Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.26 Billion |

| Market Size (2026) | USD 10.79 Billion |

| Market Size (2031) | USD 13.91 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Hospitality Market Analysis by Mordor Intelligence

The Morocco Hospitality Market size market is expected to grow from USD 10.26 billion in 2025 to USD 10.79 billion in 2026 and is forecast to reach USD 13.91 billion by 2031 at 5.21% CAGR over 2026-2031.

Sustained inbound demand from Europe, rapid expansion of low-cost air routes, and a USD 5–6 billion pre-World-Cup infrastructure program underpin the growth trajectory. Government tax incentives, land concessions, and loan guarantees embedded in Vision 2026 continue to stimulate fresh supply while maintaining investor confidence. The push toward digital nomad visas and longer-stay formats is reshaping accommodation mixes, and extended-stay demand is offering new revenue streams. Lastly, foreign chains’ multi-brand strategies are accelerating professional standards and technology adoption across the Morocco hospitality market[1]Government of Morocco, “Tourism Sector Creates 25K Jobs in 2023,” maroc.ma. .

Key Report Takeaways

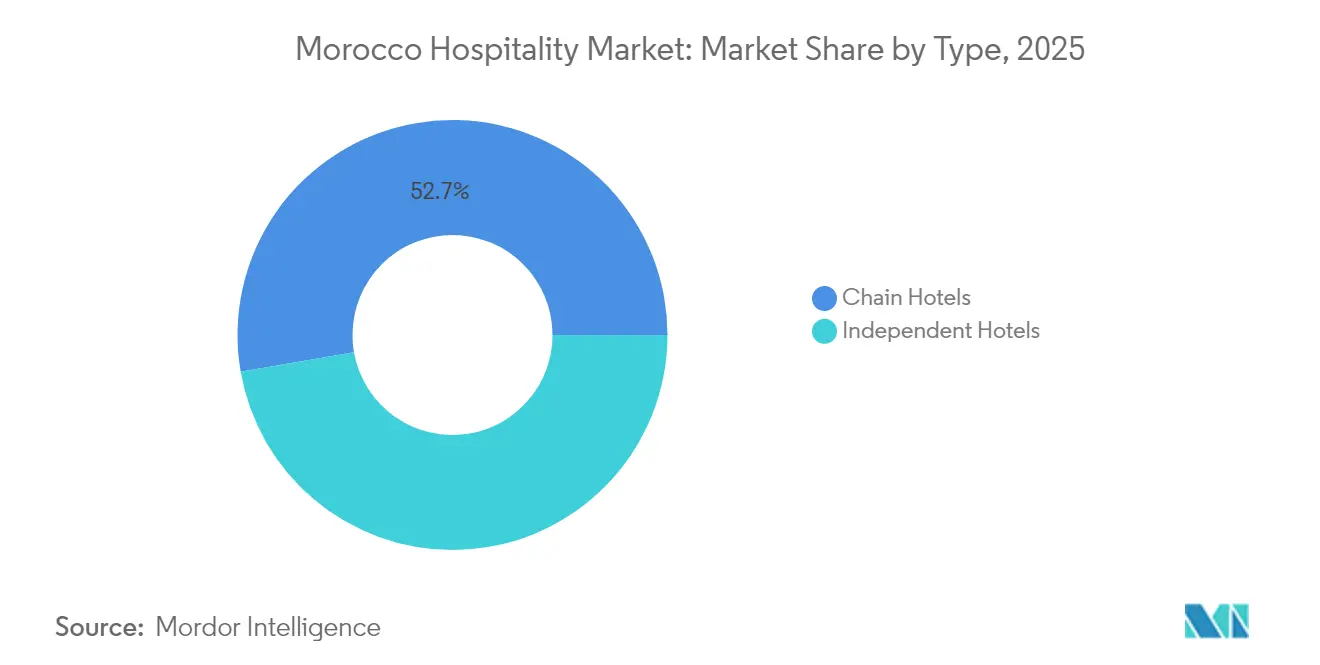

- By type, chain hotels accounted for 52.74% of the Morocco hospitality market share in 2025 and are expected to remain the fastest-growing sub-segment with a CAGR of 9.22% between 2026 and 2031.

- By accommodation class, mid & upper-mid-scale properties represented 39.66% of the Morocco hospitality market share in 2025, while service apartments are projected to grow the fastest with a CAGR of 10.74% during the forecast period.

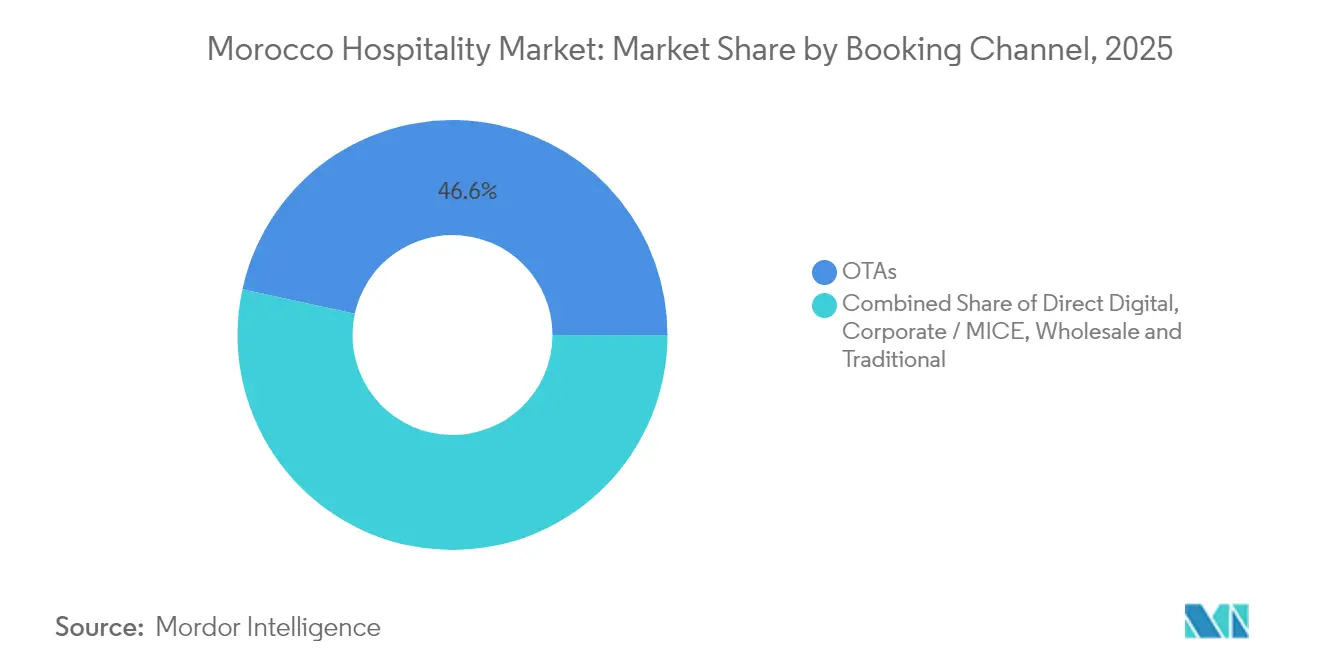

- By booking channel, OTAs captured 46.58% of the Morocco hospitality market size in 2025, but direct digital channels are forecasted to expand at the strongest pace, recording a CAGR of 12.08% through 2031.

- By geographic region, Marrakech-Safi contributed 26.92% of the Morocco hospitality market share in 2025, whereas Souss-Massa is anticipated to be the fastest-growing region with a CAGR of 9.25% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Morocco Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising inbound tourist arrivals from Europe | +1.2% | Marrakech-Safi, Casablanca-Settat, Tangier-Tétouan-Al Hoceima | Medium term (2–4 years) |

| Vision 2026 tax incentives & hotel subsidies | +0.9% | National, focus on Casablanca, Rabat, Agadir | Short term (≤ 2 years) |

| Low-cost airline route expansion | +0.8% | Souss-Massa, Marrakech-Safi, Tangier-Tétouan-Al Hoceima | Medium term (2–4 years) |

| Growth of MICE tourism | +0.6% | Casablanca-Settat, Marrakech-Safi | Medium term (2–4 years) |

| Digital-nomad visa effect | +0.4% | Marrakech-Safi, Casablanca-Settat, Rabat-Salé-Kénitra | Long term (≥ 4 years) |

| 2030 World Cup infrastructure program | +0.7% | National (host cities) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Inbound Tourist Arrivals from Europe

Western Europe supplied the bulk of Morocco’s 17.4 million international visitors in 2024, and airline seat capacity from France, Spain, and the United Kingdom climbed 19% for winter 2024 schedules[2]OAG Aviation Worldwide Limited, “Morocco Tourism: A Closer Look at Growth Trends,” OAG, April 2, 2025. A younger demographic seeking authentic medina experiences is sustaining premium room rates, especially across heritage riads in Marrakech and boutique properties in Fez. Favorable post-Brexit travel dynamics have bolstered British arrivals, stimulating higher-margin occupancy during traditional low seasons. Forward bookings indicate that the influx will further stabilize weekday demand outside core holiday windows, improving yield management for coastal resorts and city hotels. These visitor flows are pivotal to the Morocco hospitality market, keeping RevPAR momentum intact across upscale segments.

Government Vision 2026 Incentives & Hotel-Pipeline Subsidies

Vision 2026 earmarks MAD 6.1 billion for tourism infrastructure, complemented by the GO SIYAHA and Cap Hospitality programs that provide targeted renovation grants and soft-loan packages[3]Fitch Solutions BMI, “Morocco’s Tourism Arrivals Will Continue On A Robust Post Earthquake & Pandemic Growth Trajectory,” Fitch Solutions (BMI), February 6, 2024. A construction pipeline of 8,579 rooms across 58 projects now shows a 72% completion rate, narrowing accommodation gaps in Fez, Agadir, and Tangier. Mandatory sustainability benchmarks embedded in the scheme are attracting ESG-focused investors and driving hotel operators to deploy efficient utilities, renewable energy, and water-reuse technologies. The incentives have shortened development timelines, prompting mid-scale openings in secondary cities and diversifying the overall Morocco hospitality market.

Expansion of Low-Cost Airlines & New International Routes

Ryanair’s goal of 10 million annual passengers by 2027 and its newly granted cabotage rights are reshaping domestic air connectivity. Parallel capacity boosts from EasyJet and charter carriers have introduced more than 200,000 seats for Agadir and Marrakech during 2025. These route additions reduce over-reliance on gateway hubs and spread tourist traffic across emerging beach and desert destinations. Direct Madrid and Lanzarote flights to Dakhla have doubled the airport’s capacity, positioning the southern Atlantic coast for surf and adventure tourism. Airline expansion thus underpins the Morocco hospitality market by mitigating seasonality and widening the visitor base.

Rapid Growth of MICE Tourism in Casablanca & Marrakech

Casablanca’s finance districts and Marrakech’s convention facilities are capitalizing on Morocco’s strategic proximity to Europe and sub-Saharan Africa. The new Palais des Congrès wing in Marrakech will add flexible halls linked to five-star hotels, while Casablanca’s inventory of ballrooms and boardrooms already accommodates conferences of 800-plus delegates. Weekday group demand fills shoulder-season gaps, raising average daily rates for upscale city properties. Government-backed promotion in Asian source markets, including roadshows in Seoul, is broadening corporate pipelines beyond Europe. MICE activity is forecast to lift hotel food-and-beverage revenue lines and accelerate premium ancillary spending.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High seasonality and occupancy volatility | -0.8% | Coastal resorts, mountain areas (Souss-Massa, Marrakech-Safi) | Short term (≤ 2 years) |

| Euro–MAD FX risk on RevPAR | -0.6% | National, strongest in Europe-reliant regions | Medium term (2–4 years) |

| Water-scarcity compliance costs | -0.4% | Coastal and desert resorts, southern regions | Long term (≥ 4 years) |

| Skilled-labor migration to GCC | -0.3% | Luxury and upscale segments nationwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Seasonality Causing Occupancy Volatility

Peak summer and winter weeks still determine the earnings calendar for beach and ski resorts, yet domestic travelers are booking shorter stays due to rising costs. Ramadan timing further compresses demand, pushing March 2025 RevPAR down 11.2% across monitored properties[4]Hospitality Net, “Middle East & Africa Hotel Performance Update,” Hospitality Net, April 30, 2025. Staffing models remain under strain as operators juggle part-time contracts and overtime surges, which ultimately inflate payroll ratios. In Souss-Massa, weekday occupancy dips below 40% outside JUL–SEP, forcing hotels to rely on discounting that pressures margins. Better airlift and MICE traffic are slowly countering but not fully eliminating the seasonal swings.

Euro–MAD FX Risk Impacting RevPAR

Currency volatility between the Euro and Moroccan Dirham creates margin pressure for hospitality operators, particularly those with significant European clientele or Euro-denominated cost structures. The dirham's fluctuations against major European currencies directly impact pricing competitiveness, with properties forced to absorb exchange rate movements or risk demand elasticity through price adjustments. Hotels with international management contracts or franchise fees denominated in foreign currencies face additional exposure through operational cost inflation. The challenge intensifies for luxury properties targeting European markets, where pricing must remain competitive with alternative Mediterranean destinations while maintaining profitability in local currency terms. Morocco's tourism revenue of over USD 11 billion demonstrates the sector's scale, but currency risk management becomes critical as the market matures, and competition intensifies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain Hotels Drive Market Consolidation

Chain brands held 52.74% of the Morocco hospitality market share in 2025 and are projected to expand at 9.22% CAGR through 2031, dwarfing the independent category. This leadership stems from multi-brand rollouts by groups such as Accor, which fields luxury, mid-scale, and economy flags to blanket price tiers, and Marriott, whose Africa pipeline assigns high strategic weight to Morocco. Chain operators leverage central purchasing, loyalty programs, and global sales offices to boost RevPAR, squeezing traditional family-run hotels on distribution reach.

Independent properties, still 44% of rooms, are increasingly yielding control through management or franchise agreements to access broader demand pipelines. Conversion-focused brands that promise minimal capex overlays are gaining traction for older riads and city hotels. Localization remains a differentiator for boutique independents, though sustainability certifications and experiential concepts are essential to remain relevant. Over the forecast, chain affiliations will further organize the Morocco hospitality market, improving operating benchmarks and investor confidence while preserving cultural authenticity via soft-brand models.

By Accommodation Class: Service Apartments Lead Growth Momentum

Service apartments logged the swiftest growth at 10.74% CAGR, propelled by digital nomads, long-stay corporate postings, and relocating diaspora professionals. Projects such as Citadines Almaz Casablanca opened in 2025 with 61 units designed for stays exceeding one month, and forward pipelines schedule additional openings in Marrakech, Rabat, and Tangier.

Mid & upper-mid-scale hotels retain the largest footprint with 39.66% of the Morocco hospitality market size in 2025, serving cost-conscious European travelers and rising domestic middle-income groups. Luxury hotels still capture 31.5% revenue, underpinned by heritage riads, golf resorts, and branded residential offerings. Budget and economy segments remain vital for domestic tour groups yet face margin pressure from labor costs and utilities. The shift toward flexible, residential-style units is expected to recalibrate product mixes across urban hubs and coastal clusters.

By Booking Channel: Direct Digital Acceleration Challenges OTA Dominance

OTAs kept 46.58% share in 2025 but their dominance is gradually tapering as hotels fortify websites with real-time rate engines and frictionless mobile payments. A 12.08% CAGR is projected for direct digital reservations through 2031, supported by enhancements in Arabic and French language interfaces and loyalty-member discounts. Corporate/MICE channels offer predictable weekday base business in Casablanca and Rabat, benefiting large room blocks and meeting-space rentals.

Wholesale and classic agent channels still move group tours through multi-city circuits but face commissions pressure. Hotels are now bundling ancillary perks—airport transfers, cultural tours, and spa credits—to nudge guests toward direct booking, reducing overall cost of sale and enriching data ownership, a critical edge within the Morocco hospitality market.

Geography Analysis

Marrakech-Safi maintains 26.92% share in 2025, its medina-centric experiences commanding premium nightly rates that anchor luxury performance. Growing airline frequencies from Paris, London, and Madrid further reinforce occupancy stability across seasons. New suburban resorts with integrated golf and wellness components are sparking incremental leisure segments, balancing the heritage-heavy stock within city walls. Convention center expansion set for 2025 will broaden weekday corporate utilization, smoothing revenue streams throughout the year.

Casablanca-Settat stands out as Morocco’s corporate powerhouse, bolstered by its role as the country’s commercial capital and home to a key hub airport. Major hotel refurbishments and pipeline additions dovetail with World Bank finance meetings and growing fintech events, strengthening mid-week occupancy. Waterfront projects are pairing office towers with hotels, blurring live-work-play lines and extending visitor stay durations beyond traditional business patterns.

Souss-Massa leads on future growth with a 9.25% CAGR over 2026-2031, hinged on Atlantic surf beaches, mild winters, and rising European charter lift. Large-scale integrated resorts in Taghazout and Imi Ouaddar are incorporating desalination plants to mitigate water shortages, aligning with stringent ESG mandates. Adventure sports, eco-tour circuits into the Anti-Atlas, and cultural festivals in Agadir are diversifying the appeal. The region’s evolving infrastructure feeds into a virtuous cycle of investment and demand, underscoring its outsize influence on the Morocco hospitality market.

Competitive Landscape

The leading players captured a significant share of 2024 market size, reflecting a moderately fragmented market with potential for selective consolidation. Accor holds the largest share, driven by its Sofitel, Novotel, Mercure, and ibis brands, which are strategically located in major cities and coastal destinations. Marriott follows with a strong presence through premium brands like Autograph Collection and Sheraton. Hilton maintains a solid position with its full-service and upscale focused-service offerings, particularly expanding in Rabat and Laâyoune.

Technology deployment around cloud-based property-management systems, AI-driven revenue optimization, and mobile keyless entry is widening the gap between branded chains and independents. Yet local owners still command valuable medina assets, often operating under asset-light management deals that secure global distribution while preserving Moroccan heritage aesthetics. White-space exists across secondary cities Oujda, Beni-Mellal, and Errachidia where limited international supply intersects rising domestic travel and infrastructure grants.

The upcoming 2030 World Cup imposes heightened compliance on safety, accessibility, and sustainability, favoring capital-strong hotel groups that can finance retrofits. Radisson’s target of 25 hotels and Ascott’s focused service-apartment play exemplify strategic entries leveraging extended-stay demand curves. Competitive rationalization is therefore set to tilt the Morocco hospitality market toward higher concentration, though boutique independents retaining authentic experiences will continue to serve profitable niche segments.

Morocco Hospitality Industry Leaders

AccorHotels

Marriott International

Hilton Worldwide

Radisson Hotel Group

Four Seasons Hotels & Resorts

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ascott Limited opened Citadines Almaz Casablanca (61 units) and signed Citadines Bab Tangier (130 units, 2027) to tap extended-stay demand.

- January 2025: Accor unveiled a multi-brand expansion roadmap featuring premium, lifestyle, and economy flags tailored for Casablanca, Marrakech, and Agadir.

- November 2024: Ryanair and ONMT inaugurated direct flights linking Dakhla with Madrid and Lanzarote, doubling airport capacity and integrating the southern coast into European circuits.

- December 2024: Hilton signed nine Moroccan properties across seven brands, adding 1,300+ rooms and 1,500 jobs.

Morocco Hospitality Market Report Scope

Hospitality involves welcoming and entertaining guests in a manner that ensures they feel well cared for. It leverages ambiance, service, and products or amenities to provide guests with the best experience possible. The hospitality market in Morocco is segmented by type and segment. By type, the market is segmented into chain hotels and independent hotels. By segment, the market is segmented into service apartments, budget and economy hotels, mid- and upper mid-scale hotels, and luxury hotels. The report offers market size and forecasts for the Moroccan hospitality industry in value (USD) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Casablanca-Settat |

| Marrakech-Safi |

| Rabat-Salé-Kénitra |

| Fez-Meknes |

| Tangier-Tétouan-Al Hoceima |

| Souss-Massa |

| Rest of Morocco |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Casablanca-Settat |

| Marrakech-Safi | |

| Rabat-Salé-Kénitra | |

| Fez-Meknes | |

| Tangier-Tétouan-Al Hoceima | |

| Souss-Massa | |

| Rest of Morocco |

Key Questions Answered in the Report

What is the projected CAGR for the Morocco hospitality market to 2031?

The market is set to grow at 5.21% CAGR, moving from USD 10.79 billion in 2026 to USD 13.91 billion in 2031.

Which accommodation class is growing the fastest?

Service apartments post the strongest outlook, advancing at 10.74% CAGR due to demand from digital nomads and long-stay corporate guests.

How much of the market do chain hotels currently hold?

Chain brands accounted for 52.74% of 2025 room revenues and are poised for further gains as pipeline projects open.

Which region offers the highest growth potential?

Souss-Massa leads with a forecast 9.25% CAGR, leveraging Atlantic beach development and new airlift.

Why are direct digital bookings gaining momentum?

Hotels are investing in seamless mobile websites and loyalty perks, spurring a 12.08% CAGR for direct channels while lowering OTA commissions.

What impact will the 2030 World Cup have on Morocco’s hospitality sector?

USD 5–6 billion in stadium and transport upgrades will expand capacity, attract new visitors, and stimulate long-term occupancy across host cities.

Page last updated on: