EV Battery Reuse Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

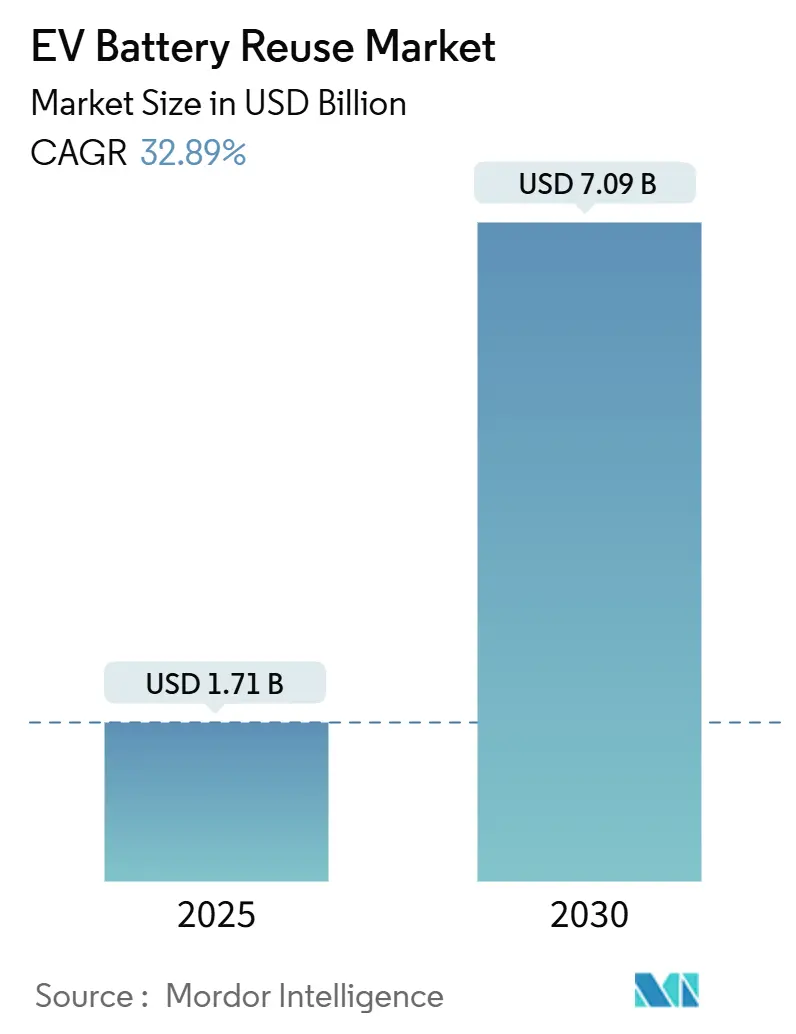

| Market Size (2025) | USD 1.71 Billion |

| Market Size (2030) | USD 7.09 Billion |

| Growth Rate (2025 - 2030) | 32.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EV Battery Reuse Market Analysis by Mordor Intelligence

The EV Battery Reuse Market size is estimated at USD 1.71 billion in 2025, and is expected to reach USD 7.09 billion by 2030, at a CAGR of 32.89% during the forecast period (2025-2030).

This rapid trajectory stems from falling lithium-ion prices, stringent producer-responsibility laws, and maturing diagnostic technologies that jointly expand addressable second-life opportunities.[1]European Parliament & Council, “Regulation (EU) 2023/1542 on batteries,” europarl.europa.euGrid-scale storage, EV charging support, and microgrids account for most deployments, while rising fire-safety standards and digital battery passports improve stakeholder confidence. Market leaders pilot multi-MWh systems that deliver 30-50% cost savings versus new packs, underlining strong cost-benefit economics. Asia-Pacific maintains dominance because China processes more than 580,000 tons of retired NEV batteries annually, but North America and Europe accelerate through public-funded microgrid programs and mandatory collection targets.

Key Report Takeaways

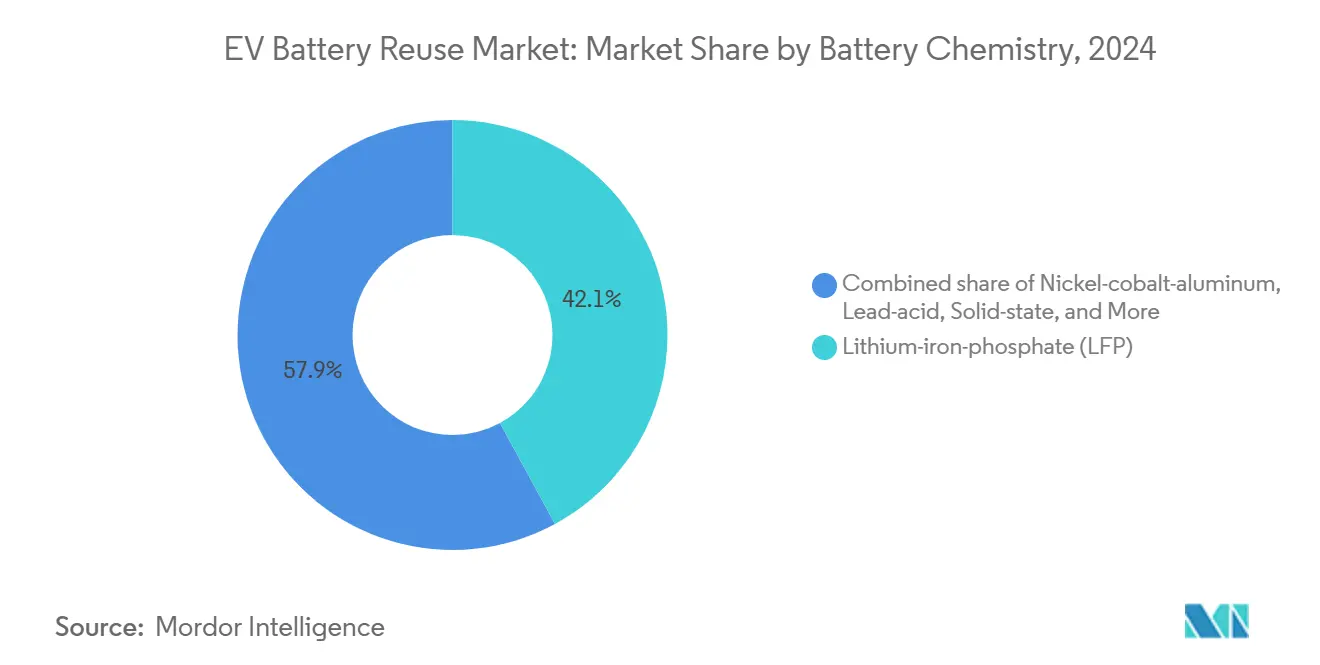

- By chemistry, LFP batteries held 42.1% of the EV battery reuse market share in 2024; NCA is projected to post the fastest 36.3% CAGR through 2030.

- By application, grid-scale storage captured 49.8% revenue in 2024, while charging-infrastructure buffering is forecast to expand at a 37.2% CAGR to 2030.

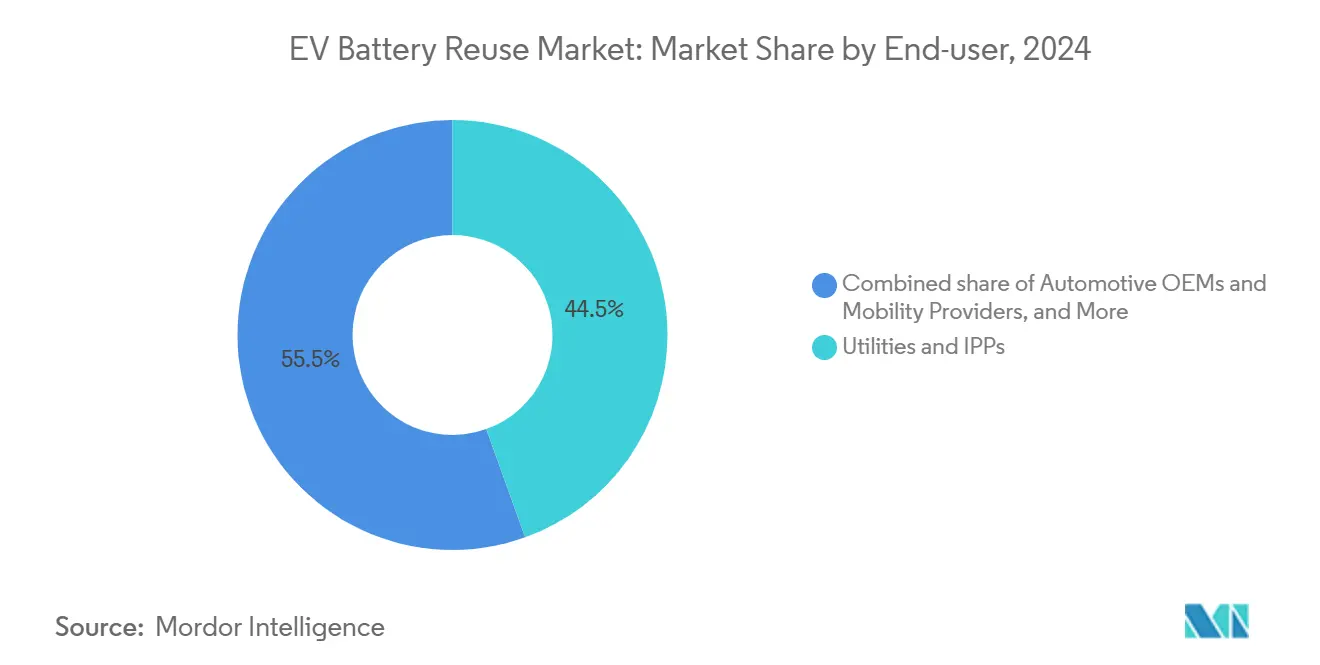

- By end-user, utilities controlled 44.5% of demand in 2024, whereas automotive OEM initiatives will advance at a 36.8% CAGR during the outlook period.

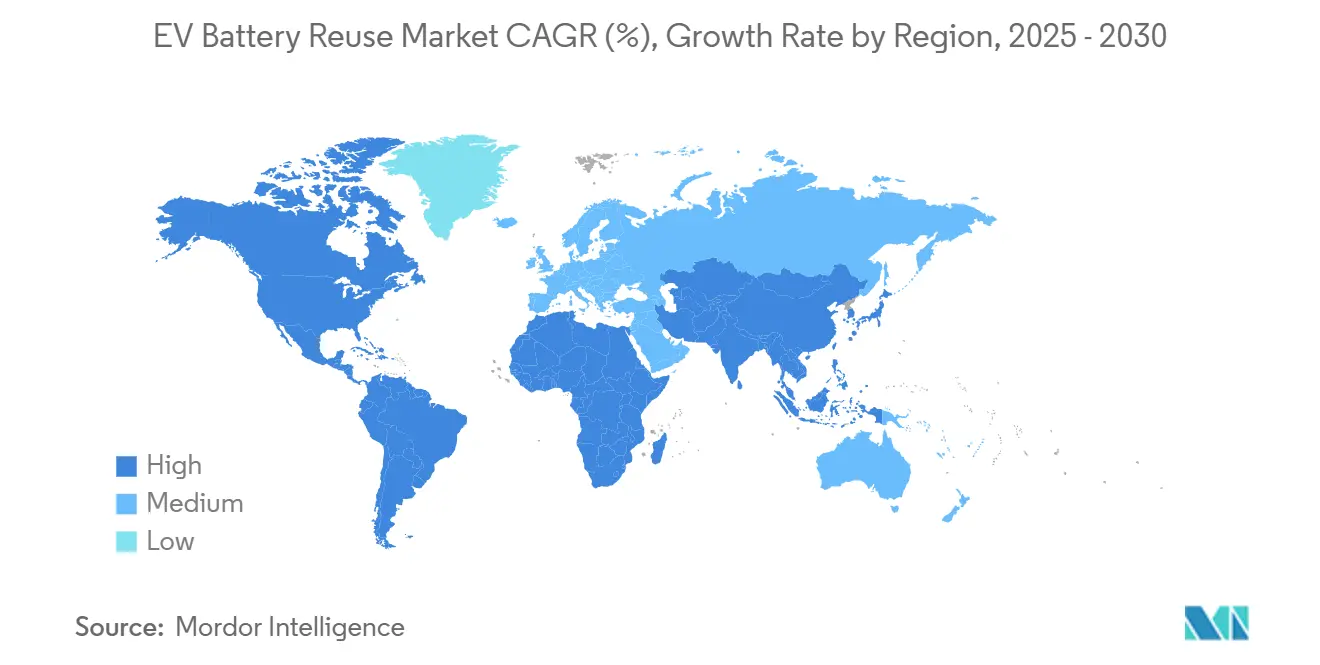

- By geography, Asia-Pacific accounted for the largest share, 35.7% in 2024, and is also likely to grow the fastest, at a CAGR of 35.9% through 2030.

Global EV Battery Reuse Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decline in EV-grade Li-ion battery costs | 8.20% | Global, APAC lead | Medium term (2-4 years) |

| Surging grid-scale ESS demand for frequency balancing | 7.80% | North America & EU | Long term (≥4 years) |

| OEM circular-economy mandates & EPR regulations | 6.40% | EU core, North America spill-over | Short term (≤2 years) |

| Emerging global second-life battery certification schemes | 4.10% | EU & Japan | Medium term (2-4 years) |

| AI-enabled SoH analytics unlocking pack-level reuse | 3.80% | APAC core | Long term (≥4 years) |

| Microgrid adoption in underserved regions | 2.60% | Global rural focus | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid decline in EV-grade Li-ion battery costs

Pack prices are trending toward USD 100-120 per kWh for LFP in 2025, down from USD 150 per kWh in 2024, with outlooks indicating USD 80 per kWh by 2026.[2]SpiderWay Research, “2025 Battery Price Outlook,” spiderway.com Such compression widens the arbitrage between retired and new units because second-life packs retain 70-80% capacity. Argonne projects automotive packs at USD 86 per kWh by 2035, with tax-credit scenarios lowering costs to USD 56 per kWh, supporting broader stationary adoption.[3]Argonne National Laboratory, “Li-ion Cost Projections 2025-2035,” anl.gov Recycled-material integration further cuts production expenses, sustaining a favourable spread for reuse.

Surging grid-scale ESS demand for frequency balancing

Renewable integration raises the need for flexible storage. Element Energy’s 53 MWh Texas plant shows reused batteries can shave 30-50% off system CAPEX while meeting grid requirements. California trials prove second-life packs cut demand charges and generate demand-response revenue, boosting commercial case studies.[4]California Energy Commission, “Second-Life Battery Demand Charge Study,” energy.ca.gov U.S. DOE’s ERA program dedicates USD 1 billion to rural clean-energy projects, many of which specify second-life storage.

OEM circular-economy mandates & EPR regulations

The EU Battery Regulation 2023/1542 forces producers to collect 51% of light-transport batteries by 2028 and include minimum recycled-content thresholds by 2031. New Jersey enacted the first U.S. EPR statute for EV packs, compelling OEM take-back schemes. BMW’s tie-up with SK Tes builds a closed loop that re-injects cobalt, nickel, and lithium into new cells.

Emerging global second-life battery certification schemes

IEC 63338, issued in 2024, sets reuse guidelines, and Japan’s Battery Association adopted aligned protocols to standardize safety. From 2026, the EU requires digital passports for packs above 2 kWh, making asset data fully traceable. UL 9540A/B testing upgrades address thermal-runaway propagation, boosting installer and insurer confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of unified reuse standards & testing protocols | -4.70% | Global | Short term (≤2 years) |

| Residual-value warranty and liability uncertainty | -3.90% | North America & EU | Medium term (2-4 years) |

| High reverse-logistics & diagnostic costs | -3.20% | Global; remote regions | Medium term (2-4 years) |

| Fire-safety perception of repurposed packs | -2.80% | Developed markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Lack of unified reuse standards & testing protocols

Fragmented rulebooks inflate compliance costs as firms juggle multiple certification ladders. New Zealand’s trade group notes absent of national guidance hampers insurer acceptance and narrows coverage. Until IEC 63338 gains universal adoption, exporters face heterogenous quality thresholds across borders, constraining scale.

Residual-value warranty and liability uncertainty

Insurers report a 17% rise in battery-fire claims, prompting policy exclusions for reused packs. Transport rules force stringent UN testing, raising refurbishment costs. California’s 8-year, 70%-capacity warranty benchmark adds residual-value pressure on reuse aggregators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: LFP cost edge underpins leadership

LFP commanded 42.1% of the EV battery reuse market 2024, outpacing NMC and NCA varieties due to lower cost, thermal stability, and long cycle life. NCA batteries are projected to grow at a 36.3% CAGR, leveraging high energy density suitable for data-center backup roles. CATL’s 99.6% material-recovery rate illustrates chemistry-agnostic circularity potential. Over the forecast window, the EV battery reuse market size for LFP systems is expected to rise with surging Chinese EV output. Meanwhile, emerging solid-state formats may enter pilot reuse programs post-2028 as safety and scalability improve.

Second-life economics favor whole-pack redeployment when residual capacity exceeds 75%, translating to seven to ten additional years of stationary duty. NMC packs remain plentiful because of legacy EV fleet volumes, sustaining a significant contribution despite higher degradation. Hybrid lead-acid use cases shrink, while Ni-MH moves toward obsolescence as OEMs migrate to lithium and sodium chemistries.

By Application: Grid storage anchors demand; charging support accelerates

Grid-scale ESS absorbed 49.8% of 2024 revenue thanks to frequency-balancing and peak-shaving projects that capitalize on moderate power requirements. The segment enjoyed early regulatory clarity and PPA-based cash flows, reinforcing bankability. Charging-infrastructure buffering shows the sharpest ascent with a 37.2% CAGR, as network operators deploy behind-the-meter units to avoid upgrade fees and smooth renewable intermittency. For instance, Electrify America’s 30 MW second-life portfolio spans 140 DC fast sites, trimming demand charges materially.

Industrial backup, telecom towers, and emerging marine backups diversify the opportunity set, each favoring cost savings over maximum energy density. The EV battery reuse market size for microgrid and off-grid deployments is poised to expand alongside rural-electrification grants and corporate net-zero targets. Application diversity mitigates over-reliance on any end-market and cushions against cyclical EV sales swings.

By End-User: Utilities dominate; OEM-led loops surge

Utilities and IPPs captured 44.5% of 2024 uptake, integrating repurposed packs into renewable portfolios to comply with dispatchable-capacity rules. OEMs represent the fastest-growing buyer pool at a 36.8% CAGR because EPR statutes drive vertical integration and lifecycle accountability. LG Energy Solution and Toyota’s Green Metals Battery Innovations JV highlights the shift, processing 13,500 t of black mass annually for cathode feedstock. The EV battery reuse market share held by utilities should slip modestly as automotive self-consumption rises.

Commercial & industrial campuses leverage demand-charge abatement and backup reliability, while residential deployment scales after UL 9540B cuts permitting friction. EPCs increasingly choose modular second-life racks because 50 kWh building blocks simplify O&M. Nissan’s Energy Share program in Japan shows how bidirectional V2G schemes monetize parked EVs and sharpen the reuse value chain

Geography Analysis

Asia-Pacific accounted for 35.7% of global revenue in 2024 and will post a 35.9% CAGR by 2030, underpinned by China’s 580,000-ton retired-battery stream and a nationwide collection network covering 85% of volume. CATL’s 37.5% global cell share ensures robust feedstock and technological leadership as it scales 30,000 swapping stations by 2030. Japan and South Korea collaborate with EU partners to harmonize digital passport data frameworks, fostering cross-border trade.

North America accelerates on the back of DOE funding and state-level EPR mandates. Element Energy’s 53 MWh Texas facility validates multi-hour grid services using retired packs, amplifying investor confidence. New Jersey’s legislation sets a U.S. precedent for producer responsibility, and California’s warranty rules refine consumer safeguards. Canada ties into continental recovery hubs, yet a unified federal framework remains pending.

Europe advances through the EU Battery Regulation’s 2026 passport deadline and escalating collection quotas. Germany spearheads recycling alliances like BASF-Stena, while Nordic ferry electrification experiments create maritime second-life niches. The UK readies for bi-directional charging law changes by 2026, tapping Nissan LEAF batteries to cut household energy costs by 50%. Emerging regions in LATAM and Africa look to donor-funded microgrids to jump-start adoption; however, capacity-building for reverse logistics and safety oversight remains essential.

Competitive Landscape

The EV battery reuse market exhibits moderate fragmentation with a tendency toward consolidation as scale economies and traceability requirements intensify. Redwood Materials processes the highest U.S. volume of spent packs and now pivots toward second-life ESS modules, potentially eclipsing pure recycling revenue by 2028. Element Energy specializes in utility-grade redeployment, securing offtake contracts that prove bankability for reused assets.

Automakers embed circular loops: BMW collaborates with SK Tes across Europe, recovering strategic metals for new cells. Toyota and LG Energy Solution partner on U.S. black-mass processing to comply with Inflation Reduction Act sourcing rules. Digital-platform innovators such as Cling Systems facilitate global trading via blockchain provenance, while Volytica Diagnostics supplies AI health-scoring that underpins warranty products. Start-ups like Circunomics and Voltfang attract venture capital, indicating a fertile environment for software-hardware synergies.

Competitive differentiation hinges on state-of-health analytics, automated pack-level grading, and modular rack design that tolerates heterogeneous chemistries. Fire-mitigation engineering and insurance underwriting partnerships emerge as gating factors for accelerating utility procurement pipelines.

EV Battery Reuse Industry Leaders

Nissan 4R Energy Corp.

B2U Storage Solutions

Spiers New Technologies

BeePlanet Factory

Fortum Battery Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: GM partnered with Redwood Materials to build ESS units from recycled and new packs.

- June 2025: LG Energy Solution and Toyota launched Green Metals Battery Innovations JV, targeting 13,500 t annual black-mass throughput.

- June 2025: Nissan LEAF packs repurposed at Rome Fiumicino Airport, powering critical infrastructure.

- May 2025: Voltfang installed large-scale second-life storage in Germany for grid balancing.

Global EV Battery Reuse Market Report Scope

| Lithium-iron-phosphate (LFP) |

| Nickel-manganese-cobalt (NMC) |

| Nickel-cobalt-aluminum (NCA) |

| Nickel-metal-hydride (NiMH) |

| Lead-acid |

| Solid-state |

| Grid-scale Energy Storage Systems |

| EV Charging Infrastructure Buffering |

| Industrial and Data-center Backup Power |

| Telecom Towers/Remote BTS |

| Off-grid Solar and Microgrids |

| Marine and Light-Rail Auxiliary Power |

| Utilities and IPPs |

| Commercial and Industrial Facilities |

| Residential and Community Energy |

| Automotive OEMs and Mobility Providers |

| EPCs/Project Developers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Chemistry | Lithium-iron-phosphate (LFP) | |

| Nickel-manganese-cobalt (NMC) | ||

| Nickel-cobalt-aluminum (NCA) | ||

| Nickel-metal-hydride (NiMH) | ||

| Lead-acid | ||

| Solid-state | ||

| By Application | Grid-scale Energy Storage Systems | |

| EV Charging Infrastructure Buffering | ||

| Industrial and Data-center Backup Power | ||

| Telecom Towers/Remote BTS | ||

| Off-grid Solar and Microgrids | ||

| Marine and Light-Rail Auxiliary Power | ||

| By End-user | Utilities and IPPs | |

| Commercial and Industrial Facilities | ||

| Residential and Community Energy | ||

| Automotive OEMs and Mobility Providers | ||

| EPCs/Project Developers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the EV battery reuse market in 2025?

The EV battery reuse market size is projected to surpass USD 1.6 billion in 2025, continuing its 32.89% CAGR trajectory.

Which application uses the most second-life batteries?

Grid-scale energy-storage systems account for nearly half of all repurposed-battery revenues in 2025.

Why do utilities favor second-life packs over new ones?

Utilities realize 30-50% capital savings and still meet frequency-balancing and peak-shaving performance needs.

What role do digital battery passports play?

Passports record manufacturing and usage data, streamlining state-of-health validation and cross-border compliance.

How long can a retired EV battery operate in stationary service?

Packs retaining 70-80% capacity can serve an additional seven-to-ten years in stationary roles before final recycling.

Page last updated on: