Cameroon Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

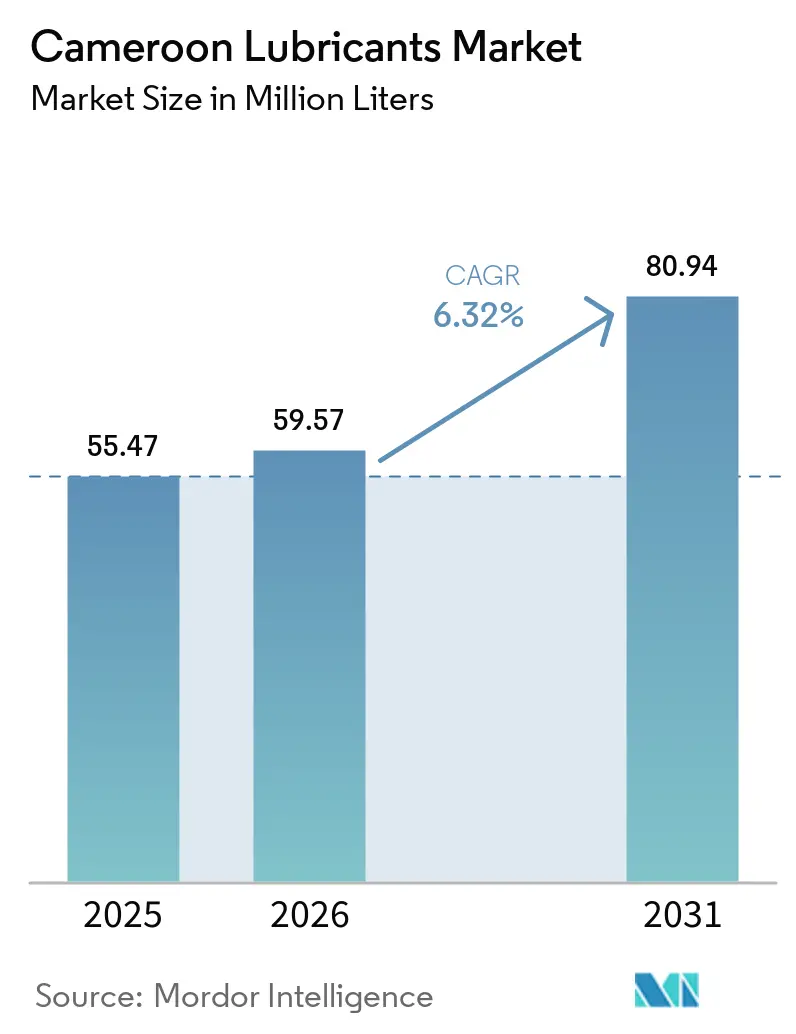

| Base Year Market Size (2025) | 55.47 Million liters |

| Market Volume (2026) | 59.57 Million liters |

| Market Volume (2031) | 80.94 Million liters |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

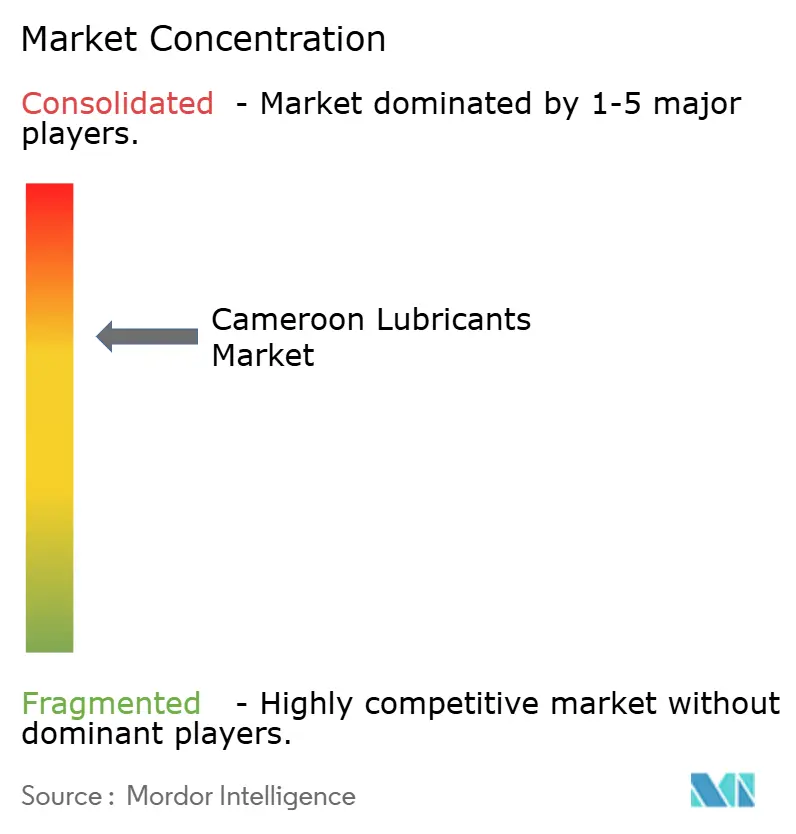

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cameroon Lubricants Market Analysis by Mordor Intelligence

The Cameroon Lubricants Market size is expected to increase from 55.47 million liters in 2025 to 59.57 million liters in 2026 and reach 80.94 million liters by 2031, and is expected to grow at a CAGR of 6.32% over 2026-2031. The growth of the Cameroon lubricants market is supported by accelerated industrialization, mining, and construction programs that rely on machinery requiring lubricants. Increasing cross-border trucking activities, the establishment of new mineral-processing hubs, and fiscal incentives for domestic blending are contributing to the rising demand. The adoption of fully synthetic lubricant grades is increasing among fleet operators seeking extended drain intervals, while micro-distribution networks are addressing supply shortages in peri-urban workshops. However, addressing counterfeit products remains a key challenge, as informal channels continue to account for a significant portion of the market.

Key Report Takeaways

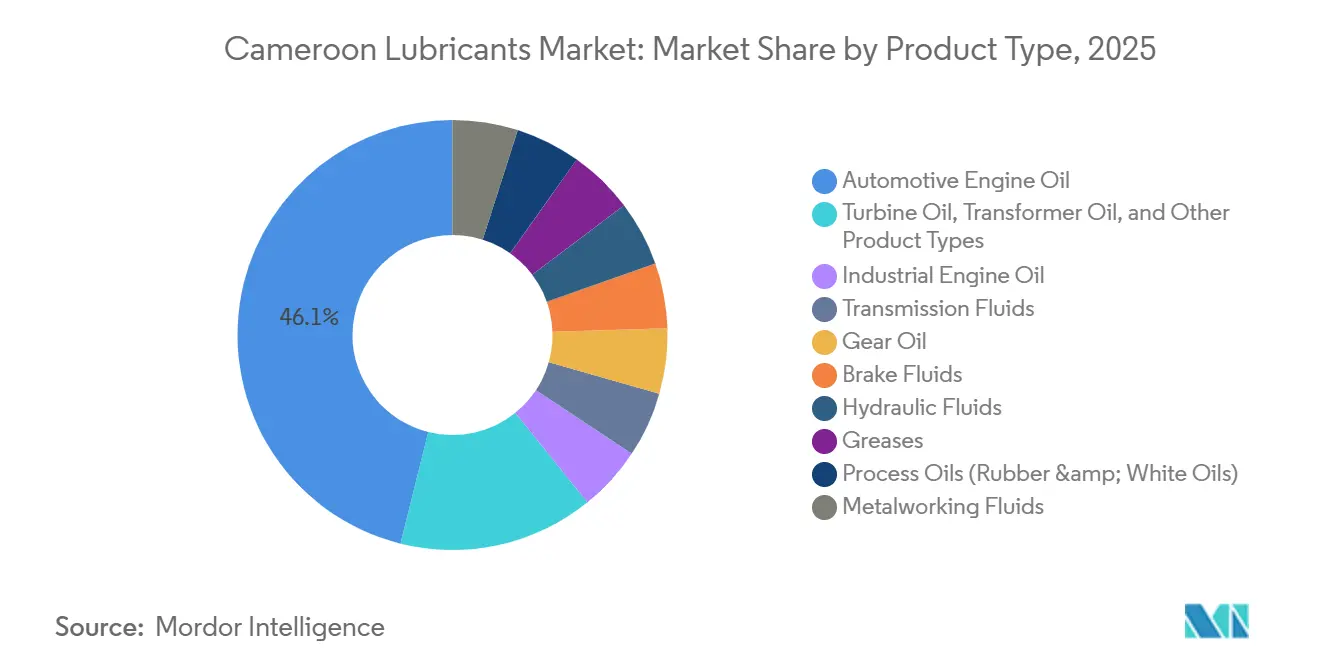

- By product type, automotive engine oil led with 46.12% of the Cameroon lubricants market share in 2025, whereas metalworking fluids are forecast to register the fastest 6.91% CAGR through 2031.

- By end-user industry, automotive accounted for 61.02% share of the Cameroon lubricants market size in 2025, while industrial manufacturing is expected to expand at a 6.85% CAGR to 2031.

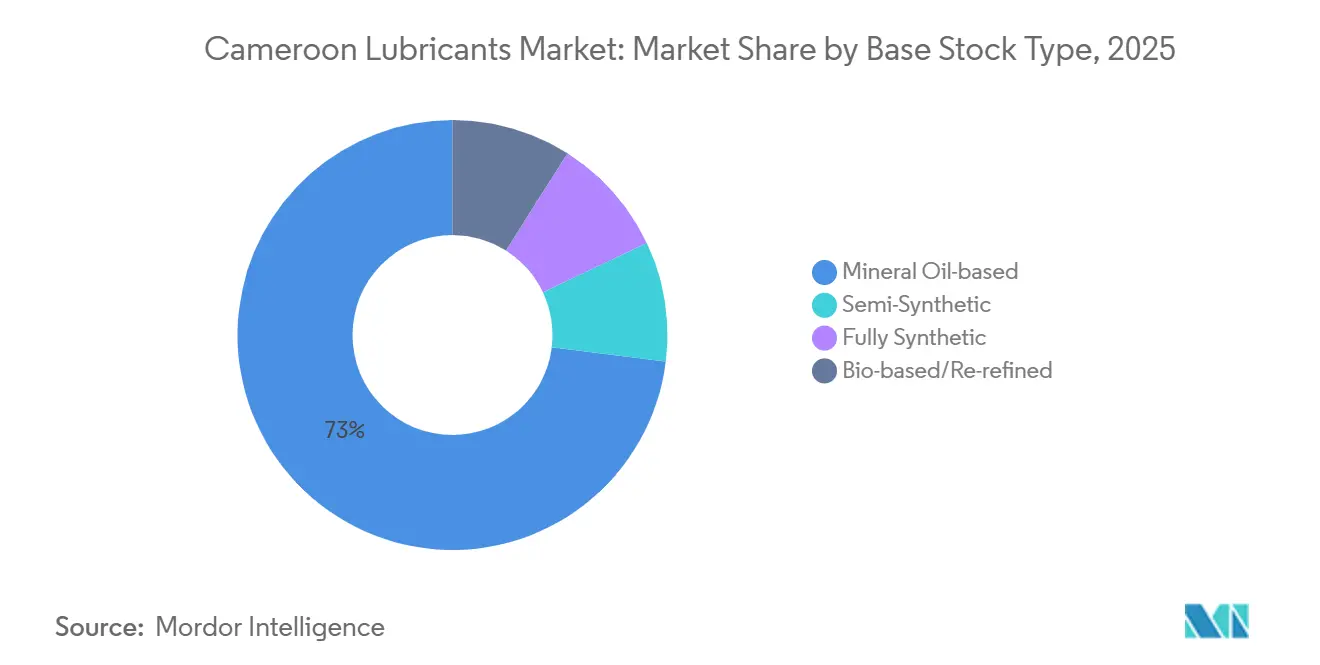

- By base stock type, mineral oil dominated with 73.04% volume share in 2025, yet fully synthetic blends will post a 6.45% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Cameroon Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Cameroon's on-road & off-road vehicle fleet | +1.2% | National, with concentration in Douala, Yaoundé, and Garoua | Medium term (2-4 years) |

| Industrial & mining expansion driving lubricant-intensive machinery use | +2.1% | Adamawa, East, and Littoral regions (mining corridors) | Long term (≥ 4 years) |

| Rising penetration of synthetic & semi-synthetic grades | +0.9% | Urban centers and OEM-serviced fleets | Medium term (2-4 years) |

| Local micro-distribution platforms improving last-mile availability | +0.7% | Peri-urban and rural areas nationwide | Short term (≤ 2 years) |

| Increase in fiscal incentives for in-country blending | +0.8% | Kribi Free Zone and priority investment zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Cameroon’s On-Road & Off-Road Vehicle Fleet

Commercial truck procurement is increasing at a faster rate than passenger car additions, driven by logistics firms servicing landlocked Chad and the Central African Republic. The African Export-Import Bank (Afreximbank) projects that Africa’s vehicle stock will more than double to 118 million units by 2050, which is expected to increase lubricant demand along Cameroon’s transit corridors. Off-road segments, such as forestry harvesters and excavators, consume gear oils at higher rates per operating hour, increasing per-unit lubricant intensity. The CFA 430 billion (USD 0.77 billion) wood-processing park in Bertoua incorporates heavy forestry equipment that depends on high-viscosity hydraulic fluids[1]Cameroon Ministry of Forestry, “Bertoua Wood-Processing Zone,” MINFOF.CM. Additionally, two-wheeler adoption is rising in secondary cities, although initial electrification pilots suggest a medium-term limit on small-engine oil growth. Overall, fleet expansion supports sustained volume growth in the Cameroon lubricants market.

Industrial & Mining Expansion Driving Lubricant-Intensive Machinery Use

Mineral extraction activities are expanding rapidly. The USD 2 billion Minim-Martap bauxite redevelopment project will utilize conveyors and crushers that require abrasion-resistant turbine and hydraulic oils. The Grand Zambi iron-ore project shipped its first ore in 2025, demonstrating the viability of large-scale mining logistics in the East. Additionally, the USD 411 million Arise Integrated Industrial Platform (IIP) hub near Douala focuses on Computer Numerical Control (CNC) machining and plastics extrusion, which continuously consume cutting fluids. This explains why metalworking fluids are growing faster than the overall Cameroon lubricants market. A new 100-megawatt (MW) transmission link to Kribi, expected by the end of 2026, is also anticipated to drive demand for turbine oils used in backup generators[2]Sonatrel, “Kribi Transmission Line Status,” SONATREL.CM.

Rising Penetration of Synthetic & Semi-Synthetic Grades

Fleet managers are increasingly adopting polyalphaolefin and ester-based formulations that extend oil-drain intervals. Shell plc’s introduction of Shell Helix Ultra aligns with Euro 5 import standards, raising awareness of synthetic lubricants. Predictive maintenance tools, such as oil-analysis kits, validate the cost-effectiveness of premium blends over their lifecycle, contributing to the growing share of synthetics in the Cameroon lubricants market. TotalEnergies has launched mid-priced semi-synthetic products to attract operators who are hesitant to pay the full premium for 100% synthetic lubricants.

Local Micro-Distribution Platforms Improving Last-Mile Availability

Companies like Nicop Oil and Fubex Lubricants are enhancing last-mile delivery by using motorcycle couriers and containerized stocks to supply rural workshops within 24 hours. This approach eliminates the need for mechanics to maintain large inventories. Additionally, digital wallets integrated with real-time inventory monitoring reduce working-capital cycles and limit the entry of counterfeit products, supporting disciplined growth in the Cameroon lubricants market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit & sub-standard products in informal channels | -0.9% | National, concentrated in informal retail networks | Short term (≤ 2 years) |

| Import-linked base-oil cost volatility | -0.6% | National, affecting all blenders and importers | Medium term (2-4 years) |

| Gradual electrification of urban mobility | -0.4% | Yaoundé, Douala, and regional capitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit & Sub-Standard Products in Informal Channels

Counterfeit lubricants cause engine damage and affect brand reputation. In 2024, Nigeria’s standards agency seized counterfeit oils worth NGN 20 billion (USD 0.01 billion), highlighting the risk of regional spillover. Cameroon lacks a hologram or Quick Response (QR)-based traceability system, allowing informal kiosks to divert buyers from the formal lubricants market. Legitimate blenders face increased warranty costs and higher marketing expenses to reassure buyers of product authenticity.

Import-Linked Base-Oil Cost Volatility

Cameroon relies entirely on imports for its base oil supply, making margins vulnerable to fluctuations in freight costs. African imports dropped from 106,000 tons in December 2025 to 42,000 tons in January 2026, tightening supply and driving up prices. Local blender SCEFL Douala, with limited bargaining power, remains a price taker, which continues to pressure profitability within the Cameroon lubricants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Metalworking Fluids Accelerate Specialized Demand

Metalworking fluids are expected to be the fastest-growing product category in the Cameroon lubricants market, with an annual growth rate of 6.91%. This growth is attributed to the establishment of Arise Integrated Industrial Platforms’ (IIP) CNC facilities and Proalu’s aluminum rolling lines, both launched in 2025. Automotive engine oil was projected to hold a 46.12% market share in 2025, supported by the registration of 518,780 internal-combustion vehicles between 2021 and 2024, as well as the trans-Saharan truck fleet, which operates under demanding load cycles, leading to consistent oil consumption. Hydraulic fluids, greases, and gear oils are essential for operations at the Minim-Martap and Grand Zambi mines, where abrasive ore handling increases lubricant usage. Additionally, brake, turbine, and transformer oils are aligned with the growth of the automotive sector and the expansion of the national power grid, contributing to the overall stability of the Cameroon lubricants market.

The growth of metalworking fluids also reflects Cameroon’s advancement in the manufacturing value chain, as machining processes consume more lubricants per ton of metal compared to raw material extraction. This shift is diversifying the product mix, enhancing average selling prices, and improving margin quality for suppliers. As precision machining workshops become more prevalent, the Cameroon lubricants market is expected to rely less on automotive products and increasingly on industrial specialty blends.

By End-User Industry: Industrial Manufacturing Outpaces Automotive Growth

In 2025, the automotive segment accounted for 61.02% of the total volume, supported by freight corridors connecting Douala to Bangui. Commercial trucks, characterized by higher sump capacities and longer duty cycles, dominate this consumption. Two-wheelers represent a smaller share, and early electrification initiatives may reduce their future demand for engine oil. Conversely, the industrial manufacturing segment is projected to grow at a CAGR of 6.85%, expanding its share in the Cameroon lubricants market. Key growth drivers include the Arise Integrated Industrial Platform (IIP) hub, Bertoua’s wood-processing complex, and distributed diesel generators that ensure operational continuity during grid outages.

Heavy equipment used in mining, construction, and agriculture contributes to periodic surges in hydraulic and gear oil demand, while marine applications remain concentrated in the ports of Douala and Kribi. Additionally, the food, cement, and chemical industries form a significant part of the demand base, reflecting a developing lubricants market in Cameroon that increasingly aligns with the characteristics of diversified middle-income economies.

By Base Stock Type: Synthetics Capture Premium Niches

In 2025, mineral oils accounted for 73.04% of the total volume, while synthetic lubricants are expected to grow at the fastest rate. Fully synthetic formulations are projected to grow at a rate of 6.45%, driven by Original Equipment Manufacturer (OEM) warranties requiring high-temperature stability. Semi-synthetic lubricants address cost concerns for fleet owners, strengthening the mid-market segment within the Cameroon lubricants market. The lack of refining infrastructure limits circular-economy volumes; however, green-equipment duty exemptions planned for 2026 indicate potential policy support for bio-based inputs. Until domestic refining begins in 2028, reliance on imports will continue to drive cost volatility, positioning synthetic lubricants as a premium option to meet extended drain interval requirements.

Geography Analysis

The Littoral region, centered around Douala, represents more than half of Cameroon’s lubricants market. This is supported by the presence of the country’s largest port, the USD 411 million Arise Integrated Industrial Platform (IIP) site, and a significant commercial fleet. Additionally, the upcoming refinery in Kribi and a 100-megawatt (MW) grid connection are expected to further strengthen the coastal region's position.

In the Center region, Yaoundé contributes to the market through government fleet demand and its role in transshipment activities to the highlands. Meanwhile, the mining corridors in Adamawa and the East are among the fastest-growing zones. The startup of Minim-Martap’s bauxite operations and Grand Zambi’s iron-ore projects are driving demand for high-viscosity oils, as heavy-haul trucks and crushers are essential for these industries. This has resulted in lubricant consumption in these interior provinces exceeding population-weighted averages.

The North and Far North regions primarily rely on agricultural machinery, generating steady but modest demand for diesel-engine and hydraulic oils. In contrast, the Anglophone Northwest and Southwest regions remain underserved by major players, creating opportunities for micro-distribution disruptors. In the South region, forestry and cocoa processing industries drive demand for greases used in sawmills and dryers. Similarly, the West region’s coffee estates and vegetable farms require tractors and two-stroke lubricants.

Cross-border traffic to Chad and the Central African Republic further amplifies transit-related lubricant consumption, particularly for gear and engine oils that endure poor road conditions. Consequently, the Cameroon lubricants market is influenced not only by gross domestic product (GDP) but also by the country’s critical role as a logistics hub in Central Africa.

Competitive Landscape

The cameroon lubricants market remains moderately consolidated. TotalEnergies operates 190 service stations and the only in-country blending site, positioning itself as a key player in the Cameroon lubricants market. Shell plc, following its acquisition of a 74% stake in Engen, utilizes a network of 4,000 stations across Africa and imports finished Shell-branded oils through Douala.

Smaller entrants such as Nicop Oil and Fubex Lubricants reduce operating costs by bypassing traditional depots. They use motorcycles to deliver sealed lubricant packs within 24 hours, targeting small-town mechanics. This approach enhances last-mile distribution and reduces counterfeit leakage, potentially improving the overall quality of the Cameroon lubricants market.

Regional suppliers are focusing on obtaining Original Equipment Manufacturer (OEM) approvals. FUCHS has increased production capacity in South Africa, while Chevron Oronite has expanded its PARATONE additive output to cater to heavy-duty engine clients in Central Africa. Puma Energy’s planned 2026 partnership with Hass Group in the Democratic Republic of the Congo highlights Cameroon's role as a transit hub in the region. However, the absence of a national traceability standard presents challenges, including counterfeit risks and reduced confidence in legitimate brands within the Cameroon lubricants market.

Cameroon Lubricants Industry Leaders

TotalEnergies

Shell plc

Exxon Mobil Corporation

Puma Energy

FUCHS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The USD 411 million Arise Integrated Industrial Platform (IIP) hub near Douala has commenced operations, contributing to a substantial increase in the demand for metalworking fluids. This development is expected to impact the lubricants market in Cameroon, as the hub's operations require significant volumes of these fluids to support industrial activities.

- March 2025: Bee Group's pilot program, valued at CFA 610 million (USD 1.09 million), introduced 40 electric motorcycles, reflecting the early stage of electric vehicle adoption in Cameroon. This development could influence the demand for lubricants, particularly in the transition from traditional to electric vehicles.

Cameroon Lubricants Market Report Scope

Lubricants are substances designed to reduce friction between moving surfaces, minimize wear, and enhance the efficiency of machines and engines. They create a protective film that prevents direct surface contact, reducing heat generation and extending the lifespan of mechanical components. Types include oils, greases, and solid lubricants, each tailored for specific applications such as automotive engines, industrial machinery, or household tools.

The cameroon lubricants market is segmented by product type, end-user industry, and base stock type. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oils (rubber & white oils), metalworking fluids, turbine oil, transformer oil, and other product types. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, and industrial manufacturing. By base stock type, the market is segmented into mineral oil-based, semi-synthetic, fully synthetic, and bio-based/re-refined. The market sizes and forecasts are provided in terms of volume (Liters).

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oils (Rubber & White Oils) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial Manufacturing | Power Generation |

| Metallurgy & Metalworking | |

| Textiles | |

| Oil & Gas | |

| Other End-Use Industries |

| Mineral Oil-based |

| Semi-Synthetic |

| Fully Synthetic |

| Bio-based / Re-refined |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oils (Rubber & White Oils) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-User Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial Manufacturing | Power Generation | |

| Metallurgy & Metalworking | ||

| Textiles | ||

| Oil & Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-based | |

| Semi-Synthetic | ||

| Fully Synthetic | ||

| Bio-based / Re-refined | ||

Key Questions Answered in the Report

What is current market size of Cameroon Lubricants Market?

The Cameroon Lubricants Market size is expected to increase from 55.47 million liters in 2025 to 59.57 million liters in 2026 and reach 80.94 million liters by 2031, and is expected to grow at a CAGR of 6.32% over 2026-2031.

Which product segment grows fastest through 2031?

Metalworking fluids are projected to advance at 6.91% annually as precision machining expands.

Why are synthetic lubricants gaining share?

Fleet operators favor longer drain intervals and better thermal stability, driving a 6.45% CAGR for fully synthetic lubricants.

Which regions contribute most to demand?

Douala’s Littoral region leads, but Adamawa and East mining corridors are the fastest-growing zones.

Page last updated on: