Body Scrub Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.82 Billion |

| Market Size (2031) | USD 3.58 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

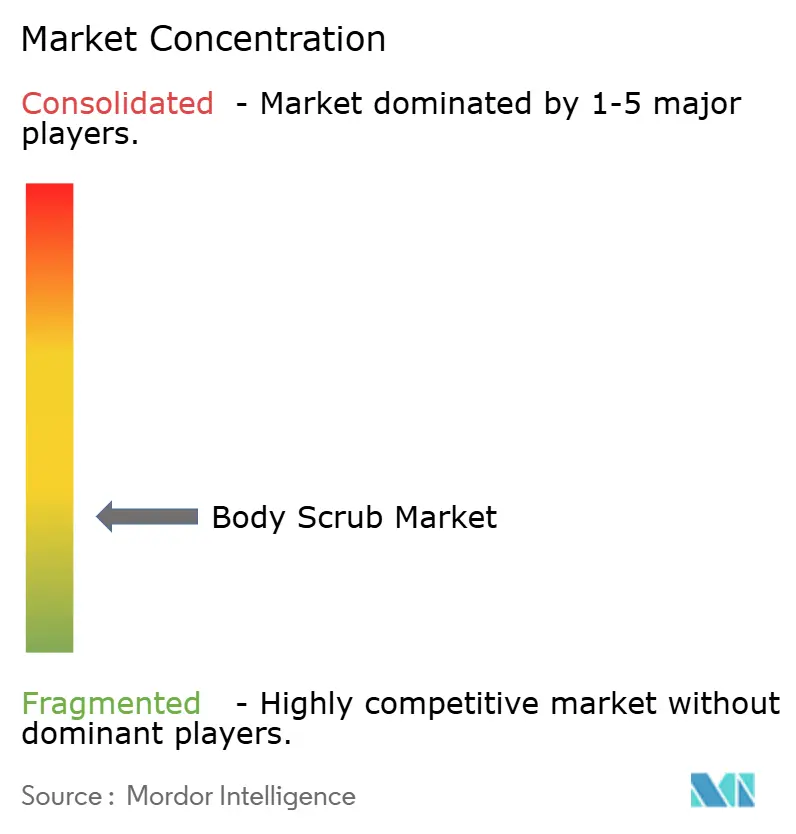

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Body Scrub Market Analysis by Mordor Intelligence

The body scrub market size is expected to grow from USD 2.70 billion in 2025 to USD 2.82 billion in 2026 and is forecast to reach USD 3.58 billion by 2031 at 4.88% CAGR over 2026-2031. Rising adoption of holistic self-care rituals, greater ingredient transparency, and the migration of performance skin-care actives into bath products underpin this upward trajectory. Coffee-based variants gain traction because caffeine’s lipolytic and antimicrobial properties are documented in peer-reviewed literature, encouraging premium pricing. Powder exfoliants capitalize on preservative-free positioning and lower shipping weights, making them e-commerce friendly. Meanwhile, online retail reshapes competitive dynamics by removing slotting fees and enabling direct-to-consumer storytelling, a shift that pressures supermarkets to create sensory retail experiences. Regulatory reforms, such as the European Union’s ban on rinse-off microplastics, accelerate reformulation toward natural abrasives and reward suppliers that can verify sustainable sourcing.

Key Report Takeaways

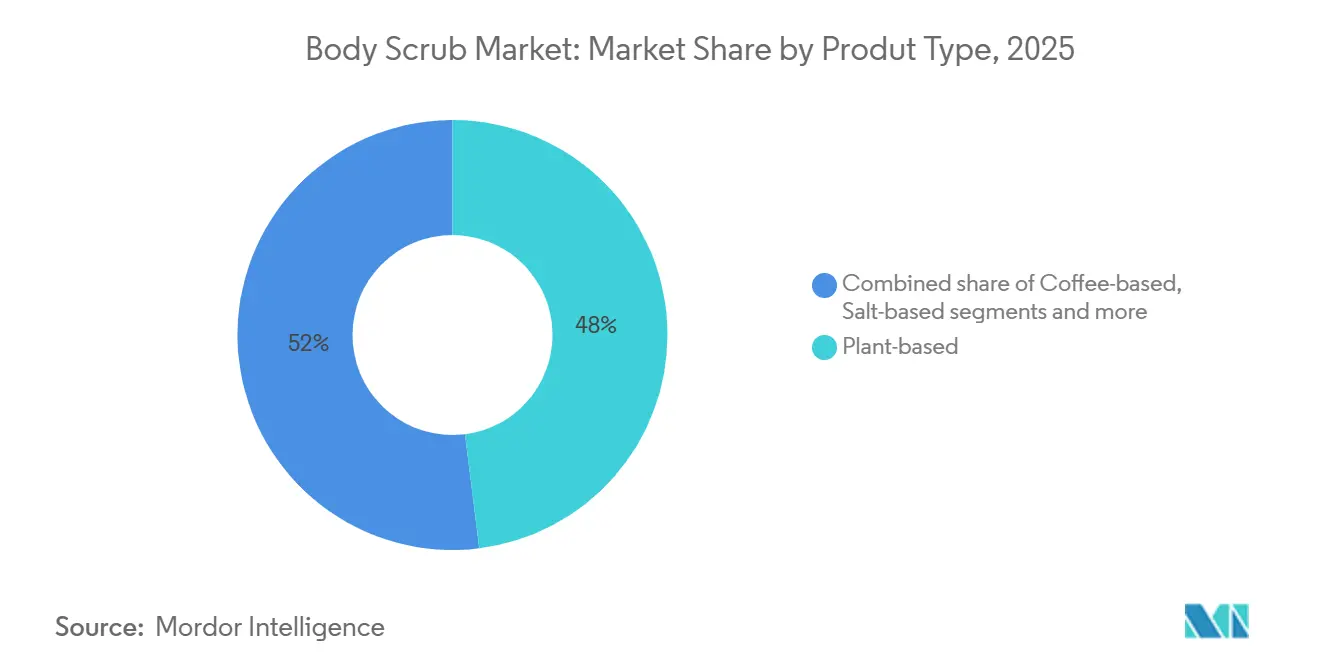

- By product type, plant-based scrubs led with 48.02% revenue share of the body scrub market size in 2025, while coffee-based variants are projected to advance at a 5.28% CAGR through 2031.

- By form, cream formats accounted for a 41.57% share of the body scrub market size in 2025, and powder exfoliants are forecast to register a 6.01% CAGR from 2026 to 2031.

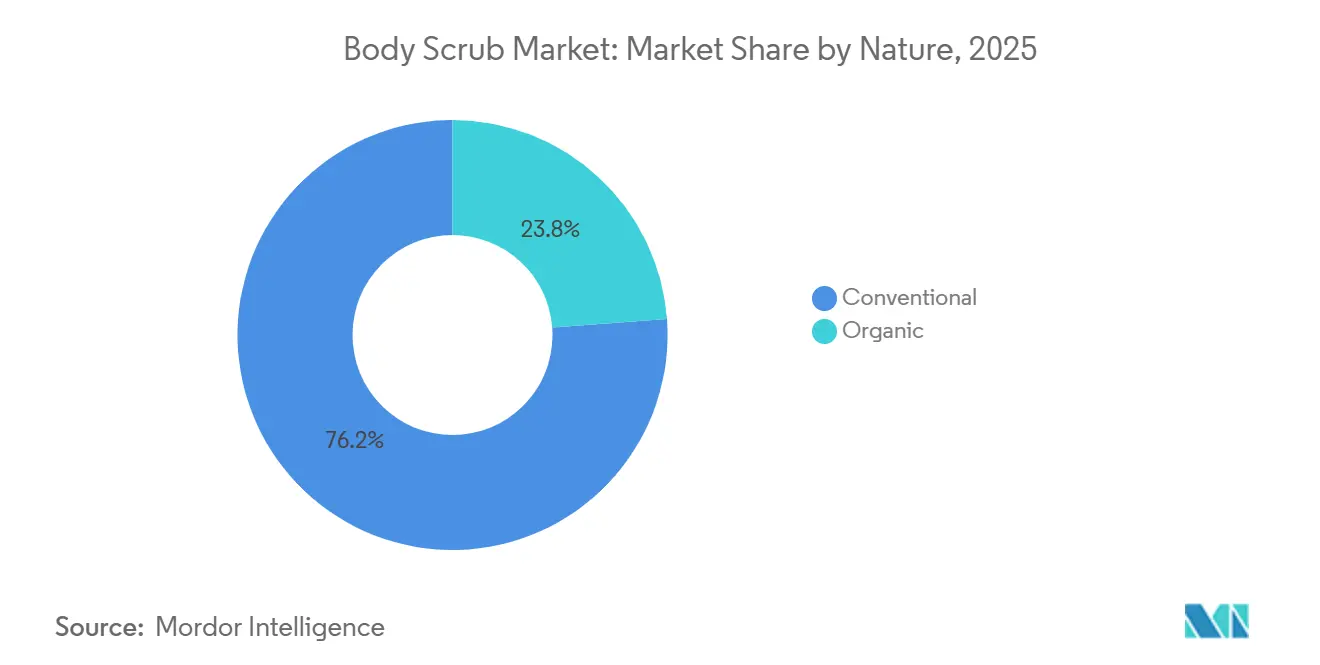

- By nature, the conventional segment held 76.19% of the body scrub market share in 2025; organic alternatives are poised for 5.87% CAGR growth over 2026-2031.

- By distribution channel, supermarkets and hypermarkets secured 30.98% revenue share in 2025, whereas online retail stores are expected to expand at a 6.62% CAGR to 2031.

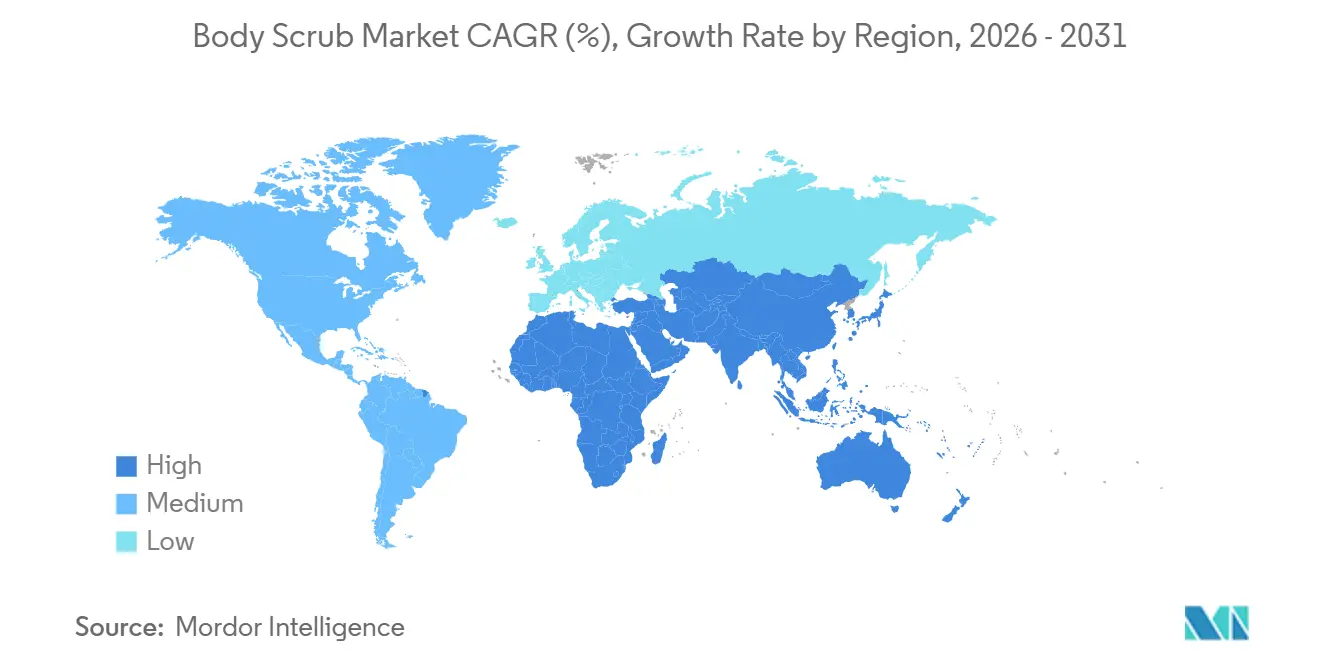

- By geography, Asia-Pacific commanded 46.45% of 2025 revenue, and the Middle East and Africa region is anticipated to post the highest 6.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Body Scrub Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer focus on skincare routines and holistic self-care | +1.1% | Global, with strongest adoption in Asia-Pacific (India, China, South Korea), North America, and Western Europe | Medium term (2-4 years) |

| Demand for dermatologist-inspired and results-driven skincare solutions | +0.9% | North America and Europe lead, expanding to urban Asia-Pacific markets (Singapore, Hong Kong, Tokyo) | Medium term (2-4 years) |

| Growing demand for multifunctional and performance-driven formulations | +1.0% | Global, with early adoption in North America and Europe, rapid uptake in Asia-Pacific premium segments | Medium term (2-4 years) |

| Strong impact of social media, influencers, and emerging beauty trends | +1.4% | Global, with peak influence in North America, Europe, and urban Asia-Pacific markets (particularly Gen Z and Millennial demographics) | Short term (≤ 2 years) |

| Rising preference for natural, clean-label, and environmentally responsible products | +1.2% | Global, particularly North America, Western Europe, and affluent Asia-Pacific segments; emerging in Middle East urban centers | Medium term (2-4 years) |

| Expanding male grooming segment supporting category growth | +0.8% | Global, with strongest momentum in North America, Europe, and urban Asia-Pacific; gradual adoption in Middle East and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer focus on skincare routines and holistic self-care

Consumer preferences are increasingly shifting towards skincare routines and holistic self-care, driving demand for body scrubs as part of comprehensive at-home spa rituals. Exfoliation is now viewed as a key step that combines cleansing, treatment, and relaxation, supported by rising personal care expenditures, such as the projected GBP 37.9 billion spent by UK households on personal care products and services in 2024, as per the Office for National Statistics (UK) [1]Source: Office for National Statistics (UK), "Consumer Trends: Q4 2024," ons.gov.uk . Body scrubs are evolving into multi-functional products that address hydration, brightening, and specific concerns like ingrown hairs or uneven texture, aligning with consumer expectations for products that deliver multiple benefits. Brands like Dove exemplify this trend by offering scrubs that combine exfoliation with moisturizing properties, integrating seamlessly into weekly self-care routines. Additionally, heightened awareness of ingredient safety and skin barrier health is driving demand for natural, plant-based, and "clean" formulations, often featuring botanicals and essential oils. Premium and masstige brands are capitalizing on this behavior by offering coordinated product ranges, enhancing consumer loyalty, and category value. Regional markets, such as Asia-Pacific, are also contributing to this shift, emphasizing traditional ingredients and ritual-inspired usage, further supporting growth in the body scrub market.

Growing demand for multifunctional and performance-driven formulations

The growing preference for multifunctional, performance-driven formulations is reshaping consumer expectations in the body scrub market. Products that integrate cleansing, exfoliation, and treatment functions are gaining traction among time-pressed individuals seeking efficient solutions with visible results. Hybrid formulations combining physical exfoliants, such as crystals, with chemical actives, such as AHAs, BHAs, or PHAs, address concerns like keratosis pilaris, dullness, and ingrown hairs, enabling a single application to cleanse, exfoliate, and treat skin issues. For instance, Frank Body introduced scrubs in 2025 designed to combat breakouts while enhancing skin smoothness, appealing to consumers prioritizing efficacy in streamlined routines. Similarly, Dove Men+Care launched all-in-one body and face scrubs in 2025 that scrub, cleanse, and moisturize, catering to men seeking simplified grooming solutions. Manufacturers are also incorporating active ingredients like hyaluronic acid, vitamin C, and retinol, transforming scrubs into multifunctional treatments that improve skin texture and enhance product absorption. Social media demonstrations showcasing quick, multi-benefit applications further amplify demand. Additionally, premium textures, sensorial elements, and eco-friendly exfoliants enhance product appeal, addressing both performance and sustainability concerns. These innovations, driven by brands like Frank Body and Dove Men+Care, are fueling growth by aligning with consumer demand for effective, time-saving body care solutions.

Strong impact of social media, influencers, and emerging beauty trends

Social media platforms such as TikTok and Instagram are significantly influencing the body scrub market by democratizing body care education through viral demonstrations of exfoliation techniques, before-and-after transformations, and routine integrations that position scrubs as essential skincare steps. The global online population grew by over 240 million by 2025, reaching approximately 6 billion users, as per the International Telecommunication Union (ITU), offering brands unprecedented opportunities to showcase product benefits and drive impulse purchases [2]Source: International Telecommunication Union (ITU), "Global Number of Internet Users Increases, but Disparities Deepen Key Digital Divides," itu.int. Influencers play a critical role by sharing authentic reviews, tutorials, and promotional codes, fostering trust and educating consumers on safe usage, which boosts the adoption of innovative scrub formats. For example, Tree Hut has leveraged TikTok virality with its Shea Sugar Scrubs, where influencers highlight silky results and appealing scents, driving significant sales spikes and bestseller status on platforms like Amazon. Emerging trends, such as glass skin-inspired body care, coffee scrubs for cellulite reduction, and glow-enhancing hybrids, further fuel demand as creators experiment and share DIY-inspired hacks. Social commerce features like TikTok Shop and Instagram Shops enable seamless purchasing, while AI-driven recommendations personalize product suggestions. This ecosystem of influencer authenticity, viral trends, and frictionless e-commerce is reshaping consumer behavior and driving sustained growth and innovation in the body scrub market.

Rising preference for natural, clean-label, and environmentally responsible products

Consumer demand for natural, clean-label, and environmentally responsible products is reshaping the personal care industry, with a notable shift toward body scrubs formulated without synthetic chemicals, microplastics, or harsh preservatives. Biodegradable exfoliants such as sugar, salt, coffee grounds, and fruit enzymes are gaining traction, aligning with wellness values and reducing ecological impact. Data from 2024 indicates that 74% of buyers prioritize organic ingredients in personal care products, reflecting a growing emphasis on transparency and safety, as per the National Sanitation Foundation [3]Source: National Sanitation Foundation, "74% of Consumers Consider Organic Ingredients Important in Personal Care Products," nsf.org . Brands like Herbivore Botanicals are responding with offerings such as the Coco Rose Body Polish, a vegan scrub featuring virgin coconut oil, Damascus rose, and quartz crystal, appealing to eco-conscious consumers seeking certified natural ingredients and sustainable packaging. Additionally, environmentally responsible sourcing practices, including the use of fair-trade shea butter, upcycled botanicals, and recyclable jars, are resonating with consumers avoiding plastic-based microbeads. Clean-label innovation emphasizes short, recognizable ingredient lists with superfoods like hibiscus or seaweed for antioxidant benefits, addressing rising sensitivity concerns. Ethical certifications such as USDA Organic and EWG Verified further reassure consumers, supporting premium pricing. Retailers are enhancing visibility through dedicated natural beauty aisles and online filters, while multifunctional scrubs that cleanse, exfoliate, and hydrate meet the needs of time-conscious, values-driven shoppers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from non-scrub exfoliation alternatives such as acids and enzymes | -0.9% | Global, with strongest adoption in North America, Europe, and urban Asia-Pacific markets influenced by dermatologist recommendations | Medium term (2-4 years) |

| Concerns over skin barrier damage and irritation from excessive exfoliation | -0.7% | Global, particularly among dermatologist-influenced consumers in developed markets (North America, Europe, Japan, Australia) | Short term (≤ 2 years) |

| Tightening regulations and ingredient restrictions across regions | -0.5% | Primarily Europe (EU Regulation 1223/2009), North America (FDA oversight), with spillover effects in Asia-Pacific markets adopting similar standards | Long term (≥ 4 years) |

| High price sensitivity in mass and mid-tier consumer segments | -0.6% | Global, with acute impact in price-sensitive markets (South America, Southeast Asia, Middle East and Africa mass segments, Eastern Europe) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from non-scrub exfoliation alternatives such as acids and enzymes

The increasing preference for non-scrub exfoliation alternatives, such as acids and enzymes, is impacting the demand for traditional body scrubs. Time-pressed consumers are opting for gentler, mess-free solutions like chemical peels, enzymatic lotions, peel pads, and dry brushing tools, which provide effective exfoliation without physical abrasion. These alternatives appeal to individuals with sensitive skin, addressing concerns about micro-tears caused by granules. Products featuring active ingredients like AHAs, BHAs, PHAs, or papaya enzymes offer seamless exfoliation during showers or as leave-on treatments. For instance, Paula's Choice expanded its 2% BHA Body Smoothing Lotion line, catering to consumers seeking simplicity and performance. Rising ingredient consciousness also drives demand for enzyme-based options derived from natural sources, such as pumpkin or pineapple, with buyers prioritizing organic ingredients in personal care products. Additionally, tools like dry brushes and exfoliation mitts are gaining traction, promoting lymphatic benefits and reducing reliance on bottled exfoliants. While premium brands introduce hybrid scrubs with mild acids, non-scrub options emphasizing dermatologist-backed efficacy for concerns like keratosis pilaris are gaining market share. Social media tutorials and convenience factors further accelerate the adoption of these alternatives, pressuring traditional body scrub formats to innovate.

Concerns over skin barrier damage and irritation from excessive exfoliation

Concerns about skin barrier damage and irritation from excessive exfoliation are influencing consumer behavior, as the abrasive particles in physical scrubs can cause microtears, dryness, inflammation, and heightened sensitivity. This has led to reduced usage or a preference for gentler alternatives, aligning with self-care trends that emphasize skin health and wellness. Brands like Dear Doer The Hidden Body Scrub & Wash are responding by formulating milder scrubs with hyaluronic acid to restore moisture post-exfoliation, addressing consumer priorities around barrier integrity. Harsh exfoliants, such as walnut shells or coarse salts, exacerbate issues like redness and infection, driving demand for biodegradable, clean-label substitutes that minimize irritation while maintaining efficacy. Dermatologists caution against frequent use, as over-exfoliation disrupts the lipid barrier, accelerates aging, and triggers breakouts, which conflicts with consumer expectations for multifunctional products. Social media influencers further amplify these concerns by advocating "exfoliation sabbaticals" and highlighting the negative effects of overuse, boosting interest in chemical or enzymatic alternatives. Ingredient-conscious consumers increasingly favor natural, soothing botanicals that support barrier resilience, prompting brands to develop hybrid products that balance exfoliation with calming actives. However, persistent concerns about abrasiveness and the need for recovery phases continue to impact product usage frequency and market loyalty, driving innovation toward safer, gentler formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coffee-Based Variants Leverage Functional Claims

The plant-based segment held the largest share of 48.02% in 2025, driven by its diverse ingredient offerings such as walnut shell, apricot kernel, and bamboo. These scrubs align with clean beauty trends emphasizing natural sourcing and sustainability. However, as the segment matures, its growth rate is slowing compared to coffee-based scrubs, which are gaining traction due to their science-backed benefits. Coffee scrubs are projected to grow at a CAGR of 5.28% from 2026 to 2031, supported by caffeine's clinically validated firming and antioxidant properties. This shift reflects a consumer preference for ingredients with proven efficacy over purely botanical appeal. Brands like mCaffeine are capitalizing on this trend by offering coffee scrub formats in various sizes and variants, combining exfoliation with antioxidant and resurfacing benefits to meet the demand for performance-driven skincare.

Salt-based scrubs maintain niche appeal through their mineral-rich positioning, particularly in Middle Eastern markets where Dead Sea salt holds cultural significance. However, their coarse texture may limit adoption among consumers seeking gentler alternatives. Sugar-based scrubs, categorized under "Others," dissolve during application, reducing abrasion risks and appealing to price-sensitive buyers due to lower manufacturing costs. Milk-based scrubs, featuring lactic acid for hydration and exfoliation, are confined to premium tiers due to formulation complexity and shorter shelf life, highlighting how ingredient science and consumer safety perceptions shape market dynamics.

By Form: Powder Formats Capture Clean-Beauty Advocates

Cream formats held the largest share of 41.57% in 2025, driven by their rich textures that convey sensory luxury and shelf stability, making them suitable for mass retail distribution. Their pre-emulsified consistency ensures convenience and predictable performance, appealing to mainstream consumers seeking ready-to-use solutions. However, growth in this segment is slowing as consumers increasingly question the value of paying for water content when powder concentrates offer comparable exfoliation at a lower per-use cost. Gel and liquid scrubs, while offering pump-based convenience, require preservatives such as phenoxyethanol, which are facing growing scrutiny from clean-beauty advocates. This shift in consumer preferences is gradually steering demand toward minimalist formulations perceived as more sustainable and transparent.

Powder exfoliants are projected to grow at a CAGR of 6.01% from 2026 to 2031, challenging traditional cream formats. Zero-water formulations eliminate the need for preservatives and align with clean-beauty trends, while their water-activated nature allows consumers to customize textures for different uses, enhancing versatility and value. Additionally, reduced shipping weight benefits e-commerce distribution by lowering logistics costs and enabling compact packaging. Sustainability further strengthens their appeal, as powders are often packaged in recyclable aluminum tins or compostable pouches. Products like YOGHBODY® Relax Peeling Body Powder with Lavandin highlight the potential of concentrated formats to deliver professional-grade results without unnecessary fillers, aligning with consumer priorities of efficacy, transparency, and environmental responsibility.

By Nature: Organic Certification Becomes Premium Table Stakes

Conventional body scrubs held the largest market share at 76.19% in 2025, driven by affordability and formulation flexibility. Synthetic emulsifiers and preservatives in these products provide a shelf life of up to 36 months, compared to 12–18 months for organic alternatives. This extended stability simplifies inventory management and supports broader geographic distribution, particularly in emerging markets. However, in developed economies where disposable incomes enable premiumization, conventional offerings are gradually losing ground as consumers increasingly prioritize certification-backed transparency. Certifications such as USDA Organic, Ecocert, and COSMOS are becoming baseline requirements in higher price segments, shifting consumer preferences toward organic products.

Organic scrubs are projected to grow at a CAGR of 5.87% from 2026 to 2031, eroding the dominance of conventional products. Certification costs, ranging from USD 500 to USD 2,000 annually for USDA Organic, along with mandatory audits, create structural entry barriers favoring established brands with sourcing scale and compliance capabilities. Retailers like Sephora and Ulta Beauty are institutionalizing clean-beauty standards by allocating shelf space based on these frameworks, compelling brands to reformulate or risk delisting. Brands such as KORA Organics leverage certified organic positioning to align with retailer mandates and build trust among ingredient-conscious consumers. Together, certification economics, retailer influence, and evolving consumer trust standards are redefining competitive dynamics, with organic positioning increasingly viewed as a measure of credibility rather than optional differentiation.

By Distribution Channel: Online Retail Disrupts Traditional Gatekeepers

Supermarkets and hypermarkets accounted for the largest share of sales in 2025, contributing 30.98% to the body scrub market. Their success is driven by convenience and impulse buying, although growth is moderating as consumers increasingly plan purchases online to compare ingredients and read reviews. Brands like Tree Hut demonstrate a hybrid strategy, leveraging mass retail partnerships with outlets such as Target and Walmart to build awareness while capturing high-intent buyers through digital platforms. These platforms cater to specific consumer searches, such as AHA-infused sugar scrubs, enabling brands to meet targeted demand. Pharmacies, salons, and direct selling channels continue to play niche roles but lack the scale to significantly influence the overall market structure.

Online retail channels are projected to grow at a CAGR of 6.62% from 2026 to 2031, challenging traditional retail formats by eliminating costs like slotting fees and promotional allowances. This cost flexibility allows brands to focus on product innovation and digital marketing, benefiting emerging players that rely on influencer partnerships and ingredient transparency. Specialty and beauty stores remain relevant through experiential merchandising, including testers and consultations, but rising commercial rents and stagnant foot traffic are compressing margins. As digital discovery increasingly shapes purchasing decisions, online platforms are becoming central to brand storytelling and conversion efficiency. Sustained investment in last-mile delivery infrastructure and disciplined pricing strategies will be critical to maintaining growth and avoiding brand dilution from unauthorized discounting.

Geography Analysis

Asia-Pacific accounted for 46.45% of the projected 2025 revenue in the body scrub market and is expected to sustain its growth trajectory through 2031. This performance is driven by India’s expanding middle class and China’s increasing focus on premiumization. While China’s body-care category trails facial skincare in per-capita spending, value growth is supported by consumers opting for imported brands perceived as safer and more effective, reflecting a shift toward quality over quantity. Brands such as L'Occitane en Provence benefit from this trend by positioning natural exfoliants in upscale retail environments. Japan’s established bath culture further drives demand for body exfoliants, embedding scrubs into routine self-care practices rather than occasional use. This cultural normalization of bathing rituals supports consistent consumption patterns across urban demographics, reinforcing Asia-Pacific’s leadership in the market.

The Middle East and Africa region is projected to record the fastest growth, with a 6.50% CAGR from 2026 to 2031. This expansion is attributed to youthful populations, high social media penetration, and ongoing economic diversification. In Saudi Arabia, the Saudi Vision 2030 initiative channels investments into retail and beauty infrastructure, aligning personal care market growth with broader non-oil sector objectives. Halal certification requirements create competitive advantages for brands capable of meeting religious compliance and ensuring ingredient transparency. The United Arab Emirates operates as a regional beauty hub, supported by high disposable incomes and expatriate demand for global brands. However, fragmented distribution networks, where independent pharmacies dominate over organized retail, pose challenges for smaller players lacking established distributor partnerships. South Africa anchors sub-Saharan consumption, while Nigeria and Egypt offer significant demographic potential but require climate-adapted formulations and melanin-sensitive product positioning to remain competitive.

North America and Europe maintain substantial market shares but face challenges from maturity-driven saturation, compelling brands to differentiate through multifunctional product claims and sustainable packaging innovations. Regulatory changes, such as the European Union’s microplastic ban introduced in October 2023, have intensified the shift toward natural exfoliants and biodegradable alternatives. In South America, macroeconomic instability in countries like Argentina and Colombia limits discretionary spending, influencing pricing strategies and promotional activities. However, smaller yet more stable markets such as Chile and Peru present opportunities for gradual premiumization. Across these regions, regulatory developments, economic volatility, and sustainability imperatives collectively shape competitive dynamics, extending beyond pure volume growth.

Competitive Landscape

Multinational conglomerates such as Unilever, Procter & Gamble, L'Oréal, and Estée Lauder hold the largest share in the body scrub market, leveraging their scale advantages in sourcing, manufacturing, and global distribution. Their diversified portfolios enable cross-category bundling, allowing body scrubs to benefit from established skincare brand equity and strong retail partnerships. These companies dominate shelf space in supermarkets and specialty beauty chains, supported by significant promotional budgets and in-store merchandising. Their research and development capabilities facilitate reformulations to comply with clean-beauty regulations and address ingredient scrutiny. However, their scale can limit agility in responding to micro-trends driven by social media. To address this, these conglomerates increasingly adopt hybrid strategies, including acquiring or incubating niche brands to maintain relevance and competitiveness.

Direct-to-consumer (DTC) brands such as Glossier, mCaffeine, and Mamaearth are disrupting traditional retail models by prioritizing digital engagement and influencer-led marketing. Their online-first approach eliminates dependency on physical shelf space, enabling rapid product iterations based on consumer feedback. By emphasizing ingredient transparency and community-driven branding, these brands appeal to younger demographics seeking authenticity and functional benefits. This agility allows them to respond quickly to trends such as coffee-based exfoliation and clean-label positioning. Additionally, their lower overhead costs enable reinvestment into targeted advertising rather than large-scale retail promotions, reshaping competitive benchmarks around speed, personalization, and narrative control.

Regional specialists like Forest Essentials and Clarins further diversify the competitive landscape by anchoring differentiation in heritage, botanicals, and premium spa associations. These brands often command higher price points through artisanal positioning and luxury retail partnerships, reinforcing exclusivity. Their strength lies in localized storytelling, such as Ayurvedic authenticity in India or plant science expertise in Europe, which resonates strongly with domestic and diaspora markets. However, scaling beyond core geographies requires navigating distribution complexities and regulatory variations. The coexistence of conglomerates, DTC disruptors, and regional specialists underscores the market’s moderate fragmentation, with competitive advantage hinging on balancing scale efficiency, brand authenticity, and evolving consumer expectations.

Body Scrub Industry Leaders

-

L'Oréal SA

-

Estée Lauder Companies Inc.

-

Unilever PLC

-

Procter & Gamble Co.

-

Natura & Co Holding S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Indian skincare company Foxtale announced its transition from a direct-to-consumer model to a house of brands with the launch of Hula Hoop by Foxtale. The new brand debuted with four products: Brightening Body Wash, Exfoliating Body Wash, Brightening Body Lotion, and Exfoliating Body Scrub. These products were made available on the brand's e-commerce platform and through various multi-brand retailers.

- August 2025: Everyday by Frank Body launched its largest product offering to date. This release reintroduced Frank Body’s signature product format, the scrub, under the Everyday by Frank Body brand. It included four new products aimed at addressing breakouts, exfoliating the skin, and delivering visible results, all priced under AUD 16. The new additions were Clearing Body Scrub, Brightening Body Scrub, Clearing Face Scrub, and Clearing Spot Pen.

- August 2025: Pattern by Tracee Ellis Ross launched a body care line. The collection included a Moisturizing Body Wash with aloe vera and olive oil, a Nourishing Body Oil, a Hydrating Body Lotion, a Moisture Rich Body Cream, and a Dry Exfoliating Body Scrub for use on dry skin before bathing. All products featured the brand's Midnite Amber scent, blending amber, musk, bergamot, citrus, and floral notes.

- February 2025: Dove Men+Care announced the launch of its Body and Face Scrubs, designed to streamline grooming routines by combining scrubbing, cleansing, and moisturizing in a single product. The scrubs were made available in three distinct scents: Eucalyptus + Cedar Oil, Coastal Cedar + Bergamot, and Charcoal + Clove Oil, offering a refreshing experience.

Global Body Scrub Market Report Scope

A body scrub is a skincare product designed to exfoliate the skin by removing dead skin cells, dirt, and oil from the skin's surface. Body scrubs can be made with various exfoliating particles, such as sugar, salt, coffee grounds, or crushed fruit pits, mixed with oils or other nourishing ingredients.

The global body scrub market has been segmented by product type into herbal, organic, and chemical-based scrubs. By form, body scrubs have been widely classified into powder, gel or liquid, and cream. Further, according to the skin type, they are differentiated into the ones made specifically for sensitive, normal, dry, and oily skin. The body scrub market is segmented by distribution channel into supermarkets/hypermarkets, independent retailers, convenience/grocery stores, online retail stores, and other distribution channels. Lastly, the report offers an analysis of major economies worldwide, including North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

The report offers the market sizes and forecasts in terms of value (USD million) for all the above segments.

| Plant-based |

| Salt-based |

| Coffee-based |

| Others (Sugar-based, Milk-based, etc.) |

| Powder |

| Gel/Liquid |

| Cream |

| Organic |

| Conventional |

| Supermarkets/Hypermarkets |

| Specialty and Beauty Stores |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Plant-based | |

| Salt-based | ||

| Coffee-based | ||

| Others (Sugar-based, Milk-based, etc.) | ||

| By Form | Powder | |

| Gel/Liquid | ||

| Cream | ||

| By Nature | Organic | |

| Conventional | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty and Beauty Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue for body scrubs in 2031?

The body scrub market size is forecast to reach USD 3.58 billion by 2031.

Which product type is growing fastest?

Coffee-based variants are expected to grow at a 5.28% CAGR between 2026 and 2031 due to caffeine’s documented skin-firming benefits.

Which sales channel will gain the most share by 2031?

Online retail stores are projected to advance at a 6.62% CAGR, riding direct-to-consumer models and augmented-reality shopping tools.

Why is male grooming significant for category growth?

Dedicated men’s scrubs like Dove Men+Care address functional needs, ingrown-hair prevention and post-workout cleansing, bringing new demographics into regular exfoliation routines, thereby expanding overall category volume.

Page last updated on: