Botanicals and Acupuncture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

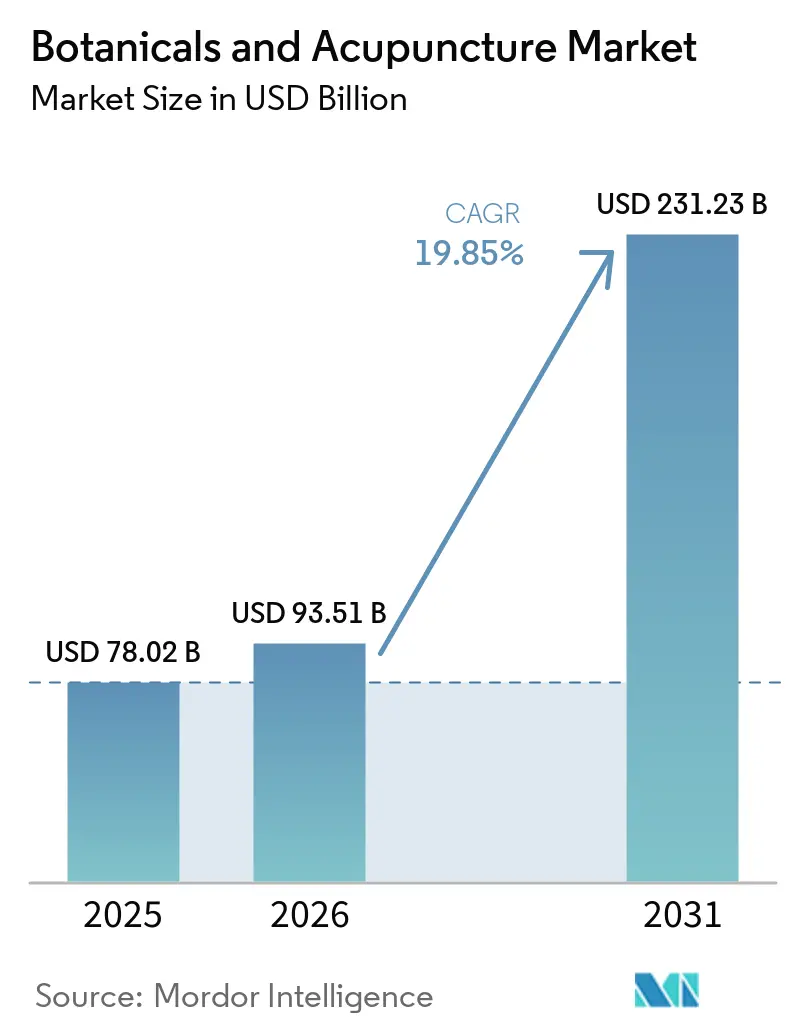

| Market Size (2026) | USD 93.51 Billion |

| Market Size (2031) | USD 231.23 Billion |

| Growth Rate (2026 - 2031) | 19.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Botanicals and Acupuncture Market Analysis by Mordor Intelligence

The Botanicals And Acupuncture Market size is expected to increase from USD 78.02 billion in 2025 to USD 93.51 billion in 2026 and reach USD 231.23 billion by 2031, growing at a CAGR of 19.85% over 2026-2031.

The market is moving on the back of stronger consumer interest in natural care, wider acceptance of non-drug treatment paths, and a deeper body of published clinical work around integrative care. Legislative and payer actions are also improving the operating backdrop, especially where acupuncture is being treated as a covered care option rather than a cash-pay add-on. The botanicals and acupuncture market is also benefiting from digital access, where subscription models and repeat purchase behavior are widening reach for botanical products across global consumer bases. At the same time, the botanicals and acupuncture market still faces practical limits from regulatory misalignment, uneven workforce availability, and the time needed to standardize evidence and product quality across countries. Competitive activity remains dispersed across botanical specialists, device makers, online retailers, and technology developers, so the botanicals and acupuncture market is expanding with room for new entrants but without strong pricing control in the middle tier.

Key Report Takeaways

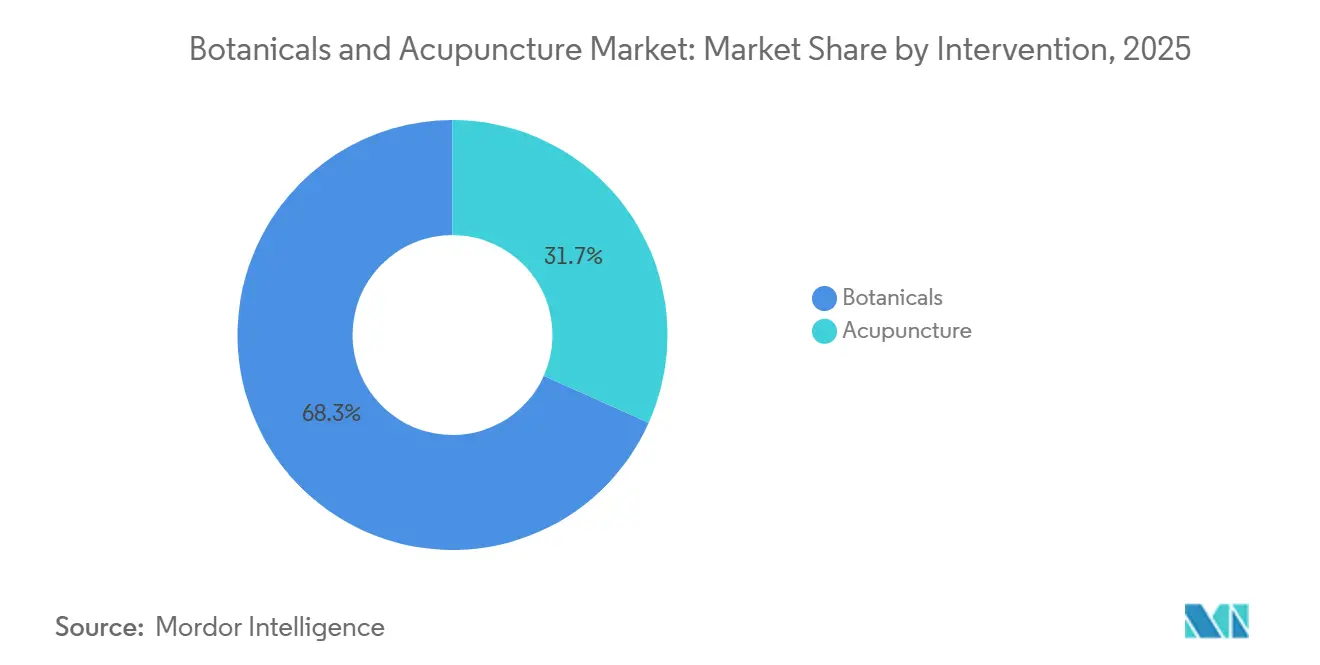

- By intervention, botanicals held 68.31% share in 2025, while acupuncture is forecast to grow at 21.38% CAGR through 2031.

- By application, pain management accounted for 35.24% share in 2025, while stress and anxiety relief is projected to expand at 22.52% CAGR through 2031.

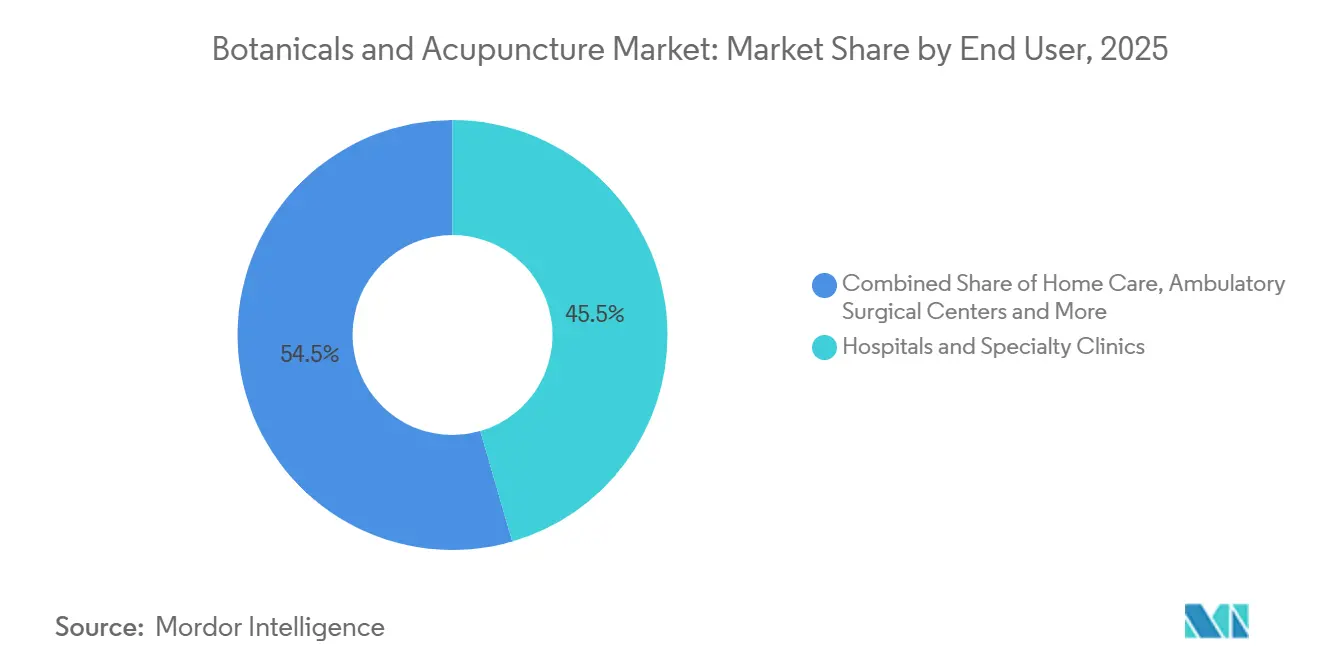

- By end user, hospitals and specialty clinics held 45.52% share in 2025, while home care is forecast to grow at 23.25% CAGR through 2031.

- By distribution channel, direct sales held 32.52% share in 2025, while e-sales is projected to grow at 22.25% CAGR through 2031.

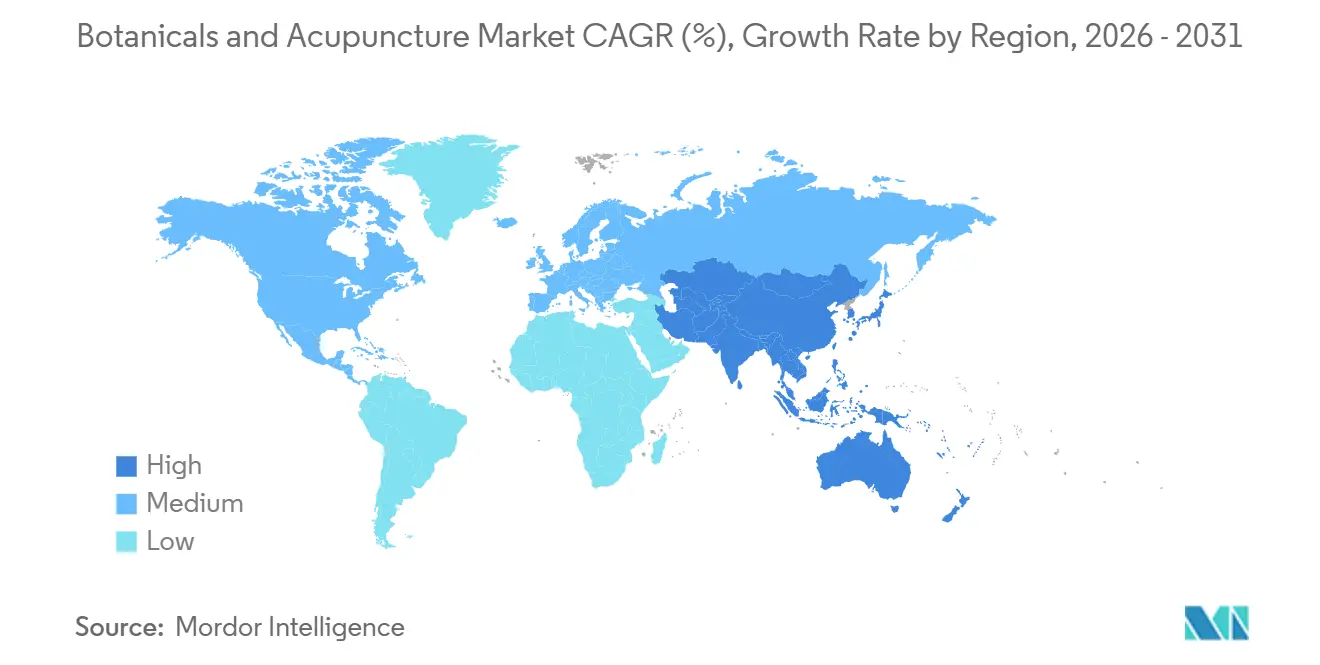

- By geography, North America held 36.22% share in 2025, while Asia-Pacific is forecast to expand at 21.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Botanicals and Acupuncture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preference for Natural and Drug-Free Therapies | +4.8% | Global, with concentration in North America, Western Europe, and APAC | Medium term (2-4 years) |

| Growing Clinical Acceptance of Integrative Pain Management | +3.5% | North America & EU, with spillover to APAC and MEA | Medium term (2-4 years) |

| Expansion of E-Commerce and DTC Access for Botanical Products | +3.2% | Global, led by North America, China, and Germany | Short term (≤ 2 years) |

| Rising Insurance and Reimbursement Support for Acupuncture in Select Markets | +2.8% | North America, select EU markets (Germany, France), APAC core | Medium term (2-4 years) |

| Micro-Segmented Botanical Standardization for Chronic Condition Protocols | +2.5% | Global, particularly EU and North America given regulatory density | Long term (≥ 4 years) |

| AI-Guided Treatment Planning and Personalized Acupuncture Protocols | +2.1% | China, USA, Japan, South Korea, early adoption in EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Natural and Drug-Free Therapies

The botanicals and acupuncture market is seeing stronger demand from consumers who want plant-based products and non-drug treatment options in routine health management. Retail sales of herbal dietary supplements in the United States reached USD 13.23 billion in 2024, rising 5.4% from the prior year and showing that demand moved well beyond a niche wellness base. The botanicals and acupuncture market is also drawing strength from new product mix changes, with mushroom-based botanicals entering the retail top 40 for the first time in 2024 after a 76% sales increase. That shift matters because it shows newer functional formats are now adding demand rather than relying only on established herbal categories. The botanicals and acupuncture market benefits when these products and therapies become normal first-step choices for everyday stress, immune support, and general wellness needs[1]American Botanical Council, “US Sales of Herbal Supplements Increased by 5.4% in 2024,” HerbalGram, herbalgram.org.

Growing Clinical Acceptance of Integrative Pain Management

The botanicals and acupuncture market is gaining support as more health systems place integrative care into regular service lines rather than separate wellness programs. A June 2025 NEJM Catalyst survey found that 35% of U.S. healthcare organizations offered acupuncture or acupressure, compared with 15% outside the United States. The same survey found that 93% of respondents said integrative care improves patient experience, which shows why providers keep these services in place even when budgets are tight. The botanicals and acupuncture market is also helped by the fact that 71% of respondents saw reimbursement stay unchanged, yet providers still continued offering care, which points to demand that is already strong inside institutions. As more hospitals use these therapies to improve pain pathways and patient experience, the botanicals and acupuncture market is likely to see broader procurement of botanical products and acupuncture-related supplies.

Expansion of E-Commerce and DTC Access for Botanical Products

The botanicals and acupuncture market is changing quickly because online sales now do more than add a new route to purchase. iHerb reported USD 2.9 billion in net sales in fiscal 2025, up 19% year over year, with more than 44 million orders and 15 million active global customers. The company also said 80% of orders came from repeat customers and its AutoShip & Save subscription program grew 370% year over year, which shows how predictable demand is becoming in online botanical retail. This matters for the botanicals and acupuncture market because subscription sales reduce dependence on store traffic and help brands build direct customer data on repeat use and product selection. Online platforms also give the botanicals and acupuncture market a faster route to international reach, broader assortment, and targeted recommendations than traditional shelf-based channels[2]iHerb Corporate, “iHerb Achieves Record 2.9 Billion Net Sales in Fiscal 2025,” iHerb Corporate, corporate.iherb.com.

Rising Insurance and Reimbursement Support for Acupuncture in Select Markets

The botanicals and acupuncture market is getting a clear lift where coverage rules start treating acupuncture as part of mainstream care access. In April 2026, the New York State Assembly passed bill A.622, requiring mandatory health insurance coverage for acupuncture under large group insurance policies. That move matters because it expands the addressable patient base in one of the largest insurance pools in the United States. The botanicals and acupuncture market also gains credibility when public discussion around access is tied to chronic pain management and opioid reduction rather than only personal wellness positioning. As more states and payers review coverage in a similar way, the botanicals and acupuncture market is likely to move toward higher visit volume and more stable demand across provider networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Fragmentation Across Botanical and Acupuncture Offerings | -2.5% | Global, most acute in EU, North America, and Southeast Asia | Long term (≥ 4 years) |

| Practitioner Shortage and Non-Uniform Certification Standards | -2.0% | North America, EU, MEA, less acute in APAC | Medium term (2-4 years) |

| Supply Volatility in Medicinal Plant and Needles Input Chains | -1.8% | Global, concentrated in South Asia (India), North Africa (Morocco), East Asia (China) | Short term (≤ 2 years) |

| Adulteration, Safety, and Evidence Threshold Concerns | -1.5% | Global, most acute in EU, USA, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Fragmentation Across Botanical and Acupuncture Offerings

The botanicals and acupuncture market still lacks a common cross-border framework for product rules, clinical standards, and market access pathways. The World Health Organization said in October 2025 that the WHO International Regulatory Cooperation for Herbal Medicines meeting advanced work on the WHO International Herbal Pharmacopoeia and the Global Traditional Medicine Strategy 2025-2034. That progress is important, but it also shows that harmonization is still a work in progress rather than a finished operating environment. The botanicals and acupuncture market therefore continues to face higher compliance costs, slower product rollout, and uneven evidence expectations from one country to another. Until common rules become more practical across regions, the botanicals and acupuncture market will keep favoring larger companies that can manage separate dossiers, quality systems, and approval processes[3]World Health Organization, “16th Annual Meeting of the WHO International Regulatory Cooperation for Herbal Medicines,” World Health Organization, who.int.

Practitioner Shortage and Non-Uniform Certification Standards

The botanicals and acupuncture market faces a supply-side limit because patient demand can rise faster than provider capacity. In the June 2025 NEJM Catalyst survey, 62% of healthcare organizations reported insufficient staffing for integrative care delivery. The same survey found that only 23% offered any form of training to clinicians, which means workforce development has not kept pace with service adoption. The botanicals and acupuncture market is especially exposed in institutional settings where credentialing, scheduling, and standardized care pathways matter more than in independent practice. Without broader training pipelines and smoother recognition standards, the botanicals and acupuncture market will remain uneven across urban, rural, and cross-border care systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Intervention: Botanicals Dominance Masking Acupuncture's Structural Acceleration

Botanicals accounted for 68.31% of botanicals and acupuncture market share in 2025, showing how much of the revenue base still sits in herbal supplements, plant extracts, essential oils, and botanical drugs. Herbal supplements remain the largest commercial layer within this segment because they combine wide consumer familiarity with recurring demand in daily wellness routines. U.S. retail sales of herbal dietary supplements reached a significant sale in 2024, while mushroom-based botanicals posted 76% growth and entered the retail top 40 for the first time, reinforcing the strength of newer functional formats. Within the botanicals and acupuncture industry, this wide product span gives botanicals a larger installed base than the procedure-led acupuncture segment.

Acupuncture is forecast to grow at 21.38% CAGR through 2031, making it the fastest-moving intervention type in the botanicals and acupuncture market. Traditional acupuncture and electroacupuncture still account for the core clinical volume because they fit more established treatment pathways in pain, rehabilitation, and supportive care. Laser acupuncture and dry needling are expanding in sports medicine and physical therapy settings where treatment protocols are widening. A Frontiers in Medicine review published in April 2026 reported AI-guided systems with 97.5% accuracy in facial acupoint identification using YOLOv8-pose models, showing how software support is starting to shape the next layer of practice development. Auricular acupuncture and acupressure are also gaining ground in home care, which extends the botanicals and acupuncture market beyond clinic-only use and gives the segment a longer growth runway.

By Application: Pain Management's Lead Faces Stress-Driven Disruption

Pain management held 35.24% share in 2025, which kept it as the largest application in the botanicals and acupuncture market. That position reflects years of clinical use and a clear fit with non-drug care pathways for chronic pain. Botanical analgesics such as boswellia, willow bark, and curcumin remain closely tied to this use case, while acupuncture continues to hold a practical role in pain-focused treatment programs. Rehabilitation also keeps a meaningful place in the mix, and a 2025 ScienceDirect study cited 93.6% accuracy in predicting upper limb function recovery after ischemic stroke from acupuncture treatment data, supporting continued clinical interest in recovery-related applications.

Stress and anxiety relief is projected to grow at 22.52% CAGR through 2031, giving it the fastest expansion pace among applications in the botanicals and acupuncture market. Kracie Pharmaceutical reported in December 2025 that demand for the stress-related kampo formulation Kamikihito grew most strongly among adults in their 20s, with social media playing an important awareness role. That pattern matters because it shows a younger demand base entering the category through emotional well-being rather than only physical symptom management. Adaptogens such as ashwagandha and rhodiola remain the main botanical expressions of this demand, while acupressure and auricular acupuncture fit well with home-use stress relief. The faster pace in this application also reflects lower historical penetration in formal care settings, which leaves more room for the botanicals and acupuncture market to add new use cases over time.

By End User: Hospital-Centric Market Giving Way to Self-Care Infrastructure

Hospitals and specialty clinics held 45.52% share in 2025, which made them the largest end-user group in the botanicals and acupuncture market. These settings still lead because they concentrate structured acupuncture delivery, practitioner oversight, and evidence-based use of botanical products. The June 2025 NEJM Catalyst survey showed that 35% of U.S. healthcare organizations offered acupuncture or acupressure, which underlines how institutional channels are already important for service delivery. Wellness and rehabilitation centers add depth between medical and consumer use, while traditional medicine clinics remain relevant in countries where formal traditional care systems are more established.

Home care is forecast to grow at 23.25% CAGR through 2031, which gives it the fastest pace of expansion in the botanicals and acupuncture market size. This shift is being supported by wearable electroacupuncture devices, app-guided acupressure tools, and direct-to-consumer botanical programs that reduce dependence on clinic visits. A 2026 Clinical Rheumatology feasibility study found that home-based transcutaneous auricular vagus nerve stimulation for rheumatoid arthritis was feasible and safe, which supports the practical use of patient-managed device care in the home. As home protocols become easier to use and easier to monitor, the botanicals and acupuncture market is likely to see a larger share of demand move toward self-care settings.

By Distribution Channel: Direct Sales' Leadership Is Structurally Challenged by Subscription E-Commerce

Direct sales held 32.52% share in 2025, which kept this as the leading distribution route in the botanicals and acupuncture market. The channel remains important because practitioner-to-patient recommendations and clinic-linked sales still shape behavior in acupuncture services and specialized botanical dispensing. Pharmacies and drug stores continue to matter for familiar products such as psyllium, herbal capsules, and essential oils, especially where consumers want quick access and known brands. Even so, the botanicals and acupuncture market is gradually shifting away from channels that rely mainly on physical shelf presence.

E-sales is projected to grow at 22.25% CAGR through 2031, marking the fastest channel growth in the botanicals and acupuncture market size. iHerb reported USD 2.9 billion in 2025 sales and processed 174,000 orders in a single day, which gives a clear benchmark for the scale now possible in digital botanical retail. The same business also showed how AI-driven recommendations and repeat purchase behavior are improving conversion and retention at the same time. That matters because brands in the botanicals and acupuncture industry can build direct consumer data, track purchase patterns, and test product bundles more effectively online than through store-led routes.

Geography Analysis

North America held 36.22% of botanicals and acupuncture market share in 2025, making it the largest regional contributor. The United States remains the anchor because it combines stronger integrative care infrastructure with broader institutional awareness than most other regions. In the June 2025 NEJM Catalyst survey, 35% of U.S. healthcare organizations offered acupuncture or acupressure and 93% said integrative care improves patient experience, which points to a solid clinical base for continued demand. New York's April 2026 move to require acupuncture coverage under large group insurance policies adds a more supportive reimbursement backdrop for one of the country's largest insured populations. Canada and Mexico add regional depth through consumer interest in botanical care and traditional medicine use, even though the United States still sets the commercial pace.

Asia-Pacific is projected to expand at 21.15% CAGR through 2031, giving it the fastest pace of growth in the botanicals and acupuncture market size. The region benefits from deeper familiarity with traditional care systems, larger practitioner bases in several countries, and stronger everyday use of botanicals in health routines. Kracie Pharmaceutical said in December 2025 that Japan's medical-use kampo market had expanded for 6 consecutive years, with younger adults driving strong demand for stress-related formulations. This supports the view that Asia-Pacific combines established traditional demand with new consumer adoption patterns, which gives the botanicals and acupuncture market a broad growth platform.

Europe remains an important part of the botanicals and acupuncture market, but it is operating with a tighter and more uneven regulatory backdrop than some other regions. The October 2025 WHO International Regulatory Cooperation for Herbal Medicines meeting showed continued work on the International Herbal Pharmacopoeia and the Global Traditional Medicine Strategy 2025-2034, which highlights both the need for and the absence of full harmonization. The Middle East and Africa and South America are smaller in current scale, but both regions offer room for sourcing, wellness services, and future expansion. The botanicals and acupuncture market is therefore geographically diverse, but regional growth still depends heavily on how quickly care access, evidence standards, and product rules move closer together.

Competitive Landscape

The botanicals and acupuncture market remains fragmented across several competitive groups rather than one unified leader set. Standardized botanical extract specialists, flavors and fragrance companies with botanical ingredient operations, acupuncture device makers, and online retail platforms all compete in different parts of the value chain. No single company appears to control a dominant cross-segment position, which keeps the botanicals and acupuncture market open but also limits broad pricing power. Most strategies still center on product differentiation, supply security, regulatory credibility, and direct access to customers.

Symrise showed one clear competitive move in October 2025 when it invested in Cellibre, a U.S.-based biotechnology company focused on fermentation-derived botanical ingredients. That step matters because it points to a route around cultivation season volatility and a more controlled production model for botanical actives. iHerb showed another important move through scale, reporting USD 2.9 billion in fiscal 2025 net sales with 80% of orders from repeat customers and strong subscription growth, which strengthens its role as a data-rich retail gatekeeper in the botanicals and acupuncture market. Sabinsa also used product quality and transparency as a competitive lever in 2026 when its Shagandha earned the Alkemist Assured seal, supporting its position in standardized botanical ingredients. These moves show that the botanicals and acupuncture market is rewarding companies that can prove consistency, scale direct reach, or improve manufacturing control.

On the acupuncture side, technology is becoming a more visible point of competition inside the botanicals and acupuncture market. The April 2026 Frontiers in Medicine review on AI-guided acupuncture decision systems highlighted 97.5% accuracy in facial acupoint identification, showing how digital support tools are moving from concept toward practical use. That shift could help standardize parts of treatment planning and lower some of the variation seen across practice settings. Even so, the botanicals and acupuncture market is still defined more by many specialized players than by a small group of dominant operators, so competition is likely to stay active across ingredients, devices, services, and digital platforms.

Botanicals and Acupuncture Industry Leaders

Archer Daniels Midland Company

International Flavors & Fragrances Inc.

Martin Bauer Group

Indena S.p.A.

SEIRIN Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Sabinsa's Curcumin C3 Reduct received approval in Great Britain for use in food supplements (max 140 mg/day for adults) from the UK FSA and FSS. This follows EU and US approvals, setting a key regulatory milestone for turmeric extracts post-Brexit.

- April 2026: New York passed bill A.622, led by Assemblymember Ron Kim, requiring large group insurance to cover acupuncture. The law highlights acupuncture's role in managing pain and reducing opioid use, expanding its insured market in the state.

Global Botanicals and Acupuncture Market Report Scope

As per the scope of the report, botanicals are plant-based remedies used for healing, while acupuncture involves inserting needles into specific points to stimulate energy flow and promote balance. The segmentation of the botanicals and acupuncture market is categorized by intervention, application, end user, distribution channel, and geography. By intervention, the market includes botanicals such as herbal supplements, medicinal plants, essential oils, plant-based extracts, botanical drugs, and others. It also covers acupuncture methods like traditional acupuncture, electroacupuncture, dry needling, auricular acupuncture, scalp acupuncture, laser acupuncture, and acupressure. By application, the market is segmented into pain management, stress and anxiety relief, rehabilitation, women’s health and fertility, gastrointestinal wellness, immunity support, and other applications. By end user, the market is divided into hospitals and specialty clinics, wellness and rehabilitation centers, home care, ambulatory surgical centers, traditional medicine clinics, and other end users. By distribution channel, the segmentation includes direct sales, e-sales, pharmacies and drug stores, and other distribution channels.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Botanicals | Herbal Supplements |

| Medicinal Plants | |

| Essential Oils | |

| Plant-Based Extracts | |

| Botanical Drugs | |

| Others | |

| Acupuncture | Traditional Acupuncture |

| Electroacupuncture | |

| Dry Needling | |

| Auricular Acupuncture | |

| Scalp Acupuncture | |

| Laser Acupuncture | |

| Acupressure |

| Pain Management |

| Stress and Anxiety Relief |

| Rehabilitation |

| Women's Health and Fertility |

| Gastrointestinal Wellness |

| Immunity Support |

| Other Applications |

| Hospitals and Specialty Clinics |

| Wellness and Rehabilitation Centers |

| Home Care |

| Ambulatory Surgical Centers |

| Traditional Medicine Clinics |

| Other End Users |

| Direct Sales |

| E-Sales |

| Pharmacies and Drug Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Intervention | Botanicals | Herbal Supplements |

| Medicinal Plants | ||

| Essential Oils | ||

| Plant-Based Extracts | ||

| Botanical Drugs | ||

| Others | ||

| Acupuncture | Traditional Acupuncture | |

| Electroacupuncture | ||

| Dry Needling | ||

| Auricular Acupuncture | ||

| Scalp Acupuncture | ||

| Laser Acupuncture | ||

| Acupressure | ||

| By Application | Pain Management | |

| Stress and Anxiety Relief | ||

| Rehabilitation | ||

| Women's Health and Fertility | ||

| Gastrointestinal Wellness | ||

| Immunity Support | ||

| Other Applications | ||

| By End User | Hospitals and Specialty Clinics | |

| Wellness and Rehabilitation Centers | ||

| Home Care | ||

| Ambulatory Surgical Centers | ||

| Traditional Medicine Clinics | ||

| Other End Users | ||

| By Distribution Channel | Direct Sales | |

| E-Sales | ||

| Pharmacies and Drug Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of botanicals and acupuncture?

The sector is estimated at USD 93.51 billion in 2026 and is projected to reach USD 231.23 billion by 2031 at a 19.85% CAGR.

Which intervention type leads revenue today?

Botanicals held the leading 68.31% share in 2025, supported by broad demand across herbal supplements, extracts, essential oils, and botanical drugs.

Which application is growing the fastest through 2031?

Stress and anxiety relief is projected to expand at 22.52% CAGR through 2031, helped by stronger uptake among younger consumers and wider use of adaptogens and home-based relief formats.

Why is North America ahead of other regions?

North America led with 36.22% share in 2025 because of stronger integrative care infrastructure, broader provider awareness, and policy support such as New York's 2026 acupuncture coverage action.

How important are online channels for future growth?

E-sales is forecast to grow at 22.25% CAGR through 2031, and iHerb's USD 2.9 billion in fiscal 2025 sales shows how online platforms are scaling botanical demand globally.

What is changing in the end-user mix?

Hospitals and specialty clinics remained largest at 45.52% share in 2025, but home care is growing faster at 23.25% CAGR through 2031 as devices, apps, and direct-to-consumer programs make self-care easier.

Page last updated on: