Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

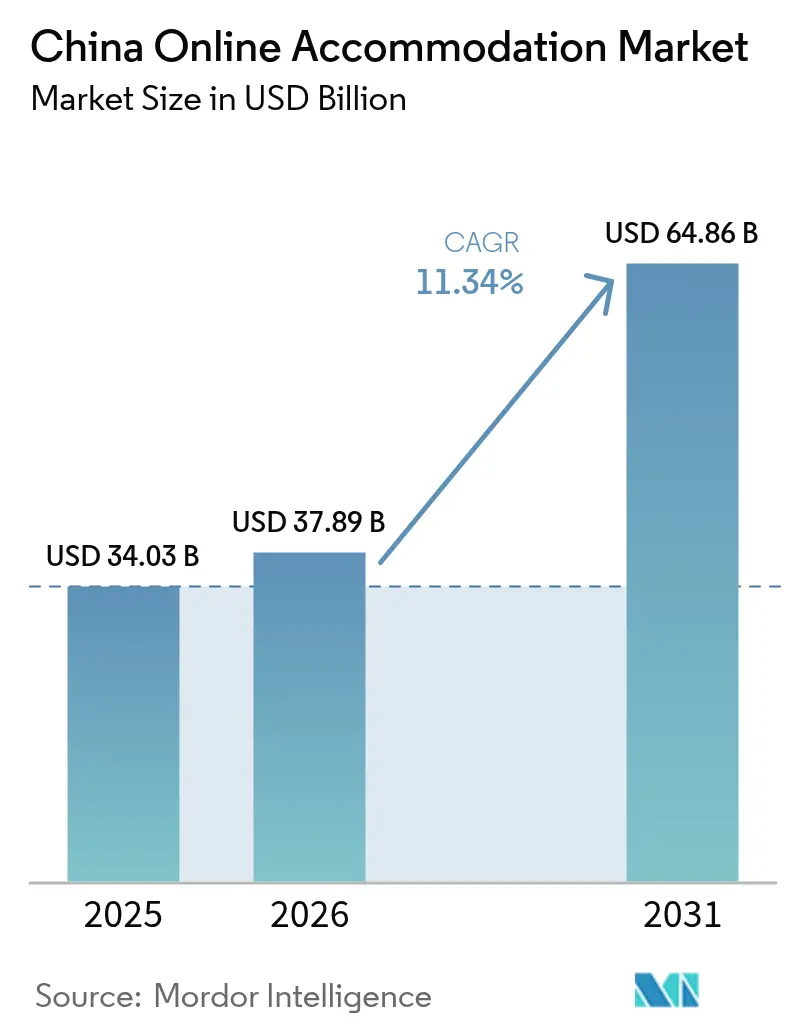

| Base Year Market Size (2025) | USD 34.03 Billion |

| Market Size (2026) | USD 37.89 Billion |

| Market Size (2031) | USD 64.86 Billion |

| Growth Rate (2026 - 2031) | 11.34% CAGR |

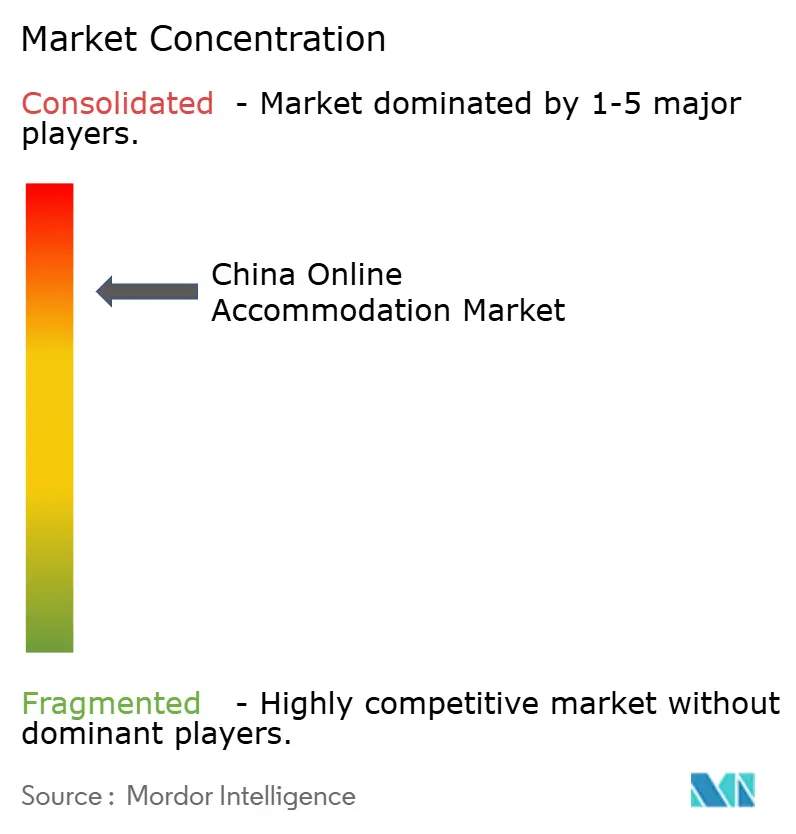

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Online Accommodation Market Analysis by Mordor Intelligence

The China online accommodation market size was valued at USD 34.03 billion in 2025 and estimated to grow from USD 37.89 billion in 2026 to reach USD 64.86 billion by 2031, at a CAGR of 11.34% during the forecast period (2026-2031). Momentum comes from the domestic tourism rebound, with 4.891 billion trips taken in 2023, and from deeper digital penetration that places mobile booking at the center of every travel journey. Platforms are intensifying investments in AI-driven personalization and in rural homestay supply to capture experience-seeking consumers. Regulatory clarity on cross-border data flows, coupled with government programs that funnel capital into transport nodes, underpins long-term confidence. Price-sensitive independent hotels, however, continue to struggle with rising OTA commissions and cybersecurity compliance costs, prompting experiments with direct-booking channels.

Key Report Takeaways

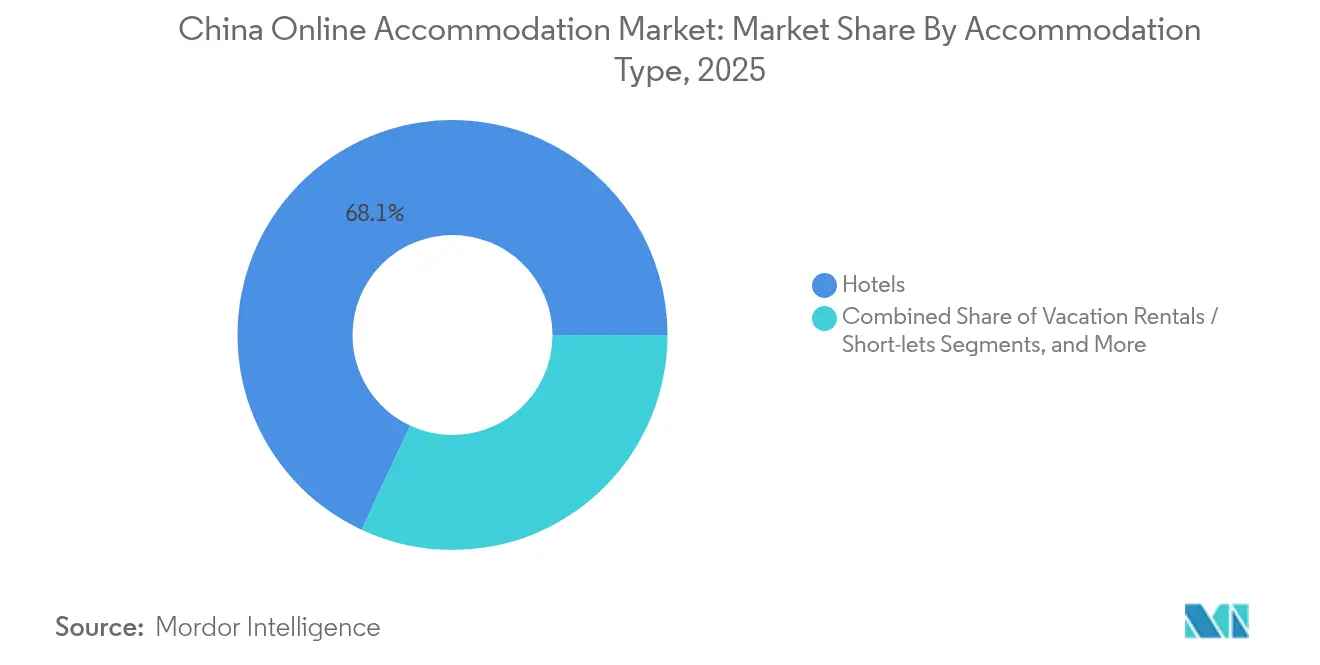

- By accommodation type, hotels led with 68.05% revenue share in 2025; vacation rentals and short-lets are forecast to expand at a 14.03% CAGR to 2031 in the China online accommodation market.

- By booking device, mobile apps captured 81.75% of the China online accommodation market share in 2025, while the same channel is advancing at a 17.12% CAGR through 2031.

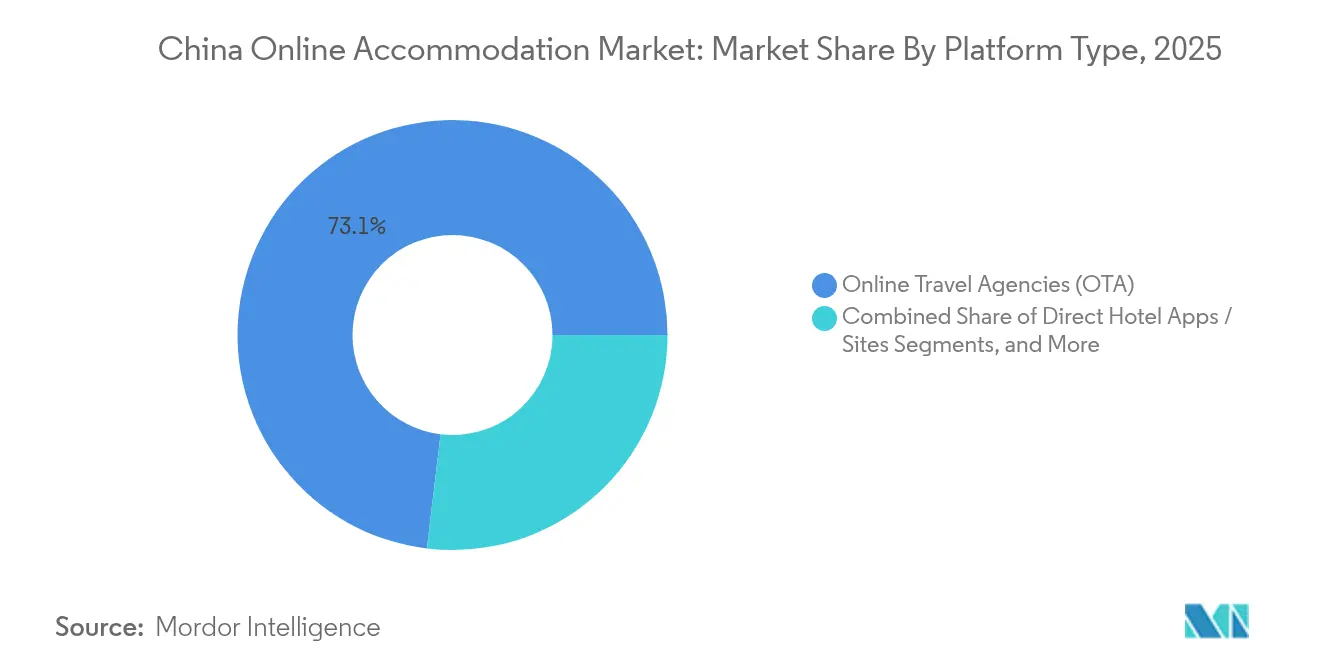

- By platform type, online travel agencies held 73.10% of the China online accommodation market share in 2025; super-app ecosystems are set to grow at a 12.55% CAGR between 2026-2031.

- By customer type, leisure travelers accounted for a 63.88% share of the China online accommodation market size in 2025, whereas long-stay and relocation bookings show the highest projected CAGR at 15.39% to 2031.

- By region, East China commanded 33.22% of the China online accommodation market size in 2025; South-Central China is the fastest-growing region with a 13.05% CAGR expected over 2026-2031.

- The China online accommodation market remains moderately concentrated: Trip.com Group, Meituan, Tongcheng Travel, Fliggy and Booking.com collectively control the majority of online room nights.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Online Accommodation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic domestic tourism rebound | +2.8% | National, with stronger impact in East China and South-Central China | Medium term (2-4 years) |

| Rise of Experience-Based Travel | +2.1% | Urban centers and cultural tourism destinations nationwide | Long term (≥ 4 years) |

| Growth of OTAs and Super Apps | +3.2% | National, with highest penetration in Tier 1 and Tier 2 cities | Short term (≤ 2 years) |

| Government Support and Regulatory Clarity | +1.4% | National, with focused benefits in designated tourism zones | Long term (≥ 4 years) |

| High Internet and Smartphone Penetration | +1.8% | National, with accelerated impact in lower-tier cities | Short term (≤ 2 years) |

| Urbanization and Tier Expansion | +2.2% | Tier 2, Tier 3, and emerging Tier 4 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic Domestic Tourism Rebound

Holiday periods in 2024 kept that pace, with the Spring Festival alone delivering 474 million trips and upscale-hotel occupancy exceeding 80%. Travellers gravitated toward local experiences, which shifted booking volumes from international to domestic inventory and opened incremental demand in rural destinations. Nearly 800 million visitors explored countryside attractions during Q1 2024, prompting platforms to fast-track listings in peripheral counties. The surge unlocked new lodge construction outside urban cores and broadened the China online accommodation market footprint.

Rise of Experience-Based Travel

Millennials and Gen Z now prioritize immersive stays: 77% of their trips are booked less than a month in advance, favoring spontaneous weekend getaways. “Traveling-at-home” trends—young residents checking into hotels in their hometowns—boosted local bookings during major holidays. Hotels, hostels and vacation rentals are weaving regional décor and artisanal workshops into packages to satisfy authenticity cravings. Douyin’s short-video creators amplify this shift by linking viral content to instant booking pages, a loop that accelerates conversion for boutique stays. As cultural immersion becomes mainstream, experience-themed inventory raises ADRs across secondary cities, fortifying long-tail supply on leading platforms.

Growth of OTAs and Super Apps

Leading OTAs together processed more than RMB 700 billion (USD 97.58 billion) in gross bookings during the most recent pre-pandemic half-year and have since scaled further, helped by broader smartphone adoption. WeChat mini-programs embed one-click room reservations inside a daily-use messaging environment, lowering discovery friction and nudging impulse purchases. Trip.com Group reported RMB 4.5 billion (USD 623 million) in Q1 2024 accommodation revenue, up 29% year-over-year, a testament to higher transaction frequency and richer product bundles. As OTAs are pushed into third- and fourth-tier cities, mobile design simplicity and alternative payment methods remain key levers for capturing incremental users.

Government Support and Regulatory Clarity

A May 2024 directive mandated nationwide acceptance of foreign guests at all hotels, lifting legacy licensing barriers that limited international demand[1]Source: Ministry of Commerce of the People’s Republic of China, “Notice on Further Optimising Services for Inbound Travellers,” mofcom.gov.cn. .Parallel efforts from the Ministry of Commerce and the China Hotel Association provide English-language training, enhancing service consistency at independent properties. New cross-border data-flow rules, effective March 2024, deliver clearer compliance templates, allowing both domestic and international platforms to invest confidently in data analytics and loyalty management. Infrastructure financing—ranging from high-speed rail to rural tourism corridors—reinforces demand stimuli, setting the stage for stable, policy-backed expansion of the Chinese online accommodation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OTA commission pressure on hotel margins | -1.8% | National, with higher impact on independent hotels | Short term (≤ 2 years) |

| Cyber-security and data-privacy regulations (PIPL) | -1.2% | National, with compliance costs affecting all digital platforms | Medium term (2-4 years) |

| Shrinking supply of urban budget hotels | -1.5% | Tier 1 cities and major urban centers | Medium term (2-4 years) |

| Inter-platform price-parity clamp-downs | -0.9% | National, with strongest impact on major OTA platforms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OTA Commission Pressure on Hotel Margins

Large OTAs command up to 20% commissions, eroding profitability for budget and mid-range operators. Continuous customer-acquisition spending by platforms pushes commissions higher, and independent properties lack scale to negotiate relief. To offset rising costs, hotels roll out direct-booking apps and partnership loyalty schemes, yet open-web marketing expenses temper their effectiveness. The imbalance is expected to nudge asset-light franchises and monarchized models forward, as they offer combined brand awareness and margin resilience.

Cyber-security and Data-privacy Regulations (PIPL)

China's Personal Information Protection Law and the new Regulations on Network Data Security Management, effective January 1, 2025. Platforms handling the data of over 10 million users must establish specialised security units, store audit logs for three years, and report all incidents within 24 hours[2]Source: National Internet Information Office of China, “Regulations on Network Data Security Management (Draft),” niio.gov.cn. . The regulations also impose restrictions on cross-border data transfers, potentially limiting international platforms' ability to integrate Chinese operations with global systems. Compliance costs are particularly burdensome for smaller platforms and accommodation providers, potentially accelerating market consolidation as only well-resourced players can afford a comprehensive data protection infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Accommodation Type: Hotels Maintain Dominance Amid Vacation Rental Surge

Hotels captured 68.05% of China's online accommodation market revenue in 2025, a testament to entrenched loyalty programs and robust distribution through major OTAs. Vacation rentals and short-lets, however, are projected to grow at a 14.03% CAGR, driven by travelers appetite for home-style amenities in emerging leisure hubs. Tujia lists more than 2.3 million units, giving it roughly 60% share of the niche and signaling that branded inventory curation is displacing informal hosts. Diversification is growing serviced apartments win favor among relocating professionals, while rural homestays expand as agritourism booms. Capsule hotels keep attracting value-focused Gen Z guests, yet premiumization across the broader China online accommodation market limits their long-run ceiling.

Preference for authenticity feeds a pipeline of hybrid models that fuse hotel services with residential layouts. Operators pilot subscription-based packages granting pool access and co-working space, aligning with digital-nomad habits. Domestic REITs include compliant homestay portfolios, reflecting investor belief in experience-driven demand. The market is therefore expected to witness intensified competition between asset-heavy hotel groups and asset-light rental platforms, each racing to widen supply breadth without compromising service standards.

By Booking Device: Mobile App Dominance Accelerates

Mobile apps controlled 81.75% of the China online accommodation market share in 2025 and are on course for a 17.12% CAGR through 2031 as super-apps weave reservation capabilities into daily utilities. With built-in wallets and loyalty points, users can book, pay and review within a single interface, collapsing the path-to-purchase into seconds. The China online accommodation market rewards speed: abandoned-cart rates drop sharply when biometric payment shortcuts auto-populate guest information.

Browser-based mobile sites retain value for extended research, especially among older demographics who prefer larger font scaling, yet they concede traffic as app UX refined. Desktop usage now concentrates on corporate travel desks where multi-traveler workflows matter most. Continuous rollouts of AI chatbots, live-stream showrooms and augmented-reality room previews maintain user attention, ensuring that mobile remains the defining battleground for platform differentiation.

By Platform Type: OTAs Lead While Super-Apps Gain Momentum

OTAs accounted for 73.10% of China online accommodation market bookings in 2025, benefiting from deep inventory, powerful cross-sell engines and extensive loyalty umbrellas. Super-apps, spearheaded by WeChat mini programs, are tracking a 12.55% CAGR to 2031 as consumer convenience trumps standalone browsing. WeChat funnels social influence into travel purchase by letting friends co-browse room types and split bills, amplifying word-of-mouth conversions. Hotels respond with targeted flash-sales inside these ecosystems to dilute OTA dependency.

Hotel-brand apps pick up pace through exclusive perks, free room upgrades and points multipliers. Chains such as IHG integrate digital check-in, meeting-room booking and upselling of F&B vouchers, nudging corporate travelers toward direct channels. Aggregators and suppliers now co-exist in an omnichannel mix, compelling revenue managers to juggle channel cost trade-offs. Future competitive edge lies in real-time API connectivity that unifies inventory, pricing, and guest-profile data across all touchpoints of the China online accommodation industry.

By Customer Type: Leisure Dominance with Long-Stay Emergence

Leisure and FIT travel represented 63.88% of the China online accommodation market size in 2025, powered by flexible family time and rising disposable incomes. Parallelly, long-stay and relocation demand a 15.39% CAGR, propelled by remote-work acceptance and urban migration of young professionals. Corporate leases for serviced apartments are lengthened as companies recalibrate mobility budgets, handing operators the chance to guarantee base occupancy. Leisure guests increasingly blend work and holiday, creating “bleisure” patterns that elongate average length of stay and lift ancillary revenue streams.

Business-travel recovery remains uneven; video-conference substitution holds back frequent short trips even as MICE events resume in major convention hubs. Group travel picks up where corporates arrange incentive tours to Tier 3 cities, spreading demand to new nodes and distributing spill-over bookings to smaller hotel chains. Personalized bundled packages—pairing stays with theme-park entry or hot-spring passes—keep broadening the appeal of the China online accommodation market beyond traditional city breaks.

Geography Analysis

East China’s lodging market benefits from sustained international linkages through Pudong and Xiaoshan airports. Continuous high-speed rail integration knits smaller cities into weekend-trip radii, adding depth to demand. Average occupancy in Shanghai premium hotels remained above 70% in 2024, prompting global brands to chase repositioning opportunities in heritage buildings. The region’s hotel operators focus on gastronomic experiences and art-themed interiors to differentiate amid mounting product homogeneity.

South-Central China is evolving into the growth locomotive of the China online accommodation market. Chongqing’s tourism bureau reported multi-digit visitor increases after the opening of its latest suspension bridge jump attraction, while Wuhan leveraged its Yangtze River cruise terminals to woo coastal vacationers. Aggressive airport expansions and upgraded metro networks compress travel friction; hoteliers respond with midscale properties that match rising yet still cost-sensitive middle-class expectations.

Across North, Southwest, Northeast and Northwest China, diverse catalysts shape local lodging contours. Winter sports grants revive demand in Jilin ski resorts, Silk Road heritage circuits spur hostel launches in Gansu, and cross-border e-visa policies increase inflows to Xinjiang. Government-backed eco-tourism pilots in Sichuan’s pandas reserves foster alliances between global hospitality groups and conservation-led developers. Collectively these shifts reinforce geographic diversification, cushioning the national market against regional shocks.

Competitive Landscape

The China online accommodation market remains moderately concentrated: Trip.com Group, Meituan, Tongcheng Travel, Fliggy and Booking.com collectively control the majority of online room nights. Trip.com logged RMB 17.3 billion (USD 2.4 billion) in accommodation revenue for 2023, up 133% year-on-year, underscoring the platform’s post-pandemic rebound. Meituan cross-sells hotel vouchers to its food-delivery users, capturing impulse bookings through same-app wallet balances. Tongcheng leverages transport ticketing data to upsell rooms adjacent to train stations, pushing conversion via precision targeting.

H World Group advocates an asset-light strategy: franchised and managed hotels contributed RMB 2.5 billion (USD 344 million) revenue in Q1 2025, with 21% growth [3]Source: Hilton Worldwide, “Hilton Garden Inn Investment Summit 2025 Press Release,” hilton.com. . Global chains—including Marriott, Accor and Hilton—embrace localization through joint ventures that expedite land-use approvals and tap local design influences. Vacation-rental disruptor Tujia fortifies its lead by onboarding professional property managers and layering service guarantees, lifting consumer trust in private-stay inventory.

Technology is the competitive fulcrum. AI-based chat agents streamline pre-arrival queries, lowering labor costs and heighten satisfaction scores. Dynamic-pricing engines crunch multi-source demand signals to refine RevPAR, and blockchain pilots attest to contract authenticity for corporate allotments. The convergence of travel with super-app ecosystems suggests that future winners will be those embedding lodging into daily-life apps, harvesting network effects that transcend classic search-and-book funnels.

China Online Accommodation Industry Leaders

Trip.com Group (Ctrip + Qunar)

Meituan

Tongcheng Travel

Fliggy (Alibaba)

Booking.com

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: H World Group reported 538 net hotel openings in Q1 2025, bringing its total to 11,685 hotels and 1,142,158 rooms.

- April 2025: Kempinski Hotels extended its partnership with BTG Hotels, targeting 200 properties under a new lifestyle brand within five years.

- January 2025: Hilton launched its first Hilton Garden Inn Gen A hotels in Chongqing, Sanya and Harbin, unveiling 19 new signings across Greater China.

- December 2024: Marriott International and Delonix Group signed eight properties to expand the Tribute Portfolio in Mainland China.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China online accommodation market as all paid lodging reservations that are initiated, transacted, and confirmed through internet-enabled platforms, principally mobile apps, super-apps, and conventional websites, covering hotels, serviced apartments, hostels, and legally registered short-term rentals booked by domestic or inbound travelers.

Scope exclusion: bookings completed entirely offline, pure airline-bundled tour packages, and unlicensed peer-to-peer home-stays are not counted.

Segmentation Overview

- By Accommodation Type

- Hotels

- Vacation Rentals / Short-lets

- Hostels and Capsule Hotels

- Serviced Apartments

- By Booking Device

- Mobile App

- Mobile Web

- Desktop / Laptop

- By Platform Type

- Online Travel Agencies (OTA)

- Direct Hotel Apps / Sites

- Super-app Ecosystems (WeChat Mini-Programs)

- By Customer Type

- Leisure / FIT

- Business Travel

- Group and MICE

- Long-stay / Relocation

- By Region

- East China

- North China

- Northeast China

- South-Central China

- Southwest China

- Northwest China

- Hong Kong and Macau SARs

- Taiwan Region

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed OTA strategy managers, mid-scale hotel revenue directors, and provincial tourism officials across East, South-Central, and Southwest China. These dialogues validated online share assumptions, average daily rate trends, and the ramp-up of super-app mini-program bookings, filling gaps that desk research alone could not bridge.

Desk Research

Mordor analysts first collated macro indicators and sector fingerprints from respected open sources such as the Ministry of Culture and Tourism visitor statistics, China Internet Network Information Center mobile-internet penetration reports, China Hospitality Association occupancy surveys, General Administration of Customs tourism balance-of-payments tables, and peer-reviewed studies in the Journal of Tourism Management. Corporate filings, IPO prospectuses, and earnings calls of leading OTAs supplemented channel-mix insights, while selective pulls from paid databases like Dow Jones Factiva and D&B Hoovers provided company-level revenue splits. The sources listed illustrate our evidence base; numerous additional publications were consulted for cross-checks and clarifications.

Market-Sizing & Forecasting

Bottom-up signals, sampled OTA gross bookings multiplied by commission yields and hotel chain digital sales audits, are overlaid on a top-down travel-spend pool reconstructed from domestic trip volumes, average length of stay, and ADR series. Key variables like smartphone penetration, OTA take-rate movements, urban disposable income, inbound visitor nights, and mobile payment usage feed a multivariate regression that projects demand to 2030. Where supplier roll-ups under-report niche segments, interpolation against occupancy and room-night growth bridges the gap before results are reconciled with the top-down view.

Data Validation & Update Cycle

Outputs undergo variance checks against independent tourism receipts and payment-network data. Senior analysts review anomalies, and findings are refreshed annually, with interim updates triggered by material shocks, regulatory pivots, major M&A, or pandemic-related travel advisories, so clients receive the latest view.

Credibility Anchor - Why Mordor's China Online Accommodation Baseline Rings True

Published estimates rarely match.

Divergences stem from how each firm slices online channels, converts room-night data to net revenue, and how frequently models are refreshed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 34.03 B (2025) | Mordor Intelligence | - |

| USD 30.60 B (2024) | Regional Consultancy A | Omits licensed short-term rentals; relies on linear CAGR extension without device-level validation |

| USD 35.00 B (2024) | Global Consultancy B | Adds web-assisted offline agency sales; biennial model refresh; currency fixed at prior-year FX |

These comparisons show that when scope is narrower or refresh cadence slower, totals drift. By combining channel-specific data with annually updated primary proofs, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace to clear variables and repeat with confidence.

Key Questions Answered in the Report

What is the current size of the China online accommodation market?

The China online accommodation market size stood at USD 37.89 billion in 2026.

How fast is the market expected to grow?

The market is projected to expand at an 11.34% CAGR, reaching USD 64.86 billion by 2031.

Which booking device dominates online reservations?

Mobile apps account for 81.75% of all online room bookings and are growing at a 17.12% CAGR.

Which region records the fastest growth in online accommodation demand?

South-Central China shows the highest forecast CAGR at 13.05% between 2026-2031.

What is the biggest challenge for hotels when working with OTAs?

Rising commission fees, which can exceed 20% of room revenue, compress margins for independent hotels.

Which accommodation segment is gaining traction beyond traditional hotels?

Vacation rentals and short-lets are projected to grow at a 14.03% CAGR as travellers seek home-style experiences.

Page last updated on: