Battery Scrap Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

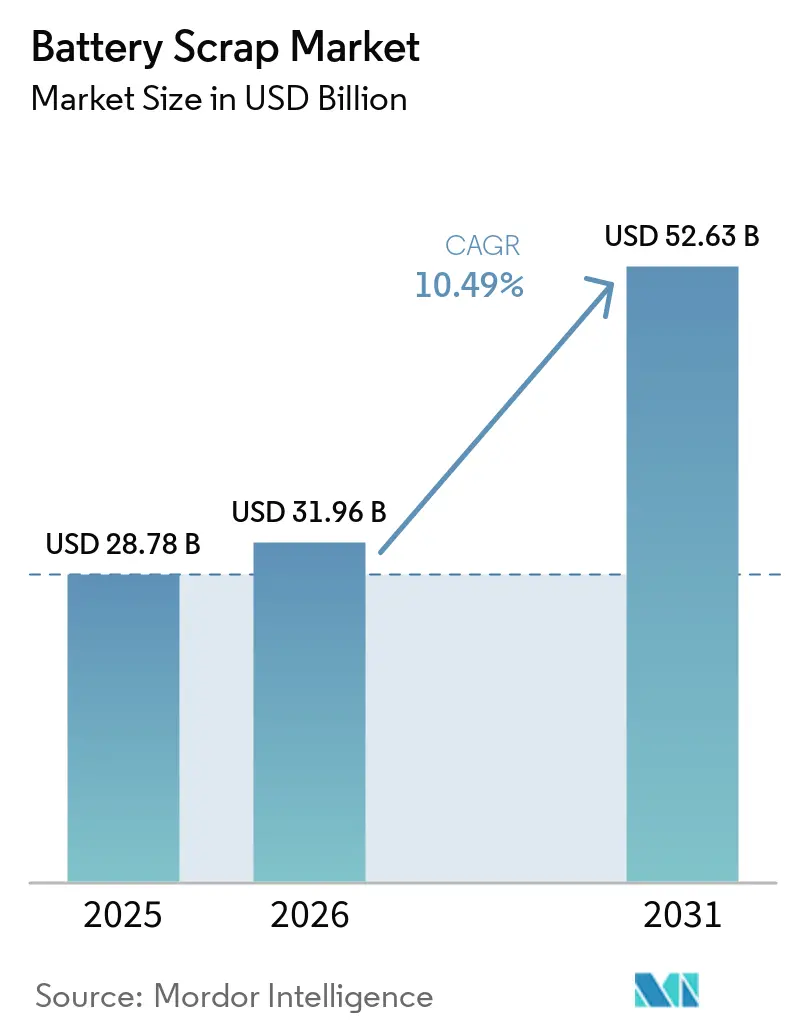

| Market Size (2026) | USD 31.96 Billion |

| Market Size (2031) | USD 52.63 Billion |

| Growth Rate (2026 - 2031) | 10.49% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Scrap Market Analysis by Mordor Intelligence

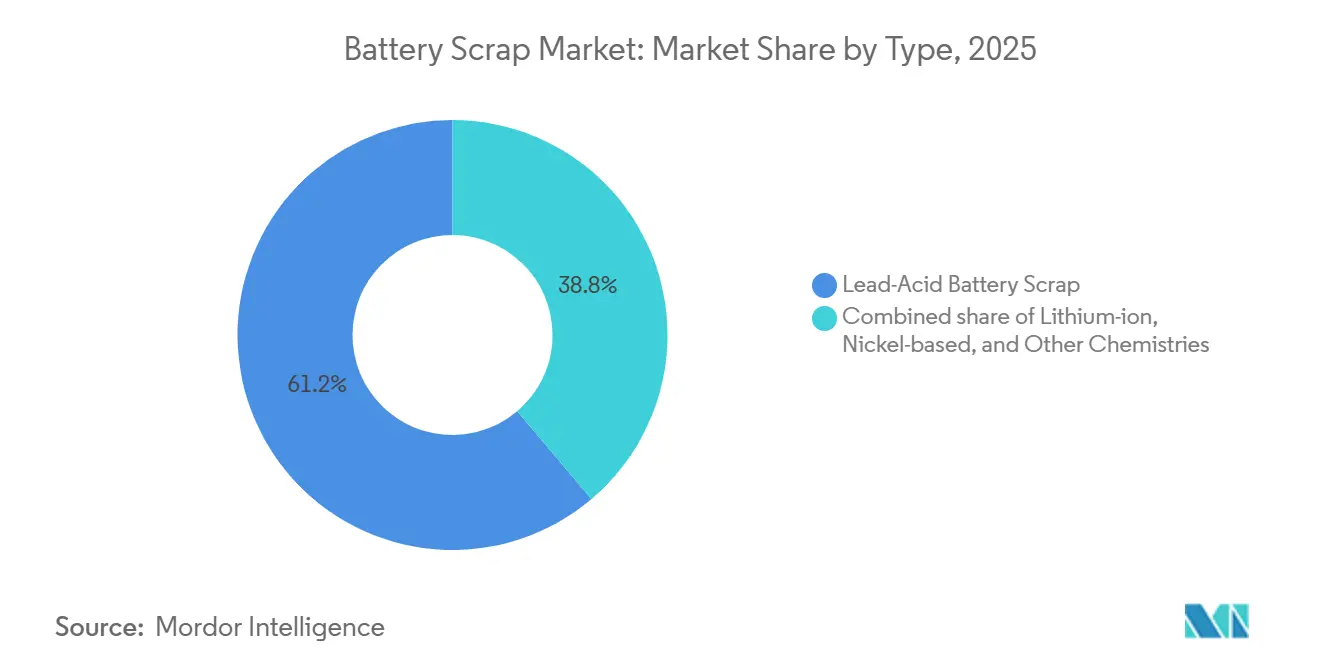

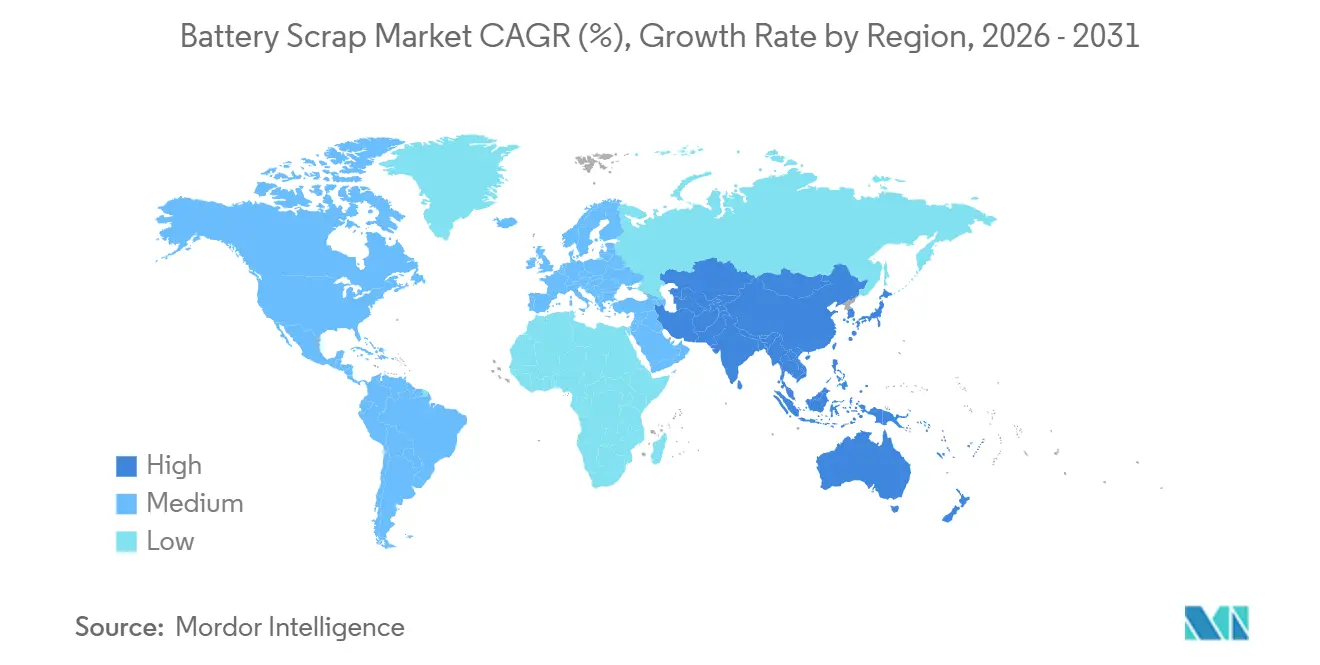

The Battery Scrap Market size is projected to expand from USD 28.78 billion in 2025 and USD 31.96 billion in 2026 to USD 52.63 billion by 2031, registering a CAGR of 10.49% between 2026 and 2031. Rising retirements of first-generation electric-vehicle (EV) packs, the tightening of producer-responsibility mandates, and the rebound in black-mass prices are combining to unlock steady, high-grade feedstock for recyclers. Lead-acid chemistries delivered 61.2% of 2025 volumes, while lithium-ion streams are poised for a 22.3% CAGR through 2031 as early EV fleets reach end-of-life. Automotive applications supplied 53.1% of 2025 scrap, yet stationary energy-storage systems are on course for a 23.6% CAGR as utility-scale batteries installed in the early 2020s retire. Regionally, Asia-Pacific held 49.3% of global flows in 2025 and should sustain a 13.3% CAGR thanks to China’s 80% share of worldwide recycling capacity.

Key Report Takeaways

- By type, lead-acid batteries captured 61.2% of battery scrap market share in 2025, whereas lithium-ion scrap is projected to grow at a 22.3% CAGR through 2031.

- By application, automotive streams held 53.1% of the battery scrap market in 2025, while stationary energy-storage packs are forecast to expand at a 23.6% CAGR over 2026-2031.

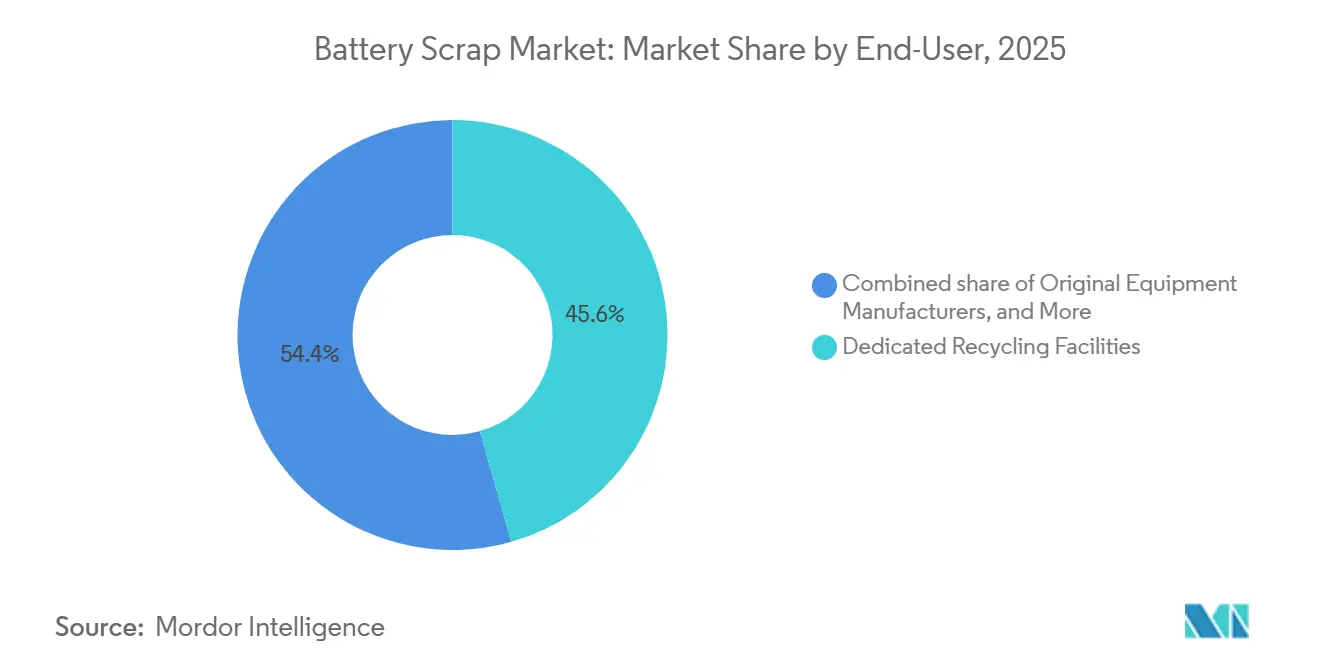

- By end user, dedicated recycling facilities secured 45.6% of 2025 volumes, yet OEM-integrated closed-loop programs are advancing at a 26.9% CAGR to 2031.

- By geography, Asia-Pacific commanded 49.3% of global flows in 2025 and is set for the fastest regional rise at a 13.3% CAGR across 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Battery Scrap Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring EV-linked Li-ion volumes hitting end-of-life | +3.2% | Global, with concentration in China, EU, North America | Medium term (2-4 years) |

| Mandatory producer-responsibility laws in EU, China, India | +2.8% | EU, China, India; spill-over to ASEAN | Short term (≤ 2 years) |

| Growing black-mass spot prices improving recycler margins | +1.9% | Global, particularly EU and North America | Short term (≤ 2 years) |

| OEM "closed-loop" offtake contracts | +1.5% | North America, EU, Japan, South Korea | Medium term (2-4 years) |

| AI-enabled scrap-stream triage boosting recovery yields | +0.9% | North America, EU, China | Long term (≥ 4 years) |

| Stationary-storage repurposing delaying recycle flows | +0.2% | Global, with early adoption in North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring EV-Linked Li-ion Volumes Hitting End-of-Life

The first mass-market EV batteries installed between 2015 and 2020 have begun retiring, creating a rapid upswing in lithium-ion scrap. Global EV battery demand stood near 1 TWh in 2024 and is forecast to exceed 3 TWh by 2030, yet worldwide recycling capacity totaled only 300 GWh in 2023, underscoring a structural supply imbalance [1]International Energy Agency, “Battery Recycling Capacity,” iea.org. China processed more than 500,000 tons of spent Li-ion cells in 2024 and targets 300,000 tons of annual throughput by 2026 through GEM’s new Jingmen line. Guangdong Brunp Recycling reported 99.6% recovery of nickel, cobalt, and manganese and 96.5% of lithium in 2024, keeping material costs 15-20% below mined equivalents. Battery retirements are forecast to climb from roughly 200 GWh in 2025 to more than 1 TWh in 2030, transforming scrap into a front-line supply source for cathode producers. Regional feedstock tightness is set to reward recyclers who lock in offtake early with automakers, cell makers, and utilities.

Mandatory Producer-Responsibility Laws in EU, China, India

Extended producer responsibility (EPR) frameworks now obligate manufacturers to fund collection and recycling, accelerating formal reverse-logistics build-outs. The EU Battery Regulation mandates 63% collection by 2027 and 90% recycling efficiency for cobalt, copper, and nickel by 2027, with recycled-content floors of 16% cobalt, 85% lead, and 6% lithium and nickel taking effect from 2031 [2]European Commission, “Regulation (EU) 2023/1542 on Batteries,” europa.eu. China’s Ministry of Industry and Information Technology requires EV producers to establish take-back channels and log traceability data, stimulating partnerships between automakers and large recyclers such as GEM and Brunp. India’s Battery Waste Management Rules, amended through 2025, lift recovery targets to 90% by 2026-2027 and introduce recycled-content mandates rising to 20% by 2030-2031. These policies marginalize informal collectors and channel volumes toward ISO 14001-certified facilities, pushing the battery scrap market toward industrial-scale operations.

Growing Black-Mass Spot Prices Improving Recycler Margins

After a severe 2022-2024 commodity slump, black-mass prices stabilized in 2025, reviving margins. Cobalt fell from USD 81,500 per ton in April 2022 to USD 24,000 in September 2024 before rebounding to USD 35,000 in early 2025, while premium black mass (>20% nickel equivalent) climbed from USD 5,000-6,000 per ton in mid-2024 to USD 8,000-10,000 by early 2026 [3]Benchmark Mineral Intelligence, “Black-Mass Pricing Update,” benchmarkminerals.com. European and North American cathode producers moved to long-term contracts to hedge against further volatility, underpinning project finance for planned hydrometallurgical hubs. Chinese recyclers also began exporting black mass to South Korean refiners that ship precursors to Europe, exploiting cross-border arbitrage. A firmer pricing floor supports scale-up decisions requiring USD 200-500 million in capital expenditure.

OEM “Closed-Loop” Offtake Contracts

Automakers are vertically integrating recycling to secure cathode-active materials, reduce supply-chain risk, and showcase circular-economy credentials. Redwood Materials handled more than 1 GWh of end-of-life packs in 2025 under agreements with Tesla, Toyota, Ford, and Panasonic, returning recycled copper foil and cathode powders to cell partners [4]Redwood Materials, “Closed-Loop Partnerships,” redwoodmaterials.com. Volkswagen and Umicore inaugurated a 15 GWh plant in Salzgitter in 2025, targeting 95% recovery and full in-house reuse. BMW has secured recycled cathode inputs for its Neue Klasse platform, while Stellantis is co-funding a 50,000-ton French facility with Orano. Such deals siphon high-grade feedstock from the open market, pressuring independent recyclers to chase lower-quality streams or pivot toward consumer-electronics scrap.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inefficient global reverse-logistics for end-of-life packs | -1.8% | Global, acute in ASEAN, South America, MEA | Medium term (2-4 years) |

| Volatile cobalt & nickel prices eroding re-seller profits | -1.4% | Global, particularly impacting North America and EU recyclers | Short term (≤ 2 years) |

| Technology-lock risk from rapid cell-chemistry shifts | -0.9% | China (LFP dominance), spill-over to ASEAN | Long term (≥ 4 years) |

| Fire-safety liabilities inflating insurance premiums | -0.7% | North America, EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inefficient Global Reverse-Logistics for End-of-Life Packs

Collection and transport of spent packs remain fragmented and costly. UN 3480 and ADR classifications demand specialized packaging and labeling, inflating per-unit logistics costs by 40-60% over non-hazardous goods. Design heterogeneity forces recyclers to invest in bespoke disassembly tooling or accept lower yields from shredding-only lines. India’s 2024 black-mass export restriction created bottlenecks for small collectors who lack domestic refining, while Indonesia’s informal sector still handles around 30-40% of lead-acid scrap outside regulatory oversight. A comprehensive battery passport system will not arrive in the EU until February 2027, keeping traceability data siloed. Until reverse-logistics standards converge, feedstock aggregation costs will temper the growth of the battery scrap market.

Volatile Cobalt & Nickel Prices Eroding Re-Seller Profits

Sharp commodity swings compress margins for recyclers tied to fixed feedstock costs. Cobalt plunged 71% from April 2022 highs to September 2024 lows before a partial recovery, while nickel dropped from USD 33,000 per ton in March 2022 to USD 16,000 by mid-2024. SungEel HiTech posted a Q1 2025 operating loss of KRW 15.5 billion (USD 11.6 million) as utilization fell to 40% at its Saemangeum plant. Li-Cycle halted its USD 1.2 billion Rochester hub in late 2024 after a USD 75.4 million quarterly loss, underscoring financing challenges in volatile markets. As China’s lithium-iron-phosphate (LFP) cathodes, free of cobalt and nickel, take 95% of its EV segment, recyclers optimized for high-nickel chemistries must retool or face stranded-asset risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Lead-Acid Maturity Anchors Global Volumes

Lead-acid batteries supplied 61.2% of 2025 flows, anchoring the battery scrap market size with recovery rates above 99% in North America and Europe. Lithium-ion volumes, however, are projected to surge at a 22.3% CAGR to 2031 as EV retirements accelerate. Hydrometallurgical refiners deliver 90-95% metal recovery but need USD 200-500 million per commercial hub, whereas pyrometallurgical operators accept 80-85% yields for lower capital intensity. The battery scrap market share for nickel-metal-hydride cells is shrinking as hybrid vehicles transition to Li-ion, yet aerospace and defense preserve a niche demand for nickel-cadmium recycling.

Direct-cathode-regeneration is disrupting lithium-ion processing by eliminating full material breakdown and cutting costs by 30-40%. Ascend Elements’ Hydro-to-Cathode line in Georgia achieves 91% recovery and reintroduces material into cell plants within weeks, shrinking working-capital cycles. ReCell Center pilots show NMC 622 scrap can regenerate NMC 811, though LFP and nickel-cobalt-aluminum variants still require separate flows. As LFP adoption rises, flexible multi-chemistry plants will determine which players retain battery scrap market share through 2031.

By Application: Automotive Leads, Stationary Storage Races Ahead

Automotive streams accounted for 53.1% of 2025 scrap, sustained by core-deposit loops that return lead-acid starters at retail and service points. EV-pack take-back is mandatory under EPR rules in the EU, China, and India, ensuring steady inflows for certified recyclers. Industrial motive-power applications, like forklifts, airport equipment, and material-handling vehicles, provide consistent but slower-growth volumes tied to warehouse automation. Consumer electronics’ share is dwindling as phone and laptop replacement cycles lengthen.

Stationary energy-storage systems are expected to forecast a 23.6% CAGR as early utility batteries and second-life EV packs converge on end-of-life. Second-life repurposing delays recycling by 5-8 years, yet amplifies eventual volumes and broadens the battery scrap market size when those systems retire. Data-center backup deployments managed by Redwood Materials illustrate how repurposed packs cycle back into recycling after extended service. Aerospace, maritime, and medical segments remain small but rising as electrification spreads across specialized platforms.

By End User: Dedicated Recyclers Face OEM Integration Pressure

Dedicated recyclers handled 45.6% of flows in 2025, but OEM-integrated programs are climbing at a 26.9% CAGR, signaling a shift in battery scrap market dynamics. Umicore’s Hoboken site processes 35,000 tons per year and extracts 17 metals, yet Volkswagen’s Salzgitter JV locks in 15 GWh of internal pack returns, limiting third-party access to premium scrap. Tesla routes Gigafactory Nevada returns directly to Redwood, cutting virgin material dependence by roughly 25%. Utilities such as Vistra are preparing dedicated take-back loops for their 1.6 GW stationary battery fleet. Informal collectors across India, Indonesia, and sub-Saharan Africa still control 30-40% of lead-acid scrap but face formalization mandates that should consolidate volumes toward certified operators.

Independent waste-management firms like TES, Stena, and Veolia are entering the battery scrap market, repurposing electronics-collection assets yet lacking hydrometallurgical depth. Their competitiveness hinges on partnerships with refiners or access to AI-enabled sorting that lifts yields without heavy capital outlays. Consolidation is likely as EPR compliance costs climb and insurers demand ISO-aligned safety protocols.

Geography Analysis

Asia-Pacific dominated the battery scrap market size with 49.3% of 2025 volumes and is forecast to have a 13.3% CAGR through 2031. China alone controls 80% of global recycling capacity; GEM’s new 50,000-ton line pushes its total to 300,000 tons and supplies CATL and BYD under contract. India’s amended Battery Waste Management Rules raise recovery targets to 90% by 2026-2027, but uneven enforcement and black-mass export bans challenge small collectors. Japan and South Korea remain technology leaders: SungEel HiTech’s 600-ton cobalt plant in Saemangeum anchors regional hydrometallurgical expertise, and Sumitomo partners with Nissan on Leaf pack recycling.

Europe ranks second by value thanks to stringent regulation. Northvolt’s Revolt plant reached 50,000 tons throughput in 2025 and aims for 125,000 tons by 2030. The EU Battery Passport, mandatory from February 2027, embeds QR-code traceability and recycled-content disclosure, tilting competitive advantage toward vertically integrated players. North America is catching up under the Inflation Reduction Act incentives: Redwood and Ascend Elements both scaled commercial lines in 2025, while Li-Cycle paused its Rochester hub amid cost overruns despite Glencore’s USD 200 million investment in an Alabama spoke.

South America and the Middle East & Africa remain nascent. Brazil’s flex-fuel car parc creates steady lead-acid flows, yet low EV penetration defers lithium-ion investment. Saudi Arabia and the UAE are evaluating recycling as part of diversification agendas, but feedstock remains scarce. Egypt’s informal operators handle over half of national lead-acid volumes, with 2024 draft rules set to push formal take-back schemes. Regional disparity suggests cross-border trade in black mass will rise until domestic hubs reach scale.

Competitive Landscape

The battery scrap market remains moderately fragmented. Pyrometallurgical incumbents such as Glencore and Umicore leverage legacy smelters, achieving lower capex but 80-85% metal recovery. Hydrometallurgical specialists, including Ascend Elements and Fortum, deliver 90-95% yields yet depend on stable cobalt and nickel prices. Direct-cathode startups like Ascend Elements, RecycLiCo, and Princeton NuMat promise 30-40% cost savings but remain limited to compatible chemistries, heightening technology-lock risk as LFP penetration rises.

Strategic moves underline consolidation pressure. Redwood will double Nevada cathode capacity to 200 GWh by 2028 under USD 500 million expansion financing tied to Toyota, Ford, and Panasonic supply contracts. Umicore-Volkswagen’s Salzgitter venture locks 95% recovery of lithium, nickel, cobalt, and manganese straight into VW cell lines, bypassing spot markets. Glencore’s stake in Li-Cycle secures North American black mass for its European smelters, illustrating cross-regional resource orchestration. American Battery Technology Company’s DOE-backed Nevada demo plant targets lithium-selective extraction that cuts chemical waste and operating costs.

White-space opportunities revolve around AI-enabled dismantling, second-life arbitrage, and emerging-market formalization. Ascend Elements reports 40-60% labor savings from computer vision sorting. Nth Cycle’s electro-extraction skips acid leaching, lowering reagent demand. ISO-driven formalization across India and Indonesia could redirect millions of spent lead-acid units toward compliant plants, reshaping global feedstock flows over the next five years.

Battery Scrap Industry Leaders

Umicore

Glencore

Li-Cycle

Redwood Materials

Guangdong Brunp Recycling

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: NITI Aayog introduced a national circular economy roadmap focused on improving the management and recycling of lithium-ion battery scrap and e-waste in India. The roadmap suggests expanding incentives under the Advanced Chemistry Cell (ACC) Production Linked Incentive (PLI) scheme. This initiative seeks to encourage the use of recycled battery materials, strengthen domestic recycling infrastructure, reduce dependence on virgin raw materials, and support the growth of the battery scrap and recycling ecosystem.

- February 2025: Cylib secured EUR 55 million (USD 58.3 million) to scale hydrometallurgical lithium-ion recovery across Europe.

- January 2025: Li Industries, a pioneer in lithium-ion battery recycling technologies, has successfully raised USD 36 million in a Series B funding round to bolster its expansion efforts.

- December 2024: NEU Battery Materials raised USD 4.28 million for processes targeting solid-state and silicon-anode scrap.

Global Battery Scrap Market Report Scope

Battery scrap consists of discarded or end-of-life batteries that are no longer functional but still contain valuable materials, such as metals, which can be recovered and reused. Recycling battery scrap is essential to prevent environmental damage caused by hazardous substances and to enhance resource efficiency, thereby supporting environmental sustainability and contributing to the circular economy.

The Battery Scrap Market is segmented by type, application, end-user, and geography. By type, the market is segmented into lead-acid, lithium-ion, nickel-based, and other chemistries. By application, the market is segmented into automotive, industrial motive-power, consumer electronics, stationary energy storage, aerospace and defense, and other niche uses. By end-user, the market is segmented into dedicated recycling facilities, OEM take-back programs, utilities, third-party waste management companies, and informal collectors. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report also covers market size and forecasts for the global battery scrap market across major countries within these regions. For each segment, market sizing and forecasts have been conducted on the basis of value (USD).

| Lead-Acid Battery Scrap |

| Lithium-ion Battery Scrap |

| Nickel-based Battery Scrap |

| Other Chemistries (NiCd, Zn-air, Solid-state pre-commercial) |

| Automotive |

| Industrial Motive-Power |

| Consumer Electronics |

| Stationary Energy-Storage Systems |

| Aerospace and Defense |

| Other Niche Uses (medical, maritime, mining) |

| Dedicated Recycling Facilities |

| Original Equipment Manufacturers (OEM Take-Back) |

| Utilities and Power Producers |

| Third-party Waste-Management Firms |

| Informal/Small-scale Collectors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Lead-Acid Battery Scrap | |

| Lithium-ion Battery Scrap | ||

| Nickel-based Battery Scrap | ||

| Other Chemistries (NiCd, Zn-air, Solid-state pre-commercial) | ||

| By Application | Automotive | |

| Industrial Motive-Power | ||

| Consumer Electronics | ||

| Stationary Energy-Storage Systems | ||

| Aerospace and Defense | ||

| Other Niche Uses (medical, maritime, mining) | ||

| By End-User | Dedicated Recycling Facilities | |

| Original Equipment Manufacturers (OEM Take-Back) | ||

| Utilities and Power Producers | ||

| Third-party Waste-Management Firms | ||

| Informal/Small-scale Collectors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global battery-recycling revenues be by 2031?

The battery scrap market size is forecast to reach USD 52.63 billion by 2031, expanding at a 10.49% CAGR between 2026 and 2031.

Which battery chemistry dominates scrap volumes today?

Lead-acid batteries supplied 61.2% of 2025 flows thanks to starter-battery and industrial-power demand.

Why are lithium-ion scrap volumes set to surge after 2026?

Early EV packs deployed between 2015 and 2020 are hitting end-of-life, pushing lithium-ion streams toward a 22.3% CAGR through 2031.

What region recycles the most batteries?

Asia-Pacific led with 49.3% of 2025 scrap, propelled by China’s 80% share of global recycling capacity.

How are automakers changing the recycling landscape?

OEMs such as Tesla and Volkswagen secure cathode materials through closed-loop contracts, raising the share of in-house recycling programs at a 26.9% CAGR.

Page last updated on: