Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.95 Billion |

| Market Size (2031) | USD 33.82 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carbon Black Market Analysis by Mordor Intelligence

The Carbon Black market size is expected to grow from USD 24.61 billion in 2025 to USD 25.95 billion in 2026 and is forecast to reach USD 33.82 billion by 2031 at 5.44% CAGR over 2026-2031. Strong demand from tire reinforcement, plastics compounding, battery electrodes, and high‐performance coatings anchors steady volume growth while enabling a gradual mix shift toward premium specialty grades. Capacity additions across Asia-Pacific underpin output expansion, yet feedstock volatility and rising sustainability requirements force producers to adopt tighter cost control and process innovation. Heightened electrification accelerates conductive grade uptake, and process breakthroughs such as plasma methane pyrolysis reshape competitive positioning. The carbon black market continues to capture value as a critical material input for traditional mobility and emerging energy storage supply chains.

Key Report Takeaways

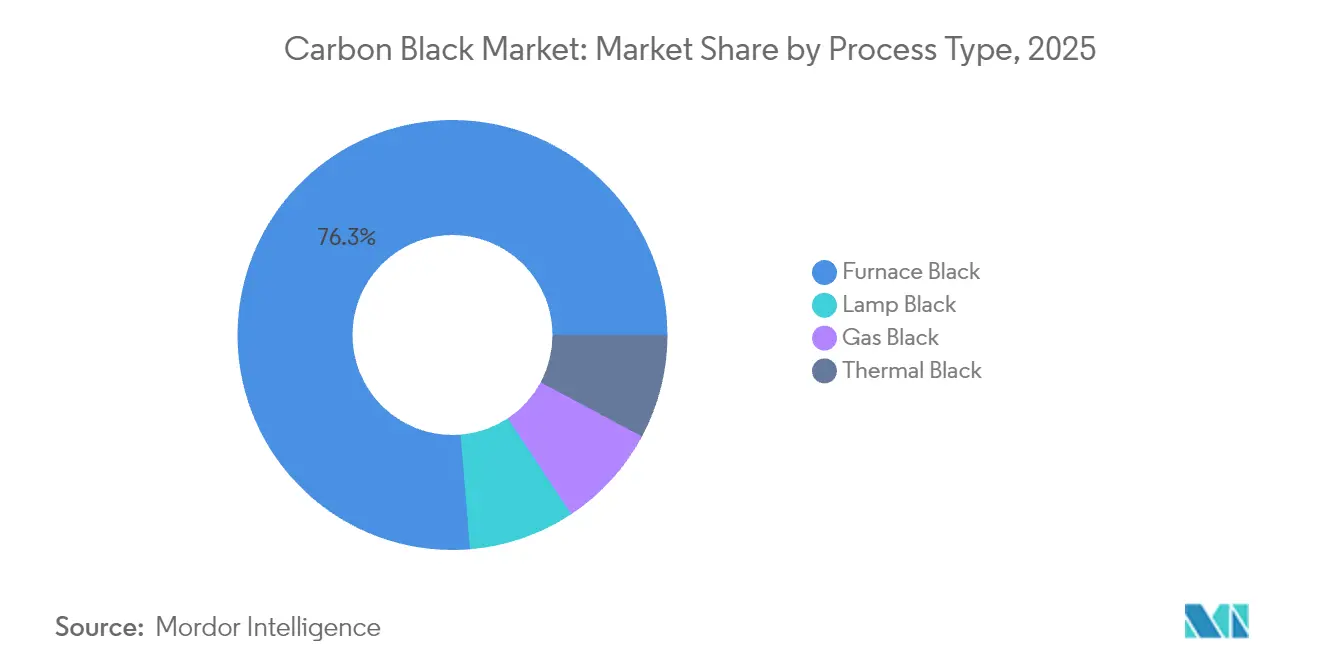

- By process type, furnace black held 76.30% of the carbon black market share in 2025. Lamp black is forecast to expand at a 7.35% CAGR through 2031, the fastest among process types.

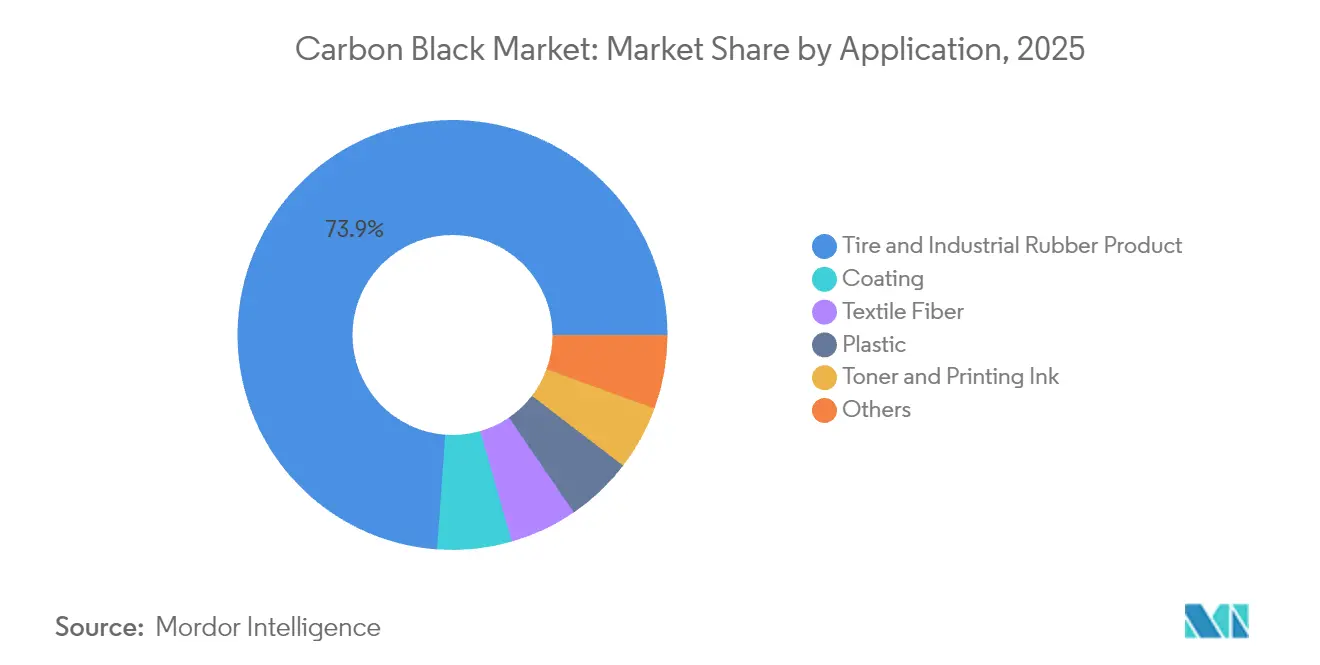

- By application, the tire and industrial rubber segment captured 73.85% of the carbon black market size in 2025. Coating applications are projected to record a 6.92% CAGR between 2026 and 2031, the highest within the application mix.

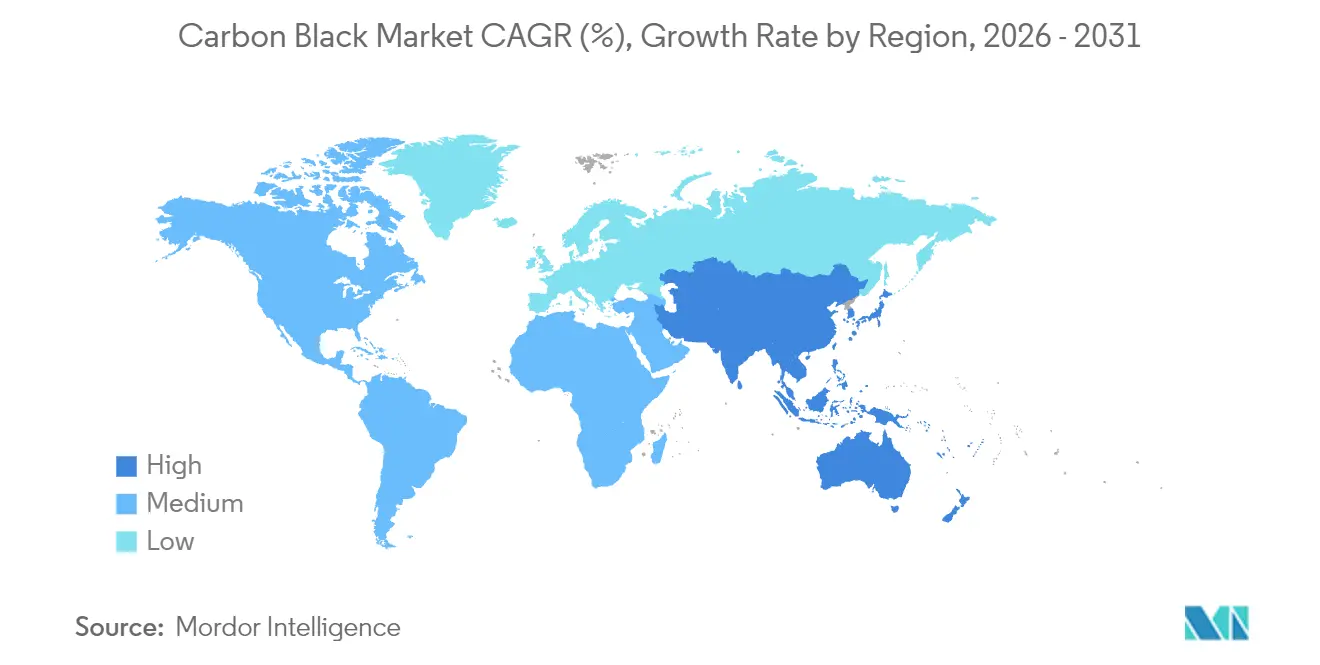

- Asia-Pacific commanded 61.85% revenue share of the carbon black market in 2025 and is advancing at a 5.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carbon Black Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tire manufacturing capacity expansion | +1.8% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Shift from standard to specialty blacks | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Electrification-led demand for conductive grades | +0.9% | Global, led by China, Europe, North America | Medium term (2-4 years) |

| Low-carbon plasma methane blacks | +0.6% | North America and Europe initially | Long term (≥ 4 years) |

| Rising electric vehicle output | +0.7% | Global, EV manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in tire manufacturing capacity, especially in the Asia-Pacific region

New tire plants across China, India, and Southeast Asia continue to lock in multi-year carbon black off-take contracts that underpin predictable demand patterns. Yokohama’s ongoing Chinese capacity additions exemplify how large tire complexes stimulate parallel investments in nearby carbon black units, lowering logistics costs and encouraging just-in-time delivery models. Regional clustering raises carbon black demand density and supports economies of scale that benefit furnace black producers. Suppliers with ISO 14001-certified operations secure preferred vendor status, consolidating share among environmentally compliant facilities[1]ISO, “ISO 14001 Environmental Management Systems,” iso.org. The structural link between tire output and carbon black consumption therefore provides a demand floor that smooths revenue cycles and aids long-range capital planning.

Rapid shift from standard to specialty blacks

OEM requirements for lower rolling resistance and higher conductivity push tire makers to adopt engineered grades that command 40-60% premiums over commodity furnace blacks. These specialty formulations enhance fuel economy and extend tread life, thereby generating measurable performance benefits that outweigh incremental cost. Producers investing in proprietary surface modification and ultra-clean furnace configurations gain sustainable advantages in a higher-margin niche. Technical differentiation and customer qualification protocols create switching costs that strengthen supplier lock-in, while the share of specialty shipments in the carbon black market rises steadily each year. Tight integration between research and development teams and tire designers accelerates the pivot toward advanced grades.

Electrification-led demand for conductive/acetylene grades

Lithium-ion battery electrodes require highly conductive additives to minimize internal resistance, and acetylene black offers superior particle morphology for this role. As electric vehicle output surges, battery manufacturers specify low-ash, high-purity carbon blacks with narrow particle-size distributions, raising qualification hurdles that only a subset of producers can meet. Orion Engineered Carbons responded by debottlenecking conductive-grade capacity and secured new supply agreements that diversify revenue beyond cyclic tire volumes. The resulting demand stream decouples from traditional automotive metrics, aligning growth with secular electrification trajectories and driving product portfolio rebalancing across the carbon black market.

Low-carbon plasma-methane blacks gain OEM credits

Plasma methane pyrolysis converts natural gas into solid carbon black and hydrogen with markedly lower CO₂ intensity than furnace processes. Monolith Materials’ commercial plant, supported by a USD 1.04 billion Department of Energy loan guarantee, positions the firm to capture carbon credit premiums and hydrogen revenue streams that offset higher capital intensity. Automotive and electronics OEMs increasingly incorporate Scope 3 emissions data into procurement scoring, giving low-carbon suppliers a competitive edge. Successful scale-up could catalyze wider adoption, compelling incumbents to reassess technology roadmaps and bundle sustainability metrics into value propositions across the carbon black market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile feedstock pricing | -0.8% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| CO₂/PAH emission caps | -0.5% | Europe and North America | Medium term (2-4 years) |

| Quality variability of recovered carbon black | -0.3% | Markets with tire recycling mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile feedstock pricing

Carbon black production relies heavily on carbonaceous feedstocks such as coal tar and residual fuel oil that can represent up to 50% of total operating cost. The Producer Price Index for carbon and graphite products climbed sharply through late 2024, squeezing margins before contractual pass-through clauses could take effect. Import-dependent plants face added freight exposure that widens regional price differentials and influences trade flow arbitrage. Integrated producers with long-term supply agreements partially shield earnings, whereas spot buyers endure profit swings that influence maintenance turnarounds and capacity utilization. Effective hedging and procurement strategies, therefore, remain essential to stabilize cash flows across the carbon black market.

Regulatory caps on CO₂/PAH emissions from furnaces

The EU Carbon Border Adjustment Mechanism introduces embedded-carbon tariffs on imported carbon-intensive goods, raising landed costs for furnace black shipped into Europe from older plants. Similar oversight expansions are under consideration in North America through tightening EPA rules on industrial combustion emissions[2]EPA, “Environmental Regulations,” epa.gov. Producers must retrofit scrubbers and optimize combustion controls to meet lower permissible thresholds for polycyclic aromatic hydrocarbons, often triggering capital outlays that challenge facilities nearing end-of-life. Compliance costs favor newer, high-efficiency units and accelerate rationalization of outdated capacity, potentially curbing overall output growth until replacement assets come online.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Furnace Black Dominance Faces Specialty Pressure

Furnace black accounted for 76.30% of 2025 revenue, highlighting its versatility and competitive economics across core tire and rubber goods. Nonetheless, the carbon black market size in furnace applications confronts a gradual share drift as specialty processes gain traction. Lamp black, supported by a 7.35% forecast CAGR through 2031, benefits from an inherent high-surface-area morphology that delivers superior conductivity in electronics and energy storage coatings. Gas black maintains usage in fine-dispersion inks, whereas thermal black serves niche polymer blends requiring low structure. The disruptive entrance of plasma methane technology extends the process palette by offering a low-emission pathway that can align with OEM carbon accounting frameworks.

Competitive responses include modular reactor retrofits that enable production of semi-specialty grades within existing furnace lines. Cabot Corporation and Birla Carbon are piloting advanced feed-injection controls to tighten particle size distribution and boost structure indices without needing new processes. Successful adaptation preserves scale advantages while capturing value migration toward specialty products. As ASTM develops a unified classification for recovered carbon black, furnace producers may incorporate rCB blending strategies to meet circularity targets without jeopardizing compound performance. Overall, the coexistence of commodity and specialty processes drives a dual-track growth model within the carbon black market.

By Application: Tire Segment Stability Enables Coating Growth

The tire and industrial rubber segment supplied 73.85% of 2025 demand, anchoring long-run production planning and capital recovery cycles. At the same time, the coating segment is projected to advance at a robust 6.92% CAGR through 2031, the fastest within the mix. This tilt illustrates strategic rebalancing from volume-driven sales toward differentiated offerings that command premium margins. Plastic compounding remains a steady outlet as automakers pursue lightweight interiors and exterior panels that require UV-protective blacks. Toner and printing ink volumes trend flat amid digitalization, yet specialized ultrafine grades retain defensible pricing.

Coating formulators increasingly specify treated carbon blacks that provide high jetness, electrical grounding, and UV durability, qualities unavailable from dyes or pigments alone. Products such as Birla Carbon’s Continua SCM cater to conductive paint systems used in electromagnetic interference shielding and battery casings. Stringent VOC rules also favor high-purity blacks that permit lower solvent usage. Textile fibers adopt carbon black for antistatic properties, opening incremental demand pockets that diversify revenue streams. Collectively, these shifts elevate the value density of each ton sold and reduce exposure to automotive production cycles, improving earnings resilience across the carbon black market.

Geography Analysis

Asia-Pacific held 61.85% of global revenue in 2025, supported by China’s tire manufacturing concentration and India’s specialty grade expansion, and is forecast to log a 5.85% CAGR to 2031. China integrates large tire plants with adjacent carbon black units, achieving feedstock and logistics efficiencies that bolster regional competitiveness. India’s Himadri Speciality Chemical added 70,000 MTPA of premium capacity in 2024, signaling a shift from commodity supply toward higher-margin powders for performance tires and battery components. Japan and South Korea contribute technology leadership, while Southeast Asian economies supply cost-effective labor and growing domestic auto demand.

North America records mature yet stable consumption, driven by replacement tire demand, high-performance coatings, and early adoption of low-emission processes. Monolith Materials’ Nebraska plasma facility introduces an alternative supply base aligned with green procurement objectives, while Cabot Corporation leverages its U.S. specialty plants to pass through inflationary costs without significant volume attrition. The Inflation Reduction Act’s battery incentives indirectly support conductive grade growth, providing a structural tailwind for the carbon black market in the region.

Europe emphasizes sustainability and specialty applications, with the Carbon Border Adjustment Mechanism encouraging localized production or preferential sourcing from low-carbon suppliers. Caps on PAH and CO₂ emissions accelerate modernization or closure of legacy furnaces. Producers with advanced after-treatment systems maintain market access and negotiate price premiums that offset compliance expenditures.

South America, the Middle East, and Africa collectively account for a smaller share but exhibit pockets of high growth linked to expanding automotive assembly and broader industrialization. Brazil’s automotive recovery drives localized tire output that stimulates domestic carbon black production investment. Middle Eastern players leverage petrochemical raw material integration to propose new furnace units, though downstream demand still lags Asia-Pacific scale. South Africa’s coatings and mining sectors require specialty dispersion blacks, yet currency volatility clouds capital planning. Combined, these regions offer expansion optionality as primary markets mature, allowing diversified producers to balance regional cycles within the global carbon black market.

Competitive Landscape

The carbon black industry remains moderately fragmented. Strategic themes include vertical integration for feedstock security, regional expansion alongside customer footprints, and research and development alliances that accelerate qualification cycles. Partnerships between carbon black makers and EV battery companies shorten prototype timelines and embed suppliers in next-generation chemistry roadmaps. Mergers and acquisitions remain a viable route to specialty grade capability, though regulatory scrutiny on emissions and circularity may influence deal valuations. Recovered carbon black suppliers race to meet ASTM D36 standards, aiming to supply sustainable material for mid-tier tire formulations. Overall, technology leadership and sustainability credentials increasingly determine competitive advantage in the carbon black market.

Carbon Black Industry Leaders

Cabot Corporation

Birla Carbon (Aditya Birla Group)

Orion Engineered Carbons S.A.

Tokai Carbon Co. Ltd

Jiangxi Black Cat Carbon Black Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bridgestone Corporation has announced the sale of its Mexican carbon black business, Mexico Carbon Manufacturing S.A. de C.V., to Cabot Corporation. This strategic move aligns with Bridgestone’s MidTerm Business Plan (2024–2026). Bridgestone aims to leverage Cabot’s supply chain, technology, and expertise by partnering with Cabot Corporation while continuing in-house production of strategic carbon black through Asahi Carbon Co., Ltd. in Japan.

- January 2024: Birla Carbon has announced major greenfield expansions in Asia, with two new carbon black manufacturing plants set to open in Naidupet, Andhra Pradesh (India), and Rayong (Thailand). Each facility will begin with a capacity of 120 kMT, scalable to 240 kMT, to meet rising demand in India and Southeast Asia.

Global Carbon Black Market Report Scope

Carbon black is a fine carbon powder made by incomplete combustion or thermal decomposition of gaseous or liquid hydrocarbons under controlled conditions. The carbon black market is segmented by process type, application, and geography. By process type, the market is segmented into furnace black, gas black, lamp black, and thermal black. By application, the market is segmented into tires and industrial rubber products, plastics, toners and printing inks, coatings, textile fibers, and other applications. The report also covers the market size and forecasts for the carbon black market in 16 countries across major regions. The report offers the volume in kiloton and market size in value terms in USD for all the abovementioned segments.

By Process Type

| Furnace Black |

| Gas Black |

| Thermal Black |

| Lamp Black |

By Application

| Tire and Industrial Rubber Product |

| Plastic |

| Toner and Printing Ink |

| Coating |

| Textile Fiber |

| Others |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Process Type | Furnace Black | |

| Gas Black | ||

| Thermal Black | ||

| Lamp Black | ||

| By Application | Tire and Industrial Rubber Product | |

| Plastic | ||

| Toner and Printing Ink | ||

| Coating | ||

| Textile Fiber | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the carbon black market in 2026?

The carbon black market size reached USD 25.95 billion in 2026 and is forecasted to reach USD 33.82 billion by 2031.

What CAGR is expected for carbon black through 2031?

The market is projected to grow at a 5.44% CAGR between 2026 and 2031.

Which region leads carbon black consumption?

Asia-Pacific accounted for 61.85% of revenue in 2025 and remains the primary growth engine.

Which application segment is expanding fastest beyond tires?

Coating applications are forecast to post a 6.92% CAGR through 2031 due to rising demand for conductive and UV-protective grades.

What technological shift could disrupt traditional furnace production?

Plasma methane pyrolysis offers low-carbon carbon black and hydrogen coproducts, supported by significant investment such as Monolith Materials’ DOE-backed plant.

Page last updated on: