Aluminum Recycling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

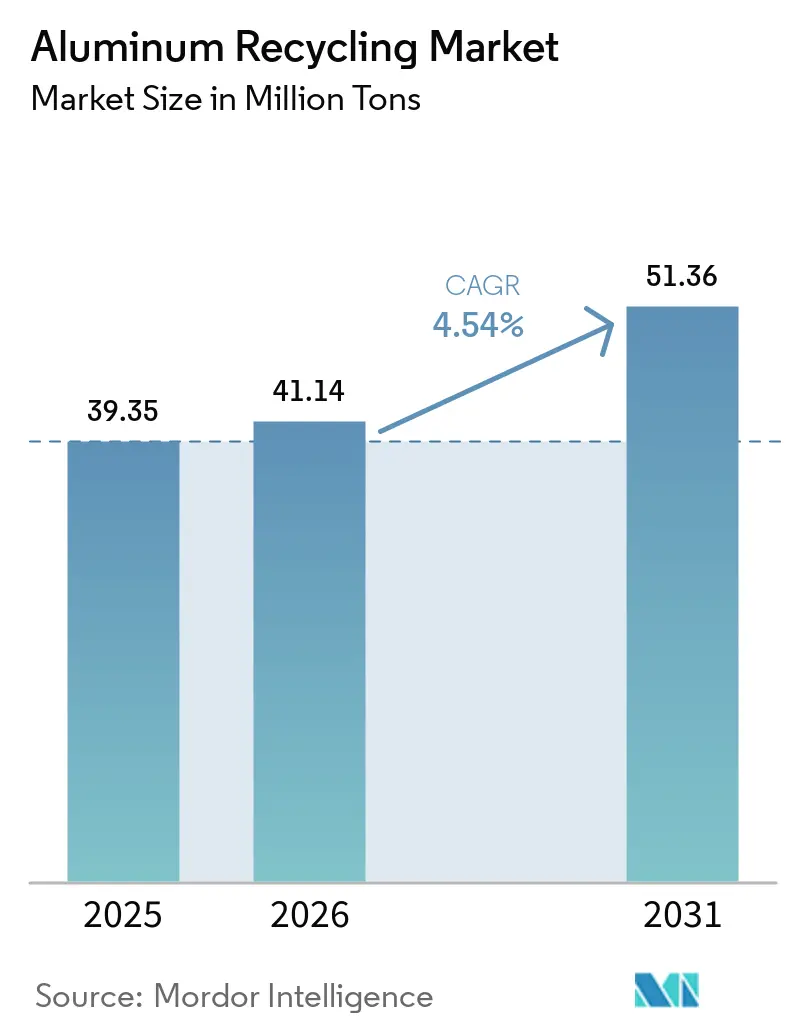

| Market Volume (2026) | 41.14 Million tons |

| Market Volume (2031) | 51.36 Million tons |

| Growth Rate (2026 - 2031) | 4.54% CAGR |

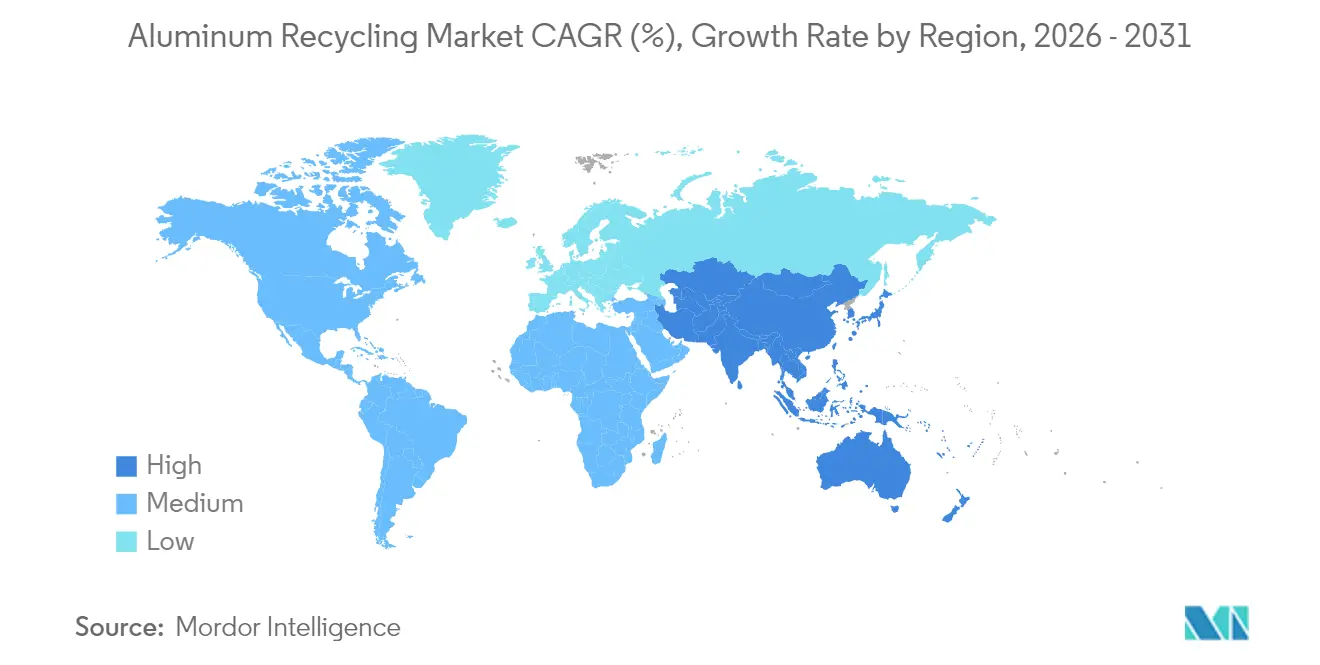

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aluminum Recycling Market Analysis by Mordor Intelligence

Aluminum Recycling Market size in 2026 is estimated at 41.14 million tons, growing from 2025 value of 39.35 million tons with 2031 projections showing 51.36 million tons, growing at 4.54% CAGR over 2026-2031. Rising energy costs, circular-economy legislation, and OEM lightweighting targets are pushing manufacturers to favor recycled over primary metal, because secondary production consumes only 5% of the energy required for virgin smelting while preserving material properties indefinitely. Construction booms in Asia-Pacific, closed-loop beverage-can schemes in Europe, and worldwide electric-vehicle (EV) adoption underpin demand for recycled billet, sheet, and casting alloys. At the same time, AI-enabled sorting systems are raising purity yields, expanding the supply of aerospace- and automotive-grade feedstock. Consolidation among mid-tier smelters is quickening as larger players acquire regional recyclers to secure scrap streams and deploy capital-intensive purification technology.

Key Report Takeaways

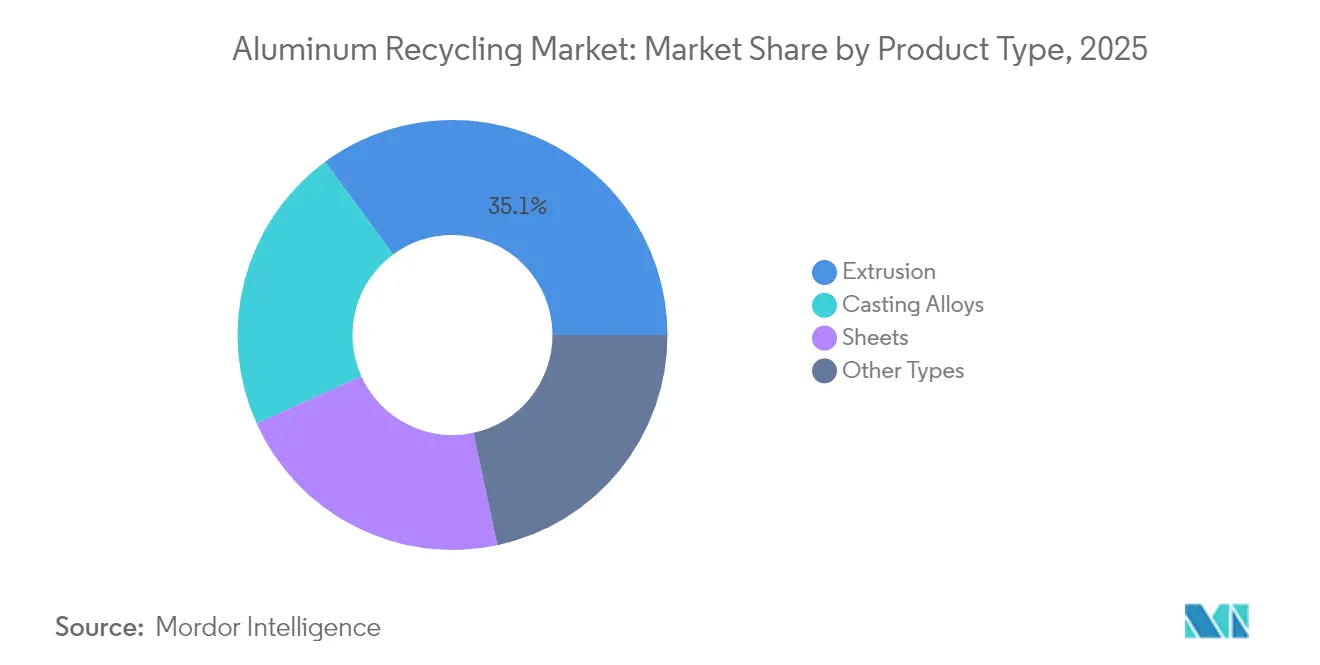

- By product type, extrusion captured 35.10% of the aluminum recycling market share in 2025 and is expected to record the fastest CAGR at 5.29% through 2031.

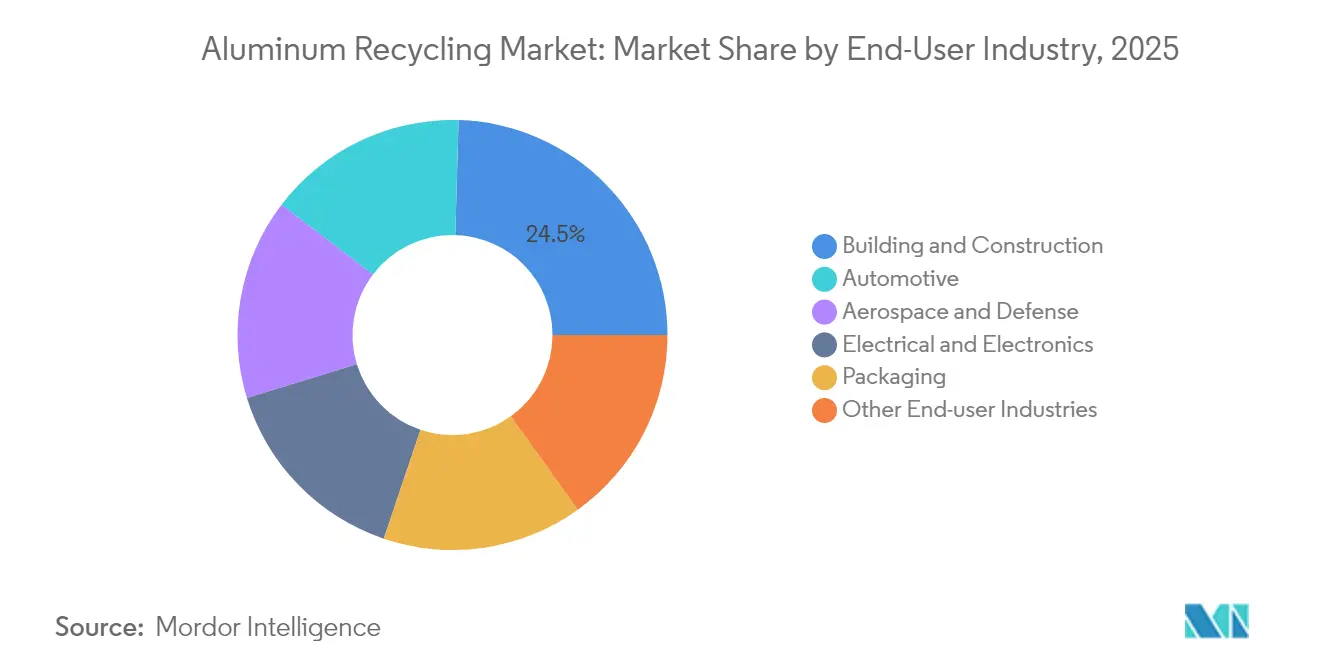

- By end-user industry, building and construction held 24.55% of the aluminum recycling market size in 2025, while aerospace and defense are advancing at a 5.17% CAGR to 2031.

- By geography, Asia-Pacific dominated with 61.20% revenue share in 2025, and the region is expanding at a 5.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aluminum Recycling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-saving advantage over primary aluminium production | +1.20% | Global; strongest in high-energy-cost regions | Long term (≥ 4 years) |

| Growing utilisation of recycled aluminium in construction | +0.80% | Asia-Pacific core; expanding to North America & EU | Medium term (2-4 years) |

| Booming demand from automotive lightweighting | +1.00% | North America & EU; spreading to APAC | Medium term (2-4 years) |

| EU beverage-can closed-loop programmes scaling up | +0.40% | Europe; policy replication elsewhere | Short term (≤ 2 years) |

| Adoption of AI-enabled scrap-sorting platforms | +0.60% | Global; early uptake in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy-saving advantage over primary aluminum production

Secondary smelting cuts energy use by 95% compared with electrolytic processes, a gap that widens when electricity prices spike and carbon fees tighten. North American secondary producers slashed their average carbon footprint by 60% between 2020 and 2024, enabling them to win supply contracts with automakers and aircraft OEMs that now audit Scope 3 emissions. Spot alumina breached USD 800 per ton in December 2024, but recyclers avoided that cost because they bypassed alumina refining entirely. Investment banks subsequently lifted 2025 aluminum- industry price forecasts, giving secondary smelters additional margin headroom. Regions with carbon-price regimes, such as the EU and parts of North America, are therefore accelerating substitution of primary with recycled metal.

Growing utilization of recycled aluminum in construction

Rapid urbanization and green-building codes are driving builders to specify high-recycled-content extrusions for curtain walls, façade systems, and window frames[1]TOMRA, “Aluminum – Material Sorting,” tomra.com . Certification schemes such as LEED and BREEAM award credits for recycled content, magnifying the pull effect beyond pure cost savings. Asian construction demand climbed 9% between 2022 and 2024, and similar momentum is forecast through 2027 as megacities in India, Indonesia, and the Philippines expand mass-transit and residential projects. Europe’s extrusion plants already operate at recycling rates above 90%, serving as policy templates for new material-passport initiatives in Canada and Japan. Strong construction uptake also shortens scrap collection loops, ensuring a stable inflow of post-consumer profiles for remelt furnaces.

Booming demand from automotive lightweighting

EV platforms incorporate 30% more aluminum by mass than internal-combustion counterparts to offset battery weight, and manufacturers increasingly specify closed-loop scrap return agreements with their rolling-mill suppliers. Novelis demonstrated an 85% recycled-content rear subframe in 2024 pilot builds for a U.S. automaker, proving that stringent formability and crash-performance targets can be met. The EU Battery Regulation 2023/1542 introduces minimum recycled-content thresholds for battery housings from 2027, further lifting demand. Automakers are also investing in dismantling facilities to capture end-of-life aluminum from bumpers, engines, and closures, improving material traceability and security of supply.

Adoption of AI-enabled scrap-sorting platforms

TOMRA’s GAINnext system reaches 98% purity when sorting used beverage cans at 2,000 ejections per minute, eliminating manual pickers and boosting plant throughput. Norsk Hydro and PADNOS are co-deploying similar deep-learning recognition units across the U.S. Midwest, proving scalability for regional processors. Sortera Technologies closed a USD 30.5 million funding round in January 2025 to commercialize its multi-material upcycling facility that extracts aluminum, copper, and zinc from mixed demolition debris[2]Sortera Technologies, “Sortera Technologies Closes $30.5 Million in New Funding,” sorteratechnologies.com . Higher purity lets smelters access premium aerospace and automotive contracts and reduces chlorine salt-slag volumes, improving ESG metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of undesirable impurities (Fe, Mg, Zn) | -0.70% | Global; acute in mixed-scrap regions | Long term (≥ 4 years) |

| Scrap-price volatility compressing secondary-smelter margins | -0.50% | Global; regional variations | Short term (≤ 2 years) |

| Competition from low-cost virgin metal in periods of surplus | -0.30% | Regions with surplus primary capacity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Presence of undesirable impurities (Fe, Mg, Zn)

Contamination above 0.20% iron disqualifies aluminum for most aerospace and EV structural uses, forcing recyclers to divert tainted batches to foundry or de-oxidation markets at steep discounts. Mixed streams from demolition sites often blend 6000-series and 7000-series alloys with painted architectural profiles, raising purification costs and energy consumption. Large smelters add fluxing agents and employ electromagnetic stirrers to lower iron pick-up, but the capital hurdle keeps smaller operators out of premium markets. Iron contamination also creates micro-segregation during solidification, impairing fatigue resistance—an issue that aircraft OEMs monitor closely through rigid supplier-qualification audits.

Scrap-price volatility compressing secondary-smelter margins

Fragmented supply chains and regional demand spikes cause scrap premiums to whipsaw; European used-beverage-can prices swung from USD 1,450 to USD 1,020 per ton during H1 2024. Secondary smelters carry just 30-45 days of raw-material inventory, so sudden jumps squeeze conversion margins before they can renegotiate off-take contracts. Smaller recyclers lack hedging desks and must frequently buy spot, amplifying financial risk. Volatility chills investment in furnace upgrades and high-speed sorters, delaying capacity additions that could alleviate supply tightness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Extrusion Dominance Across Applications

Extrusions held a commanding 35.10% aluminum recycling market share in 2025 as architects and automakers turned to light, corrosion-resistant profiles for façades, chassis members, and battery enclosures. The segment is on track for a 5.29% CAGR through 2031, steadily widening its gap over sheet and casting grades. Extruded sections often use single-alloy compositions, making them ideal candidates for closed-loop recycling, which conserves alloy chemistry and minimizes downgrading losses. Constellium successfully remelted end-of-life aircraft skins into aerospace-grade billet during 2024 trials, demonstrating the technical viability of multiple recycling loops without alloy dilution.

Sheets represent a key category, supplying automotive outer panels and beverage can bodies where surface quality is critical. Sheet mills are investing in continuous casting lines that accept higher scrap percentages while meeting strict earing and formability targets. Casting alloys account for a smaller volume but enjoy robust demand in engine blocks and e-motor housings that require complex geometry and thermal conductivity. Foil and wire applications remain steady niche outlets; however, rising substitution by recycled polymers in flexible packaging is capping foil growth.

By End-user Industry: Construction Leadership with Aerospace Acceleration

Building and construction contributed 24.55% to the aluminum recycling market size in 2025, underpinned by infrastructure stimulus in China, India, and the United States. Recycling rates are buoyed by the ease of separating extruded frames during demolition and the growing availability of design-for-disassembly guidelines in building codes. Future growth remains healthy but incremental, reflecting the mature nature of the sector.

Aerospace and defense is the standout growth engine, advancing at a 5.17% CAGR to 2031 as airframe manufacturers certify recycled billet for wing ribs, seat tracks, and internal brackets. Stringent AS9100D quality-management requirements push recyclers to deploy high-resolution X-ray fluorescence scanners and vacuum-degassing furnaces that remove trace hydrogen and alkali metals. Automotive demand stays resilient thanks to higher aluminum intensity in EV platforms, with automakers now issuing recycled-content targets of 30-50% per vehicle. Electrical and electronics growth is moderated by complex multi-metal assemblies that complicate disassembly and purity control, whereas packaging enjoys steady volumes from beverage can loops but faces competition from steel and PET in food containers.

Geography Analysis

Asia-Pacific accounted for 61.20% of global aluminum recycling market share in 2025 and is projected to expand at a 5.55% CAGR through 2031. China’s secondary capacity additions align with its 45 million-ton primary cap, nudging smelters toward scrap imports and domestic collection schemes. India’s Smart Cities Mission is injecting recycled extrusions into transit corridors and affordable housing, further lifting billet demand. Japan and South Korea supply high-grade scrap sorting technology, reinforcing regional vertical integration from collection to finished goods.

North America and Europe collectively represent a significant portion of global demand. More than 80% of U.S. aluminum production was secondary in 2024, up from less than 30% four decades earlier. Deposit-return laws in ten U.S. states and federal tax credits for recycled content underpin stable can-sheet flows. The EU’s 90% collection requirement for metal beverage containers by 2029 is accelerating investment in dedicated can-recycling plants. Both regions face high power tariffs, creating extra impetus to integrate renewables: Hydro’s EUR 180 million Torija plant in Spain will source on-site solar to cut melt costs.

The Middle East and Africa trail in volume but offer outsized growth. Emirates Global Aluminium (EGA) acquired Minnesota-based Spectro Alloys for USD 80 million and restarted production in July 2025, signaling a push to capture the GCC’s USD 6 billion recycling potential. Morocco commissioned its first dedicated aluminum scrap refinery in 2024, leveraging low solar power costs. South America’s prospects cluster around Brazil, where a 90% renewable-electricity grid lowers the carbon intensity of secondary metal and meets the sustainability thresholds of multinational beverage and auto brands.

Competitive Landscape

The aluminum recycling market remains moderately fragmented but is consolidating as technology-rich incumbents absorb regional specialists. Novelis, Norsk Hydro, Alcoa, and Speira control significant smelting and rolling capacity, each pursuing vertical integration to secure scrap pipelines and deploy capital-intensive AI sorters. Speira invested EUR 11 million in four German and Norwegian recycling furnaces in 2024 to lift billet output for automotive sheet. Hydro’s Torija project underscores European majors’ shift toward localized circular-economy hubs.

EGA’s acquisition spree exemplifies cross-regional consolidation, granting it immediate access to U.S. customers and a technology platform for its RevivAL recycled-billet brand. Smaller U.S. players are responding by forming scrap-aggregation cooperatives to pool feedstock and achieve scale economies. Investment is gravitating toward AI-powered impurity detection, vacuum refining, and chlorine-free fluxing agents, which together push melt-loss rates below 2% and enable entry into high-margin aerospace contracts. Compliance capabilities are becoming a decisive differentiator: plants certified to ISO 14064 and AS9100D gain preferred-supplier status with OEMs, whereas operators lacking digital traceability risk exclusion from premium value chains. Competition is therefore shifting from volume to quality, technology, and regulatory adherence.

Aluminum Recycling Industry Leaders

Norsk Hydro ASA

Novelis Inc.

REAL ALLOY

Matalco Inc

Constellium

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Emirates Global Aluminium PJSC has initiated production at the expanded Spectro Alloys aluminium recycling facility in Minnesota, USA. The first phase of this expansion increases secondary billet production capacity by 55,000 tonnes. Full-scale production is anticipated to be achieved by early next year.

- March 2025: Norsk Hydro ASA has initiated the construction of its flagship aluminium recycling plant in Torija, Spain. This advanced facility, situated north of Madrid, involves a EUR 180 million investment. The project underscores Hydro's dedication to enhancing the European circular economy by retaining more post-consumer scrap within the production cycle.

Global Aluminum Recycling Market Report Scope

Aluminum recycling is the process by which scrap aluminum can be reused in products after its initial production. Aluminum recycling involves reprocessing used aluminum products to create new materials. This sustainable practice conserves resources and energy. In applications, recycled aluminum finds use in various industries, including automotive parts, beverage cans, packaging materials, and construction components. The aluminum recycling market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into casting alloys, extrusion, sheets, and other product types. By end-user industry, the market is segmented into automotive, aerospace and defense, building and construction, electrical and electronics, packaging, and other end-user industries. The report also covers market sizes and forecasts in 28 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Casting Alloys |

| Extrusion |

| Sheets |

| Other Types |

| Automotive |

| Aerospace and Defense |

| Building and Construction |

| Electrical and Electronics |

| Packaging |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Spain | |

| Turkey | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Casting Alloys | |

| Extrusion | ||

| Sheets | ||

| Other Types | ||

| By End-user Industry | Automotive | |

| Aerospace and Defense | ||

| Building and Construction | ||

| Electrical and Electronics | ||

| Packaging | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the aluminum recycling market in 2026?

The market processes 41.14 million tons of recycled aluminum in 2026 and is projected to reach 51.36 million tons by 2031.

What is the forecast growth rate for recycled aluminum?

Volume is expected to expand at a 4.54% CAGR from 2026 to 2031, driven by energy savings, lightweighting, and circular-economy policies.

Which region leads in recycled-aluminum consumption?

Asia-Pacific holds 61.20% of global demand thanks to China’s massive capacity and India’s infrastructure expansion.

Why is recycled aluminum gaining popularity in automotive manufacturing?

EV platforms use more aluminum for lightweighting, and closed-loop deals let automakers secure low-carbon, high-purity metal while meeting recycled-content mandates.

What technologies are improving scrap purity?

AI-enabled optical and X-ray sorters, vacuum-degassing furnaces, and chlorine-free fluxes are collectively boosting recycled-metal purity to 98% for demanding aerospace and automotive applications.

Page last updated on: