Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

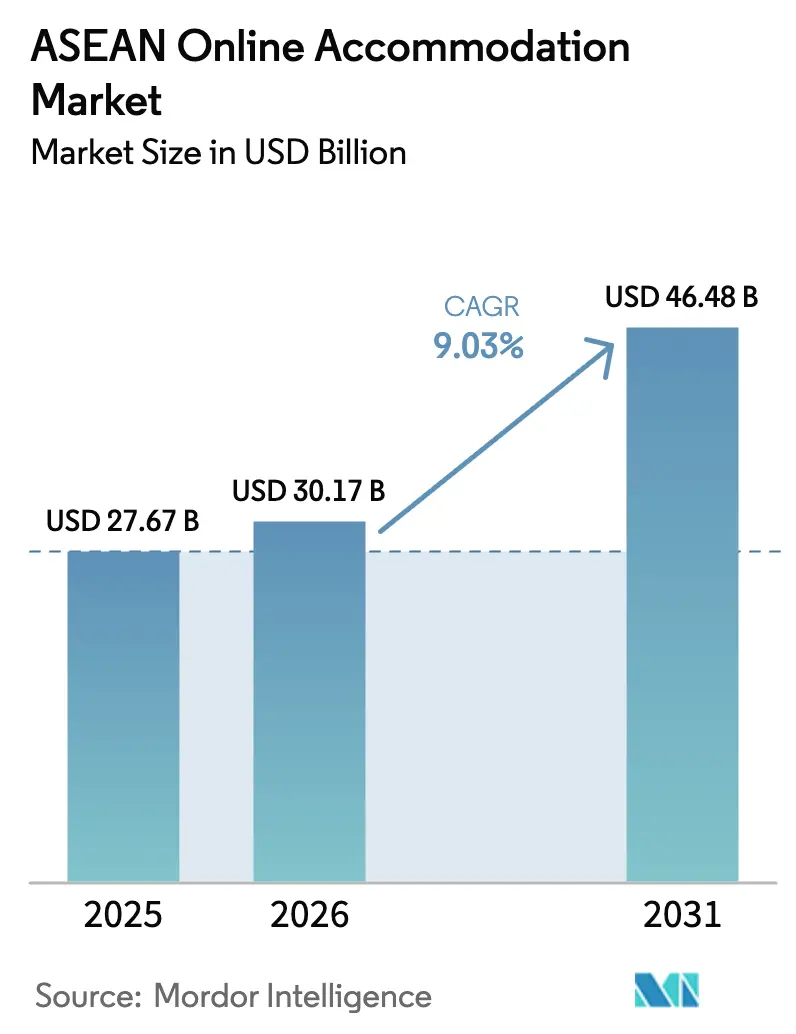

| Base Year Market Size (2025) | USD 27.67 Billion |

| Market Size (2026) | USD 30.17 Billion |

| Market Size (2031) | USD 46.48 Billion |

| Growth Rate (2026 - 2031) | 9.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Online Accommodation Market Analysis by Mordor Intelligence

The ASEAN Online Accommodation Market size is expected to grow from USD 27.67 billion in 2025 to USD 30.17 billion in 2026 and is forecast to reach USD 46.48 billion by 2031 at 9.03% CAGR over 2026-2031.

Growing smartphone penetration that already exceeds 80% in large member economies, seamless QR-based cross-border payments, and a rapid rebound in international arrivals continue to propel digital booking volumes. Demand momentum is reinforced by low-cost carrier (LCC) route expansions that cut average intra-ASEAN fares significantly, making secondary leisure destinations more accessible. Government visa-free entry programs, especially Thailand’s 60-day stay policy for 93 countries, complement the post-pandemic “revenge travel” surge, while new digital-nomad visa schemes in the Philippines and Thailand nurture a lucrative workcation segment. Competitive intensity within the online travel agency (OTA) market remains significant. The leading OTAs dominate a considerable share of bookings and allocate substantial resources toward marketing efforts in the first quarter of 2024. Despite the competitive landscape, participation in OTA platforms enhances the average hotel’s return on assets by providing incremental exposure, which contributes to improved financial performance.

Key Report Takeaways

- Mobile applications are projected to dominate the platform segment, accounting for a substantial market share of 55.63% of the ASEAN Online Accommodation Market in 2025. Furthermore, this sub-segment is anticipated to expand at a strong CAGR of 14.63% during the forecast period from 2026 to 2031.

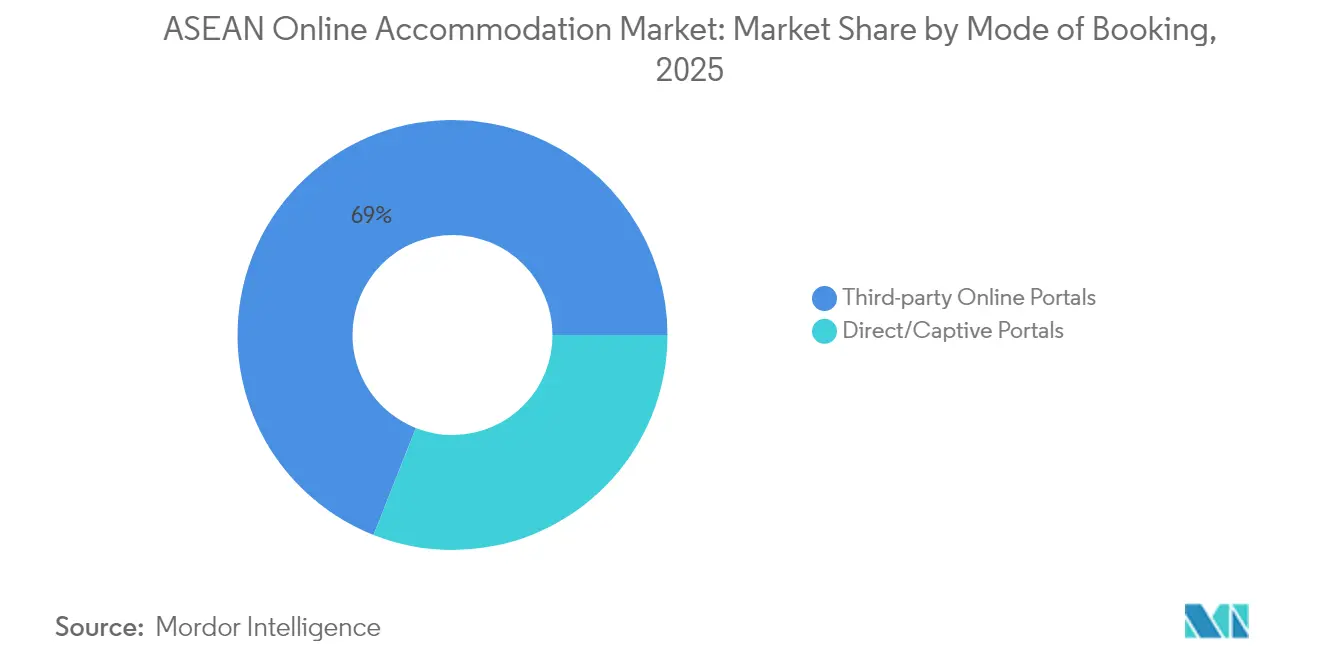

- Third-party online portals are expected to lead the mode of booking category, capturing a significant share of 69.02% of the ASEAN Online Accommodation Market in 2025. Meanwhile, direct or captive portals in ASEAN Online Accommodation Market are forecasted to exhibit the highest growth rate, with a CAGR of 15.51% over the same forecast period.

- Within the property type segment, hotels and resorts are estimated to hold the largest share of 50.61% of the ASEAN Online Accommodation Market in 2025. However, alternate lodgings in ASEAN Online Accommodation Market are identified as the fastest-growing sub-segment, with a notable CAGR of 18.32% projected for 2026-2031.

- From a geographical perspective, Vietnam is expected to secure a leading position with a 25.12% market share of the ASEAN Online Accommodation Market in 2025. On the other hand, Thailand in ASEAN Online Accommodation Market is projected to witness accelerated growth, with a CAGR of 12.78% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Online Accommodation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-cost carrier expansion | +2.1% | ASEAN corridor routes | Medium term (2-4 years) |

| Cross-border QR payment interoperability | +1.8% | TH, MY, ID, VN, SG | Short term (≤2 years) |

| Post-pandemic “revenge travel” | +2.3% | ASEAN-wide | Short term (≤2 years) |

| Visa-free entry programs | +1.9% | TH, MY, PH | Medium term (2-4 years) |

| Remote work “workcation” policies | +1.2% | PH, TH, ID | Long term (≥4 years) |

| Super-app ecosystem cross-selling | +1.4% | SG, ID, MY | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Low-Cost Carriers Boosting Intra-ASEAN Leisure Trips

Low-cost carriers, including AirAsia, Scoot, and Cebu Pacific, have strategically increased point-to-point routes, effectively bypassing traditional hub airports. This operational shift has driven significant growth in passenger traffic at secondary airports, highlighting the evolving dynamics of air travel demand. Additionally, the substantial reduction in average leisure fares on key routes, such as Kuala Lumpur to Bangkok and Jakarta to Phuket, has further stimulated travel activity. This fare decline has particularly encouraged weekend travel among middle-income households, reflecting a shift in consumer behavior and preferences within the aviation market. The widened network footprint feeds directly into incremental room nights for emerging beach, cultural, and eco-tourism destinations that previously lacked international lift. Sustained LCC orderbooks for narrow-body aircraft signal capacity growth through the late-2020s, anchoring a durable demand engine for the ASEAN online accommodation market[1]Asian Development Bank, “ADB Forecasts Developing Asia’s Economy to Grow 4.9% in 2024,” adb.org .

Digital Payments Interoperability (QR-Code Cross-Border)

Central-bank-led collaboration has linked domestic e-wallet schemes so that Thai, Malaysian, Indonesian, Vietnamese, and Singaporean tourists can scan familiar QR codes abroad and settle in their home currency. For small and mid-scale lodging operators, the ability to collect digital payments without foreign-merchant accounts removes a key barrier to online distribution. According to industry case studies, implementing streamlined checkout processes significantly enhances booking completion rates, with an observed increase when compared to systems that rely solely on card payment options. This highlights the importance of optimizing payment flows to improve user experience and drive higher conversion rates. Over the next two years, the network is slated to expand to Cambodia, Laos, and the Philippines, making frictionless payments a near-universal feature across the ASEAN online accommodation market.

Post-Pandemic Pent-Up Demand for “Revenge Travel”

The ongoing impact of lockdown fatigue has shifted consumer behavior, with travelers increasingly prioritizing experiential value over material consumption. This trend has resulted in extended travel itineraries and higher daily expenditures. By the end of 2024, ASEAN tourism is projected to recover to 2019 arrival levels. Survey insights indicate a growing trend among households, with a significant proportion planning to undertake two or more international leisure trips annually through 2026. Vietnam and Thailand, in particular, have reported occupancy rates exceeding in key urban and resort hubs, while average daily rates have surpassed pre-pandemic benchmarks. This sustained consumer willingness to spend is driving growth across both traditional hotel chains and premium alternative accommodations, thereby reinforcing revenue streams for hospitality platforms and operators. The data underscores a robust recovery trajectory for the region's tourism sector, supported by evolving consumer preferences and spending patterns[2]Savarin Luxury Property, “Thailand’s Hotel Industry: Bright Outlook Continues in 2025,” savarinluxprop.com .

Government Visa-Free Entry Programs

Thailand’s decision to waive visas for citizens of 93 countries and allow 60-day stays sets a high regional bar for facilitation[3]VnExpress, “Which Southeast Asian Country Welcomes Highest Number of American Tourists?” vnexpress.net . The Destination Thailand Visa, which permits multiple 180-day entries over five years, is strategically designed to attract digital nomads, long-term retirees, and repeat leisure travelers. Malaysia and the Philippines have implemented comparable initiatives, reflecting a regional trend toward targeting these high-value visitor segments. Preliminary arrival data for 2024-2025 highlights a significant double-digit increase in travelers from the United States and Europe. This influx of extended-stay visitors, who typically prefer accommodations with higher nightly rates and flexible options, is driving a notable rise in premium demand within the ASEAN online accommodation market, underscoring a shift toward more lucrative customer demographics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented taxation & short-stay regulations | -1.3% | MY, TH, VN, PH | Long term (≥4 years) |

| High OTA customer-acquisition cost | -0.9% | ASEAN-wide | Medium term (2-4 years) |

| Limited rural broadband coverage | -0.7% | ID, PH, MM, LA | Long term (≥4 years) |

| Currency volatility | -0.6% | ASEAN-4 | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Fragmented Taxation and Short-Stay Regulations Across ASEAN

Businesses operating in the Southeast Asian hospitality sector face significant challenges due to varying hotel and tourism levies across the region. For instance, Malaysia enforces a straightforward flat RM10 tourism tax, whereas Thailand implements a more intricate framework that includes a multi-layer VAT and TM.30 guest-registration requirements. Providers of alternative accommodations encounter additional complexities, as they must navigate unclear zoning regulations and condominium bylaws. These regulatory ambiguities contribute to the proliferation of a gray market, which undermines the competitiveness of licensed operators. The inconsistent enforcement of these regulations further exacerbates the issue, placing compliant businesses at a disadvantage due to higher operational costs. This disparity not only erodes their price competitiveness but also impedes the overall professionalization and growth of the ASEAN online accommodation market.

High Customer-Acquisition Cost on OTAs

Independent hotels, particularly those with limited negotiating leverage, experience significant margin erosion due to commission rates applied to room revenue. While leveraging Online Travel Agencies (OTAs) increases overall occupancy levels and has been demonstrated to improve return on assets by approximately 3 percentage points, many properties encounter difficulties in securing the necessary capital for strategic investments. These investments, which are critical for reducing long-term distribution expenses, include the development of direct-booking platforms, implementation of loyalty programs, and execution of digital marketing strategies. The financial strain is especially severe in secondary markets, where Average Daily Rates (ADRs) remain relatively low, yet commission rates persist at consistent levels, further compressing profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Mobile Applications Drive Digital-First Booking Behaviors

Mobile Apps accounted for 55.63% of the ASEAN online accommodation market share in 2025, dwarfing desktop channels as travellers pivot to on-the-go planning. Indonesia exemplifies this shift, with more than half of OTA users booking via smartphones as early as 2018. The convenience of fingerprint login saved traveller profiles, and e-wallet checkout underpins a forecast 14.63% CAGR for mobile bookings through 2031. Website interfaces remain relevant for complex multi-city itineraries and corporate travel, yet their growth lags that of app-centric channels.

The ascendancy of apps dovetails with super-app monetization strategies that fuse transport, food delivery, and lodging into a single user journey. Enhanced push-notification targeting and AI-based price alerts further raise app engagement, siphoning share from both traditional desktop portals and call-centre bookings. Regulators, meanwhile, are codifying mobile payment standards that recognize the app as the default commerce environment, cementing its primacy in the ASEAN online accommodation market.

By Mode of Booking: Third-Party Portals Maintain Distribution Dominance Despite Direct Channel Growth

Third-party portals captured 69.02% of the total 2025 transaction value thanks to their deep inventory pools and metasearch visibility. Even so, direct/captive portals will post the fastest growth—15.51% CAGR—as chains deploy dynamic-packaging engines, member-only rates, and cashback rewards. Hotels aim to claw back share to ease commission drag, but outcome success hinges on competitive parity with OTAs’ seamless UX, multilingual support, and instant confirmation.

Independent properties, especially in rural or island locations, still lean heavily on OTAs for reach. For them, the ASEAN online accommodation market size attributable to direct sales remains limited by marketing budgets and technology gaps. Aggregator strength is likely to persist, but its share edge could narrow by the late 2020s as loyalty ecosystems and white-label booking solutions mature.

By Property Type: Alternative Lodgings Capitalize on Experience-Driven Travel Demand

Hotels & Resorts retained a 50.61% slice of the 2025 transaction value, benefiting from established brands and corporate demand. Yet, Alternate Lodgings, glamping tents, farm-stays, and boutique villas clock the fastest trajectory at 18.32% CAGR. Rural Vietnam now counts 11 government-endorsed ecological farms that blend lodging with agritourism workshops, while Philippine farm-stay clusters around CALABARZON report occupancy uplift after digital onboarding to major OTAs.

Premium short-term rental properties on select Thai islands generate significant annual host revenues, often exceeding USD 40,000. While hostels and budget hotels continue to cater to the preferences of Gen Z backpackers, the upscale experiential accommodation segment is experiencing the most rapid expansion. This growth is driven by a rising consumer demand for authentic, immersive experiences and visually appealing properties that align with social media trends, particularly those suitable for platforms like Instagram.

Geography Analysis

Vietnam commanded 25.12% of the ASEAN online accommodation market size in 2025 as post-COVID recovery reached near-full normalization. American inbound searches rank the country top among ASEAN peers, funneling traffic to both coastal resorts and new inland farm-stays. Regulatory clarity around VAT and personal-income tax for home-stay operators, although burdensome, helps formalize supply and instill traveler confidence.

Thailand’s pace-setting growth stems from destination marketing that positions the kingdom as both a wellness mecca and a flexible remote-work base. Permanent visa-free status for Chinese travelers and 60-day stays for 93 nationalities decrease planning friction. Domestic developers and global brands are reacting: Centara Life, lyf and Novotel have announced or inaugurated dozens of mixed-use properties catering to millennials, long-stay professionals and families. Regulatory grey zones persist for condo-based short-term rentals, yet sustained political will to align rules with demand could unlock fresh inventory. Indonesia benefits from a diversified archipelago where Bali still reigns, but “10 New Balis” campaigns funnel infrastructure spending toward Mandalika, Labuan Bajo and Lake Toba. The World Travel & Tourism Council sees international visitor spending hitting record highs in 2025, translating into robust booking throughput. Meanwhile, Malaysia’s linked payments with Singapore and Thailand, plus the Philippines’ June 2025 digital-nomad visa, add competitive texture to the ASEAN online accommodation market landscape. Smaller economies—Cambodia, Laos, Myanmar and Brunei—stand to capture spillover when main hubs reach peak occupancy, provided broadband and airlift gaps close.

Competitive Landscape

Oligopolistic dynamics define the marketplace: Booking Holdings, Expedia Group, Trip.com Group, Traveloka, and Agoda collectively hold a significant share, enabling scale advantages in search-engine marketing, loyalty programs, and AI-driven personalization. Regional challengers leverage localization—language, payment methods, and after-sales support—to defend niche strongholds, while super-app entrants Grab and GoTo exploit embedded user bases to cross-sell hotels at marginal acquisition cost.

Product innovation is relentless. Booking.com unveiled generative-AI trip assistants in late 2024, and Centara rolled out chat-based booking bots in early 2025, aiming to lift direct share among Gen Z. Asset-light virtual-hotel brands sign revenue-share deals with independent properties, supplying centralized pricing algorithms and brand standards in exchange for inventory. Compliance complexity around taxation, data residency, and guest registration favors well-capitalized platforms that maintain legal teams across all ten ASEAN jurisdictions.

The supply side is equally active. Ascott added more than 3,400 units via 28 Southeast Asia signings in 2024, focusing on co-living label lyf to target digital natives. Accor’s Swissôtel Bangkok Pratunam and Centara’s Indonesian debut bolster upscale room counts. Alternative-accommodation specialists expand vetted host programs to raise consistency and meet traveler expectations for hygiene and safety. With the top five brokers still controlling over three-quarters of gross bookings, the ASEAN online accommodation market remains tightly held despite a steady flow of new niche entrants.

ASEAN Online Accommodation Industry Leaders

Booking Holdings (Booking.com, Agoda)

Traveloka

Expedia Group

Airbnb Inc.

Trip.com Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Trip.com Group and Traveloka announced a strategic distribution alliance to pool outbound Chinese and regional Southeast Asian traffic.

- June 2025: The Philippines launched a digital-nomad visa designed for remote professionals seeking extended ASEAN stays.

- March 2025: Centara Hotels & Resorts launched a guest-centric mobile app with an AI chatbot to accelerate direct bookings.

- January 2024: Thailand implemented permanent visa-free entry for Chinese nationals, reinforcing its visitor-volume targets.

ASEAN Online Accommodation Market Report Scope

Online accommodation refers to the lodging booked online by travellers for the purpose of stay. Travelers can choose from the various types of accommodations available such as hotels, hostels, resorts, vacation rentals, and others. Accommodation can be booked through various sources, which include online travel agencies, hotel websites, booking through agents, and direct bookings. ASEAN Online Accommodation Market is segmented by Platform type (Mobile application and Website), by Mode of Booking Type (Third Party online portals and Direct/Captive portals), and by Country (Singapore, Malaysia, Indonesia, Thailand, and Rest of ASEAN).

By Platform

| Mobile Application |

| Website |

By Mode of Booking

| Third-party Online Portals |

| Direct/Captive Portals |

By Property Type

| Hotels & Resorts |

| Vacation Rentals |

| Hostels & Budget Accommodations |

| Alternate Lodgings (Glamping, Farm-stays) |

By Geography

| Indonesia |

| Thailand |

| Malaysia |

| Philippines |

| Vietnam |

| Singapore |

| Cambodia |

| Laos |

| Myanmar |

| Brunei |

| By Platform | Mobile Application |

| Website | |

| By Mode of Booking | Third-party Online Portals |

| Direct/Captive Portals | |

| By Property Type | Hotels & Resorts |

| Vacation Rentals | |

| Hostels & Budget Accommodations | |

| Alternate Lodgings (Glamping, Farm-stays) | |

| By Geography | Indonesia |

| Thailand | |

| Malaysia | |

| Philippines | |

| Vietnam | |

| Singapore | |

| Cambodia | |

| Laos | |

| Myanmar | |

| Brunei |

Key Questions Answered in the Report

How large is the ASEAN online accommodation market in 2026?

The ASEAN online accommodation market size stood at USD 30.17 billion in 2026 and is projected to exceed USD 46.48 billion by 2031.

What is the expected growth rate for online lodging bookings in Southeast Asia?

The market is forecast to register a 9.03% CAGR between 2026 and 2031, lifted by mobile adoption, open-visa policies and LCC connectivity.

Which booking channel is growing fastest within Southeast Asia?

Direct or captive portals are expanding the quickest, with a 15.51% CAGR outlook as hotel groups invest in loyalty apps and member-only rates.

Why are alternative lodgings gaining popularity among ASEAN travelers?

Travelers seek unique, immersive experiences such as farm-stays and glamping; this preference propels alternative lodging bookings at a 18.32% CAGR.

Which country currently leads Southeast Asia in online accommodation revenue?

Vietnam held the largest geographic share at 25.12% in 2025, buoyed by a near-complete tourism rebound and diversified lodging options.

How do visa policies influence booking trends across ASEAN?

Expanded visa-free and digital-nomad schemes in Thailand, the Philippines and Malaysia lower travel barriers, directly boosting room-night demand across the region.

Page last updated on: