Bed And Breakfast Accommodation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

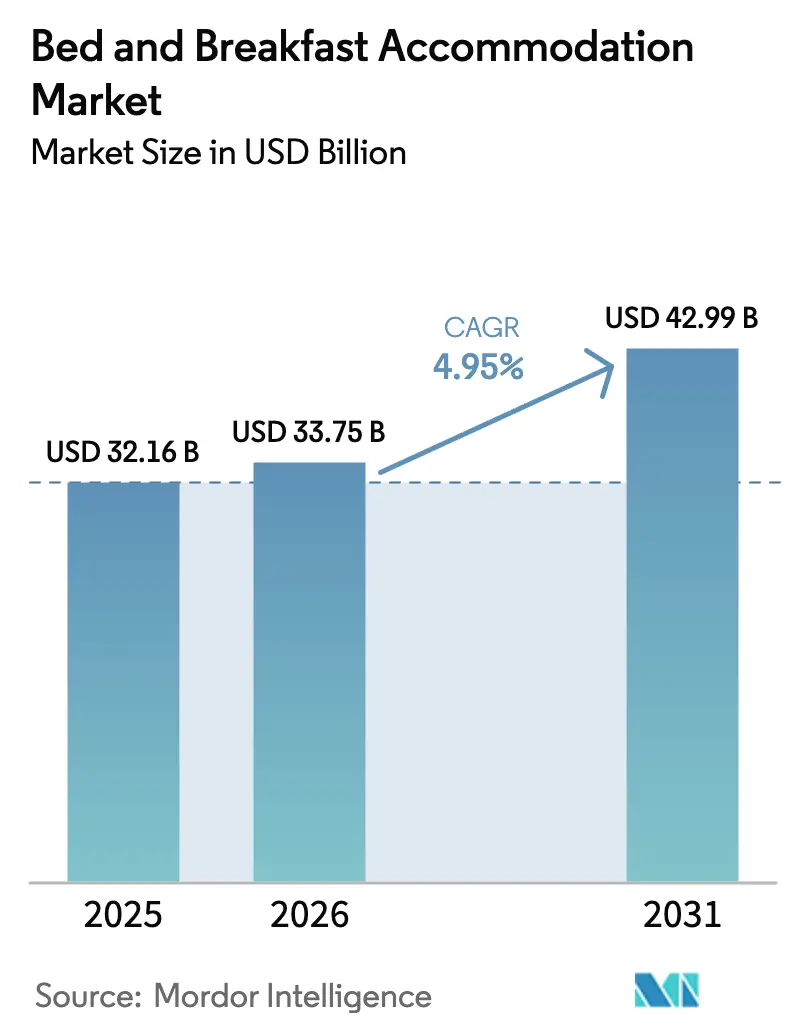

| Market Size (2026) | USD 33.75 Billion |

| Market Size (2031) | USD 42.99 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

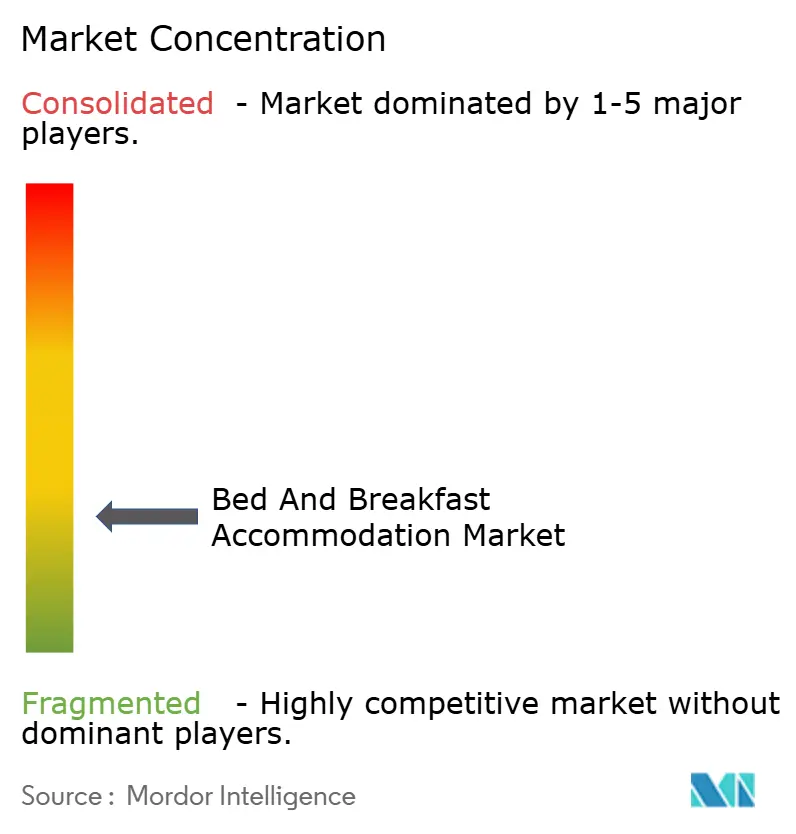

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bed And Breakfast Accommodation Market Analysis by Mordor Intelligence

The bed and breakfast market size was valued at USD 32.16 billion in 2025 and estimated to grow from USD 33.75 billion in 2026 to reach USD 42.99 billion by 2031, at a CAGR of 4.95% during the forecast period (2026-2031). A decisive shift toward authentic, small-scale lodging, coupled with digital booking innovations, shapes this expansion. Rural properties continue to capture growing domestic tourism flows, while boutique and heritage inns outperform generic lodging by leaning into experiential travel. Technology-enabled distribution platforms have reduced entry barriers for independent operators yet tightening short-term rental rules in urban centers underscore the need for agile compliance strategies. Ongoing labor shortages and climate-linked insurance costs remain the principal headwinds.

Key Report Takeaways

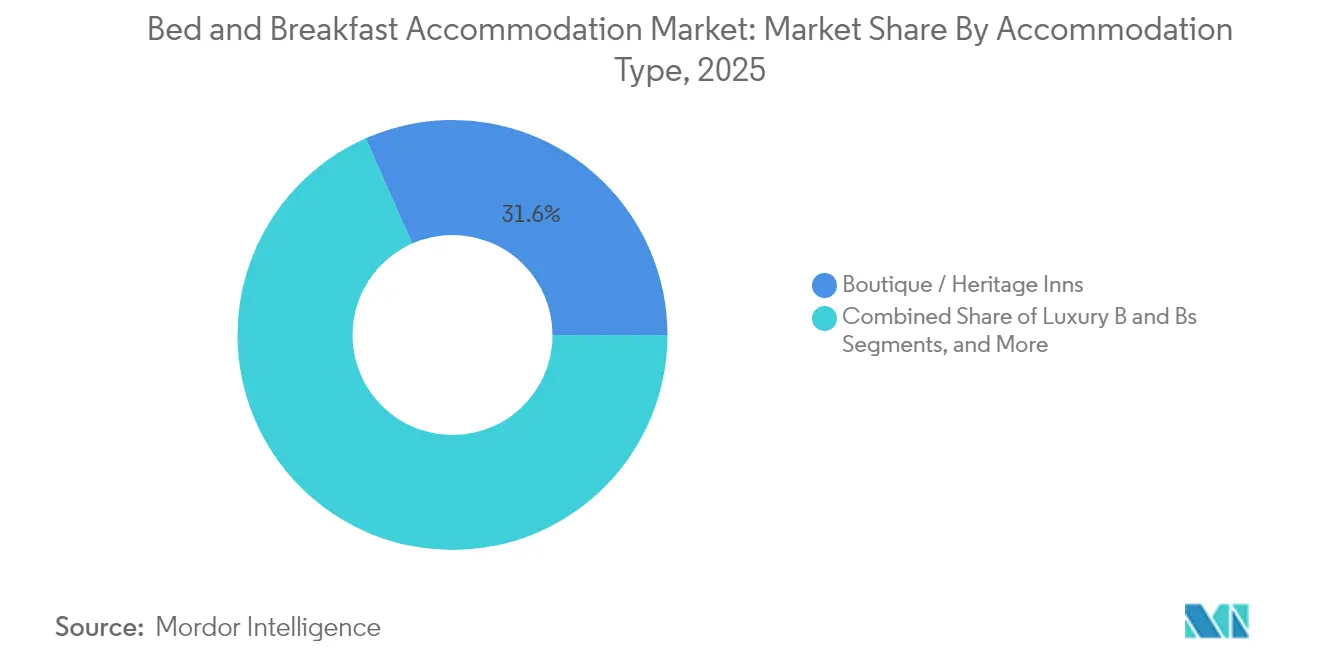

- By accommodation type, boutique and heritage inns led with 31.62% revenue of the bed and breakfast accommodation market share in 2025.

- By location setting, rural properties accounted for 42.98% of the bed and breakfast accommodation market share in 2025.

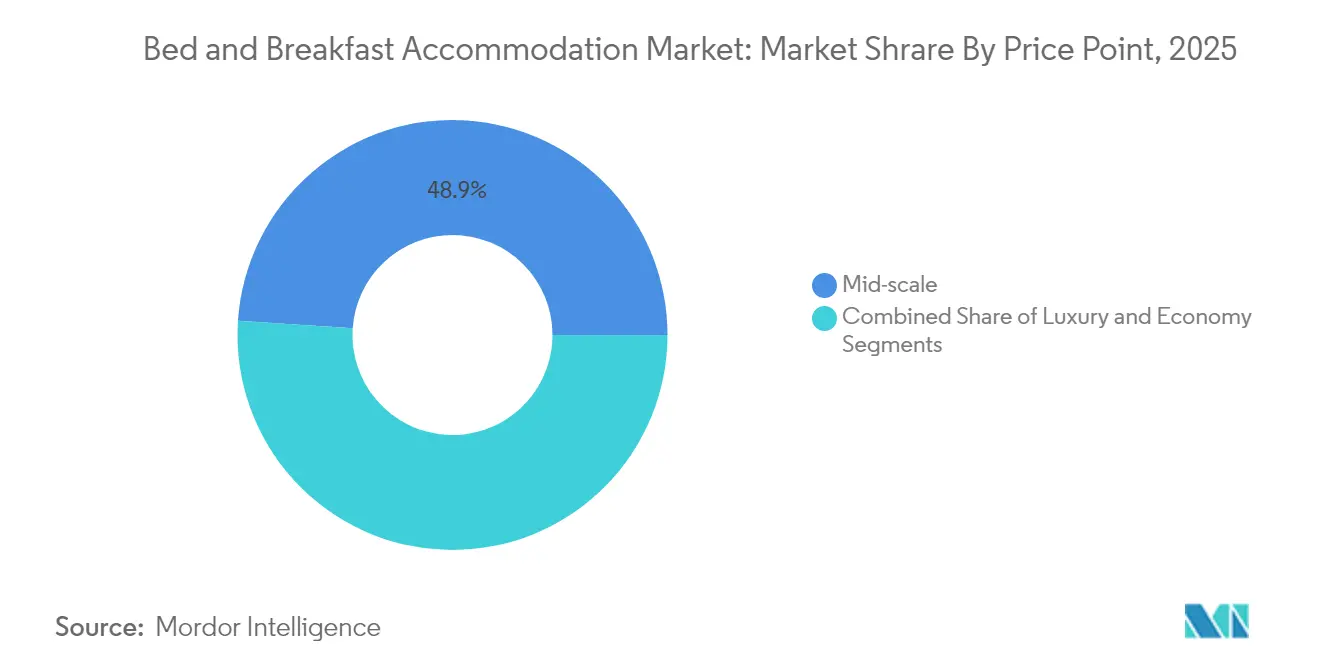

- By price point, the mid-scale segment contributed 48.94% of the bed and breakfast accommodation market size in 2025; luxury is projected to rise at 6.88% CAGR to 2031.

- By geography, North America held 43.15% of the bed and breakfast accommodation market share in 2025, whereas Asia-Pacific posts the fastest regional CAGR at 8.45% through 2031.

- The bed and breakfast market exhibits high fragmentation with the top 5 players, Airbnb, B&B HOTELS Group, OYO Hotels & Homes, Select Registry Distinguished Inns, and The Inn Collection Group, collectively holding modest market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bed And Breakfast Accommodation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for personalized experiential travel | +1.2% | Global, with premium impact in North America & Europe | Medium term (2-4 years) |

| Rapid expansion of online booking and OTA ecosystems | +0.9% | Global, accelerated in Asia-Pacific markets | Short term (≤ 2 years) |

| Surge in domestic short-stay tourism post-pandemic | +0.8% | North America, Europe, India core markets | Short term (≤ 2 years) |

| Rising disposable incomes of Millennials and Boomers | +0.7% | North America, Europe, emerging APAC markets | Long term (≥ 4 years) |

| Hybrid "work-cation" B&B packages for remote workers | +0.4% | North America, Europe, select urban-adjacent rural areas | Medium term (2-4 years) |

| Rural sustainability grants fueling community B&Bs | +0.2% | Europe, North America, Australia regional focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Personalized Experiential Travel

Travelers increasingly seek culturally rooted stays, and 54% of recent guests said local immersion now outweighs a property’s star classification. Bed and breakfasts embed themselves in neighborhood life by partnering with artisans, farmers, and guides to craft one-off activities ranging from foraging walks to pottery workshops. Average U.S. guests booked 4.7 on-site experiences in 2023, up sharply from pre-pandemic norms, signaling higher ancillary-revenue opportunities. Millennials, who represent a large outbound cohort in Europe, commonly choose alternative lodging over chain hotels, fueling premium rates for story-rich heritage inns. Rural operators are layering in wellness sessions such as forest-bathing and yoga, positioning themselves for the fast-growing health-and-nature segment.

Rapid Expansion of Online Booking and OTA Ecosystems

Digital platforms captured a dominant share of reservations in 2024, yet direct website conversions display the strongest momentum at 12.9% CAGR through 2030. Commission-sensitive hosts now combine OTA reach for first-time discovery with sustained guest lifecycle tactics via email, loyalty perks, and mobile apps. The cost to acquire a direct booking fell to 7.1% of room revenue in 2023 as programmatic advertising tools matured, whereas OTA fees linger between 15% and 30%. Embedded AI within search engines automates personalized trip bundling, helping small properties deliver friction-free booking journeys. Voice search and “book-on-Google” flows are expected to elevate direct volumes further in the near term.

Surge in Domestic Short-Stay Tourism Post-Pandemic

Border uncertainty redirected many leisure budgets toward local destinations. Domestic lodging nights rose in the double digits across numerous high-income economies during 2024, providing sustained demand that insulated rural B&Bs from foreign visitor volatility. India’s internal travel rebound has spurred record highway traffic and rail ticketing, translating into elevated mid-week occupancy in hill-station guesthouses. Similar momentum in China’s tier-two cities is lifting weekend-stay business for family-run courtyard inns. This urban-to-rural migration of leisure spend reduces currency risk for operators and aligns neatly with government programs that champion small-community tourism.

Rural Sustainability Grants Fueling Community B&Bs

Public funding in Europe, North America, and Australia channels fresh capital into historic barn conversions and eco-cabins, bringing new supply to sparsely populated areas [1] Source: HM Government, “Tourism Cooperation Grants,” gov.uk. . Qualifying owners secure low-interest loans for solar panels, grey-water systems, and heritage restoration, enabling them to meet rising guest expectations around responsible travel. These grants lower upfront costs and accelerate payback periods, encouraging clusters of community-run B&Bs that collectively market entire villages as single tourism propositions. The model strengthens local employment and diversifies rural economies while feeding the broader bed and breakfast market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening zoning and STR regulations | -0.8% | North America, Europe, Australia urban markets | Short term (≤ 2 years) |

| Intensifying competition from whole-home rentals | -0.6% | Global, concentrated in urban and resort areas | Medium term (2-4 years) |

| Escalating climate-linked insurance premiums | -0.3% | Global, severe impact in coastal and wildfire-prone regions | Medium term (2-4 years) |

| Rural labour shortages impacting service quality | -0.2% | North America, Europe, Australia rural tourism areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Zoning and STR Regulations

Provincial law in British Columbia restricts most urban short-term rentals to a principal residence, with significant fines for violators [2]Source: Government of British Columbia, “Short-Term Rental Accommodations Act,” gov.bc.ca. Scotland now mandates licenses for all hosts, and parts of France require annual energy audits for new listings. City caps on permissible rental nights further constrain inventory in Paris, Barcelona, and Amsterdam. Compliance costs—ranging from safety certifications to digital registration—hit independent hosts hardest because they lack dedicated legal staff. In rural districts, the same rules often prove less stringent, producing an unintended shift of supply toward countryside markets.

Intensifying Competition for Whole-Home Rentals

Professional management firms now operate large portfolios with revenue-optimization software, eroding the service gap that once favored host-occupied B&Bs. Cleaning fees and higher nightly rates have risen across the entire alternative-lodging spectrum, yet platforms such as Airbnb are broadening into add-on experiences, amplifying their competitive reach. In response, many B&B owners emphasize hosted interaction, heritage storytelling, and farm-to-table breakfasts to preserve differentiation. Airbnb's expansion into services and experiences through its 2025 platform redesign creates additional competitive pressure by offering comprehensive travel solutions that extend beyond accommodation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Accommodation Type: Heritage Properties Drive Premium Positioning

Boutique and heritage inns captured 31.62% revenue in 2025, giving them the largest share across accommodation styles. Their curated architecture and localized storytelling tap directly into travelers’ quest for memorable stays, a dynamic that keeps occupancy sturdy even during shoulder seasons. Within the bed and breakfast market, farm-stay and Agri-tourism venues register the quickest 9.22% CAGR, boosted by regional grants and consumer interest in food provenance. Luxury B&Bs, though niche, command high ADRs that fortify segment profitability during peak demand weekends. At the opposite end, economy units face margin compression from citywide yield wars against professional whole-home rentals.

Heritage hosts often integrate smart room controls and contactless check-ins while safeguarding historic character. This digital layer hastens guest satisfaction and raises review scores, protecting rate integrity. Agritourism sites in the European countryside leverage the bed and breakfast market size for rural tourism grants, reinforcing economic resilience. The segment’s evolution underscores the broader preference shift toward immersive lodging over standardized hotel chains.

By Booking Channel: Digital Transformation Accelerates Direct Engagement

Online travel agencies owned 70.82% of reservations in 2025, yet direct website sales mark the fastest expansion path at 12.3% CAGR through 2031. Improved SEO, loyalty discounts, and one-click mobile payments empower independents to recapture costly OTA traffic. Predictive pricing engines adjust room rates against real-time comp-set data, ensuring channel profitability. Legacy offline agents still cater to seniors booking complex itineraries, but their share diminishes annually.

The shift toward direct bookings is supported by artificial intelligence integration in marketing platforms, with Google's Performance Max campaigns enabling small B&B operators to optimize advertising spend across multiple channels effectively. Mobile app adoption accelerates direct booking growth, particularly among younger travelers who prefer seamless, personalized booking experiences that OTAs struggle to deliver for individual properties.

By Traveler Type: Remote Work Reshapes Accommodation Demand

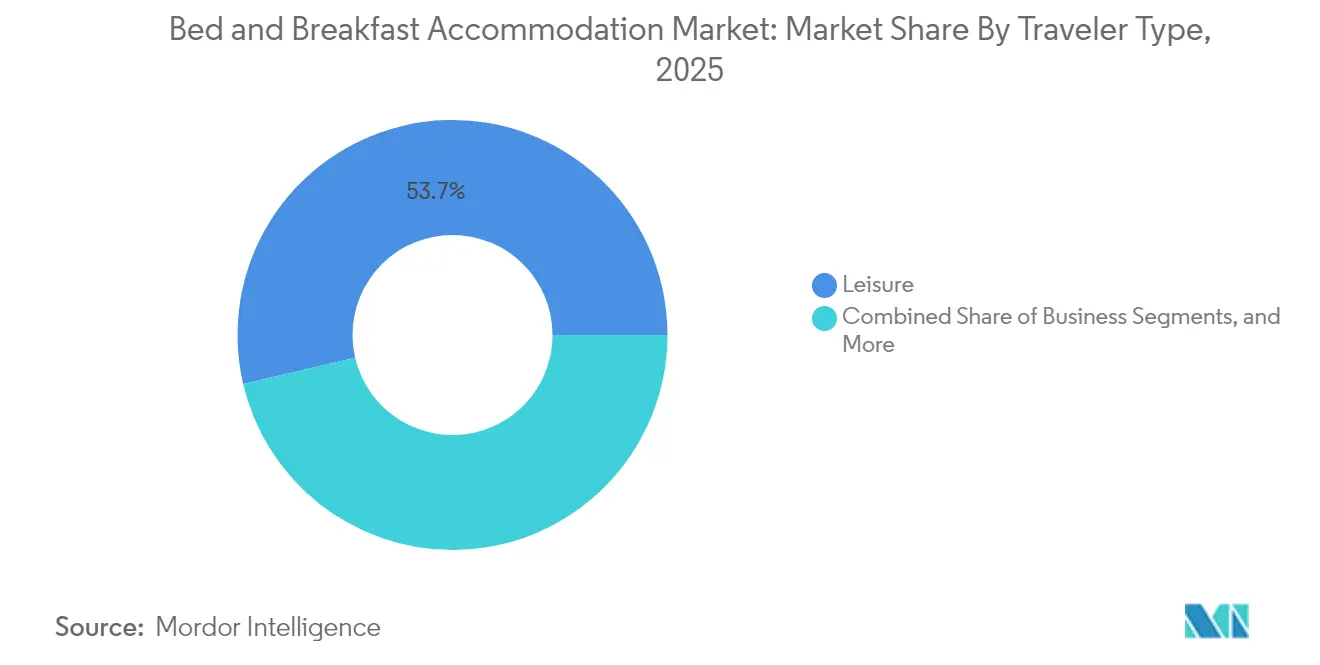

Leisure guests represented 53.65% of stays in 2025, yet the work-cation niche races ahead at 11.15% CAGR. Properties outfitted with fiber internet and sound-isolated corners report weekday occupancy surges that buffer seasonality. Business-only travel lags pre-2020 levels, but hybrid meetings now migrate to rural inns offering conference barns and evening bonfire socials. Solo travel upticks among Gen Z foster demand for communal kitchens and hosted group excursions.

Extended-stay patterns favor B&Bs' cost advantages over hotels, while the integration of work amenities such as high-speed internet, dedicated workspace areas, and flexible check-in/check-out policies creates competitive differentiation opportunities. Operators tailoring package bundles—combining coworking credits, guided hikes, and mindfulness sessions—see higher ancillary spend per booking. Such offerings place B&Bs at the heart of evolving digital-nomad ecosystems.

By Location Setting: Rural Dominance Reflects Sustainability Trends

Rural properties accounted for 42.98% of the bed and breakfast market share in 2025, and their growth trajectory sits at a robust 7.25% CAGR to 2031. Travelers seek open space, lower crowd density, and farm-fresh cuisine, attributes city stock cannot match. Coastal and island B&Bs achieve premium ADRs but remain highly seasonal, whereas heritage-town locations benefit from steady cultural tourism footfall.

Government tax relief for green renovation and digital connectivity upgrades accelerates rural inventory expansion. Carbon-conscious visitors favor countryside lodgings with verified low emissions, nudging urban hoteliers to adopt similar standards or risk share attrition. Broadband rollouts reduce remote-work friction, transforming once-isolated hamlets into viable year-round bases for mobile professionals.

By Price Point: Mid-Scale Segment Balances Value and Experience

Mid-scale B&Bs delivered 48.94% of global revenue in 2025, blending affordability with bespoke hosting. Their sweet-spot positioning attracts families during peak vacation windows and millennials on experiential road trips. Luxury properties, though smaller in count, anticipate 6.88% CAGR, underpinned by affluent boomers and well-healed digital entrepreneurs chasing exclusive settings.

The mid-scale segment's dominance reflects broader hospitality trends where travelers seek authentic experiences at accessible price points, particularly in domestic markets where value consciousness remains high despite increased travel spending. Luxury segment growth is supported by the wealth accumulation among millennials and baby boomers, who prioritize unique experiences over standardized luxury hotel offerings.

By Ownership Model: Independent Operators Maintain Market Leadership

Independents dominate supply, a reality rooted in the hyper-local nature of B&B hospitality. Yet franchise and soft-brand affiliations gain momentum where marketing muscle and cross-selling engines matter. Consortia provide light-touch shared services—central reservations, group promotions—while respecting each inn’s identity.

Technology partners now bridge capability gaps for solo hosts, offering yield management, AI chatbots, and bundled insurance. As these tools mature, the performance divide between branded and standalone properties narrows, preserving independence as the defining feature of the bed and breakfast industry across most regions. The emergence of technology platforms that provide independent operators with sophisticated marketing and management tools reduces traditional advantages of franchise models while preserving the authenticity that drives B&B demand.

Geography Analysis

North America retained 43.15% revenue share in 2025, buoyed by the United States’ USD 1 trillion domestic travel spend and Canada’s CAD 19.5 billion (USD 14.27 billion) accommodation turnover, up 14.7% year over year. Deep-rooted B&B culture in New England, the Pacific Northwest, and Atlantic Canada secures a stable guest pipeline, although urban zoning caps constrain new listings in cities such as New York and Vancouver. Mexico’s revitalized heritage towns supplement regional momentum by attracting cross-border leisure traffic.

Asia-Pacific posts the quickest 8.45% CAGR through 2031 on the back of India’s expanding middle class and China’s progressive reopening. Improved air links streamlined visa processes, and government-funded rural tourism corridors spark fresh supply in hill stations, tea estates, and coastal fishing villages. Australia’s state grants for agri-lodging conversion further draw investment to countryside estates. Varied regulations across jurisdictions require operators to fine-tune compliance strategies, yet the sheer scale of intra-regional travel propels steady occupancy gains.

Europe remains mature yet opportunity rich. Scotland’s licensing, France’s energy performance mandates, and Italy’s new national accommodation codes raise compliance expenses, which could trigger consolidation. EU sustainability goals and Common Agricultural Policy funds channel capital into farmhouse restorations and eco-ins. Intraregional weekend breaks and rail travel keep domestic nights high, supporting occupancy even as long-haul segments fluctuate. Rural Brittany, the Italian Alps, and Eastern European wine valleys illustrate pockets where experiential demand sustains healthy rate growth despite broader regulatory friction.

Competitive Landscape

The sector is markedly fragmented; Airbnb, B&B HOTELS Group, OYO Hotels & Homes, Select Registry Distinguished Inns, and The Inn Collection Group jointly control only a small slice of global revenues. Such diffusion allows nimble independents to thrive by highlighting uniqueness rather than brand uniformity. Technology has leveled the playing field, enabling single-property hosts to access channel managers, dynamic pricing, and AI-driven marketing once reserved for large chains.

Strategic thrusts center on portfolio diversification and digital direct-to-consumer funnels. OYO’s USD 525 million purchase of G6 Hospitality widened its economy footprint while Marriott’s USD 355 million CitizenM acquisition diversified its lifestyle offering [3]Source: Marriott International, “Marriott to Acquire CitizenM,” marriott.com. . Airbnb’s 2025 platform revamps now bundles services like catering and personal coaching, extending its customer lifetime value beyond lodging. Meanwhile, regional collectives leverage shared procurements to cut linen, amenity, and insurance costs.

High-growth adjacencies include work-cation-centric clusters, sustainability-certified farm stays, and blockchain-enabled loyalty exchanges. Mergers among third-party management groups, such as Pyramid Global’s tie-up with Axiom Hospitality, illustrate the race to scale operational synergies. Looking forward to data-rich revenue management, embedded fintech for trip financing, and dynamic packaging APIs from suppliers like Expedia will further reshape competitive contours.

Bed And Breakfast Accommodation Industry Leaders

Airbnb, Inc.

B&B HOTELS Group

OYO Hotels & Homes

Select Registry Distinguished Inns

The Inn Collection Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Airbnb unveiled a redesigned app and new services business covering 260 cities to expand revenue beyond lodging.

- April 2025: Marriott International agreed to acquire CitizenM for USD 355 million, with a potential USD 110 million earn-outs tied to growth.

- April 2025: Accor entered exclusive talks to buy 17 management agreements from Royal Holiday Group for USD 79 million.

- December 2024: OYO completed its USD 525 million acquisition of G6 Hospitality, adding roughly 1,500 franchised U.S. and Canadian hotels.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the bed-and-breakfast accommodation market as all licensed or legally hosted properties offering fewer than twenty guest rooms where the nightly rate includes breakfast prepared on-site and served in a shared or private dining area. Properties listed on online travel agencies (OTAs) or home-sharing platforms are counted only when they meet this definition.

Scope exclusion: whole-home vacation rentals, hostels, and large boutique hotels are left out to preserve comparability.

Segmentation Overview

- By Accommodation Type

- Luxury BandBs

- Boutique / Heritage Inns

- Farm-stay and Agri-tourism BandBs

- Budget / Economy BandBs

- By Price Point

- Luxury

- Mid-scale

- Economy

- By Traveller Type

- Leisure

- Business

- Bleisure / Work-cation

- Solo

- By Booking Channel

- Online Travel Agencies (OTAs)

- Direct Website / Mobile

- Offline Travel Agents

- By Location Setting

- Urban

- Suburban

- Rural

- Coastal / Island

- Heritage / Historic Towns

- By Ownership Model

- Independent

- Franchise / Affiliated

- Cooperative / Consortium

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with owners across North America, Europe, and Asia Pacific, regional B&B associations, OTA revenue managers, and tourism zoning officials. Interviews clarified unregistered supply, seasonal closures, fee structures, and the likely trajectory of OTA commission rates, all of which were used to fine-tune assumptions and cross-check secondary signals.

Desk Research

We began with public datasets such as UNWTO inbound overnight stays, OECD tourism satellite accounts, World Bank disposable income series, and national statistics from the US National Park Service, VisitBritain, and Tourism Research Australia, which reveal traveler flows and rural lodging preferences. Industry trackers, STR occupancy dashboards, Airbnb transparent listings, and Eurostat short-stay permits help size available B&B inventory and average daily rates. Company financials drawn from D&B Hoovers and news coverage screened through Dow Jones Factiva round out price and expansion cues. These sources anchor historic demand, room stock, and tariff patterns that feed our model. The list is illustrative; many other references support validation.

Market-Sizing & Forecasting

A top-down build starts with domestic and international leisure nights spent in small lodging, reconstructed from tourism arrival data and average length of stay, and then applies a penetration ratio for B&B preferences by traveler cohort. Results are balanced with selective bottom-up checks, sampled room counts, typical occupancy, and blended ADR to confirm revenue plausibility before adjustments. Key variables include rural versus urban stay mix, OTA share of B&B bookings, regulatory permit issuances, disposable income per capita, and ADR inflation. Forecasts employ multivariate regression with scenario analysis, where the base case aligns income growth, online booking penetration, and expected permit trends with expert consensus.

Data Validation & Update Cycle

Outputs undergo variance scans against independent occupancy sets and taxation receipts; anomalies trigger model reruns and senior review. Reports refresh each year, and material events, for example, zoning reform or a travel ban lift, prompt an interim revision so clients receive the most current view.

Why Our Bed And Breakfast Accommodation Baseline Commands Reliability

Published figures differ because firms pick contrasting scopes, price proxies, and refresh cadences.

Key gap drivers stem from whether guesthouses and farm stays are grouped in, how ADRs are sourced, and how unlicensed supply is treated before currency conversion and inflation adjustments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 32.2 B (2025) | Mordor Intelligence | - |

| USD 34.4 B (2024) | Global Consultancy A | Includes guesthouses and hostels; wider Asia Pacific uplift; single-year currency average |

| USD 35.7 B (2024) | Sector Analyst B | Applies hotel ADR to B&B rooms; limited rural coverage; two-year growth extrapolation |

| USD 6.3 B (2024) | Trade Journal C | Counts only registered B&Bs; omits platform-hosted properties; excludes breakfast upsell revenue |

The comparison shows that when supply definition, pricing basis, and refresh cadence are aligned, totals converge; when they diverge, gaps widen.

By openly stating scope, using verifiable variables, and revisiting models annually, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can reliably trace and replicate.

Key Questions Answered in the Report

What is the current size of the global bed and breakfast market?

The market reached USD 33.75 billion in 2026 and is forecast to grow to USD 42.99 billion by 2031.

Which region is expanding the fastest in the bed and breakfast market?

Asia-Pacific posts the quickest growth, registering an 8.45% CAGR through 2031, driven by rising domestic travel in India and gradual reopening in China.

Which accommodation type holds the largest share?

Boutique and heritage inns lead the segment with 31.62% revenue share, owing to traveler demand for authentic, culturally immersive stays.

How are booking channels changing for B&B operators?

Online travel agencies still dominate but direct website bookings are rising at 12.3% CAGR, helped by mobile apps and lower acquisition costs.

What regulatory challenges face the sector?

Urban zoning limits and principal-residence rules in markets such as British Columbia and Scotland impose compliance costs and restrict new urban inventory.

Page last updated on: