Pediatric Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.53 Billion |

| Market Size (2031) | USD 19.90 Billion |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

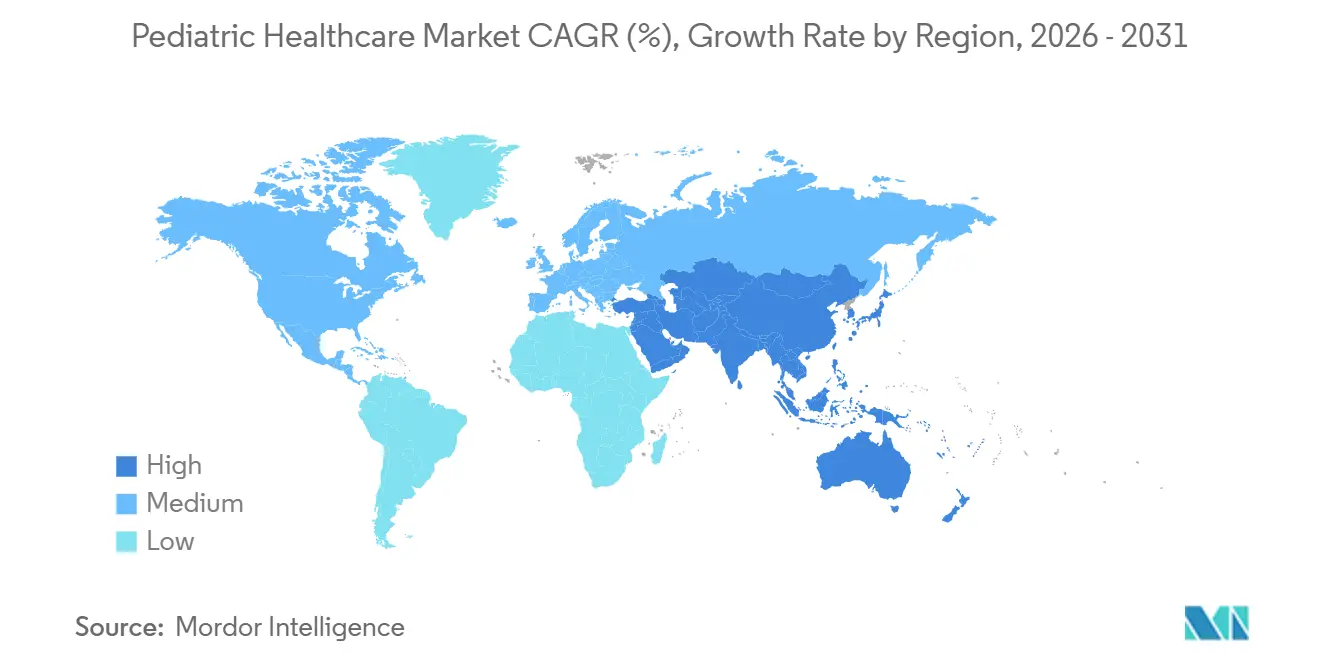

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pediatric Healthcare Market Analysis by Mordor Intelligence

The Pediatric healthcare market size was valued at USD 15.93 billion in 2025 and estimated to grow from USD 16.53 billion in 2026 to reach USD 19.90 billion by 2031, registering a 3.78% CAGR between 2026 and 2031. Gene therapies are entering routine clinical pathways, pushing payers toward outcomes-based contracts, while artificial intelligence tools are shortening diagnostic queues in radiology and behavioral health. Remote monitoring platforms are gaining favor because they lower emergency-department use and let clinicians intervene earlier. High-income governments continue to expand immunization budgets, guaranteeing vaccine uptake even as digital therapeutics draw a rising share of venture funding. Meanwhile, investment in micro-hospital formats brings specialty care closer to peri-urban neighborhoods, tempering the capacity gap that once funneled every complex case to tertiary centers.

Key Report Takeaways

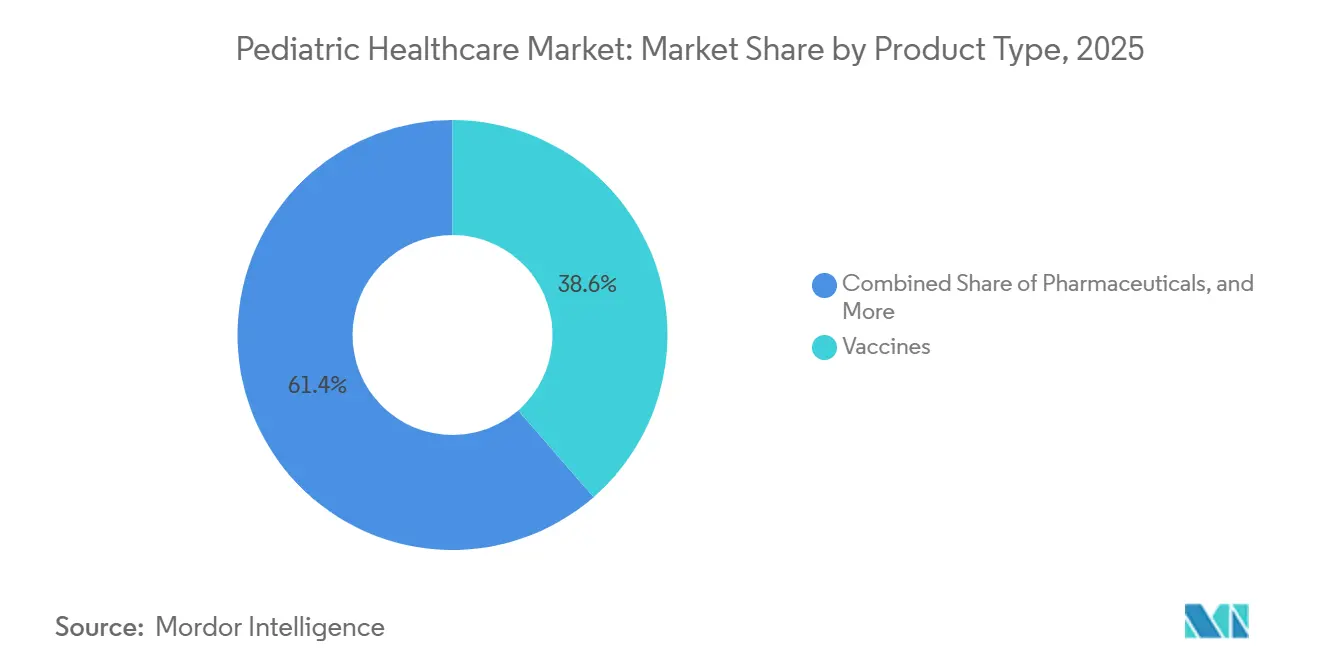

- By product type, vaccines led with a 38.55% share of the pediatric healthcare market in 2025, while digital health solutions posted the fastest growth at a 5.25% CAGR through 2031.

- By therapeutic area, infectious diseases accounted for 33.53% of 2025 revenue, whereas oncology is forecast to expand at a 4.75% CAGR to 2031.

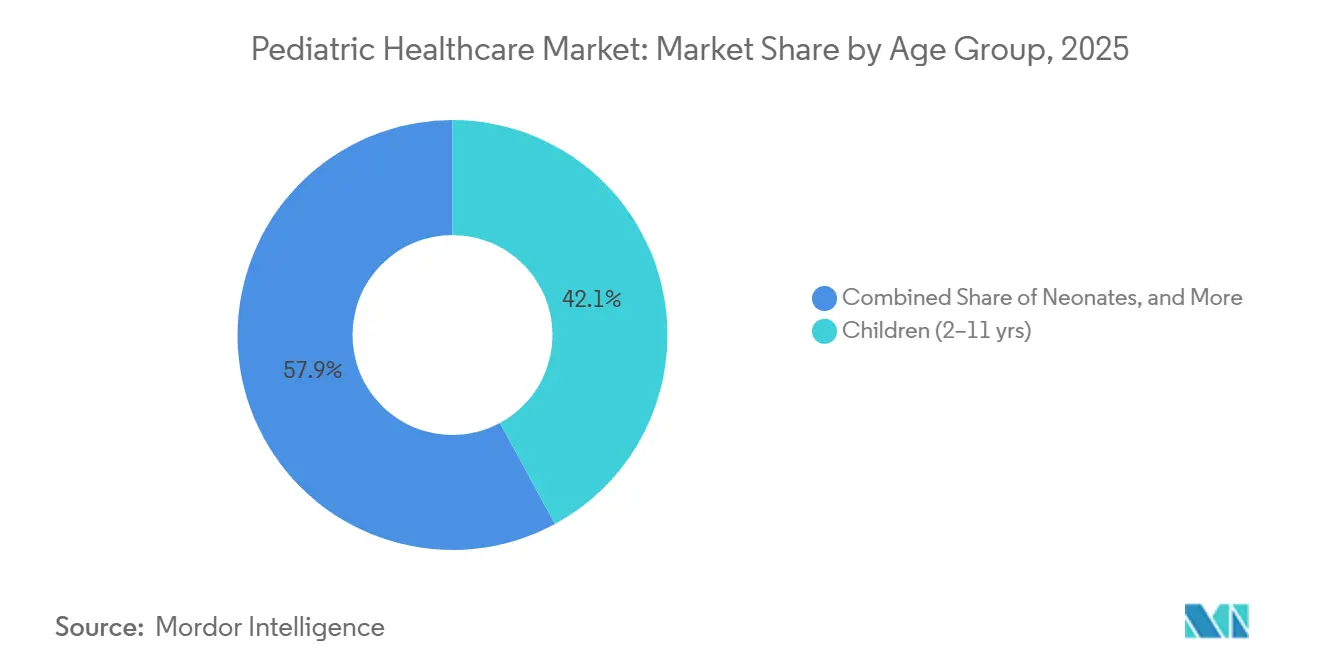

- By age group, school-age children (2–11 years) accounted for 42.15% of demand in 2025; adolescents (12–18 years) are advancing at a 4.82% CAGR on the back of digital mental health tools.

- By care setting, hospitals accounted for 54.65% of 2025 revenue; telehealth is growing at a 6.32% CAGR as several U.S. states lock in payment parity.

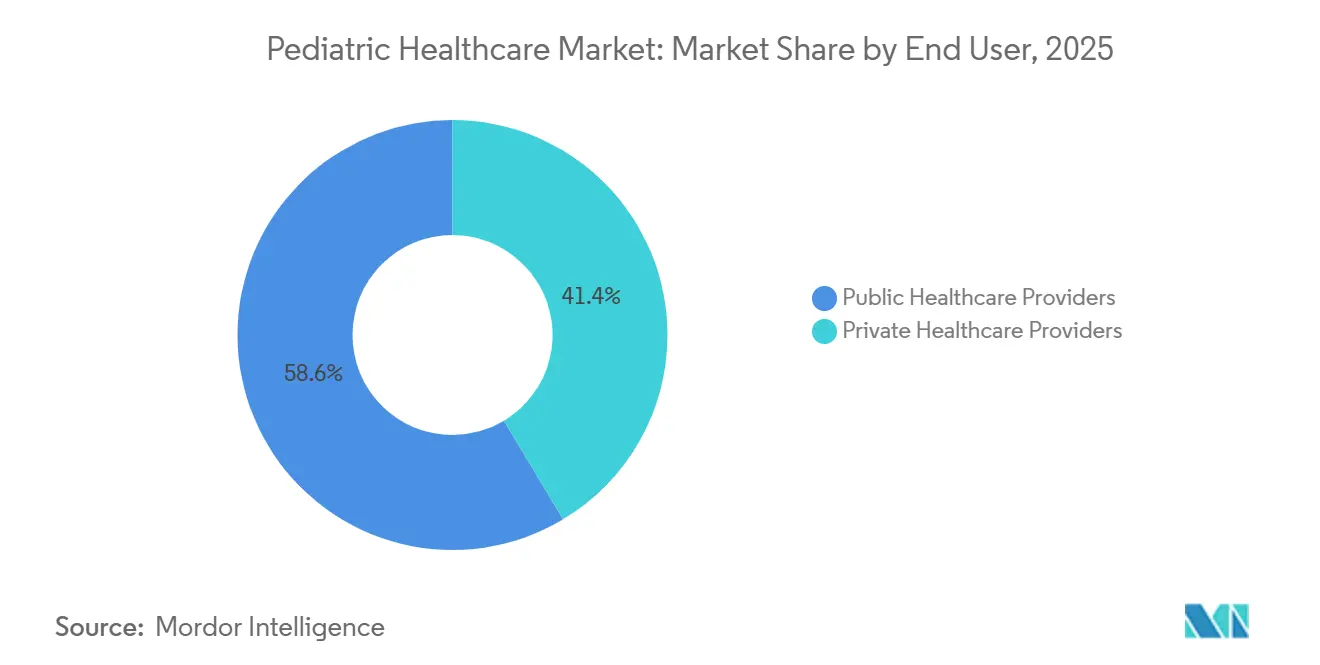

- By end user, public providers accounted for 58.55% of spending in 2025, yet private operators are growing at a 5.22% CAGR, signaling affluent families' willingness to bypass public queues.

- By geography, North America accounted for 35.23% revenue in 2025, while Asia-Pacific leads growth at 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pediatric Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Routine Pediatric-Immunization Funding Momentum | +0.9% | Global, concentrated in GAVI-eligible nations and the U.S. VFC program | Medium term (2-4 years) |

| Gene-Therapy Approvals for Rare Pediatric Diseases | +0.7% | North America, EU, urban hubs in China and India | Long term (≥ 4 years) |

| AI-Assisted Pediatric Radiology Adoption | +0.6% | North America, Western Europe, APAC tier-1 cities | Medium term (2-4 years) |

| Re-Emergence of RSV and Other Respiratory Outbreaks | +0.8% | Global, with acute seasonal impact in temperate zones | Short term (≤ 2 years) |

| School-Based Telehealth Roll-Outs | +0.5% | United States, Canada, pilots in the UK and Australia | Medium term (2-4 years) |

| Micro-Hospital Formats for Children | +0.3% | Emerging markets in APAC, Latin America, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Routine Pediatric-Immunization Funding Momentum

Record sums are flowing into childhood immunization schedules. GAVI allocated USD 9 billion for 2024-2025 to subsidize HPV, pneumococcal conjugate, and rotavirus vaccines, assuring manufacturers of multi-year demand[1]GAVI The Vaccine Alliance, “2024-2025 Investment Opportunity,” gavi.org . In the United States, the Vaccines for Children program distributed 84 million doses in 2024, 6% above 2023 volumes, as catch-up campaigns recaptured pandemic-era defaulters. Guaranteed procurement compresses time-to-market for combination vaccines, yet the infectious-disease focus crowds out research on adolescent-specific shots for non-communicable threats. Manufacturers now aim to bundle multiple antigens to maximize throughput on established filling lines, a strategy that also reduces cold-chain burden. Still, divergent political attitudes toward mandates in some regions limit the penetration of newly recommended vaccines.

Gene-Therapy Approvals for Rare Pediatric Diseases

Five pediatric gene therapies were approved in 2024-2025, each priced above USD 2 million per patient, shifting conversations from dose-based billing to milestone-based contracts. Surrogate endpoints, such as enzyme activity, enable earlier launches, enticing venture capital into next-generation vectors. Accelerated pathways shave 18-24 months off development cycles, but questions remain on durability and equitable rollout in middle-income markets that lack long-term monitoring infrastructure. Hospitals must upgrade virology suites to handle on-site reconstitution, and payers are layering annuity payments over five years to hedge therapeutic uncertainty. The Pediatric healthcare market is poised to absorb more one-time curative modalities as manufacturing yields climb.

AI-Assisted Pediatric Radiology Adoption

Twelve pediatric-tailored AI tools cleared by the FDA between 2024 and 2025 now triage neonatal hemorrhage, scoliosis, and chest infections. Early adopters report 30-40% faster turnaround times, letting general radiologists flag urgent cases before subspecialist review. Algorithmic bias remains a hurdle because training images skew toward older children in high-income geographies. Regulators have begun requiring real-world performance audits, which could slow procurement but will standardize quality baselines. Vendors are partnering with children’s hospitals in underrepresented regions to diversify datasets, aiming to lift accuracy for neonates and minority populations.

Re-Emergence of RSV and Other Respiratory Outbreaks

RSV hospitalizations dipped by 43% in locales that deployed monoclonal prophylaxis, yet the pathogen surged overall as pandemic immunity debt exposed new birth cohorts. The WHO’s 2024 endorsement of maternal RSV vaccination introduces dual-prophylaxis choices, maternal shots plus infant antibodies, confusing payers on cost-effectiveness. The bifurcated approach splits the Pediatric healthcare market between vaccine and biologic suppliers, each lobbying ministries for preferential placement on formularies. Rapid antigen tests are selling briskly because clinicians want respiratory differentiation at the bedside instead of waiting for central labs. Device makers are bundling RSV, influenza, and COVID-19 assays into single cartridges to streamline triage in emergency departments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Antimicrobial Resistance in Children | -0.6% | Global, highest in South Asia and Sub-Saharan Africa | Long term (≥ 4 years) |

| Gap in Pediatric-Specific Device Reimbursement | -0.4% | United States, fragmented in EU and emerging markets | Medium term (2-4 years) |

| Dearth of Long-Term Safety Data for mRNA Vaccines | -0.3% | Global, heightened scrutiny in EU | Medium term (2-4 years) |

| Shortage of Pediatric Subspecialists in Low-Income Regions | -0.7% | Sub-Saharan Africa, South Asia, rural Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Antimicrobial Resistance in Children

Antimicrobial resistance killed 1.14 million children under five in 2024, with South Asia and Sub-Saharan Africa reporting resistance above 50% for third-generation cephalosporins[2]World Health Organization, “Global Antimicrobial Resistance Surveillance,” who.int. Clinicians escalate to carbapenems as first-line therapy, quickening the march toward pan-resistant strains. Pediatric antibiotic pipelines stay thin because short courses and stewardship rules limit commercial returns. Multilateral donors now fund “pull” incentives, yet uptake remains slow. Without rapid diagnostics, physicians still prescribe empirically, compounding selection pressure.

Shortage of Pediatric Subspecialists in Low-Income Regions

China logged 0.6 pediatricians per 1,000 children in 2025, below the 1.0 benchmark, while many African countries reported fewer than 0.1 pediatric cardiologists per million children[3]National Health Commission of China, “Pediatric Healthcare Development Plan 2024-2029,” nhc.gov.cn. Brain drain to urban or foreign posts erodes already thin rosters. Telehealth only partly fills the gap because broadband remains patchy outside metro cores. Training consortia are expanding fellowship seats, but mentorship shortages hamper skill transfer. The constraint also limits enrollment in clinical trials, slowing the generation of evidence on region-specific disease burdens.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vaccines Lead, Digital Tools Accelerate

Vaccines accounted for 38.55% of 2025 revenue, anchoring the Pediatric healthcare market through stable procurement tied to national schedules. The Pediatric healthcare market size for digital health solutions is projected to advance at a 5.25% CAGR, the fastest among categories, as payers accept that remote monitoring curbs costly admissions. Pharmaceutical revenues grow modestly because biosimilar erosion offsets gains from orphan drugs. Device makers benefit from miniaturization, translating adult inventions into child-sized form factors that drive adherence. Services revenue spans inpatient care, outpatient consults, and expanding home health visits, optimized by virtual check-ins.

Digital platforms embed AI to flag deteriorating vitals, allowing clinicians to intervene before crises. FDA clearance of Canvas Dx for early autism screening showed regulators’ willingness to back algorithmic assessments[4]U.S. Food and Drug Administration, “Device Approvals 2024-2025,” fda.gov. Vaccines for emerging pathogens will deliver incremental gains, but finite schedules cap upside. Manufacturers respond with multivalent formulations that free clinic slots and attract bundled tenders. Overall, the Pediatric healthcare market continues to balance preventive biologics with technology-enabled chronic-care management.

By Therapeutic Area: Infectious Diseases Dominate, Oncology Surges

Infectious diseases comprised 33.53% of therapeutic spending in 2025, driven by respiratory and vaccine-preventable illnesses. Oncology is on track for a 4.75% CAGR through 2031, driven by CAR-T therapies and earlier tumor detection enabled by expanded newborn screening. Respiratory disorders benefit from monoclonals that extend dosing intervals, while neurological portfolios grow as gene therapies target intractable epilepsies. Cardiovascular interventions shift toward catheter-based repairs, reducing hospital days.

The Pediatric healthcare market for oncology will expand as more solid-tumor cell therapies, such as afamitresgene autoleucel, reach adolescents. Yet capacity constraints for apheresis and cytokine-management beds could bottleneck penetration. Infectious-disease allocations may fall marginally as RSV prophylaxis dampens hospital costs, but persistent funding for routine vaccines keeps the category atop spending tables.

By Age Group: School-Age Children Largest, Adolescents Fastest

School-age children (2–11 years) generated 42.15% of 2025 revenue, reflecting frequent well-child visits and high vaccine uptake. Adolescents (12–18 years) will record the fastest growth at a 4.82% CAGR, driven by digital therapeutics for mental health and HPV vaccine catch-ups. Neonates represent a smaller slice but command higher per-patient spend due to intensive-care technology.

The Pediatric healthcare market share for adolescents will rise as school-based telehealth normalizes behavioral screenings. Meanwhile, advances in non-invasive ventilation and phototherapy boost neonatal outcomes, though reimbursement lags in lower-income systems. Tailoring product design to age-specific ergonomics remains an R&D priority.

By Care Setting: Hospitals Anchor, Telehealth Expands

Hospitals accounted for 54.65% of 2025 revenue because they are the only providers of surgery, ICU, and advanced imaging. Telehealth will climb at a 6.32% CAGR, propelled by extended reimbursement through December 2025 and growing clinician comfort with asynchronous consults. Clinics consolidate to negotiate better payer rates and invest in interoperable records.

The Pediatric healthcare market size in home care is rising as payers quantify savings from early discharge, supplemented by remote monitoring. Licensing barriers across state lines still restrict platform scale, but interstate compacts are under discussion. Hospitals respond by creating virtual wards, protecting revenue as inpatient days decline.

By End User: Public Providers Lead, Private Sector Gains

Public entities accounted for 58.55% of 2025 spending, underpinned by insurance schemes such as Medicaid and the NHS. Private operators will outpace at a 5.22% CAGR as families pay for shorter queues and novel diagnostics. Private equity’s USD 4.2 billion bet on pediatric urgent-care centers underscores confidence in cash-pay niches.

Innovation often debuts in private settings, then trickles to public systems once cost curves fall. This diffusion lag risks widening outcome disparities, prompting policymakers to pilot voucher schemes that let public patients access private facilities for high-priority services. The Pediatric healthcare industry thus faces a balancing act between entrepreneurial agility and universal access.

Geography Analysis

North America accounted for 35.23% of global revenue in 2025, driven by high per-capita outlays and a dense network of children’s hospitals. Value-based contracts are nudging providers toward preventive interventions that curb emergency utilization. The Pediatric healthcare market in the region is expected to grow steadily as gene therapies debut at flagship centers, though payer scrutiny of million-dollar price tags intensifies.

Asia-Pacific will record a 6.12% CAGR to 2031 as China and India expand pediatrician pipelines and upgrade county-level hospitals. Middle-class demand for premium care sparks joint ventures with multinational device makers that localize production to sidestep tariffs. In Southeast Asia, micro-insurers bundle telehealth consults with wellness apps, widening access among gig-economy workers.

Europe enjoys universal coverage but faces stalling birth rates in Germany and Italy, tempering volume growth. Still, EU funds are modernizing neonatal ICUs in Eastern states, narrowing East-West equipment gaps. In the Middle East, Gulf states allocate hydrocarbon windfalls to pediatric care hubs to attract medical tourism. Africa’s fragmented infrastructure limits reach, yet pilot drone networks now ferry vaccines to remote clinics, inching coverage upward.

Competitive Landscape

The pediatric healthcare market is moderately fragmented, with pharma majors, device giants, regional hospital chains, and digital startups vying for share. Multinationals pursue vertical integration, snapping up telehealth portals and home-health agencies to secure downstream revenues. Device manufacturers miniaturize adult platforms; Abbott’s FreeStyle Libre gained pediatric clearance for children as young as two, expanding the continuous glucose monitoring segment.

Startups leverage AI to democratize subspecialist insight, attracting licensing deals from incumbent imaging firms. Hospital groups pilot micro-hospitals to plant flags in fast-growing suburbs, offering emergency care minus tertiary overhead. Reimbursement for pediatric-specific devices remains patchy, so vendors lobby for dedicated payment codes. Overall, competition hinges on who can bundle diagnostics, therapeutics, and virtual support into seamless journeys that satisfy both payers and families.

Pediatric Healthcare Industry Leaders

Johnson & Johnson

GSK plc

Merck & Co., Inc.

Sanofi S.A

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The FDA approved Zycubo (copper histidinate) injection, the first treatment for Menkes disease in pediatric patients.

- October 2025: Arcutis Biotherapeutics received FDA clearance for ZORYVE cream 0.05% to treat mild-to-moderate atopic dermatitis in children aged 2-5 years.

Global Pediatric Healthcare Market Report Scope

As per the scope of this report, pediatric healthcare is a branch of medicine that deals with the medical care, development, and related diseases of infants, children, and adolescents. The pediatric healthcare market grows significantly as children often suffer from gastrointestinal, allergic, respiratory, and other chronic diseases owing to their lower immunity.

The pediatric healthcare market is segmented by product type, therapeutic area, age group, care setting, end user, and geography. By product type, the market is segmented into pharmaceuticals, vaccines, medical devices, and digital health solutions. By therapeutic area, the market is segmented into infectious diseases, respiratory disorders, neurological disorders, cardiovascular disorders, oncology, and gastrointestinal disorders. By age group, the market is segmented into neonates (0–28 days), infants (1–23 months), children (2–11 years), and adolescents (12–18 years). By care setting, the market is segmented into hospitals, clinics, home care, and telehealth. By end user, the market is segmented into public healthcare providers and private healthcare providers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Pharmaceuticals |

| Vaccines |

| Medical Devices |

| Digital Health Solutions |

| Infectious Diseases |

| Respiratory Disorders |

| Neurological Disorders |

| Cardiovascular Disorders |

| Oncology |

| Gastro-intestinal Disorders |

| Neonates (0–28 days) |

| Infants (1–23 months) |

| Children (2–11 years) |

| Adolescents (12–18 years) |

| Hospitals |

| Clinics |

| Homecare |

| Telehealth |

| Public Healthcare Providers |

| Private Healthcare Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Pharmaceuticals | |

| Vaccines | ||

| Medical Devices | ||

| Digital Health Solutions | ||

| By Therapeutic Area | Infectious Diseases | |

| Respiratory Disorders | ||

| Neurological Disorders | ||

| Cardiovascular Disorders | ||

| Oncology | ||

| Gastro-intestinal Disorders | ||

| By Age Group | Neonates (0–28 days) | |

| Infants (1–23 months) | ||

| Children (2–11 years) | ||

| Adolescents (12–18 years) | ||

| By Care Setting | Hospitals | |

| Clinics | ||

| Homecare | ||

| Telehealth | ||

| By End User | Public Healthcare Providers | |

| Private Healthcare Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the Pediatric healthcare market in 2031?

It is projected to reach USD 19.90 billion by 2031.

Which product category is expanding the fastest?

Digital health solutions are advancing at a 5.25% CAGR through 2031.

Which region will show the quickest growth?

Asia-Pacific is expected to grow at a 6.12% CAGR on the back of policy drives to boost pediatrician ratios and hospital capacity.

How large is the vaccines segment today?

Vaccines captured 38.55% of 2025 global revenue.

Why is telehealth important for pediatric care?

Permanent reimbursement parity and asynchronous platforms enable cost-efficient specialist access, supporting a 6.32% CAGR for telehealth revenue.

Page last updated on: