Angola Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

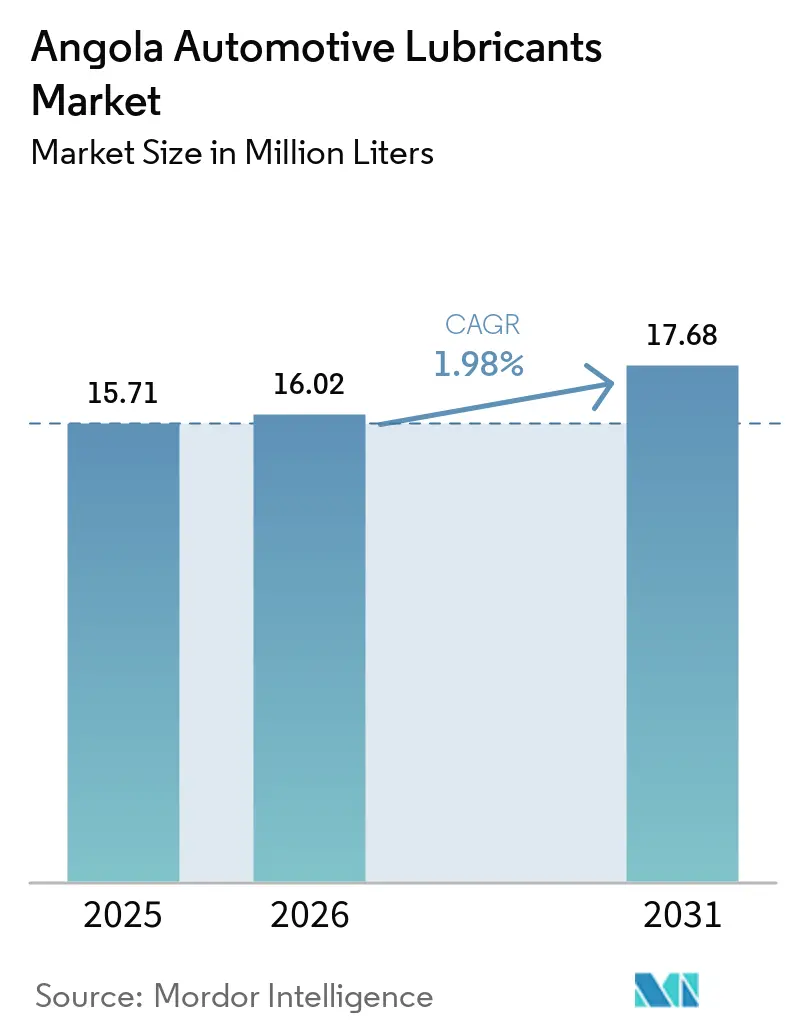

| Base Year Market Size (2025) | 15.71 Million liters |

| Market Volume (2026) | 16.02 Million liters |

| Market Volume (2031) | 17.68 Million liters |

| Growth Rate (2026 - 2031) | 1.98% CAGR |

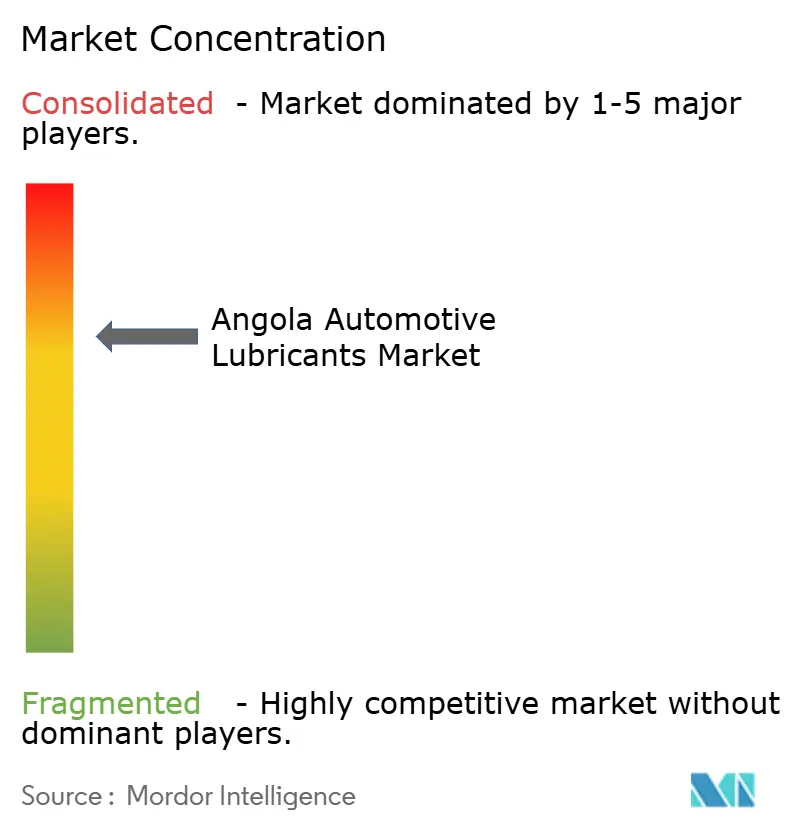

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Angola Automotive Lubricants Market Analysis by Mordor Intelligence

The Angola Automotive Lubricants Market size is expected to grow from 15.71 Million liters in 2025 to 16.02 Million liters in 2026 and is forecast to reach 17.68 Million liters by 2031 at 1.98% CAGR over 2026-2031. Structural expansion is unfolding behind these modest volume gains. Angola still imports nearly 80% of its refined-product needs, prompting the government to accelerate the development of three greenfield refineries, such as Cabinda, Soyo, and Lobito, to reduce foreign-exchange outflows and stabilize supply. Domestic blending currently meets less than 20% of lubricant demand. However, Sonangol anticipates nearly a five-fold increase in production once feedstock becomes available, positioning local brands to compete with imported premium products. Growing vehicle sales, an aging vehicle fleet, and increased mining activity are expanding the serviceable parc. However, challenges such as counterfeiting, foreign-exchange volatility, and longer OEM drain intervals are limiting annual consumption. The competitive environment remains intense, with international majors, regional fuel marketers, and local distributors competing for market share in an unregulated retail space affected by informal trade.

Key Report Takeaways

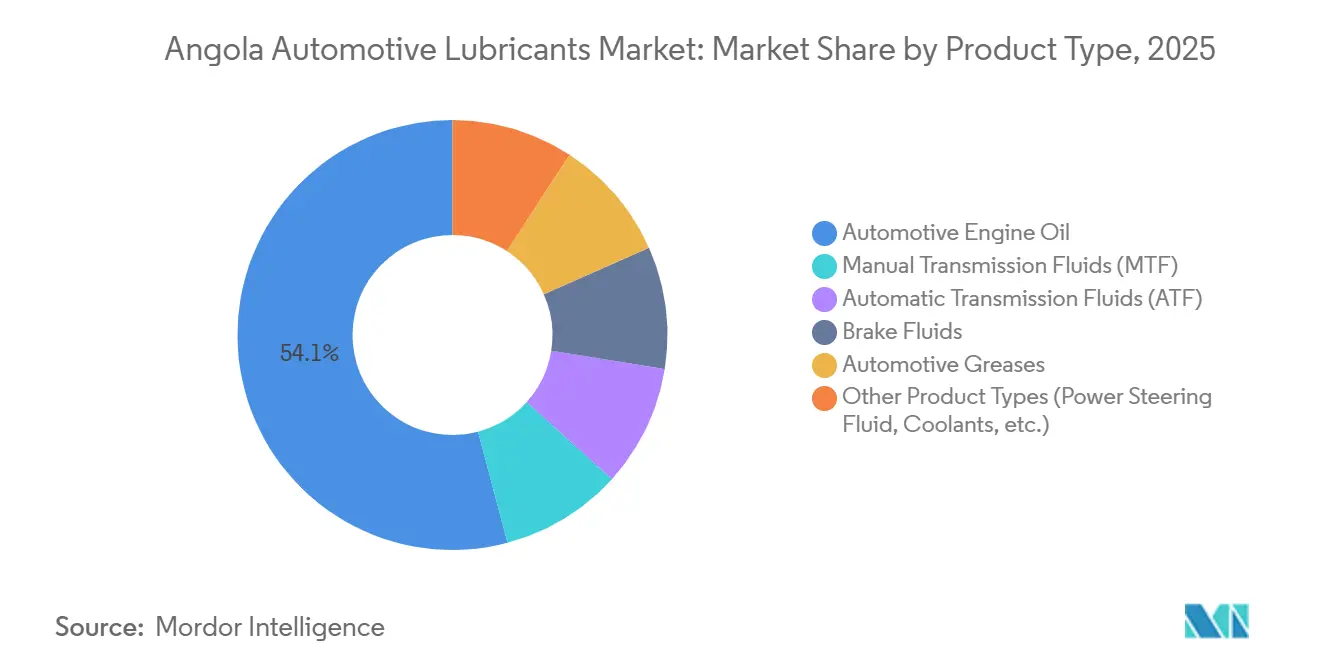

- By product type, automotive engine oil accounted for 54.12% of the Angola automotive lubricants market share in 2025, while brake fluids are forecast to expand at a 2.90% CAGR through 2031.

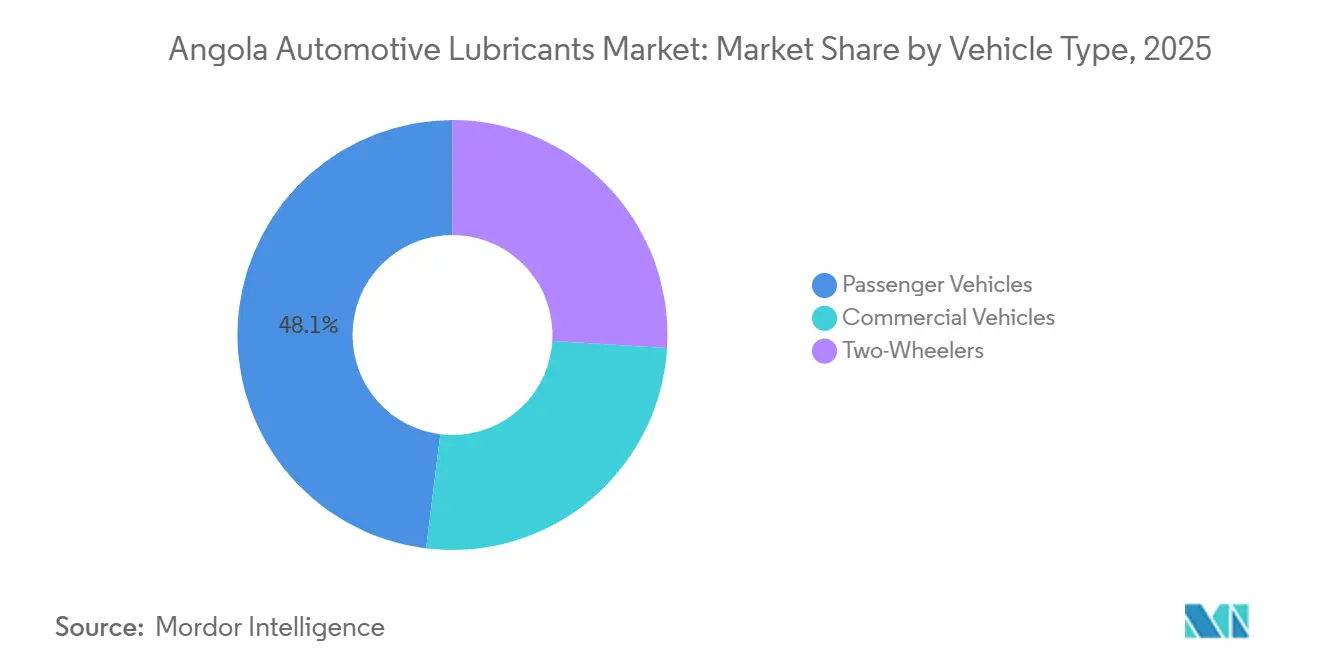

- By vehicle type, passenger vehicles held 48.06% of the Angola automotive lubricants market share in 2025 and are projected to grow at a 2.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Angola Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing average vehicle age | +0.5% | National, concentrated in Luanda and coastal provinces | Medium term (2–4 years) |

| Growth in used-vehicle imports and parc expansion | +0.6% | National, with early gains in Luanda, Benguela, Huíla | Short term (≤ 2 years) |

| Mining and construction equipment fleet growth | +0.4% | National, strongest in Lunda Norte, Lunda Sul, Benguela (Lobito corridor) | Long term (≥ 4 years) |

| Transition toward high-performance synthetic grades | +0.3% | National, led by Luanda and urban centers | Medium term (2–4 years) |

| OEM-backed extended-service contracts boosting branded lubricant uptake | +0.2% | National, concentrated in dealership networks (Luanda, Benguela) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Increasing Average Vehicle Age

Angola’s vehicle parc reached 989,000 units in 2019 and continues to grow as constrained household incomes delay vehicle replacement. The decline in new-car sales has resulted in older engines requiring more frequent top-ups and shorter oil change intervals, increasing per-vehicle lubricant demand even as overall fleet growth slows. Import restrictions limit incoming vehicles to relatively modern models, but a significant portion of the existing fleet still operates on legacy 20W-50 grades, broadening the product mix and sustaining high-volume mineral oil sales.

Growth in Used-Vehicle Imports and Parc Expansion

New-vehicle sales rebounded by 38% to 6,175 units in 2025, with Chinese brands Jetour, Chery, and Changan rapidly expanding their networks, while Suzuki alone accounted for 55% of registrations[1]Suzuki Motor Corporation, “2025 Angolan sales summary,” suzuki.co.jp. Each vehicle typically consumes 4 to 6 liters of engine oil per service and requires additional fluids such as Automatic Transmission Fluid (ATF) and coolants. App-based taxi fleets, which operate with extended daily mileage, reduce service intervals to 45-60 days, creating consistent aftermarket demand.

Mining and Construction Equipment Fleet Growth

Flagship mineral projects, including the USD 600 million Catoca Luele diamond mine and the USD 217 million Longonjo rare-earth project, are driving the mobilization of earth-moving equipment that requires high-viscosity heavy-duty oils, extreme-pressure greases, and hydraulic fluids. In March 2026, Rokbak appointed Trevotech as an authorized hauler dealer, offering fleet-service contracts that bundle lubricants with equipment packages.

Transition Toward High-Performance Synthetic Grades

Import age restrictions are keeping the incremental fleet relatively young, leading OEMs to recommend low-Sulfated Ash, Phosphorus, and Sulfur (SAPS) multigrades such as 5W-30 and 0W-20. Products like FUCHS TITAN SUPERSYN LONGLIFE 5W-40 and TotalEnergies FLUIDMATIC SYN T668, both carrying multiple global approvals, are now prominently displayed on dealership shelves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and low-quality lubricant proliferation | -0.4% | National, concentrated in informal retail channels (Luanda, provincial markets) | Short term (≤ 2 years) |

| Price sensitivity amplified by import tariffs and foreign-exchange volatility | -0.5% | National, acute in Luanda and import-dependent regions | Short term (≤ 2 years) |

| Longer OEM-mandated oil-drain intervals | -0.3% | National, led by dealership networks and modern fleet segments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Low-Quality Lubricant Proliferation

Authorities shut down an illicit blending operation in early 2026 that distributed counterfeit Castrol and Sonangol products across Angola and the DRC. Weak roadside testing and insufficient border controls continue to allow adulterated oils to undercut legitimate brands, eroding consumer trust and causing engine damage.

Price Sensitivity Amplified by Tariffs and Foreign-Exchange Volatility

A 9.1% depreciation of the kwanza against the USD in 2024 increased the landed costs of imported lubricants, which already face an average 10.9% tariff and 14% VAT. High retail prices have led consumers to delay oil changes or switch to unbranded, lower-cost products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automotive Engine Oil Dominates, Brake Fluids Outpace

Automotive engine oil accounted for 54.12% of Angola's automotive lubricants market share in 2025, highlighting its widespread application across various vehicle categories. Sub-grades such as 5W-XX and 10W-XX are increasingly replacing high-viscosity 15W-40 mineral blends as Original Equipment Manufacturers (OEMs) focus on stricter fuel economy standards. Brake fluids are expected to achieve the highest CAGR of 2.90% through 2031, driven by mandatory inspections that identify hydraulic issues requiring DOT 4 or DOT 4-Plus refills.

Manual and automatic transmission fluids are benefiting from the increasing adoption of automatic gearboxes in Chinese SUVs. Products like TotalEnergies FLUIDMATIC SYN T668 and Puma Synthetic ATF meet Allison TES 668 and Dexron IIIH standards, providing authorized options for warranty-related repairs. Greases continue to offer high margins; for example, Mobilgrease XHP 222 is priced at AOA 280,000 (USD 300) per 18 kg pail, catering to quarrying and logistics operators requiring water resistance under heavy loads.

By Vehicle Type: Passenger Cars Lead and Accelerate

Passenger vehicle represented 48.06% of Angola's automotive lubricants market size in 2025 and are projected to grow at a 2.72% CAGR, supported by app-based taxi fleets with high annual mileage. Light-duty pickups and heavy trucks consume larger sump volumes, but their growth potential is limited due to a decline in registrations, which fell to 750 units in 2019 before stabilizing at 127 heavy units in Q1 2025. Two-wheelers remain a niche segment in Angola, as the country lacks the motorcycle-taxi culture prevalent in West Africa, and import age caps set at three years further restrict volumes.

Commercial fleets, however, contribute significantly to lubricant consumption per vehicle. Lubex Africa supplies 210-liter drums of Mobil Delvac MX 15W-40 and Shell Rimula R4 X from its Cabinda depot to inland mining sites, leveraging a logistics advantage that smaller importers find challenging to replicate.

Geography Analysis

Luanda province controls close to 70% of imports and aftermarket outlets, making it the epicenter of Angola automotive lubricants market demand. However, Benguela, Lunda Norte, Lunda Sul, and Huíla are becoming increasingly important due to the expansion of mining and infrastructure projects. The Lobito corridor rail rehabilitation, supported by USD 1 billion in sovereign and multilateral funding, is expected to deploy numerous heavy machines reliant on premium hydraulic and gear oils.

Refining expansion is critical for future supply security. The 30,000 barrels per day (bpd) Cabinda refinery completed mechanical trials in March 2026, with phase two expected to double capacity by 2027. The Soyo (150,000 bpd) and Lobito (200,000 bpd) refineries remain underfunded, with only 2% and 10% completion, respectively. Sonangol’s USD 4.8 billion fundraising initiative aims to bridge this gap. If all projects proceed as scheduled, Angola could become a net exporter of base oil by 2029.

Provincial markets currently face challenges such as limited availability of branded products and high freight costs. Local blending presents a viable import-substitution strategy. Sonangol projects domestic lubricant production to increase from 8,850 metric tons (MT) in 2024 to 69,700 MT in 2026, potentially eliminating imports and reshaping pricing dynamics in neighboring markets such as the Democratic Republic of Congo (DRC) and Zambia. While execution risks remain significant, even partial success could reduce lead times and create private-label opportunities for regional distributors.

Competitive Landscape

The market exhibits moderate concentration, with top players including Shell, BP, Sonangol EP, Puma Energy, and TotalEnergies. The PETRONAS-Sinopec MoU signed in May 2024 hints at fresh competition through joint-venture blending or regional franchise models.

Majors differentiate through OEM endorsements and service-station networks. TotalEnergies is rolling out 50 retail sites that combine fuels, fleet cards, and lubricant bays, while Shell focuses on quick-lube partnerships inside Luanda’s shopping malls. Puma Energy courts mining fleets with Total Fluid Management contracts that promise contamination control and used-oil retrieval, claiming that USD 1,000 spent on preventive lubrication yields USD 40,000 in machine-life savings[2]Puma Energy Holdings, “Total Fluid Management Africa brochure,” pumaenergy.com.

Counterfeiting distorts price competition. A Luanda raid uncovered an illicit factory blending diesel, water, and thickeners into fake 20W-50, packaged in counterfeit Castrol drums and sold cross-border. Brand owners are responding with QR code authentication and tamper-evident seals, but police capacity remains thin. Regulatory reforms, Decreto Executivo 30/21 and 31/21, set quality standards, yet limited laboratory accreditation forces importers to rely on foreign test reports, raising compliance costs and slowing product launches.

Angola Automotive Lubricants Industry Leaders

TotalEnergies

Shell plc

Puma Energy

Sonangol E.P.

BP p.l.c. (Castrol)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Chevron achieved first oil from the South N'dola field in Block 0, offshore Angola. The project was completed in just over two years, utilizing a cost-efficient tieback to the existing Mafumeira facility and reinforcing Chevron's 70-year presence in the country by offsetting declines from mature fields.

- April 2024: Etu Energias and Malaysia's Glide Technology partnered to establish a lubricant blending plant in Angola, representing a significant development for local production and the first facility of its kind in the country. This joint venture aligned with Etu Energias' strategy to expand its downstream operations and diversify its product portfolio.

Angola Automotive Lubricants Market Report Scope

Automotive lubricants, such as engine oils, gear oils, and grease, are critical fluids designed to reduce friction, minimize wear, and cool moving components, thereby improving engine performance and extending vehicle lifespan. They also prevent corrosion, remove sludge, and support smooth operation.

The Angola Automotive Lubricants Market is segmented into product type and vehicle type. By product type, the market is segmented into automotive engine oil, other automotive fluids, and other product types (power steering fluid, coolants, etc.). The automotive engine oil is further segmented into 0W-XX, 5W-XX, 10W-XX, 15W-XX, monogrades, and other grades. By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and two-wheelers. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid, Coolants, etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid, Coolants, etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

What is the size of the Angola automotive lubricants market?

The Angola automotive lubricants market stands at 16.02 million liters in 2026 and is projected to reach 17.68 million liters by 2031.

Which product type dominates volume in 2025?

Automotive engine oil led with 54.12% share in 2025, driven by routine sump changes across all vehicle classes.

Why are brake fluids the fastest-growing segment through 2031?

Mandatory inspections detect hydraulic issues, driving brake fluids at a forecast 2.90% CAGR to 2031.

How will local refining affect prices?

If Cabinda, Soyo, and Lobito refineries hit schedule, the domestic base-oil supply could cut import costs and improve availability from 2027 onward.

Page last updated on: