Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

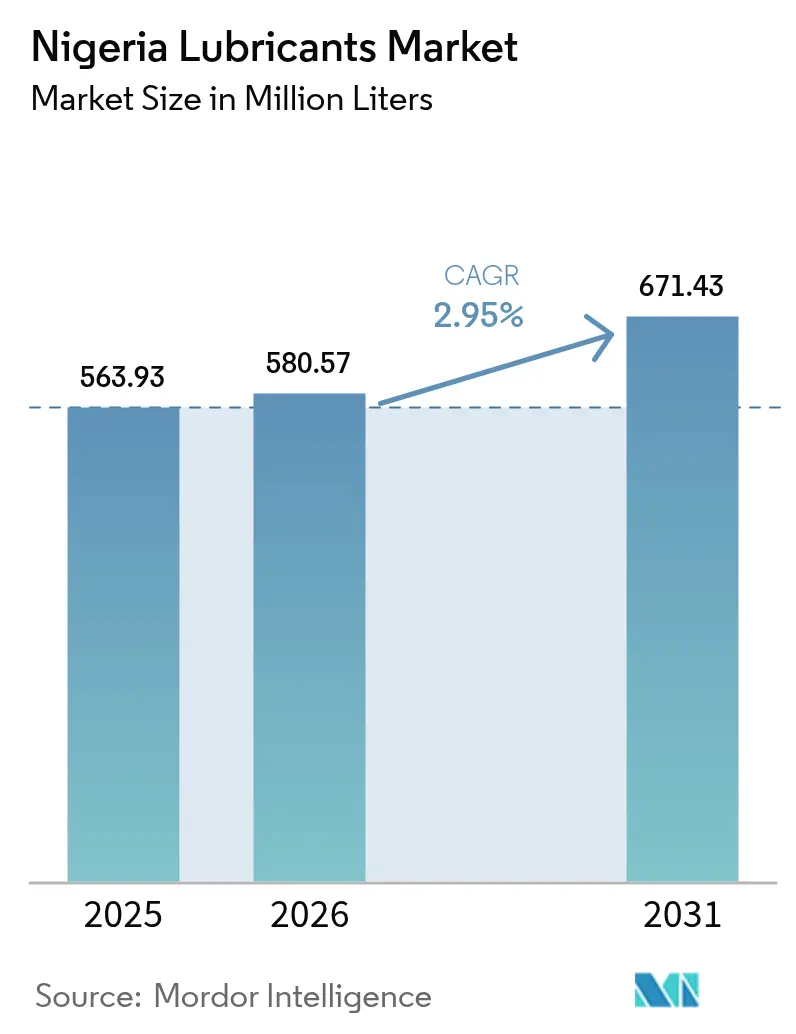

| Base Year Market Size (2025) | 563.93 Million Liters |

| Market Volume (2026) | 580.57 Million Liters |

| Market Volume (2031) | 671.43 Million Liters |

| Growth Rate (2026 - 2031) | 2.95% CAGR |

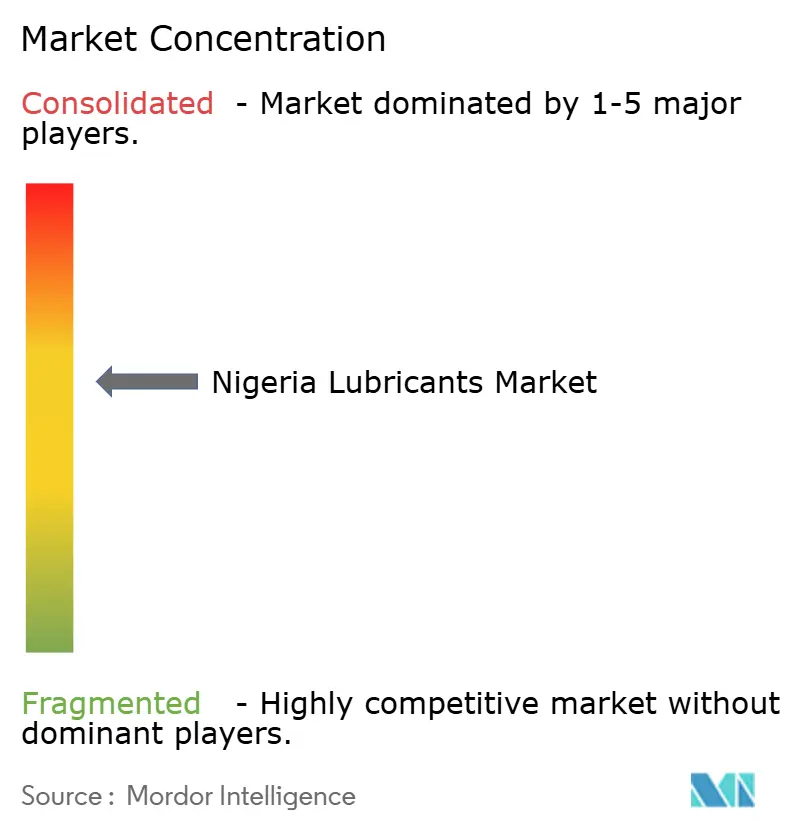

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Lubricants Market Analysis by Mordor Intelligence

Nigeria Lubricants Market size in 2026 is estimated at 580.57 Million Liters, growing from 2025 value of 563.93 Million Liters with 2031 projections showing 671.43 Million Liters, growing at 2.95% CAGR over 2026-2031. Current growth reflects a blend of vehicle-driven demand, widening industrial use, and a gradual pivot toward synthetic formulations that promise extended drain intervals and fuel-saving properties. Consumer preference keeps mineral oils firmly in the lead, yet sales of synthetic and semi-synthetic grades are rising in Lagos, Ogun, and Abuja as vehicle fleets modernize. Exchange-rate volatility remains the biggest margin risk, as nearly all base oils are imported. Meanwhile, tightening federal quality controls curbs counterfeit volumes and supports legitimate suppliers. New e-commerce channels, led by platforms such as Petro Powers, shorten distribution chains, reduce inventory costs, and provide lubricant makers with direct insight into customer buying patterns.

Key Report Takeaways

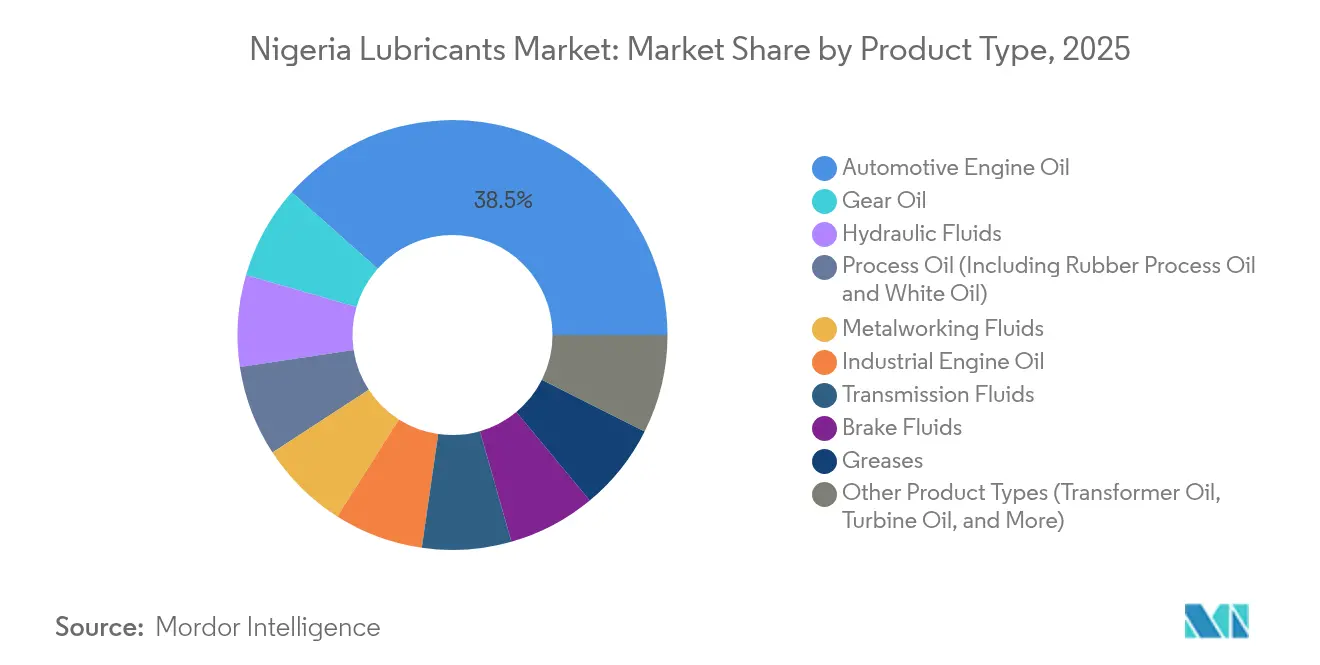

- By product type, automotive engine oil accounted for 38.45% of the market share in 2025. The market size of gear oils is expected to increase with a CAGR of 4.36% during the forecast period (2026-2031).

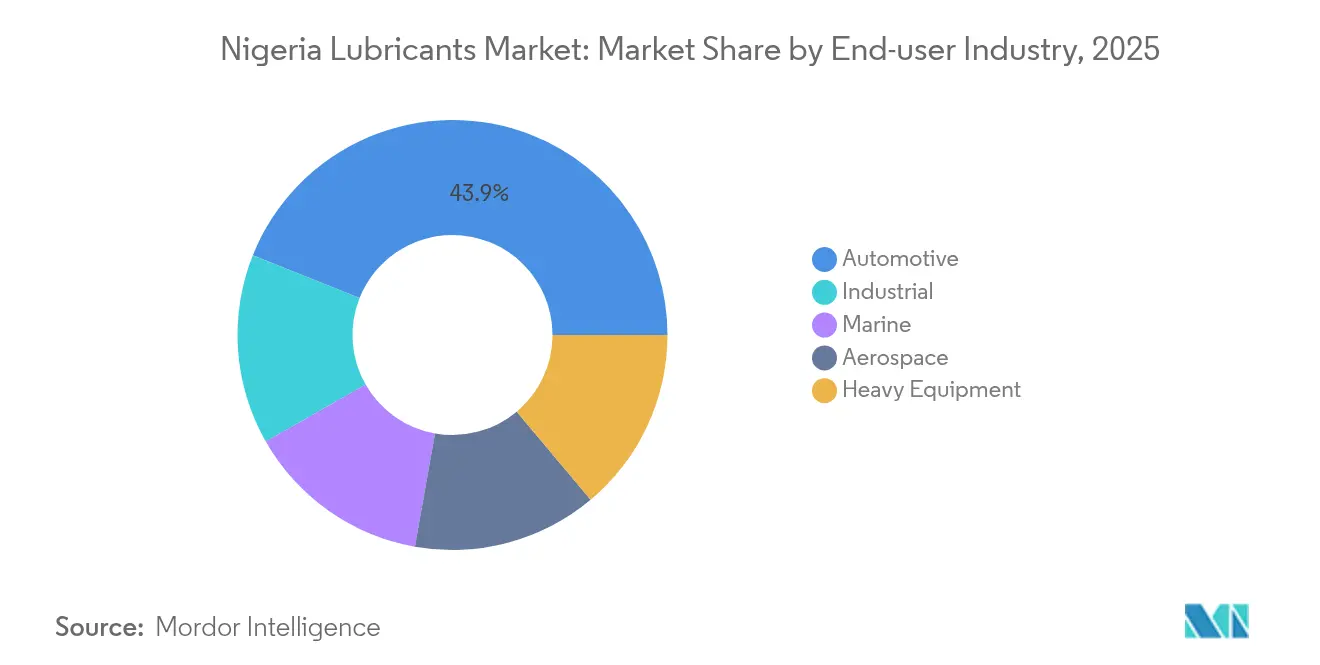

- By end-user industry, the automotive sector held a 43.95% market share in 2025, and during the forecast period (2026-2031), the industrial sector's share is expected to increase at a CAGR of 5.09%.

- By base stock type, the market share of the mineral oil-based lubricants was 75.95% in 2025 and the share of synthetic lubricants is expected to increase with a CAGR of 4% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for synthetic and semi-synthetic lubricants | +0.8% | Lagos-Ogun-Ibadan corridor and other urban centers | Medium term (2-4 years) |

| Rapid expansion of Nigeria's used-vehicle fleet | +0.6% | Lagos, Kano, Port Harcourt | Short term (≤ 2 years) |

| Growth in Lagos-Ogun industrial corridor | +0.4% | Southwest Nigeria | Long term (≥ 4 years) |

| Digitalisation of lubricant retail channels | +0.3% | Lagos, Abuja, Port Harcourt, Kano | Medium term (2-4 years) |

| Federal auto-assembly incentives for OEM-approved lubes | +0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Synthetic and Semi-Synthetic Lubricants

Synthetic grades are expanding as fleet operators weigh extended drain intervals against upfront price premiums. Sales of premium products climb fastest where turbocharged and hybrid vehicles enter the parc under OEM assembly programs in Lagos and Kaduna. TotalEnergies notes a nationwide upswing in Quartz branded synthetics, while Shell’s Helix Ultra is now standard across several logistics fleets that target lower service downtime[1]TotalEnergies Marketing Nigeria Plc, “Quartz Synthetic Oil Uptake Report 2025,” totalenergies.com. Local blenders, notably MRS Oil and Ardova, have retrofitted plants to incorporate Group III base stocks and stricter additive chemistries that meet API SP and ACEA C6 specs, reinforcing the move to higher-quality formulations.

Rapid Expansion of Nigeria's Used-Vehicle Fleet

Used-vehicle imports feed aftermarket demand because older engines require more frequent oil changes. National policies project 11.8 million registered vehicles by 2030, with commercial transport making up 56% and consuming 3–4 times more oil than private cars. Registration data shows the heaviest concentrations in Lagos, Kano, and Rivers, turning these states into high-volume hubs for multi-grade diesel and gasoline engine oils.

Growth in Lagos-Ogun Industrial Corridor

This corridor contributes over 60% of manufacturing output, spurring purchases of hydraulic fluids, metal-working oils, and turbine oils. Power-plant expansion, led by gas-fired projects, raises demand for high-temperature turbine lubricants that protect against varnish and deposit formation. Easy port access lowers inbound freight costs for base oils, supporting competitive pricing for industrial users.

Digitalisation of Lubricant Retail Channels

Online platforms connect blenders directly to mechanics and end-users, shrinking traditional mark-ups. In Lagos and Abuja, where internet coverage exceeds 70%, Petro Powers offers same-day delivery of packaged lubricants, enabling small workshops to source genuine products with QR-code authentication. Suppliers gain real-time sales analytics for better demand forecasting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit/adulterated lubricant prevalence | -0.40% | National, concentrated in northern markets and border regions | Short term (≤ 2 years) |

| FX volatility and import-dependent base-oil costs | -0.60% | National, highest impact on import-dependent blenders | Short term (≤ 2 years) |

| Stringent waste-oil disposal regulation | -0.30% | National, with stricter enforcement in Lagos, Rivers, and FCT | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit/Adulterated Lubricant Prevalence

Substandard products undermine engine integrity and erode brand trust. The Standards Organisation of Nigeria confiscated NGN 20 billion worth of counterfeit goods in 2024, highlighting the scale of the challenge[2]Standards Organisation of Nigeria, “2024 Enforcement Results,” son.gov.ng. Smuggled stocks in border states retail at 30–40% discounts, drawing cost-sensitive buyers but causing premature engine failures that raise total ownership costs.

FX Volatility and Import-Dependent Base-Oil Costs

Nigeria imports nearly all its base oils, exposing blenders to dollar-denominated feedstock prices, which can be volatile. A 100% naira depreciation historically inflated domestic petroleum product costs by 136.7%, compressing margins for local blenders that cannot adjust pump prices quickly. Frequent price resets strain customer contracts and working capital cycles, particularly for SMEs in the Nigerian lubricants industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Drive Market Leadership

Automotive engine oils controlled 38.45% of sales in 2025, a dominance rooted in frequent service intervals and a hot climate that accelerates oil oxidation. Gear oils are projected to be the fastest-growing segment at a 4.36% CAGR, driven by the demand for heavy-duty trucks in the construction and mining industries. Process oils find demand in tire production, while metalworking fluids align with the expansion of auto-assembly plants. The Lagos-based manufacturing cluster boosts consumption of stamping oils and cutting fluids, while nationwide infrastructure projects sustain demand for hydraulic fluids. Brake fluids and greases register steadier growth as vehicle parc expansion underpins basic maintenance volumes.

The shift toward synthetic and semi-synthetic grades boosts the premium end of the product mix. Local blenders incorporate Group III imports to produce API SN-Plus and CK-4 oils, which offer longer drain intervals, thereby reducing downtime for fleet operators. Gearbox technologies in newer passenger vehicles also demand higher viscosity-index oils, reinforcing the shift to synthetics.

By End-User Industry: Automotive Dominance with Industrial Acceleration

The automotive sector accounted for 43.95% of 2025 demand, led by commercial transport fleets that log high annual mileage. Commercial vehicles consume 3–4 times more oil than private cars, resulting in high rotation of multi-grade diesel engine oil. Motorcycle taxis have pushed demand for small-engine two-stroke and four-stroke oils in urban centers. Industrial users, however, are forecast to register the highest 5.09% CAGR, tracking new power-generation and manufacturing investments in the Southwest.

Power plants switching from diesel to natural-gas turbines require premium turbine oils and long-life transformer fluids. The oil-and-gas upstream segment continues to require compressors and circulating oils, while marine lubricants support offshore supply vessels gathering at Lagos and Port Harcourt ports. A small but rising aerospace segment specifies high-temperature, low-volatility oils for turbine maintenance in Nigeria’s developing aviation hubs.

By Base Stock Type: Mineral Oils Lead with Synthetic Growth

Mineral oils held 75.95% of the Nigeria lubricants market in 2025, owing to lower retail prices and entrenched supply chains. Synthetic grades, though, are forecast to post a 4% CAGR as OEM approvals, fleet trials, and total cost of ownership gains become more widely recognized. Semi-synthetic blends appeal to commercial fleets that want longer drain intervals without incurring the full premiums of full synthetic oils. Emerging bio-based lubricants remain niche, but they benefit from stricter disposal rules under the National Environment Regulations 2023.

Synthetic adoption is concentrated in Lagos and Abuja, where new-car sales are highest and service networks offer access to genuine low-viscosity oils. Mineral-oil pricing fluctuates with base-oil imports; the Dangote Refinery’s eventual Group I and Group II output could reduce dependence on offshore supply and stabilize prices after 2027.

Geography Analysis

The Nigeria lubricants market is heavily weighted toward the Lagos-Ogun-Ibadan axis, which absorbed about 39.45% of national volumes in 2025. Lagos alone hosts over 2.1 million registered vehicles and most blending plants, providing rapid access to seaports that handle base-oil imports. The industrial estate density here generates steady orders for hydraulic, process, and metal-working fluids.

Kano, in the north, with 890,000 vehicles, serves as a distribution hub for neighboring states and Sahel markets. While high transport volumes favor sales, porous borders also heighten counterfeit penetration, depressing legitimate supplier margins. To counteract this, Chevron expanded its Texaco dealer network in 2024, adding 15 licensed outlets across the north to shore up brand presence and product authenticity.

Port Harcourt and Rivers State contribute a sizable industrial demand, anchored in oil and gas processing, refineries, and marine logistics. Marine lubricants gain from the ONNE port’s growing role as a bunkering hub after TotalEnergies’ USD 12 million Lubmarine upgrade in 2024. Abuja and its environs emerge as a growth pocket backed by government fleet renewals and infrastructure investment. New road and rail links, notably the Lagos-Ibadan expressway, will shift distribution economics and could dilute Lagos’ concentration advantage over the forecast period.

Competitive Landscape

The Nigeria lubricants market displays moderate concentration. International majors control premium tiers through exclusive distributor networks and comprehensive OEM-approval lists. Shell (via Ardova), TotalEnergies, ExxonMobil, and Chevron rely on their global R&D strength to supply factory-fill and service-fill oils that meet new engine specifications. Indigenous firms such as MRS Oil Nigeria, Conoil, and Oando integrate blending with downstream retail, capturing cost-sensitive consumers who favor mineral oils but still demand better quality verification. Exchange-rate risk remains the great equalizer; high-import content exposes both multinationals and locals to the same currency swings, keeping cost management central to competitive strategy.

Nigeria Lubricants Industry Leaders

Conoil PLC

Exxon Mobil Corporation (11 PLC)

MRS Oil Nigeria PLC

TotalEnergies

Shell plc (Ardova PLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CDN Oil & Lubricants announced a multibillion-naira plan to construct an ultra-modern lubricant blending plant in Anambra State to meet the demand in the country.

- May 2024: Eraskon reported 70% completion of its USD 50 million lubricant blending plant in Nigeria, which is expected to have a capacity of 64,000 liters per day.

Nigeria Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil & White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy & Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil & White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy & Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

What is the projected demand for lubricants in Nigeria by 2031?

Consumption is forecast to reach 671.43 million liters, growing at a 2.95% CAGR from 2026 to 2031.

Which product type currently dominates Nigerian sales?

Automotive engine oils lead the Nigeria lubricants market, holding 38.45% of 2025 volumes.

How fast are synthetic lubricants expanding?

Synthetic grades are expected to log a 4% CAGR, outpacing mineral oils due to OEM and fleet adoption.

Which end-user group is forecast to grow the quickest?

Industrial users, especially manufacturing and power plants, are set to expand at 5.09% CAGR through 2031.

What geographic corridor consumes the most lubricants?

The Lagos-Ogun-Ibadan region accounts for most of national demand thanks to its vehicle density and industrial base, absorbing about 39.45% of national volumes in 2025.

Page last updated on: