Black Phosphorus Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 21.72 Million |

| Market Size (2031) | USD 119.58 Million |

| Growth Rate (2026 - 2031) | 40.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Black Phosphorus Market Analysis by Mordor Intelligence

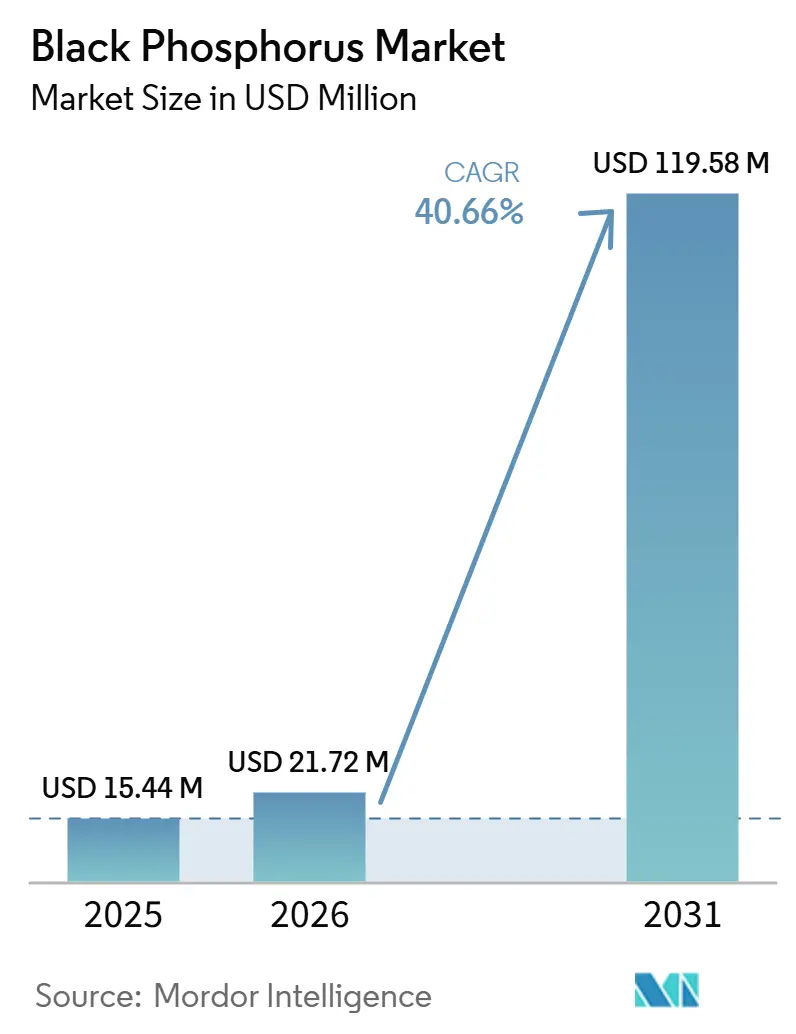

The Black phosphorus market, valued at USD 15.44 million in 2025, is projected to grow to USD 21.72 million in 2026 and is expected to reach USD 119.58 million by 2031, with a CAGR of 40.66% from 2026 to 2031. Foundries and battery manufacturers are increasingly focusing on two-dimensional semiconductors that offer a combination of high carrier mobility and tunable bandgaps. This performance range addresses the limitations of graphene and many transition-metal dichalcogenides. A significant shift in market dynamics is driven by cost reductions, such as Ruifeng High-Tech’s supercritical CO₂ exfoliation, which reduced production costs from 3,000 CNY to 1 CNY per gram. This development is facilitating the transition of the market toward ton-scale volumes. Additionally, Black phosphorus's ability to biodegrade into non-toxic phosphate ions is expanding its applications in biomedical devices while simplifying compliance with future waste disposal regulations. In the U.S. and Europe, increased investments in defense and photonics are creating diverse revenue streams, helping to mitigate short-term price fluctuations associated with battery cycles.

Key Report Takeaways

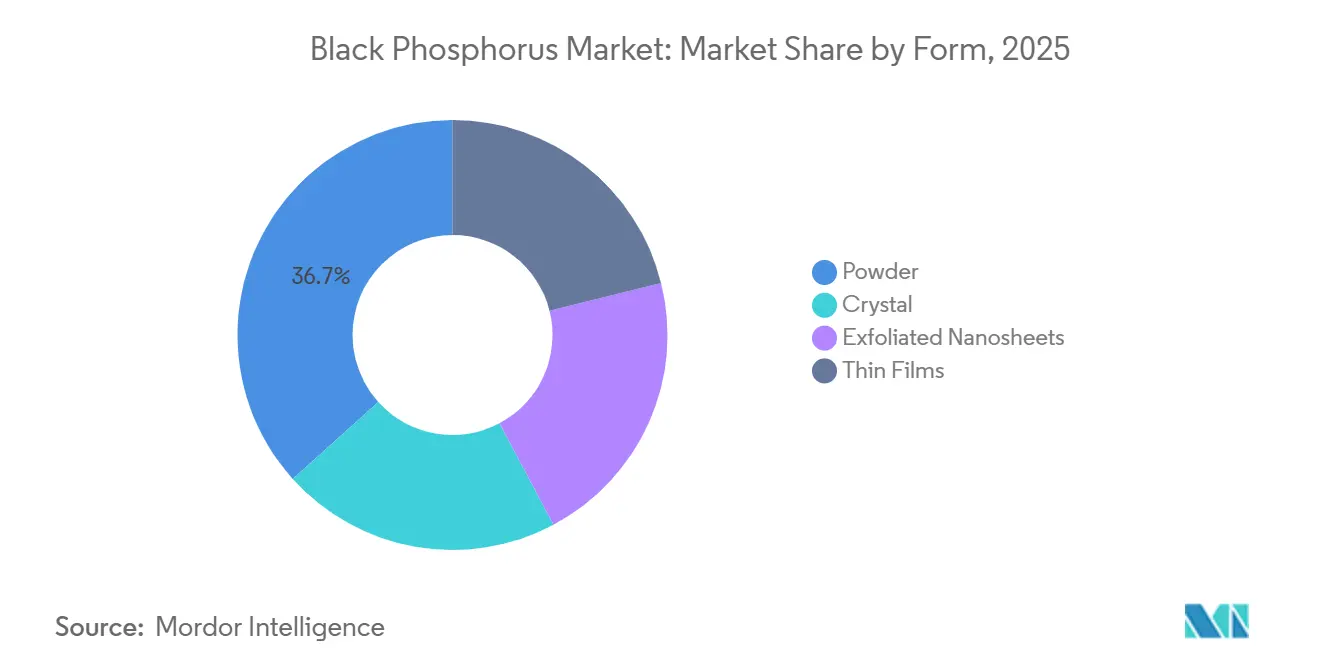

- By form, powder led all forms with 36.67% of the black phosphorus market share in 2025, whereas exfoliated nanosheets represent the fastest-growing form at a 41.23% CAGR from 2026 to 2031.

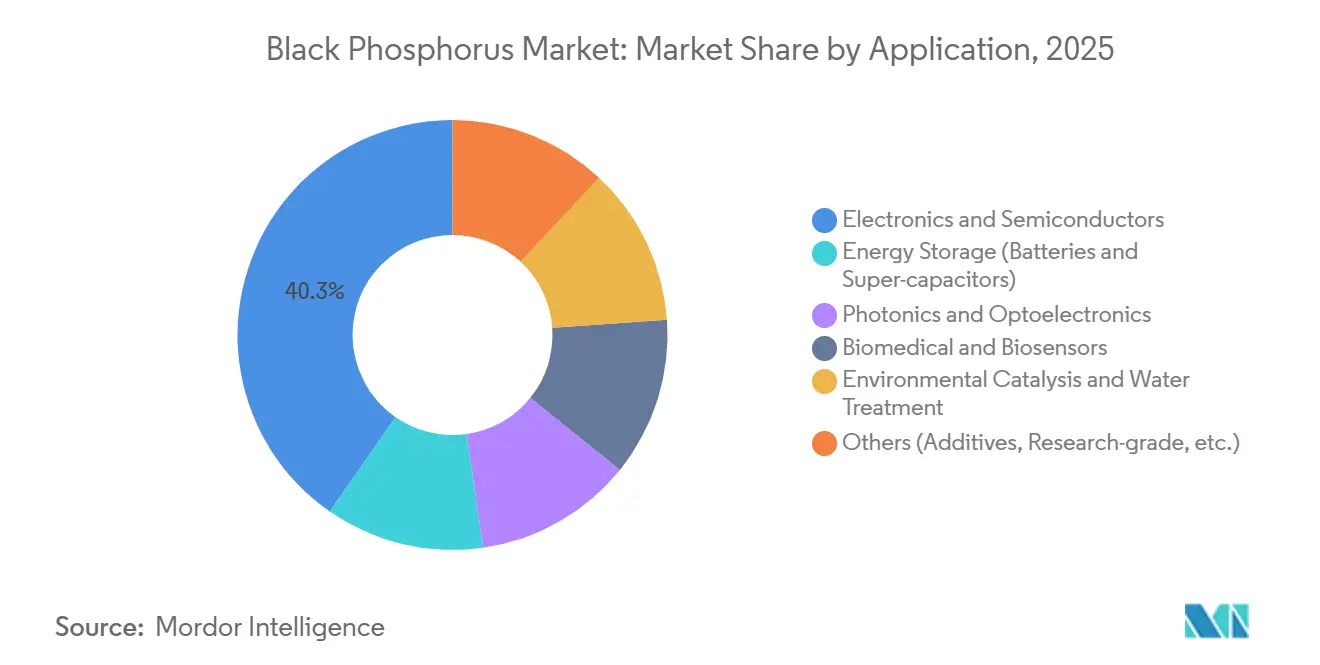

- By application, electronics and semiconductors commanded 40.33% of the black phosphorus market size in 2025, while energy storage applications are expanding at a 42.46% CAGR from 2026 to 2031.

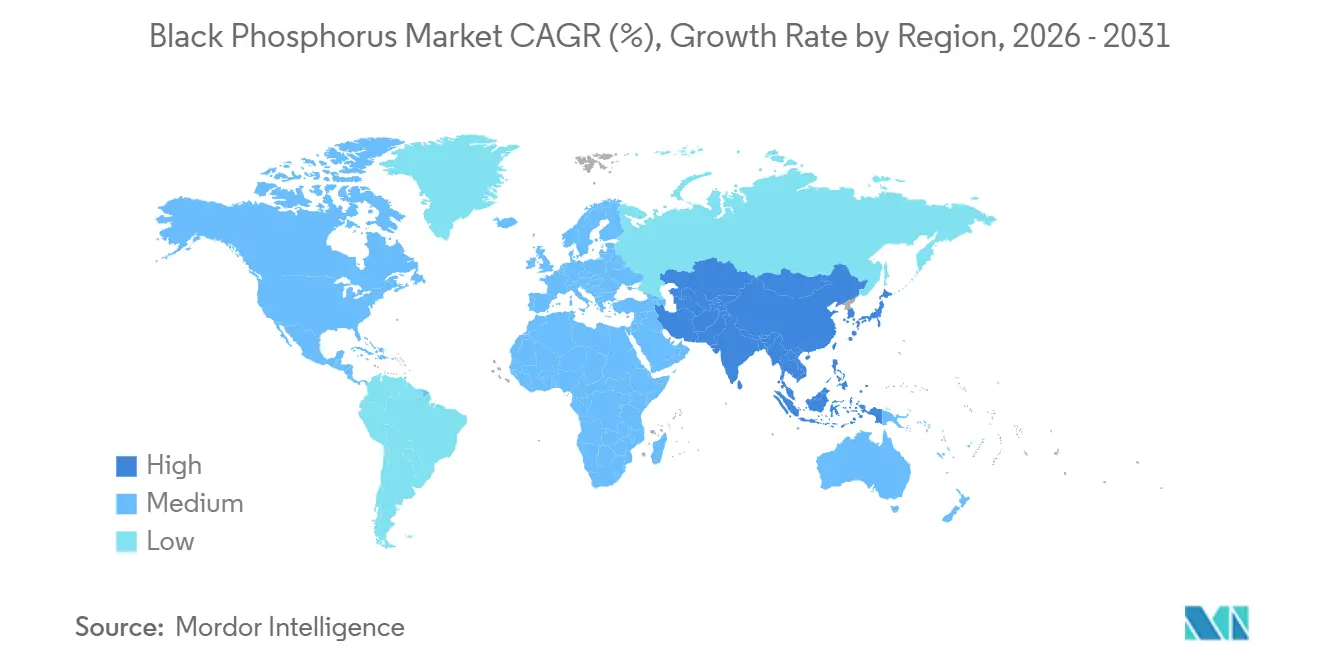

- By geography, Asia-Pacific captured 47.78% revenue share in 2025, and the region is advancing at a 41.56% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Black Phosphorus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for 2D semiconductors in flexible and high-frequency electronics | +9.2% | Global, with early adoption in Asia-Pacific (China, South Korea, Taiwan) and spillover to North America R&D hubs | Medium term (2-4 years) |

| Rapid uptake of BP-based photonic integrated circuits | +8.5% | North America and Europe (silicon photonics clusters), expanding to Asia-Pacific | Medium term (2-4 years) |

| Mainstream R&D funding for BP anodes in next-gen Li/Na-ion batteries | +10.8% | Asia-Pacific core (China, Japan, South Korea), with pilot projects in North America and Europe | Long term (≥4 years) |

| Defense investment in BP-enabled mid-IR stealth and secure-comms coatings | +5.3% | North America (DoD, AFRL), Europe (EU defense programs), selective Middle East adoption | Long term (≥4 years) |

| European Union Chips-Act pilot-line grants catalyzing wafer-scale BP synthesis | +6.9% | Europe (Germany, France, Netherlands), with technology transfer to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for 2D Semiconductors in Flexible and High-Frequency Electronics

In 2024, nanoribbon transistors fabricated from sonochemically exfoliated black phosphorus demonstrated on/off ratios of 1.7 × 10⁶ and mobilities of 1,506 cm² V⁻¹ s⁻¹, meeting the sub-5 nm roadmap thresholds. One of the key drivers for their adoption is the width-dependent bandgaps, which range from 0.29 eV to 0.64 eV. This feature allows designers to modify logic levels without relying on alloying processes, providing flexibility in design. Another significant driver is the material's in-plane anisotropy, which enables directional charge control. This characteristic is particularly important for applications such as bendable displays, where precise charge control is essential. The use of smooth-edge channels addresses short-channel effects, ensuring that transconductance levels remain above 200 µS µm⁻¹ at gate lengths smaller than 20 nm, a size where silicon typically encounters increased leakage issues. Additionally, the ability to operate at transfer temperatures below 150 °C is a critical factor for manufacturers, as it aligns with the requirements of polyimide substrates commonly used in wearable technology. Furthermore, surface-coordination chemistry supported by the NSF and introduced in 2026 provides ambient stability lasting up to a month. This stability is expected to play a significant role in accelerating the commercialization of these transistors.he upstream revenue stream of the black phosphorus market.

Rapid Uptake of BP-Based Photonic Integrated Circuits

Using NanoBLACK™, Iris Light Technologies achieved an impressive 11.2 A W⁻¹ responsivity at 1,550 nm on standard CMOS wafers. By employing twist-stacked devices, they expanded detection capabilities to 2,700 nm and incorporated bipolar circular-polarization discrimination, a crucial feature for encrypted free-space optics. Through out-of-plane strain engineering, they successfully red-shifted cavity modes by over 100 nm under −3% compression, even without thermal loading, paving the way for dense photonic routing. This material not only surpasses molybdenum disulfide in quantum efficiency within the near-infrared spectrum but also boasts a bandgap, unlike graphene, facilitating efficient modulation. The 2025 contract from AFRL underscores the end-user's confidence in translating these advancements to defense-grade mid-IR systems.

Mainstream R&D Funding for BP Anodes in Next-Gen Li/Na-Ion Batteries

Black phosphorus has a theoretical capacity of 2,596 mAh g⁻¹, which is significantly higher than that of graphite. Prototype sodium-ion batteries have demonstrated an energy density of 160 Wh kg⁻¹, with 82% efficiency retention at temperatures as low as −20 °C over 800 cycles. The planned 100-ton-per-year facility by Xingfa Group, combined with Ruifeng's use of a CO₂ exfoliation method, is expected to reduce costs to below USD 0.20 per gram at scale. These advancements are driving the integration of black phosphorus into battery supply chains. Sodium-ion battery developers are increasingly favoring phosphorus due to its volumetric expansion of up to 300%, which is lower compared to silicon's expansion of over 400%. This characteristic contributes to improved mechanical durability. Additionally, black phosphorus is being utilized in other applications, such as catalysts that improve H₂O₂ yields by 20% and odor-control media adopted by Midea. Furthermore, China’s National Natural Science Foundation has allocated multi-million-dollar grants for 2025 to support research on PEGylated nanosheet anodes, which is expected to strengthen collaboration between academic institutions and industrial players.

Defense Investment in BP-Enabled Mid-IR Stealth and Secure-Comms Coatings

AFRL's 2025 to 2026 awards emphasize the growing importance of broadband mid-IR absorption, particularly in scenarios where traditional radar-absorbing layers are less effective. The ability to tune bandgaps enables the suppression of thermal signatures within the 3 to 5 µm atmospheric window, which is a critical factor for enhancing aircraft stealth capabilities. Twist-stacked photodetectors contribute to improved circular-polarization readouts that are resistant to linear noise, thereby supporting the development of covert optical communication systems. Spin-valve tests indicate lifetime anisotropy ratios nearing 6, which facilitates the implementation of direction-selective logic essential for quantum-secure data transport. Although hermetic packaging continues to increase system costs by 30 to 50 percent, its biodegradation into harmless phosphate offers a more sustainable end-of-life solution compared to fluorinated coatings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ambient-air instability and encapsulation cost premium | -7.4% | Global, most acute in regions with humid climates (Southeast Asia, coastal manufacturing zones) | Short term (≤2 years) |

| Regulatory uncertainty around nanomaterial toxicology | -4.1% | Europe (REACH), North America (EPA TSCA), with cascading effects on Asia-Pacific exports | Medium term (2-4 years) |

| IP thicket on BP exfoliation routes drives licensing costs | -3.80% | Global, particularly impacting North America and Europe startups; Asia-Pacific benefits from domestic patent pools | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ambient-Air Instability and Encapsulation Cost Premium

Unprotected nanosheets experience a significant reduction of 60% in UV-visible absorption within 72 hours. This degradation necessitates the use of glovebox handling and multi-layer barriers, which can increase landed costs by up to 50%. Coordination bonding with oxaliplatin improves absorption retention to 62%. Cell-membrane coatings further enhance retention to 78%, although each additional layer contributes to increased material and labor costs. Polydopamine films are capable of extending the lifespan of these nanosheets to several weeks, but this improvement comes with a 30% rise in raw material expenses. Embedding in PLGA offers a slow-release mechanism but results in a cost increase of 35-45%. Electrochemical exfoliation in phytic acid produces edge-passivated flakes that require minimal post-encapsulation processing. However, the throughput remains limited to less than 10 grams per batch, which restricts its industrial relevance. Battery manufacturers encounter challenges as they must maintain anode prices below USD 5 per gram to remain competitive with graphite. In comparison, buyers in the photonics sector are more accommodating, with a willingness to pay between USD 500 and 1,000 per gram, making it easier for them to manage overhead costs.

Regulatory Uncertainty Around Nanomaterial Toxicology

Agencies face challenges due to the absence of harmonized dose-response frameworks, which contributes to delays in safety-data submissions as cytotoxicity increases beyond 200 µg mL⁻¹. Exfoliated Black phosphorus has not been categorized under REACH, resulting in a lack of clarity for importers regarding tonnage bands and labeling requirements. The omission of nanophase listings in the U.S. TSCA inventory leads to delays in pre-manufacture notifications, which can extend timelines by six to twelve months. Quantum-dot grades remain in vivo for extended periods but eventually degrade into harmless phosphate, presenting a complex risk-benefit scenario that regulators need to address. Companies planning multi-regional launches encounter increased compliance costs, with budgets potentially rising by up to 25 % due to inconsistencies in national regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Nanosheets Narrow the Cost Gap With Powder

In 2025, powder accounted for 36.67% of the Black phosphorus market share, supported by its application in battery slurries and catalysts that accommodate irregular morphologies. Exfoliated nanosheets, priced at USD 800–1,200 per gram, are expected to grow at a rate of 41.23%. This growth is attributed to the increasing demand from device engineers for thicknesses under 10 nm and atomically smooth edges. The market size for Black phosphorus nanosheets is projected to increase from USD 5.7 million in 2026 to USD 36 million by 2031. Crystals, with a purity level exceeding 99.999%, continue to attract interest for research purposes. However, their market share may decline due to competition from wafer-scale chemical-vapor growth. Thin-film methods, such as molecular beam epitaxy, currently achieve less than 8% device-grade coverage. The Chips-Act pilot lines are anticipated to improve output and reduce defectivity by 50%, potentially lowering costs.

Equipment manufacturers report that sonochemical exfoliation achieves 95% yield for nanoribbons, which helps reduce post-sorting waste. By reducing edge roughness, nanosheets demonstrate better performance than powder-derived sintered layers in both transistor mobility and photodetector responsivity. On the other hand, powder remains a key material for anode prototypes targeting a cost ceiling of USD 0.20 Wh⁻¹, as its downstream milling aligns well with existing slurry lines. With the scaling of CO₂ exfoliation, the Black phosphorus market may experience a reduction in nanosheet pricing to approximately USD 150 per gram. This price adjustment could eliminate the historical premium and strengthen their position in terms of compound annual growth rate.

By Application: Energy Storage Surges Past Electronics in Growth Velocity

In 2025, electronics and semiconductors accounted for 40.33% of total revenue, supported by nanoribbon FETs achieving a mobility benchmark of 1,506 cm² V⁻¹ s⁻¹. The market for Black phosphorus in energy storage is projected to grow from USD 6.9 million in 2026 to USD 46.8 million by 2031, reflecting a 42.46% CAGR. This growth is primarily driven by the increasing focus of anode developers on achieving a theoretical capacity of 2,596 mAh g⁻¹. The photonics segment holds a 22% market share, influenced by the performance of infrared detectors with responsivities of 11.2 A W⁻¹. In the biomedical segment, demand is supported by the biodegradability of Black phosphorus and its photothermal conversion efficiency, which ranges between 21% and 25%. These properties are being utilized in applications such as cancer treatment and chronic wound care.

In the energy storage segment, advancements in cost efficiency by Ruifeng have positioned Black phosphorus electrodes as competitive alternatives to traditional materials like hard carbon and silicon. Sodium-ion cells are demonstrating an energy density of 160 Wh kg⁻¹ at temperatures as low as −20 °C, which is enabling their use in applications such as cold-climate grids and electric vehicles. Growth in the electronics segment is expected to slow after 2028 as material replacements stabilize at sub-5 nm nodes. However, the integrated photonics segment is anticipated to maintain its growth trajectory, driven by the increasing demand for Telecom-grade 1,550 nm modulators that require broadband gain. The environmental catalysis segment, although currently accounting for less than 5% of the market share, shows potential for future growth. BP-Pd hybrids have demonstrated a 20% increase in H₂O₂ yields, which has attracted interest from water-treatment OEMs.

Geography Analysis

In 2025, the Asia-Pacific region contributed 47.78% of global revenue and is projected to grow at a compound annual growth rate (CAGR) of 41.56%. Within the region, China has implemented Ruifeng’s CO₂ route, which reduces batch cycles from 15 days to 3 days. This process significantly lowers variable costs by 98% and supports local cell factories located in Jiangsu and Guangdong. Additionally, Japan and South Korea are concentrating on advancements in photonic and logic benchmarks. These countries have published notable data on spin-transport and chiral-detection, which are expected to influence fab evaluations planned for 2028.

In North America, funding from AFRL and NSF programs is directed toward secure-communication photonics and oxidative-stability chemistry. However, the region continues to rely on imports, as domestic producers have not yet achieved kilogram-scale throughput. This dependency exposes buyers to risks associated with freight and lead times from the Asia-Pacific region. Canada is actively collaborating on spin transport research, while Mexico is conducting tests on environmental catalysts. Despite these efforts, commercial production volumes in the region remain limited.

Europe is encountering challenges due to ambiguities in REACH regulations, which can extend product-qualification cycles by up to a year. Although Chips-Act grants are intended to enhance the region’s competitiveness, pilot production lines still depend on seed crystals imported from China. This reliance keeps per-gram spot prices above USD 500. Italy and Spain are leading efforts in biomedical trials, focusing on controlled degradation techniques to accelerate the development of bone-regrowth scaffolds. In other regions, emerging clusters in Brazil and South Africa are exploring the use of water-purification catalysts. However, these efforts are hindered by import tariffs ranging from 15% to 25%, which delay the implementation of these initiatives.

Competitive Landscape

Black Phosphorus market remains partially consolidated, with HQ Graphene, ACS Material LLC, Ossila Ltd, American Elements, and 2D Semiconductors Inc. leading the pack.

Nanjing XFNANO and SixCarbon Technology, boasting greater than 99.999% purity crystals and custom functionalization, command premiums of USD 552–1,056 per gram. Meanwhile, volume-driven players like ACS Material and Ossila cater to battery and catalyst users, selling powder at USD 435–585 per gram. Disruptors such as Iris Light Technologies, with their NanoBLACK™, are targeting wafer-level CMOS integration, pricing below USD 100 per 200 mm wafer. This strategic pricing could divert demand from traditional exfoliated flakes.

As patent thickets emerge around liquid-phase exfoliation and electrochemical routes, competitive intensity heightens, nudging smaller entrants towards licensing or exit. Encapsulation expertise acts as a significant barrier, with dual-layer chemistries enhancing stability to 78% absorption retention and extending shelf life to several weeks. Suppliers with pre-approved REACH dossiers can expedite European customer launches by up to a year, justifying a 10–15% price premium.

Globally, fewer than 20 firms can stabilize Black Phosphorus beyond 72 hours, granting early movers a moderate pricing edge. Xingfa Group’s forthcoming 100-ton-per-year line has the potential to outpace all competitors combined, steering the Black Phosphorus market towards an oligopoly and pressuring research-grade vendors to merge. Ruifeng’s developing supercritical CO₂ exfoliation technology, which promises a 30–40% cost advantage over traditional methods, sees European fabs negotiating local production licenses at USD 50,000 per variant.

Black Phosphorus Industry Leaders

2D Semiconductors

American Elements

Ossila

ACS Material

HQ graphene

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: National Science Foundation funded dual metal complex functionalization research on black phosphorus to stabilize surfaces via coordination chemistry, addressing oxidation-induced mobility degradation and extending device lifetimes from weeks to months, with findings published in Nano Letters.

- January 2025: United States Air Force Research Laboratory awarded Iris Light Technologies a USD 110,000 STTR Phase I contract to develop low-swap frequency combs for atomic clocks enabled by black phosphorus absorbers, advancing mid-infrared photonics for defense, secure communications, and precision timing applications.

Global Black Phosphorus Market Report Scope

Black phosphorus (BP) is the most thermodynamically stable, least reactive, and densest crystalline allotrope of phosphorus. It is a 2D-layered, semiconductor material characterized by a puckered, orthorhombic honeycomb lattice that behaves similarly to graphite. It is valued for its tunable bandgap, high carrier mobility, and ability to exfoliate into thin sheets known as phosphorene.

The market is segmented by form, application, and geography. By form, the market is segmented into powder, crystal, exfoliated nanosheets, and thin films. By application, the market is segmented into electronics and semiconductors, energy storage (including batteries and super-capacitors), photonics and optoelectronics, biomedical and biosensors, environmental catalysis and water treatment, and other applications (including additives and research-grade). The report also covers the market size and forecasts for Black Phosphorus in 17 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| Powder |

| Crystal |

| Exfoliated Nanosheets |

| Thin Films |

| Electronics and Semiconductors |

| Energy Storage (Batteries and Super-capacitors) |

| Photonics and Optoelectronics |

| Biomedical and Biosensors |

| Environmental Catalysis and Water Treatment |

| Others (Additives, Research-grade, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Powder | |

| Crystal | ||

| Exfoliated Nanosheets | ||

| Thin Films | ||

| By Application | Electronics and Semiconductors | |

| Energy Storage (Batteries and Super-capacitors) | ||

| Photonics and Optoelectronics | ||

| Biomedical and Biosensors | ||

| Environmental Catalysis and Water Treatment | ||

| Others (Additives, Research-grade, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the Black phosphorus market expected to grow through 2031?

The Black phosphorus market is projected to expand at 40.66% CAGR between 2026 and 2031, rising from USD 21.72 million in 2026 to USD 119.58 million by 2031.

Which application area will add the most new revenue?

Energy-storage uses, especially Li-ion and Na-ion anodes, are forecast to post the highest 42.46% CAGR, outpacing electronics and photonics.

Which region leads demand for black phosphorus?

Asia-Pacific holds 47.78% share and registers the fastest 41.56% CAGR.

Why is encapsulation critical for commercial adoption?

Unprotected material oxidizes within days; hermetic or chemical barriers extend shelf life and are currently responsible for up to 50% of landed costs.

What competitive advantage does Black phosphorus offer over graphene?

It combines high mobility with an intrinsic, width-tunable bandgap, enabling efficient switching and broadband photonics that graphene’s zero-bandgap limits.

How concentrated is industry supply?

Fewer than 20 suppliers handle stability-grade material, and the top five are on track to control roughly 70% of capacity once new Chinese plants ramp, indicating moderate concentration.

Page last updated on: