India AYUSH And Alternative Medicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

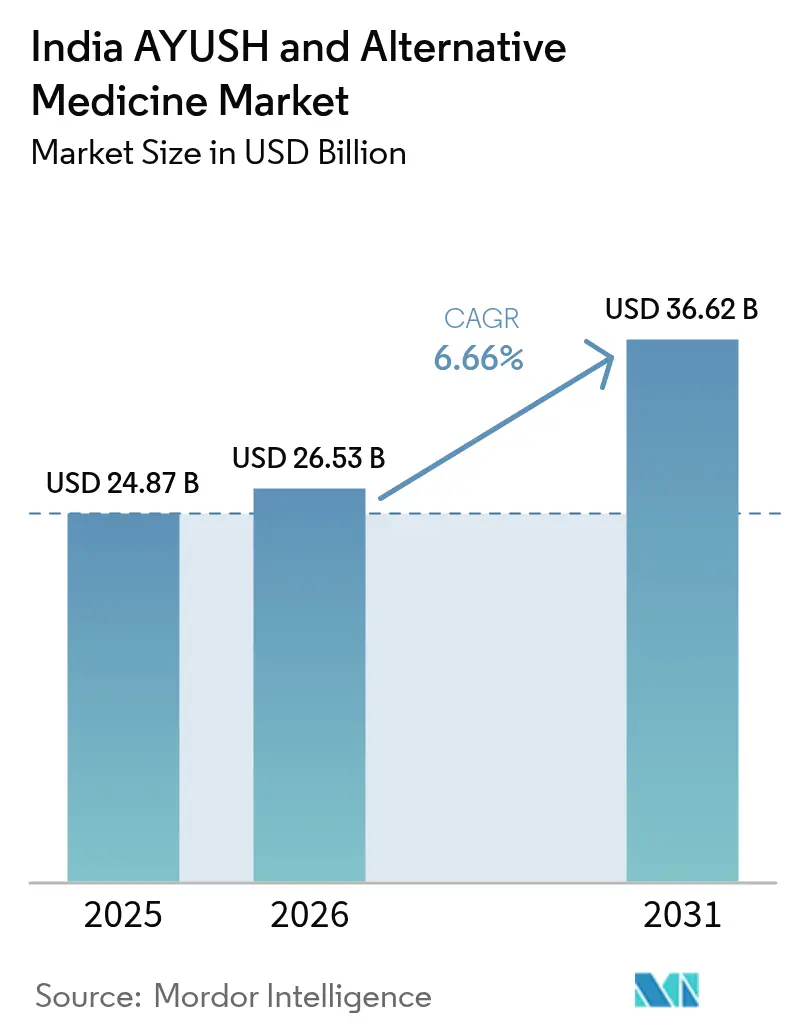

| Base Year Market Size (2025) | USD 24.87 Billion |

| Market Size (2026) | USD 26.53 Billion |

| Market Size (2031) | USD 36.62 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India AYUSH And Alternative Medicine Market Analysis by Mordor Intelligence

The India AYUSH and Alternative Medicine market size is expected to grow from USD 24.87 billion in 2025 to USD 26.53 billion in 2026 and is forecast to reach USD 36.62 billion by 2031 at 6.66% CAGR over 2026-2031. The mid-single-digit growth reflects the sector’s rapid alignment with modern insurance frameworks, production incentives, and digital distribution channels. Government directives mandating AYUSH coverage under all retail and public health plans remove the affordability barrier for nearly 400 million potential policyholders, while a USD 288 million Production Linked Incentive (PLI) scheme secures herb supplies and stabilizes prices. Global credibility rises after the World Health Organization (WHO) opened its Global Centre for Traditional Medicine (GCTM) in Jamnagar, positioning India as a scientific hub for validated traditional therapies. Simultaneously, e-commerce penetration crossed 25% of sector sales in 2024, catalyzing direct-to-consumer competition, QR-based product authentication, and AI-enabled dosage personalization. Companies with GMP-compliant plants leverage these shifts to capture premium demand, yet the market remains fragmented, creating ample room for consolidation and niche expansion.

Key Report Takeaways

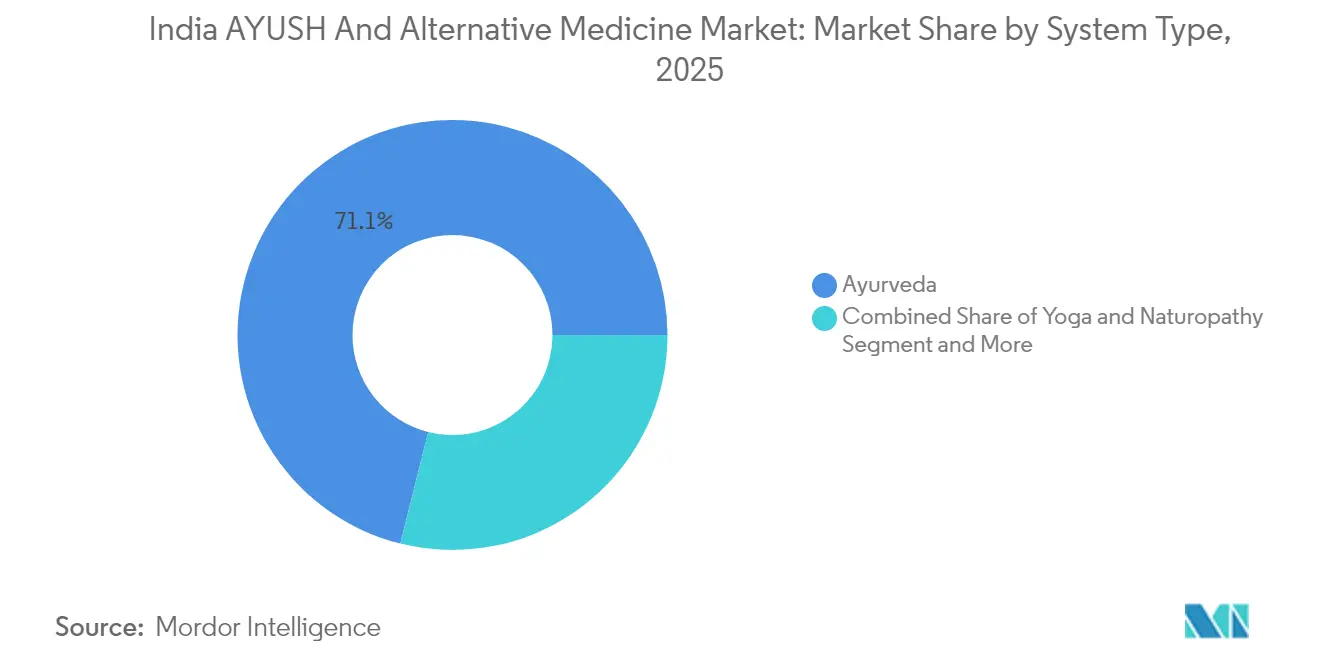

- By system type, Ayurveda led with 71.10% revenue share in 2025; Yoga & Naturopathy is projected to expand at a 14.79% CAGR through 2031.

- By product category, Classical Medicines held 37.20% of the India AYUSH and Alternative Medicine market share in 2025, while Personal-Care & Cosmeceuticals is forecast to advance at a 10.63% CAGR to 2031.

- By form, Tablets & Capsules commanded 45.10% of the India AYUSH and Alternative Medicine market size in 2025, whereas Patches & Topicals post the fastest 12.62% CAGR to 2031.

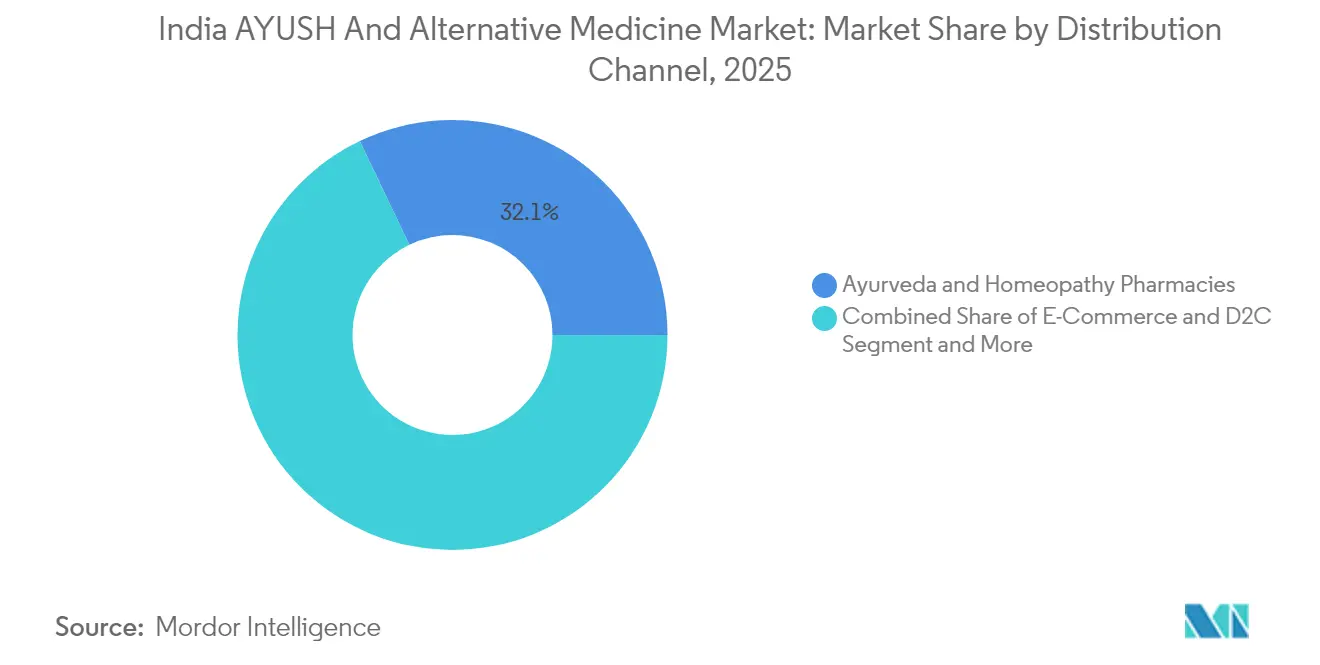

- By distribution channel, Ayurveda & Homeopathy pharmacies accounted for 32.10% of the India AYUSH and Alternative Medicine market share in 2025; e-commerce & D2C platforms are climbing at a 15.68% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India AYUSH And Alternative Medicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government insurance mandate for AYUSH treatments | +1.8% | National, early uptake in metro areas | Short term (≤ 2 years) |

| Accelerated e-commerce & D2C adoption for herbal products | +1.2% | Tier-1 & Tier-2 cities | Medium term (2-4 years) |

| Herbal raw-material PLI subsidy boosts domestic supply | +0.9% | Cultivation states | Long term (≥ 4 years) |

| WHO-GCTM recognition elevates export credibility | +0.7% | Export-oriented regions | Medium term (2-4 years) |

| AI-enabled personalized “Prakriti” formulations | +0.6% | Urban tech-enabled clinics | Long term (≥ 4 years) |

| Tele-AYUSH integration with Ayushman Arogya Mandir network | +0.5% | Rural and semi-urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Insurance Mandate for AYUSH Treatments

The Insurance Regulatory and Development Authority of India mandated in April 2024 that every retail and public health plan reimburse 170 standardized AYUSH therapies, instantly converting previously out-of-pocket spending into claimable benefits. Initial actuarial skepticism eased after pilots in Karnataka and Kerala showed 22% lower average episode costs for chronic diabetes compared with allopathic care. Reimbursement also compels clinics to digitize records, accelerating outcome tracking and quality audits. Organized hospital chains scale faster under the new regime, yet informal practitioners race to upgrade premises and documentation to remain accredited. As a result, policy inclusion is expected to broaden the India AYUSH and Alternative Medicine market by nearly half within two years.

Accelerated E-Commerce & D2C Adoption for Herbal Products

Digital-native consumers now buy classical churnas, cosmeceuticals, and OTC nutraceuticals from branded websites and marketplace storefronts that guarantee QR-based authenticity tags. Direct-to-consumer start-ups exploit social media education campaigns and algorithmic recommendation engines to grow pan-India without costly brick-and-mortar logistics. Established brands, in turn, pivot to omnichannel, integrating in-clinic consult video chats and same-day fulfillment via hyper-local warehouses. While digital outreach lifts unit sales, it also heightens scrutiny; marketplace delistings jump when sellers fail real-time batch-testing audits. Consequently, only manufacturers with transparent supply chains and rapid customer-service loops sustain high ratings and repeat sales.

Herbal Raw-Material PLI Subsidy Boosting Domestic Supply

The National Medicinal Plants Board earmarked INR 2,400 crore in 2024 to co-fund greenhouse irrigation, organic certification, and GPS-enabled farm mapping for 45 cultivars covering 80,000 hectares nationwide[1]National Medicinal Plants Board, “Production Linked Incentive Scheme for Medicinal Plants,” nmpb.nic.in. Import dependence on Chinese licorice and Nepalese kutki has already fallen from 35% in 2023 to 27% in 2025, lowering input price volatility by 18%. Tiered subsidies favor marginalized farmers, which spreads risk geographically and improves climate resilience. Mandatory Good Agricultural and Collection Practices (GACP) audits now feed directly into blockchain ledgers demanded by leading exporters, creating a credible farm-to-vial trail that underpins export growth.

WHO-GCTM Recognition Elevates Export Credibility

WHO’s Global Centre for Traditional Medicine inaugurated in Jamnagar in late-2024 delivers globally accepted lab protocols for safety, pharmacovigilance, and efficacy, shrinking dossier approval times in the European Union and United States. Post-recognition, Indian finished-dose herbal exports climbed 14% in 2025, with ashwagandha capsules and turmeric curcumin extracts leading shipments. Joint translational research with American and Japanese universities opens the door to co-developed botanical drugs eligible for fast-track review. Enhanced credibility helps premium Ayurveda resorts in Kerala and Goa attract wellness tourists seeking physician-curated detox programs reimbursable by international insurers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited GMP compliance among MSME manufacturers | -1.1% | Traditional manufacturing clusters | Short term (≤ 2 years) |

| Insurance pricing caps compress clinic margins | -0.8% | Urban organized clinics | Medium term (2-4 years) |

| Raw-herb climate-risk supply shocks | -0.6% | Key cultivation belts | Short term (≤ 2 years) |

| Rising global scrutiny on heavy-metal contamination | -0.4% | Export-oriented plants | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited GMP Compliance Among MSME Manufacturers

Roughly 4,200 micro and small units still miss WHO-GMP thresholds for air-handling, in-process validation, and residual solvent testing, prompting multiple deadline extensions to March 2025[2]Drug Controller General of India, “GMP Compliance Guidelines for AYUSH Manufacturers,” cdsco.gov.in. Capital upgrades typically cost USD 60,000-240,000 per site, straining cash flows in a segment where average EBITDA margins hover near 9%. Non-compliance limits access to high-margin export orders and e-commerce platforms that mandate laboratory certificates. As insurers and marketplace portals tighten vendor rosters, sub-scale players face either attrition or acquisition by larger peers in search of incremental capacity.

Insurance Pricing Caps Compress Clinic Margins

Standardized reimbursement rates under Ayushman Bharat cap provider charges for panchakarma, kshar sutra, and leech therapy at levels 18-25% below urban private clinic rack rates. Multi-specialty chains absorb margin pressure by cross-selling proprietary medicines, wellness retreats, and nutraceutical subscriptions. Independent clinics, however, confront reduced earnings and may downscale or exit high-rent metros. Over time, market equilibrium will likely favor integrated delivery networks with diversified ancillary revenue streams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Ayurveda Dominates While Yoga Wellness Surges

Ayurveda accounted for 71.10% of the India AYUSH and Alternative Medicine market in 2025, supported by 500,000 registered practitioners and a robust educational pipeline of 280 colleges. Yoga & Naturopathy, currently a smaller base, records the swiftest 14.79% CAGR through 2031, propelled by office-based stress disorders and social-media-amplified wellness retreats. Homeopathy maintains around 14.80% share, appealing to pediatric and chronic dermal cases that favor gentle dosing schedules. Unani and Siddha, while niche, leverage concentrated regional loyalty and benefit from tele-consult platforms that transcend geographic confines.

Digitization blurs system boundaries as integrative clinics bundle Ayurveda detox, Yogic breathing, and Homeopathic constitutional remedies under a single subscription. Insurance recognition further legitimizes cross-referrals, expanding each discipline’s patient pool. Nevertheless, Ayurveda’s entrenched pharmacopeia and industry-wide R&D spending ensure its continued dominance, even as newer modalities command media attention.

By Product Category: Classical Medicines Lead, Cosmeceuticals Accelerate

Classical Medicines contributed 37.20% to the India AYUSH and Alternative Medicine market size in 2025, anchored by chronic-disease protocols for joint pain, gastrointestinal issues, and metabolic disorders. Personal-Care & Cosmeceuticals outpace all other segments with a 10.63% CAGR, riding urban demand for natural skin-brightening creams, anti-aging serums, and sulfate-free shampoos. Nutraceuticals & Dietary Supplements garner rising share from lifestyle conditions such as non-alcoholic fatty liver disease, while Proprietary OTC combinations serve first-time herbal users seeking familiar pill formats. Regulatory clarity under the Food Safety and Standards Authority of India tightens label claims and boosts consumer confidence.

Brands increasingly launch cosmeceuticals as gateway offerings, then up-sell therapeutic lines after trust forms. Conversely, companies rooted in classical therapeutics diversify into beauty SKUs to smooth revenue seasonality. Supply-side investments in nano-emulsion and liposomal delivery unlock higher-potency cosmetic actives, blending traditional botanicals with modern cosmeceutical science.

By Form: Tablets Dominate, Topicals Show Innovation

Tablets & Capsules represent 45.10% of the India AYUSH and Alternative Medicine market share in 2025. Shelf-stable and easy to dose, the format suits chronic ailments requiring months-long adherence. Patches & Topicals post a 12.62% CAGR, thanks to transdermal analgesic plasters and herbal sheet masks that resonate with tech-savvy millennials. Oils & Ointments hold cultural cachet in post-partum care and sports massage, while Juices, Syrups, and Powders retain rural loyalty where consumers still prize traditional preparation rituals.

R&D momentum now concentrates on nano-encapsulated actives in dissolvable oral films and bi-layer tablets that phase-release over 12 hours. Manufacturers adopting continuous-manufacture lines achieve 40% lower per-unit costs and superior batch consistency, setting new quality benchmarks.

By Distribution Channel: Digital Transformation Reshapes Access

Ayurveda & Homeopathy pharmacies secured 32.10% of 2025 sales, sustained by in-store consultations and credible sourcing narratives. E-commerce & D2C channels, expanding at a 15.68% CAGR, empower consumers to compare ingredient transparency and third-party lab reports instantly. Modern trade aisles in supermarkets introduce impulse purchases in urban locales, while hospitals integrate in-house dispensaries endorsed by attending surgeons.

Brick-and-click hybrids emerge as the norm; pure-play online brands open flagship clinics for experiential therapies, whereas legacy store chains launch subscription models with auto-replenishment. Data analytics from digital outlets feed directly into new-product ideation, compressing feedback loops and refining packaging iterations in weeks rather than quarters.

Geography Analysis

Northern India leads current value contribution, with Uttar Pradesh and Punjab benefiting from proactive state insurance rollouts and large practitioner bases. Western hubs, notably Gujarat and Maharashtra, capture manufacturing investments spurred by proximity to the WHO-backed GCTM campus and a mature pharmaceutical supply chain. Southern states such as Kerala and Karnataka intertwine medical tourism with classical Panchakarma centers, attracting inbound travelers seeking detox packages now partly reimbursable by overseas insurers. Eastern corridors, including West Bengal and Odisha, show notable uptake through government primary-care centers stocked with AYUSH prescriptions. Across semi-urban districts, Tele-AYUSH connectivity mitigates physician shortages, creating new demand pockets. Rural heartlands adopt herb cultivation programs under the PLI subsidy, stabilizing farmer incomes and anchoring local processing units. Metropolitan metros remain the crucible for premium cosmeceuticals and personalized subscription plans, supplying critical volumes for digital storefronts.

Climate-sensitive hill regions in Uttarakhand diversify into greenhouse Isabgol and saffron cultivation, offsetting volatility from rain-fed crops. Coastal Andhra Pradesh and Tamil Nadu experiment with hydroponic Tulsi and Ashwagandha, leveraging brackish-water resilience. Meanwhile, exporters congregate near Nhava Sheva and Mundra ports, optimizing cold-chain lanes for heat-sensitive extracts. Taken together, these regional contrasts forge a geographically diverse growth matrix that guards the India AYUSH and Alternative Medicine market against localized shocks.

Competitive Landscape

India’s AYUSH sector remains highly fragmented; the top 10 manufacturers collectively control significant domestic sales, leaving ample white space for regional specialists and digital insurgents. Patanjali Ayurved, Dabur India, and Himalaya Wellness retain scale advantages in distribution and advertising, yet face rising competition from e-commerce disruptors like Kapiva and Guduchi. These new entrants prioritize single-ingredient purity, rapid social-media engagement, and transparent lab analytics to capture health-conscious urban cohorts.

Strategic moves in 2025 include Dabur’s blockchain partnership for farm-level traceability and Himalaya’s acquisition of a minority stake in an AI formulation start-up. Simultaneously, regional cooperatives in Kerala pool capital to install shared GMP facilities, elevating smaller brands into export eligibility. Intellectual-property activity accelerates; the Indian Patent Office logged a 40% rise in Ayurveda and plant-based patent filings in 2024 versus 2023, driven by proprietary extraction technologies.

Cross-border alliances multiply as Japanese nutraceutical groups license Indian ashwagandha adaptogen blends, while European spa chains white-label Kerala herbal oils. Fragmentation nonetheless persists because consumer trust hinges on local practitioner endorsements and lineage authenticity. Consolidation is expected primarily in OTC and cosmeceutical verticals where marketing muscle outweighs practitioner gatekeeping.

India AYUSH And Alternative Medicine Industry Leaders

Himalaya Wellness

Baidyanath

Dabur India

Sydler India

Patanjali Ayurved

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Apollo AyurVAID expanded from precision Ayurveda hospitals into a proprietary product line, covering classical formulations, OTC remedies, and medical foods aimed at lifestyle disorders.

- July 2025: Aayush Wellness Limited introduced Brain Fuel Capsules nationally, blending standardized Bacopa monnieri and Shankhpushpi extracts to support memory and focus.

India AYUSH And Alternative Medicine Market Report Scope

AYUSH signifies the combination of an alternative system of medicine, which was earlier known as the Indian system of medicine. AYUSH includes Ayurveda, yoga and naturopathy, Unani, Siddha, and homeopathy. The objective of AYUSH is to promote medical pluralism and to introduce strategies for mainstreaming the indigenous systems of medicine. In India, at the Union Government level, AYUSH activities are coordinated by the Department of AYUSH under the Ministry of Health and Family Welfare. Most of these medical practices originated in India and its neighboring countries and were adopted in India over time. The AYUSH and Alternative Medicine Industry in India is Segmented by type (Ayurvedic medicine, herbal medicine, aroma therapy, homeopathy, acupuncture, and other types). The report offers values in USD million for all the above-mentioned segments.

| Ayurveda |

| Homeopathy |

| Unani |

| Siddha |

| Yoga & Naturopathy |

| Classical Medicines |

| Proprietary / OTC Formulations |

| Nutraceuticals & Dietary Supplements |

| Personal-Care & Cosmeceuticals |

| Others |

| Tablets / Capsules |

| Powders / Churnas |

| Juices / Syrups |

| Oils / Ointments |

| Patches / Topicals |

| Ayurveda & Homeopathy Pharmacies |

| Modern Trade & Supermarkets |

| E-Commerce & D2C |

| Hospitals & Clinics |

| Other Distribution Channels |

| By System Type | Ayurveda |

| Homeopathy | |

| Unani | |

| Siddha | |

| Yoga & Naturopathy | |

| By Product Category | Classical Medicines |

| Proprietary / OTC Formulations | |

| Nutraceuticals & Dietary Supplements | |

| Personal-Care & Cosmeceuticals | |

| Others | |

| By Form | Tablets / Capsules |

| Powders / Churnas | |

| Juices / Syrups | |

| Oils / Ointments | |

| Patches / Topicals | |

| By Distribution Channel | Ayurveda & Homeopathy Pharmacies |

| Modern Trade & Supermarkets | |

| E-Commerce & D2C | |

| Hospitals & Clinics | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the projected value of the India AYUSH and Alternative Medicine market by 2031?

The sector is expected to reach USD 36.62 billion by 2031 on a 6.66% CAGR.

Which system dominates sector revenue today?

Ayurveda leads with a 71.10% share of 2025 sales.

Which product category is expanding fastest?

Personal-Care & Cosmeceuticals are growing at a 10.63% CAGR through 2031.

How is e-commerce shaping distribution?

Online and D2C platforms, rising at a 15.68% CAGR, now compose a quarter of total sector sales.

What policy change has widened insurance access?

In April 2024, the Insurance Regulatory and Development Authority required all health plans to reimburse 170 AYUSH procedures.

Why is WHO-GCTM significant for exports?

The center's global safety and efficacy protocols smooth regulatory approvals abroad, boosting export momentum.

Page last updated on: