Ayurveda Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

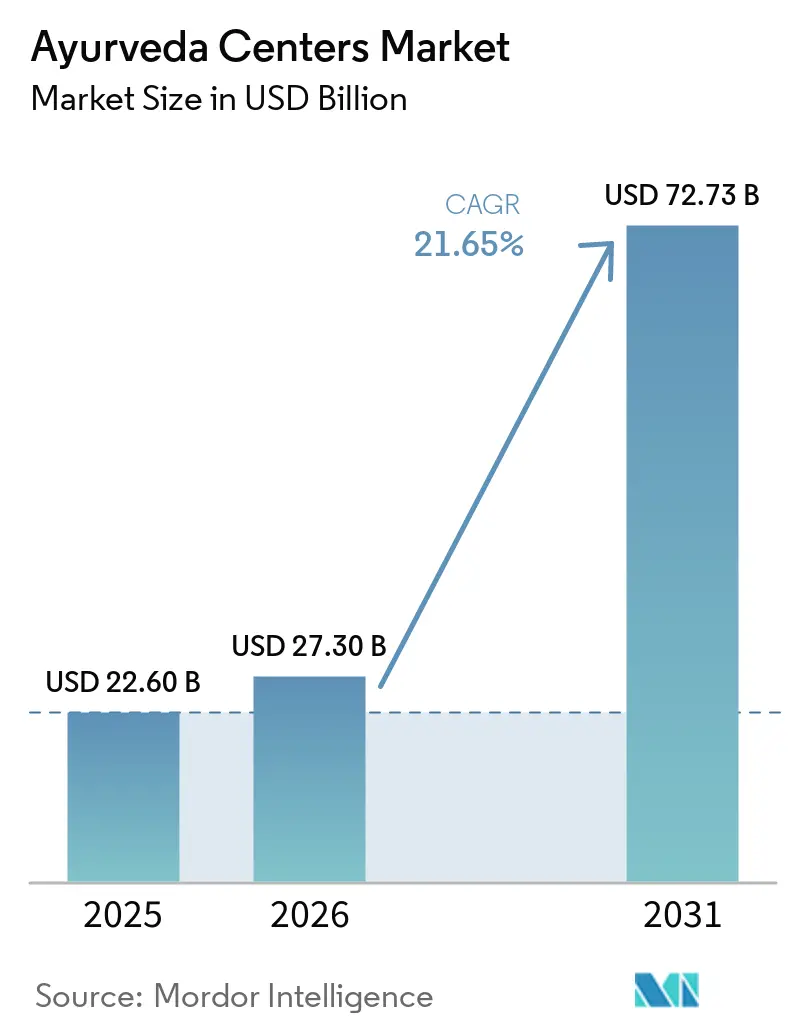

| Market Size (2026) | USD 27.30 Billion |

| Market Size (2031) | USD 72.73 Billion |

| Growth Rate (2026 - 2031) | 21.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

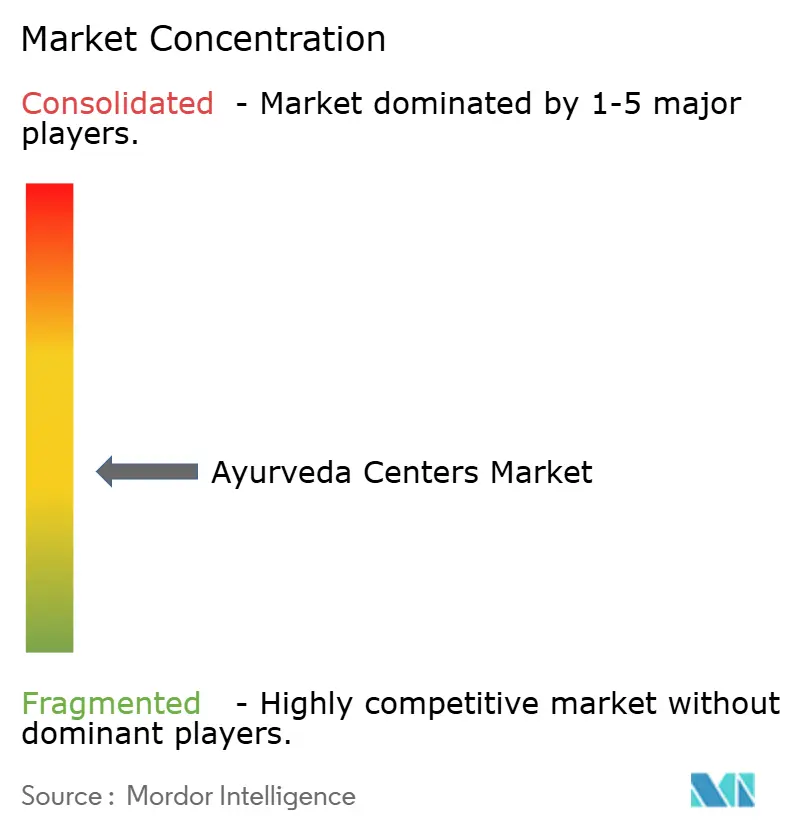

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ayurveda Centers Market Analysis by Mordor Intelligence

The Ayurveda Centers Market size is projected to expand from USD 22.60 billion in 2025 and USD 27.30 billion in 2026 to USD 72.73 billion by 2031, registering a CAGR of 21.65% between 2026 to 2031.

Insurance parity for AYUSH care, a formal medical-value-travel visa, and the World Health Organization’s elevation of traditional medicine are realigning wellness budgets toward regulated clinical spending [1]World Health Organization, “WHO Global Centre for Traditional Medicine,” who.int. Facility economics are shifting to day-care Panchakarma protocols that dovetail with third-party payers, and service-line revenues are bifurcating between high-volume outpatient consultations and high-margin detox packages. Consolidation is accelerating as hospital chains and private equity funds acquire standalone networks to blend allopathic and Ayurvedic modalities under one roof.

Key Report Takeaways

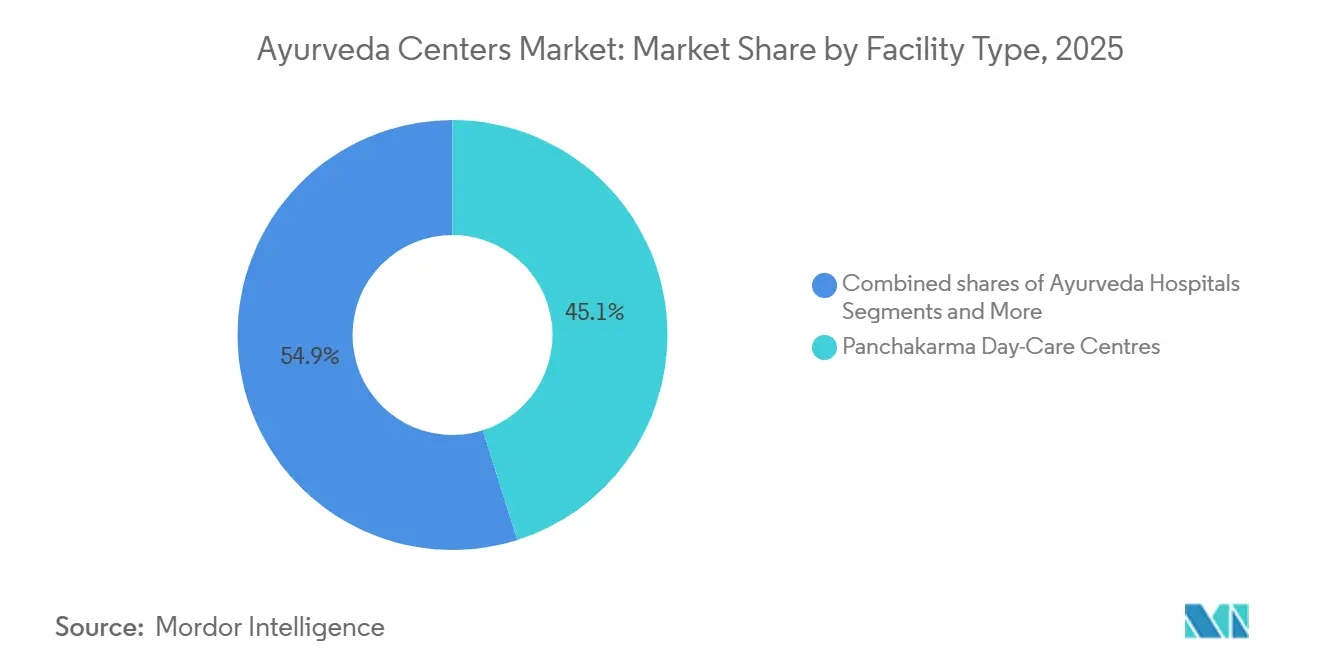

- By facility type, panchakarma day-care centers led with 45.12% revenue share in 2025, and wellness retreats/resorts are projected to expand at a 23.14% CAGR to 2031.

- By service line, OPD Consultations & Medicines accounted for 52.34% of the Ayurveda centers market size in 2025, while wellness/aesthetic programs are advancing at an 24.15% CAGR through 2031.

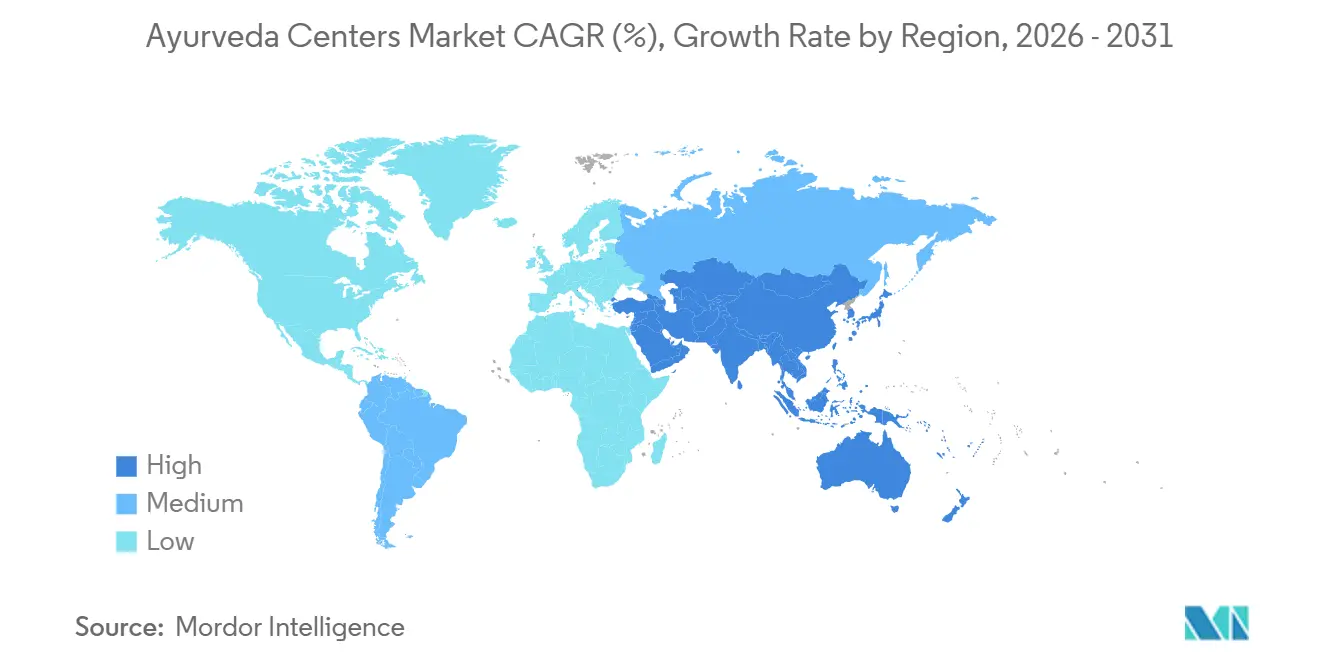

- By geography, Asia-Pacific held 79.02% of the Ayurveda centers market share in 2025 and is forecast to register a 22.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ayurveda Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IRDAI parity for AYUSH unlocking insurance-backed demand | +4.5% | India, Nepal, Bangladesh | Medium term (2-4 years) |

| AYUSH visa and medical value travel promotion | +3.8% | India, Sri Lanka | Short term (≤ 2 years) |

| WHO Global Centre for Traditional Medicine elevates standards | +2.5% | Global | Long term (≥ 4 years) |

| Rapid growth in global wellness tourism | +4.2% | Global | Medium term (2-4 years) |

| Rising NABH accreditation enabling cashless referrals | +3.0% | India, GCC | Short term (≤ 2 years) |

| ICD-11 coding improves reimbursement | +2.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IRDAI Parity Unlocking Insurance-Backed Demand

India’s January 2024 directive mandates equal insurance coverage for Ayurveda, Yoga, Unani, Siddha, and Homeopathy, removing historical exclusion from cashless reimbursement. Twenty-seven insurers have launched AYUSH-inclusive products, yet claim rejection remains common because most hospitals lack standardized procedure codes and digital records. NABH-accredited centers that invest in structured documentation already secure faster approvals and higher patient inflows. The Ministry of Ayush, with NABH support, is drafting a unified taxonomy that will standardize claims nationwide. Over the medium term the directive is expected to convert out-of-pocket detox spending into insured medical expenditure, shrinking price resistance among urban consumers.

AYUSH Visa and Medical Value Travel Promotion

India issued 411 dedicated Ayush visas in 2024, and cumulative issuances topped 1,600 by early 2025, funneling an estimated INR 300-400 million (USD 3.17–4.23 million) in monthly Ayurveda tourism revenue to Kerala alone. Resorts in Sri Lanka report that 80% of international guests need stays longer than typical tourist visas allow, underscoring the scheme’s importance[2]Barberyn Resorts, “Barberyn Ayurveda Resorts,” barberyn.com. Short-term growth concentrates in Kerala and Karnataka, where English-proficient clinicians and heritage resorts reduce cultural friction. In the medium term, marketing alliances with airline and hotel chains are expected to triple inbound volumes. The visa also legitimizes Ayurveda in the eyes of regulators abroad, smoothing bilateral accreditation talks.

WHO Global Centre for Traditional Medicine Elevates Standards

WHO’s USD 250 million Global Centre in Jamnagar anchors evidence-generation for traditional medicine. Its protocols for multicenter trials, pharmacopeial harmonization, and digital governance place Ayurveda within mainstream regulatory pathways. February 2025 summits in New Delhi clarified that digital health tools for Panchakarma must meet the same outcome-tracking thresholds as medical devices [3]CAYEIT, “Digital Ayurveda & AI Integration in 2025,” cayeit.com. Insurers and ministries are already referencing draft guidelines when deciding reimbursement. Over the long term, standardized data will improve international acceptance and facilitate cross-border insurance portability.

Rapid Growth in Global Wellness Tourism

Panchakarma programs bundle detox, yoga, lifestyle coaching, and cultural immersion, satisfying travelers’ preference for transformational experiences. Kerala’s February 2026 International Ayurveda and Wellness Conclave attracted global tour operators who now integrate seven- to 14-night packages into premium itineraries. Forward bookings at Somatheeram stretch 18 months, USD 6,200–9,600 for two-week stays. As destination marketers pivot from sightseeing to preventive health, Ayurveda centers capture a rising share of discretionary travel budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly fragmented provider base; limited standardization | -1.5% | India, Southeast Asia, East Africa | Medium term (2-4 years) |

| Sparse high-quality clinical evidence for many indications | -1.2% | Global; acute in North America, Europe, GCC | Long term (≥ 4 years) |

| Insurance coverage outside India remains limited | -1.3% | North America, Europe, GCC, South America | Long term (≥ 4 years) |

| Accreditation costs and compliance burden for small centers | -1.0% | India, Southeast Asia, emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Highly Fragmented Provider Base and Limited Standardization

India’s 3,844 hospitals and 36,848 dispensaries vary widely in lineage, therapeutic philosophy, and record-keeping practices. Just 52 of 167 government-supported integrated hospitals were operational in 2025, amplifying supply bottlenecks. Without uniform clinical protocols, insurers face unpredictable costs, and adverse events at poorly regulated clinics risk reputational contagion. Although accreditation drives consolidation, epistemological resistance to protocolization slows harmonization. The fragmentation trims growth by steering complex cases to a handful of premium centers, leaving smaller outlets with low-margin acute care.

Sparse High-Quality Clinical Evidence for Many Indications

Randomized trials show Panchakarma can lower HbA1c and blood pressure, yet evidence remains thin for claims on anti-aging, fertility, and chronic fatigue. International insurers demand meta-analyses before reimbursing, and sample sizes across studies remain small. New Ayurinformatics hubs and AI-enabled reverse pharmacology are generating molecular data, but translating discoveries into peer-reviewed guidelines requires sustained funding. Until stronger evidence underpins a broader indication portfolio, reimbursement will stay narrow, and self-pay volumes will dominate outside India.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Facility Type: Wellness Retreats Outpace Clinical Facilities

In 2025, Panchakarma day-care centers generated 45.12% of facility revenue because their 90- to 120-minute therapies fit neatly into insurance rules and the busy schedules of urban patients. Still, the fastest growth is expected from wellness retreats and resorts, which are projected to expand at a 23.14% CAGR through 2031 as affluent travelers pay USD 6,000–12,000 for two-week packages that blend detox treatments with yoga, meditation, and sattvic meals. This split shows two clear strategies. Day-care centers, typified by Apollo AyurVAID’s plan to scale from 285 beds in 2024 to 1,000 beds by 2028, focus on high patient volumes and low per-visit costs while maintaining clinical outcomes for conditions such as osteoarthritis and metabolic syndrome on par with those of longer stays.

Full-service Ayurveda hospitals account for a notable share of revenue, mainly treating complex cases that need 14- to 28-day supervision; Patanjali Yogpeeth’s new 250-bed integrated hospital shows how critical-care units and Ayurveda can work together in post-acute rehabilitation. Stand-alone outpatient clinics hold a modest share and feel pressure as insurers steer patients toward accredited networks, pushing smaller operators toward niches such as ophthalmology—the focus of Sreedhareeyam’s 22-center eye-care chain.

By Service Line: Aesthetic Wellness Disrupts the Traditional Mix

Routine OPD consultations and medicine sales accounted for 52.34% of service revenue in 2025, with first visits priced at INR 500–2,000 (USD 5.28–21.13) and follow-ups at INR 300–800 (USD 3.17–8.45), yet margins remain slim unless patients upgrade to longer programs. The standout growth, however, will come from wellness and aesthetic programs, forecast to grow at a 24.15% CAGR through 2031, as urban millennials seek short, seven- to ten-day packages focused on weight control, skin care, and stress relief that marry Ayurvedic methods with modern spa touches.

Panchakarma detox programs still represent notable share of revenue and will grow at a healthy CAGR as insurers increasingly reimburse structured, doctor-led protocols; Somatheeram’s 14-night package, priced at USD 6,202–9,618, shows what patients will pay when the treatment is pitched as medical rather than spa therapy.

Geography Analysis

Asia-Pacific generated 79.02% of the Ayurveda centers market revenue in 2025 and will compound at 22.13% through 2031. India’s 2026 budget allocation of INR 45,000 million (USD 475.5 million) for three new All India Institutes of Ayurveda and five regional hubs bolsters supply, while Kerala hosts more than 250 NABH-accredited institutions that act as magnets for medical tourists. Sri Lanka complements GMP-certified resorts that export to 40+ countries and report the majority of Panchakarma uptake among foreign guests. China and Japan currently restrict Ayurveda to urban spas, but bilateral recognition talks could unlock scaled growth post-2027. Australia’s stringent therapeutic-goods rules hinder rapid expansion yet open differentiated opportunities for evidence-rich manufacturers.

North America delivers a modest share of global revenue. U.S. wellness spending has climbed significantly each year since 2019, but most Ayurveda centers remain boutique cash-pay clinics, such as The Raj in North Carolina, offering seven-night Panchakarma packages priced at USD 5,500-12,843. Fragmented state licensing limits insurance reimbursement, capping penetration. Canada mirrors this landscape, while Mexico’s nascent offerings serve expatriate demand.

In Europe Germany anchors growth via the ISO 9001-certified European Academy of Ayurveda, providing Master of Science programs and ambulatory detox clinics. The United Kingdom pilots Ayurveda inside the National Health Service for chronic pain, though reimbursement remains research-bound. Southern Europe positions Ayurveda as a spa amenity, and Eastern Europe is an untapped frontier contingent on disposable-income gains.

In Middle East & Africa United Arab Emirates recognized Ayurveda as early as 2002, and Dubai now licenses multiple cashless-enabled clinics. Jeena Sikho Lifecare’s AED 1.53 million (USD 0.42 million) acquisition of Back to Roots Ayurveda targets 223% revenue growth in 2025 by addressing expatriate demand. South Africa and East Africa house small but growing networks driven by diaspora communities. In South America, Brazil and Argentina operate wellness-first centers within tight pharmaceutical regulations. Market expansion depends on bilateral accreditation treaties that are still under negotiation.

Competitive Landscape

The Ayurveda centers market is moderately fragmented: the top 10 players account for a notable share of global revenue. Apollo Hospitals set the consolidation tone by buying a majority stake in AyurVAID for INR 260 million (USD 2.75 million) in 2022 and targeting INR 1,000 million (USD 10.57 million) in revenue by October 2026 through 18 hospitals and integrated referrals. Private equity has funneled USD 3.8 billion into India’s broader wellness sector since 2020, spotlighting Ayurveda for science-backed extensions. Dabur’s INR 32,000 million (USD 338.11 million) purchase of Sesa Care illustrates incumbents’ willingness to pay premiums for heritage brands with omnichannel reach.

Accreditation and digital infrastructure now differentiate leaders. CGH Earth Ayurveda’s NABH-certified facilities command 30-50% pricing premiums owing to structured protocols and post-stay follow-ups. Technology adoption lags; only over one-third of hospitals maintain electronic health records, gifting first-mover advantage to chains integrating Ayush Grid and teleconsultation platforms like eSanjeevani, which has crossed 276 million nationwide consults.

Ayurveda Centers Industry Leaders

Patanjali Yogpeeth

Arya Vaidya Sala

Sri Sri Tattva

Vaidyaratnam Oushadhasala

Apollo Hospitals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Patanjali Yogpeeth inaugurated a 250-bed integrated hospital in Haridwar combining Ayurveda with catheterization labs, neurosurgery, and intensive care.

- January 2026: Jeena Sikho Lifecare approved the 51% acquisition of Back to Roots Ayurveda in Abu Dhabi for AED 1.53 million (USD 0.42 million) to accelerate Gulf expansion.

- November 2025: Apollo AyurVAID opened a 35-bed Chennai facility, raising its network to eight hospitals and four treatment centers with a 1,000-bed target by 2028.

Global Ayurveda Centers Market Report Scope

As per the scope of the report, ayurveda Centers are healthcare facilities dedicated to the practice and promotion of Ayurveda, the traditional system of medicine that originated in India. These centers offer treatments, therapies, consultations, and wellness programs based on Ayurvedic principles to promote health, balance, and holistic well-being.

The segmentation for the ayurveda centers market by facility type includes standalone outpatient clinics, Ayurveda hospitals (inpatient department), Panchakarma day-care centers, wellness retreats and resorts, and additional facilities. By service line, the segmentation covers outpatient consultations and medications, Panchakarma detoxification and rejuvenation programs, management of chronic diseases and rehabilitation, wellness and aesthetic programs, and other services. By Geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Standalone OP Clinics |

| Ayurveda Hospitals (IPD) |

| Panchakarma Day-Care Centres |

| Wellness Retreats/Resorts |

| Other Facilities |

| OPD Consultations & Medicines |

| Panchakarma Detox/Rejuvenation Programs |

| Chronic Disease Management & Rehabilitation |

| Wellness/Aesthetic Programs |

| Other Service Lines |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Facility Type | Standalone OP Clinics | |

| Ayurveda Hospitals (IPD) | ||

| Panchakarma Day-Care Centres | ||

| Wellness Retreats/Resorts | ||

| Other Facilities | ||

| By Service Line | OPD Consultations & Medicines | |

| Panchakarma Detox/Rejuvenation Programs | ||

| Chronic Disease Management & Rehabilitation | ||

| Wellness/Aesthetic Programs | ||

| Other Service Lines | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Ayurveda centers market in 2031?

It is forecast to reach USD 72.73 billion by 2031.

Which region generates the highest revenue for Ayurveda centers?

Asia-Pacific contributed 79.02% of global revenue in 2025 and continues to dominate.

Which facility type currently holds the largest share of the Ayurveda centers market?

Panchakarma Day-Care Centres led with 45.12% revenue share in 2025.

What driver is accelerating insurance adoption for Ayurvedic treatments?

The IRDAI’s 2024 parity directive mandates equal coverage for AYUSH therapies.

Page last updated on: