Market Overview

| Study Period | 2021 - 2031 |

|---|---|

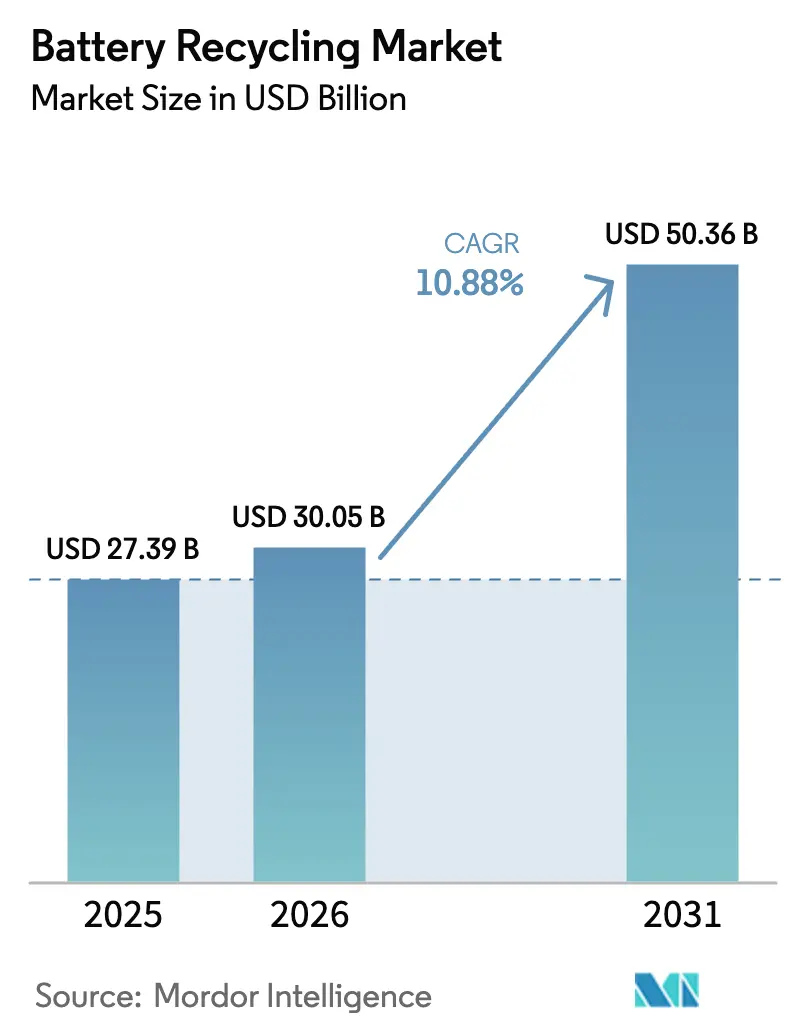

| Market Size (2026) | USD 30.05 Billion |

| Market Size (2031) | USD 50.36 Billion |

| Growth Rate (2026 - 2031) | 10.88% CAGR |

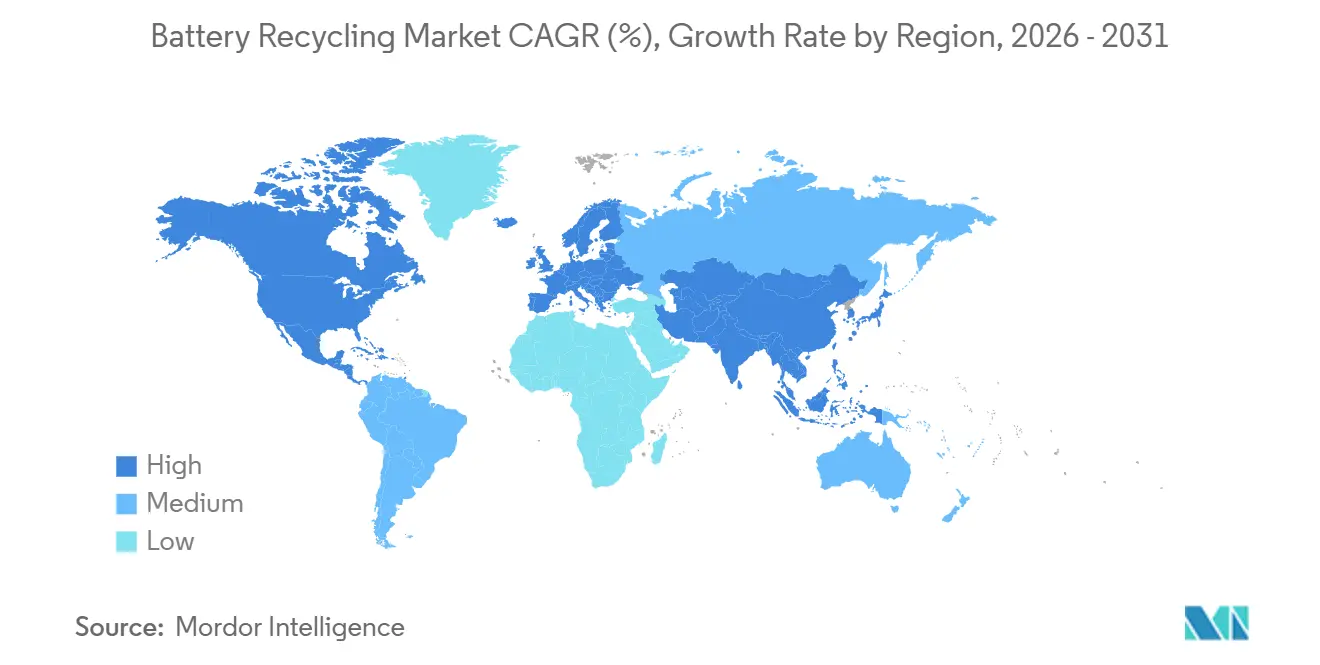

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

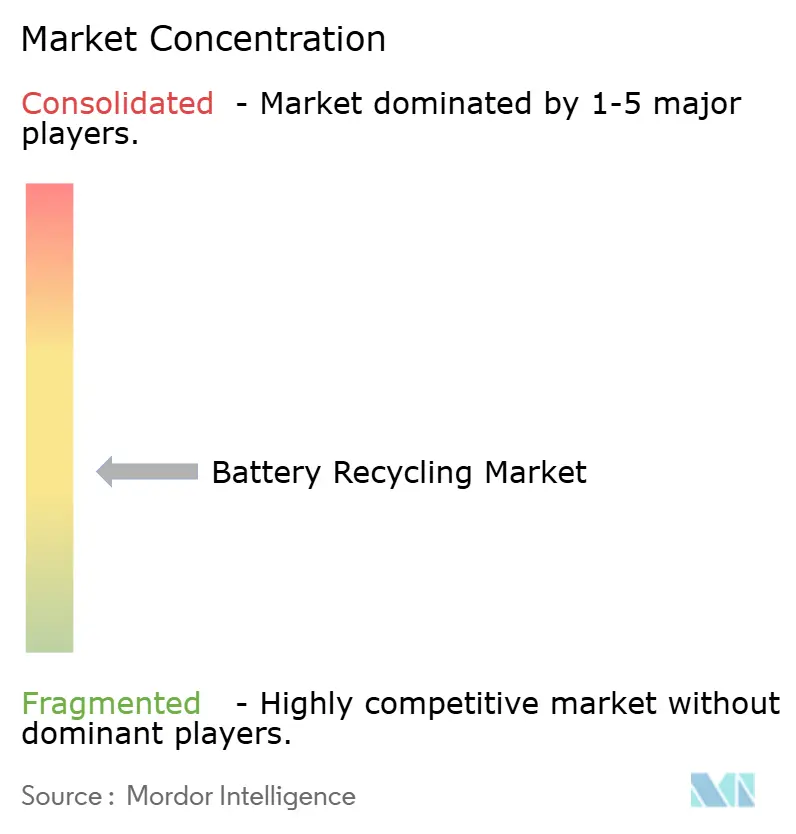

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Recycling Market Analysis by Mordor Intelligence

The Battery Recycling Market size is expected to grow from USD 27.39 billion in 2025 to USD 30.05 billion in 2026 and is forecast to reach USD 50.36 billion by 2031 at 10.88% CAGR over 2026-2031.

The expansion is underpinned by extended-producer-responsibility mandates, rising critical-metal scarcity, and automaker commitments to closed-loop cathode supply chains that treat end-of-life cells as strategic feedstock rather than waste. Lead-acid batteries retained dominant volumes thanks to mature collection networks, yet lithium-ion chemistries are gaining ground as electric-vehicle (EV) penetration accelerates and legacy automotive lead-acid demand plateaus.[1]International Energy Agency, “Global EV Outlook 2025,” iea.org Hydrometallurgical routes are scaling quickly because they deliver high-purity nickel and cobalt sulfates demanded by cathode producers, while direct-recycling pilots show energy savings that could cut pack costs by USD 1,000 per vehicle once commercialized. Regionally, Asia-Pacific anchors more than half of revenue due to China’s integrated gigafactory-recycler clusters, whereas North America posts the fastest growth as the Inflation Reduction Act incentives subsidize domestic black-mass refining.[2]European Commission, “Regulation (EU) 2023/1542 on Batteries,” eur-lex.europa.eu

Key Report Takeaways

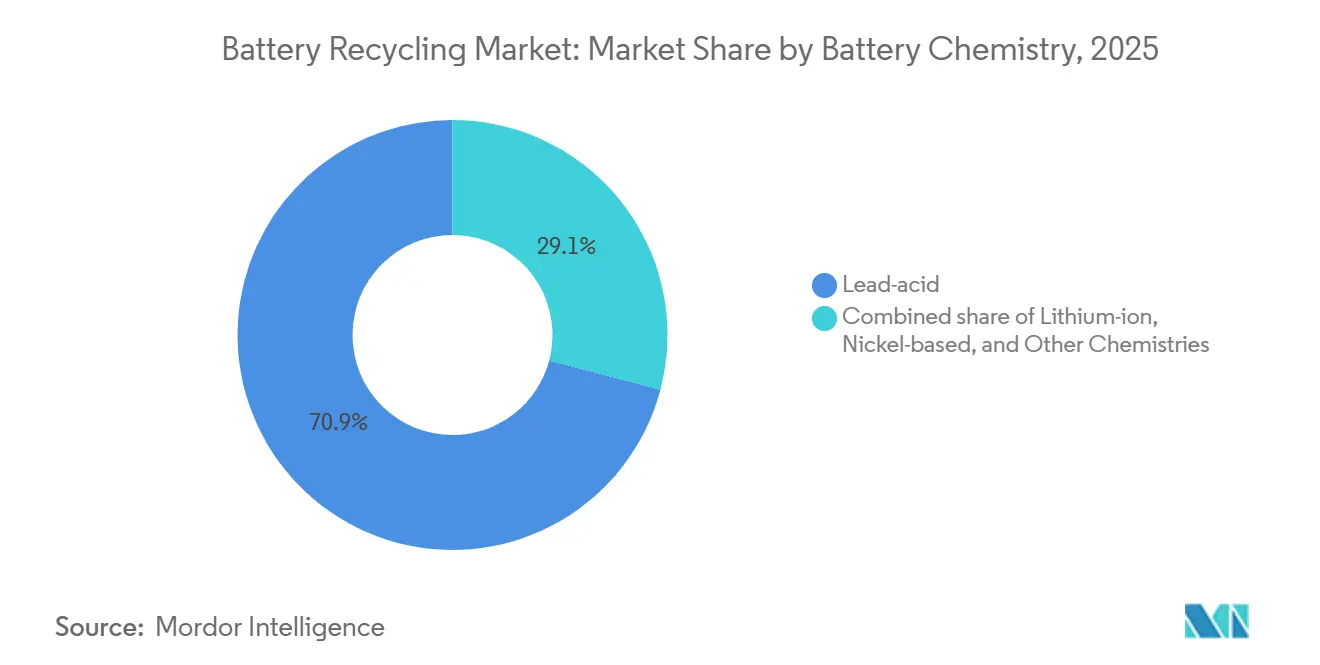

- By battery chemistry, lead-acid held 70.9% of the battery recycling market share in 2025; lithium-ion is forecast to grow at a 23.9% CAGR through 2031.

- By source of scrap, automotive batteries led with 58.5% of the battery recycling market share in 2025, while consumer electronics batteries are projected to rise at a 20.5% CAGR through 2031.

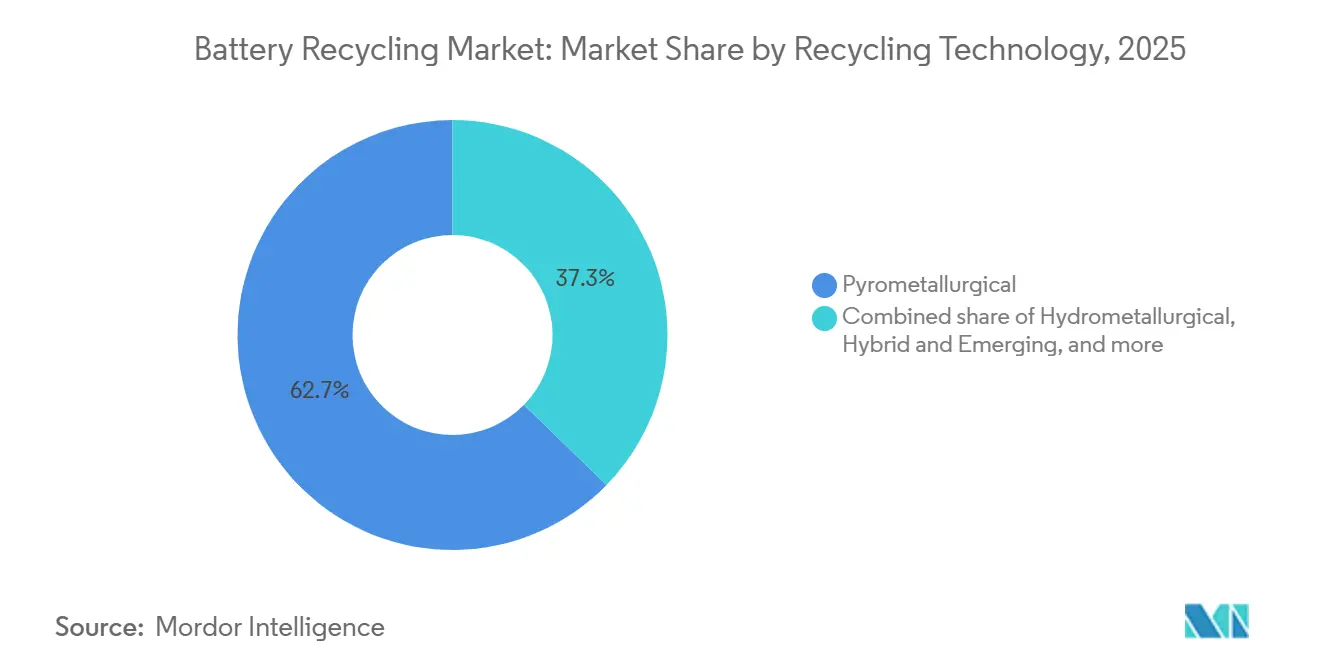

- By recycling technology, pyrometallurgy led with a 62.7% share in 2025, while hydrometallurgy is advancing at a 22.7% CAGR to 2031.

- By process stage, material refining and recovery accounted for 28.6% of the battery recycling market size in 2025, while black-mass production is forecast to advance at a 25.1% CAGR to 2031.

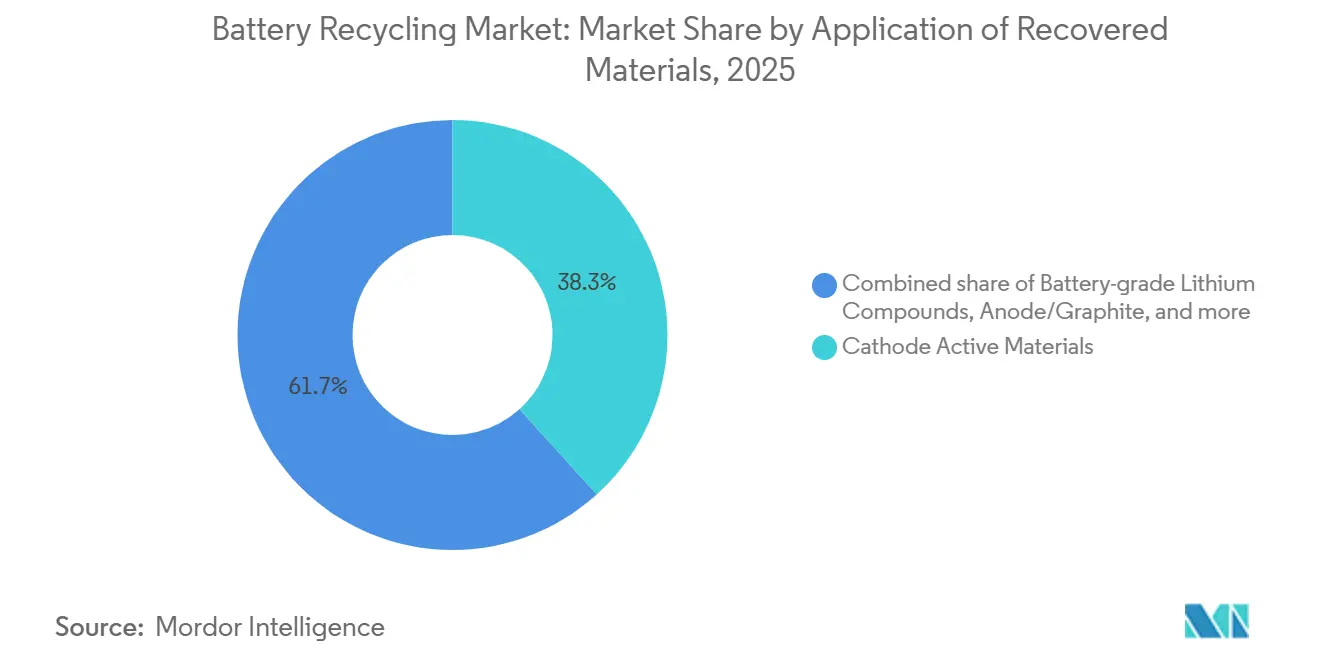

- By application of recovered materials, the cathode active materials segment claimed 38.3% of revenue in 2025, whereas battery-grade lithium compounds are expected to register the highest growth at 27.6% CAGR over 2026-2031.

- By end-user industry, automotive captured 43.1% of the battery recycling market size in 2025, and power & energy storage is climbing at a 19.8% CAGR to 2031.

- By geography, Asia-Pacific commanded 52.4% revenue in 2025; North America is projected to expand at a 21.3% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Battery Recycling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV penetration surge | +3.2% | Global, strongest in China, EU, North America | Medium term (2-4 years) |

| Global end-of-life battery rules tighten | +2.1% | EU, China, North America; emerging India & ASEAN | Long term (≥ 4 years) |

| Critical-metal price inflation | +1.8% | Global, acute where cathode imports dominate | Short term (≤ 2 years) |

| OEM ESG & circular-economy mandates | +1.5% | North America, EU; pilots in Japan, South Korea | Medium term (2-4 years) |

| Liquid black-mass spot markets emerge | +1.1% | China, EU; nascent North America | Short term (≤ 2 years) |

| Break-through direct-recycling economics | +0.9% | North America, EU; R&D in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV penetration surge

Global battery-electric and plug-in hybrid sales passed 14 million units in 2024, embedding roughly 1.1 TWh of lithium-ion capacity that will reach end-of-life after 2032, creating a predictable feedstock wave.[3]International Energy Agency, “Global EV Outlook 2025,” iea.org Tesla recovered 92% of critical minerals from retired packs at its Nevada facility, proving technical feasibility at scale. China projects 12 million t of retired lithium-ion cells by 2030, triple the current global recycling capacity. Europe’s tightening fleet-average CO₂ limits accelerate EV adoption and bring first-generation packs into dismantling networks earlier.[4]European Commission, “Regulation (EU) 2023/1542 on Batteries,” eur-lex.europa.eu The lag between sales and retirements compresses the window for recyclers to build capacity and secure offtake agreements with cathode makers.

Global End-of-Life Battery Regulations Tighten

The EU Battery Regulation requires 16% recycled cobalt, 6% recycled lithium, and 6% recycled nickel in new EV batteries by 2031, with steeper thresholds by 2036. China’s 2024 extended-producer-responsibility rules oblige automakers to finance collection networks and reach 85% lithium-ion recovery, alongside penalties up to CNY 500,000 per violation. The U.S. Environmental Protection Agency proposed a stewardship framework in 2025 that would impose producer fees on cells lacking certified recycling pathways. India’s draft EPR rules target 70% collection by 2028 but lack enforcement clarity. These policies reduce revenue volatility for recyclers but fragment supply chains across jurisdictions.

Critical-Metal Price Inflation

Lithium carbonate averaged CNY 95,000 (USD 13,400) t in Q4 2024, still 180% above 2020 levels. Cobalt sulfate traded near USD 12,800 t in December 2024 as artisanal-mining governance issues in the Democratic Republic of Congo added risk premiums. Nickel sulfate suitable for batteries reached USD 16,200 t in early 2025 amid Indonesian ore-export curbs. Recycled cathode precursors now sell only 5-8% below virgin equivalents, improving recycler margins as volumes rise.

OEM ESG & Circular-Economy Mandates

Volkswagen aims to source 50% of cathode nickel and cobalt from recycled content by 2030 and is co-locating hydrometallurgical refining at its Salzgitter gigafactory. General Motors signed a 50,000 t y black-mass offtake pact with Cirba Solutions through 2030. BMW reached 30% recycled content in Neue Klasse cells via direct-recycling pilots that cut processing energy 40% versus hydro routes. Such mandates lock recyclers into long-term supply contracts, de-risking capital expenditure but concentrating buyer power.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex / opex of recycling plants | -1.4% | Global, acute where subsidies absent | Medium term (2-4 years) |

| Patchy collection logistics in emerging markets | -0.9% | India, ASEAN, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Safety & hazardous-material transport hurdles | -0.7% | Global, most stringent in EU & North America | Short term (≤ 2 years) |

| Shift to low-value LFP chemistries | -1.2% | China, India; spreading to entry EV segments elsewhere | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex / Opex of Recycling Plants

A 20,000 t y hydrometallurgical facility requires USD 180-250 million, with reactors and solvent-extraction trains comprising 60% of the installed cost. Operating expenses range USD 1,800-2,400 t input, driven by acid consumption and wastewater treatment. Li-Cycle’s Rochester Hub budget ballooned from USD 485 million to USD 960 million by mid-2024, exposing cost-overrun risk. Smaller firms in emerging markets face debt costs of 18-22%, widening the infrastructure gap.

Patchy Collection Logistics in Emerging Markets

India’s formal lithium-ion collection rate was 28% in 2024, with the rest funneled to informal dismantlers lacking discharge protocols, wasting 30-40% recoverable material. Indonesia operates collection points in only 12 of 34 provinces, and reverse logistics from outer islands can exceed USD 150 t. Sub-Saharan Africa recovers under 5% of EV batteries, and Brazil’s collection lags in municipalities below 100,000 residents, keeping volumes below the 15,000 t scale needed for hydro plant viability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Lead-Acid Dominates Revenue, Lithium-Ion Drives Growth

Lead-acid retained 70.9% of 2025 revenue as nearly 99% of spent units are collected in developed markets and recycled through established smelters.[5]Battery Council International, “U.S. Lead-Acid Recycling Statistics 2025,” batterycouncil.org Lithium-ion’s 23.9% CAGR signals where the battery recycling market is pivoting; International Energy Agency data show 1.8 million t of lithium-ion scrap annually by 2030, creating an addressable battery recycling market size surge. Incumbent lead-acid recyclers are modernizing pyro lines, while new entrants finance hydrometallurgical hubs to capture upcoming lithium-rich flows. Redwood Materials processed 18,000 t of lithium-ion scrap in 2024, confirming commercial momentum.

The battery recycling market is therefore split: lead-acid offers stable, low-growth cash flows; lithium-ion offers high-growth, technology-intensive upside. Competitive advantage will hinge on securing EV-derived feedstock ahead of the post-2028 inflection and on achieving metal-recovery rates above 90% to satisfy automaker specifications.

By Source of Scrap: Automotive Dominates, Consumer Electronics Accelerates

Automotive batteries supplied 58.5% of 2025 throughput, reflecting large lead-acid replacement volumes and early EV retirements such as 2013-16 Nissan Leaf packs. Consumer electronics scrap is expanding 20.5% CAGR as device lifecycles shorten; however, sub-40% collection rates reveal upside for policy-driven capture programs. Manufacturing scrap delivers high-purity feedstock and turns inventory within 45 days at CATL’s Ningde campus, improving working capital compared with post-consumer flows.

Rapid consumer electronics growth ensures the battery recycling market continues diversifying feedstock, reducing reliance on automotive volumes, and improving blended margins as clean manufacturing scrap offsets lower-grade household batteries.

By Recycling Technology: Pyrometallurgy Holds Scale, Hydrometallurgy Gains Precision

Pyrometallurgy provided 62.7% of the 2025 capacity because existing copper and nickel smelters can accept mixed chemistries without pre-sorting. Yet hydrometallurgy is growing 22.7% CAGR as cathode producers demand battery-grade nickel sulfate with ≤50 ppm impurities, a purity that pyro slag cannot cost-effectively achieve. Direct-recycling pilots account for 8.4% today but could carve high-margin niches once homogeneous EV scrap streams become available.

Hydrometallurgy’s rise will lift the battery recycling market share of high-value converted salts, while pyro lines may shift toward lower-value, cobalt-lean LFP and stationary-storage scrap where absolute purity is less critical.

By Process Stage: Refining Anchors Value, Black-Mass Surges

Material refining and recovery contributed 28.6% of 2025 revenue, delivering USD 1,200-1,800 t gross margin owing to technical barriers and permitting complexity. Black-mass production is the fastest riser at 25.1% CAGR as vertically integrated cell makers bypass third-party smelters. CATL’s Brunp subsidiary already runs 180,000 t/y of black-mass lines feeding captive cathode plants.

The battery recycling market size for black-mass tolling will therefore expand rapidly, yet ultimate value capture rests with refiners that can supply battery-grade salts under automaker quality contracts.

By Application of Recovered Materials: Cathode Actives Lead, Lithium Compounds Accelerate

Cathode-active materials secured 38.3% of the 2025 value as LG Energy Solution, SK On, and Samsung SDI consumed 42,000 t of recycled precursors. Recycled lithium compounds are forecast at a 27.6% CAGR, lifted by direct-recycling yields of 95-98% lithium recovery. Anode and graphite initiatives remain R&D-stage, and manganese recovery fetches one-tenth the cobalt price, keeping it a marginal revenue stream.

Accelerating lithium recovery ensures the battery recycling market maintains competitiveness against new brine and hard-rock projects, particularly in jurisdictions with strong environmental-permitting hurdles.

By End-User Industry: Automotive Anchors Demand, Energy Storage Surges

Automotive consumed 43.1% of recycled-battery output in 2025 as OEMs hedge cobalt and nickel exposure through closed-loop programs. Power and energy-storage systems represent the fastest-growing demand at 19.8% CAGR, driven by first-wave utility-scale lithium-ion retirements and second-life repurposing economics that extend pack life by up to 10 years.

Utility growth diversifies the battery recycling industry customer base, reducing correlation with automotive cycles and providing a stable offtake for lithium-rich black mass.

Geography Analysis

Asia-Pacific captured 52.4% of 2025 revenue, led by China's vertically integrated ecosystem where recycler-gigafactory clusters reach 88-92% metal-recovery through hydro routes. The national battery passport, launched in 2024, tags every cell for traceability, cutting contamination by 15-18%. Japan processed 68,000 t of NiMH and lithium-ion scrap, recovering rare-earth elements at Toyota-Sumitomo's Onahama smelter. South Korea's fee-backed EPR scheme lifted lithium-ion recovery to 72% by end-2025. India has 42,000 t capacity, but informal dismantlers still siphon 60% of volumes.

North America is the fastest-growing region at 21.3% CAGR. Section 45X provides a USD 10 kWh production credit for recycled material, and Section 30D requires 50% battery value from North America or FTA partners by 2026. Redwood Materials is investing USD 3.5 billion in a 100 GWh cathode-anode campus, with 30% recycled feedstock. Li-Cycle's Rochester Hub secured a USD 475 million DOE loan guarantee, targeting late-2026 commissioning. Canada earmarked CAD 1.5 billion for recycling infrastructure, with Glencore and Electra expanding hydrometallurgy in Quebec and Ontario.

Europe's share is also increasing at a high rate, driven by rNorthvolt'stent strong mandates. Northvolt's Revolt facility achieved 95% lithium, nickel, and cobalt recovery at 8,000 t throughput and targets 125,000 t/y by 2030. Germany granted EUR 200 million to Duesenfeld and Accurec for 50,000 tFrance'sd hydro capacity. France's Veolia-Solvay JV will build a 15,000 t plant in ACC 'sirk, co-located with ACC's gigafactory. South America and MEA combined for share, limited to Brazil's network and South Africa's Eco-Bat smelter; large-scale lithium-ion projects await higher EV penetration.

Competitive Landscape

The top 10 recyclers controlled roughly 50% of global throughput in 2025; no single company exceeded 12% share, yielding a moderately fragmented structure. Legacy lead-acid firms like Eco-Bat and Glencore leverage existing smelters, while lithium-focused specialists such as Redwood Materials, Li-Cycle, and Ascend Elements compete on hydrometallurgical purity and direct-recycling innovation. Chinese incumbents CATL, GEM, and Brunp exploit captive gigafactory scrap and internal transfer pricing that undercuts merchant recyclers by up to 15%.

Cirba Solutions consolidated Retriev and Heritage Battery Recycling and secured USD 200 million from Koch Strategic Platforms to lift capacity to 120,000 t y by 2027. Neometals’ mixed-hydroxide-precipitate process recovers 96% lithium, allowing only a 3% discount versus virgin carbonate. Patent filings in direct recycling jumped 140% from 2022-2024, signaling intensifying intellectual-property competition. Scale, vertical integration, and process IP will dictate future share shifts as the battery recycling market evolves.

Battery Recycling Industry Leaders

Brunp Recycling Technology

Li-Cycle Holdings Corp.

Umicore SA

GEM Co. Ltd.

Glencore plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Botree Recycling Technologies raised new capital to broaden its proprietary extraction footprint to 10 countries, including a joint venture for closed-loop recycling.

- May 2025: LG Energy Solution and Derichebourg formed a European recycling JV, amplifying regional circular-economy initiatives.

- April 2025: Green Li-ion opened a commercial plant in Oklahoma that converts unsorted waste into precursor cathode active material in 12 hours, cutting emissions up to 90%.

- December 2024: American Battery Technology Company secured USD 150 million DOE funding for a 100,000 tpa Nevada facility.

- September 2025: CATL committed CNY 8 billion to double Brunp capacity to 350,000 t y by 2028, with 50% feedstock sourced from retired energy-storage systems.

- March 2025: Li-Cycle secured USD 75 million equity from Glencore, plus a 10-year offtake for Rochester Hub black mass, enabling construction restart.

Global Battery Recycling Market Report Scope

Battery recycling is the practice of reusing and reprocessing batteries to reduce the quantity disposed of as material waste. Batteries comprise several poisonous chemicals and heavy metals, and their disposal has attracted environmental concerns due to contamination of water and soil. As such, batteries need recycling to comply with environmental and health benefits.

The Global Battery Recycling Market Report is Segmented by Battery Chemistry (Lead-acid, Lithium-ion, Nickel-based, Other chemistries), Source of Scrap (Automotive, Consumer Electronics, Industrial and ESS, Manufacturing Scrap), Recycling Technology (Hydrometallurgical, Pyrometallurgical, Direct/Mechanical, Hybrid and Emerging), Process Stage (Collection and Logistics, Dismantling and Discharge, Mechanical Shredding/Sorting, Black-Mass Production, Material Refining and Recovery), Application of Recovered Materials (Cathode Active Materials, Anode/Graphite, Battery-grade Lithium Compounds, Cobalt and Nickel Salts, Manganese, Others), End-user Industry (Automotive, Marine, Power and Energy Storage, Consumer Electronics, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Battery Chemistry

| Lead-acid |

| Lithium-ion (NMC, LFP, NCA, LMO) |

| Nickel-based |

| Other chemistries (Zn-air, Sodium-ion etc.) |

By Source of Scrap

| Automotive Batteries |

| Consumer Electronics Batteries |

| Industrial and ESS Batteries |

| Manufacturing Scrap |

By Recycling Technology

| Hydrometallurgical |

| Pyrometallurgical |

| Direct/Mechanical |

| Hybrid and Emerging (Bio/ Electro-chemical) |

By Process Stage

| Collection and Logistics |

| Dismantling and Discharge |

| Mechanical Shredding/Sorting |

| Black-Mass Production |

| Material Refining and Recovery |

By Application of Recovered Materials

| Cathode Active Materials |

| Anode/Graphite |

| Battery-grade Lithium Compounds |

| Cobalt and Nickel Salts |

| Manganese |

| Others (Cu, Al) |

By End-user Industry

| Automotive |

| Marine |

| Power and Energy Storage |

| Consumer Electronics |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Chemistry | Lead-acid | |

| Lithium-ion (NMC, LFP, NCA, LMO) | ||

| Nickel-based | ||

| Other chemistries (Zn-air, Sodium-ion etc.) | ||

| By Source of Scrap | Automotive Batteries | |

| Consumer Electronics Batteries | ||

| Industrial and ESS Batteries | ||

| Manufacturing Scrap | ||

| By Recycling Technology | Hydrometallurgical | |

| Pyrometallurgical | ||

| Direct/Mechanical | ||

| Hybrid and Emerging (Bio/ Electro-chemical) | ||

| By Process Stage | Collection and Logistics | |

| Dismantling and Discharge | ||

| Mechanical Shredding/Sorting | ||

| Black-Mass Production | ||

| Material Refining and Recovery | ||

| By Application of Recovered Materials | Cathode Active Materials | |

| Anode/Graphite | ||

| Battery-grade Lithium Compounds | ||

| Cobalt and Nickel Salts | ||

| Manganese | ||

| Others (Cu, Al) | ||

| By End-user Industry | Automotive | |

| Marine | ||

| Power and Energy Storage | ||

| Consumer Electronics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the battery recycling market today and where is it headed by 2031?

The battery recycling market size reached USD 30.05 billion in 2026 and is projected to climb to USD 50.36 billion by 2031 at a 10.88% CAGR.

Which battery chemistry offers the strongest growth opportunity for recyclers?

Lithium-ion scrap is forecast to expand at a 23.9% CAGR through 2031 as EV retirements accelerate, outpacing mature lead-acid volumes.

Why is hydrometallurgy gaining share over pyrometallurgy?

Hydrometallurgical processes yield battery-grade nickel and cobalt sulfates with impurity levels below 50 ppm, meeting cathode-maker specifications that pyrometallurgical slag cannot achieve economically.

How do government incentives in North America support recycling investment?

Section 45X of the Inflation Reduction Act awards USD 10 kWh for recycled battery materials, while DOE loan programs have financed large projects such as Li-Cycles Rochester Hub and Ascend Elements Apex plant.

What limits recycling expansion in emerging markets?

Patchy collection logistics, informal dismantling networks, and high capital-cost financing keep formal recovery rates below 40% in India, ASEAN, and parts of Africa.

Will low-value LFP chemistries hurt recycler margins?

LFP's lower cobalt and nickel content reduces black-mass value by up to 65%, pressuring profit unless recyclers adopt direct-recycling routes that recover lithium efficiently.

Page last updated on: