Lithium-ion Battery Recycling Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.07 Billion |

| Market Size (2031) | USD 14.79 Billion |

| Growth Rate (2026 - 2031) | 23.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

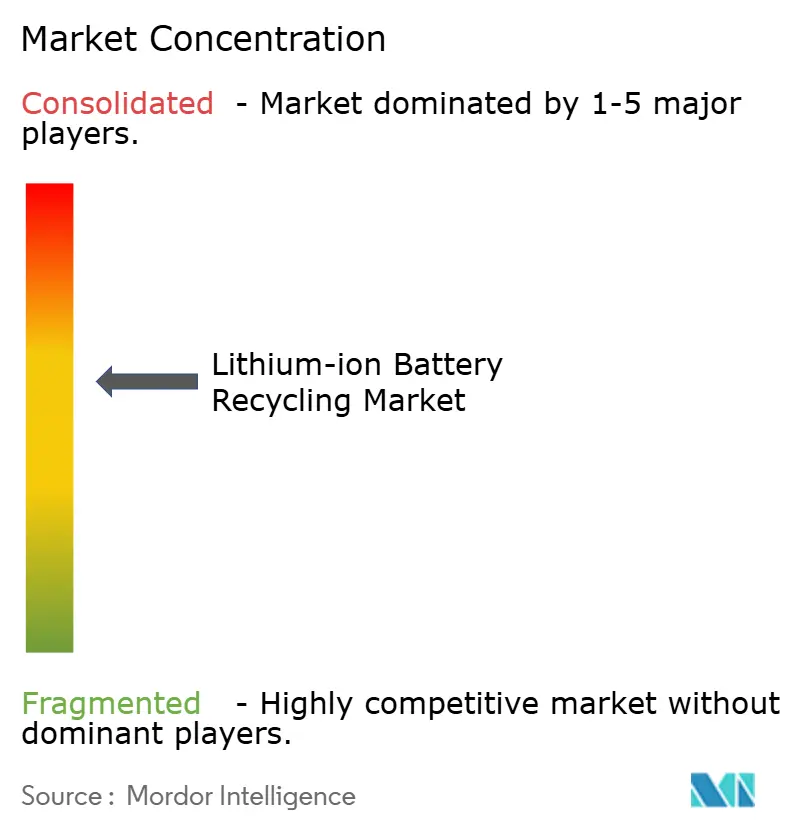

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lithium-ion Battery Recycling Market Analysis by Mordor Intelligence

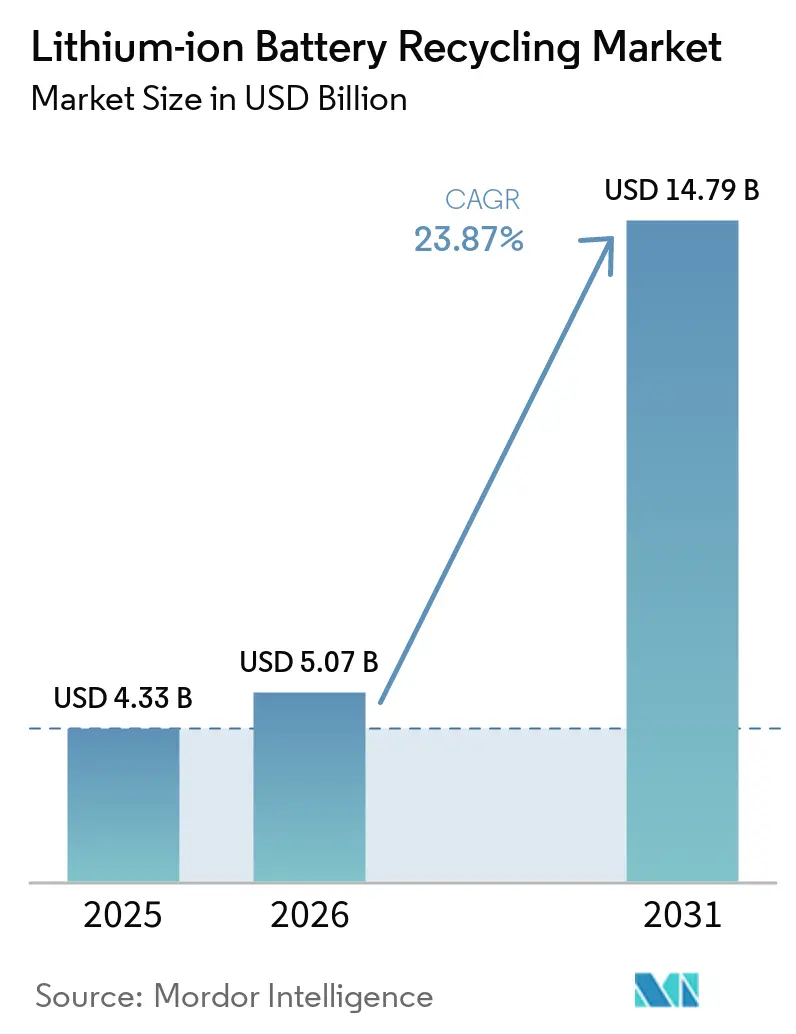

The Lithium-ion Battery Recycling Market size was valued at USD 4.33 billion in 2025 and is estimated to grow from USD 5.07 billion in 2026 to reach USD 14.79 billion by 2031, at a CAGR of 23.87% during the forecast period (2026-2031).

Automakers are accelerating closed-loop supply chains to insulate themselves from raw-material price swings, while regulatory mandates in the European Union, China, and the United States are turning recycling into a cost-of-sales item rather than a sustainability add-on. Extended Producer Responsibility (EPR) rules, Inflation Reduction Act (IRA) domestic-content thresholds, and the rise of black-mass spot markets are channeling capital toward hydrometallurgical and direct processes that maximize lithium and cobalt recovery at lower energy intensities. Asia-Pacific currently dominates throughput thanks to vertically integrated players such as CATL and BYD, yet North America is expanding fastest on the back of IRA tax credits and Department of Energy loan guarantees that de-risk capacity additions. Supply-side fragmentation persists, keeping barriers to entry low but pressuring margins whenever lithium carbonate prices soften.

Key Report Takeaways

- By end-of-life source, automotive batteries held 63.8% of the lithium-ion battery recycling market share in 2025 and posted the fastest growth at 25.3% CAGR to 2031.

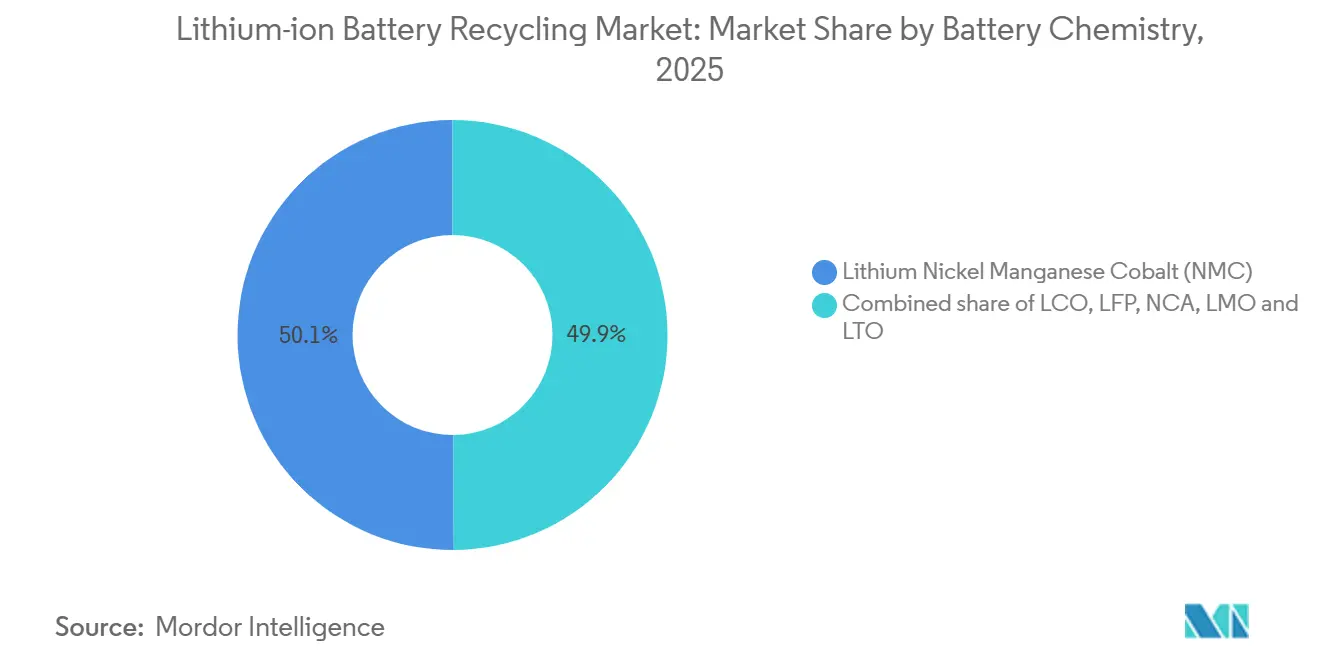

- By battery chemistry, NMC products accounted for 50.1% of the lithium-ion battery recycling market size in 2025; LFP is forecast to expand at a 26.8% CAGR.

- By recycling technology, hydrometallurgy captured 54.7% of revenue in 2025, whereas direct/mechanical methods are set to grow at a 28.7% CAGR through 2031.

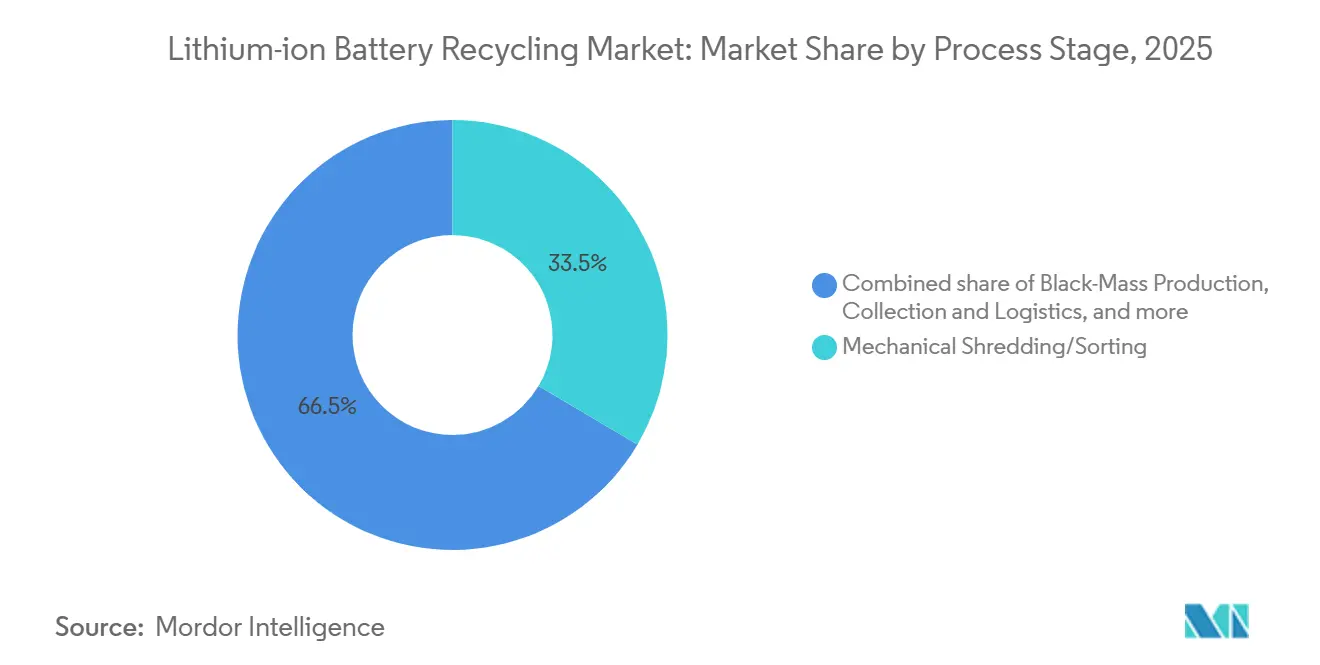

- By process stage, mechanical shredding/sorting held 33.5% of the lithium-ion battery recycling market share in 2025, while black-mass production posted the fastest growth at a 26.2% CAGR to 2031.

- By application of recovered materials, battery-grade lithium compounds accounted for 40.4% of the lithium-ion battery recycling market size in 2025; the cathode active materials segment is forecast to expand at a 24.9% CAGR.

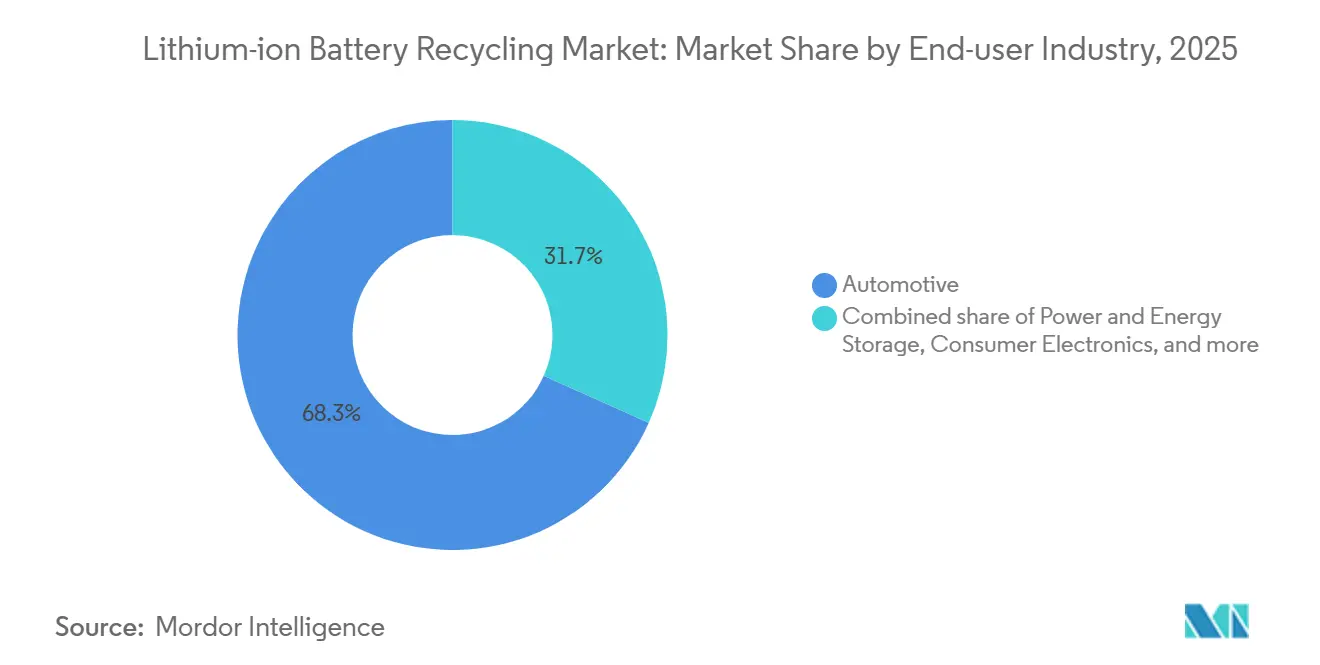

- By end-user industry, automotive captured 68.3% of revenue in 2025, whereas power and energy storage are set to grow at a 27.5% CAGR through 2031.

- By geography, Asia-Pacific led with 44.6% revenue share in 2025, but North America is projected to post the highest 27.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lithium-ion Battery Recycling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating wave of EV battery retirements | +6.2% | Global, early focus on China, Europe, North America | Medium term (2–4 years) |

| Tightening global EPR & EU Battery Regulation mandates | +5.1% | Europe, China, emerging in U.S. and South Korea | Short term (≤2 years) |

| Raw-material price inflation spurring closed loops | +4.8% | Global, highest in import-dependent regions | Short term (≤2 years) |

| Step-change yields from next-gen hydro & direct recycling | +3.9% | North America, Europe, pilot projects in Asia-Pacific | Medium term (2–4 years) |

| OEM design-for-recycling packs | +2.7% | Global, led by Tesla, BYD, GM | Long term (≥4 years) |

| Emergence of liquid black-mass spot markets | +1.5% | Europe, North America, expanding to Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Accelerating wave of EV battery retirements

Early cohorts of mass-market EVs sold between 2015 and 2018 began hitting end-of-warranty in 2024-2025, sending an estimated 280,000 tonnes of packs into global collection systems.[1]International Energy Agency, “Global EV Outlook 2024,” iea.org China’s electric buses and taxis from the 2016-2018 subsidy boom are now retiring, while Europe’s Nissan Leaf and Renault Zoe fleets move into recycling channels. The shift means recyclers can tap higher-value cobalt-rich packs instead of relying on lower-margin manufacturing scrap. Tesla reported that 92% of critical minerals in its 4680 cells can be recovered and looped back into new batteries, validating the economic case for closed loops. A subsequent surge in volumes is expected from 2027-2030 as vehicles sold in the 2019-2022 growth spurt reach retirement.

Tightening global EPR & EU Battery Regulation mandates

The EU Battery Regulation, effective February 2024, sets a 63% collection target by 2027 and 73% by 2030, underpinned by fines of up to 4% of annual turnover for non-compliance.[2]International Energy Agency, “Global EV Outlook 2024,” iea.org China mandates 65% recycling of power batteries by 2025 through a digital traceability system, and South Korea requires 80% collection by 2028. Automakers, therefore, must finance reverse logistics networks; Volkswagen allocated EUR 200 million in March 2025 to integrate 1,200 dealerships and 350 third-party sites. Compliance costs are driving the lithium-ion battery recycling market toward scale and vertical integration.

Raw-Material Price Inflation Spurring Closed-Loop Supply Chains

Lithium carbonate rocketed to USD 82,000 per tonne in March 2024 before sliding to USD 12,000 by December 2025, underscoring the commodity’s volatility. Cobalt sulfate stayed elevated at USD 28,000–35,000, and nickel sulfate averaged USD 17,500 in 2025. OEMs such as BMW and Ford now lock in recycled nickel and cobalt at fixed spreads that undercut virgin-metal costs by 15-20%. Such contracts transform recyclers into strategic suppliers and stabilize margins across the lithium-ion battery recycling market.

Step-change yields from next-generation hydro & direct recycling

Ascend Elements’ Hydro-to-Cathode line, commercialized in 2024, recovers 98% of critical metals while reducing energy demand by 70% versus pyrometallurgy. Worcester Polytechnic Institute demonstrated direct recycling with 99% capacity retention after 500 cycles, and a 2025 Joule study found direct methods cut lifecycle CO₂ by 53% against hydro processes. Although feedstock homogeneity remains a barrier, early OEM-captive loops show compelling economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile metal prices & high reverse-logistics costs | -3.4% | Global, acute in geographically dispersed markets like North America, Australia | Short term (≤2 years) |

| Safety & haz-mat compliance in high-voltage collection | -1.8% | Global, particularly stringent in North America (DOT, OSHA), Europe (ADR), and developed APAC markets | Short term (≤2 years) |

| Regional over-capacity creating feedstock scarcity risk | -2.1% | North America, Europe (localized over-build in 2023-2024) | Medium term (2-4 years) |

| Low intrinsic value of LFP chemistries | -1.3% | Global, most acute in China where LFP dominates (60% of EV batteries), spreading to North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Metal Prices & High Reverse-Logistics Costs

Lithium carbonate’s 85% crash between March 2024 and December 2025 dragged black-mass prices down to USD 6,500 per tonne, forcing some recyclers into negative margins. Reverse-logistics costs range from USD 150–250 per tonne because packs are hazmat-classified under UN 3480 rules that require fire-resistant packaging and state-of-charge testing.[3]United Nations Economic Commission for Europe, “UN Model Regulations on Transport of Dangerous Goods,” unece.org These structural costs compress margins whenever metals fall.

Regional Over-Capacity Creating Feedstock Scarcity Risk

North America announced 450,000 tonnes of annual recycling capacity versus only 180,000 tonnes of available feedstock in 2025, pushing utilization below 40% and prompting Li-Cycle to idle multiple spokes.[4]Bloomberg, “Lithium Prices Plunge as Supply Glut Threatens Battery Makers,” bloomberg.com Similar imbalances exist in Europe, although collection mandates may narrow the gap by 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-of-Life Source: Automotive Dominance Masks Manufacturing Scrap’s Near-Term Role

Automotive packs accounted for 63.8% of revenue in 2025, a figure expected to rise as the 2015-2020 vehicle cohort retires. Manufacturing scrap, however, supplies immediate volume, sidestepping collection bottlenecks and enabling rapid ramp-up of hydrometallurgical plants. OEM take-back programs such as GM's Ultium warranty eliminate consumer friction, and higher targets for automotive than portable electronics further tilt flows toward vehicle batteries. The lithium-ion battery recycling market size for automotive sources is set to expand at a 25.3% CAGR, while consumer electronics lags due to fragmented collection and "drawer hoarding."

Manufacturing scrap represented only 7% of tonnage in 2025 but supplied steady, chemistry-homogeneous feedstock that supports direct recycling pilots. As the gigafactories' first-pass yields improve from 89% in 2022 to 96% in 2025, this stream will plateau; nonetheless, minimum-volume clauses in scrap contracts de-risk new capacity investments for recyclers like Umicore.

By Battery Chemistry: LFP’s Surge Challenges Recycling Economics

NMC held a 50.1% share in 2025 thanks to its dominance in long-range EVs and high cobalt content, which sustains favorable economics. LFP is growing fastest as Tesla and BYD deploy the chemistry in standard-range vehicles; however, its zero-cobalt composition erodes intrinsic value, lowering black-mass pricing by 65% relative to NMC. Recyclers, therefore, rely on high throughput and regulatory credits to profit from LFP streams.

LCO remains lucrative in laptops and smartphones, but shrinking device footprints cap tonnage. NCA, LMO, and LTO fill niche roles in high-performance or long-cycle applications. China’s draft rule raising the required lithium recovery for LFP from 70% to 85% aims to close the value gap, potentially unlocking a broader economic case for LFP recycling.

By Recycling Technology: Direct Methods Gain as Energy Costs Bite

Hydrometallurgy dominated with a 54.7% share in 2025 because it handles mixed chemistries and achieves 92–95% metal recovery. Direct/mechanical recycling is growing at 28.7% CAGR thanks to lower energy inputs, 0.8 kWh per kg versus 3.2 kWh for hydro, and high purity output suitable for cathode reuse. Yet direct routes need chemistry-pure feedstock, often achievable only in OEM-captive loops.

Pyrometallurgy retains relevance in integrated smelters where sunk infrastructure offsets energy intensity, but EU carbon-pricing schemes may erode this advantage. Hybrid flows that combine pyro pre-treatment with hydro refining are emerging, exemplified by Glencore’s Portovesme JV with Li-Cycle.

By Process Stage: Black-Mass Spot Markets Unlock Working Capital

Mechanical shredding captured 33.5% of the value in 2025 due to its labor and safety requirements. Black-mass production is the fastest-growing stage at 26.2% CAGR, driven by new spot markets that let small operators monetize intermediate output without financing full refining lines. The collection represents 18% of the value, with logistics bottlenecks persisting in rural or cross-border lanes.

Refining still delivers the highest gross margins, 38% for Umicore in 2025, and vertical integration boosts profitability for giants such as CATL’s Brunp, which retains 42% margins. Automated dismantling and EU design mandates are expected to reduce the cost share of initial disassembly.

By Application of Recovered Materials: Cathode Precursors Command Premium

Battery-grade lithium compounds held 40.4% of application value in 2025, while cathode active materials are poised for a 24.9% CAGR as OEMs seek IRA-compliant domestic content. Recycled cobalt and nickel salts trade at 15–20% premiums when certified as low-carbon, creating a pricing moat for audited supply chains.

Anode graphite recovery lags due to low commodity pricing, but Redwood Materials’ recycled copper foil line demonstrates scope for margin capture in balance-of-plant components. Manganese remains under-monetized until the LMFP cathodes scale.

By End-User Industry: Grid Storage Emerges as Second Feedstock Wave

Automotive accounted for 68.3% of 2025 revenue, yet utility-scale power and energy-storage systems are on a 27.5% CAGR trajectory. California’s grid batteries installed in 2020-2022 will retire from 2030 onward, feeding a concentrated LFP stream that is ideal for direct recycling. Consumer electronics face structural headwinds as replacement cycles lengthen, and marine or micro-mobility segments remain nascent but offer high-value cobalt-rich packs.

Geography Analysis

Asia-Pacific generated 44.6% of global revenue in 2025, buoyed by China’s 65% recycling mandate and Brunp’s 120,000-tonne capacity. Europe held a 28% share, anchored by Northvolt’s Revolt plant and strict EU Battery Regulation targets. North America posted the highest 27.1% CAGR forecast through 2031 as the IRA links tax credits to recycled content thresholds, catalyzing DOE-backed projects such as Redwood Materials’ 100 GWh cathode facility.

South America’s share sits at 4% but is rising as lithium-rich nations launch domestic recycling pilots. The Middle East and Africa claim 3% but may expand through regional hubs in Singapore and incentives tied to solar-plus-storage installations in Gulf states. Japan and India have announced subsidy programs and draft rules, respectively, yet commercial deployments remain early-stage.

Competitive Landscape

The top five players controlled less than 35% of global revenue in 2025, keeping the lithium-ion battery recycling market fragmented and regionally nuanced. CATL’s Brunp earns leading margins via vertical integration, while Ascend Elements differentiates on direct-recycling IP that cuts energy use 70%. Glencore leverages mining assets to bolt on black-mass capacity at lower capital intensity, and Umicore focuses on high-nickel NMC refining for premium cathodes.

Disruptors include bio-leach specialists that slash acid consumption, and trading platforms that tokenize black-mass streams. Patent filings center on high-nickel chemistries and direct-recycling electrodes, signaling a race for intellectual-property defensibility. OEM captive programs at Tesla, BYD, and Volkswagen are expanding, shrinking third-party addressable volume but offering stable feedstock to strategic partners.

Lithium-ion Battery Recycling Industry Leaders

Brunp Recycling (CATL)

GEM Co., Ltd.

Umicore SA

Glencore PLC

Li-Cycle Holdings Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lyten revealed its plans to acquire the Northvolt Revolt battery recycling plant located in Skellefteå, Sweden. This facility stands as one of Europe's key integrated battery recycling hubs, specifically engineered to extract lithium, nickel, cobalt, and manganese from used batteries.

- October 2025: CATL’s Brunp expanded Foshan capacity to 120,000 tonnes, including an LFP line.

- March 2025: Glencore entered preliminary discussions to acquire Li-Cycle following its earlier USD 75 million investment, indicating growing consolidation in battery recycling.

- June 2025: LG Energy Solution and Toyota set up Green Metals Battery Innovations joint venture in North Carolina, targeting 13,500 t of black-mass output per year, supporting U.S. supply-chain localisation.

Global Lithium-ion Battery Recycling Market Report Scope

The lithium-ion battery recycling market encompasses the global industry focused on the collection, transportation, processing, and recovery of valuable materials, including lithium, cobalt, nickel, manganese, copper, aluminum, and graphite, from end-of-life, defective, or manufacturing-scrap lithium-ion batteries.

The lithium-ion battery recycling market is segmented by end-of-life source, battery chemistry, recycling technology, process stage, application of recovered materials, end-user industry, and geography. By end-of-life source is segmented into automotive batteries, consumer electronics batteries, industrial and ess batteries, and manufacturing scrap. By battery chemistry, the market is divided among lithium cobalt oxide (LCO), lithium iron phosphate (LFP), lithium nickel manganese cobalt (NMC), lithium nickel cobalt aluminium (NCA), lithium manganese oxide (LMO), and lithium titanate (LTO). By recycling technology, the market is segmented into Hydrometallurgical, Pyrometallurgical, Direct/Mechanical, Hybrid, and Emerging (Bio/ Electro-chemical). By the process stage, the market is divided into collection and logistics, dismantling and discharge, mechanical shredding/sorting, black-mass production, material refining, and recovery. By application, the market is segmented into cathode active materials, anode/graphite, battery-grade lithium compounds, cobalt and nickel salts, manganese, and others (Cu, Al). By end-user industry, the market is divided into automotive, marine, power and energy storage, consumer electronics, and others. The report also covers the market size and forecasts for the market across the world. For each segment, market sizing and forecasts have been done based on revenue (USD billion).

| Automotive Batteries |

| Consumer Electronics Batteries |

| Industrial and ESS Batteries |

| Manufacturing Scrap |

| Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) |

| Lithium Nickel Manganese Cobalt (NMC) |

| Lithium Nickel Cobalt Aluminium (NCA) |

| Lithium Manganese Oxide (LMO) |

| Lithium Titanate (LTO) |

| Hydrometallurgical |

| Pyrometallurgical |

| Direct/Mechanical |

| Hybrid and Emerging (Bio/ Electro-chemical) |

| Collection and Logistics |

| Dismantling and Discharge |

| Mechanical Shredding/Sorting |

| Black-Mass Production |

| Material Refining and Recovery |

| Cathode Active Materials |

| Anode/Graphite |

| Battery-grade Lithium Compounds |

| Cobalt and Nickel Salts |

| Manganese |

| Others (Cu, Al) |

| Automotive |

| Marine |

| Power and Energy Storage |

| Consumer Electronics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By End-of-Life Source | Automotive Batteries | |

| Consumer Electronics Batteries | ||

| Industrial and ESS Batteries | ||

| Manufacturing Scrap | ||

| By Battery Chemistry | Lithium Cobalt Oxide (LCO) | |

| Lithium Iron Phosphate (LFP) | ||

| Lithium Nickel Manganese Cobalt (NMC) | ||

| Lithium Nickel Cobalt Aluminium (NCA) | ||

| Lithium Manganese Oxide (LMO) | ||

| Lithium Titanate (LTO) | ||

| By Recycling Technology | Hydrometallurgical | |

| Pyrometallurgical | ||

| Direct/Mechanical | ||

| Hybrid and Emerging (Bio/ Electro-chemical) | ||

| By Process Stage | Collection and Logistics | |

| Dismantling and Discharge | ||

| Mechanical Shredding/Sorting | ||

| Black-Mass Production | ||

| Material Refining and Recovery | ||

| By Application of Recovered Materials | Cathode Active Materials | |

| Anode/Graphite | ||

| Battery-grade Lithium Compounds | ||

| Cobalt and Nickel Salts | ||

| Manganese | ||

| Others (Cu, Al) | ||

| By End-user Industry | Automotive | |

| Marine | ||

| Power and Energy Storage | ||

| Consumer Electronics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the lithium-ion battery recycling market in 2026?

The lithium-ion battery recycling market size is projected at USD 5.07 billion in 2026, on its way to USD 14.79 billion by 2031.

Which segment will add the most absolute revenue through 2031?

Automotive end-of-life batteries will add the most revenue as mass-market EVs sold after 2019 retire in large numbers.

Why is LFP chemistry challenging for recyclers?

LFP contains no cobalt and less lithium per kilogram, cutting black-mass value by about 65% versus NMC and compressing margins.

What technology is growing fastest?

Direct or mechanical recycling is expanding at roughly 28.7% CAGR thanks to lower energy intensity and high recovery rates.

How do U.S. regulations influence plant siting decisions?

IRA domestic-content rules and DOE loan programs steer new capacity to the United States to qualify batteries for tax credits.

When will grid-scale batteries become a meaningful feedstock?

Utility storage systems installed in 2020-2022 start retiring around 2030, creating a second, chemistry-homogenous wave of LFP packs.

Page last updated on: