Market Overview

| Study Period | 2020 - 2031 |

|---|---|

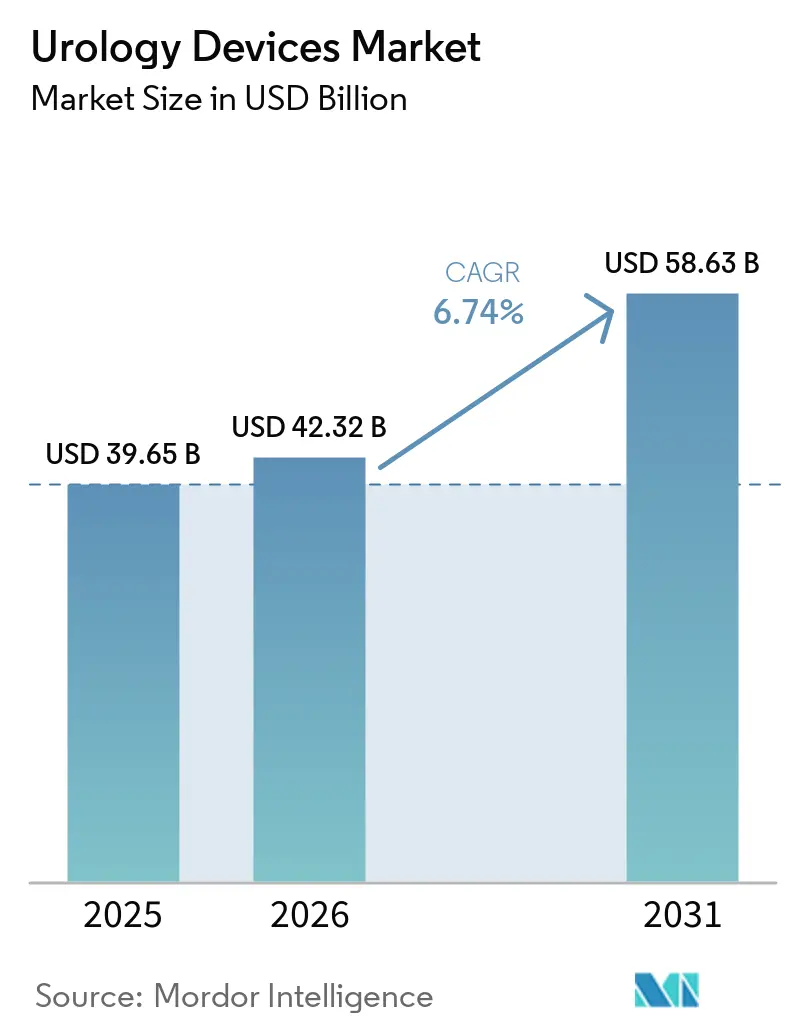

| Market Size (2026) | USD 42.32 Billion |

| Market Size (2031) | USD 58.63 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

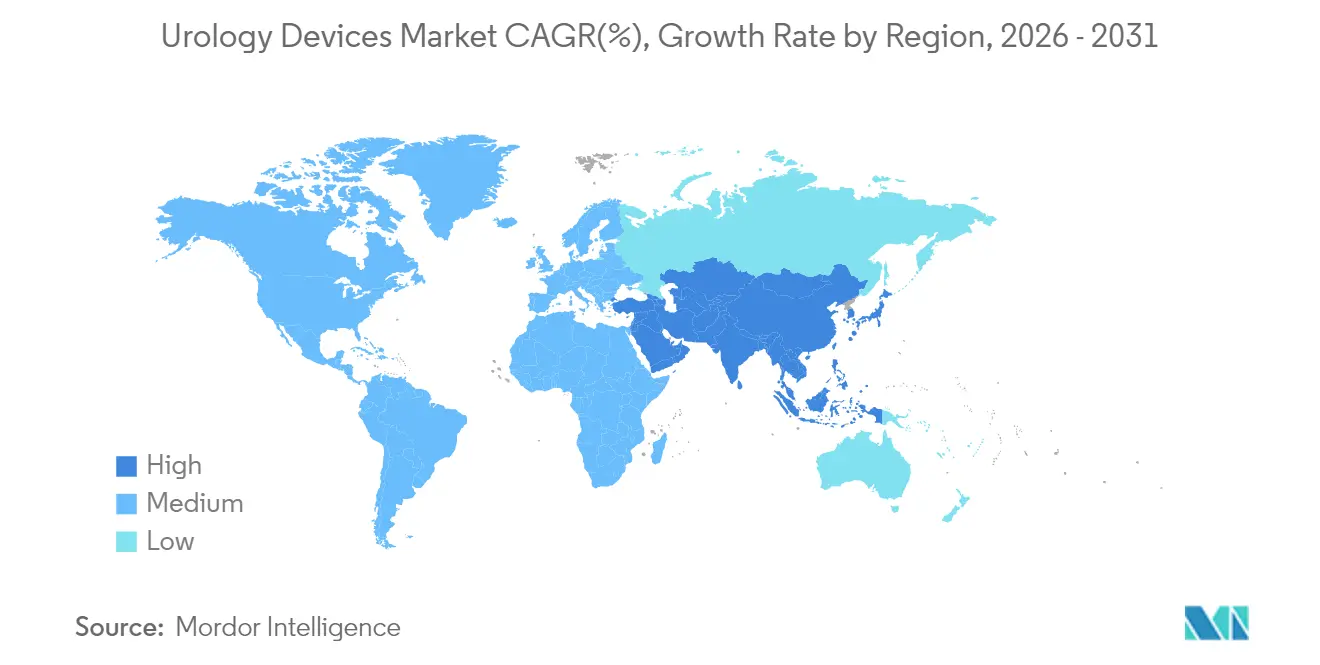

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urology Devices Market Analysis by Mordor Intelligence

The Urology Devices Market size is projected to be USD 39.65 billion in 2025, USD 42.32 billion in 2026, and reach USD 58.63 billion by 2031, growing at a CAGR of 6.74% from 2026 to 2031.

Rising life expectancy is enlarging the patient base for urological disorders, while minimally invasive and robotic technologies shorten recovery times and lift procedure volumes. Home-based dialysis and self-catheterization are migrating treatments away from hospitals, and single-use devices are lowering infection risks that once constrained outpatient growth. Robotics, thulium fiber lasers, and AI-guided imaging systems justify premium pricing, and regulatory agencies in the United States and Europe are accelerating approvals for breakthrough platforms such as burst wave lithotripsy and AI-assisted robotic systems. Against this backdrop, the urology devices market continues to draw investment even as venture funding in broader med-tech contracts.

Key Report Takeaways

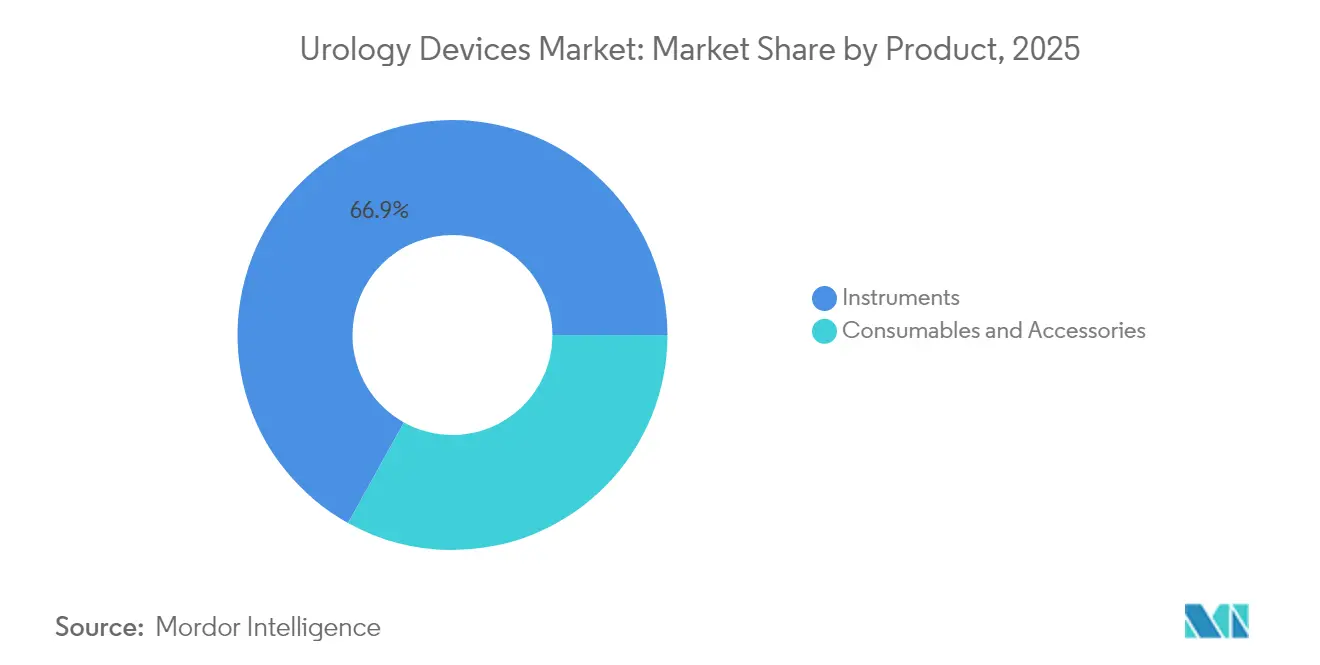

- By product category, instruments captured 66.92% revenue share in 2025; consumables and accessories are advancing at an 8.27% CAGR through 2031.

- By technology, minimally invasive surgery devices held 45.71% of the urology devices market share in 2025, while robotic urologic surgery systems are projected to expand at a 10.31% CAGR to 2031.

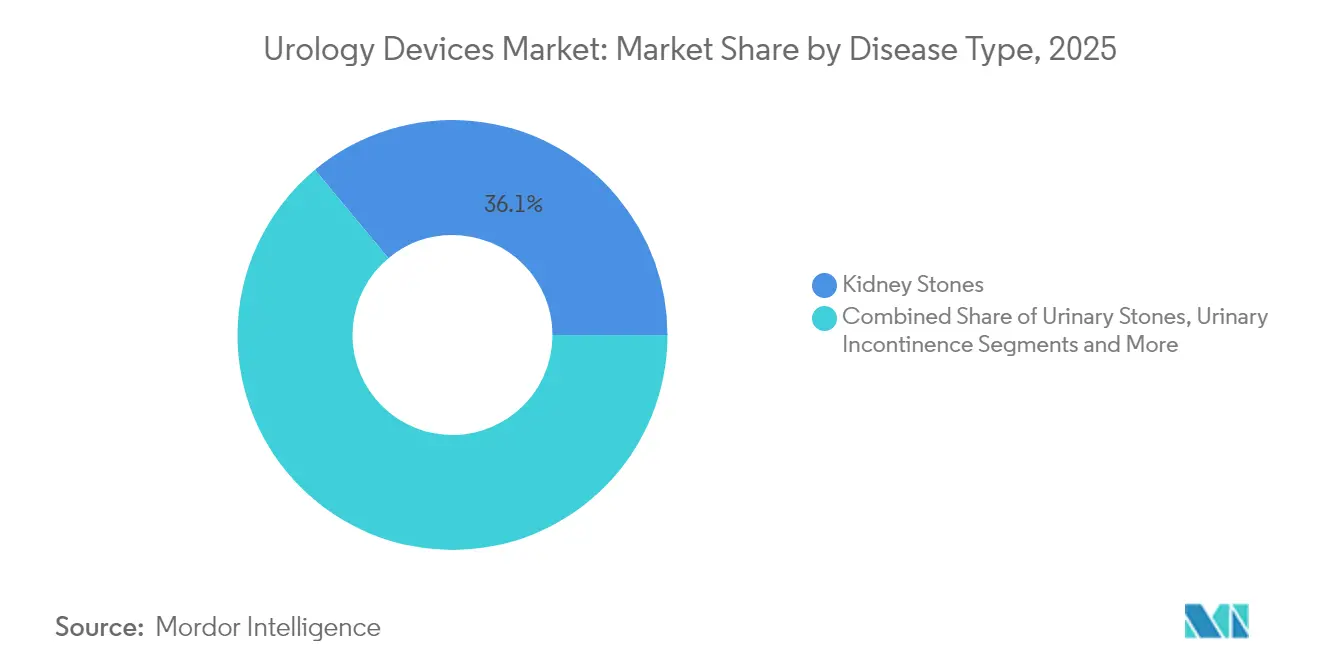

- By disease, kidney-stone management accounted for 36.05% of the urology devices market size in 2025, whereas urinary incontinence solutions are forecast to grow at an 8.38% CAGR.

- By end user, hospitals and clinics commanded 67.98% share of the urology devices market size in 2025, yet ambulatory surgical centers exhibit the fastest growth at an 8.44% CAGR through 2031.

- By geography, North America led with 38.76% urology devices market share in 2025; Asia-Pacific is the fastest-growing region at a 8.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Urology Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High incidence of urologic conditions | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Rising geriatric population | +1.1% | Global | Long term (≥ 4 years) |

| Technological advancements in minimally invasive and robotic surgery | +1.5% | North America, Europe, APAC | Medium term (2-4 years) |

| Preference for single-use endoscopes and catheters | +0.9% | Global | Short term (≤ 2 years) |

| AI-enabled imaging and navigation improving procedural throughput | +1.0% | North America, Europe, APAC | Medium term (2-4 years) |

| Home-based dialysis and self-catheterization enabled by tele-urology | +0.8% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Incidence of Urologic Conditions

Kidney stones affect about 40 million men in the United States, underpinning sustained demand for lithotripsy devices and disposable ureteroscopes. Benign prostatic hyperplasia eventually impacts 8 of every 10 men, broadening the addressable base for minimally invasive treatments. Urinary incontinence afflicts roughly 30 million adults, fueling uptake of neuromodulation implants. Because these conditions require repeated or lifelong interventions, they provide recurring revenue streams that stabilize the urology devices market throughout economic cycles.

Rising Geriatric Population

Longer life expectancy is boosting the share of older adults who often present with multifactorial urological issues. Health-system planners are reallocating procedure volumes from inpatient wards to ambulatory settings in order to manage cost pressures while accommodating elderly patients’ need for shorter stays . Manufacturers respond by designing devices that suit frail physiology and support at-home monitoring, reinforcing the long-run expansion of the urology devices market.

Technological Advancements in Minimally Invasive and Robotic Surgery

Robotic systems such as Medtronic’s Hugo platform delivered a 98.5% surgical success rate in the Expand URO trial, illustrating performance gains that are persuading payers to authorize premium reimbursements. Thulium fiber lasers shorten lithotripsy times by 20%, and AI modules embedded in consoles assist with real-time tissue recognition. As a result, hospitals buy new capital equipment even in flat budget cycles, lifting the urology devices market.

Preference for Single-Use Endoscopes and Catheters

Single-use ureteroscopes from Cook Medical eliminate reprocessing costs and lower cross-infection risk, factors that accelerated adoption during and after COVID-19 insideindianabusiness.com. Economic models that account for labor, sterilization, and litigation increasingly show net savings, enabling outpatient centers to keep procedure prices competitive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global approval and post-market surveillance requirements | −0.8% | Global | Long term (≥ 4 years) |

| High capital and procedure costs of advanced systems | −0.6% | Global | Medium term (2-4 years) |

| Sustainability pressure on single-use plastics and PFAS coatings | −0.5% | Europe, global spillover | Medium term (2-4 years) |

| Shortage of trained urology surgeons and nurses in emerging markets | −0.4% | APAC, Latin America, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Approval and Post-Market Surveillance Requirements

The FDA’s forthcoming Quality System Regulation amendments align with ISO 13485 but force manufacturers to retrofit documentation and audit practices, raising compliance costs.[1]Federal Register, “Medical Devices; Quality System Regulation Amendments,” federalregister.gov Post-market surveillance under 21 CFR Part 822 demands long-horizon follow-up studies, a burden that weighs heaviest on small innovators.[2]U.S. Food and Drug Administration, “21 CFR Part 822—Postmarket Surveillance,” FDA, ecfr.gov Similar toughened regimes from ANVISA and the EU delay launches and reduce the pace at which the urology devices market can absorb new entrants.

High Capital and Procedure Costs of Advanced Systems

Robotic suites, advanced lasers, and AI workstations require seven-figure capital budgets plus maintenance contracts. Smaller hospitals in Latin America and Southeast Asia must often rely on refurbished units or financing programs, slowing penetration during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Instruments Lead While Consumables Accelerate

Instruments account for 66.92% of the urology devices market in 2025 because robotic systems, dialysis machines, and thulium lasers require sizable upfront purchases. Consumables and accessories are growing at an 8.27% CAGR as single-use ureteroscopes and catheters create predictable reorder cycles. Endoscopic visualization towers, lithotripters, and urodynamic carts anchor capital budgets, but revenue predictability now tilts toward disposables that match every case. The instruments subcategory remains pivotal when facilities pursue high-complexity surgeries that demand integrated imaging and navigation. Dialysis consoles like Fresenius 5008X, cleared to deliver high-volume hemodiafiltration, illustrate how incremental upgrades sustain replacement demand. On the consumables side, biodegradable ureteral stents and antimicrobial coatings are differentiating brands without adding reprocessing burdens.

In this context, the urology devices market size for consumables is on track to carve a larger revenue slice, especially in regions where cost-per-procedure transparency drives buyer preference. Instruments will keep dominating absolute value, but their growth rate will trail that of accessories because budget committees lengthen approval cycles for large capital outlays. Facilities that own older holmium YAG lasers increasingly redeploy them to lower-acuity cases while allocating fresh capital to thulium platforms, reinforcing a barbell spending pattern inside the urology devices market.

By Technology: Robotics Surge While AI Integration Accelerates

Minimally invasive surgery devices held 45.71% share of the urology devices market size in 2025, yet robotic systems are producing the steepest curve at a 10.31% CAGR. New entrants such as Medtronic’s Hugo are broadening customer choice beyond Intuitive Surgical and, by offering modular components, lowering adoption thresholds. AI modules layer computer vision onto optics, translating video feeds into actionable prompts that help shorten learning curves. Burst wave lithotripsy, delivered via compact ultrasound emitters, is further expanding the non-invasive toolkit and may cannibalize traditional shock-wave systems over the next decade.

Looking ahead, additive manufacturing is enabling patient-specific implants such as biodegradable ureteral stents with controlled elution profiles. Integration between imaging AI and robotic arms is expected to automate sub-steps like calyx entry during percutaneous nephrolithotomy, refining efficiency benchmarks. The convergence of these modalities should deepen overall penetration and protect pricing power across the urology devices market.

By Disease: Kidney Stones Dominate While Incontinence Accelerates

Kidney-stone interventions represented 36.05% of disease-linked revenue in 2025, reflecting high recurrence rates that necessitate repeat lithotripsy or ureteroscopy. Innovations such as portable burst wave lithotripsy increase treatment accessibility by eliminating anesthesia, which may further widen case volumes. Urinary incontinence is the fastest-growing segment at an 8.38% CAGR, buoyed by favorable clinical data for miniaturized neuromodulation implants and growing patient willingness to seek care.

Benign prostatic hyperplasia remains a large installed base for surgical and device therapies, now augmented by an AMA CPT Category I code for Aquablation that becomes effective in 2026. Urological cancers are moving toward focal therapy under AI-assisted imaging guidance, while pelvic organ prolapse benefits from lighter mesh constructs that aim to balance tensile strength with biocompatibility. Together, these shifts diversify revenue channels inside the urology devices market.

By End-User: Hospitals Dominate While ASCs Gain Ground

Hospitals and clinics held 67.98% of global revenue in 2025 because they host complex reconstructive and oncologic cases that rely on comprehensive support services. Ambulatory surgical centers are expanding fastest at an 8.44% CAGR thanks to lower overhead structures that align with payer preferences for site-neutral reimbursement. Diagnostic cystoscopy volumes in ASCs have climbed steadily as infection-control protocols favor settings with streamlined workflows.

Home-care environments constitute an emerging frontier as portable dialysis and self-catheterization kits gain regulatory support. Dialysis chains are also piloting hub-and-spoke tele-monitoring to balance staffing constraints with patchy rural access. As clinical responsibilities diffuse, the urology devices market will spread revenue across a wider set of care settings.

Geography Analysis

North America preserved 38.76% global share in 2025 due to robust reimbursement, rapid regulatory pathways, and a well-entrenched installed base of robotic platforms. The FDA’s Breakthrough Device Program expedites access for technologies such as burst wave lithotripsy, allowing early revenue capture that feeds back into R&D budgets. The United States is also reallocating routine diagnostics into ambulatory venues, giving manufacturers new channels to place compact endoscopy towers. Canada and Mexico generate incremental growth through cross-border purchasing agreements that standardize device specifications and shorten procurement cycles.

Asia-Pacific is the fastest climber with a 8.86% CAGR through 2031. Aging populations in China, Japan, and South Korea expand procedure demand while public-sector reforms unlock capital budgets for advanced lasers and imaging. Olympus chose South Korea to launch next-generation BPH devices, a sign that multinational firms view the region as a proving ground for premium technologies. Venture financing pullbacks have lowered valuations, which may spur consolidation that helps well-capitalized incumbents accumulate regional footprints.

Europe is a mature but policy-driven market in which environmental legislation can reshape material choices overnight. The anticipated PFAS prohibition challenges suppliers of ePTFE-based catheters and vascular grafts, prompting accelerated research into fluorine-free coatings. Germany, France, and Italy remain demand anchors, yet hospitals here are steeply discounting high-volume consumables, pushing vendors to extract margin from value-added services. South America holds pockets of growth led by Brazil, where ANVISA’s e-labeling push may lower localization costs, easing compliance for exporters. The Middle East invests heavily in specialist hospitals while many African states prioritize low-cost dialysis and catheterization solutions, presenting tiered opportunities for the urology devices market.

Competitive Landscape

The urology devices market is moderately fragmented, with technology differentiation eclipsing scale as the main source of competitive edge. Boston Scientific’s USD 3.7 billion Axonics acquisition extends its sacral neuromodulation footprint and underscores how larger conglomerates buy their way into high-growth niches. Stryker’s USD 4.9 billion bid for Inari Medical illustrates similar logic in peripheral vascular cross-fertilization, broadening solution portfolios for overlapping surgeon customers.

Robotic surgery remains a focal battleground. Intuitive Surgical still commands a dominant installed base, yet Medtronic leverages hospital-wide purchasing relationships to seed its Hugo systems, often bundling them with energy devices and staplers. PROCEPT BioRobotics differentiates through water-jet tissue ablation and AI-directed planning, offering outcome data that resonates with value-based procurement teams. Consumables players contend on infection control and ergonomic design; Cook Medical’s single-use ureteroscope and Teleflex’s UroLift 2 exemplify fast-cycle updates that help retain accounts.

Strategic partnerships with software specialists supply computer-vision and machine-learning layers that hardware vendors cannot easily build in-house. Hospitals increasingly request interoperability, prompting vendors to publish open APIs. In parallel, sustainability pledges press companies to redesign packaging, which is gradually becoming a purchase criterion alongside price and performance inside the urology devices market.

Urology Devices Industry Leaders

Baxter International Inc.

Boston Scientific Corporation

Becton, Dickinson and Company

Olympus Corporation

Fresenius Medical Care AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Avvio Medical treated its first patients with a non-invasive kidney-stone therapy that could shift fragmentation procedures to outpatient clinics.

- April 2025: Medtronic reported 98.5% success in its Expand URO trial, supporting broader rollout of the Hugo robotic-assisted surgery system

- February 2025: .Neuspera’s ultra-mini neuromodulation implant met gold-standard endpoints for incontinence therapy, validating miniature leadless formats.

- December 2024: Teleflex released the UroLift 2 System with Advanced Tissue Control, expanding BPH indications to prostates up to 100 g.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the urology devices market as all capital equipment and single-use accessories that diagnose, treat, or monitor disorders of the urinary tract and the male reproductive system. Devices embraced in the model include dialysis machines, endoscopes and cameras, laser or shock-wave lithotripters, urodynamic testers, robotic surgery consoles, catheters, stents, and other purpose-built consumables.

Scope exclusion: Pharmaceuticals, general surgical disposables, and nephrology-only implants sit outside this assessment.

Segmentation Overview

- By Product

- Instruments

- Dialysis Devices

- Endoscopes & Endovision Systems

- Lasers & Lithotripsy Devices

- Robotic Surgical Systems

- Urodynamic Systems

- Imaging & Navigation Devices

- Bladder Management Devices

- Other Instruments

- Consumables & Accessories

- Dialysis Consumables

- Guidewires & Urinary Catheters

- Stents (Ureteral & Urethral)

- Biopsy Devices

- Disposable Ureteroscopes

- Continence Care Products

- Other Consumables & Accessories

- Instruments

- By Technology

- Minimally-Invasive Surgery Devices

- Robotic Urologic Surgery Systems

- AI-enabled Imaging & Navigation

- 3-D Printed & Patient-specific Implants

- Other Emerging Technologies

- By Disease

- Kidney Diseases

- Urological Cancer & BPH

- Urinary Stones (Urolithiasis)

- Pelvic Organ Prolapse

- Urinary Incontinence

- Other Diseases

- By End-User

- Hospitals & Clinics

- Dialysis Centres

- Ambulatory Surgical Centres

- Home-care Settings

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing urologists, biomedical engineers, procurement managers, and regional distributors across North America, Europe, and Asia-Pacific. The discussions validated typical replacement cycles, price corridors, and procedure mix trends that secondary data alone could not clarify.

Desk Research

We began with open datasets from authorities such as the WHO, FDA MAUDE, Eurostat, UN Comtrade, and the National Kidney Foundation, then layered in hospital utilization figures released by the American Urological Association and EAU guidelines. Trade association yearbooks, company 10-Ks, and recent patent filings accessed through Questel furnished technology diffusion clues. To size corporate revenues, we referenced D&B Hoovers and cross-checked news flow on Dow Jones Factiva. These sources, although representative, are not exhaustive; many additional publications informed our desk work.

Market-Sizing & Forecasting

A top-down model converts national procedure volumes, dialysis enrolments, and stone-surgery counts into device demand pools, which are then reconciled with sampled ASP × volume roll-ups from selected suppliers to fine-tune totals. Key variables like kidney failure prevalence, urolithiasis incidence, aging population growth, elective procedure recovery, and regulatory approvals drive both the base year and the outlook. Multivariate regression, informed by our expert panel's consensus on hospital capital budgets and unit ASP glide paths, underpins the 2025-2030 forecast. Where bottom-up estimates under-represent low-income markets, proportional trade data fills the gap.

Data Validation & Update Cycle

Before release, model outputs face anomaly checks against import values, insurer claim trends, and peer literature. Any variance beyond preset bands triggers re-contact with sources. Reports refresh every twelve months, with interim updates when material events, such as major recalls or guideline shifts, occur.

Why Mordor's Urology Devices Baseline Commands Reliability

Published estimates often diverge because analysts choose different product baskets, price anchors, and refresh cadences. Our disciplined scope selection and dual-path modeling help clients rely on one coherent baseline.

Key gap drivers include whether consumables are counted, if nephrology-only hardware is folded in, the currency year chosen, and how far primary validation goes before numbers are frozen.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 39.65 B (2025) | Mordor Intelligence | |

| USD 17.61 B (2025) | Regional Consultancy A | Excludes consumables and home-dialysis disposables; limited Asia-Pacific coverage |

| USD 36.8 B (2024) | Global Consultancy B | Includes nephrology capital goods, older base year, static currency conversion |

| USD 39.03 B (2025) | Trade Journal C | Relies on single top-down pass with minimal primary interviews |

The comparison shows that figures swing when scope or validation depth shifts. By pairing transparent assumptions with continuous field feedback, Mordor Intelligence delivers a balanced, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the urology devices market?

The urology devices market stands at USD 42.32 billion in 2026 and is projected to reach USD 58.63 billion by 2031.

Which product category holds the largest share?

Instruments such as robotic systems and dialysis machines captured 66.92% revenue share in 2025.

Which region is growing the fastest?

Asia-Pacific is expanding at a 8.86% CAGR through 2031 due to aging populations and rising healthcare investments.

Why are single-use devices gaining popularity?

They reduce infection risk and eliminate sterilization costs, making them attractive for ambulatory centers.

What technology is propelling growth in surgical procedures?

Robotic surgery platforms combined with AI-guided imaging are driving a 10.31% CAGR in the robotic segment.

How are environmental regulations affecting device materials?

An impending European ban on PFAS compounds is prompting manufacturers to seek fluorine-free alternatives for catheters and grafts.

Page last updated on: