Recovered Carbon Black Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 138.21 kilotons |

| Market Volume (2031) | 363.70 kilotons |

| Growth Rate (2026 - 2031) | 21.35% CAGR |

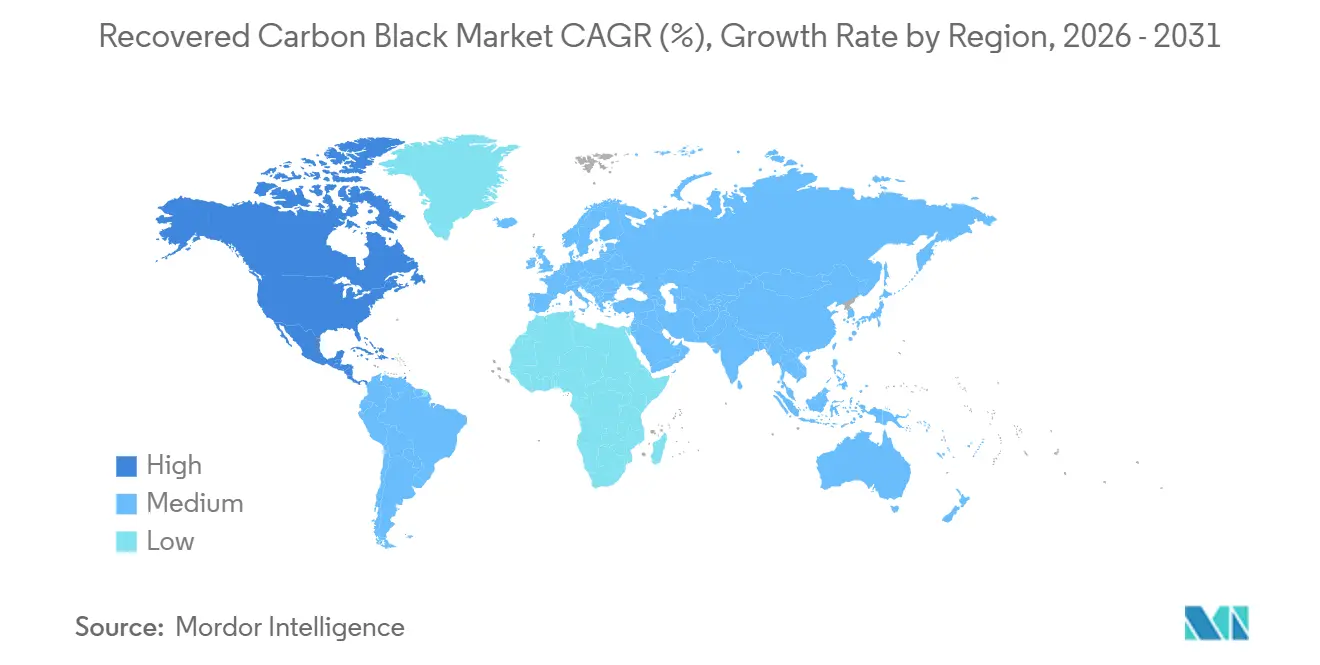

| Fastest Growing Market | North America |

| Largest Market | Europe |

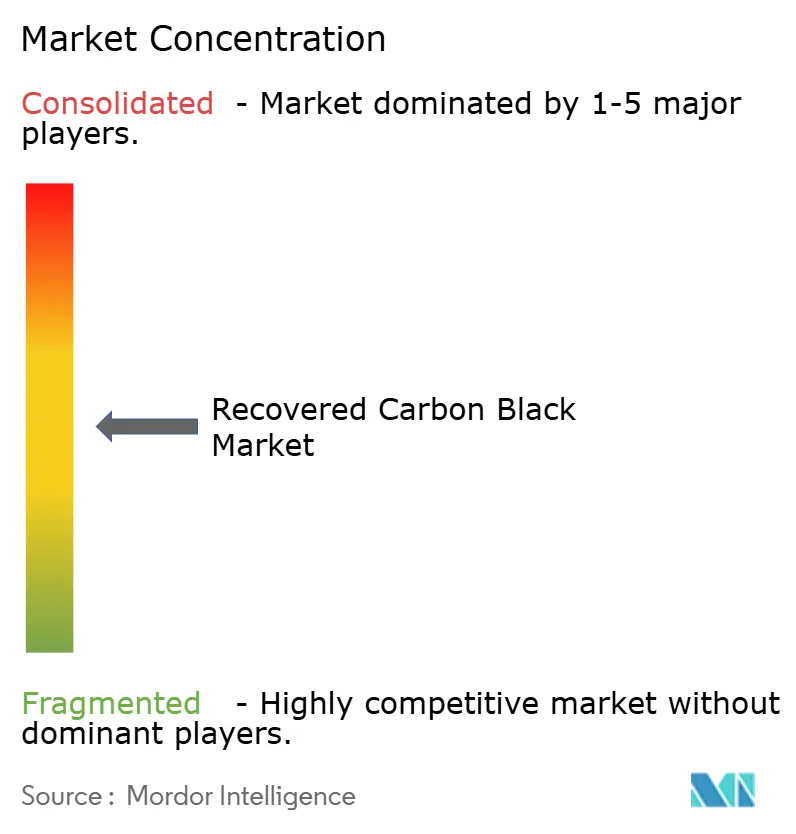

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recovered Carbon Black Market Analysis by Mordor Intelligence

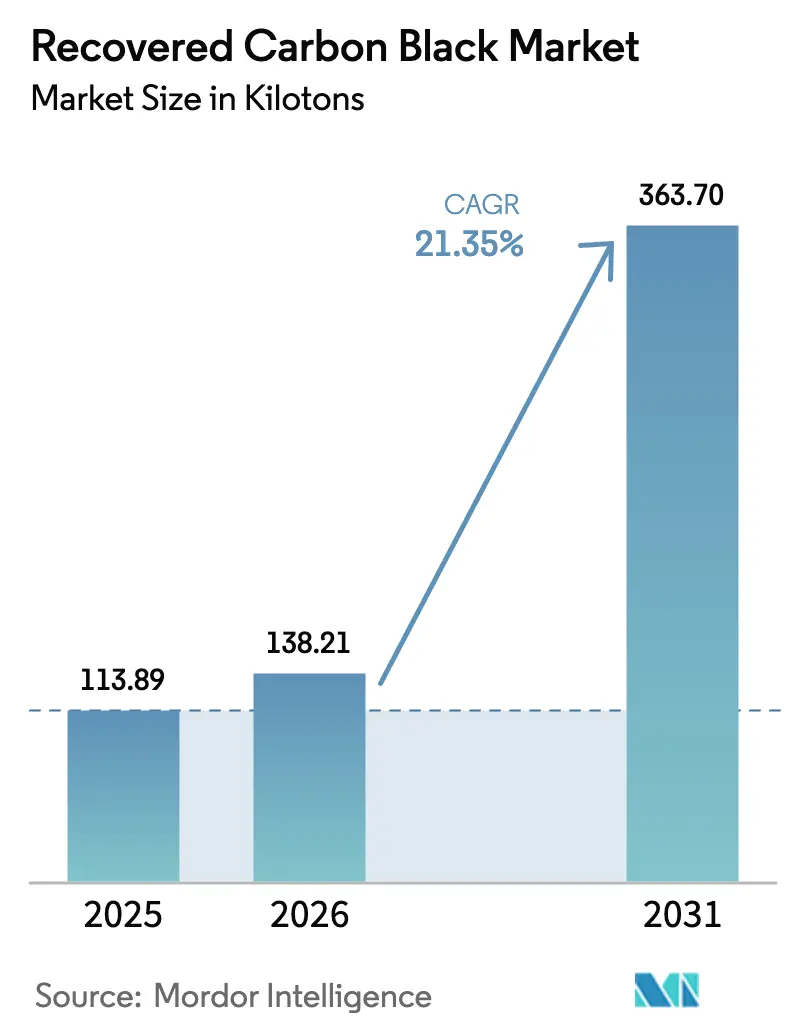

The Recovered Carbon Black Market size is expected to grow from 113.89 kilotons in 2025 to 138.21 kilotons in 2026 and is forecast to reach 363.70 kilotons by 2031 at 21.35% CAGR over 2026-2031. Strong regulatory pressure, OEM sustainability targets, and widening cost differentials with virgin carbon black are accelerating capacity commitments across Europe, North America, and Asia-Pacific. Pyrolysis technology—now the dominant pathway—remains supply-constrained even as new joint-venture plants come online, while specialty grades aimed at 5G and electric-vehicle applications open margin-rich opportunities for operators with advanced post-treatment. Europe retains the largest production and consumption base, yet North America is on track to log the fastest volumetric expansion once its 2026–2027 projects reach steady state. Competitive intensity is sharpening as traditional carbon-black producers take equity stakes in pyrolysis firms to hedge virgin feedstock risk and secure secondary-material streams.

Key Report Takeaways

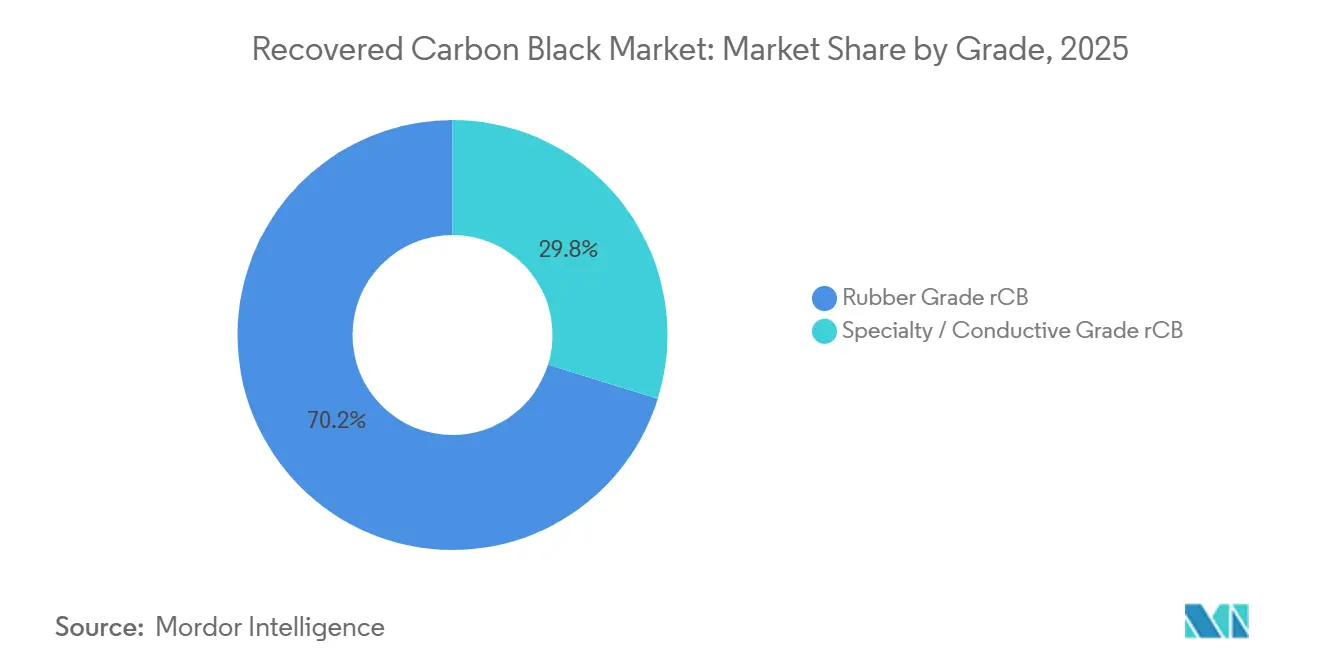

- By grade, rubber-grade rCB captured 70.21% volume in 2025, while specialty/conductive rCB is forecast to expand at 22.89% CAGR through 2031.

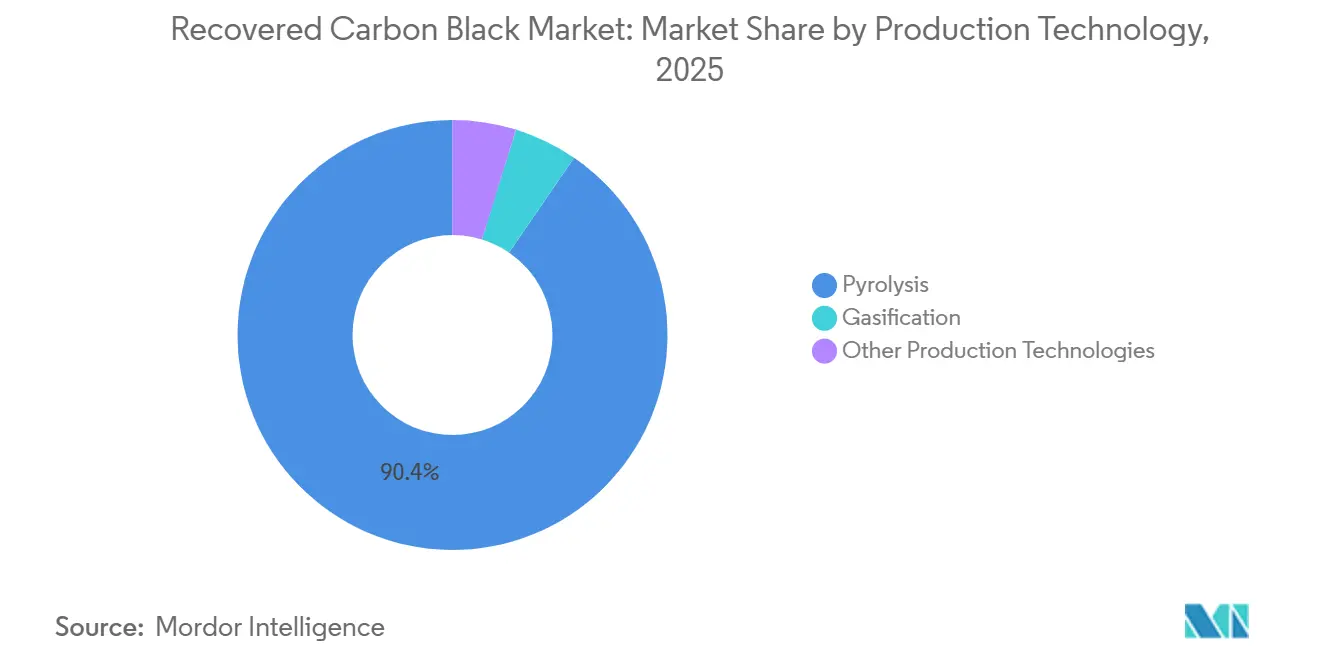

- By production technology, pyrolysis controlled 90.45% output in 2025 and is set to grow at 22.93% CAGR, underscoring that capacity rather than demand remains the binding constraint.

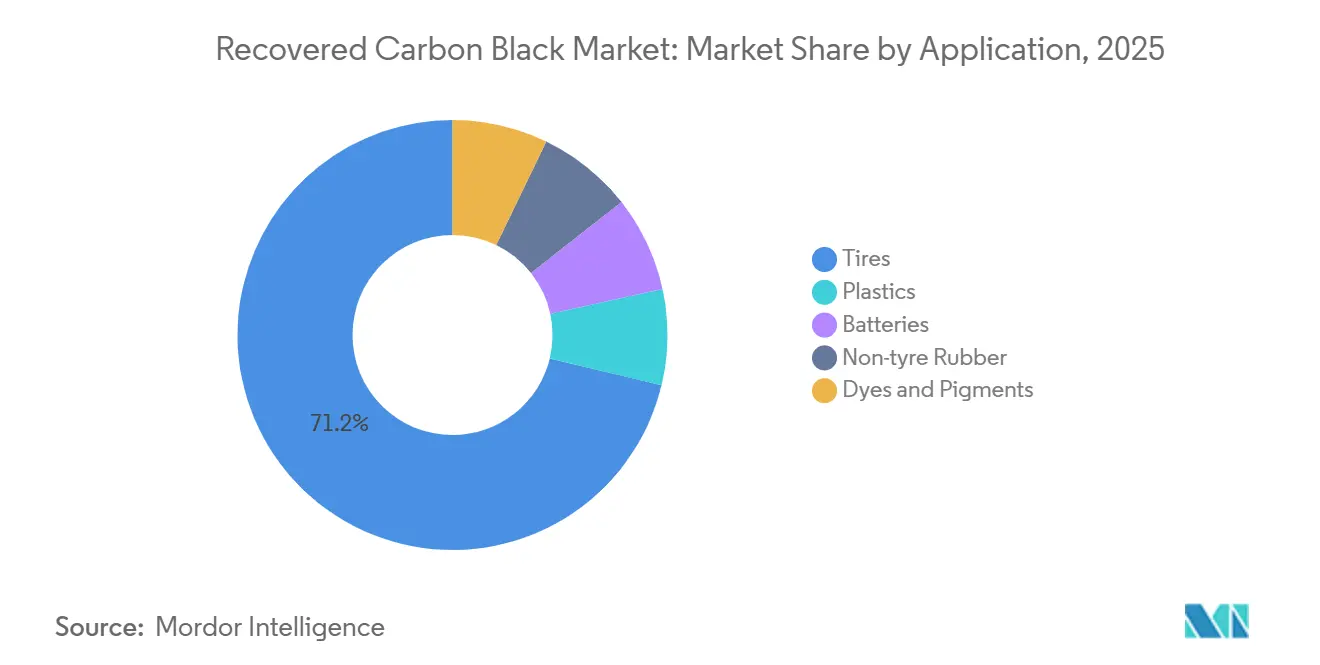

- By application, tires held 71.23% share in 2025 and is forecast to expand at 21.97% CAGR through 2031.

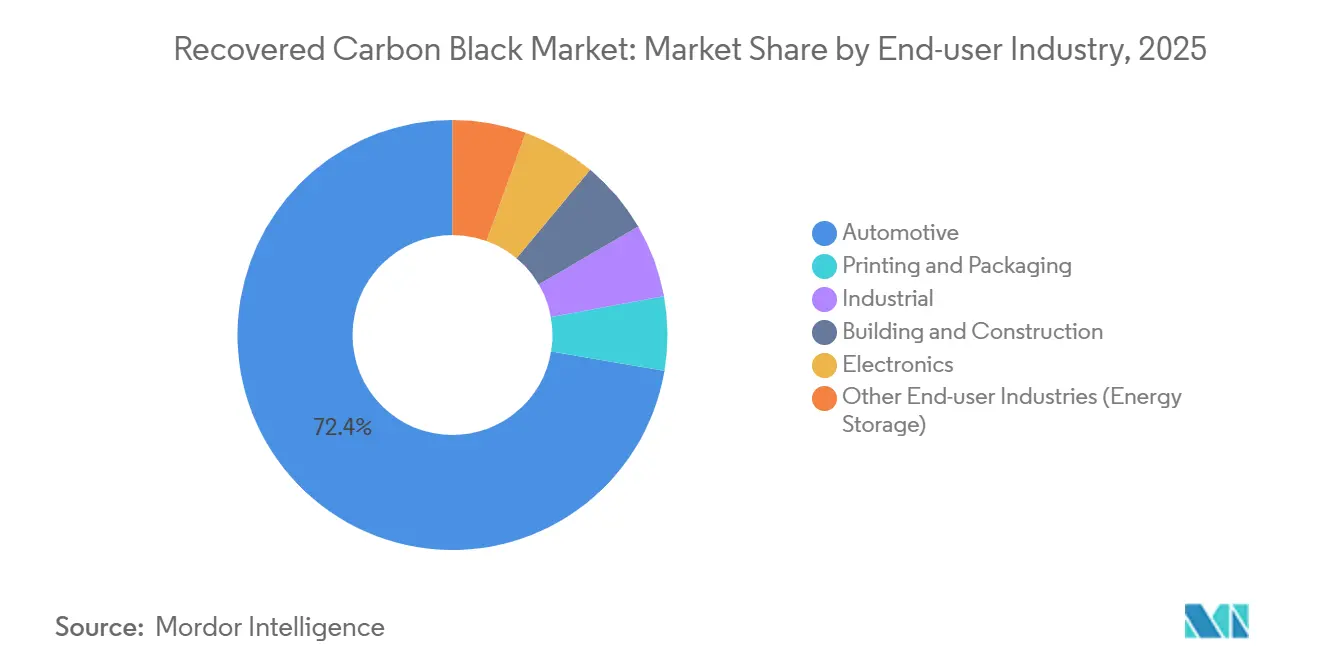

- By end-user industry, automotive commanded 72.35% share in 2025, whereas industrial is projected to climb at 22.07% CAGR to 2031.

- By geography, Europe accounted for 51.24% in 2025, while North America is expected to pace the field at 21.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recovered Carbon Black Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Sustainability and Circular-Economy Mandates | +5.2% | Global, with EU and India leading implementation | Medium term (2-4 years) |

| OEM Target of ≥40% Sustainable Materials in Tires By 2030 | +6.8% | Global, concentrated in Europe and North America | Short term (≤ 2 years) |

| Cost Advantage Versus Virgin Carbon Black | +4.1% | Asia-Pacific, Middle East, price-sensitive markets | Short term (≤ 2 years) |

| EU Carbon Border Adjustment Mechanism (CBAM) Incentives | +3.7% | Europe, spillover to North America and ASEAN | Medium term (2-4 years) |

| rCB Use in Conductive Polymer Composites for 5G and EV EMI Shielding | +2.9% | North America, Europe, East Asia (China, Japan, South Korea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental Sustainability and Circular-Economy Mandates

Mandatory tire-collection rules and carbon-pricing schemes are moving from voluntary to enforceable. India raised its Extended Producer Responsibility (EPR) target to 100% collection from FY 2024-25 and recognized recovered carbon black for tire manufacturing, establishing a closed-loop incentive. The EU’s product carbon-storage regulation (Regulation 2024/3012) obliges ≥35-year monitoring, rewarding pyrolysis operators with ISO 59014 traceability over virgin suppliers. China’s national carbon market, effective May 2024, penalizes high-emission feedstocks, pushing local compounders toward low-carbon fillers. These measures enable tread formulations to replace up to 60% of virgin carbon black without breaching ASTM D8474 benchmarks. The convergence of EPR, carbon fees, and product-level certification gives the recovered carbon black market a structural compliance advantage.

OEM Target of ≥40% Sustainable Materials in Tires by 2030

Tier-one tire makers are locking in multi-year offtake to de-risk pyrolysis financing. Michelin’s 40% sustainable-materials goal underpins its co-investment in Scandinavian Enviro’s Uddevalla plant, pre-selling 10 kt of annual output before commissioning. Nokian and Pirelli have adopted similar agreements, while Bridgestone and Tokai Carbon formed a dedicated venture in January 2025. These binding contracts absorb merchant-market liquidity and convert the recovered carbon black market into a strategic supply chain, not a spot commodity.

Cost Advantage Versus Virgin Carbon Black

When crude oil prices exceed USD 80 per barrel, a notable price gap emerges between virgin and recycled carbon black, with the former commanding a significant premium. In May 2025, in the U.S., virgin carbon black was priced higher, while regional recycled carbon black (rCB) was comparatively lower. Battery-grade rCB traded at a fraction of the cost of top-tier virgin additives. Furthermore, purified rCB, containing less than 5% ash, commands a premium in coatings and inks, underscoring that it's the quality control, rather than the feedstock, that dictates value capture.

EU Carbon Border Adjustment Mechanism (CBAM) Incentives

CBAM reporting began in 2023 and tariff collection starts 2026, effectively raising the landed cost of virgin carbon black by 10%–15% for exporters without an equivalent carbon price[1]European Commission, “CBAM Transitional Phase Guidance,” ec.europa.eu . India is racing to operationalize a domestic carbon-credit scheme to protect a trade line that grew 20% CAGR between 2017 and 2024. ISCC-certified rCB from plants such as Enviro’s Uddevalla qualifies for exemption, providing an embedded cost edge for European tire makers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Infrastructure and Immature Pyrolysis Technologies | -2.8% | Global, acute in South America and Middle-East and Africa | Medium term (2-4 years) |

| Feed-Stock Quality Variability from Fragmented Collectors | -1.9% | Asia-Pacific, South America, emerging markets | Short term (≤ 2 years) |

| Potential REACH Reclassification of Pyrolysis Oils | -1.4% | Europe, spillover regulatory risk to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Infrastructure and Immature Pyrolysis Technologies

Capital intensity and co-product monetization hurdles delay green-field plants in regions lacking tire-collection grids. Black Bear Carbon’s Chemelot project illustrates the need for multi-stream offtake—bio-fuel, steel, electricity—to reach hurdle rates. Higher-temperature gasification offers theoretical efficiency but demands even larger ticket sizes, explaining why pyrolysis captured more than 90% of 2025 output. Module-based reactors lower the entry bar but still require robust front-end sorting, a weak spot in South America and parts of Africa.

Potential REACH Reclassification of Pyrolysis Oils

An EU debate on Annex XVII could tag pyrolysis oils as hazardous, triggering more stringent handling and elevating compliance costs. Although no final decision emerged in 2025, the prospect slows financing for plants banking on oil revenue, especially in Germany and France[2]European Chemicals Agency, “Annex XVII Consultation on Pyrolysis Oils,” echa.europa.eu . North American investors monitor Brussels closely, aware that a negative ruling could echo in U.S. state regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Specialty Grades Capture Premium Applications

In 2025, rubber-grade rCB held 70.21% volume, driven by Michelin, Nokian, and Pirelli offtakes that pre-sold all Uddevalla capacity. The recovered carbon black market share for rubber-grade is poised to erode modestly as conductive and specialty grades grow 22.89% CAGR through 2031, buoyed by 5G and EV shielding. Purified grades with less than 5% ash already command 15%-25% premiums in automotive coatings and inks. Cabot’s EVOLVE and Orion’s specialty portfolios validate that quality can outrank cost in decisive use cases. Over the forecast horizon, specialty tonnage could increase substantially, keeping utilization high at post-treatment units.

By Production Technology: Pyrolysis Dominance Masks Gasification’s Niche

Pyrolysis supplied 90.45% of global output in 2025 and is on track for 22.93% CAGR, making it the engine behind most recovered carbon black market additions. Scandinavian Enviro’s five-reactor Uddevalla design and Bolder Industries’ Terre Haute plant exemplify scaled, reactor-train architectures that monetize oil and steel alongside rCB. Gasification remains a niche, constrained to energy-recovery models rather than product-grade rCB. Modular auger reactors are emerging in small European installations, but bankability still hinges on proven offtake agreements.

By Application: Tire Dominance Coexists with Plastics Diversification

Tires consumed 71.23% of 2025 volume and will continue growing at 21.97% CAGR as OEMs target ≥40% sustainable content. Michelin’s Le Mans tire showcased 63% sustainable materials, including rCB, without compromising performance. Meanwhile, plastics, batteries, and coatings provide a hedge against any tapering in tire demand. Polyolefin masterbatch containing 20%-40% rCB delivers UV stability and conductivity at a substantial discount, supporting faster traction in consumer electronics and building products.

By End-user Industry: Automotive Lock-In Drives Industrial Catch-Up

Automotive captured 72.35% of 2025 volume, reflecting the lock-step integration between pyrolysis operators and global tire majors. The industrial is forecast to expand at 22.07% CAGR on the back of Scope 3 emissions targets for conveyor belts, hoses, and seals. Printing and packaging inks are adopting purified grades, especially when crude prices exceed USD 80 bbl-1, making rCB a compelling hedge against petrochemical volatility.

Geography Analysis

Europe remains the nucleus of policy-driven demand. CBAM tariffs, effective 2026, push local OEMs toward certified rCB that avoids surcharges, while Regulation 2024/3012 awards long-term carbon-storage credits to pyrolysis operators with traceable supply chains. Uddevalla, Dole, and Dillingen plants now anchor regional output, and pre-sold capacity suggests chronic under-supply through 2028.

North America follows a capacity-build narrative. Joint ventures involving Continental Carbon, Eco-Infinic, and CSRC materially de-risk financing, while Bolder Industries brings an 18 kt unit to Indiana in 2026 and plans a 30 kt module near Antwerp, Indiana, by 2027. Regional pricing remains the world’s highest, reflecting both freight economics and evolving tire-take-back infrastructure.

Asia-Pacific balances feedstock abundance with policy complexity. India’s 100% EPR target and South Korea’s Woven Capital-backed LD Carbon project illustrate clear momentum, yet inconsistent collection quality and capital constraints in Southeast Asia drag on utilization rates. China’s national ETS, effective 2024, introduces carbon costs that are likely to sharpen the competitive edge of domestically produced rCB over imported virgin fillers.

Competitive Landscape

The recovered carbon black market presents moderate concentration. First movers - Scandinavian Enviro, Pyrum, Bolder Industries - control the bulk of contracted volume, while legacy carbon-black makers such as Cabot and Orion hedge with equity stakes or offtake agreements. Vertical integration stands out: Michelin’s stake in Enviro guarantees rCB for its European plants, and Bridgestone co-develops production with Tokai Carbon to buffer virgin supply risk. Technology competition pivots on post-treatment that yields less than 5% ash and tight particle-size distributions, enabling penetration into coatings and inks that demand high jetness.

Regulatory alignment is becoming a barrier to entry. Plants bearing ISCC, ISO 59014, and REACH-compliant certifications gain tariff exemptions under CBAM, putting uncertified operators at a cost disadvantage. Intellectual-property filings center on maximizing value from oil and gas coproducts to buttress project returns. New entrants push modular designs, but bankability still depends on long-term, credit-worthy offtake—an advantage held by European and North American incumbents.

Recovered Carbon Black Industry Leaders

Black Bear Carbon B.V.

Bolder Industries

Scandinavian Enviro Systems AB

Pyrum Innovations Ltd.

Cabot Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NEXEN TIRE, a global tire manufacturer, announced the signing of a long-term supply agreement with LD Carbon Co., Ltd., a resource circulation and material recycling company, for recovered carbon black. LD Carbon Co., Ltd. produced recovered carbon black through the pyrolysis of end-of-life tires in an oxygen-free environment, significantly reducing carbon emissions and supporting resource recycling.

- January 2025: Tokai Carbon Co., Ltd., Bridgestone Corporation, Kyushu University, and Okayama University launched a technology development project to conduct secondary processing on recovered carbon black extracted from polymer products, including end-of-life tires containing rubber. The objective of the project was to transform these materials into eco carbon black with rubber reinforcement properties comparable to those of virgin carbon black which is derived from petroleum and coal.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the recovered carbon black (rCB) market as the sale of post-pyrolysis carbonaceous material that is milled, classified, and pelletized to meet ASTM D36 ash, structure, and tint thresholds so it can substitute virgin furnace black in tires, plastics, coatings, and conductive compounds. We model only freshly produced rCB volumes moving through formal commercial channels during the base year.

Scope Exclusions: Virgin carbon black grades, unrefined char, ground rubber powder, and pyrolysis oil streams are excluded.

Segmentation Overview

- By Grade

- Rubber Grade rCB

- Specialty/Conductive Grade rCB

- By Production Technology

- Pyrolysis

- Gasification

- Other Production Technologies

- By Application

- Tires

- Plastics

- Batteries

- Non-tyre Rubber

- Dyes and Pigments

- By End-user Industry

- Automotive

- Printing and Packaging

- Industrial

- Building and Construction

- Electronics

- Other End-user Industries (Energy Storage)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Nigeria

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed pyrolysis operators, tire formulators, plastics compounders, and regional regulators across North America, Europe, and East Asia. These conversations clarified typical rCB yields, target ash levels, discount structures versus N330, and upcoming regulatory triggers, letting us close data gaps surfaced in desk work.

Desk Research

We pulled baseline supply cues from tire-scrappage and recycling datasets issued by the U.S. EPA, Eurostat, and the European Tyre & Rubber Manufacturers' Association. Trade volumes for HS 2803 and 4004 were mined through UN Comtrade, while China's Ministry of Ecology & Environment circular-economy bulletins aided Asia yield assumptions. Trend context came from peer-reviewed articles in Waste Management and patent families tagged "C04B 18/02" through Questel. Company 10-Ks and investor decks added plant-level capacities. The sources listed illustrate our foundation; many more publications and databases supported verification.

Market-Sizing & Forecasting

A blended bottom-up, top-down model is applied. National end-of-life tire generation, average pyrolysis throughput, rCB yield factors, and plant utilization create a demand pool that is cross-checked against exporter rolls and sampled ASP × volume invoices. Key variables like ELT generation per capita, pyrolysis capacity additions, average rCB yield-to-ELT ratio, price discount to virgin N300, and mandated recycled content targets drive yearly deltas. Multivariate regression links those indicators to observed volume shifts, and scenario analysis stress-tests high-growth and policy-delay cases. Where supplier roll-ups under-report emerging plants, conservative capacity proxies are inserted and flagged for review.

Data Validation & Update Cycle

Outputs undergo variance screening versus historical trade and price curves, then a senior analyst reviews anomalies before sign-off. Reports refresh annually, and material events, major capacity start-ups, policy changes, and force majeure trigger an interim update. A final pre-publication sweep ensures clients receive the newest view.

Why Mordor's Recovered Carbon Black Baseline Delivers Dependability

Published rCB figures often diverge because firms differ in unit of measure, the breadth of applications considered, and how they treat unrefined pyrolysis char. By anchoring our base year on auditable ELT flows and vetted yield factors, Mordor's methodology offers a traceable, moderate middle ground that decision-makers can confidently build on.

Key gap drivers include: (1) several publishers convert to USD using assumed high premium prices; (2) some omit specialty/conductive grades; (3) others bundle ancillary pyrolysis outputs, inflating totals; and (4) refresh cadences vary, so outdated policy assumptions persist elsewhere.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 136.44 kilotons (2025) | Mordor Intelligence | - |

| USD 491 million (2023) | Global Consultancy A | Early base year; limited regions; aggressive ASP uplift |

| USD 331.1 million (2025) | Industry Tracker B | Uses virgin black pricing; omits specialty grades |

| USD 2.35 billion (2024) | Data Specialist C | Includes char and other pyrolysis by-products |

In sum, our stepwise, variable-linked model, reviewed each year by Mordor analysts, keeps the baseline balanced, transparent, and easier to replicate than estimates built on opaque price multipliers or expansive material scopes.

Key Questions Answered in the Report

How large will the recovered carbon black market be by 2031?

Volume is projected to reach 363.70 kilotons by 2031, reflecting a 21.35% CAGR from the 2026 baseline of 138.21 kilotons.

Which region grows fastest after 2026?

North America leads with a forecast 21.89% CAGR, fueled by joint-venture plants that come online between 2026 and 2027.

Why are tire makers locking in long-term rCB contracts?

OEM sustainability targets of ≥40% recycled content and CBAM-related cost pressures drive manufacturers to secure future supply at predictable prices.

What share does pyrolysis hold among production technologies?

Pyrolysis accounts for 90.45% of global output in 2025 and is expected to retain leadership as its capacity expands at 22.93% CAGR.

Page last updated on: