Botswana Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

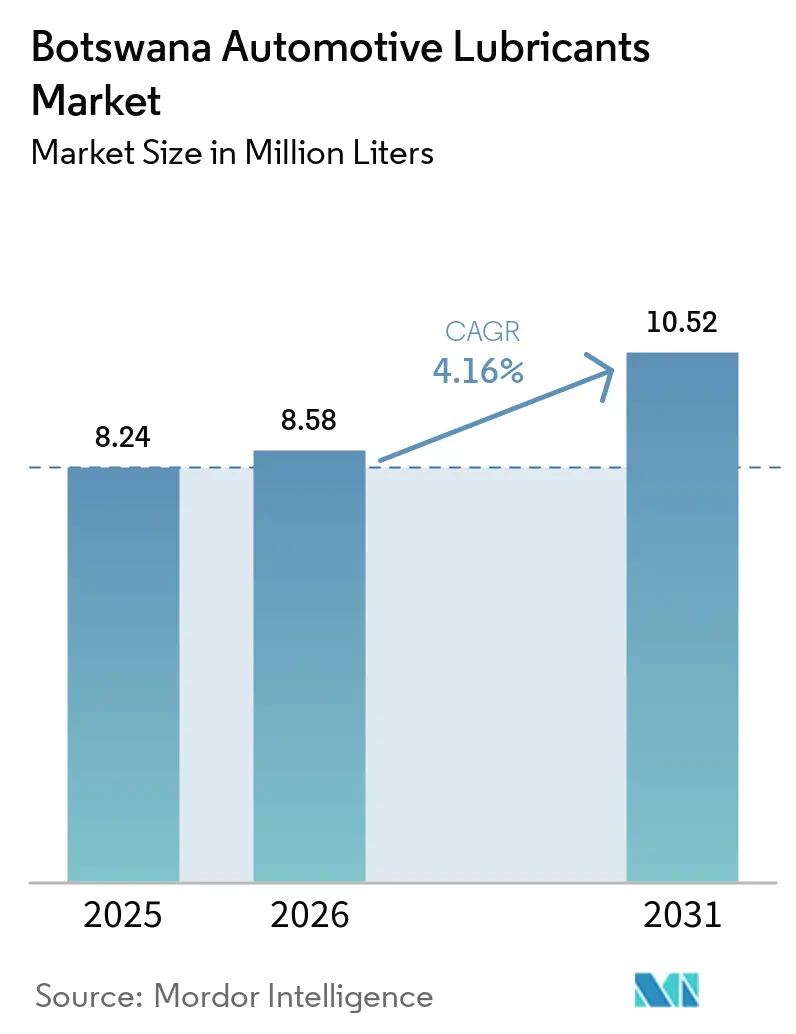

| Base Year Market Size (2025) | 8.24 Million liters |

| Market Volume (2026) | 8.58 Million liters |

| Market Volume (2031) | 10.52 Million liters |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Botswana Automotive Lubricants Market Analysis by Mordor Intelligence

The Botswana Automotive Lubricants Market size is expected to grow from 8.24 Million liters in 2025 to 8.58 Million liters in 2026 and is forecast to reach 10.52 Million liters by 2031 at 4.16% CAGR over 2026-2031. Freight traffic through the Kazungula Bridge nearly doubled between 2021 and 2025, sustaining lubricant demand despite an 8.6% quarter-on-quarter decline in first-time vehicle registrations in Q3 2025. The aging vehicle parc, with over three-quarters of Q2 2025 registrations being used imports, has increased service frequency and oil consumption per vehicle. Mining expansions, such as MMG’s USD 900 million Khoemacau project and Debswana’s ongoing lubricant tenders, have bolstered industrial lubricant demand. Additionally, exclusive distributor agreements and 24-hour forecourt convenience stores are enhancing retail penetration while intensifying competition.

Key Report Takeaways

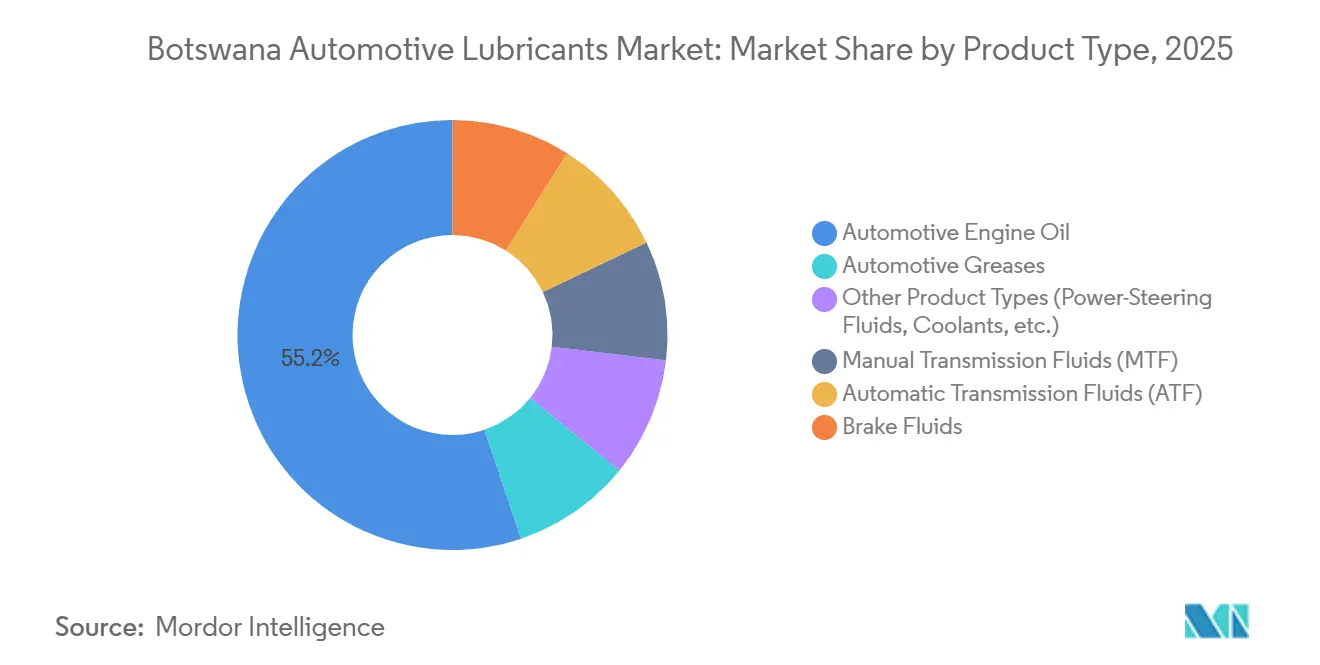

- By product type, automotive engine oil led with 55.18% of the Botswana automotive lubricants market share in 2025 and is projected to advance at a 4.35% CAGR through 2031.

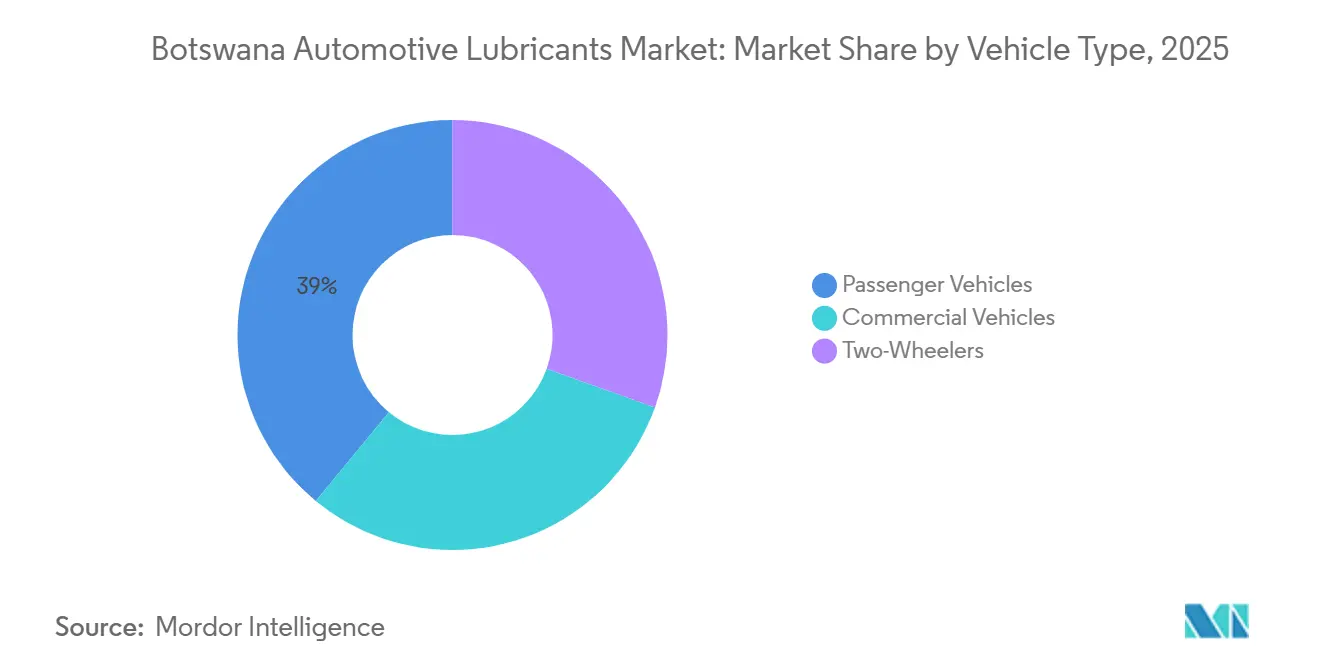

- By vehicle type, passenger vehicles accounted for 39.04% of the Botswana automotive lubricants market share in 2025 and are set to grow at a 4.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Botswana Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing average vehicle age | +0.8% | National, concentrated in Gaborone (63.6% of registrations) | Medium term (2-4 years) |

| Growth in vehicle parc and used-vehicle imports | +1.1% | National, with spillover to cross-border corridors (Kazungula, Martin's Drift, Trans-Kalahari) | Long term (≥ 4 years) |

| Expansion of mining, construction and logistics sectors | +1.3% | Northwest (Khoemacau), Central (Orapa, Letlhakane), Southern (Jwaneng); regional freight corridors | Long term (≥ 4 years) |

| Shift toward synthetic and high-performance lubricants | +0.5% | Mining sites, premium urban segments (Gaborone, Francistown) | Medium term (2-4 years) |

| Botswana as regional transit hub boosting cross-border freight demand | +0.9% | Border posts (Kazungula, Martin's Drift, Mamuno/Buitepos, Pioneer Gate) and North-South Corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Average Vehicle Age

Quarterly first-time vehicle registrations fell to 10,324 units in Q3 2025, while license renewals rose by 22.3% to 149,709 in Q2 2025, reflecting a large and aging active fleet. Used imports, which accounted for 77.4% of Q2 2025 registrations, require more frequent oil changes due to worn seals and piston rings. Regulatory changes in March 2026, tightening dealership licensing, may reduce future imports, potentially extending vehicle lifespans. In response, Castrol launched GTX 5W-30 and 10W-40 oils with American Petroleum Institute (API) SP and 3X Clean technology in April 2026, targeting high-mileage engines. With Toyota, Mazda, and Honda renewals comprising 61.2% of the vehicle parc, distributor AEG Group aligns its inventory with Japanese Original Equipment Manufacturer (OEM) viscosity grades. These factors collectively support steady growth in the Botswana automotive lubricants market as vehicles remain operational for longer periods.

Growth in Vehicle Parc and Used-Vehicle Imports

Total registered vehicles increased from 391,690 in 2015 to 442,800 in 2019 and continued to grow through 2025, despite quarterly fluctuations. Japan supplied 66.8% of first-time registrations in Q2 2025, predominantly pre-owned vehicles, while South Africa contributed 22.4%, mostly new vehicles, creating dual price tiers. Duty-free imports from Southern African Development Community (SADC) countries reinforce South Africa’s role in the supply chain, limiting diversification. Government partnerships with Botswana Oil aim to empower citizen-owned distributors, potentially fragmenting wholesale channels and increasing competition among multinational brands. Urban demand in Gaborone drives stocking strategies, while cross-border corridors are emerging as high-throughput nodes, boosting demand for heavy-duty lubricants.

Expansion of Mining, Construction, and Logistics Sectors

MMG’s Khoemacau mine plans to add 32 Sandvik underground units by Q2 2026 and invest USD 900 million to double copper output to 130,000 tonnes per annum (tpa) by H1 2028, increasing demand for CK-4 diesel oils, hydraulic fluids, and premium greases. Debswana, which procures approximately 100 million liters of fuel annually, issued a three-year lubricant tender in August 2025, emphasizing OEM compliance and uninterrupted supply. Infrastructure projects along the Trans-Kalahari and North-South corridors keep construction equipment operational for extended hours, driving lubricant turnover. Contractors such as Barminco, Sinohydro, and Sladen International specify global OEM standards, favoring distributors with technical accreditation.

Shift Toward Synthetic and High-Performance Lubricants

Harsh conditions in the Kalahari, including dust, sand, and temperature fluctuations, are driving fleets toward synthetic lubricants that offer better oxidation stability and extended drain intervals. Puma Energy’s HD Ultra S 15W-40 (API CK-4, Volvo VDS-4.5) supports 500-hour intervals, reducing downtime for Sandvik and Caterpillar equipment. Castrol’s GTX line now includes Quick Response (QR)-code authentication and low-speed pre-ignition protection for turbocharged gasoline engines. However, with household purchasing power declining by 8.6% in Q3 2025, conventional mineral oils continue to dominate the mass-market retail segment. Broader adoption of synthetics depends on OEM warranty enforcement and value-added services like total fluid management in mining, which, while niche, enhances the value mix of the Botswana automotive lubricants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of counterfeit and adulterated lubricants | -0.4% | National, concentrated in informal retail and border areas | Short term (≤ 2 years) |

| Price sensitivity and dependence on imports | -0.6% | National, acute in rural and low-income urban segments | Medium term (2-4 years) |

| Potential environmental levies on base-oil imports | -0.3% | National, contingent on policy implementation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Presence of Counterfeit and Adulterated Lubricants

A fuel-quality breach in February 2026 highlighted weak in-country testing, which facilitates counterfeit flows. Botswana Oil had to send samples to Durban for verification. Current compulsory standards cover tires and headlights but exclude engine oils, creating a regulatory gap. Informal border trade exploits this loophole, undercutting legitimate brands and risking engine damage for consumers. To address this, brand owners are introducing tamper-evident seals and mobile authentication. Proposed tighter import certification could increase compliance costs in the short term. Until enforcement improves, counterfeit penetration will continue to constrain growth in the Botswana automotive lubricants market.

Price Sensitivity and Dependence on Imports

Cumulative fuel under-recoveries reached BWP 1.2 billion by 2022, equivalent to a BWP 3.86 per-liter gap that squeezed marketing margins before periodic pump-price adjustments. All lubricants are imported via South Africa, incurring levies, Value-Added Tax (VAT), and logistics mark-ups that raise retail prices[1]Botswana Trade Portal, “Tariff Schedule for Petroleum Products,” botswanatradeportal.gov.bw. Base-oil shipments to South Africa declined in Q4 2025 due to supply constraints from the US and Middle-East, increasing spot costs. With household incomes under pressure, motorists are delaying oil changes or opting for mineral grades. Policymakers are negotiating a 30% stake in an Angolan refinery to diversify supply, but timelines remain uncertain. These factors collectively limit volume growth in the Botswana automotive lubricants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automotive Engine Oil Dominate Market Growth

Automotive engine oil accounted for 55.18% of the 2025 volume, driven by the high share of passenger cars and the widespread use of diesel in mining and logistics fleets. This dominance is supported by Toyota, Mazda, and Honda models requiring API SN/SP gasoline oils and CK-4 diesel formulations. Castrol, Puma Energy, and Engen introduced upgraded CK-4 grades in 2025-2026, competing on extended service life and soot-handling capabilities. Mining clients like Debswana demand OEM-approved fluids, securing premium positioning for suppliers with technical accreditation.

The automotive engine oil is projected to have a 4.35% CAGR through 2031. Synthetic Automatic Transmission Fluid (ATF) meeting DEXRON-IIIH/Mercon and Allison TES-295 standards is gaining traction among fleet operators seeking to avoid costly gearbox repairs. Emerging retail formats, such as 24-hour Pick n Pay GO stores at Shell stations, are increasing the availability of ATF and CVT pouches. Manual transmission fluids, brake fluids, greases, and other niche products are also growing steadily, supported by mining equipment requiring specialty greases for extreme pressures.

By Vehicle Type: Passenger Vehicles Lead Growth Despite Fleet Pressures

Passenger vehicles accounted for 39.04% of the 2025 volume and are expected to grow at a 4.81% CAGR through 2031. Older Japanese imports dominate this segment, driving demand for mineral 10W-30 and 10W-40 grades. Retailers like Vivo Energy are bundling lubricant sales with loyalty programs and convenience stores, encouraging consumers to shift toward mid-tier semi-synthetics. The passenger vehicle segment will continue to expand but remain sensitive to disposable income trends.

Commercial trucks, vans, and buses are critical to mining and freight corridors. Crossings at Kazungula and Martin’s Drift generate millions of additional truck-kilometers, each requiring CK-4 diesel oils, gear oils, and greases. Fleet telematics from providers like Cartrack and Ctrack enable predictive maintenance, favoring higher-quality oils with extended drain capabilities. Two-wheelers remain a negligible segment, with fewer than 500 units renewed in Q2 2025, leaving motorcycle oils as a boutique niche.

Geography Analysis

Gaborone led first-time registrations in Q1 2025 and serves as the logistical hub for the Botswana automotive lubricants market, hosting headquarters and depots for AEG Group, Vivo Energy, and Engen. High retail density facilitates access to 5-liter packs, while industrial parks consume drums and Intermediate Bulk Containers (IBCs). Francistown acts as the northern hub, with AEG and Botswana Oil maintaining depots to serve mining regions.

Mining districts such as Jwaneng, Orapa, Letlhakane, and Khoemacau, though sparsely populated, account for a significant share of bulk lubricant consumption. Service stations in these areas, like Vivo’s new Jwaneng site, combine retail and contract supply for mining contractors. Border towns like Kazungula and Martin’s Drift have become lubricant hotspots due to continuous freight movement, with bulk sellers staging stocks nearby to minimize downtime for haulers.

If the government finalizes equity in an Angolan refinery, coastal import routes via Walvis Bay could gain prominence, shifting warehouse footprints toward the western corridor. Until then, the Durban-Gauteng trucking lanes remain the primary supply routes for the Botswana automotive lubricants market.

Competitive Landscape

The market is moderately concentrated, with key players including Shell, BP, Engen, Puma Energy, and TotalEnergies. TotalEnergies’ 2024 divestment of its 20-station network to Prax South Africa signaled portfolio realignment. Vivo Energy Botswana, operating 83 Shell stations by March 2026, leverages its continental scale of over 4,000 stations, supported by Pick n Pay co-branded convenience stores.

AEG Group, Castrol’s exclusive agent since 1998, capitalizes on OEM dealership alliances and depots in Gaborone and Francistown to lead in the passenger-car and mining segments[2]AEG Group, “Company Profile,” aeg.co.bw. Engen Botswana, listed locally, blends Mobil-branded lubricants at Southern African refineries, benefiting from ExxonMobil’s formulation technology. Tropical Lubricants introduced FUCHS products with technical support from South Africa, focusing on mining-grade synthetics.

Local empowerment initiatives are reshaping distribution. Puma Energy’s Project Maatlafatsa transferred its 45th site to a citizen manager in February 2026, while Botswana Oil collaborates with Debswana to onboard emerging suppliers. Digital solutions from Cartrack and Ctrack intersect with lubricant life-cycle management, creating advisory opportunities for suppliers capable of translating data into product recommendations within the Botswana automotive lubricants market.

Botswana Automotive Lubricants Industry Leaders

BP p.l.c. (Castrol)

Puma Energy

Shell plc

Engen Petroleum (PTY) LTD

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Government of Botswana suspended three key fuel levies for six months to protect consumers from rising global oil prices caused by tensions in the Middle-East. This suspension affected the automotive lubricants market by potentially altering vehicle usage and maintenance demand.

- June 2025: BP p.l.c. (Castrol) launched its next-generation Castrol GTX 5W-30 and 10W-40 engine oils in Gaborone, Botswana, representing a notable enhancement to its product portfolio in Southern Africa. The launch, facilitated by authorized distributor Lubricants Supplies Botswana, emphasized a "3x action formula" aimed at cleaning existing sludge and preventing the formation of new deposits.

Botswana Automotive Lubricants Market Report Scope

Automotive lubricants, such as engine oils, gear oils, and grease, are critical fluids designed to reduce friction, minimize wear, and cool moving components, thereby improving engine performance and extending vehicle lifespan. They also prevent corrosion, remove sludge, and support smooth operation.

The Botswana Automotive Lubricants Market is segmented into product type and vehicle type. By product type, the market is segmented into automotive engine oil, manual transmission fluids (MTF), automatic transmission fluids (ATF), brake fluids, automotive greases, and other product types (power-steering fluids, coolants, etc.). The automotive engine oil is further segmented into 0W-XX, 5W-XX, 10W-XX, 15W-XX, monogrades, and other grades. By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and two-wheelers. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power-Steering Fluids, Coolants, etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power-Steering Fluids, Coolants, etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

What is the size of the Botswana automotive lubricants market?

The Botswana automotive lubricants stand at 8.58 million liters in 2026 and are forecast to reach 10.52 million liters by 2031.

Which product type dominated volume in 2025?

Automotive engine oil leads with 55.18% of the 2025 volume.

How does mining influence lubricant consumption?

Projects like Khoemacau and Debswana’s operations require high volumes of CK-4 diesel engine oil, hydraulic fluids and greases, lifting industrial demand.

What risks could slow market growth?

Counterfeit products, price sensitivity from full import dependence and possible environmental levies on base-oil imports are key restraints.

Page last updated on: