Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

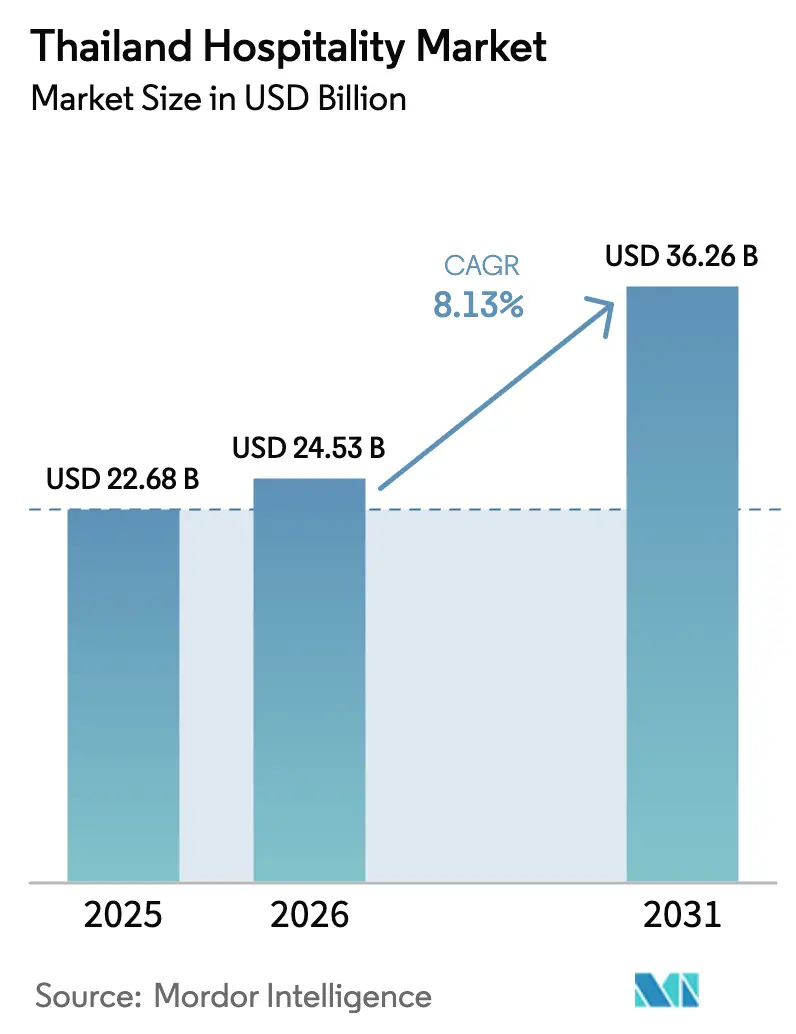

| Base Year Market Size (2025) | USD 22.68 Billion |

| Market Size (2026) | USD 24.53 Billion |

| Market Size (2031) | USD 36.26 Billion |

| Growth Rate (2026 - 2031) | 8.13% CAGR |

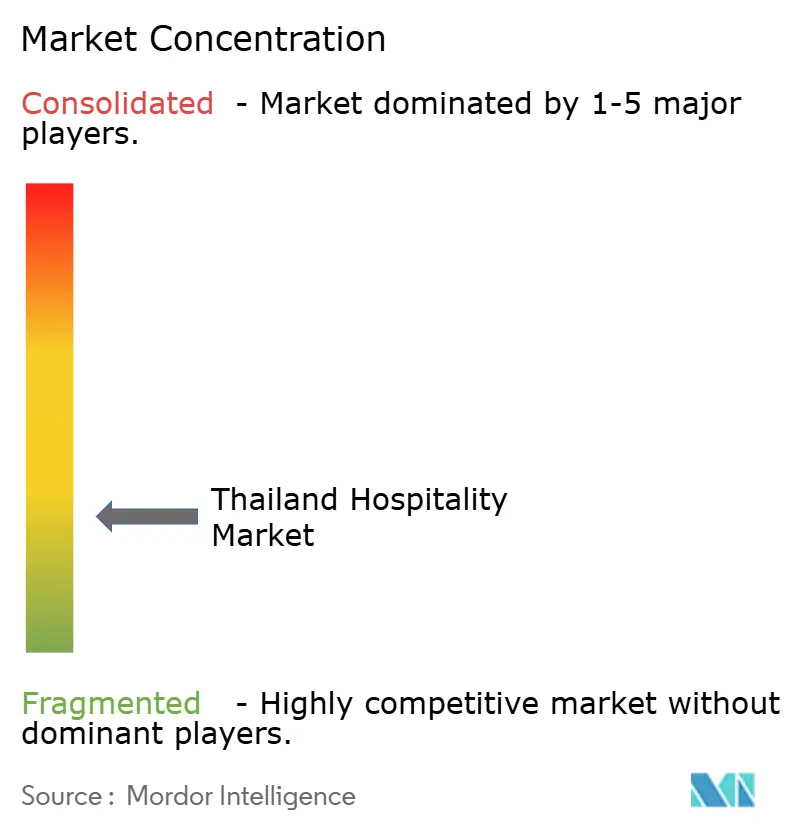

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Hospitality Market Analysis by Mordor Intelligence

The Thailand Hospitality Market size is expected to grow from USD 22.68 billion in 2025 to USD 24.53 billion in 2026 and is forecast to reach USD 36.26 billion by 2031 at 8.13% CAGR over 2026-2031.

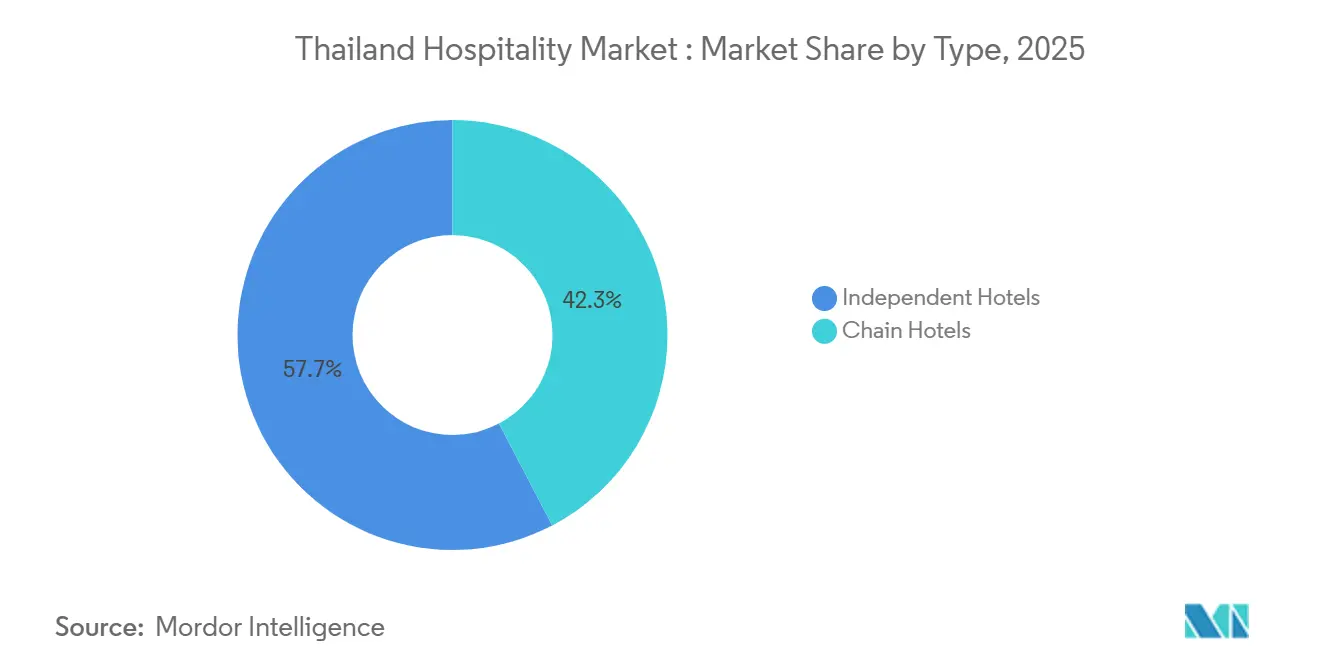

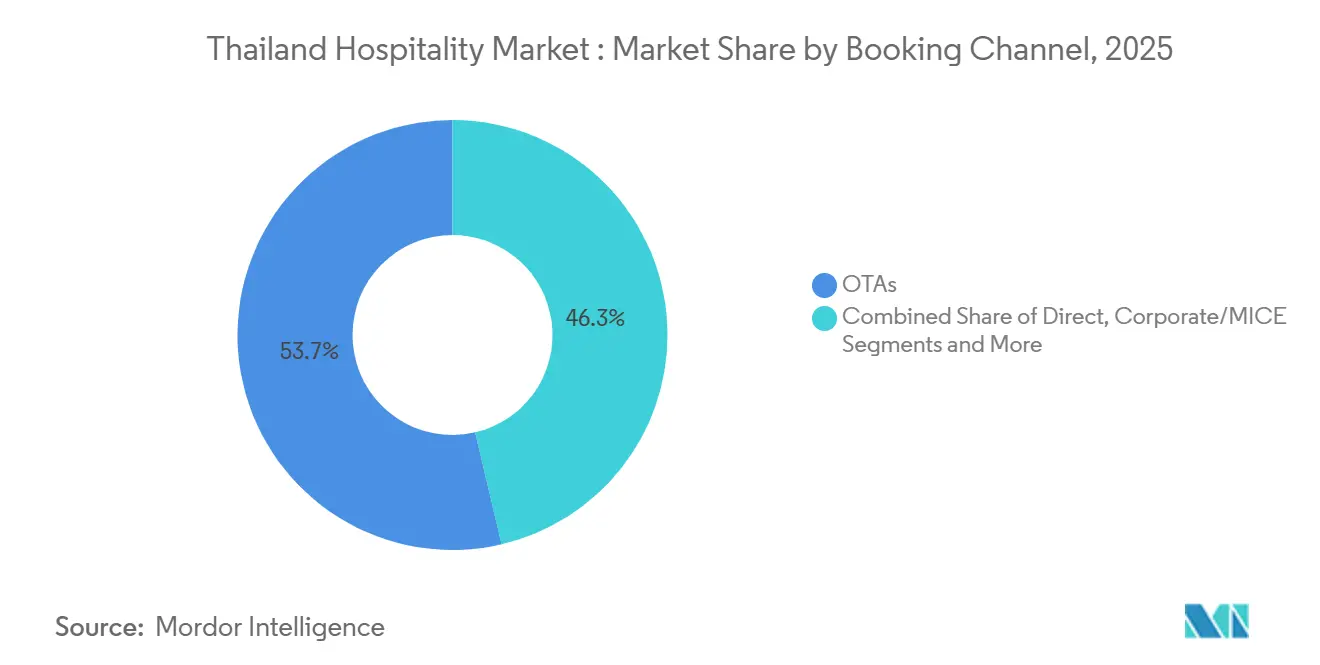

Independent hotels continue to hold a larger revenue base, while chain operators scale faster on asset-light models and brand systems that raise conversion and distribution efficiency. Rate-led growth concentrates in luxury room categories as pricing rises faster than consumer price inflation, while mid and upper-mid-scale properties sustain volume from business and domestic segments seeking consistent quality. Online travel agencies retain the largest booking share across the Thailand hospitality market, but direct digital gains momentum as owners invest in customer relationship management tools, loyalty, and more efficient rate distribution. Regional performance is anchored by Bangkok and the Central Plains for scale, with the Eastern Economic Corridor pipeline setting up Eastern Thailand as the fastest growth region in the second half of the decade.

Key Report Takeaways

- By type, independent hotels led with 57.65% of the Thailand hospitality market share in 2025; chain hotels recorded the fastest Thailand hospitality market size growth at a 9.66% CAGR through 2031.

- By accommodation class, mid and upper-mid-scale properties accounted for 47.58% share of the Thailand hospitality market size in 2025; luxury accommodations posted the fastest Thailand hospitality market share expansion at a 10.77% CAGR to 2031.

- By booking channel, online travel agencies captured 53.66% of the Thailand hospitality market share in 2025; direct digital bookings posted the fastest Thailand hospitality market size growth at an 11.66% CAGR through 2031.

- By geography, Bangkok and the Central Plains held 39.66% of the Thailand hospitality market share in 2025; Eastern Thailand is projected to post the fastest Thailand hospitality market size growth at a 9.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in long-haul arrivals from Russia and India | +1.8% | Global inflows to Bangkok, Southern Thailand, and Northern Thailand | Medium term (2-4 years) |

| Domestic tourism via “We Travel Together.” | +1.4% | National, higher in secondary cities | Short term (≤ 2 years) |

| Luxury ADR inflation outpacing CPI | +1.6% | Bangkok luxury, Phuket beachfront, Eastern coastal nodes | Medium term (2-4 years) |

| Accelerated hotel-REIT transactions | +1.1% | Bangkok, Phuket, Pattaya, selected secondary cities | Long term (≥ 4 years) |

| Niche lifestyle positioning, wellness, halal, plant-based | +0.9% | Northeastern medical hubs, secondary coasts | Long term (≥ 4 years) |

| Digital nomad visas lengthening stays | +1.2% | Bangkok, Chiang Mai, Phuket, spillover islands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in long-haul arrivals from Russia and India

Thailand’s recovery in foreign arrivals in 2024 and continuing momentum in 2025 strengthen the Thailand hospitality market as long-haul capacity returns and flight networks broaden. The country recorded 35.54 million foreign tourist arrivals in 2024, which supports higher room-night demand across city and beach destinations and encourages operators to sustain yield-focused pricing strategies during peak periods. Route renewals and longer-haul services into Bangkok and Phuket improve seat availability, while broader Asia-Pacific network expansion aids Thailand’s inbound traffic recovery in the medium term [1]EUROCONTROL.INT eurocontrol-aviation-trends-evolution-traffic-asia-pacific.pdf. Large operators cite stronger performance in European source markets in early 2025, signaling resilient long-haul demand at family-friendly beach properties favored by value-seeking travelers. [2]PRESS.ONYX-HOSPITALITY.COM https://press.onyx-hospitality.com/onyx-hospitality-group-unveils-2025-strategic-plan-aiming-to-lead-asean-hospitality-launch-onyxrt-reit-and-strengthen-core-brands This pattern supports balanced seasonality, with Russians and Europeans helping fill the high winter season in Southern Thailand, while regional travelers and Indians sustain city occupancy around retail and cultural attractions. The result is a more diversified demand mix that mitigates volatility and underpins networked growth plans of major brands that are expanding through management agreements and franchise deals.

Domestic tourism via “We Travel Together”

Revived domestic subsidies in 2025 improved secondary destination performance and unfolded a useful demand buffer for the Thailand hospitality market during shoulder months. The Tourism Authority of Thailand’s program architecture focuses on accommodation and dining subsidies delivered through digital channels, helping smaller cities capture incremental trips and weekend getaways that lift occupancy and food and beverage revenue. The policy aligns with a larger pattern of domestic travel normalization through 2024 and 2025 as mobility and household confidence recover, with program design nudging the discovery of lesser-visited provinces. Coordinated promotion with regional airlines and intercity transport can lift multi-city itineraries and reduce frictions for longer domestic loops, reinforcing network effects. The impact is more pronounced for independent mid-scale properties that package rooms with dining credits and local experiences tailored to Thai travelers. By spreading demand beyond a few hubs, subsidies also enable a more durable revenue base that can smooth seasonal swings for smaller hotels reliant on domestic business.

Luxury ADR inflation outpacing CPI

Price strength at the upper end has reshaped revenue composition in the Thailand hospitality market, with ADR expansion running ahead of headline inflation and widening the premium over mid-scale rates. Operators with luxury city and resort assets report higher room yields aided by strong high-spend segments and event-led demand, with one leading owner-operator citing a 2024 portfolio Average Daily Rate (ADR) of USD 167.8 per night and RevPAR of USD 120.0 on 72% occupancy. [3]ASSETWORLDCORP-TH.COM AWC Announces Record-Breaking 2024 Performance with Remarkable Growth, Doubling Assets in Five Years, Targeting Another Doubling in the Next Five with the Vision of "Building a Better Future" | Asset World Corporation. Luxury repositioning projects have targeted a threefold ADR uplift through brand elevation and asset renovation, anchored by partnerships with global brands that command rate premiums. The broader economic backdrop shows consumer prices growing modestly in 2024, a helpful setting for rate-led hospitality revenue gains. Beachfront resorts in Phuket and other coastal nodes also benefit from constrained prime supply relative to peak-season demand, reinforcing pricing power at the top of the market. This rate structure supports margin resilience in properties with robust food and beverage revenue, event facilities, and premium ancillaries that scale well with higher-spend guests.

Accelerated hotel-REIT transactions

The Thailand hospitality market is benefiting from REIT-led capital recycling that frees operators to expand through management contracts while owners secure stable rental cash flows. A prominent operator filed in mid-2025 to establish a leasehold hospitality REIT that includes four high-performing hotels, reinforcing the case for asset-light scaling based on branded management expertise. [4]PRESS.ONYX-HOSPITALITY.COM https://press.onyx-hospitality.com/onyx-hospitality-group-unveils-2025-strategic-plan-aiming-to-lead-asean-hospitality-launch-onyxrt-reit-and-strengthen-core-brands/. Thailand’s REIT framework requires at least USD 14.3 million initial investment in real estate and mandates distribution of at least 90% of net profits to qualify for corporate income tax exemption, while leasing and leverage rules help balance investor protections with operational flexibility. The policy mix has catalyzed portfolio transactions where operating companies retain management agreements and brands while disposing of real estate to investors seeking income stability. Leading Thai operators are also growing the share of managed hotels in their portfolios, which reduces capital intensity and speeds entry into new markets. This evolution improves returns on invested capital and creates more contestable white space for brand-led competition in secondary cities and emerging resort corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic skilled-labour shortages and payroll inflation | -1.5% | National, higher in large metros | Short term (≤ 2 years) |

| Elevated utility tariffs compressing margins | -0.9% | National, especially independents | Medium term (2-4 years) |

| Short-term rental oversupply is pressuring RevPAR | -1.1% | Bangkok, Phuket, emerging Chiang Mai, Pattaya | Medium term (2-4 years) |

| High dependence on Chinese arrivals | -0.7% | Bangkok, Southern Thailand, Northern Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic skilled-labour shortages and payroll inflation

A tight labor market continues to constrain service levels and stretch payroll budgets for operators across the Thailand hospitality market. Sector wage indices point to sustained upward pressure in accommodation and food services during 2025, elevating unit costs in a period of still-normalizing demand. International evidence on wage concentration confirms that hotel and restaurant workers in upper-middle-income economies remain clustered in the lower earnings quintiles, which complicates recruitment for skill-intensive roles and encourages out-migration from the sector. Operators respond by redesigning processes to cope with leaner staffing, but that approach has limits for premium service properties where guest expectations remain high. Pressure is more pronounced in city hotels that rely on higher daily throughput of front-office, housekeeping, and food service teams. For listed Thai hotel groups, margin narratives in 2025 point to increased room cost ratios and lower gross profit margins in cases where rate gains have not fully offset wage inflation.

Elevated utility tariffs compressing margins

Electricity tariffs remain a large, fixed expense for hotels, which operate around the clock across rooms, public areas, and back-of-house facilities. Under the Provincial Electricity Authority’s Schedule 5 for hotel-type users with average maximum demand above 30 kW, the tariff structure includes demand charges and Time of Use energy charges that can weigh on cash flow when occupancy softens. Minimum charge rules tied to prior-period demand exacerbate the burden during off-peak months, which hurts independent properties without scale advantages and energy management systems. Portfolio owners with centralized monitoring and capital for efficiency retrofits are better positioned to bring down kilowatt-hours per occupied room. By contrast, family-run hotels face steep upfront costs for retrofits, longer paybacks, and fewer options to participate in advanced green power programs. As a result, utility expenses compress gross operating profit for smaller players and raise the bar for breakeven occupancy across the hospitality industry in Thailand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent Hotels Dominate While Chains Accelerate

Independent hotels held 57.65% of the Thailand hospitality market by type in 2025. A tight labor market continues to constrain service levels and stretch payroll budgets for operators across the Thailand hospitality market. Sector wage indices point to sustained upward pressure in accommodation and food services during 2025, elevating unit costs in a period of still-normalizing demand. International evidence on wage concentration confirms that hotel and restaurant workers in upper-middle-income economies remain clustered in the lower earnings quintiles, which complicates recruitment for skill-intensive roles and encourages out-migration from the sector. Operators respond by redesigning processes to cope with leaner staffing, but that approach has limits for premium service properties where guest expectations remain high. Pressure is more pronounced in city hotels that rely on higher daily throughput of front-office, housekeeping, and food service teams. For listed Thai hotel groups, margin narratives in 2025 point to increased room cost ratios and lower gross profit margins in cases where rate gains have not fully offset wage inflation.

By Accommodation Class: Luxury Surges While Mid-Scale Anchors Volume

Mid and upper-mid-scale properties held 47.58% share in 2025, anchoring volume for business travelers and domestic tourists across the Thailand hospitality market. The category’s appeal rests on reliable quality at moderate price points, which supports weekday corporate stays and weekend domestic trips with balanced ancillary spend. Stronger city demand and conference activity help mid-scale hotels deploy meeting space and food and beverage more effectively. At the same time, the luxury class shows the fastest growth at a 10.77% pace, helped by premium international segments and experience-driven travelers. Operators pursuing luxury repositioning report rate gains that significantly outstrip the rest of the market, with leading owners delivering 2024 ADR at 5,873 THB (USD 167.8) and portfolio-wide RevPAR advancement.

Luxury growth reflects strong ancillary spending and a willingness to pay for wellness, privacy, and design-led experiences within the Thailand hospitality market. Spending profiles of international guests also support upselling into dining, spa, and activities that raise per-guest revenue beyond room rates. Supply discipline around true five-star developments, higher build standards, and brand thresholds preserves pricing power at the top of the market. Renovation-led repositioning, such as city landmark conversions into luxury flags, demonstrates how strategic capex can triple achievable ADR when paired with global brand equity and product upgrades. In aggregate, the result is a tiered structure where mid-scale carries room-night volume, and luxury captures disproportionate revenue growth across the hospitality industry in Thailand.

By Booking Channel: OTAs Lead While Direct Digital Gains

Online travel agencies held the largest booking share at 53.66% in 2025, which underscores their reach and conversion advantages in a fragmented market. For independents and smaller chains, OTAs deliver demand aggregation, global language support, and payment capabilities that are costly to build alone. However, direct digital is the fastest-growing channel at 11.66% growth as hotel operators raise investment in websites, mobile apps, first-party data, and loyalty. Thai groups that operate across hotels and large dining networks develop multi-vertical ecosystems that reinforce direct relationships and reward redemption options. This mix shift helps owners reduce commission leakage and build richer guest profiles tied to repeat business and cross-sell opportunities over time.

The Thailand hospitality market’s channel evolution also reflects corporate account recovery, where negotiated rates still anchor volume. City hotels with strong MICE and corporate programs benefit from stable blocks and shoulder-night demand that balances leisure exposure. Technology upgrades in property management and point-of-sale systems shorten onboarding times and help groups standardize operations and analytics across properties. As direct channels mature and loyalty propositions improve, OTAs remain critical for top-of-funnel discovery while brands prioritize conversion on owned channels, especially for repeat guests. Over the forecast, the balance implies a slightly higher share for direct digital within a still OTA-led distribution landscape.

Geography Analysis

Regional shares and growth profiles reveal a balanced yet distinct pattern across the Thailand hospitality market, with Bangkok and Central Plains accounting for 39.66% in 2025 and Eastern Thailand pacing fastest at a 9.68% CAGR through 2031. The capital city benefits from the country’s 2024 foreign arrivals rebound and a broad base of domestic trips, which together underpin steady demand across upscale and mid-scale inventory. Upscale city hotels leverage events and premium leisure to grow rates in 2026, while mid-scale assets lean on corporate travelers and residents seeking short breaks. Product uplift in well-located properties continues to improve, meeting and event capabilities to compete for regional conferences. The city’s continued focus on brand partnerships and renovations supports rate integrity over the medium term.

Eastern Thailand’s momentum is shaped by infrastructure commitments and developer pipelines that enhance the region’s positioning for business and leisure. Pattaya’s new luxury and upper-upscale openings by leading Thai platforms broaden the area’s appeal to MICE groups and high-spend family segments. Better connectivity and airport capacity additions improve access, an element that compounds with new room supply optimized for events. Over 2026 and beyond, a rising share of corporate and event-led demand complements leisure, which leads to steadier shoulder seasons. The region’s operators also invest in brand repositioning to capture higher ADR segments.

Southern and Northern Thailand round out the national picture with distinct demand drivers and product configurations. Southern beach destinations capture long-haul demand across winter months and leverage wellness and villa product to extract higher ADRs. Northern cities benefit from domestic programs that disperse trips across secondary provinces, with cultural itineraries and food experiences drawing repeat visitation. Across these regions, the Thailand hospitality market shows improving channel mix as larger groups build direct digital capability alongside OTA reach. This approach helps smooth seasonal peaks with targeted promotions and loyalty campaigns that drive repeat business.

Competitive Landscape

Competition in the Thailand hospitality market remains moderate and fragmented, with the top five operators holding a combined near-40% room share and a long tail of independent and smaller chain properties. Thai-born multi-brand groups leverage deep local knowledge, strong food and beverage ecosystems, and policy familiarity, which support speed-to-market and cost control. Larger Thai platforms report revenue and profit acceleration in 2024 and 2025, reflecting operating leverage from higher occupancy and stronger ADRs across selected portfolios. Portfolio management emphasizes renovations, brand elevation, and selective new builds in corridors showing durable growth. Meanwhile, technology upgrades in PMS and POS shorten deployment times and deepen analytics usage across estates.

International chains continue to expand through management agreements and franchises that import loyalty scale, standardized training, and global sales engines. Thai developers pair with global brands to elevate rate ceilings and attract international corporate and leisure demand. Capital recycling is accelerating as operators convert owned assets into REITs or partner vehicles, a model highlighted by a 2025 leasehold REIT filing by a leading Thai platform to unlock value while retaining management and brand control. The regulatory framework under Thailand’s SEC supports this model with clear rules on minimum asset size and distributions, which draws institutional capital seeking yield. These moves collectively raise competitive intensity around brand-led, asset-light growth.

Strategic initiatives in 2025 and 2026 include new hotel openings in Eastern Thailand, luxury repositionings in Bangkok, and ecosystem expansion in dining and retail by diversified Thai groups. Operators emphasize sustainability and certification across portfolios to align with corporate travel ESG criteria, with one major Thai operator reporting full certification across hotels by 2025. Larger groups also post strong financial momentum and shareholder return programs in late 2025, signaling confidence for the next investment cycle. Overall, the Thailand hospitality market’s competitive edge tilts toward players that combine brand systems, capital agility, technology adoption, and ESG alignment to defend rate and drive higher-value stays.

Thailand Hospitality Industry Leaders

-

Minor International (MINT)

-

Accor Group

-

Marriott International

-

Centara Hotels & Resorts

-

Dusit Thani PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Minor International expanded its share repurchase program to USD 142.9 million following strong multi-segment performance through 2025, as disclosed in investor communications.

- July 2025: ONYX Hospitality Group submitted filings to the Thai SEC to establish ONYXRT, a leasehold hospitality REIT consisting of four high-performing hotels, enabling asset-light expansion while preserving brand and management control.

- March 2025: Asset World Corporation completed the acquisition of the company owning Swissotel Bangkok Ratchada and a large office tower and announced a USD 248.6 million redevelopment plan under a luxury global brand, with operations expected by 2028.

- January 2025: Asset World Corporation opened Meliá Pattaya Hotel as part of a multi-year investment program, reinforcing Eastern Thailand’s upscale and MICE positioning with new branded capacity.

Thailand Hospitality Market Report Scope

Hospitality refers to the dynamic between a host and a guest, wherein the host extends goodwill by welcoming and entertaining guests, visitors, or even strangers. The report covers a complete background analysis of Thailand's hospitality industry, including an assessment of the industry associations, the overall economy, emerging market trends by segments, significant changes in the market dynamics, and a market overview.

The Thailand Hospitality Market Report is Segmented by Type (Chain Hotels, Independent Hotels), by Accommodation Class (Luxury, Mid & Upper-Mid-scale, Budget & Economy, Service Apartments), by Booking Channel (Direct Digital, OTAs, Corporate/MICE, Wholesale & Traditional Agents), and Geography (Bangkok & Central Plains, Northern Thailand, Northeastern Thailand, Eastern Thailand, Southern Thailand).

By Type (Value)

| Chain Hotels |

| Independent Hotels |

By Accommodation Class (Value)

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel (Value)

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region (Value)

| Bangkok & Central Plains |

| Northern Thailand |

| Northeastern Thailand |

| Eastern Thailand |

| Southern Thailand |

| By Type (Value) | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class (Value) | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel (Value) | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region (Value) | Bangkok & Central Plains |

| Northern Thailand | |

| Northeastern Thailand | |

| Eastern Thailand | |

| Southern Thailand |

Key Questions Answered in the Report

What is the Thailand hospitality market outlook through 2031?

The Thailand hospitality market size grows from USD 24.53 billion in 2026 to USD 36.26 billion by 2031 at an 8.13% CAGR, supported by diversified source markets, luxury rate strength, and asset-light expansion.

Which segments lead growth in Thailand between 2026 and 2031?

Luxury accommodations and chain-operated hotels record the fastest growth, while mid and upper-mid-scale properties and independent hotels anchor volume and room-night share.

How is booking distribution evolving in Thailand?

Online travel agencies remain the largest channel, and direct digital bookings are the fastest-growing as operators invest in loyalty, CRM, and website conversion to reduce commission costs.

Which regions are most important for performance?

Bangkok and the Central Plains hold the largest share, while Eastern Thailand posts the fastest growth as connectivity and project pipelines mature around Pattaya and nearby provinces.

What are the main risks to a smooth recovery?

Labor shortages, electricity tariffs, short-term rental competition, and ongoing volatility in Chinese arrivals remain key risks, though diversified source markets help dampen swings.

How are Thai operators financing expansion?

Many are recycling capital through REITs and growing asset-light portfolios with management agreements, allowing faster scale-up with lower balance-sheet intensity.

Page last updated on: