Student Accommodation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

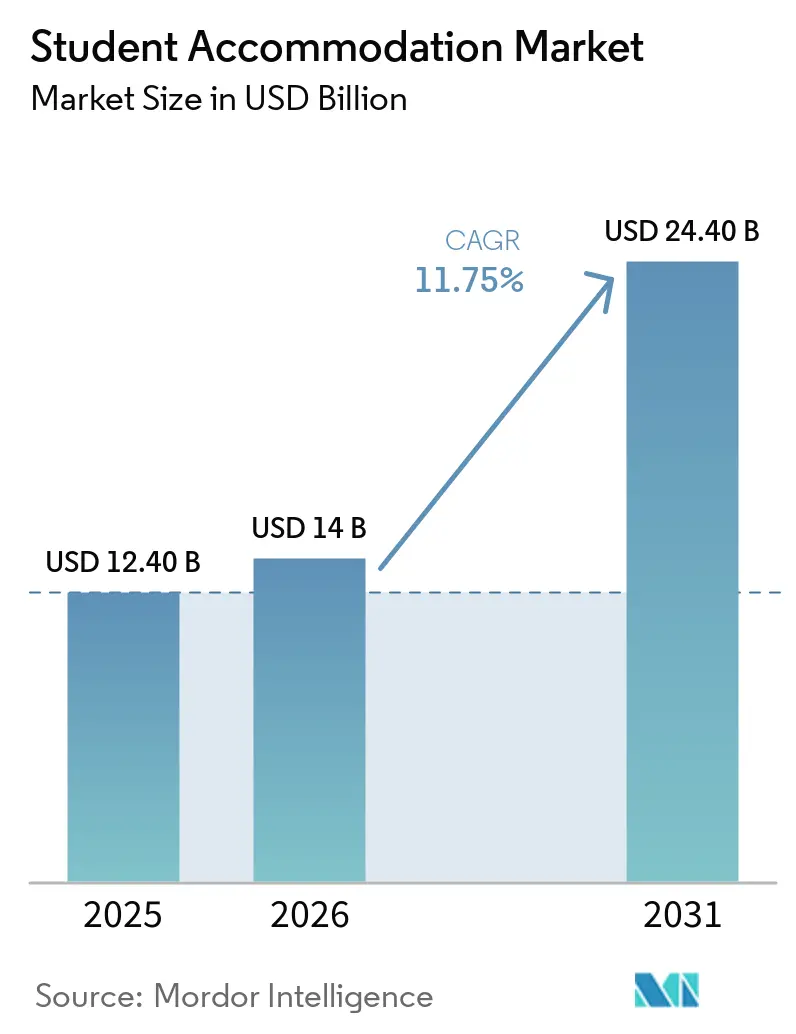

| Market Size (2026) | USD 14 Billion |

| Market Size (2031) | USD 24.40 Billion |

| Growth Rate (2026 - 2031) | 11.75% CAGR |

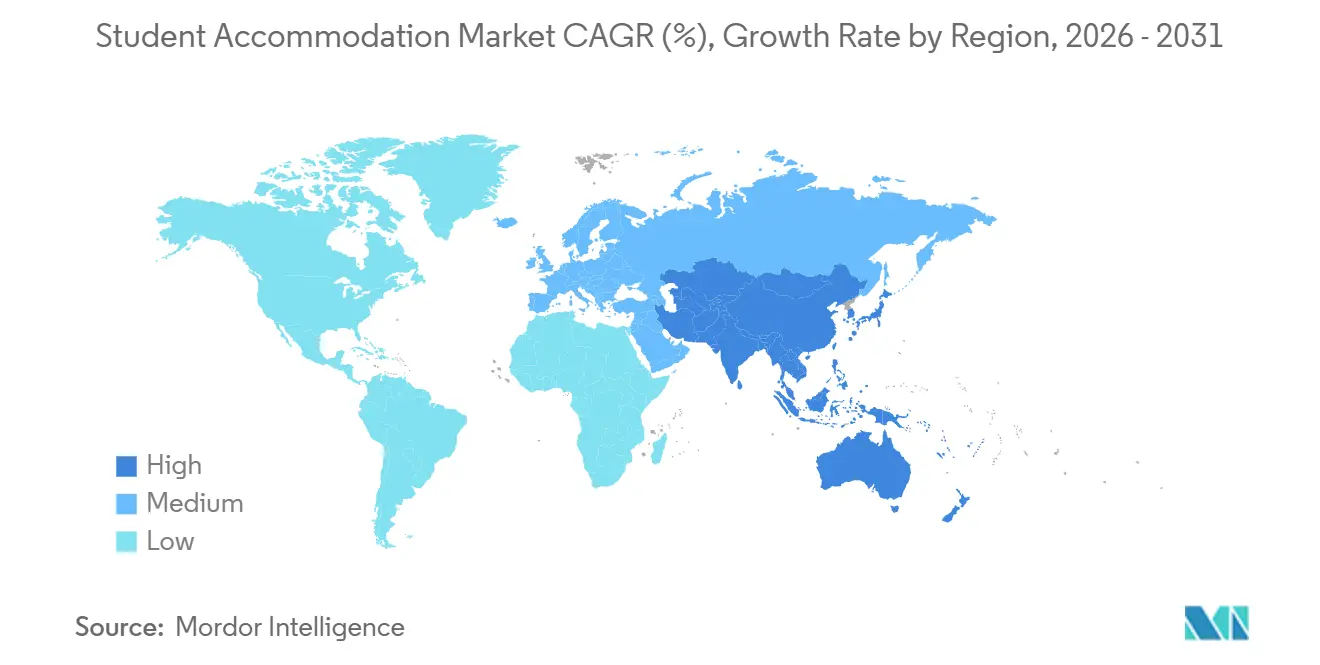

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

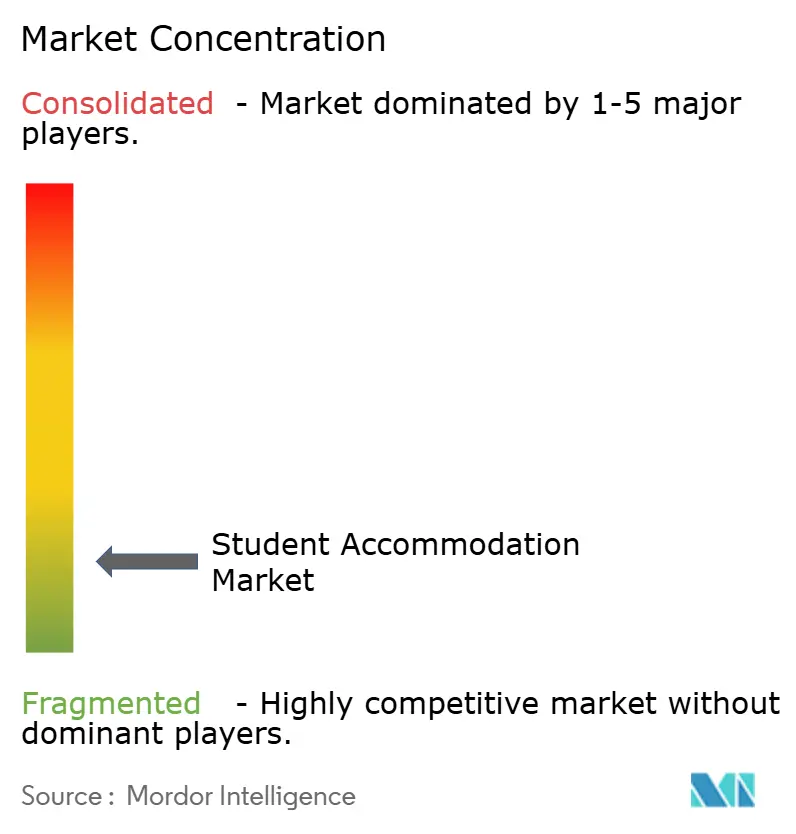

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Student Accommodation Market Analysis by Mordor Intelligence

The Student Accommodation Market size is projected to expand from USD 12.40 billion in 2025 and USD 14 billion in 2026 to USD 24.40 billion by 2031, registering a CAGR of 11.75% between 2026 to 2031.

Rising cross-border enrollment continues to support the student accommodation market, even as visa changes shift demand between countries rather than reducing it outright. Chronic shortages of purpose-built beds in major university cities are keeping occupancy high and sustaining investor interest in the student accommodation market. Institutional capital is also moving more decisively into scaled platforms, which is increasing consolidation, expanding secondary transactions, and improving operating efficiency across the student accommodation market. At the same time, construction cost pressure, labor shortages, and longer planning timelines are slowing new supply, which supports pricing power for existing assets. This leaves the clearest opportunity for operators in cities to add well-managed beds near high-enrollment institutions while also adapting formats to local affordability needs.

Key Report Takeaways

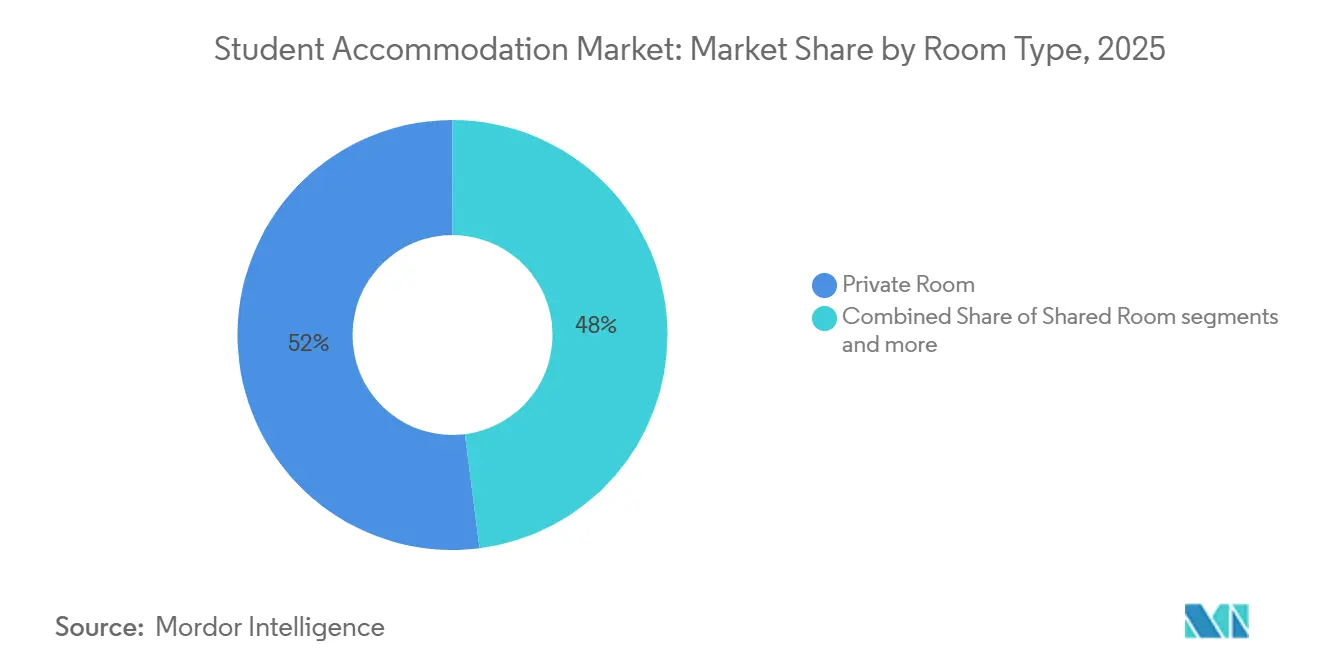

- By room type, private rooms held a 52% share in 2025, while shared rooms are projected to grow at a 12.8% CAGR through 2031.

- By type of institution, higher education accounted for 88% of the student accommodation market size in 2025, while the other segment is projected to grow at a 13.2% CAGR through 2031.

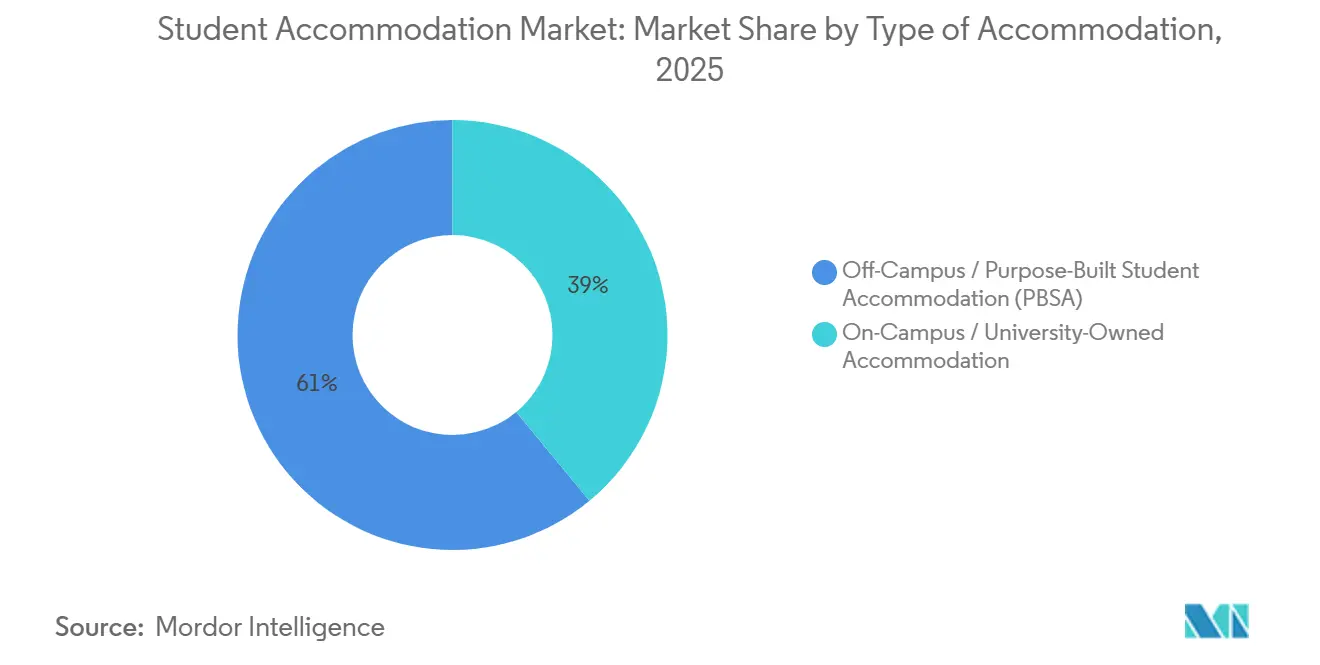

- By type of accommodation, off-campus / purpose-built student accommodation (PBSA) accounted for 61% of the student accommodation market in 2025 and is projected to grow at a 12.4% CAGR through 2031.

- By student type, international students held 58% of the student accommodation market share in 2025 and are projected to grow at a 12.0% CAGR through 2031.

- By geography, Europe held a 33% share in 2025, while Asia-Pacific is projected to grow at 13.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Student Accommodation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising International Student Mobility Increases Accommodation Demand | +3.5% | Global | Medium term (2-4 years) |

| Growth of Purpose-Built Student Accommodation Expands Market Supply | +2.5% | Global, concentrated in Europe and APAC | Long term (≥ 4 years) |

| Urbanization of Higher Education Hubs Supports Student Housing Demand | +1.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Preference for Safe and Secure Living Drives Premium Accommodation Adoption | +1.2% | North America and Europe | Medium term (2-4 years) |

| Expansion of Private Higher Education Providers Boosts Student Enrollment | +1.0% | Global | Long term (≥ 4 years) |

| Rising Demand for Value-Added Amenities Enhances Premium Accommodation Uptake | +0.8% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising International Student Mobility Increases Accommodation Demand

International enrollment remains the clearest demand engine for the student accommodation market across major education destinations. The United States hosted 1.18 million international students in the 2024-2025 academic year, which confirmed that global study demand remained strong even before the next intake cycle[1]Institute of International Education, “Open Doors 2025 Report on International Educational Exchange,” IIE, iie.org. Visa tightening in parts of North America created friction in 2025, but the broader pattern still points to redistribution across destinations rather than a collapse in student flows. Demand is instead shifting toward destination markets with more accessible visa pathways, established university ecosystems, and limited student housing supply, suggesting the student accommodation market is being reshaped by corridor shifts rather than weaker interest in overseas education. Operators near highly ranked universities are better protected in this environment because international students continue to prioritize academic reputation, safety, and housing certainty when selecting both destination and residence. This continues to support the student accommodation market through mobility growth, even when individual countries face temporary policy or enrollment disruptions.

Growth of Purpose-Built Student Accommodation Expands Market Supply

The student accommodation market continues to attract institutional capital because purpose-built stock offers scale, operating control, and stronger income visibility than fragmented private rentals. United Kingdom PBSA (Purpose-Built Student Accommodation) investment reached GBP 4.3 billion (USD 5.6 billion) in 2025, indicating that investor appetite remained strong despite a more challenging financing backdrop[2]The Landlord Association, “UK PBSA Investment Hit £4.3bn in 2025,” The Landlord Association, landlordassociation.org.uk. JP Morgan Asset Management entered a joint venture with I Live to develop a EUR 1.5 billion (USD 1.65 billion) student apartment portfolio in Germany, showing that underpenetrated markets with low organized supply are attracting long-term institutional capital. In the United States, American Campus Communities and Northeastern University broke ground in February 2026 on a 1,200-bed residence hall, highlighting how public-private partnerships are expanding professionally managed student housing in major university markets. Greystar also expanded its presence through portfolio acquisitions in Ireland and Spain, which reflects a broader push to build multi-country platforms in supply-constrained university cities. This pattern matters because professionally managed purpose-built student accommodation is becoming the preferred route for both universities and investors seeking dependable delivery and operational performance. As a result, the student accommodation market is moving toward larger platforms with stronger development pipelines, better refinancing access, and wider geographic reach.

Urbanization of Higher Education Hubs Supports Student Housing Demand

The student accommodation market is also benefiting from the concentration of students in large urban education corridors where land is limited, and supply takes longer to add. In China, Hubei University acquired 352 residential units for CNY 198 million (USD 27 million), to create 2,800 beds, while 3 universities affiliated with the Ministry of Education prepared a combined CNY 706 million (USD 97 million) budget for additional stock acquisitions. Those moves show that dense university cities are now using conversion strategies to secure new campus land as securing new campus land becomes harder. They also indicate that demand is strong enough for institutions to compete directly for existing residential inventory rather than wait for slower ground-up development. This gives private operators a clear signal that adaptive reuse can become a viable entry strategy in fast-growing education hubs. The student accommodation market is therefore becoming more dependent on urban redevelopment capacity and local execution speed than on campus expansion alone.

Preference for Safe and Secure Living Drives Premium Accommodation Adoption

Resident priorities are changing the product mix within the student accommodation market. A 2025 survey by uForis found that WiFi reliability, private bedrooms, and physical security features were the 3 most important housing priorities for student residents, ahead of more discretionary lifestyle features. This means operators are seeing stronger returns from spending on broadband capacity, secure access systems, and practical study environments. It also helps explain why professionally managed Purpose-Built Student Accommodation (PBSA) continues to gain share over informal rentals that cannot offer the same level of consistency. Safety and reliability matter even more to international students and first-year cohorts, further supporting premium positioning in the student accommodation market. Over time, this preference should continue lifting occupancy and pricing for assets that combine functional quality with accessible rent points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital and Long Payback Periods Limit New Developments | -2.0% | Global | Long term (≥ 4 years) |

| Regulatory and Zoning Complexity Delays Student Housing Projects | -1.5% | North America and Europe | Medium term (2-4 years) |

| Affordability Pressures in Major Cities Constrain Student Housing Demand | -1.2% | North America and Europe | Medium term (2-4 years) |

| Seasonal Occupancy and Academic Cycles Create Revenue Volatility | -0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital and Long Payback Periods Limit New Developments

High capital intensity remains one of the clearest limits on supply growth in the student accommodation market. In the United States, mid-2025 tariffs doubled the cost of steel and aluminum, affecting Heating, Ventilation, and Air Conditioning (HVAC) systems and machinery and raising development costs across new student housing projects. Rising insurance premiums, especially in coastal markets, and ongoing skilled labor shortages added further pressure to project viability and developer margins. United States student housing deliveries were projected to fall 42% to nearly 22,000 new beds in 2025, showing how quickly cost inflation can suppress new supply. This creates barriers for smaller developers who lack strong access to funding, established operating platforms, or existing land positions. For the student accommodation market, the result is slower bed creation but stronger economics for scaled operators that can still build or reposition assets.

Regulatory and Zoning Complexity Delays Student Housing Projects

Planning rules and local approvals remain a meaningful friction point for the student accommodation market in several major countries. In California, Assembly Bill 893 was enacted in 2025 to streamline housing approvals in campus development zones, which reflected growing recognition that approval bottlenecks were worsening student housing shortages. Texas also passed Senate Bill 1567 in 2025 to limit how college-town municipalities can restrict occupancy in shared student rentals. These reforms matter because they show that lawmakers increasingly view zoning complexity as a supply problem rather than just a local planning issue. Even so, compliance steps, appeals, and discretionary reviews still stretch project timelines and increase financing risk. That keeps the student accommodation market more favorable to large operators that can absorb delays and navigate complex permitting systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Room Type: Shared Rooms Signal an Affordability-Driven Demand Shift

Private rooms accounted for 52% of the student accommodation market in 2025, making them the largest room format by revenue. This lead reflects the strong preference for privacy, secure access, and predictable living conditions in professionally managed assets. A 2025 uForis survey found that private bedrooms were among the most important housing priorities for student residents, which supports continued demand for this format[3]uForis, “The Resident Perspective, Student Survey & Operator/Developer Insights on New Developments 2025,” uForis, uforis.com. In supply-constrained markets such as the United Kingdom, occupancy in premium student housing remained very high, reinforcing the case for private room formats in mature university cities. The student accommodation industry has therefore continued to place a structural premium on private rooms, especially in cities with strong international demand and limited bed availability.

Shared rooms are still the fastest-growing room format, with a 12.8% CAGR projected through 2031, suggesting a stronger affordability response in the student accommodation market. This growth is concentrated in markets where income levels, tuition burdens, and limited supply make single-occupancy formats harder to access. It suggests that room preferences are being shaped not only by lifestyle expectations but also by local price capacity and market maturity. Entire place or studio units remain a narrower premium option, with demand centered on postgraduate residents and international students seeking more independence. For operators, the room-type mix is becoming a portfolio decision rather than a single-format choice. The student accommodation market is therefore likely to sustain a dual model, with private rooms leading mature corridors and shared formats driving expansion in more price-sensitive locations.

By Type of Institution: Higher Education Anchors Demand, While Others Segments Open New Frontiers

Higher education held 88% of the student accommodation market in 2025, which shows how closely the sector still tracks university enrollment, campus reputation, and gateway-city demand. This dominance also reflects the scale advantage of degree-granting institutions, where student flows are larger and residence demand is more predictable from year to year. American Campus Communities highlighted this operating logic through its University of Michigan South 5th Residential project, a 2,300-bed development scheduled for Fall 2026 that shows the size and visibility of campus-linked demand in major university markets. In practice, higher education remains the core demand base because universities generate the deepest leasing pools, the strongest partnership pipelines, and the most financeable location profiles. This keeps the student accommodation market centered on established education hubs where institutional operators can scale efficiently.

The others segment is projected to grow at 13.2% CAGR through 2031, making it the fastest-growing institution category in the student accommodation market. This category includes vocational training, professional education, and hybrid learner groups that do not fit the traditional 4-year university model. Its rise matters because it broadens demand into cities and submarkets that are not defined only by flagship universities. It also supports flexible operating models where residents may include trainees, researchers, interns, or young professionals with education-linked housing needs. K-12 remains a smaller and more regulated category, which limits its influence on overall sector growth. The student accommodation industry is therefore gaining a wider demand base, even though higher education will remain the central anchor through the forecast period.

By Type of Accommodation: Off-Campus / Purpose-Built Student Accommodation (PBSA) Consolidates as the Dominant Investment Vehicle

Off-campus or purpose-built student accommodation (PBSA) captured 61% of the student accommodation market share in 2025 and is also projected to grow at a 12.4% CAGR through 2031. This alignment between current scale and future growth shows that the student accommodation market increasingly favors professionally managed off-campus stock over fragmented informal supply. The model combines campus access, operational control, and shared amenities without placing all capital demands directly on universities. Institutional confidence in this format remained visible in 2025 and 2026 through large portfolio transactions and platform expansion by major operators. Edifice Invest also noted that retrofit conversions in the United Kingdom can be 40% to 60% cheaper than new builds, which supports faster off-campus supply creation amid difficult construction economics.

On-campus or university-owned accommodation still accounted for 39% of revenue in 2025, which means it remains an important base layer in the student accommodation market. This format continues to matter because universities want more control over resident experience, student support, and campus integration. It is also becoming more dependent on partnership structures rather than direct balance-sheet expansion by institutions alone. American Campus Communities and Northeastern University broke ground on a 1,200-bed residence hall in February 2026, demonstrating how on-campus growth is increasingly delivered through structured models. Even so, off-campus / purpose-built student accommodation (PBSA) appears better placed for large-scale expansion because it can serve multiple campuses, attract wider capital pools, and adapt more quickly to local housing shortages. The student accommodation market is therefore likely to keep shifting toward off-campus formats, while on-campus supply remains strategically important in selected university partnerships.

By Student: International Cohort Drives Revenue Premium Despite Near-Term Enrollment Headwinds

International students accounted for 58% of the student accommodation market in 2025, indicating that their revenue contribution exceeded their share of total enrollments in many destination markets. This reflects a structural rent premium because international residents are more likely to choose private rooms, studios, and professionally managed buildings during their first housing search. The United States recorded 1.18 million international students in the 2024-2025 academic year, confirming the continued scale of this cohort despite policy uncertainty in parts of the market. The segment is also projected to grow at a 12.0% CAGR through 2031, suggesting continued confidence that global study demand will remain resilient even as visa rules tighten in individual countries. For operators, international residents are especially valuable because they often lease earlier, stay in higher-yield room types, and place greater emphasis on secure and branded accommodation.

Domestic students accounted for 42% of revenues in 2025, which makes them a large but more price-sensitive resident group in the student accommodation market. This cohort provides stable baseline demand, but it is more exposed to rent affordability and commuting trade-offs, especially in expensive university cities. As a result, domestic demand supports a greater mix of shared rooms, older stock, and value-led formats than the international segment. It also makes the pricing strategy more sensitive in markets where household incomes do not keep pace with rents for premium purpose-built student accommodation (PBSA). Even when occupancy remains strong, operators often need a sharper product and price match to sustain domestic absorption. The student accommodation market, therefore, depends on international students for revenue uplift, while domestic students remain essential for depth, resilience, and long-run occupancy balance.

Geography Analysis

Europe held a 33% of the student accommodation market in 2025, making it the largest regional contributor by revenue. The region benefits from mature university systems, deep investor familiarity with purpose-built student accommodation, and persistent undersupply in several major cities. In the United Kingdom, occupancy in premium student housing remained at 97% to 98%, indicating strong leasing resilience in a highly constrained market. Europe also remains attractive because operators can scale across several countries while staying within well-established higher education corridors. Germany, France, Spain, and the Netherlands continue to gain strategic relevance as demand broadens beyond the oldest and most mature purpose-built student accommodation markets.

Asia-Pacific is projected to grow at 13.5% CAGR through 2031, making it the fastest-growing regional segment in the student accommodation market. India remains one of the clearest long-run opportunities because formal supply is still well below current demand, which keeps institutionalization room high. That direction became more apparent in 2026, when HDFC Capital Advisors and Curated Living Solutions launched India’s first institutional rental housing platform with an initial corpus of INR 1,000 crore (USD 115 million). China is also showing an important supply response, with universities using residential acquisitions and conversions to add dormitory capacity in dense urban locations. Across the Asia-Pacific region, the student accommodation market is being supported by both rising enrollments and a clearer shift toward institutional capital and more formal operating models.

North America accounted for a material share of global revenue in 2025, as the United States combines large enrollment volumes with a well-developed base of specialized operators. The region remains attractive, but its growth is being shaped by supply constraints, development costs, and policy shifts that can alter student flows from one cycle to the next. Canada faced a more difficult intake setting after lower study permit limits in 2026, which redirected attention toward stronger institutions and better-located assets. South America, the Middle East, and Africa remain smaller in current scale. However, they continue to present long-run potential, with private education expanding and the organized student housing supply still limited.

Mordor Intelligence provides coverage of the united kingdom student accommodation market across other key regional markets, including Asia and Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to India, United Kingdom, Germany, and United States incorporating local coverage and market participation, as required.

Competitive Landscape

The student accommodation market is fragmented, with a large number of institutional investors, specialist operators, universities, and regional providers competing across different countries and university cities. Although several international platforms have expanded their portfolios, no single operator holds a dominant global position because competition remains dispersed across national markets with different regulatory environments, ownership structures, and student demand patterns. Scale continues to provide advantages in financing, operations, and university partnerships, but local market expertise and city-level execution remain equally important for winning and managing assets.

Leading operators are nevertheless strengthening their positions through selective acquisitions and development partnerships. Greystar expanded into Denmark in May 2025 through the acquisition of a 1,758-bed Copenhagen portfolio before extending its presence in Ireland in December 2025 with a 724-bed acquisition valued at USD 115.5 million. Unite Group acquired Empiric Student Property in January 2026, adding 7,700 beds across 68 properties in 22 United Kingdom cities while also progressing joint ventures with Newcastle University and Manchester Metropolitan University for 4,300 additional beds. Similarly, Yugo acquired Campus Advantage in September 2025, creating a combined portfolio of nearly 40,000 beds across 88 properties in the United States. These developments illustrate that consolidation is occurring among leading operators, but it has not fundamentally changed the fragmented structure of the global market.

Significant competitive opportunities remain because many countries continue to have limited purpose-built student accommodation (PBSA) supply and rely on a mix of universities, private landlords, and regional operators. Providers that can tailor accommodation formats, affordability, and resident services to local market needs are often better positioned than those pursuing scale alone. As investment continues to expand into underpenetrated university markets, competition is expected to remain fragmented, with regional specialization, operational quality, and targeted expansion continuing to shape long-term competitive success.

Student Accommodation Industry Leaders

Greystar Real Estate Partners

Unite Students

Scape

GSA Group

The Social Hub

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Greystar expanded its Spanish purpose-built student accommodation (PBSA) portfolio to approximately 3,000 beds through the acquisition of two assets in Salamanca and Valencia (approximately 1,600 beds) from Straco Capital, with all properties operating under the Canvas brand.

- February 2026: American Campus Communities and Northeastern University broke ground on a 1,200-bed, 23-story residence hall at 840 Columbus Avenue in Boston. Scheduled for completion in Fall 2028, the project is the largest on-campus equity development in the company's history and is targeting LEED Gold certification.

- February 2026: Unite Group announced joint ventures with Newcastle University and Manchester Metropolitan University to develop 4,300 student beds between 2028 and 2030, further strengthening its university partnership strategy.

- December 2025: Greystar acquired a 724-bed purpose-built student accommodation (PBSA) portfolio in Dublin and Galway from EQT Exeter for approximately EUR 105 million (USD 115.5 million), expanding its Irish portfolio to more than 1,700 beds under the Canvas brand.

Global Student Accommodation Market Report Scope

The Student Accommodation Market Report is Segmented by Room Type (Entire Place / Studio, Private Room, and Shared Room), Type of Institution (K-12, Higher Education, and Others), Type of Accommodation (On-Campus / University-Owned Accommodation and More), Student (Domestic and International), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Entire Place / Studio |

| Private Room |

| Shared Room |

| K-12 (School Education) |

| Higher Education (Colleges & Universities) |

| Others |

| On-Campus / University-Owned Accommodation |

| Off-Campus / Purpose-Built Student Accommodation (PBSA) |

| Domestic |

| International |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| SouthEast Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Room Type | Entire Place / Studio | |

| Private Room | ||

| Shared Room | ||

| By Type of Institution | K-12 (School Education) | |

| Higher Education (Colleges & Universities) | ||

| Others | ||

| By Type of Accommodation | On-Campus / University-Owned Accommodation | |

| Off-Campus / Purpose-Built Student Accommodation (PBSA) | ||

| By Student | Domestic | |

| International | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| SouthEast Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for student accommodation?

The student accommodation market is projected to reach USD 24.4 billion by 2031 from USD 14.0 billion in 2026, growing at an 11.75% CAGR over 2026-2031.

Which room format is growing fastest in student housing?

Shared rooms are projected to grow the fastest at 12.8% CAGR through 2031, even though private rooms held the largest 52% share in 2025.

Why are international students so important to student housing revenues?

International students held 58% of revenue in 2025 and tend to lease earlier, prefer professionally managed housing, and choose higher-yield room formats.

Which accommodation format leads global demand?

Off-campus / purpose-built student accommodation (PBSA) led with 61% share in 2025 and is also the fastest-growing accommodation type at 12.4% CAGR through 2031.

Which region is expanding the fastest for student housing investors?

Asia-Pacific is the fastest-growing region with a projected 13.5% CAGR through 2031, supported by supply shortages and rising institutional interest.

Page last updated on: