Complementary And Alternative Medicines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

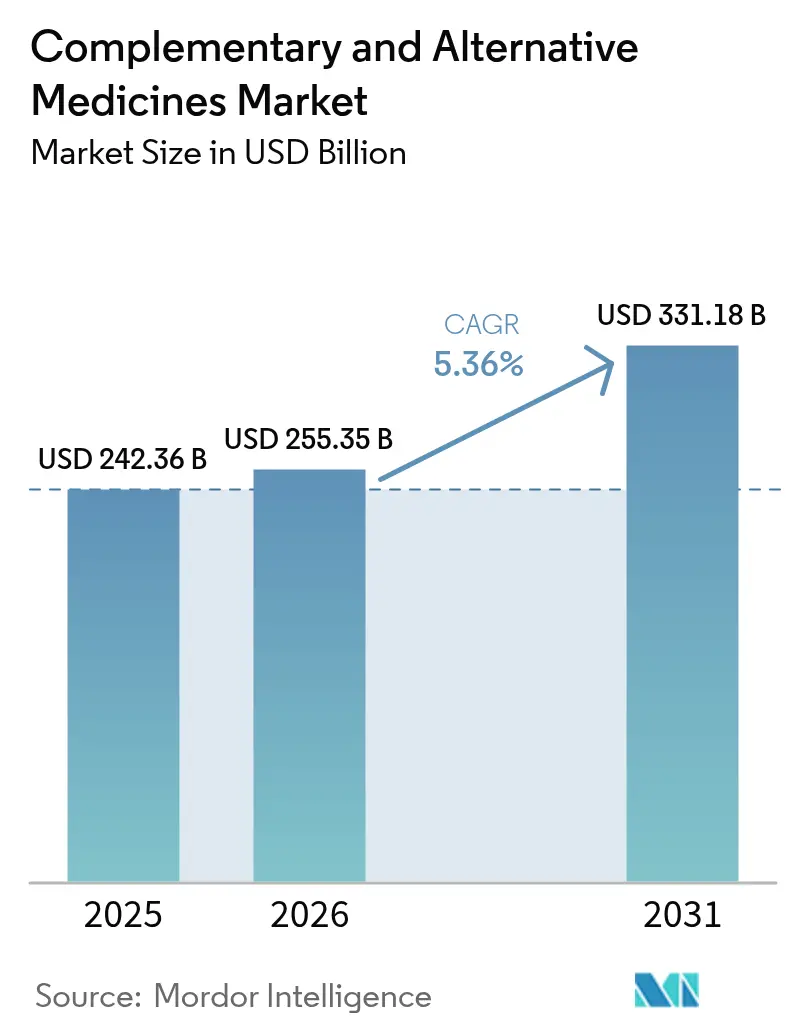

| Market Size (2026) | USD 255.35 Billion |

| Market Size (2031) | USD 331.18 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

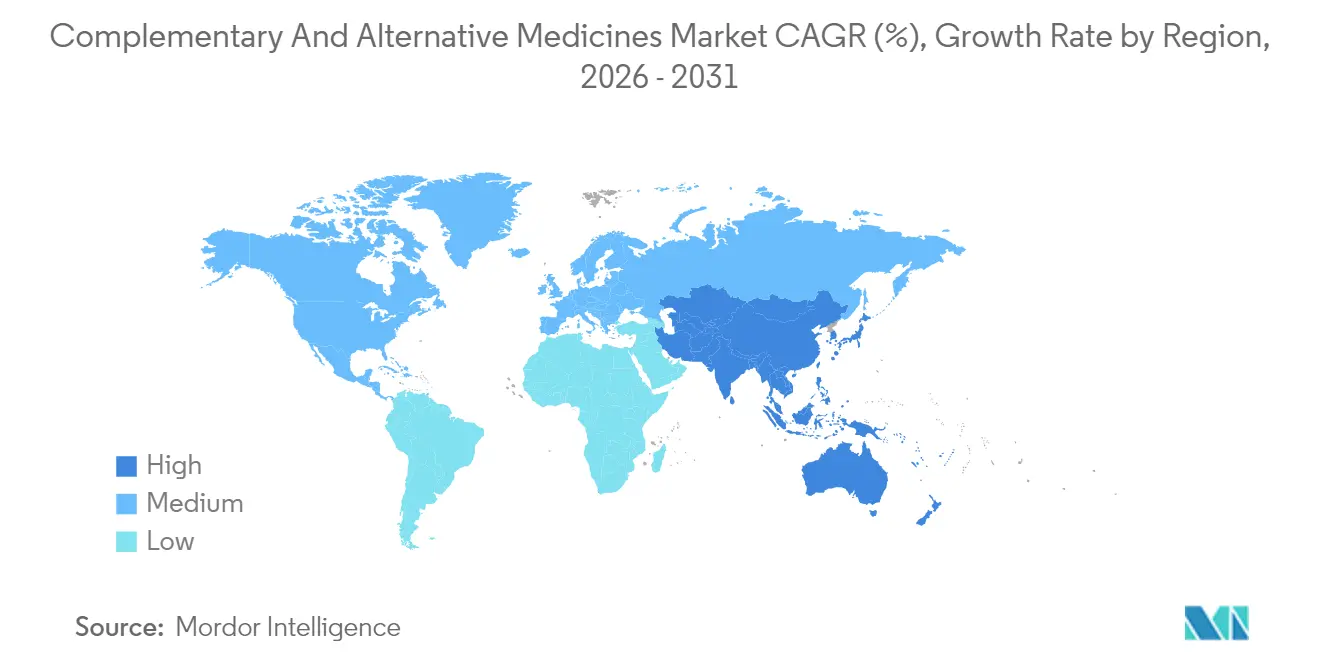

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Complementary And Alternative Medicines Market Analysis by Mordor Intelligence

The complementary and alternative medicines market size was valued at USD 242.36 billion in 2025 and estimated to grow from USD 255.35 billion in 2026 to reach USD 331.18 billion by 2031, at a CAGR of 5.36% during the forecast period (2026-2031). Rising chronic disease prevalence, digitization of practitioner services, stronger insurance reimbursement, and expanding regulatory recognition collectively accelerate revenue growth. Employer benefit plans that repay employees for acupuncture and meditation, such as the USD 300 annual reimbursement from Blue Cross Blue Shield of Massachusetts, illustrate how corporate wellness programs mainstream mind–body care. Simultaneously, the U.S. FDA increases botanical drug oversight while describing streamlined pathways for novel herbal products. Strengthening supply-chain digitization in Asia–Pacific, coupled with targeted cultivation subsidies for medicinal plants, further broadens access and lowers costs. The complementary and alternative medicines market now presents a scalable convergence of ancient therapeutics with modern distribution, analytics, and clinical evidence generation.

Key Report Takeaways

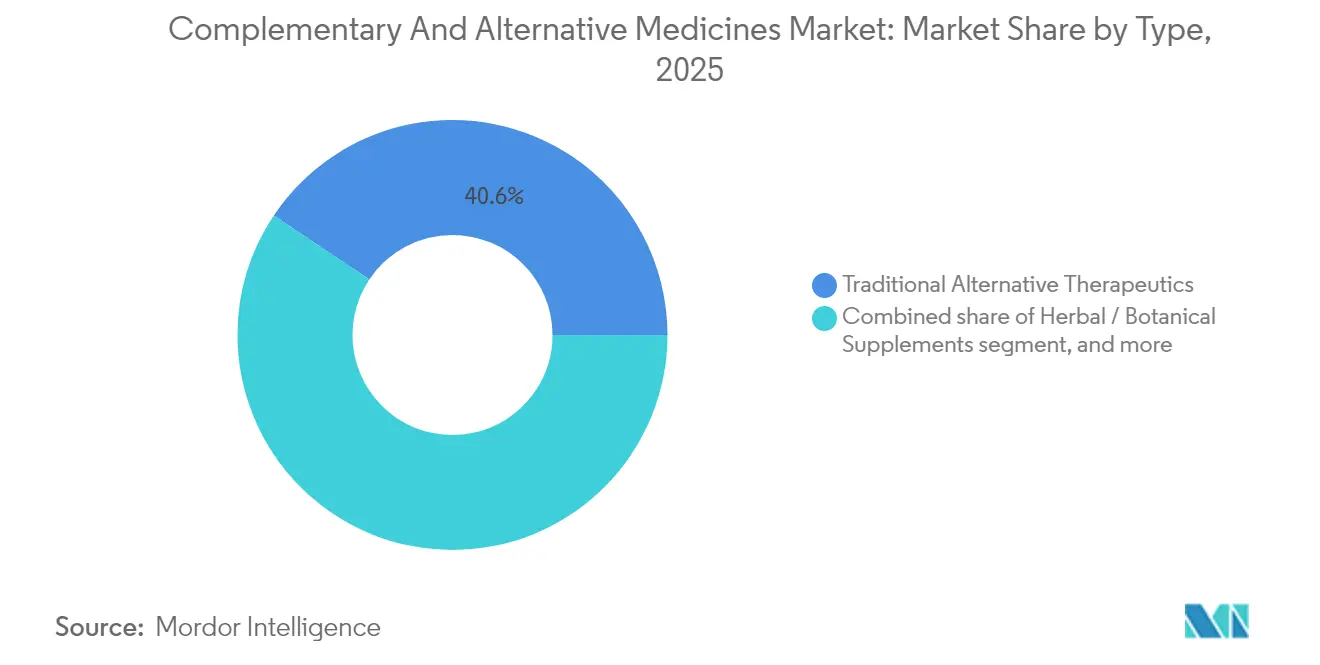

- By type, traditional alternative therapeutics led with 40.62% revenue share in 2025, while Mind & Body Practices is projected to post a 7.12% CAGR through 2031.

- By application, metabolic disorders accounted for 27.08% of the complementary and alternative medicines market share in 2025; neurology & mental health is forecast to expand at a 7.68% CAGR to 2031.

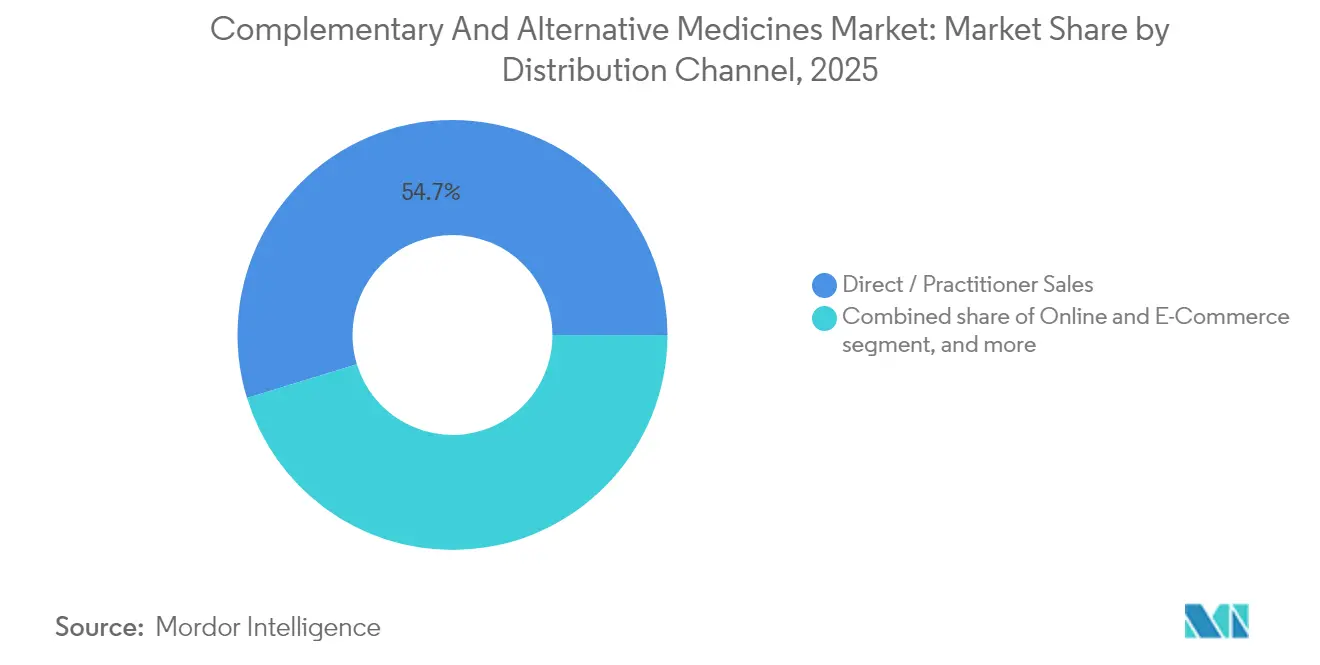

- By distribution channel, direct/practitioner sales held 54.74% of the complementary and alternative medicines market size in 2025; online & e-commerce is advancing at an 8.35% CAGR through 2031.

- By end user, hospitals & specialty clinics captured 44.81% of 2025 revenue, whereas homecare & self-care is projected to grow at an 8.06% CAGR between 2026 and 2031.

- By geography, North America dominated with 42.58% revenue share in 2025, while Asia–Pacific is poised for the fastest 6.32% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Complementary And Alternative Medicines Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic diseases | +1.2% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Rising consumer shift toward natural and organic healthcare | +1.5% | Global, led by developed markets | Medium term (2-4 years) |

| Expanding government support and regulatory recognition | +0.8% | Core APAC, spill-over to MEA | Long term (≥ 4 years) |

| Proliferation of digital CAM platforms and virtual wellness ecosystems | +1.1% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Integration of CAM into corporate wellness and insurance programs | +0.6% | North America & EU | Medium term (2-4 years) |

| Globalization of traditional medicine supply chains through e-commerce | +0.9% | Global, strongest impact in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic Diseases

Chronic metabolic disorders drive sustained patient demand for cost-effective preventive care. Diabetes and obesity heighten worldwide health-care expenses, positioning traditional Chinese medicine, Ayurveda, and evidence-based herbal nutraceuticals as attractive adjuncts to conventional treatment. Americans already spend USD 30.2 billion out-of-pocket each year on complementary modalities, underscoring a mature pay-for-wellness culture[1]National Center for Complementary and Integrative Health, “Complementary Health Approaches: Consumer Spending,” nccih.nih.gov. Large hospital systems, including Penn Medicine HealthWorks, offer acupuncture and therapeutic massage to employees to manage musculoskeletal pain and stress. Such initiatives elevate practitioner credibility and encourage insurers to expand coverage. As metabolic disorders remain a leading global disease burden beyond 2030, their intersection with affordable herbal and mind–body interventions materially supports a rising complementary and alternative medicines market trajectory.

Rising Consumer Shift Toward Natural and Organic Healthcare

Post-COVID consumers actively seek chemical-free, transparent, and minimally processed remedies. Brands highlighting whole-plant extracts, such as Zenko’s performance-oriented Ayurvedic supplements, build loyalty by validating purity and traceability. McKinsey reports that 82% of U.S. adults now prioritize wellness, revealing a structural change in purchase behavior. Demand is strongest in women’s health, where end-to-end ingredient disclosure influences buying decisions from menstruation to menopause support. Corporate benefit platforms respond by subsidizing certified organic mind–body programs, thereby fortifying institutional pathways for natural remedies. These consumer expectations reinforce premium pricing and expand the complementary and alternative medicines market.

Expanding Government Support and Regulatory Recognition

The WHO inserted Traditional Chinese Medicine diagnostic codes into ICD-11, legitimizing centuries-old protocols in official mortality and morbidity statistics. India’s National Medicinal Plants Board scales cultivation grants for high-demand botanicals to assure raw material quality, while the European Union’s Traditional Herbal Medicinal Products Directive offers a fast-track registration for time-tested formulas[2]Frontiers in Medical Technology, “European Herbal Market Projections,” frontiersin.org. Although regional implementation varies, these statutes create legal clarity that encourages cross-border investment. Multinational pharmaceutical firms now pilot traditional formulations under botanical drug pathways, responding to the FDA’s updated guidance on new dietary ingredient notifications. Enhanced oversight balances safety with innovation, supporting long-term legitimacy and expansion of the complementary and alternative medicines market.

Proliferation of Digital CAM Platforms and Virtual Wellness Ecosystems

Telemedicine enables qualified acupuncturists, naturopaths, and Ayurvedic physicians to consult worldwide, accelerating revenue without geographic limits. Artificial-intelligence-assisted tongue and pulse analysis raises diagnostic accuracy in Traditional Chinese Medicine, increasing patient confidence. Meditation apps monetizing subscription models anticipate a 21.44% CAGR by 2032, delivering low-cost, high-engagement mind–body content. Supply-chain digitization also streamlines cross-border herbal commerce, with China importing USD 7.75 billion worth of health foods through e-commerce in 2024. Digital acceleration shortens therapy discovery cycles and expands practitioner reach, sustaining momentum for the complementary and alternative medicines market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Insufficient clinical evidence and standardization | -1.8% | Global, particularly developed markets | Long term (≥ 4 years) |

| Regulatory fragmentation and reimbursement gaps | -1.2% | Global, highest impact in emerging markets | Medium term (2-4 years) |

| Sustainability concerns for medicinal herb resources | -0.7% | Global, with acute pressure in high-export APAC regions | Long term (≥ 4 years) |

| Quality control challenges in cross-border e-commerce distribution | -0.6% | Global, most pronounced in APAC-to-EU/US trade | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Insufficient Clinical Evidence and Standardization

Worldwide funding for rigorous CAM trials remains limited; in 2022, only 0.17% of U.S. NIH grants targeted integrative medicine. Botanical preparations often vary by origin, harvest date, and processing, complicating reproducibility and hindering FDA approval beyond the two currently licensed prescription botanicals. The lack of consistent pharmacopoeia grades restricts broad insurance coverage because payers favor standardized dosage forms. Practitioner education gaps further slow adoption, as many physicians remain cautious about potential herb-drug interactions. Without expanded randomized controlled trials and harmonized quality benchmarks, uncertainty could slow uptake in high-income regions and temper the complementary and alternative medicines market size narrative.

Regulatory Fragmentation and Reimbursement Gaps

Ayurvedic capsules enter the United States as dietary supplements, while India treats identical ingredients as prescription therapies, forcing global brands to juggle conflicting dosage and labeling rules[3]U.S. Food and Drug Administration, “Botanical Drug Development Guidance,” fda.gov. Europe’s unified directive exists, yet national agencies interpret documentation requirements differently, delaying pan-EU launches. Out-of-pocket payments still dominate despite broader acceptance, with U.S. consumers paying USD 30.2 billion annually for CAM services. Cross-border e-commerce magnifies oversight challenges in product authentication, heavy-metal limits, and contamination screening. Fragmentation raises compliance costs and may deter small innovators from scaling, moderating near-term growth of the complementary and alternative medicines market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Traditional Therapies Lead Digital Innovation

Traditional Alternative Therapeutics retained leadership with 40.62% of 2025 revenue, driven by hospital integration of acupuncture, Ayurveda, homeopathy, and herbal pharmacopeias. Institutional endorsement—including Mitsui’s SGD 800 million purchase of Eu Yan Sang—signals investor belief in scalable heritage brands. High clinical familiarity positions these modalities as the cornerstone of the complementary and alternative medicines market, even as AI-powered diagnostic software modernizes delivery. Mind & Body Practices, though smaller, is the fastest-growing sub-sector at a projected 7.12% CAGR. Corporate wellness platforms that reimburse yoga and meditation training accelerate mainstream adoption and increase lifetime user value. Herbal supplements rise on the back of good-agricultural-practice certifications, while chiropractors benefit from insurance coverage at 87% of large U.S. firms. Energy & Biofield modalities remain niche but draw research attention for chronic pain relief. Continued digitization improves transparency and personalized intervention, reinforcing segment synergies.

The complementary and alternative medicines market size for Mind & Body Practices is expected to surpass USD 92.4 billion by 2031, reflecting compound growth and consumer loyalty to habit-forming digital programs. Remote mindfulness sessions reduce overhead for practitioners and maintain continuity during mobility restrictions. In traditional therapeutics, partnerships with biopharmaceutical manufacturers are expanding to co-develop botanical derivatives for oncology and immunology support. Market entrants that integrate smartphone analytics with tongue imaging or pulse variation tracking can deliver differentiated clinical dashboards, expanding the complementary and alternative medicines market footprint in evidence-seeking health systems.

By Application: Metabolic Disorders Drive Clinical Integration

Metabolic disorders commanded 27.08% revenue share in 2025, underscoring how diet-linked diseases heighten demand for safe, multi-target botanical solutions. Controlled trials in Indian populations show that fenugreek, cinnamon, and gymnema extracts reduce fasting glucose and improve lipid profiles, strengthening physician confidence. Neurology & Mental Health leads future expansion with a 7.68% CAGR through 2031, as pandemic-related stress catalyzes demand for adaptogenic herbs and mindfulness training reimbursed by employers. Oncology support therapies benefit from randomized evidence that traditional Chinese formulas reduce chemotherapy-induced fatigue, promoting their inclusion in integrative cancer clinics. The complementary and alternative medicines market size devoted to oncology is forecast to grow steadily as patient advocacy groups lobby for symptom management options.

Cardiovascular applications evolve alongside preventive health programs that incorporate traditional breathing exercises and therapeutic massage, offering cost-effective blood-pressure control. Women’s health remains a high-growth niche driven by phytoestrogenic herbs that mitigate menopausal discomfort without synthetic hormones. The complementary and alternative medicines market share in women’s health is projected to widen as life-science companies launch age-specific nutraceutical packs with clinical backing. Across all applications, digital adherence tools and wearable integration showcase measurable health outcomes, deepening payer engagement.

By Distribution Channel: Digital Transformation Reshapes Access

Direct/practitioner sales accounted for 54.74% of 2025 revenue, confirming that face-to-face consultations and personalized decoction prescriptions remain the backbone of patient trust. Homeopathy pharmacies, Ayurvedic clinics, and acupuncture centers collectively drive refill frequency and data-rich case histories. Meanwhile, online & e-commerce is projected to register an 8.35% CAGR from 2026 to 2031, propelled by cross-border marketplaces that extend product portfolios far beyond local inventories. The complementary and alternative medicines market size attributable to online channels is projected to exceed USD 103.6 billion by the decade’s end, even as regulators intensify surveillance of imported botanicals.

Pharmacies and drugstores expand shelf space for clinically substantiated natural products, integrating QR-code-linked monographs for on-the-spot education. Mail-order programs bridge rural gaps where practitioners are scarce, ensuring continuity of chronic care. Leading brands now blend subscription shipments with virtual coaching, creating integrated experiences that enhance treatment adherence. Omnichannel strategies improve inventory turnover and enable agile consumer feedback loops, broadening the complementary and alternative medicines market reach across demographic cohorts.

By End User: Healthcare Integration Accelerates Adoption

Hospitals and specialty clinics captured 44.81% of 2025 revenue, reflecting physician acceptance of acupuncture, naturopathy, and medical herbalism in multimodal care plans. Academic medical centers create integrative departments that publish outcomes data, legitimizing traditional interventions among skeptical clinicians. Homecare & Self-Care is forecast to grow at an 8.06% CAGR, pushed by wearable-enabled monitoring, smartphone dosing reminders, and on-demand virtual consultations with licensed practitioners. Consumers already spend USD 12.8 billion annually on natural products for self-care, illustrating a preference for autonomy in daily health management.

Wellness centers and spas rebrand as preventive health hubs, offering medical oversight alongside relaxation services to capture value-conscious millennials. Corporate wellness programs integrate digital vouchers for CAM services, driving sustained volumes across providers. The complementary and alternative medicines market share commanded by corporate wellness networks will expand as employers quantify productivity improvements and healthcare cost offsets. This confluence of clinical, residential, and lifestyle delivery sites underpins robust demand diversification and encourages further research investment.

Geography Analysis

North America remained the largest regional contributor, holding 42.58% of 2025 revenue. Mature reimbursement mechanisms, robust practitioner infrastructure, and proactive corporate wellness investments fueled demand. Hospitals embed integrative oncology and chronic pain protocols, enabling higher throughput of herbal prescriptions and mind–body therapies. The complementary and alternative medicines market size in the United States is poised to climb steadily as insurers refine outcome-based payment models and as the FDA widens botanical guidance. Canadian provinces likewise expand acupuncture coverage within public insurance, signaling convergent policy momentum.

Asia–Pacific is projected to post the fastest 6.32% CAGR from 2026 to 2031. China’s dual strategy of strengthening domestic usage and accelerating export certification supports scale economies. Baidyanath’s launch of 27 nutraceutical SKUs targeting 10–12 countries evidences regional ambitions to command global shelf space. India’s cultivation subsidies reduce raw material costs and improve traceability, meeting stringent import standards in Europe and North America. Cross-border e-commerce drives demand in Southeast Asian metros, where smartphone penetration exceeds 80% and health-app usage intersects with local payment wallets. Government-funded tele-Ayurveda pilots in rural India reinforce adoption by demonstrating low-cost consultation viability.

Europe benefits from the Traditional Herbal Medicinal Products Directive, providing market entry clarity that attracts foreign investment. Germany ranks as the second-largest exporter of health foods to China, with 2024 shipments rising 57.84% to USD 1.165 billion. European consumers favor plant-based remedies for chronic musculoskeletal disorders, spurring collaboration between pharmacists and herbalists. National health systems in Italy and the Netherlands investigate cost-saving potential of reimbursing CAM for chronic migraine and irritable bowel syndrome, respectively. The complementary and alternative medicines market continues to deepen its European footprint as clinical trial outputs trigger evidence-based policy inclusion.

Competitive Landscape

The market is moderately concentrated in nature with the increasing investment in the area and growing awareness among the general population, the competition in the market is increasing. However, the complementary and alternative medicines market is fragmented, with many players. Some key players in the studied market are Ayush Ayurvedic Pte Ltd., Columbia Nutritional LLC, The Healing Company Ltd., Pure encapsulations, LLC, and Herb Pharm, among others.

Complementary And Alternative Medicines Industry Leaders

Columbia Nutritional LLC

Pure encapsulations, LLC

Herb Pharm

Healing Company Ltd

Ayush Ayurvedic Pte Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Barentz acquired China’s Fengli Group to boost participation in the Chinese pharmaceuticals and nutraceuticals supply chain and capture Asia–Pacific demand.

- May 2025: Baidyanath introduced its global nutraceutical brand Siddhayu at Vitafoods Europe 2025, unveiling 27 clinically substantiated products for men’s and women’s health with plans to enter 10–12 countries within six months.

- April 2025: The U.S. FDA released updated procedures for new dietary ingredient notifications, clarifying electronic submission protocols for innovative herbal products.

- February 2025: Several California start-ups—including Healy Lab, Christara, and MyHerbPharm—launched personalized digital herbal platforms targeting younger demographics.

- December 2024: The FDA India Office expanded training on Good Agricultural and Manufacturing Practices for herbal exporters to the United States, addressing heavy-metal contamination concerns.

Global Complementary And Alternative Medicines Market Report Scope

As per the scope of the report, the medical items and practices that are not considered part of conventional or mainstream medical therapy are referred to as complementary and alternative medicine (CAM). It combines self-administered items and activities such as herbal medications, homeopathic remedies, dietary supplements, yoga, chiropractic, massage therapy, and acupuncture. Manipulative and body-based therapies, biofield therapy, and entire medical systems are all included. The Complementary and Alternative Medicines Market is Segmented by Type (Traditional Alternative Therapeutics, Body Therapy, Mind Therapy, Sensory Therapy, and Other Types), Application (Arthritis, Cancer, Diabetes, Cardiovascular, Neurology, and Other Applications), Distribution Channel (Direct Sales, Online Sales, and Distance Correspondence), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD million) for the above segments.

| Traditional Alternative Therapeutics (Ayurveda, Tcm, Homeopathy) |

| Herbal / Botanical Supplements |

| Mind & Body Practices (Yoga, Meditation, Tai-Chi) |

| Body-Based Therapies (Chiropractic, Massage) |

| Energy & Biofield Therapies (Reiki, Quantum-Touch) |

| Arthritis & Musculoskeletal |

| Oncology Support |

| Metabolic Disorders (Diabetes, Obesity) |

| Cardiovascular |

| Neurology & Mental Health |

| Women's Health & Fertility |

| Other Applications |

| Direct / Practitioner Sales |

| Online & E-Commerce |

| Pharmacies & Drug Stores |

| Distance Correspondence / Mail Order |

| Hospitals & Specialty Clinics |

| Wellness Centers & Spas |

| Homecare & Self-Care |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Traditional Alternative Therapeutics (Ayurveda, Tcm, Homeopathy) | |

| Herbal / Botanical Supplements | ||

| Mind & Body Practices (Yoga, Meditation, Tai-Chi) | ||

| Body-Based Therapies (Chiropractic, Massage) | ||

| Energy & Biofield Therapies (Reiki, Quantum-Touch) | ||

| By Application | Arthritis & Musculoskeletal | |

| Oncology Support | ||

| Metabolic Disorders (Diabetes, Obesity) | ||

| Cardiovascular | ||

| Neurology & Mental Health | ||

| Women's Health & Fertility | ||

| Other Applications | ||

| By Distribution Channel | Direct / Practitioner Sales | |

| Online & E-Commerce | ||

| Pharmacies & Drug Stores | ||

| Distance Correspondence / Mail Order | ||

| By End User | Hospitals & Specialty Clinics | |

| Wellness Centers & Spas | ||

| Homecare & Self-Care | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the complementary and alternative medicines market?

The market stands at USD 255.35 billion in 2026 and is forecast to reach USD 331.18 billion by 2031.

Which segment is growing fastest within the complementary and alternative medicines market?

Mind & Body Practices is projected to grow at a 7.12% CAGR, fueled by corporate wellness demand and digital meditation apps.

How much of the complementary and alternative medicines market share does North America hold?

North America accounted for 42.58% of global revenue in 2025.

Why is Asia–Pacific considered the high-growth region?

Government support, expansive e-commerce, and digitized supply chains are expected to drive a 6.32% CAGR in Asia–Pacific from 2026 to 2031.

What are the main barriers to wider adoption of complementary and alternative medicines?

Limited large-scale clinical trials, inconsistent global regulations, and variable insurance reimbursement remain the key challenges.

Which distribution channel is expanding most rapidly?

Online & e-commerce sales are forecast to post an 8.35% CAGR, reflecting consumer comfort with virtual consultations and cross-border shopping.

Page last updated on: