Personal Care Wipes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 15.85 Billion |

| Market Size (2031) | USD 20.15 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

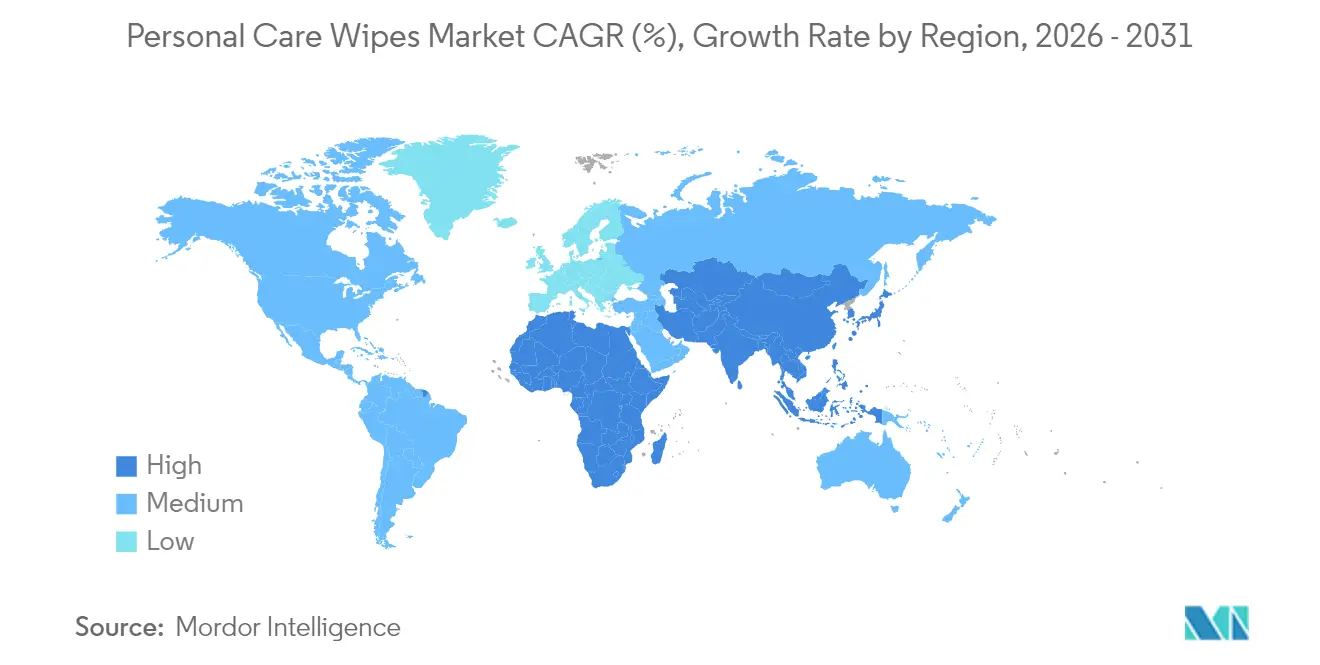

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Care Wipes Market Analysis by Mordor Intelligence

The personal care wipes market size is projected to expand from USD 14.89 billion in 2025 and USD 15.85 billion in 2026 to USD 20.15 billion by 2031, registering a CAGR of 4.92% between 2026 and 2031. Sustained consumer preference for quick, single-use hygiene formats, new regulatory scrutiny over ingredient safety, and accelerating substrate innovation together reinforce the structural momentum behind the personal care wipes market. The U.S. Modernization of Cosmetics Regulation Act now requires facility registration and adverse-event reporting, lifting compliance costs yet raising consumer trust in product safety. Europe’s ban on plastic-containing wet wipes has shifted procurement toward cellulose, lyocell, and PLA, prompting global supply-chain redesigns. Strengthening flushability labeling standards in North America and a pronounced premiumization trend in the Asia-Pacific further differentiate growth pockets inside the personal care wipes market. Finally, direct-to-consumer subscription models help brands bypass shelf-space constraints and gather high-frequency preference data, reinforcing pricing power despite raw-material volatility.

Key Report Takeaways

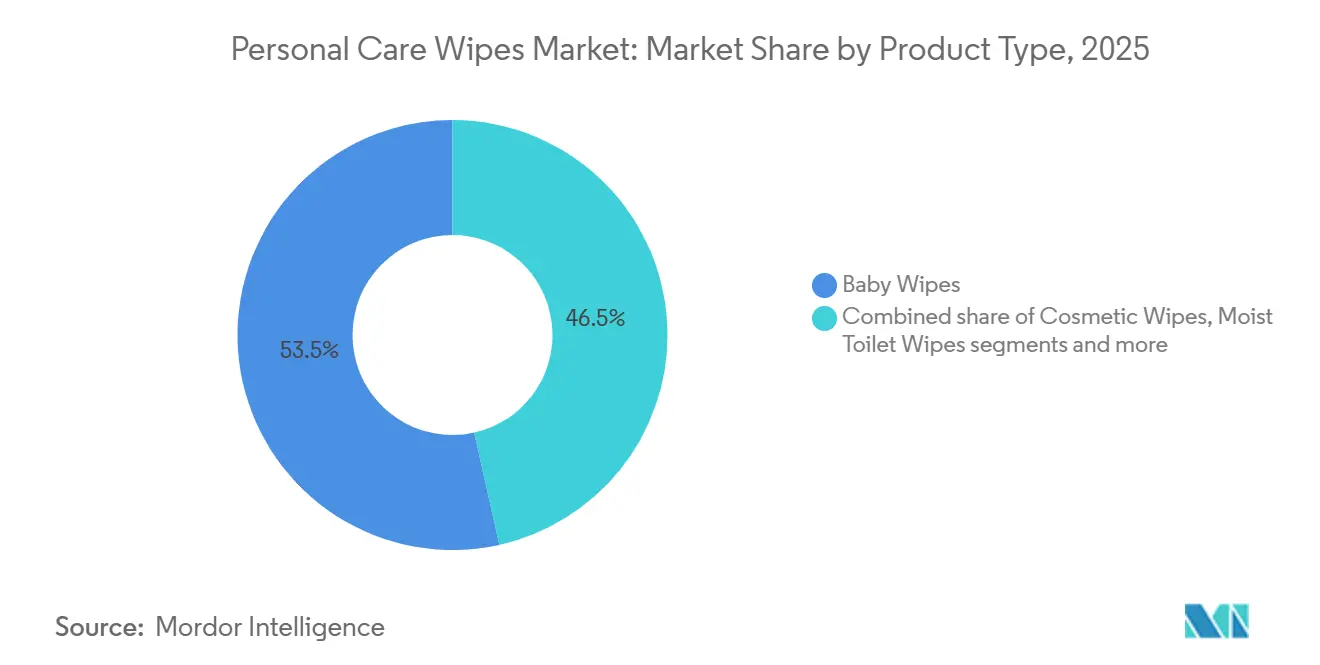

- By product type, baby wipes led with 53.48% of the personal care wipes market share in 2025, while cosmetic wipes are forecast to advance at a 6.23% CAGR through 2031.

- By ingredient, natural and organic variants captured 34.51% of 2025 volume and are progressing at a 6.68% CAGR to 2031.

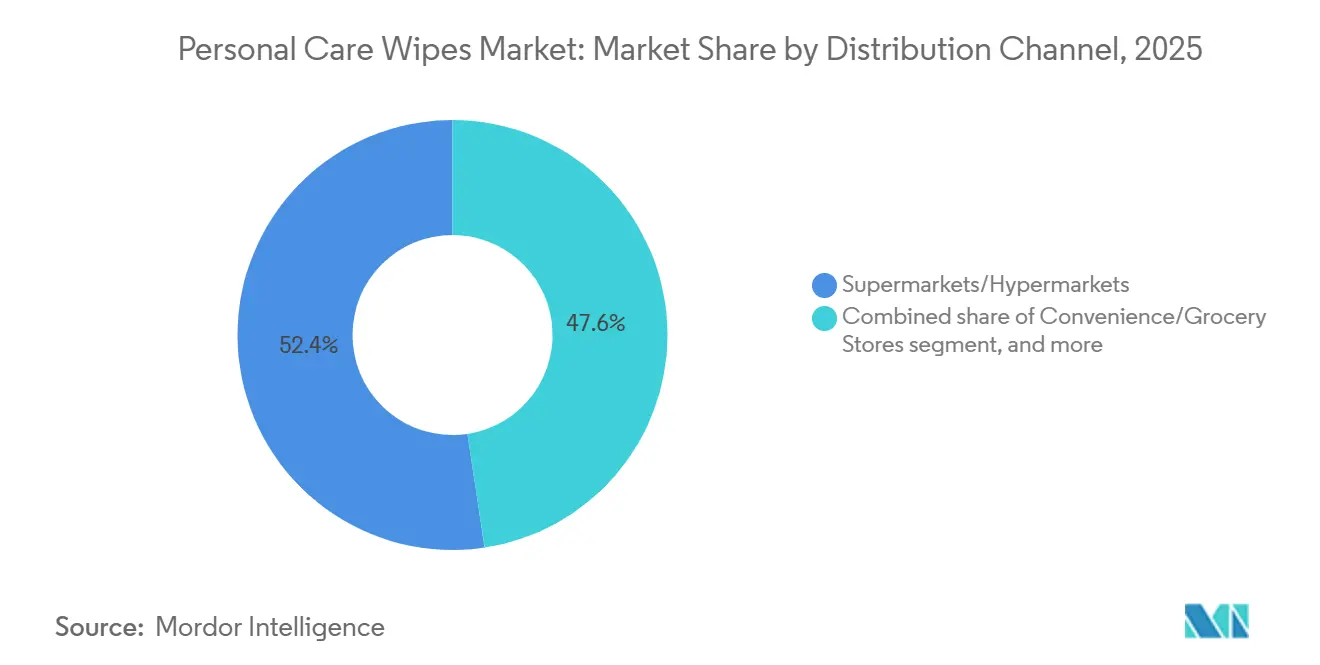

- By distribution channel, online retail accounted for the fastest growth, expanding at a 7.05% CAGR between 2026 and 2031 and narrowing the gap with supermarkets that dominated in value terms.

- By geography, North America generated 40.28% revenue in 2025; Asia-Pacific represents the quickest expansion, rising at 6.88% annually through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Care Wipes Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Health And Hygiene Awareness | +1.2% | Global, with peaks in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Rising Demand For Natural, Organic, And Clean Hygiene Products | +1.0% | North America and Europe core, expanding to urban Asia-Pacific | Long term (≥ 4 years) |

| Growing Popularity Of Sustainable And Biodegradable Wipes | +0.8% | Europe leadership, North America adoption, Asia-Pacific emerging | Long term (≥ 4 years) |

| Product Innovation In Functionality And Fragrance | +0.7% | Global, with R&D concentrated in Japan, South Korea, and United States | Medium term (2-4 years) |

| Urbanization Driving Demand For Quick Solutions | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Growth In E-Commerce Accessibility | +0.6% | Global, accelerated in North America, Europe, and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Health and Hygiene Awareness

Post-pandemic hygiene protocols have become embedded in daily routines, sustaining demand for single-use wipes even as acute infection fears recede. The U.S. Centers for Disease Control and Prevention continues to recommend surface disinfection in high-traffic environments, which has normalized the use of antimicrobial wipes in households and commercial settings. This behavioral stickiness is particularly pronounced among parents of young children, where baby wipes serve dual purposes, diaper changes and rapid surface cleaning, reducing the price elasticity of demand. Regulatory agencies in Japan and South Korea have tightened microbiological safety standards for wipes intended for infant use, requiring manufacturers to validate preservative efficacy against Pseudomonas aeruginosa and Staphylococcus aureus, which raises formulation complexity but also creates barriers to entry for smaller brands

Rising Demand for Natural, Organic, and Clean Hygiene Products

Consumers are scrutinizing ingredient lists with the rigor once reserved for food labels, driving brands to reformulate around plant-derived surfactants and eliminate parabens, phthalates, and synthetic fragrances. The Honest Company's January 2025 launch of its Pure Aqua wipes line, featuring 99% water and organic cotton substrate, exemplifies this shift and has captured shelf space in premium retail channels despite a 20-30% price premium over conventional alternatives. COSMOS certification, administered by the European Natural and Organic Cosmetics Association, has become a de facto requirement for brands targeting millennial and Gen Z consumers in Western Europe, where 42% of personal-care purchasers report actively seeking certified-organic claims. This trend is now diffusing into Asia-Pacific, where South Korea's Ministry of Food and Drug Safety introduced a "green cosmetics" labeling framework in 2024, creating regulatory tailwinds for natural formulations[1]Source: Ministry of Food and Drug Safety Korea, “Green Cosmetics Policy,” mfds.go.kr.

Growing Popularity of Sustainable and Biodegradable Wipes

The United Kingdom's October 2024 prohibition on plastic-containing wet wipes has catalyzed substrate innovation across the industry, with manufacturers pivoting to lyocell, viscose, and polylactic acid (PLA) blends that meet ISO 14855 aerobic biodegradation standards. Kimberly-Clark de México's 2024 introduction of Honeykeeper biodegradable baby wipes, which achieve 85% biodegradation within 45 days under composting conditions certified by TÜV SÜD, demonstrates that performance parity with conventional non-wovens is now commercially viable. The European Union's Single-Use Plastics Directive, which mandates Extended Producer Responsibility for wipes manufacturers, is pushing brands to invest in closed-loop collection systems and chemical recycling partnerships, with early pilots in France and Germany showing 15-20% recovery rates for used wipes. These infrastructure investments are capital-intensive, but position compliant brands favorably as municipal waste-management authorities tighten landfill acceptance criteria.

Product Innovation in Functionality and Fragrance

Micellar-water technology, initially designed for facial cleansing, has now expanded into cosmetic wipes. This advancement enables quick and easy makeup removal in a single step, appealing to busy consumers. In December 2024, Yuhan Kimberly introduced "Kleenex My Bidet Pure," a flushable toilet wipe featuring a pH-balanced formulation and a plastic-free substrate. Released in South Korea, it is distributed through convenience stores, where limited shelf space favors products with multiple benefits. Fragrance innovation is evolving, with a shift toward microencapsulation techniques that release scents gradually during use. This enhances the perceived effectiveness of products and supports premium pricing. In 2024, Procter & Gamble filed patents for wipes containing probiotic strains aimed at promoting skin-microbiome health. Although this concept remains scientifically debated, it resonates with health-conscious consumers. Furthermore, accumulating clinical evidence could create new regulatory opportunities, as noted in the USPTO Patent Database[2]Source: U.S. Patent and Trademark Office, “Patent Database,” uspto.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Concerns And Waste Management Issues | -0.9% | Global, with regulatory pressure concentrated in Europe and North America | Long term (≥ 4 years) |

| Regulatory And Safety Compliance Challenges | -0.5% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Stricter Regulations On Ingredients And Disposal Hindering Market Growth | -0.6% | Europe leadership, North America following, Asia-Pacific selective enforcement | Long term (≥ 4 years) |

| Fluctuating Prices Of Non-Woven Fabrics And Chemicals Impacting Margins | -0.7% | Global, with acute exposure in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns and Waste Management Issues

Municipal wastewater systems in North America and Europe report that non-dispersible wipes are responsible for 20-30% of sewer blockages. These blockages result in annual remediation costs exceeding USD 1 billion and have prompted utilities to file lawsuits against manufacturers to recover these expenses, as noted by the Water Environment Federation[3]Source: Water Environment Federation, “Flushable Wipes and Wastewater,” wef.org. In 2024, the International Water Services Flushability Group revised its flushability test protocols, requiring wipes to disintegrate within 30 minutes under turbulent flow conditions. Most existing products fail to meet this standard, restricting the use of the "flushable" label and hindering growth in the moist toilet wipes segment. Landfill operators in California and New York have introduced surcharges on waste streams with high levels of synthetic textiles, including wipes, leading retailers to reconsider shelf space for non-biodegradable options. Consumer advocacy groups have intensified concerns about microplastic shedding from polypropylene-based wipes. Laboratory studies have identified fiber fragments in 60% of sampled wastewater effluent. This finding has influenced draft legislation in the European Parliament, proposing that wipes be classified as "problematic plastics" subject to phase-out timelines.

Fluctuating Prices of Non-Woven Fabrics and Chemicals Impacting Margins

During 2024-2025, polypropylene resin, the key feedstock for spunbond non-wovens, experienced price volatility of 25-35%. These fluctuations were primarily driven by crude oil price changes and disruptions in petrochemical supply chains across the Middle East and Asia. Manufacturers with limited vertical integration are under pressure, facing margin compression as retail prices remain inflexible due to intense competition and the rising presence of private labels in supermarkets. Kimberly-Clark Corporation's 2024 annual report highlighted that raw material inflation reduced operating margins by 150 basis points in its personal-care segment. To address this, the company expedited its USD 3.4 billion joint venture with Suzano to secure a long-term pulp supply at fixed prices. Smaller brands, particularly those lacking hedging mechanisms or long-term supply agreements, are especially at risk. This has led to market exits or consolidations among several regional players in South America and Southeast Asia in 2025. Furthermore, chemical preservatives such as phenoxyethanol and benzalkonium chloride saw price increases of 15-20%, driven by stricter environmental regulations in China that reduced production capacity and shifted supply-demand dynamics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Baby Wipes Dominance Faces Cosmetic Wipes Surge

Baby wipes captured 53.48% of the personal care wipes market size in 2025, supported by established usage for diaper changes and emergent roles in quick household cleaning. Cosmetic wipes, however, are expanding at a 6.23% CAGR through 2031, leveraging micellar-water technologies that compress multi-step Korean-inspired routines into portable sachets. Moist toilet wipes face growth constraints because most products cannot meet the IWSFG 30-minute disintegration standard, limiting their flushable positioning.

General-purpose wipes deliver cross-category utility yet suffer thinner margins, while intimate wipes remain small but are accelerating where pharmacy endorsement destigmatizes purchase. Competitive intensity is rising: Harper Hygienics’ Kindii Water Care launch and Procter & Gamble’s Pampers Pure Aqua extension both rely on plastic-free substrates and 99%-water formulas to resonate with ingredient-minimalist parents. Industry-wide, probiotic, fermented, and active-ingredient wipes illustrate how R&D is redefining value perception in the personal care wipes market. Regulatory scrutiny over preservatives injects further complexity; Europe’s SCCS opinions on formaldehyde-releasing agents are already sending formulators back to the lab.

By Ingredient: Natural and Organic Variants Outpace Conventional Formulations

Natural and organic wipes, featuring COSMOS or USDA Organic certifications, are experiencing a strong annual growth rate of 6.68%. This growth rate exceeds that of conventional wipes by a significant 176 basis points. However, conventional wipes are projected to maintain a dominant 65.49% share of the personal care wipes market in 2025, primarily due to their cost-effectiveness and better preservation under hot and humid logistical conditions. The COSMOS certification has become a key factor for shelf presence in Western Europe, with 42% of shoppers actively seeking products with certified claims.

Brands are adopting advanced preservation techniques, such as hurdle technology, which incorporates low water activity, chelators, and botanical peptides. These approaches help extend the shelf life of natural product lines while avoiding the use of parabens and phenoxyethanol. Unilever's 2024 patent filings emphasize plant-derived antimicrobial peptides, showcasing their ability to remain effective over 24 months of storage. Nonetheless, the market faces challenges as organic cotton and sustainably sourced cellulose incur feedstock premiums of 40% to 60%. These higher costs create difficulties for brands that cannot effectively pass them along the personal care wipes market value chain.

By Distribution Channel: Online Retail Disrupts Traditional Shelf Dynamics

Online retail is expected to grow at an annual rate of 7.05% through 2031, surpassing the growth of the overall personal care wipes market by nearly 200 basis points. The rise of subscriptions and direct-to-consumer platforms not only ensures a steady stream of recurring revenue but also facilitates the creation of extensive data repositories. These data insights enable companies to make swift and precise adjustments to product formulations, catering to evolving consumer preferences. Supermarkets, which accounted for 52.38% of the market's value in 2025, are now facing increasing competition from private-label brands. To address this challenge, major supermarket chains are introducing biodegradable and organic store-brand products, often priced at significant double-digit discounts to attract cost-conscious consumers.

WaterWipes has strategically leveraged Amazon’s auto-replenishment programs to secure long-term customer loyalty and maximize customer lifetime value. This innovative approach was a key factor in 3i Group’s decision to invest EUR 145 million in the company during 2024. Meanwhile, traditional brick-and-mortar retailers are adopting new strategies, such as implementing smart-shelf technology and creating curated premium product displays, to enhance the in-store shopping experience. Despite these efforts, e-commerce platforms continue to dominate as the preferred channel for launching new products. This preference is driven by the lower slotting fees associated with warehousing and the ability to gather rapid consumer feedback, which is critical for success in the highly competitive personal care wipes sector.

Geography Analysis

In 2025, North America contributed 40.28% of the revenue, driven by high per-capita usage and robust regulatory frameworks. The EPA's "Do Not Flush" icon, mandated since 2024, has reduced consumer confusion and saved municipalities USD 1 billion annually by preventing blockages. In Canada, the increasing birth rate among immigrant families supports the demand for baby wipes. Meanwhile, in Mexico, the expanding middle class now views wipes as everyday essentials rather than occasional luxuries. Companies are optimizing their portfolios; for example, Procter & Gamble divested in Argentina in 2024, reallocating resources to U.S. and Canadian markets, where premiumization trends help sustain gross margins.

Asia-Pacific is the fastest-growing region, with an annual growth rate of 6.88% projected through 2031. Urbanization rates exceeding 3% annually in India and Indonesia are driving demand for convenient product formats. Unicharm opened its Ahmedabad plant in February 2025, enhancing domestic production capacity. Concurrently, its Sofy East Africa initiative is transferring expertise from Asia to emerging African markets. In China, the premium segment is expanding as consumers shift to natural or imported brands, while domestic leader Hengan leverages vertical integration to maintain competitive pricing. In Japan, the aging population is fueling demand for adult-incontinence wipes, where gentle formulations and odour-control features are particularly valued.

Europe exerts significant regulatory influence on the personal care wipes market. The U.K.'s ban on plastic-containing wet wipes is driving a shift toward compostable alternatives. The EU's Extended Producer Responsibility increases production costs by 2-4%, but it also enhances brand reputation among environmentally-conscious consumers. In South America, growth is concentrated in Brazil and Argentina despite currency fluctuations. In contrast, per-capita wipes consumption in the Middle East and Africa remains below 10% of North American levels. However, ongoing investments in logistics and retail infrastructure in the United Arab Emirates and Saudi Arabia are paving the way for a gradual increase in the adoption of premium hygiene products by 2031.

Competitive Landscape

In 2025, Procter & Gamble, Kimberly-Clark, and Kenvue collectively accounted for approximately 45% of global sales in the personal care wipes market, signifying moderate consolidation. Their market dominance is attributed to their economies of scale in non-woven material procurement and well-established relationships with major retailers. In January 2026, Kimberly-Clark and Kenvue obtained regulatory approval for a planned merger, which is anticipated to be finalized later this year. This merger aims to integrate their baby-care and adult-incontinence product portfolios, thereby strengthening their negotiating power for raw materials and enhancing their competitive positioning.

Smaller, niche players such as WaterWipes and The Honest Company capitalize on their use of ultra-pure ingredients and direct-to-consumer strategies, enabling them to charge premium prices that are 30-40% higher than standard offerings. WaterWipes, supported by a capital infusion from 3i Group, is expanding its production capacity and entering new regional markets to solidify its leadership in the ultra-clean product segment. The competitive landscape is further shaped by patent activity, with Procter & Gamble focusing on microbiome-supporting wipes to enhance functionality branding, while Kimberly-Clark's patents on fiber dispersion technology could potentially unlock opportunities in the controversial flushable-wipe segment. Sustainability initiatives are also driving competition, as Essity has committed to using 100% renewable or recycled materials by 2030, putting pressure on other market players to accelerate their efforts in reducing carbon footprints and meeting environmental goals.

Digital commerce capabilities are increasingly becoming a key differentiator between market leaders and followers. Brands experimenting with smart-shelf sensors in convenience stores across Asia have reported a 10-15% reduction in out-of-stock situations, improving on-shelf availability without significantly increasing working capital requirements. Furthermore, subscription-based commerce models not only help reduce customer churn but also generate extensive data insights. These insights enable brands to enhance forecast accuracy and implement agile micro-segmentation strategies, thereby driving growth and efficiency within the personal care wipes market.

Personal Care Wipes Industry Leaders

The Procter & Gamble Company

Kimberly-Clark Corporation

Kenvue Inc.

Essity Hygiene and Health AB

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Coterie has launched 'The Flush Wipe' collection, featuring ultra-soft, 100% plant-derived, plastic-free fibers that are sewer and septic safe, disintegrating as well as toilet paper within 30 minutes when flushed. According to the brand, the wipes use a minimal ingredient list—99% purified water and five clean ingredients—are hypoallergenic, dermatologist tested, and have earned the National Eczema Association’s Seal of Acceptance.

- April 2025: Niches & Nooks has launched a line of intimate care wipes, “Wipe Your Nooks Refreshing Towelettes,” exclusively at Target and Target.com, offering pH-balanced, dermatologist- and gynecologist-tested formulas enriched with Aloe Vera and powered by microbiome-friendly scents in options like Soft Clementine, Airy Vanilla, Fresh Fig, and fragrance-free, according to the brand.

- March 2025: Safely has expanded its retail footprint with the launch of eco-friendly Multi-Surface Wipes, available in Sunrise and Calm scents, designed to clean all surfaces effectively while being gentle and suitable for everyday messes. According to the brand, these wipes align with Safely’s commitment to sustainability and convenience, offering consumers a practical, versatile cleaning solution for home use.

- January 2025: Panacea Biotec’s wholly owned subsidiary, Panacea Biotec Pharma Limited, has launched premium baby diapers and wipes under the brand name “NikoMom,” targeting the domestic market with plans for international expansion in the future. According to the brand, the NikoMom range is designed to deliver high-quality baby care essentials focused on comfort and well-being.

Global Personal Care Wipes Market Report Scope

Personal care wipes are disposable products primarily used to maintain hygiene and cleanliness.

The personal care wipes market is segmented by product type, distribution channel, and geography. The market is segmented by product type into baby wipes, facial wipes, hand and body wipes, and personal hygiene wipes. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online stores, and other distribution channels. The market is geographically segmented into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Baby Wipes |

| Cosmetic Wipes |

| Moist Toilet Wipes |

| General Purpose Wipes |

| Intimate Wipes |

| Conventional |

| Natural/Organic |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Norway | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Baby Wipes | |

| Cosmetic Wipes | ||

| Moist Toilet Wipes | ||

| General Purpose Wipes | ||

| Intimate Wipes | ||

| By Ingredient | Conventional | |

| Natural/Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Norway | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast revenue for the personal care wipes market by 2031?

The personal care wipes market is projected to reach USD 20.15 billion by 2031, growing at a 4.92% CAGR during 2026-2031.

Which segment holds the largest personal care wipes market share today?

Baby wipes commanded 53.48% value share in 2025, maintaining the dominant position.

Which region is growing fastest in personal care wipes consumption?

Asia-Pacific is expanding at a 6.88% CAGR through 2031, driven by urbanization and rising middle-class incomes.

How quickly are online channels expanding for wipes sales?

Online retail is advancing at a 7.05% CAGR between 2026-2031, outpacing all other channels.

Page last updated on: