BeLux (Belgium And Luxembourg) Courier, Express, And Parcel (CEP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

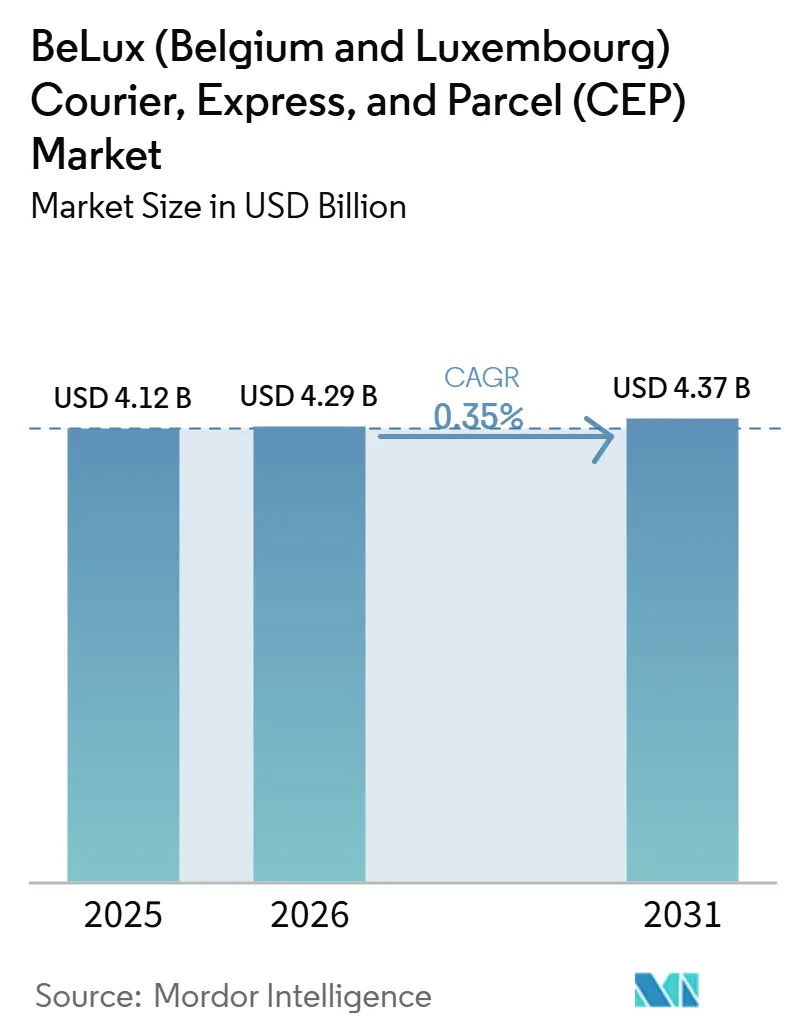

| Base Year Market Size (2025) | USD 4.12 Billion |

| Market Size (2026) | USD 4.29 Billion |

| Market Size (2031) | USD 4.37 Billion |

| Growth Rate (2026 - 2031) | 0.35% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

BeLux (Belgium And Luxembourg) Courier, Express, And Parcel (CEP) Market Analysis by Mordor Intelligence

The BeLux courier, express, and parcel (CEP) market size was valued at USD 4.12 billion in 2025 and is expected to increase to USD 4.29 billion in 2026 and reach USD 4.37 billion by 2031, growing at a 0.35% CAGR from 2026 to 2031.

The near-flat growth trajectory reflects a mature landscape where incremental volume gains from cross-border e-commerce and ultrafast grocery delivery barely offset mounting cost headwinds tied to congestion charges, carbon pricing, and persistent driver shortages. Intensifying regulatory pressure around fleet emissions in Brussels and Antwerp is compressing margins, forcing operators to modernize vehicles and invest in automated depots that sustain service reliability without price hikes that consumers resist. Consolidation among parcel locker providers and pharmacy-grade cold-chain specialists is reshaping competitive rules, while digital customs platforms reduce clearance times and establish next-day standards for sub EUR 50 (USD 57) cross-border parcels. Modal diversification toward rail and air is gathering pace as carbon costs bite, yet road continues to shoulder more than half of all volumes, demonstrating the entrenched role of highways inside the BeLux courier express parcel market.

Key Report Takeaways

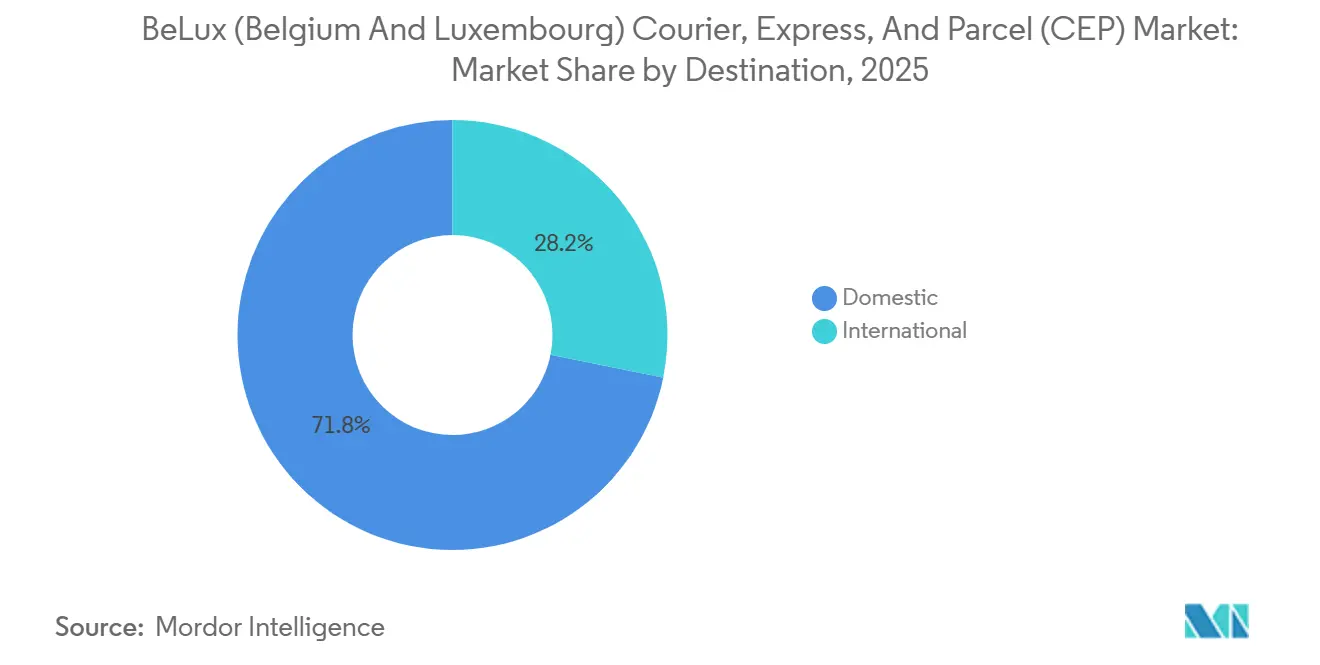

- By destination, domestic flows kept a 71.83% of the BeLux courier, express, and parcel (CEP) market share in 2025; international parcels are projected to expand at a 5.97% CAGR through 2031, the fastest among all destination types.

- By business model, the B2C segment led with 57.5% of the BeLux courier, express, and parcel (CEP) market share in 2025, whereas C2C is forecast to post the highest CAGR at 7.64% between 2026 and 2031.

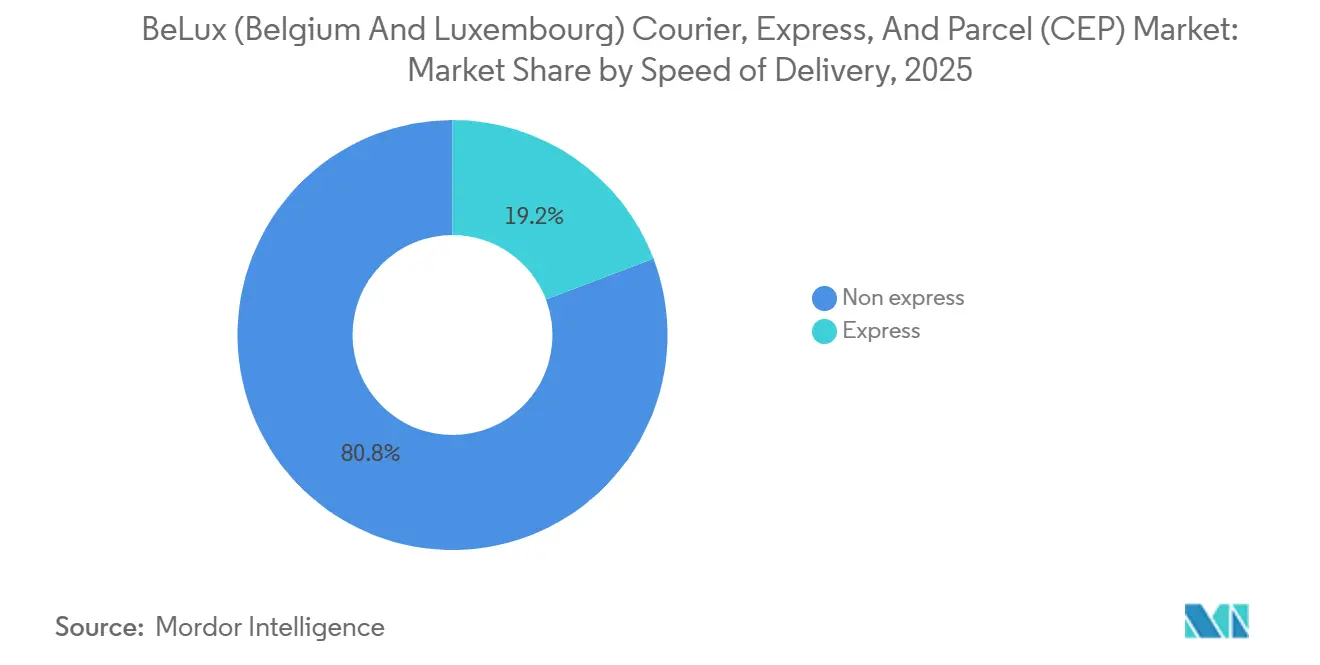

- By speed of delivery, non-express services captured 80.78% of the BeLux courier, express, and parcel (CEP) market size in 2025, and express services are advancing at a 6.1% CAGR through 2031.

- By country, Belgium held 86.84% of regional revenue in 2025, while Luxembourg is set to grow at 6.03% CAGR over 2026-2031.

- By shipment weight, light-weight shipments captured 72.17% of the BeLux courier, express, and parcel (CEP) market size in 2025, and medium shipments are advancing at a 5.72% CAGR through 2031.

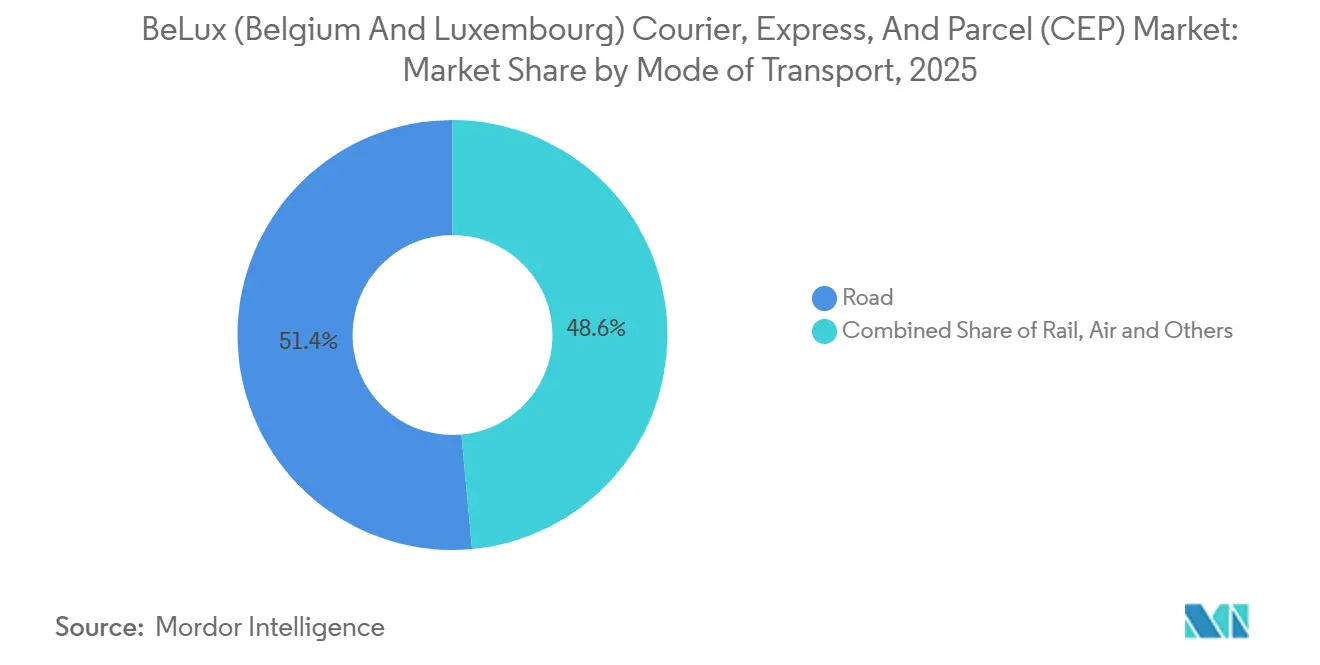

- By mode of transport, road captured 51.44% of the BeLux courier, express, and parcel (CEP) market size in 2025, and air is advancing at a 5.2% CAGR through 2031.

- By end-user industry, e-commerce captured 44.57% of the BeLux courier, express, and parcel (CEP) market size in 2025, and healthcare is advancing at a 5.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

BeLux (Belgium And Luxembourg) Courier, Express, And Parcel (CEP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-border e-commerce under EU VAT One-Stop-Shop | +0.6% | Belgium & Luxembourg | Medium term (2-4 years) |

| Ultrafast ≤2 h grocery delivery micro-hubs | +0.5% | Brussels, Antwerp, Ghent | Short term (≤2 years) |

| Liege–Findel dual-gateway air corridor | +0.4% | Wallonia & Luxembourg | Long term (≥4 years) |

| Corporate fleet electrification pledges | +0.3% | Belgium & Luxembourg | Long term (≥4 years) |

| Digital customs and smart lockers | +0.5% | Urban e-commerce hubs | Medium term (2-4 years) |

| Pharma cold-chain demand from Wallonia | +0.2% | Wallonia & Luxembourg | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acceleration of Cross-Border E-Commerce Under the VAT One-Stop-Shop

Simplified VAT registration lets Belgian and Luxembourg sellers serve all 27 EU states through a single filing portal, eliminating compliance costs that previously deterred exports. International parcel volumes are therefore set to rise at 5.97% CAGR, far eclipsing domestic growth. Clearance times have dropped to hours thanks to the Import Control System 2, unlocking next-day delivery economics for low-value items. Luxembourg’s hosting of major fulfillment hubs such as Amazon further amplifies outbound flows, while SMEs leverage marketplaces to reach pan-EU buyers without setting up foreign entities. The BeLux courier express parcel market benefits from the premium service levels and customs-cleared options these merchants require.

Rise of Ultrafast ≤2 h Grocery Delivery

Operators like Getir and Flink operate more than 40 micro-fulfillment sites across Brussels, stocking 2,000-3,000 SKUs and dispatching e-bikes for emission-free drops. Order density above 50 orders/km² and baskets topping EUR 25 (USD 29) underpin viable unit economics in dense urban cores. Consolidation evidenced by Gorillas’ 2025 sale to Getir signals a pivot toward scale. Restocking those dark stores generates B2B parcel demand, giving road carriers fresh revenue pockets. Ultrafast fulfillment, therefore, stimulates medium-weight parcel growth inside the BeLux courier express parcel market while accelerating locker use for returns[1]Luxembourg Ministry of Mobility and Public Works, “Sustainable Urban Logistics Strategy,” mmtp.public.lu.

Luxembourg Findel & Liege Airport Dual-Gateway

Findel handled 1.04 million tons of freight in 2024, while Liege moved 1.05 million tons, and a 90-minute truck run connects the two. Integrators exploit this corridor to marry Findel’s long-haul freighters with Liège’s European express sort. Pharmaceutical exporters in Wallonia gain GDP-compliant connectivity to Asia within 48 h, safeguarding cold-chain integrity. Upcoming high-speed rail links will further shorten corridor lead times. This synergy lifts Air’s 5.2% CAGR outlook and positions the BeLux courier express parcel market as a gateway for temperature-sensitive flows.

Corporate Sustainability Targets and Fleet Electrification

Tax breaks now waive company-car levies on zero-emission vans, propelling electric fleet penetration to 18% of commercial vehicles in 2025. bpost aims for fully electric urban delivery by 2030, while DHL will deploy 80,000 e-vans regionwide. With fuel representing a quarter of the cost per stop, parity in total cost of ownership arrives once daily mileage stays under 150 km. On-site solar and EIB-financed chargers slash energy bills, turning sustainability into a procurement differentiator across the BeLux courier express parcel market[2]Brussels Environment, “Low Emission Zone (LEZ),” environnement. brussels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brussels & Antwerp congestion charges | -0.8% | Belgium | Short term (≤2 years) |

| Driver shortage & rigid labor rules | -0.6% | Belgium & Luxembourg | Medium term (2-4 years) |

| Air-slot scarcity at Findel peak season | -0.5% | Luxembourg | Short term (≤2 years) |

| EU Fit for 55 carbon pricing on diesel | -0.4% | Belgium & Luxembourg | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Urban Congestion-Charging Zones in Brussels & Antwerp Inflating Last-Mile Costs

Brussels’ 2025 Low Emission Zone (EUR 35 (USD 41)/day for non-Euro 6 diesel) and Antwerp’s 2027 congestion charges (EUR 8-12 (USD 9.4-14.1)) are driving up last-mile delivery costs, especially for small operators. Large integrators like DHL and UPS benefit from scale and electrification plans. Fragmented regional rules complicate compliance, while hub-and-spoke models with electric vehicles raise handling costs. E-commerce pricing pressures prevent passing charges to customers, squeezing margins.

Chronic Driver Shortage Amid Aging Workforce and Rigid Labor Regulations

Belgium faces a chronic driver shortage, with 15,000 vacancies in 2025 and 40%+ annual turnover, driven by an aging workforce (median age 48) and low appeal to younger workers. Rigid labor rules raise costs by 25-30% and limit scheduling flexibility. Urban delivery roles are physically demanding, while rural areas have limited candidates. Cross-border competition, such as Luxembourg, pushes wages 15-20% higher. Operators invest in automation, but last-mile delivery remains labor-intensive, constraining growth and limiting low-margin e-commerce expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Destination: International Pace Outstrips Domestic Saturation

By destination, domestic flows held 71.83% of the BeLux courier, express, and parcel (CEP) market share in 2025, while international parcels are set to grow fastest, at a 5.97% CAGR through 2031. Although domestic shipments remain the volume backbone, they face congestion charges and rising labor costs.

Operators investing in bilingual tracking, EU-wide returns, and locker networks reduce cross-border friction and protect customer loyalty. Competitive advantage hinges on customs expertise, with EU-compliant firms commanding up to 30% per-parcel premiums. Road-rail intermodal pilots on the Brussels-Luxembourg corridor may unlock subsidies, making international niches a growing driver of strategic capex across the BeLux courier express parcel market.

By Business Model: Peer-to-Peer Upsurge

By business model, the B2C segment led with 57.5% of the BeLux courier, express, and parcel (CEP) market share in 2025, while C2C is set to grow fastest, posting a 7.64% CAGR from 2026 to 2031. C2C already accounts for 1 in 5 parcels and is expected to nearly double by 2031 as resale apps like Vinted drive circular consumption.

Locker networks reduce privacy concerns, and in-app shipping fees of EUR 3-4 are widely accepted. If locker density rises, C2C’s BeLux courier express parcel market share could increase significantly. B2C remains the largest revenue contributor, though free shipping pressures squeeze margins. B2B volumes decline as digital invoicing reduces document courier needs, pushing operators toward pharmaceuticals, groceries, and high-value reverse logistics. Diversification becomes essential for survival.

By Speed of delivery: Express vs. Non-Express Delivery Trends in BeLux

By speed of delivery, non-express services captured 80.78% of the BeLux courier, express, and parcel (CEP) market size in 2025, while express services are expanding fastest, with a 6.1% CAGR through 2031. Non-express volumes dominate due to cost-sensitive e-commerce, but rising consumer demand for faster delivery is driving express adoption. Operators are investing in route optimization, urban micro-hubs, and same-day fulfillment to capture premium segments, balancing speed with profitability across the BeLux courier express parcel market.

Express growth is fueled by B2B time-sensitive shipments and high-value e-commerce, where customers are willing to pay premiums. Last-mile congestion and labor costs challenge scalability, prompting pilot programs for electric and cargo-bike fleets. Cross-border express flows also benefit from customs simplification, making international express a key strategic focus.

By Shipment Weight: Light vs. Medium Parcels

By shipment weight, light-weight shipments captured 72.17% of the BeLux courier, express, and parcel (CEP) market size in 2025, while medium shipments are growing fastest, with a 5.72% CAGR through 2031.

Light-weight parcels dominate due to e-commerce volumes, but medium shipments, including bulk B2B and multi-item orders, are driving growth. Operators are optimizing packaging, consolidating loads, and deploying specialized vehicles to handle medium parcels efficiently. This shift influences network design, warehouse layouts, and pricing strategies across the BeLux courier express parcel market.

By Mode of Transport: Road vs. Air Parcels

By mode of transport, road captured 51.44% of the BeLux courier, express, and parcel (CEP) market size in 2025, while air shipments are growing fastest, with a 5.2% CAGR through 2031. Road transport dominates due to cost efficiency and dense domestic networks, but air is expanding for time-sensitive and high-value parcels. Operators are investing in intermodal solutions, express air corridors, and hub optimization to balance speed, cost, and sustainability.

Cross-border e-commerce and international B2B shipments are driving air parcel growth, particularly for high-margin express services. Environmental regulations and rising fuel costs are prompting carriers to explore greener air and road fleet options, making multimodal strategies increasingly central to competitiveness across the BeLux courier express parcel market.

By End-User Industry: E-Commerce vs. Healthcare

By end-user industry, e-commerce captured 44.57% of the BeLux courier, express, and parcel (CEP) market size in 2025, while healthcare is growing fastest, with a 5.62% CAGR through 2031. E-commerce dominates due to high consumer parcel volumes, but healthcare shipments, including pharmaceuticals, medical devices, and cold-chain products, are driving growth.

Operators are investing in temperature-controlled logistics, specialized packaging, and compliance solutions to meet strict regulatory requirements. Rising demand for reliable healthcare deliveries and high-value B2B shipments is shaping network design, service offerings, and strategic investments across the BeLux courier express parcel market.

Geography Analysis

Belgium drives over 86.84% of the BeLux courier, express, and parcel (CEP) market, leveraging Antwerp’s seaport, Brussels’ EU institutions, and dense urban demand. Yet the medium growth reflects saturation and heavier regulation. Pharma exports and expanding parcel locker grids still create premium niches, while federal road taxes challenge small haulers.

Luxembourg is set to experience a robust 6.03% CAGR. This growth is fueled by affluent consumers, the presence of major headquarters, and the prominence of Findel in air cargo. Additionally, government-backed digital customs initiatives and enhanced rail connections are propelling Luxembourg's rise.

Regional harmonization under Luxembourg’s 2025 Benelux presidency could slash paperwork across borders, fostering a more unified BeLux courier express parcel market that rewards carriers boasting pan-Benelux capabilities[3]Luxembourg Government, “Luxembourg Presidency of the Benelux Union 2025,” mae.gouvernement.lu .

Competitive Landscape

Tier-one incumbents bpost and POST Luxembourg anchor domestic distribution through universal-service mandates but grapple with legacy labor costs. Global integrators DHL, UPS, and FedEx focus on time-definite, cross-border, and cold-chain niches where scale and certifications justify premiums. Technology disruptors led by InPost target OOH delivery; its locker network processed 20% more volumes in 2024, eroding incumbents’ doorstep differentiation.

Strategic moves include UPS’s 2025 cold-chain acquisitions and DHL’s electric-van roll-outs, both signaling bets on healthcare and sustainability. Asset-light brokers test AI route-planning to squeeze further costs. Reverse-logistics specialists emerge as returns hit 30% in apparel.

M&A potential remains high: mid-tier road haulers lacking capital to electrify become acquisition targets for integrators chasing density inside the BeLux courier express parcel market. The top five firms control roughly 62% of revenue, indicating moderate concentration but freedom for niche entrants[4]UPS, “UPS Completes Acquisitions of Healthcare Cold-Chain Logistics Providers,” investors.ups.com.

BeLux (Belgium And Luxembourg) Courier, Express, And Parcel (CEP) Industry Leaders

DPDgroup / Geopost

UPS

Post Luxembourg

Bpost Group

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: POST Luxembourg entered a referral agreement with ING Luxembourg, likely tied to customer and financial services.

- March 2025: POST Luxembourg rebranded Michel Greco to Inflow, investing EUR 15 million (USD 17 million) in Bettembourg automation.

- February 2025: bpost committed to doubling its locker estate to 2,500+ units by year-end, citing 44% locker-volume growth in 2024.

- January 2025: United Parcel Service (UPS) completed the acquisition of European healthcare cold chain logistics specialists Frigo Trans and BPL, enhancing temperature controlled logistics across Europe.

BeLux (Belgium And Luxembourg) Courier, Express, And Parcel (CEP) Market Report Scope

| Domestic |

| International |

| Express |

| Non-Express |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

| Air |

| Road |

| Others |

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| Belgium |

| Luxembourg |

| Destination | Domestic |

| International | |

| Speed of Delivery | Express |

| Non-Express | |

| Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Consumer-to-Consumer (C2C) | |

| Shipment Weight | Heavy Weight Shipments |

| Light Weight Shipments | |

| Medium Weight Shipments | |

| Mode of Transport | Air |

| Road | |

| Others | |

| End-User Industry | E-Commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others | |

| Country | Belgium |

| Luxembourg |

Key Questions Answered in the Report

How large will parcel revenue become across Belgium and Luxembourg by 2031?

The BeLux courier express parcel market size is forecast to reach USD 4.37 billion by 2031, reflecting 0.35% CAGR over 2026-2031.

Which segment is expanding fastest?

International cross-border parcels are projected to rise at a 5.97% CAGR, the quickest among all destination categories

Why is locker delivery critical in BeLux?

Lockers cut failed deliveries by 35%, lower reverse-logistics costs by up to 60%, and underpin C2C’s 7.64% CAGR growth trajectory.

What role does pharma play in regional volumes?

Healthcare parcels grow 5.62% CAGR, leveraging Wallonia’s vaccine and biologic export base that requires GDP-compliant cold-chain

How will carbon pricing affect carriers?

Fit for 55 will raise diesel costs 8-12%, pressuring road-based margins and accelerating investment in electric fleets and rail alternatives.

Which airports anchor express air freight?

Luxembourg Findel and Belgium’s Liège combine as a dual-gateway handling more than 2 million t of cargo annually, fueling a 5.2% CAGR in air shipments.

Page last updated on: