Ghana Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

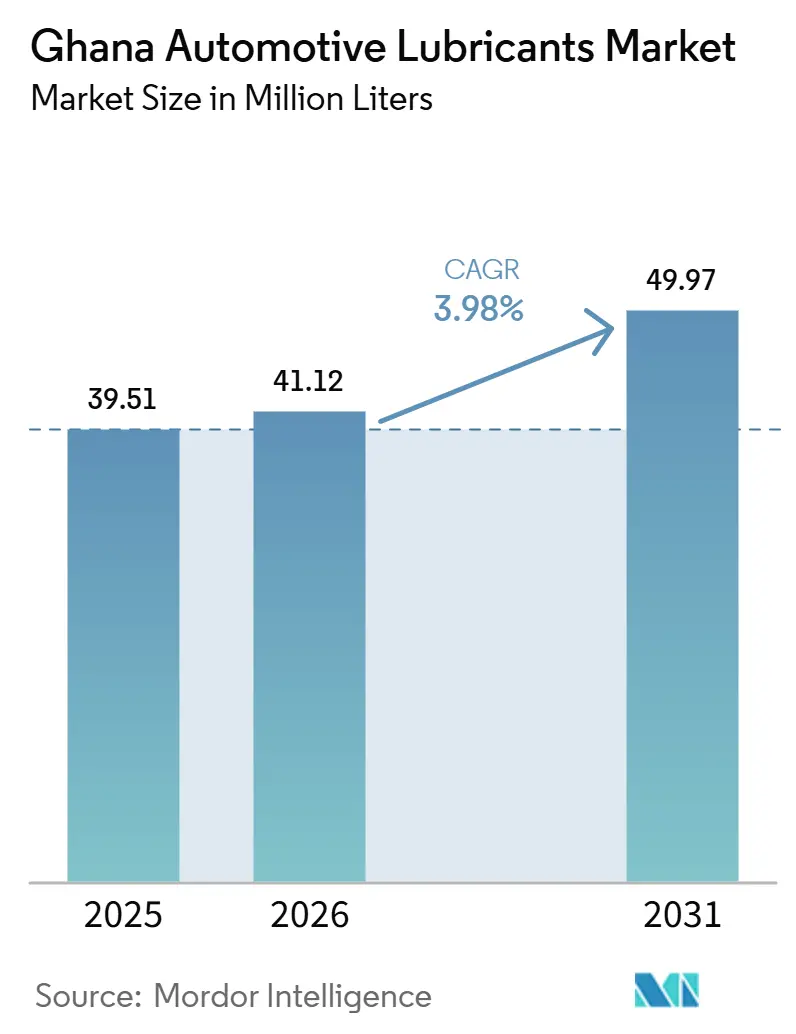

| Base Year Market Size (2025) | 39.51 Million liters |

| Market Volume (2026) | 41.12 Million liters |

| Market Volume (2031) | 49.97 Million liters |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

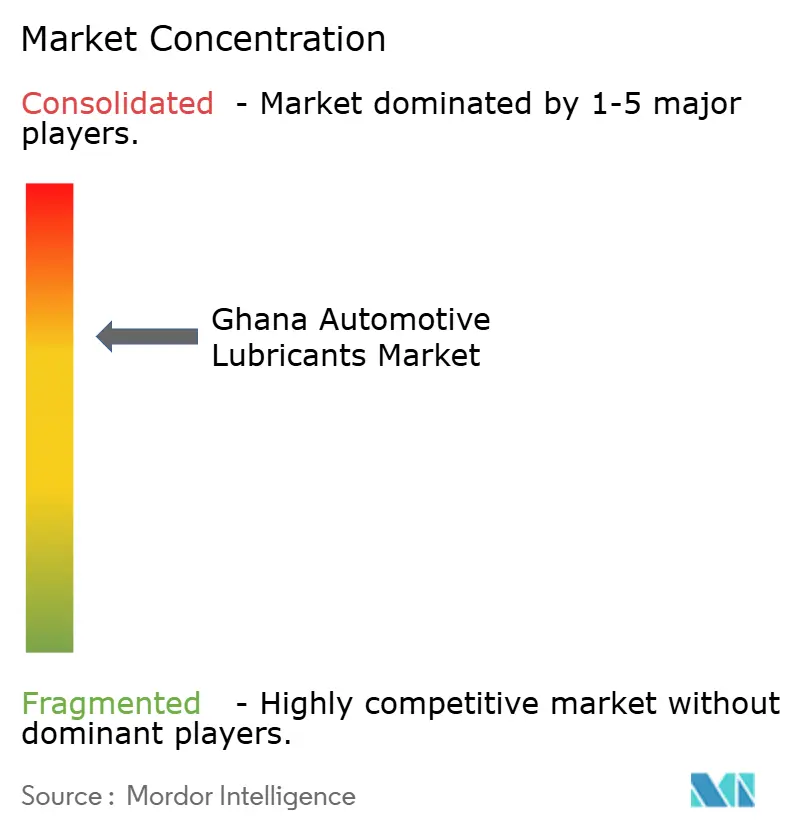

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ghana Automotive Lubricants Market Analysis by Mordor Intelligence

The Ghana Automotive Lubricants Market size is projected to be 39.51 million liters in 2025, 41.12 million liters in 2026, and reach 49.97 million liters by 2031, growing at a CAGR of 3.98% from 2026 to 2031. The Ghana automotive lubricants market is supported by a fleet structure that depends heavily on used vehicle imports, as older vehicles typically require more frequent oil changes and rely more on conventional grades than newer vehicles. Vehicle registration growth is also expanding the service base, with 149,440 registrations recorded between January and July 2025, up 34.4% from the same period in 2024, indicating a broader maintenance cycle across passenger and commercial vehicles. Demand is further supported by higher mining and construction activity, stronger freight movement, and the local blending operations of Tema Lube Oil Company Limited, in which GOIL PLC and TotalEnergies both hold equity interests. Cost pressures from cedi volatility and counterfeit products continue to weigh on the market; however, the 2026 budget supports transport and energy spending while fleet growth continues to drive lubricant demand across the country.

Key Report Takeaways

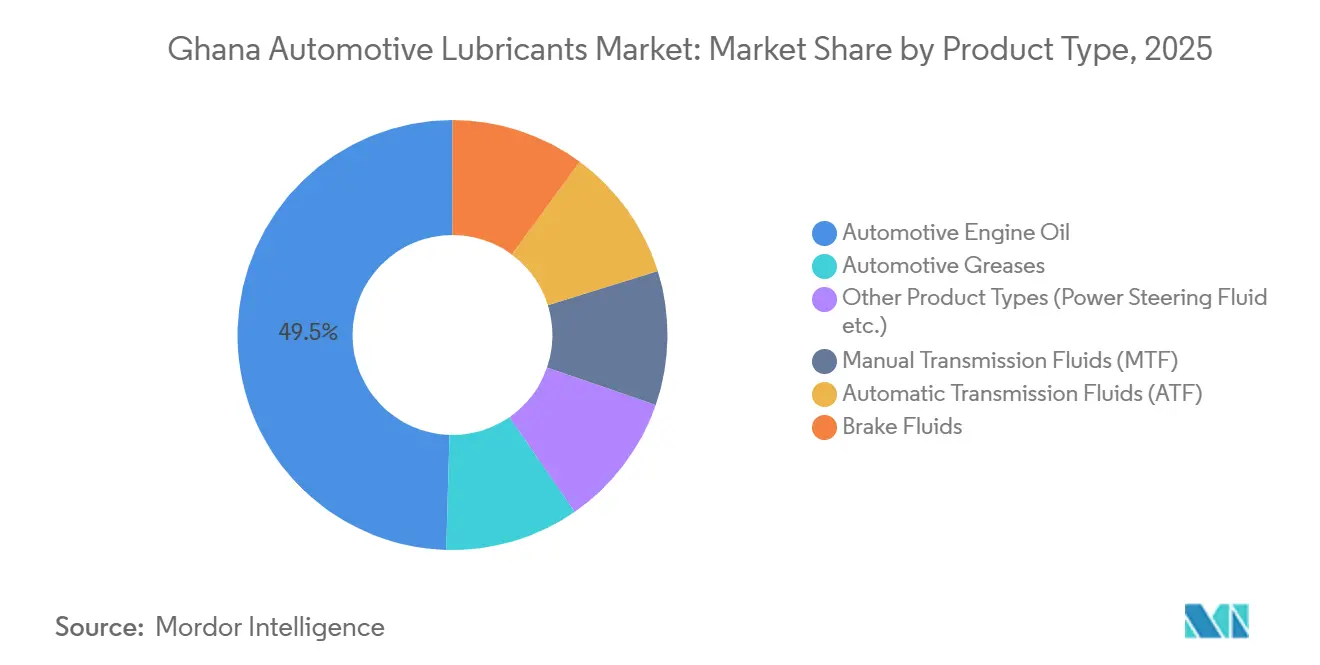

- By product type, Automotive Engine Oil held 49.53% of the Ghana automotive lubricants market share in 2025, while Automatic Transmission Fluid recorded the highest projected CAGR at 4.65% through 2031.

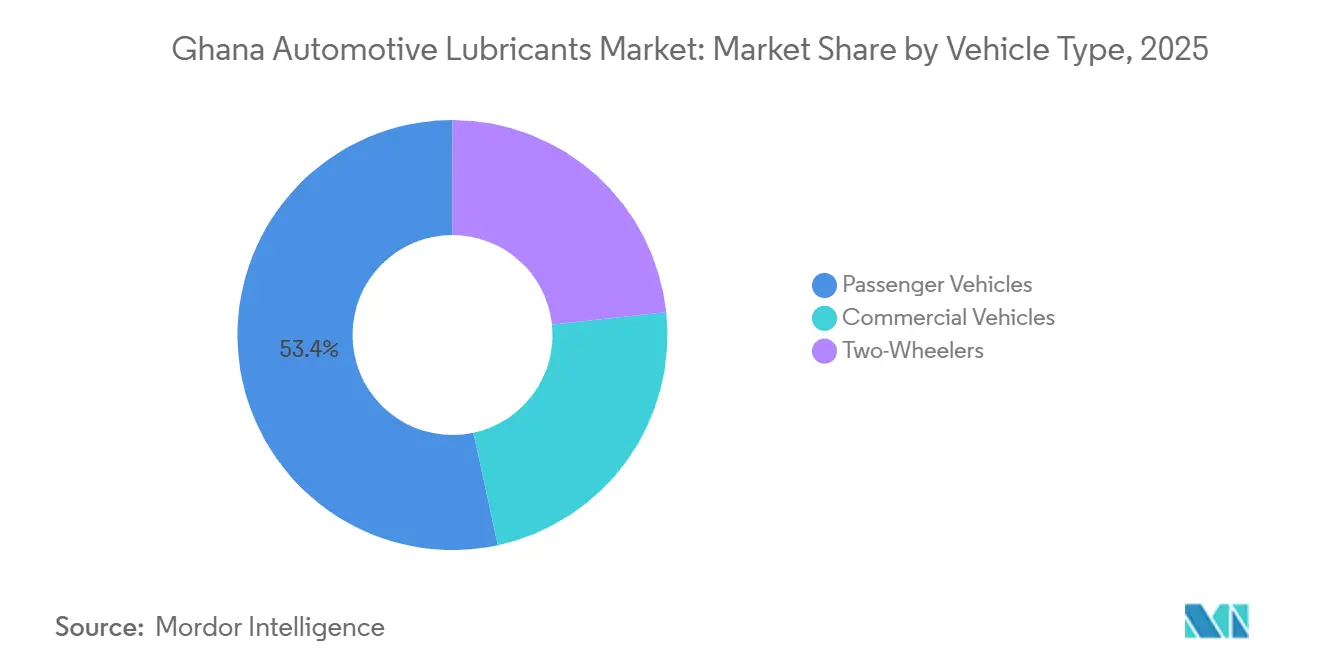

- By vehicle type, Passenger Vehicles accounted for 53.38% share of the Ghana automotive lubricants market size in 2025, while Commercial Vehicles are forecast to expand at a 4.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ghana Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Average Vehicle Age and Used-Vehicle Dominance | +1.2% | National, with highest concentration in Greater Accra and Ashanti Region urban vehicle clusters | Short term (≤ 2 years) |

| Growing Vehicle Parc and Expanding Fleet Operations | +1.0% | National, with spillover into peri-urban corridors of Kumasi, Takoradi, and Tamale | Medium term (2-4 years) |

| Mining and Construction Expansion Driving Heavy Equipment Demand | +0.7% | Western Region and Ashanti mining belt, and infrastructure corridors nationally | Medium term (2-4 years) |

| Rising Motorcycle and Two-Wheeler Usage | +0.5% | National, with stronger relevance in urban centers and northern transport corridors | Short term (≤ 2 years) |

| Local Blending Capacity Investments | +0.3% | Greater Accra, especially Tema Industrial Area, with spillover to regional distribution hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Average Vehicle Age and Used-Vehicle Dominance

Ghana's active fleet continues to support structurally high lubricant demand, as used imports dominate the market mix and older engines require more frequent maintenance than newer vehicles[1]Ghana Revenue Authority, “Official Website,” Ghana Revenue Authority, gra.gov.gh. Annual vehicle imports total approximately 100,000 units, with 85-90% being second-hand vehicles, which keeps service intervals shorter and lubricant turnover higher across the installed fleet. This operating profile also supports steady demand for conventional mineral oils and heavier viscosity grades, as aging engines and worn seals are less compatible with lower-viscosity premium formulations. This fleet profile explains why Automotive Engine Oil remained the largest product category in 2025, with older gasoline and diesel vehicles anchoring the largest share of recurring lubricant purchases. The age mix of vehicles also slows premiumization by keeping a large share of users focused on compatibility, price, and availability rather than formulation upgrades. As a result, the Ghana automotive lubricants market is more resilient to swings in new vehicle sales than markets where lubricant demand is more closely tied to new car ownership trends.

Growing Vehicle Parc and Transport Sector Expansion

The rise in registered vehicles is widening the recurring maintenance base for the Ghana automotive lubricants market, as every addition to the active fleet adds future oil change cycles, workshop visits, and replacement demand[2]Bank of Ghana, “Monetary Policy Report,” Bank of Ghana, bog.gov.gh. The Bank of Ghana's September 2025 Monetary Policy Report cited 149,440 vehicle registrations between January and July 2025, which was 34.4% higher than the comparable 2024 period, signaling a clear expansion in the national vehicle parc. Ride-hailing activity in Accra and Kumasi raises annual mileage per vehicle well above private ownership levels, meaning lubricant use grows faster as commercially operated vehicles expand. Ghana's broader automotive market was valued at USD 2.0 billion in 2025 and is estimated at USD 2.2 billion in 2026, placing lubricant demand within a wider transport spending cycle. Consumer lending and leasing pilots from commercial banks are gradual enablers of newer vehicle access, which would support a measured shift toward multi-grade and synthetic-compatible vehicles over time. This shift does not reduce demand in the Ghana automotive lubricants market but is likely to change the product mix that distributors and service networks emphasize through the forecast period.

Expansion of Mining and Construction Sectors

Mining and construction activity is adding a high-volume commercial layer to the Ghana automotive lubricants market, as heavy equipment consumes large lubricant volumes across engines, hydraulics, transmissions, and gears. Ghana's gold output reached 5.9 million ounces in 2025, up 23.4% from 2024, marking a record year and expanding the operating base for lubricant-intensive machinery in mining corridors. Small-scale mining output surged 63.8% in 2025, adding a diffuse but meaningful demand stream beyond large formal operations. In 2026, Damang Gold Mine began a USD 250 million fleet investment program that included 52 major machines, Liebherr excavators, Caterpillar 395 excavators, and Caterpillar 777 dump trucks, all of which carry intensive lubrication requirements. This creates a channel opportunity for suppliers that can serve mining belts and infrastructure corridors with reliable bulk supply, field support, and product ranges suited to heavy-duty equipment cycles.

Rising Motorcycle and Two-Wheeler Usage

Motorcycle usage is becoming a more visible demand segment in the Ghana automotive lubricants market, particularly as two-wheelers take on a larger role in urban mobility, delivery services, and informal transport. The Road Traffic Amendment Bill passed in 2025 provided legal backing for motorcycle taxis, opening a clearer operating environment for branded suppliers seeking to serve the Okada segment through formal channels. A government-backed electric motorcycle hire-purchase scheme launched in 2026; however, the installed base remains overwhelmingly combustion-based for the period covered in this report. Conventional two-stroke and four-stroke lubricant demand therefore has room to expand as commercial usage becomes more organized and more accessible to established distributors. Formalization also matters at the channel level, as branded suppliers can deepen penetration into service networks that have historically operated outside organized distribution and quality control structures. While two-wheelers are not the largest segment, they represent a more strategic category for product specialization and route-to-market planning in the Ghana automotive lubricants market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and Sub-Standard Products | -0.6% | National, with highest severity in peri-urban markets and informal service channels across Greater Accra, Ashanti, and Central regions | Short term (≤ 2 years) |

| High Consumer Price Sensitivity | -0.4% | National, with stronger effect in rural and semi-urban markets where purchasing power is tighter | Medium term (2-4 years) |

| Cedi Exchange-Rate Volatility and Import Cost Pressure | -0.3% | National, affecting all import-dependent SKUs and distributors with unhedged USD exposure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Sub-Standard Products

Counterfeit lubricants remain a structural restraint on the Ghana automotive lubricants market. Fake and sub-standard products undermine trust, distort pricing, and weaken the position of branded suppliers in informal channels. The problem extends across West Africa, and enforcement cases in neighboring countries in late 2025 and mid-2026 highlight how active these illicit supply chains remain across the region. Counterfeit products are often repackaged in original containers or near-identical bottles, making detection difficult for consumers and small workshops at the point of purchase. Ghana's National Petroleum Authority regulates product quality standards, but enforcement is less consistent in informal service channels, where price and availability often outweigh verification. This limits premium brand capture in the middle of the market, as volume growth does not fully translate into stronger branded revenue when counterfeit supply remains readily accessible. This restraint is particularly relevant for suppliers attempting to move customers toward higher-value formulations, since quality uncertainty shifts purchasing decisions toward price rather than specification.

High Price Sensitivity Constraining Premiumization

Price sensitivity remains a meaningful restraint in the Ghana automotive lubricants market, as many buyers prioritize upfront affordability over longer-drain performance or higher specification grades. Genuine branded lubricants can be priced 50-70% above counterfeit or sub-standard alternatives, creating a persistent trade-down risk in semi-urban and rural markets. This pressure is stronger in fleets where older engines dominate, as many users remain tied to monograde or 15W-40 products that fit both the mechanical profile of the vehicle and the financial constraints of the owner. Puma Energy's positioning of mineral oil variants as suitable for Ghana's second-hand vehicle market illustrates that major suppliers already design their product architecture around affordability constraints. Premium formulations still have room to grow, but uptake is more concentrated in commercial fleets and mining operations, where downtime, engine protection, and lifecycle cost receive more attention than shelf price alone. As a result, mass-market premiumization is likely to remain gradual even as total lubricant demand continues to expand through the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automotive Engine Oil Anchors Volume; Transmission Grades Accelerate

Automatic Transmission Fluid is the fastest-growing product segment in the Ghana automotive lubricants market, projected to expand at a 4.47% CAGR through 2031. This growth is linked to the gradual increase in newer used vehicle imports equipped with automatic transmissions, which is slowly changing the service mix even though the broader fleet remains old by regional standards. The trend is also supported by Ghana's 10-year import-age rule, which favors post-2016 model-year vehicles and drives a measured shift toward newer SUVs and sedans entering the active fleet. The Q4 2025 import profile reinforces this point, as used vehicles with engine capacities between 1,500 cm³ and 3,000 cm³ ranked among the largest import categories by value at GHS 3.1 billion. Manual Transmission and Brake Fluids continue to serve the larger installed base of legacy vehicles, but their growth outlook is more limited as incremental fleet renewal shifts the balance between older and newer drivetrains.

Automotive Engine Oil held 49.53% of the Ghana automotive lubricants market share in 2025, maintaining its position at the center of national lubricant demand as petrol and diesel vehicles continue to dominate the active fleet. Within this segment, 15W-XX and monograde products account for the bulk of volume, as compatibility with older engines and lower retail prices remain more important than formulation sophistication across much of the market. At the same time, 0W-XX and 5W-XX grades are gaining visibility in premium retail channels as newer vehicle owners and organized service points broaden the range of available products. Vivo Energy Holding B.V's launch of Shell Helix Ultra 0W-20 SP in March 2024 and the Shell Advance range in March 2026 illustrate how suppliers are expanding synthetic and specialized product tiers. National Petroleum Authority licensing requirements and Ghana Standards Authority homologation standards also favor established brands, as compliance serves as a practical barrier for lower-quality and unverified imports.

By Vehicle Type: Passenger Vehicle Maintenance Dominates; Commercial Demand Surges

Commercial vehicles are the fastest-growing vehicle segment in the Ghana automotive lubricants market, with the segment forecast to grow at a 4.47% CAGR through 2031. This growth is linked to freight movement, mining output, infrastructure construction, and ECOWAS-related logistics activity, all of which collectively raise utilization rates for trucks and heavy equipment. Damang Gold Mine's 2026 fleet investment added 52 large machines to the operating base, directly expanding demand for heavy-duty engine oils, hydraulic fluids, and gear lubricants in the Western Region. GOIL PLC's focus on deeper mining-sector penetration in 2025 further indicates that major suppliers view commercial and industrial accounts as an important growth channel. High-viscosity oils such as 15W-40 remain dominant in this segment, although the entry of newer trucks is beginning to drive a gradual shift toward multi-grade formulations.

Passenger vehicles accounted for 53.38% of the vehicle-type mix in 2025, making them the largest end-use segment, as private cars and informal taxis continue to dominate the licensed fleet. Ghana's registered vehicle parc stands at 3.6 million units, with daily vehicle activity concentrated in Accra and Kumasi, where routine oil changes and workshop visits are most frequent. Two-wheelers remain the smallest segment by volume; however, the legalization of motorcycle taxis and a government-backed hire-purchase scheme are increasing their commercial relevance for lubricant suppliers. This segment also differs from four-wheel vehicles in formulation requirements, making specialized products such as Shell Advance AX7 and Shell Advance Ultra relevant despite the segment's smaller base. Passenger vehicles remain the volume anchor of the Ghana automotive lubricants market, while commercial vehicles and two-wheelers continue to shape product and channel planning going forward.

Geography Analysis

Greater Accra accounts for the largest share of lubricant transactions in Ghana, reflecting the region's role as the country's commercial and administrative center and the main entry point for imported finished lubricants and base oils. Tema Port reinforces this position by serving as the primary logistics gateway for the lubricant value chain, giving Accra and Tema an advantage in supply access, pricing reference, and product availability. TotalEnergies operates a 273-station network, and Vivo Energy Holding B.V runs more than 244 Shell-branded outlets, with strong concentration along the Accra, Tema, and Kumasi corridor. Tema Lube Oil Company Limited, located in the Tema Industrial Area, further reinforces Greater Accra's role as the main domestic blending and distribution base. The National Petroleum Authority's licensing and quality oversight functions are also centered in Accra, making formal compliance strongest in areas where organized brands are already most visible.

Ashanti Region forms the second-largest consumption center in Ghana, as Kumasi combines high transport activity with proximity to major mining zones. Mining operations around Obuasi and nearby corridors support sustained demand for heavy-duty engine oils, hydraulic fluids, and gear oils serving both fleets and stationary equipment. AngloGold Ashanti projected combined 2026 production from Obuasi and Iduapriem at 472,000 to 530,000 ounces, indicating a durable operating base for specialty lubricant demand in Ghana's mining belt. Brong-Ahafo and Western Regions are recording higher consumption from small-scale mining activity, where service demand is present but remains difficult to capture through formal branded channels.

Northern, Upper East, Upper West, and Volta Regions remain smaller in absolute volume but are strategically relevant, as two-wheeler usage and informal service activity give them a distinct lubricant demand profile. Distribution constraints remain a key factor in these markets, where roadside mechanics and spare-parts shops handle much of the lubricant trade, increasing exposure to counterfeit supply. The opening of a new service station in Bibiani in 2024 under Engen Ghana, now MISA Energy, reflects a broader effort by organized operators to reach secondary markets. As road investment under the 2026 budget improves corridor connectivity, demand in these regions is expected to grow faster from a smaller base, giving suppliers the opportunity to expand physical reach without altering the overall national hierarchy.

Competitive Landscape

The Ghana automotive lubricants market is moderately consolidated. GOIL PLC, TotalEnergies, Vivo Energy Holding B.V, and Engen, now MISA Energy, form the core branded group competing most visibly through service stations, product availability, and customer trust. GOIL's position is reinforced by its scale in petroleum product sales and vertical integration through Tema Lube Oil Company Limited, which helps protect blended product economics from some import cost pressure. GOIL's 54.8% profit increase to GHS 84.7 million in 2024 reflects the company's operating strength as it competes across fuel, lubricants, and network reach. TotalEnergies benefits from its own TLOC stake, while Vivo Energy strengthened its broader African supply chain and technology access through the completed Engen acquisition in 2024.

The most open space lies in commercial and mining-fleet accounts, where specification-led selling remains less developed than retail passenger-car selling. Fleet operators and mine contractors purchase based on uptime, drainage performance, OEM alignment, and service support, which gives premium and specialty suppliers a clearer value case than in price-driven consumer channels. FUCHS, Motul, and Gulf Oil are mid-tier international brands that can target this space outside the largest oil marketing company networks. At the same time, counterfeit products continue to undermine the formal market structure, as brand strength in organized outlets does not consistently extend into informal workshops and roadside channels.

Competition is also becoming more product-driven, as market participants are using product launches and network upgrades to defend share and improve lubricant attachment across fuel retail points. Vivo Energy Holding B.V launched Shell Helix Ultra 0W-20 SP in 2024 and Shell Advance AX7 and Ultra in 2026, demonstrating how global technology pipelines are being adapted for Ghanaian vehicle and motorcycle requirements. GOIL's plan to renovate 270 stations by December 2025 reflects a network modernization strategy aimed at improving customer experience and increasing lubricant sales within its existing footprint. Electric two-wheelers remain a longer-term consideration, but the 2026-2031 window is still dominated by combustion-engine demand, so competitive positioning remains centered on conventional lubricants and formal channel execution.

Ghana Automotive Lubricants Industry Leaders

TotalEnergies

GOIL PLC

Puma Energy

Oando PLC

Vivo Energy Holding B.V

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Vivo Energy Holding B.V launched the Shell Advance AX7 and Shell Advance Ultra lubricant range at Airport Shell Service Station, Accra. The products are designed for two-wheelers and feature wear-protection and friction-reduction technology. They are available nationwide through Shell outlets and accredited resellers, targeting Ghana's newly legalized Okada segment.

- July 2025: GOIL PLC announced plans to renovate 270 fuel stations nationwide by December 2025. The upgrades include structural improvements, enhanced pump systems, and improved customer facilities, aimed at increasing lubricant attachment rates and strengthening brand experience.

Ghana Automotive Lubricants Market Report Scope

Automotive lubricants are fluids and greases designed to reduce friction, dissipate heat, and prevent wear between moving parts in vehicles. They are composed of base oils and chemical additives that protect engines, transmissions, and chassis components from corrosion and rust.

The Ghana automotive lubricants market is segmented by product type and vehicle type. By product type, the market is segmented into automotive engine oil, manual transmission fluids (MTF), automatic transmission fluids (ATF), brake fluids, automotive greases, and other product types (power steering fluid etc.). By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and two-wheelers. The market sizes and forecasts are provided in terms of volume (Liters).

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

What is current market size of Ghana Automotive Lubricants Market?

The Ghana Automotive Lubricants Market size is projected to be 39.51 million liters in 2025, 41.12 million liters in 2026, and reach 49.97 million liters by 2031, growing at a CAGR of 3.98% from 2026 to 2031.

Which product category leads lubricant consumption in Ghana?

Automotive Engine Oil remained the largest category in 2025 with 49.53% share, supported by the large base of older petrol and diesel vehicles that need frequent servicing and remain more reliant on conventional grades.

Which vehicle segment is growing fastest in Ghana’s lubricant space?

Commercial Vehicles are projected to grow at a 4.47% CAGR through 2031, supported by freight activity, mining output, infrastructure work, and higher usage intensity than private vehicles.

Why do used vehicles matter so much for lubricant sales in Ghana?

Used imports dominate the fleet mix, and older engines usually require shorter drain intervals, higher-viscosity oils, and more frequent maintenance, which lifts recurring lubricant demand across workshops and retail outlets.

Page last updated on: