Botanical Extracts Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

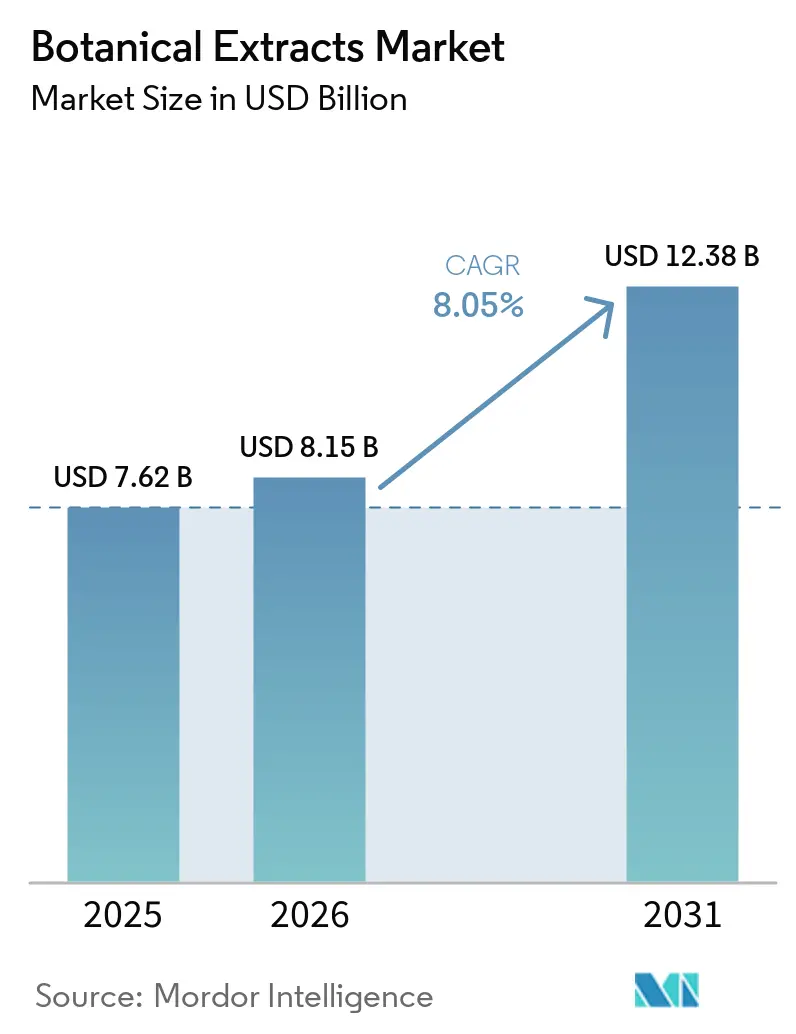

| Market Size (2026) | USD 8.15 Billion |

| Market Size (2031) | USD 12.38 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Botanical Extracts Market Analysis by Mordor Intelligence

The botanical extracts market size is expected to grow from USD 7.62 billion in 2025 to USD 8.15 billion in 2026 and is forecast to reach USD 12.38 billion by 2031 at 8.05% CAGR over 2026-2031. Growth in the botanical extracts market is tied to steady demand for plant-derived inputs across food, nutrition, and personal care, where buyers are placing more weight on ingredient origin, standardized active levels, and clean-label positioning. The opportunity is widening as brands seek botanicals that can support functional claims in areas such as metabolic health, skin wellness, and stress support, while extraction methods continue to improve yield consistency and purity. Climate-related shifts in phytochemical consistency and the rising risk of adulteration are also changing supplier selection, because buyers now need tighter traceability and stronger analytical controls than before. Regulatory differences between the United States and Europe continue to raise the operating burden for globally active suppliers, and this is favoring companies with stronger dossier development, preventive control systems, and audited sourcing networks. The botanical extracts market is therefore rewarding operators that combine extraction capability, sustainable sourcing, and regulatory readiness, while leaving less room for undifferentiated commodity suppliers.

Key Report Takeaways

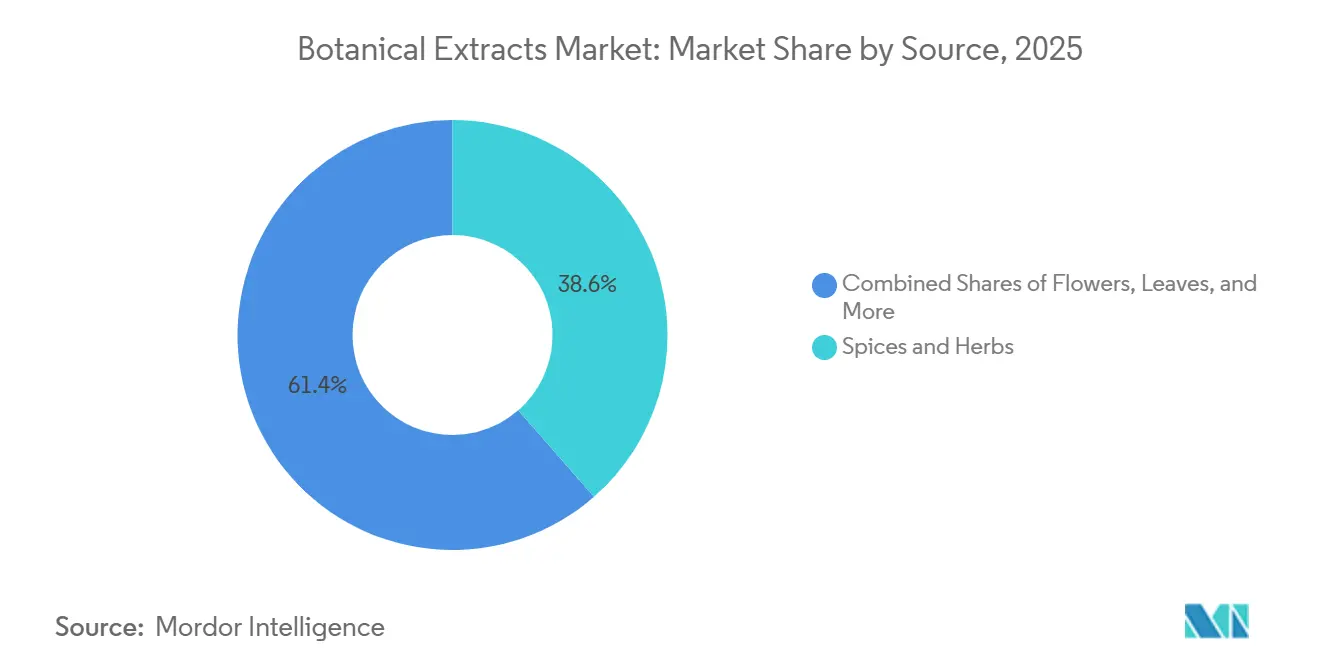

- By source, spices and herbs led with 38.56% of revenue in 2025, while flowers are projected to record the highest growth at 9.85% through 2031 in the botanical extracts market.

- By form, powder accounted for 56.37% of the botanical extracts market size in 2025, while liquid is forecast to expand at 9.78% through 2031.

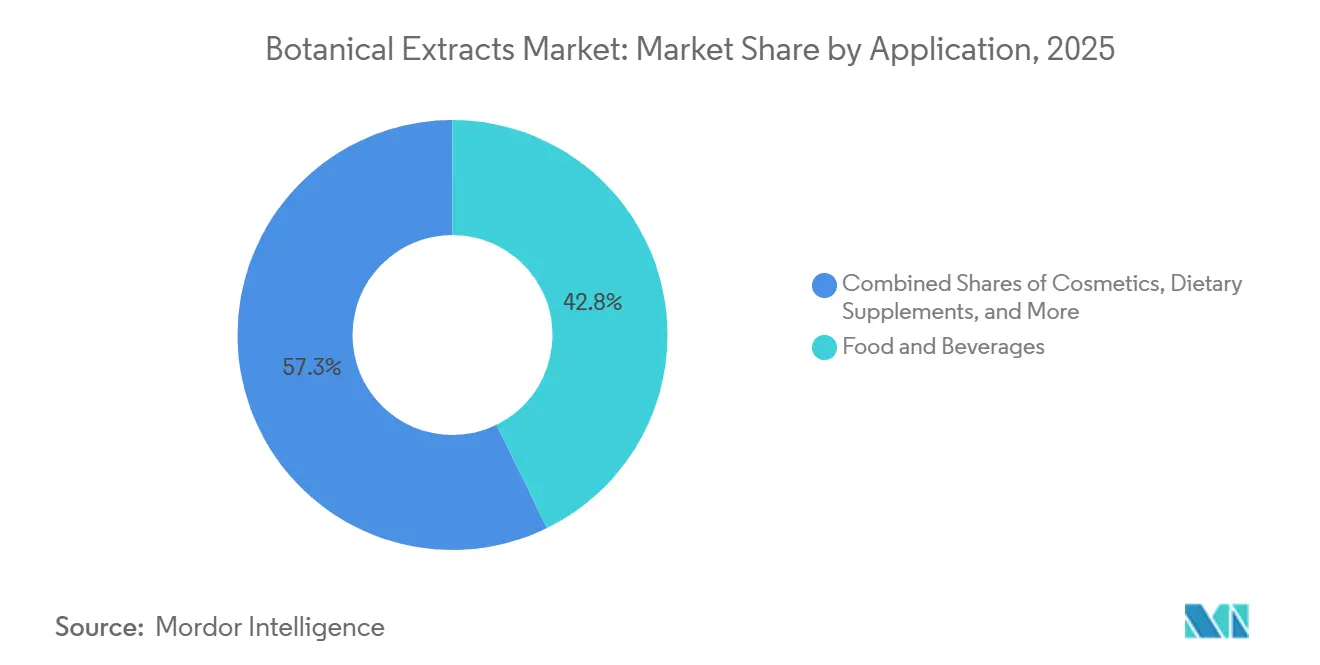

- By application, food and beverages held 42.75% of the botanical extracts market share in 2025, while dietary supplements are expected to advance at 9.16% through 2031.

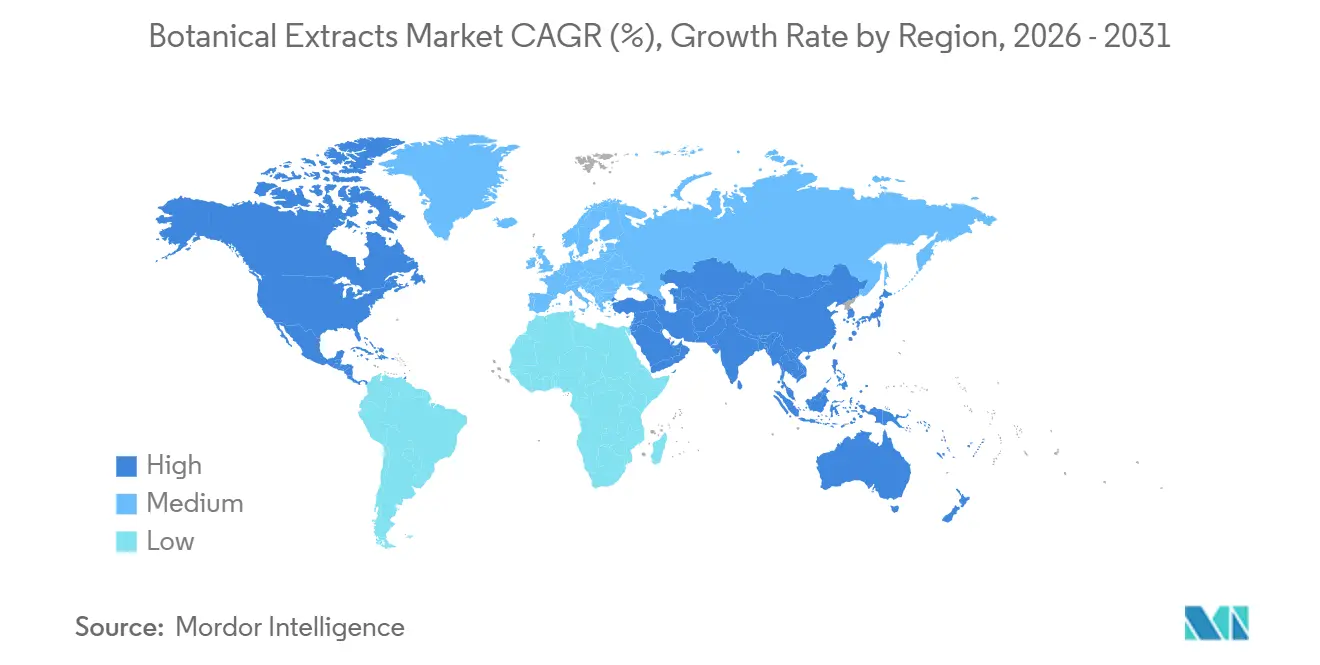

- By geography, North America represented 33.78% of the botanical extracts market in 2025, while the Asia-Pacific is set to post the fastest growth at 9.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Botanical Extracts Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Natural and Plant-Based Ingredients | +1.8% | Global | Short term (≤ 2 years) |

| Growing Nutraceutical and Dietary Supplement Industry | +1.4% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Increasing Consumer Interest in Herbal and Traditional Medicine | +0.8% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Advancements in Extraction Technologies | +0.7% | Global | Long term (≥ 4 years) |

| Growth of Organic and Sustainable Product Markets | +0.5% | North America & EU | Medium term (2-4 years) |

| Growing Applications in Natural Cosmetics and Personal Care Products | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural and Plant-Based Ingredients

Demand for natural and plant-based inputs remains the strongest force shaping the botanical extracts market across packaged food, dietary supplements, and personal care. This demand is becoming more specific, because buyers are not only asking for natural origin claims, they are also asking for standardized extracts with defined active content and stronger product documentation. That change is compressing the commercial space available to undifferentiated botanical powders and basic commodity extracts. It is also pushing suppliers to align more closely with formulation needs tied to metabolic health, skin support, and adaptogenic positioning. The botanical extracts market is therefore moving toward higher-value plant actives with clearer quality markers and more stable supply credentials. This direction fits broader policy and consumer acceptance of traditional and complementary health approaches in many countries.

Growing Nutraceutical and Dietary Supplement Industry

The nutraceutical channel is changing how extract suppliers compete in the botanical extracts market. Buyers in this channel are placing greater emphasis on traceability, clinical support, and compatibility with capsules, powders, gummies, and liquid delivery systems. That shift means supplier relationships are becoming harder to win with scale alone, because quality documentation and formulation support are now part of the purchasing decision. Public health systems in several countries are also recognizing the role of traditional and complementary medicine, which supports longer-term demand for botanical-based interventions beyond short consumer cycles[1]Source: World Health Organization, “Global Report on Traditional and Complementary Medicine,” World Health Organization, who.int. As a result, the botanical extracts market is seeing stronger demand for suppliers that can connect plant sourcing with evidence-backed product positioning. This is reinforcing premiumization in supplement formats that target cognition, stress, gut health, and metabolic support.

Advancements in Extraction Technologies

Extraction technology is expanding what the botanical extracts market can deliver in terms of purity, stability, and recovery efficiency. Supercritical CO2 extraction is particularly important because it supports high-purity isolation of thermolabile compounds while avoiding the residue issues associated with harsher solvent systems. Research also shows that combining supercritical CO2 with process improvements such as controlled pressure design and downstream optimization can improve recovery performance and operating efficiency. These gains matter commercially because they help suppliers produce consistent botanical actives for food, nutraceutical, and cosmetic applications. They also raise the value of proprietary extraction know-how, since better process control can protect margins and support premium quality positioning. The botanical extracts market is likely to reward companies that own extraction capability rather than relying only on third-party processing.

Growing Applications in Natural Cosmetics and Personal Care Products

Personal care is becoming a more important growth avenue for the botanical extracts market as cosmetic formulators move beyond broad natural claims. Buyers now want defined active levels, stronger efficacy support, and more transparent sourcing, especially in premium skin care and anti-aging products. DSM-Firmenich's 2026 launches of ALPAFLOR NEUROSOOTH and EXOVIVE LIFT show how botanical ingredients are moving into more specialized cosmetic functions, including skin stress response and advanced elasticity support. This raises the technical bar for botanical suppliers serving cosmetics, because efficacy and delivery profile now matter alongside natural origin. The botanical extracts market is therefore gaining a higher-margin application path where extraction science and product validation carry more weight than simple ingredient storytelling.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variability In Raw Material Quality And Availability | -1.0% | Asia-Pacific core, Middle East and Africa, South America | Short term (≤ 2 years) |

| High Production And Processing Costs | -0.8% | Global | Medium term (2-4 years) |

| Risk Of Adulteration And Quality Concerns | -0.6% | North America and Europe | Short term (≤ 2 years) |

| Competition From Synthetic Alternatives | -0.5% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Variability in Raw Material Quality and Availability

Raw material variability remains one of the clearest constraints on the botanical extracts market, and the issue goes well beyond simple price swings. Research published in 2025 showed that changing temperature and precipitation conditions are affecting plant distribution, growth patterns, and secondary metabolite profiles in medicinal species. The user-supplied case around ashwagandha also points to a deeper problem, because cultivation expansion into lower-quality areas can weaken active compound consistency and create regulatory concerns over plant-part usage. Wetter conditions in parts of South and Southeast Asia are further complicating drying and contamination control for sensitive crops, which raises quality assurance costs. UEBT's 2025 work on biodiversity and resilient sourcing suggests that more stable supply chains will depend on stronger sourcing models, but that approach also implies higher procurement discipline and tighter supplier screening[2]Source: Union for Ethical BioTrade, “Resilience Rooted in Nature, Flagship Report on Biodiversity and Sustainable Botanical Supply Chains,” Union for Ethical BioTrade, uebt.org. The botanical extracts market is therefore becoming more demanding for companies that depend on narrow sourcing regions or weak agronomic oversight.

Risk of Adulteration and Quality Concerns

Adulteration risk is rising with supply pressure, and this remains a direct constraint on trust in the botanical extracts market. A systematic review from the ABC-AHP-NCNPR Botanical Adulterants Prevention Program found that a meaningful share of tested bulk ingredients and finished products showed signs of adulteration or substitution, often in ways that can pass basic marker-compound tests. The 2025 Echinacea bulletin also documented issues such as plant-part mislabeling, undeclared excipients, and substitution with other species in commercial channels. Export pricing differences across destination markets create added economic pressure for lower-cost offerings, which can widen incentives for quality dilution in value-sensitive channels. This is pushing buyers toward advanced authentication tools such as DNA barcoding, metabolomics, and multi-parameter testing, especially in North America and Europe. The botanical extracts market is likely to keep favoring suppliers that can prove identity and consistency through stronger analytical frameworks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Spices and Herbs Command Volume; Flowers Signal Value Shift

Spices and herbs held 38.56% of the botanical extracts market in 2025, which reflected the broad use of turmeric, black pepper, capsicum, and ginger across food, nutrition, and personal care applications. This segment benefits from established logistics, strong familiarity among formulators, and clearer analytical standards for widely traded materials. Leaves, roots, and rhizomes also remain important for volume, especially where green tea, echinacea, valerian, and ashwagandha continue to support stable demand across several end uses. The other category serves smaller but important niches in pharmaceuticals, cosmetics, and specialty ingredient programs. Flowers is projected to grow at 9.85% through 2031, and that pace shows how value is shifting toward botanicals such as hibiscus, chamomile, rose, and elderflower in premium applications. In this part of the botanical extracts industry, sensory profile, origin story, and fit with high-value formulations are becoming more important than bulk volume alone.

The source mix also highlights a supply concentration issue inside the botanical extracts market, because a large share of global extract activity still depends on a few producing regions. China's plant extract exports reached USD 3.0 billion in 2025 with total volumes of 138,000 tons, which underlines the scale of its role in global supply chains. The same source showed wide differences in value per kilogram across export destinations, and that points to clear premium opportunities for higher-purity and more traceable materials. Suppliers that can pair source origin with extraction purity and third-party verification are better positioned to capture those premiums. That is why the botanical extracts market is moving away from simple source availability and toward source-level differentiation built on geographic origin, cultivation method, and downstream certification.

By Form: Powder Anchors Volume; Liquid and Oils Drive Margin Expansion

Powder accounted for 56.37% of the botanical extracts market size in 2025, which shows how strongly manufacturers still prefer formats that support shelf stability, dosing precision, and easy integration into tablets, capsules, and dry mixes. Powder remains the operational backbone for large-scale food and supplement production, particularly where spray-dried and freeze-dried formats help preserve handling efficiency across industrial lines. This part of the botanical extracts market also benefits from mature buyer familiarity, because formulators can work with powders across a wide range of product types without major process changes. MartinBauer's 2025 investment in a new spray drying tower in Kleinostheim supports the need for tighter specification control and greater in-house drying capacity. The investment also reflects sustained demand from European food and beverage customers for consistent extract performance. In the botanical extracts industry, form choice still has a direct effect on production efficiency and quality assurance.

Liquid is forecast to expand at 9.78% through 2031, which makes it the fastest-growing form in the botanical extracts market. This growth is linked to the rise of functional beverages, traditional herbal formats in Asia, and demand for ready-to-blend concentrates that fit faster product development cycles. Oils and oleoresins also hold an important high-value role, especially in flavor, fragrance, and cosmetic applications where plant-derived alternatives are replacing synthetic inputs. Work published in the Journal of CO2 Utilization showed that improved supercritical CO2 processing can increase bioactive recovery in plant oils, which supports better economics for premium producers. As these technical gains improve commercial feasibility, liquid and oil-based products are likely to take a larger share of premium formulation budgets. The botanical extracts market is therefore seeing form innovation become a route to margin expansion rather than a simple packaging decision.

By Application: Food and Beverages Anchor Scale; Supplements and Cosmetics Accelerate Premiumization

Food and beverages held 42.75% of the botanical extracts market share in 2025. That lead came from the broad use of botanical colors, flavor components, and functional ingredients across packaged foods, beverages, bakery products, and condiments. The segment remains the largest base for the botanical extracts market, absorbing a wide range of sources and formats at commercial volumes. Functional foods and beverages inside this application are especially important because they give brands room to combine clean-label positioning with health-oriented formulation. Natural replacement of synthetic colors and flavors also continues to support stable demand across everyday product categories. Dietary supplements are expected to grow at 9.16% through 2031, which shows that more targeted use cases such as stress support, cognition, gut health, and metabolic positioning are gaining share. This keeps the botanical extracts market closely tied to higher-value consumer health formats even when core food demand remains the main volume anchor.

Cosmetics and personal care are also becoming more important because buyers now want botanicals with clearer active content, bioavailability support, and certified origin rather than broad natural claims. DSM-Firmenich's 2026 launch activity in plant-derived cosmetic actives illustrates how this application is moving toward more specialized functionality and more formal efficacy language. Pharmaceuticals remain smaller in share, but they carry premium value where clinical substantiation for anti-inflammatory, antimicrobial, and cognitive support applications is stronger. Other uses, including agricultural and animal-related applications, remain a developing space with room to outperform if regulatory pathways become more favorable. This mix means the botanical extracts market is balancing scale from mainstream food uses with premium growth from supplements and science-led personal care. That balance should keep application diversity high even as buyer requirements become stricter.

Geography Analysis

North America held 33.78% of the botanical extracts market in 2025, and the region remained the largest geographic base because of strong supplement demand, high spending on functional nutrition, and mature formulation capabilities. The United States continues to offer relatively accessible supplement pathways under DSHEA, which supports broad product activity compared with stricter novel food routes in other regions. At the same time, FDA preventive control requirements under FSMA are raising expectations for traceability, handling, and supply chain quality across imported and domestic botanical ingredients[3]Source: US Food and Drug Administration, “Food Safety Modernization Act (FSMA),” US Food and Drug Administration, fda.gov. This gives an edge to suppliers with audited sourcing networks and better compliance systems. Canada and Mexico are also building botanical demand, but the United States remains the dominant revenue center within the regional structure.

Europe remains a premium destination in the botanical extracts market, especially for standardized and certified-organic materials used in functional foods, cosmeceuticals, and herbal pharmaceutical products. Germany, the United Kingdom, France, and Italy continue to serve as the region's main formulation and consumption hubs. EFSA's novel food framework and related European requirements create a clear regulatory filter that can slow new ingredient scaling but also strengthen entry barriers for prepared suppliers. Northern Europe is also supporting demand through stronger functional food and natural retail channels. In South America, Brazil is becoming more important not only as a source base but also as a value creation platform, and IFF's 2025 bioprospecting partnership in Legado das Águas shows how biodiversity access is gaining strategic value for future cosmetic and fragrance ingredient development.

Asia-Pacific is forecast to grow at 9.66% through 2031, which makes it the fastest-growing regional segment in the botanical extracts market. The region combines two strengths, because it is both a major raw material production hub and an expanding end-use market with rising local demand. China's 2025 plant extract exports of USD 3.0 billion and 138,000 tons show the scale of regional processing capacity and export relevance. Japan stands out as a premium destination, where willingness to pay for traceable and high-purity materials supports better value realization. WHO documentation on traditional medicine also supports the importance of established medical and cultural use frameworks in parts of Asia, including Japan's integration of Kampo into healthcare practice. The Middle East and Africa is smaller but still expanding, with the United Arab Emirates and South Africa acting as distribution anchors and Morocco and Nigeria showing early local formulation momentum. This keeps the botanical extracts market geographically broad, even though value capture remains uneven across sourcing and demand centers.

Competitive Landscape

The botanical extracts market has a medium concentration profile, with large multinational ingredient groups operating alongside specialized botanical processors. The leading company set in the user-supplied draft included International Flavors and Fragrances, Givaudan SA, DSM-Firmenich AG, Symrise AG, Indena S.p.A., Martin Bauer Group, Sabinsa Corporation, Synthite Industries, and Nexira SAS. That mix shows that scale still matters, but it is not enough by itself because buyers now expect stronger sourcing control, cleaner extraction, and deeper technical support. The botanical extracts market is increasingly shaped by three practical forms of differentiation, which are vertical integration, proprietary process capability, and the ability to support regulatory and formulation work with customers.

MartinBauer's acquisition of American Botanicals in October 2025 is a clear example of how companies are securing upstream raw material control and stronger provenance stories in the botanical extracts market. IFF's August 2025 partnership with Reservas Votorantim in Brazil is another example, because it gives LMR Naturals exclusive research access to a large native species base with downstream relevance for cosmetics and perfumery. Givaudan's September 2025 acquisition of Vollmens Fragrances also shows how regional fragrance and botanical capability can be added through portfolio expansion rather than organic build-out alone. These moves suggest that companies are competing not only for volume, but also for differentiated access to supply, formulation know-how, and regional customer reach.

A second layer of competition is centered on technology and compliance in the botanical extracts market. MartinBauer's Kleinostheim spray drying investment points to the importance of internal process control for tighter specifications and more reliable customer supply. DSM-Firmenich's 2026 cosmetic launches also show that botanical competition is extending into more specialized efficacy-led spaces where ingredient performance and validation matter more. Compliance credentials are also becoming a competitive requirement, because buyers need suppliers that can meet organic, food safety, and identity verification expectations in major regulated markets. Smaller specialists can still compete effectively when they bring deep knowledge of a specific botanical, geography, or cultivation system. That keeps the botanical extracts market open to niche players even as larger companies consolidate around sourcing, process capability, and customer support depth.

Botanical Extracts Industry Leaders

International Flavors and Fragrances Inc.

Archer Daniels Midland Company

Givaudan SA

DSM-Firmenich AG

Döhler GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DSM-Firmenich launched EXOVIVE™ LIFT, a plant-derived exosome ingredient sourced from Alpine Apple, Mediterranean Tangerine, and Sicilian Papaya from Italian biodiversity, at In-cosmetics Global 2026. Testing demonstrated 30% skin elasticity improvement, representing the company's entry into plant-based exosome cosmetic actives and opening a new botanical extract application in science-backed anti-aging.

- March 2026: DSM-Firmenich introduced ALPAFLOR NEUROSOOTH, a climate-adaptive botanical bioactive from Alpine plant sources targeting the skin-mind stress axis by inhibiting key neuroinflammatory mediators and boosting β-endorphin production. The ingredient extends botanical extract utility into precision neurocosmetics, a functionality tier previously occupied by synthetic actives.

- October 2025: MartinBauer acquired American Botanicals, the leading US supplier of wildcrafted botanicals, securing agricultural stewardship of 33,000 acres in the Appalachian region. The deal achieves vertical integration from field to finished ingredient and supplies a traceable provenance infrastructure for US-sourced wildcrafted botanical materials.

Global Botanical Extracts Market Report Scope

| Leaves |

| Roots and Rhizomes |

| Flowers |

| Spices and Herbs |

| Others |

| Powder |

| Liquid |

| Oils/Oleoresin |

| Food and Beverages | Bakery and Confectionery |

| Functional Food and Beverages | |

| Sauces and Condiments | |

| Others | |

| Dietary Supplements | |

| Cosmetics and Personal Care | |

| Pharmaceuticals | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Leaves | |

| Roots and Rhizomes | ||

| Flowers | ||

| Spices and Herbs | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| Oils/Oleoresin | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Functional Food and Beverages | ||

| Sauces and Condiments | ||

| Others | ||

| Dietary Supplements | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is botanical extracts expected to grow through 2031?

The botanical extracts market is projected to rise from USD 8.15 billion in 2026 to USD 12.38 billion by 2031, which reflects an 8.05% CAGR over the forecast period.

Which source category leads revenue in botanical extracts?

Spices and herbs held the largest share in 2025 at 38.56%, supported by broad use across food processing, nutraceuticals, and personal care.

Which form is expanding the fastest in botanical ingredients?

Liquid extracts are expected to grow the fastest at 9.85% through 2031, helped by functional beverages and ready-to-blend formulations.

Why does Asia-Pacific matter so much for global supply and demand?

Asia-Pacific is the fastest-growing region at 9.66% through 2031.

Page last updated on: