacity for scroll compressors and microchannel coils.

Strategic partnerships center on renewable integration and refrigerant transition. Bosch’s 2024 acquisition of Johnson Controls’ HVAC arm created a vertical stack from residential split systems to York centrifugal chillers, all of which migrate to R454B by 2027 to stay ahead of Kigali timelines. Samsung invests in technician upskilling to ease installer aversion to R32 charging protocols, whereas Carrier co-markets rooftop heat-pump-photovoltaic bundles with three solar developers to guarantee building owners a blended payback under six years. Software differentiation now matters as much as hardware, so suppliers embed IoT gateways that feed machine-learning platforms for predictive maintenance, slashing unscheduled outages by up to 30%.

Local assemblers attempt to win public-procurement lots on price, but stringent NOM-035 performance thresholds and two-year spare-parts availability clauses tend to favor multinationals with certified labs. Still, disruptive entrants are exploring heat-as-a-service contracts under which they fund equipment and recover costs through monthly fees indexed to verified energy savings, an approach that could thin the capital barrier for small commercial buyers. If industry consolidation proceeds as forecast, the Mexico heat pump industry may settle into an oligopoly of six or seven dominant vendors by 2031, each operating at scale across Latin America and South America export corridors.

Mexico Heat Pump Industry Leaders

-

Daikin Industries Ltd.

-

Mitsubishi Electric Corporation

-

Carrier Corporation

-

Panasonic Corporation

-

Samsung Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Comisión Nacional de Energía finalized regulations for a 12.5 MW binary-cycle geothermal plant in Guanajuato, opening a pathway for shallow-loop direct-use demonstrations.

- January 2026: Federal authorities removed commercial LPG price caps while retaining residential ceilings, realigning fuel-switching economics for hotels, hospitals, and factories.

- January 2026: Secretaría de Energía published hydrochlorofluorocarbon limits for 2026-2030, accelerating the refrigerant pivot toward R32 and R454B.

- November 2025: Danfoss completed a USD 100 million capacity-doubling project in Monterrey, adding sensor and compressor lines with 300 new jobs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Mexico heat pump market as the annual value of factory-built air-source, water-source, ground-source, hybrid, and exhaust-air heat pump systems rated below 100 kW that are installed for space conditioning or sanitary hot-water duties in residential, commercial, industrial, and institutional buildings. The valuation tracks equipment revenue only; service, rental, and spare-parts streams remain outside the scope.

Scope exclusion: mobile refrigeration and vehicle cabin heat pumps are not counted.

Segmentation Overview

-

By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

-

By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

-

By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

-

By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

-

By End User

- Residential

- Commercial

- Industrial

-

By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured calls with Mexican OEM managers, Guadalajara-based distributors, Baja installers, housing developers, and energy-policy advisors. These interactions clarified typical installed prices, subsidy uptake, and regional mix shifts, helping us reconcile secondary numbers and fine-tune penetration assumptions.

Desk Research

We begin by mapping the addressable stock using open datasets such as INEGI housing and commercial floor-space surveys, Secretaría de Energía (SENER) appliance-efficiency registers, customs import codes from UN Comtrade, and tariff schedules published by Comisión Federal de Electricidad. Policy context comes from NOM-020/023 building codes and CONAVI "Hipoteca Verde" subsidy guidelines, while climate fingerprints draw on Servicio Meteorológico Nacional weather files. Company financials and shipment clues are extracted from D&B Hoovers and Dow Jones Factiva news archives. The sources cited above illustrate the breadth; many additional public and paid repositories were reviewed before figures were locked in.

Market-Sizing & Forecasting

A top-down stock-turn model converts dwelling counts, new-build completions, and retrofit rates into annual demand, which is then multiplied by weighted average selling prices. Bottom-up cross-checks, import volume multiplied by declared CIF value and sampled local assembly output, flag any material gaps before totals are finalized. Key variables feeding the model include cooling-degree-day trend, CFE tariff differentials, heat-pump share of HVAC permits, refrigerant phase-down timelines, and average mortgage interest rates. A multivariate regression, stress-tested via scenario analysis, projects these drivers through 2030; outliers are returned to experts for validation.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, peer analyst challenge, and research-manager sign-off. We refresh every twelve months or sooner if subsidy budgets, currency swings, or major factory openings alter baseline conditions; a quick update is run again just before report delivery.

Why Mordor's Mexico Heat Pump Baseline Earns Trust

Published values often diverge because firms pick different product mixes, price bases, or refresh cadences, and because Mexico's import-heavy supply chain obscures true local shipments.

Key gap drivers include narrower technology scope, use of list rather than net prices, and extrapolations from regional instead of country-level housing data, which can inflate or deflate totals against our evidence-backed base year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.03 billion (2025) | Mordor Intelligence | - |

| USD 476 million (2024) | Regional Consultancy A | Omits ground-source and hybrid units; applies ex-factory prices only |

| USD 963 million (2024) | Industry Database B | Relies on import value without adjusting for local assembly or dealer margins |

The comparison shows that once consistent scope, price netting, and assembly adjustments are applied, Mordor's balanced figure becomes a dependable anchor for strategic planning.

Key Questions Answered in the Report

How large is the Mexico heat pump market today?

It was valued at USD 1.08 billion in 2026 and is projected to reach USD 1.38 billion by 2031 at a 5.02% CAGR.

Which capacity range sells the most units?

Systems between 10 kW and 50 kW account for 39.16% of 2025 shipments because they match the loads of strip malls and multifamily buildings.

What segment is growing fastest?

Units above 200 kW show the highest 5.57% CAGR forecast, fueled by data centers, hospitals, and industrial plants electrifying process loads.

How are new regulations affecting product design?

NOM-035-ENER-2025 and NOM-011-ENER-2025 raise minimum efficiency ratios, so manufacturers are adding inverter compressors and low-GWP refrigerants.

Why are hybrid PV-heat-pump systems popular?

Rapid rooftop solar adoption and simplified 0.7 MW permitting allow building owners to offset operating costs and secure faster payback.

Are installation skills improving?

Yes, manufacturer-led academies in Nuevo León and Jalisco now certify hundreds of technicians annually, closing the talent gap for R32 and R454B systems.

Page last updated on: