Tea Extracts Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.05 Billion |

| Market Size (2031) | USD 7.56 Billion |

| Growth Rate (2026 - 2031) | 8.38% CAGR |

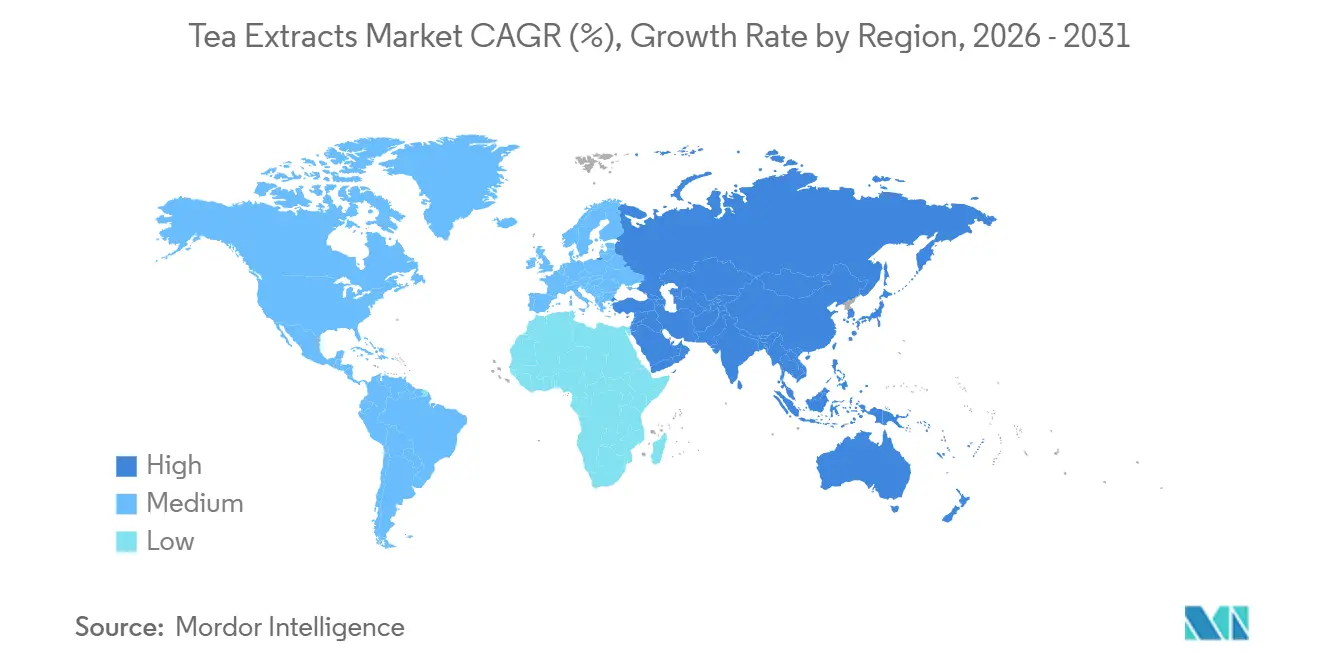

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

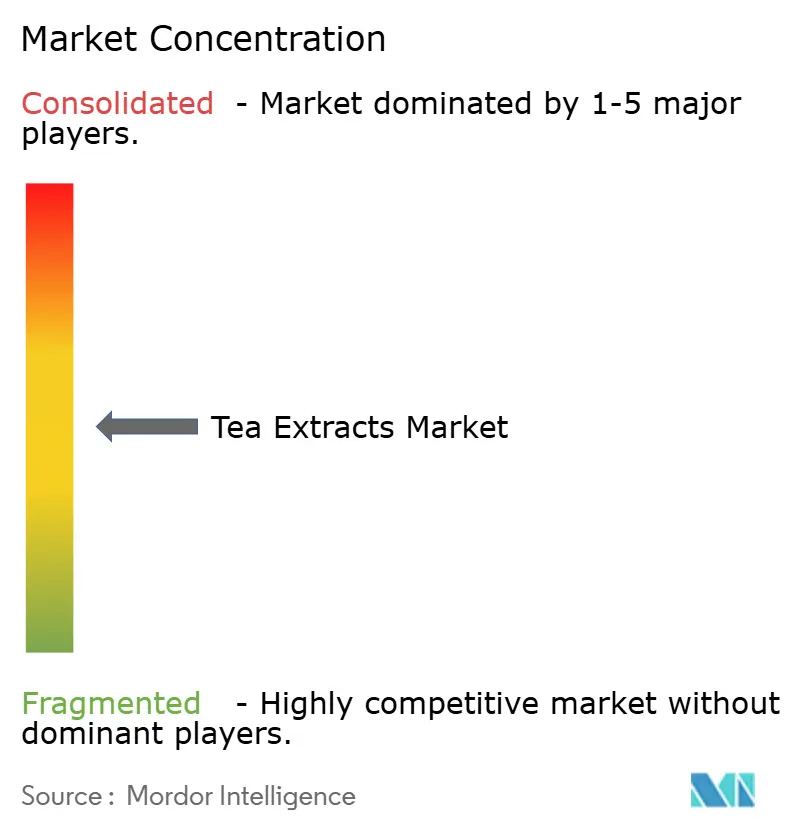

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tea Extracts Market Analysis by Mordor Intelligence

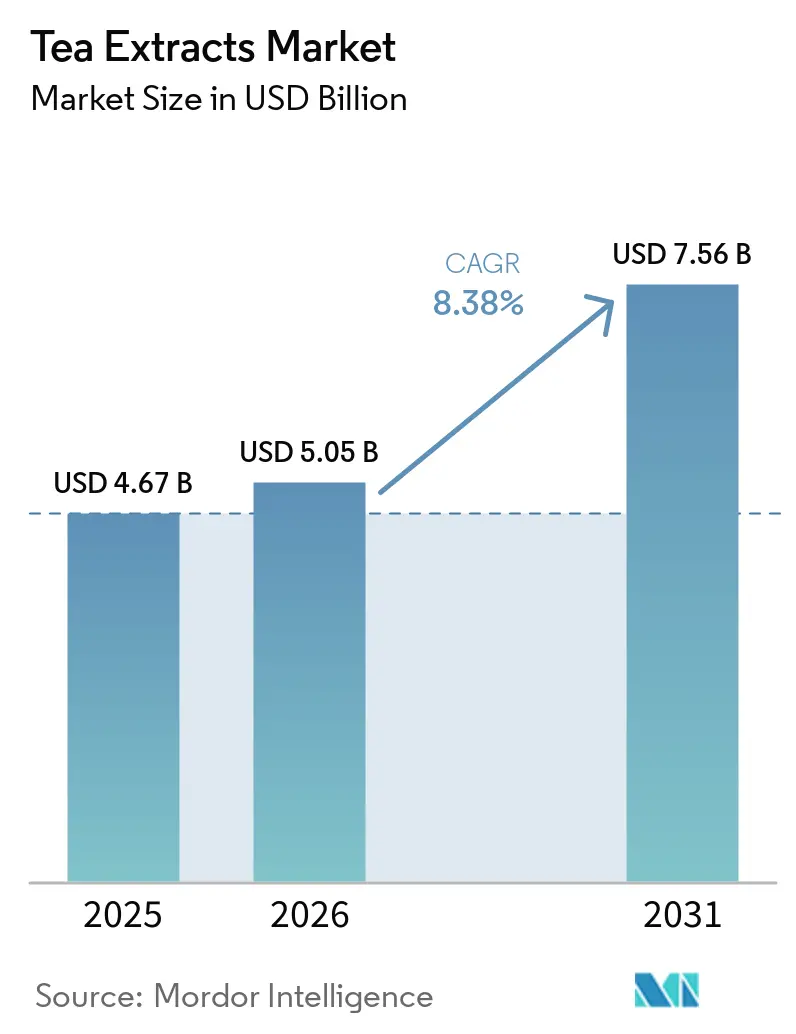

The tea extracts market size was valued at USD 4.67 billion in 2025 and estimated to grow from USD 5.05 billion in 2026 to reach USD 7.56 billion by 2031, at a CAGR of 8.38% during the forecast period (2026-2031). Demand accelerates after the February 2026 U.S. ban on petroleum-based synthetic dyes, which pushed beverage and food formulators toward plant-derived solutions such as green tea polyphenols. Asia-Pacific leads revenue generation, while North America quickly adopts matcha and EGCG-standardized grades in ready-to-drink beverages. Encapsulation breakthroughs that preserve catechin potency at neutral pH, and growing interest in low-dose, multi-ingredient dietary supplements, further widen end-use opportunities. Rising raw-leaf prices and stringent limits on daily EGCG intake temper profitability, yet suppliers with traceable, certified supply chains continue to enjoy pricing power.

Key Report Takeaways

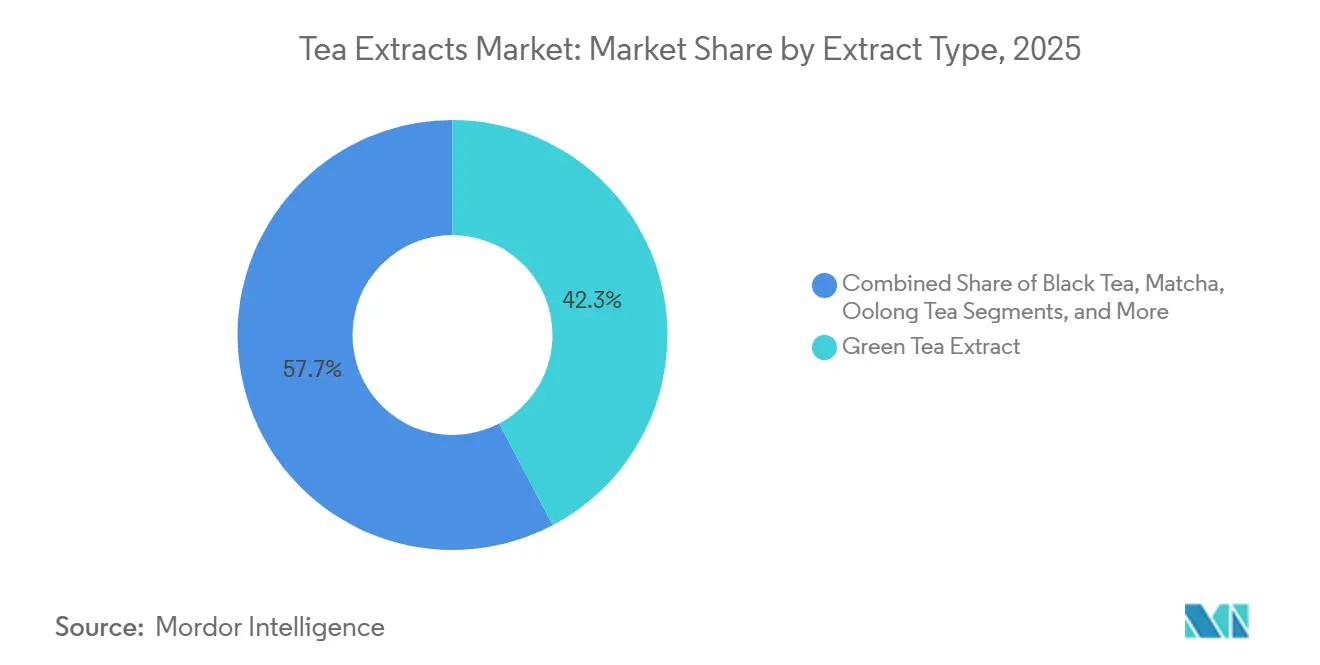

- By extract type, green tea commanded 42.27% of 2025 revenue, while matcha is advancing at a 9.65% CAGR through 2031.

- By form, powder formats accounted for 59.33% of the 2025 volume; encapsulated products are forecast to expand at a 10.48% CAGR through 2031.

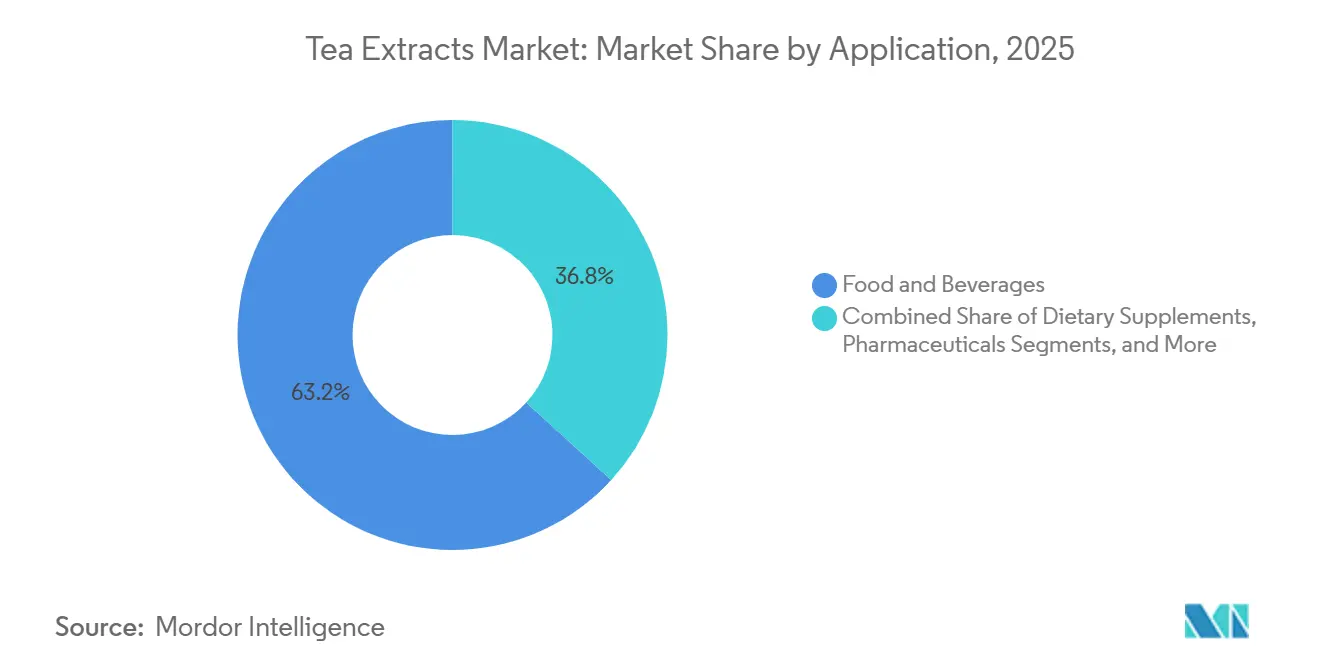

- By application, food and beverage accounted for 63.21% of 2025 demand, whereas dietary supplements are on track for a 9.42% CAGR through 2031.

- By geography, Asia-Pacific accounted for 47.44% of 2025 revenue and will retain the fastest regional growth rate of 10.14% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tea Extracts Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural antioxidants in functional beverages | +1.8% | North America and EU, spillover to APAC | Short term (≤ 2 years) |

| Clean-label shift from synthetic to natural food additives | +1.5% | Global, led by North America and EU | Medium term (2-4 years) |

| Green tea EGCG-driven weight and metabolism formulations | +1.2% | North America, Europe, urban APAC | Medium term (2-4 years) |

| Growing application of tea-extract botanicals in skincare and haircare | +0.9% | APAC core, North America and EU premium segments | Long term (≥ 4 years) |

| Organic and specialty-tea extracts creating premium tiers | +1.0% | North America, Europe, Japan | Long term (≥ 4 years) |

| Encapsulation of tea polyphenols in smart active packaging | +0.7% | Global, early adoption in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural antioxidants in functional beverages

Functional beverage formulators face a narrowing palette of permissible synthetic colorants following the FDA's February 2026 ban on petroleum-derived dyes, which approved natural alternatives, including butterfly pea flower, spirulina, beetroot red, and Galdieria sulphuraria extract as replacement options. This regulatory pivot accelerates tea polyphenol adoption because green tea extracts deliver both antioxidant functionality, measured at ORAC values exceeding 15,000 micromoles Trolox equivalents per gram for high-polyphenol grades, and a clean-label positioning that resonates with consumers scrutinizing ingredient panels. Ready-to-drink tea launches incorporating matcha or EGCG-standardized extracts rose sharply in North America during 2025, exemplified by Ito En's October 2024 introduction of matcha LOVE RTD beverages in aseptic carton packs, which combine Matcha Banana Latte and Matcha Cacao Latte formats to capture café-quality experiences in shelf-stable packaging. The FDA's enforcement discretion on "no artificial colors" claims, announced concurrently with the dye ban, incentivizes brands to reformulate legacy SKUs with tea extracts rather than risk label compliance challenges. Beverage developers now prioritize water-soluble instant grades and low-caffeine variants to avoid bitterness and dosing conflicts in multi-serve formats, a technical requirement that favors suppliers offering customizable EGCG-to-caffeine ratios and particle-size specifications below 15 micrometers for smooth mouthfeel.

Clean-label shift from synthetic to natural food additives

The clean-label movement extends beyond colorants into antioxidant preservation systems, where tea polyphenols replace synthetic antioxidants such as butylated hydroxyanisole and butylated hydroxytoluene in packaged foods. Kemin Industries' OLESSENCE line, launched in North America, blends olive fruit, rosemary, green tea, and mixed tocopherols to delay staling, curb rancidity, and stabilize fats in baked goods, snack foods, dressings, and sauces, positioning olive leaf polyphenols as the lead antioxidant while green tea extracts provide synergistic free-radical quenching. Formulators value tea extracts' dual role as both preservatives and label-friendly ingredients, particularly in markets where consumer surveys link synthetic additives to health concerns and retailers impose restricted-ingredient lists that exclude artificial preservatives. The European Union's stringent novel-foods framework and the United States' Generally Recognized as Safe self-affirmation pathway create regulatory asymmetry; suppliers targeting both regions must navigate batch-specific certificates of analysis with individual catechin breakdowns per ISO 14502-2 and heavy-metals testing compliant with EU Regulation 1881/2006. This compliance burden favors vertically integrated suppliers offering end-to-end traceability dossiers, plantation coordinates, harvest dates, and unredacted COAs over commodity brokers, a dynamic that consolidates market share among manufacturers holding USDA Organic, EU Organic, Kosher, and Halal certifications simultaneously.

Green tea EGCG-driven weight and metabolism formulations

Clinical evidence supporting EGCG's thermogenic and lipolytic effects underpins its incorporation into weight-management supplements, despite mixed trial outcomes. Studies demonstrate a 4-5% body-fat reduction when EGCG doses of 300-400 milligrams per day are combined with caffeine, a synergy attributed to catechol-O-methyltransferase inhibition that prolongs norepinephrine activity and elevates energy expenditure, according to the International Journal of Obesity. Dietary supplement brands position EGCG as a metabolic-support ingredient compatible with glucagon-like peptide-1 receptor agonist therapies, marketing formulations that pair green tea extract with chromium, L-carnitine, or conjugated linoleic acid to address consumers seeking non-pharmaceutical adjuncts to calorie restriction. Standardization to 50% EGCG, delivering 200 milligrams per 400-milligram capsule, has become the de facto industry benchmark, with brands such as NOW Foods achieving NSF certification and Non-GMO Project verification to differentiate in a crowded category. Regulatory caution tempers growth; the USP's 2020 mandate for "Do not take on an empty stomach" warnings and Health Canada's 300-milligram daily cap reflect hepatotoxicity case reports, including rare instances requiring liver transplantation, that prompt formulators to lower per-serving EGCG content and add hepatoprotective co-ingredients such as milk thistle or N-acetylcysteine. Japan's Foods with Function Claims regime and South Korea's Health Functional Food Code offer pathways for metabolic-health claims, yet require substantiation through randomized controlled trials, a barrier that limits smaller brands' ability to compete on efficacy messaging.

Growing application of tea-extract botanicals in skincare and haircare

Cosmetic formulators incorporate green tea polyphenols for antioxidant, anti-aging, and soothing claims, leveraging EGCG's ability to scavenge reactive oxygen species and modulate inflammatory pathways in dermal fibroblasts. Water-soluble instant grades standardized to 60-95% EGCG and particle sizes passing through an 80-mesh screen enable seamless integration into serums, lotions, and micellar waters without cloudiness or sedimentation. The European Union's Cosmetics Regulation requires safety dossiers demonstrating the absence of heavy metals, lead below 1.0 parts per million, arsenic below 1.0 ppm, cadmium below 0.5 ppm, and microbial limits below 1,000 colony-forming units per gram, specifications that align with pharmaceutical-grade tea extracts and create quality-tier differentiation versus food-grade inputs, according to the EU Cosmetics Regulation. Asian beauty brands emphasize matcha's chlorophyll content, which exceeds 100 milligrams per gram in ceremonial grades and imparts a vibrant green hue suitable for "clean beauty" positioning, while North American and European brands favor decaffeinated extracts to avoid stimulant-related skin sensitivity. Patent filings reveal interest in liposomal encapsulation and solid-lipid nanoparticles that enhance EGCG bioavailability by 3.5-fold and enable controlled release over 12-24 hours, addressing the compound's rapid degradation at neutral pH, approximately 88% loss within 2 hours at pH 7.0 versus 95% retention at pH 2.0.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility and supply gaps | -0.8% | Global, acute in Sri Lanka, Kenya, China | Short term (≤ 2 years) |

| Regulatory scrutiny around high-dose EGCG safety | -1.2% | EU, North America, spillover to APAC | Medium term (2-4 years) |

| High cost of organic and specialty tea extracts | -0.6% | North America, Europe, Japan | Long term (≥ 4 years) |

| Competition from other natural extracts and synthetics | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-material price volatility and supply gaps

Tea commodity prices reached USD 2.80 per kilogram in October 2025, 15% above long-term averages, driven by Sri Lanka's 2022 crop shortfall due to a fertilizer-import ban and economic crisis, coupled with increased logistics costs reflected in the Baltic Dry Index's 40% rise between April and October 2025[1]Source: Food and Agriculture Organization, “Tea Composite Price Index,” FAO.org . Climate projections compound supply risks; yield declines by 2050 are estimated at 5% in China, 14% in Sri Lanka, and 25% in Kenya, threatening the 60% of global production sourced from smallholder farms that employ 13 million workers. India's black tea import proxy prices fell to approximately USD 1,780 per metric ton in 2024, a 5-year compound annual decline of 3.05%, yet green tea extract pricing moved inversely; Chinese suppliers raised 98% EGCG to USD 250-330 per kilogram in 2026, an 11-23% increase versus 2024, and 50% polyphenol extracts climbed 15-21% to USD 14-34 per kilogram. This divergence reflects extraction's capital intensity, spray-drying towers, chromatographic fractionation, and organic certification, which insulates processors from commodity deflation but transmits raw-leaf inflation with a multiplier effect. Supplier concentration exacerbates volatility; India imported 77% of its tea from Kenya and Nepal in 2025, creating single-origin dependency that amplifies geopolitical and weather shocks, according to the Tea Board of India. Mechanization reaches only 70% of tea bushes globally, leaving labor-intensive harvesting vulnerable to wage inflation and demographic shifts as rural populations age and migrate to urban centers IISD.

Regulatory scrutiny around high-dose EGCG safety

European Union Regulation 2022/2340 restricts EGCG to below 800 milligrams per day and mandates hepatotoxicity warnings for individuals under 18 years, pregnant or lactating women, following a 2018 EFSA scientific opinion linking doses at or above 800 milligrams daily to elevated alanine aminotransferase and aspartate aminotransferase levels indicative of liver stress[2]Source: European Food Safety Authority, “Regulation 2022/2340 on EGCG Limits,” EFSA.europa.eu. Health Canada tightened limits to 300 milligrams EGCG per day in supplemented foods effective January 2024, and the United Kingdom's Committee on Toxicity identified HLA-B*35:01 genetic susceptibility and UGT1A4 genotype polymorphisms associated with transaminase elevations, suggesting inter-individual variability in hepatotoxic risk. The USP's 2020 monograph revision requires cautionary labeling, "Do not take on an empty stomach. Take with food," reflecting case reports of liver injury, including rare transplant cases, attributed to high-dose EGCG supplements. These constraints push formulators toward lower per-serving doses and multi-ingredient blends, diluting EGCG's differentiation versus generic green tea extracts and limiting premium pricing. Brands now invest in genetic screening partnerships or consumer education to manage liability, yet regulatory harmonization remains elusive; Japan's Foods with Function Claims permits metabolic-health assertions with clinical substantiation, while the FDA treats structure-function claims under the Dietary Supplement Health and Education Act without pre-market approval, creating compliance complexity for global SKUs, according to the MHLW Japan.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Extract Type: Matcha Premiumization Outpaces Commodity Green Tea

Green tea extracts accounted for 42.27% of 2025 revenue, yet matcha extracts will grow at a 9.65% CAGR through 2031. This divergence reflects matcha's dual positioning as both a functional ingredient and a lifestyle product, with North American café chains sourcing approximately 1,000 metric tons annually and social-media platforms amplifying visually distinct matcha lattes, smoothie bowls, and desserts. Black tea extracts serve niche applications in ready-to-drink iced tea and malt beverages, while oolong and white tea extracts remain specialty ingredients for premium cosmetics and limited-edition beverage launches. Oolong exports from China declined in 2025, reflecting substitution by green tea in functional applications where EGCG standardization and clinical evidence favor Camellia sinensis var. sinensis over semi-oxidized cultivars, according to the China Tea Marketing Association. VICELLA Laboratory's July 2025 launch of matcha supplement capsules, 194 milligrams matcha per capsule, 100% Kyoto Uji Matcha blended with 18 grains, exemplifies product innovation targeting gut health and metabolic support, a positioning that leverages matcha's chlorophyll and L-theanine content beyond EGCG alone.

Shade-growing techniques elevate matcha's L-theanine to 2.5% or higher and chlorophyll above 100 milligrams per gram, creating a 20-day pre-harvest shading requirement at 95% light exclusion that differentiates ceremonial from culinary grades and justifies 2-3 times the margin for single-origin Uji, Nishio, and Shizuoka powders. Stone-milling at low friction preserves particle size below 10 micrometers for ceremonial grades versus 15 micrometers for culinary, a specification critical for smooth mouthfeel in traditional tea ceremonies and premium lattes. Nitrogen-flushed packaging and refrigerated storage extend shelf life to 12-24 months, yet matcha's sensitivity to oxygen, moisture, and light demands opaque, oxygen-barrier materials and cold-chain logistics that raise landed costs by 15-25% versus bulk green tea extracts. Yen depreciation during 2022-2025 lowered effective dollar prices for U.S. importers, spurring café chains to consolidate supplier relationships and lock in multi-year contracts, a procurement dynamic that favors large Japanese cooperatives over artisanal producers and accelerates matcha's penetration into mainstream foodservice.

By Form: Encapsulated Formats Gain on Stability and Controlled Release

Powder formulations captured 59.33% of 2025 volume, driven by cost efficiency, ease of blending into capsules and tablets, and compatibility with spray-drying infrastructure that delivers 88.5% encapsulation efficiency versus 83.5% for freeze drying, according to the International Journal of Food Science & Technology[3]Source: International Journal of Food Science & Technology, “Spray Drying vs Freeze Drying Efficiency,” onlinelibrary.wiley.com . Encapsulated and granular formats will expand at 10.48% CAGR through 2031, propelled by polyethylene glycol-chitosan nanoparticles that achieve 81 milligrams of polyphenols per gram and extend EGCG half-life approximately sixfold when paired with ascorbic acid at a 1:1 molar ratio. Liquid extracts serve ready-to-drink beverages and cosmetic serums, yet face stability challenges at neutral pH. EGCG degrades 88% within 2 hours at pH 7.0 versus 95% retention at pH 2.0, necessitating acidic formulations or antioxidant co-ingredients such as ascorbic acid and metal chelators. Whey protein isolate-beta-cyclodextrin nanocomplexes retain 77-80% of jasmine tea polyphenols during 6-month ambient storage, outperforming unencapsulated controls that lose over 50% potency, a performance gap that justifies 20-40% price premiums for encapsulated ingredients in dietary supplements and functional foods.

Active packaging films incorporating green tea extracts extend shelf life in protein-rich and acidic foods; polyamide films with embedded polyphenols increased beef shelf life to 23 days versus 14 days for controls, while low-density polyethylene films extended orange juice freshness to 14 days, and polyvinyl alcohol nanofibers retained 88% polyphenol content with 79.7% migration into food simulants. Zhejiang Minghuang's 2013 patent for tea polyphenol liposoluble microcapsules (CN103330213A) and ongoing R&D into solid-lipid nanoparticles that enhance bioavailability by 3.5-fold signal sustained intellectual property activity in controlled-release platforms, according to the China National Intellectual Property Administration. Encapsulation addresses EGCG's protein-binding tendency, which causes cloudiness in dairy and high-protein matrices, enabling formulators to incorporate tea extracts into protein shakes, yogurt, and cheese without sedimentation or off-flavors. Granular formats, often spray-dried agglomerates with improved flowability, facilitate direct compression into tablets and reduce dust generation during manufacturing, a safety and efficiency advantage that resonates with contract manufacturers serving the dietary supplement sector.

By Application: Dietary Supplements Leverage Clinical Evidence and Dosing Precision

Food and beverage applications accounted for 63.21% of 2025 demand, yet dietary supplements will grow at a 9.42% CAGR through 2031, supported by clinical trials demonstrating 4-5% body-fat reduction at 300-400 milligram daily EGCG doses and synergy with caffeine for thermogenic effects, according to the International Journal of Obesity. Standardization to 50% EGCG, delivering 200 milligrams per 400-milligram capsule, has become the industry benchmark, with brands such as NOW Foods achieving NSF certification, Non-GMO Project verification, and Kosher approval to differentiate in a crowded category. Beverages and functional drinks dominate the food and beverage sub-segments, driven by ready-to-drink tea, matcha lattes, and energy drinks containing 50-200 milligrams of EGCG per serving, a dosing range that balances efficacy claims with regulatory caution and consumer tolerance for bitterness. Cosmetics and personal care applications expand at 8-9% CAGR, leveraging water-soluble instant grades standardized to 60-95% EGCG for serums, lotions, and micellar waters that deliver antioxidant and anti-aging benefits without cloudiness or sedimentation.

Pharmaceutical applications remain niche, yet attract interest for EGCG's potential in neurodegenerative, cardiovascular, and inflammatory conditions. Animal feed applications uses tea polyphenols as natural antioxidants to preserve feed quality and support gut health in poultry and aquaculture, a segment constrained by cost sensitivity and limited willingness-to-pay for premium botanicals versus synthetic alternatives. Meat and seafood preservation within food and beverage sub-segments benefits from tea extracts' antimicrobial properties; polyamide films with embedded polyphenols extended beef shelf life to 23 days, a 64% improvement over controls, positioning tea extracts as dual-function ingredients that address both oxidation and microbial spoilage. Bakery and dairy applications incorporate tea extracts at 50-150 milligrams per serving to delay staling and rancidity, yet face formulation challenges from EGCG's protein-binding tendency, which requires encapsulation or pH adjustment to prevent cloudiness and off-flavors.

Geography Analysis

Asia-Pacific commanded 47.44% of 2025 revenue and will grow at 10.14% CAGR through 2031, driven by China's export surge in 2025, according to the China Tea Marketing Association. China's average export price recovered to USD 3.81 per kilogram in October 2025, a 4.1% rise versus October 2024's USD 3.66 per kilogram, reversing a multi-year decline from USD 6.23 per kilogram in 2021 to USD 3.70 per kilogram in 2024, yet extract pricing moved inversely; 98% EGCG reached USD 250-330 per kilogram in 2026, an 11-23% increase versus 2024, reflecting extraction's capital intensity and organic certification premiums. India's tea imports rose during January-July 2025, sourcing primarily from Kenya, Nepal, and Sri Lanka, yet domestic extract production remains limited by infrastructure gaps and certification costs, according to the Tea Board of India. Southeast Asian markets, Indonesia, Thailand, Singapore, adopt tea extracts in halal-certified functional beverages and beauty-from-within formulations as middle-class consumers prioritize wellness and clean-label ingredients.

North America accounted for a significant share of 2025 revenue, with café chains sourcing roughly matcha and dietary supplement brands standardizing on 200 milligrams of EGCG per capsule to align with clinical trial dosing. U.S. imports of tea from grew signaling a shift toward functional and antioxidant-rich varieties according to the U.S. International Trade Commission. The FDA's February 2026 ban on petroleum-based synthetic dyes compelled beverage and food formulators to replace artificial colorants with plant-derived alternatives including green tea polyphenols, accelerating adoption in ready-to-drink teas, energy drinks, and functional waters. Canada's 300-milligram daily EGCG limit in supplemented foods, effective January 2024, constrains high-dose formulations yet spurs innovation in multi-ingredient blends that pair tea extracts with adaptogens, probiotics, or collagen peptides to deliver holistic wellness positioning. Mexico's growing middle class and rising health consciousness drive tea extract demand in functional beverages and beauty products, yet price sensitivity limits organic and ceremonial-grade penetration, favoring culinary-grade matcha and commodity green tea extracts.

EU Regulation 2022/2340 caps EGCG at 800 milligrams per day and mandates hepatotoxicity warnings, pushing formulators toward lower per-serving doses and multi-ingredient blends that dilute EGCG's share of active-ingredient cost. Germany, the United Kingdom, France, and the Netherlands lead demand for tea extracts in dietary supplements and functional foods, supported by robust health-and-wellness retail channels and high penetration of organic and clean-label products. The European Pharmacopoeia's residual-solvent limits and ICH Q3D heavy-metals guidelines create quality-tier differentiation, favoring pharmaceutical-grade extracts with EGCG above 95%, total catechins above 98%, and caffeine below 0.5%. South America and Middle East & Africa collectively represent 5-10% of 2025 revenue, with Brazil, Argentina, and South Africa showing nascent demand for tea extracts in functional beverages and cosmetics, yet infrastructure constraints, import tariffs, and limited organic certification slow adoption relative to developed markets.

Competitive Landscape

The tea extracts market exhibits moderate concentration, with five leading suppliers, Martin Bauer Group, Finlays, Taiyo International, Kemin Industries, and Synthite Group, with a majority market share, yet fragmentation persists among regional processors, contract manufacturers, and vertically integrated beverage brands that backward-integrate extraction assets. Martin Bauer doubled tea extract capacity at its Hangzhou, China, facility in October 2024, expanding the plant to 200,000 square feet to serve U.S. ready-to-drink demand, and commissioned a new spray-drying tower at Kleinostheim, Germany, in April 2024 that doubles capacity, reduces CO2 emissions by 800 metric tons annually, and cuts energy consumption by 75%. Finlays acquired tea extraction assets from Natural Instant Foods in Paraguay in July 2023 and relocated operations to its Saosa facility in Kericho, Kenya, which offers same-day fresh-leaf extraction and positions the company to serve African and Middle Eastern markets at lower logistics costs.

DSM-Firmenich's Taste, Texture & Health division posted 4% organic growth in 2025 with a 20.6% EBITDA margin, leveraging botanical extraction, biotech, and encapsulation platforms to differentiate in natural colors, functional beverages, and health ingredients. Givaudan's Taste & Wellbeing segment generated CHF 1,909 million in sales during H1 2025, a 4.1% like-for-like increase, and expanded specialist labs for protein, oral care, and encapsulation in Switzerland, the United Kingdom, and Singapore, targeting 4-6% like-for-like growth through 2030. White-space opportunities cluster around encapsulation technology, halal-certified formulations, and direct-to-consumer premium matcha, where brands leverage live commerce, subscription starter kits, and EGCG-milligram labeling to educate consumers and justify 2-3 times the margin of volume-grade powders.

Kemin Industries' polyphenol-retention patent for spearmint drying, granted in 2024, demonstrates the strategic value of process intellectual property that preserves rosmarinic acid and other bioactives, a capability transferable to tea extracts where post-harvest handling determines EGCG and L-theanine retention. Emerging disruptors include Chinese suppliers offering EU-certified organic green tea extracts with third-party testing for over 500 pesticide compounds, end-to-end traceability dossiers, and 25-kilogram minimum order quantities that undercut established European suppliers by 15-25% while meeting USDA NOP and EU Regulation 834/2007 standards. ISO 22000 and HACCP certifications become table stakes for EU and North American buyers, while SQF Code 31 supplement-manufacturing certification, adopted by private-label manufacturers such as Caraway Tea, creates a compliance moat that forces brands to pay premiums for certified production and reduces regulatory liability.

Tea Extracts Industry Leaders

Martin Bauer Group

Finlays

Taiyo International

Kemin Industries, Inc.

Synthite Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Finlays, a provider of black tea extract, launched "Finlays Solutions," an evolved extracts business designed to provide comprehensive support to beverage operators and brands through advanced technology and consumer insights. The initiative represents a strategic shift toward customer-centric service delivery, emphasizing innovation and commercial viability in beverage solution development.

- October 2024: PLT Health Solutions expanded its portfolio by introducing cellflo6, a patented green tea (Camelia sinensis) extract. This ingredient is formulated to enhance energy, sports performance, and overall health benefits. Cellflo6 is a clinically studied, gallate-enhanced oligomer extract from green tea with standardized levels of galloylated procyanidins.

- July 2024: Mazza Innovation Ltd., which produces solvent-free botanical extracts, opened a commercial extraction facility to manufacture PhytoClean extracts from cranberry, green tea, and blueberry, along with other clean label ingredients.

- October 2023: MartinBauer, a leader in tea and botanical ingredients, unveiled a premium line of tea and botanical syrups tailored for beverage applications. The latest collection from MartinBauer features six distinct syrups, one of which is Black Tea. Emphasizing its dedication to quality, MartinBauer ensures that the product is devoid of artificial colors and flavors, underscoring its commitment to all-natural beverage solutions.

Global Tea Extracts Market Report Scope

Tea extracts are concentrated forms of tea derived from tea leaves and contain key bioactive compounds, flavors, and antioxidants. The tea extracts market is segmented by extract type, form, application, and geography. By extract type, the market includes green tea, black tea, oolong tea, white tea, matcha extract, and other types. Based on form, the market is categorized into powder, liquid, and encapsulated/granular forms. By application, the market covers food and beverage, dietary supplements, cosmetics and personal care, pharmaceuticals, and animal feed. By geography, the report covers North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, market sizing and forecasts have been done on the basis of value (USD million) and volume (Tons).

| Green Tea |

| Black Tea |

| Oolong Tea |

| White Tea |

| Matcha Extract |

| Other Types |

| Powder |

| Liquid |

| Encapsulated/Granular |

| Food and Beverage | Beverages and Functional Drinks |

| Meat and Seafood | |

| Dairy | |

| Bakery | |

| Others | |

| Dietary Supplements | |

| Cosmetics and Personal Care | |

| Pharmaceuticals | |

| Animal feed |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Extract Type | Green Tea | |

| Black Tea | ||

| Oolong Tea | ||

| White Tea | ||

| Matcha Extract | ||

| Other Types | ||

| By Form | Powder | |

| Liquid | ||

| Encapsulated/Granular | ||

| By Application | Food and Beverage | Beverages and Functional Drinks |

| Meat and Seafood | ||

| Dairy | ||

| Bakery | ||

| Others | ||

| Dietary Supplements | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals | ||

| Animal feed | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global tea extracts market in 2031?

The tea extracts market size is forecast to reach USD 7.56 billion by 2031, expanding at an 8.38% CAGR from 2026-2031.

Which region will contribute the largest incremental revenue through 2031?

Asia-Pacific will remain the primary growth engine, adding the highest absolute revenue as it grows at 10.14% CAGR through 2031.

Why are encapsulated formats gaining popularity?

Nanoparticle and spray-dry technologies protect EGCG at neutral pH, extend shelf life in RTD beverages, and support smart active packaging, driving a 10.48% CAGR for encapsulated products.

How are regulators shaping EGCG dosage limits?

The EU caps daily intake at 800 mg, Health Canada limits supplemented foods to 300 mg, and the USP mandates “take with food” warnings, pushing brands toward lower-dose blends.

Which extract type is growing fastest?

Matcha extracts are projected to outpace other types with a 9.65% CAGR through 2031, fueled by café demand and social-media visibility.

Page last updated on: