Battery Backup Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

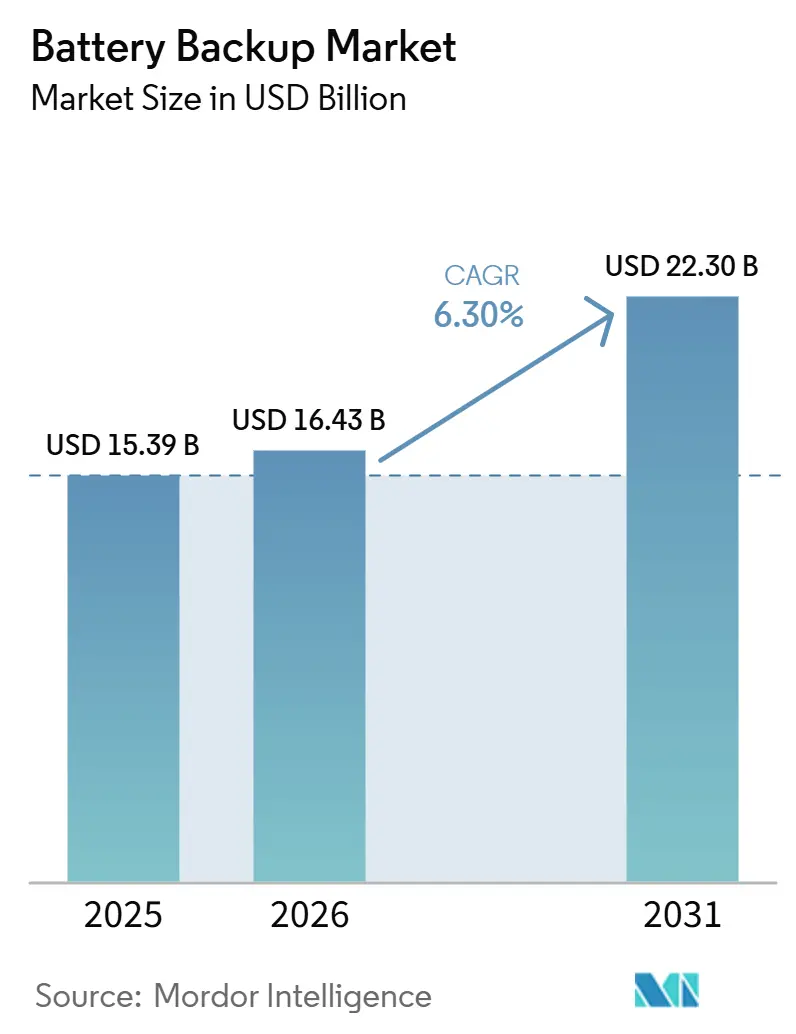

| Market Size (2026) | USD 16.43 Billion |

| Market Size (2031) | USD 22.30 Billion |

| Growth Rate (2026 - 2031) | 6.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Backup Market Analysis by Mordor Intelligence

The Battery Backup Market size is projected to be USD 15.39 billion in 2025, USD 16.43 billion in 2026, and reach USD 22.30 billion by 2031, growing at a CAGR of 6.30% from 2026 to 2031. The growth in hyperscale data center construction, the densification of small-cell 5G networks, and advancements in AI-enabled battery management are reshaping the economics of uptime and expanding the battery backup market. Lithium-ion systems are increasingly replacing lead-acid batteries in power-intensive applications due to declining cell prices and higher energy density, which enable longer runtimes within the same rack space. Additionally, manufacturing facilities are leveraging predictive analytics alongside backup power systems to minimize unplanned shutdowns, highlighting the market's shift toward software-driven reliability. Suppliers incorporating long-duration chemistries, such as vanadium redox flow batteries, are addressing utility resilience requirements in regions prone to weather-related grid disruptions. Meanwhile, competition from Asian manufacturers offering modular lithium-ion UPS solutions at a lower total cost of ownership is exerting pressure on traditional players, leading to compressed gross margins.

Key Report Takeaways

- By battery type, lead-acid captured 53.5% of the battery backup market share in 2025, while lithium-ion is projected to expand at a 10.6% CAGR to 2031.

- By power rating, sub-10 kVA systems accounted for 47.9% share of the battery backup market size in 2025 and are expected to advance at a 7.1% CAGR through 2031.

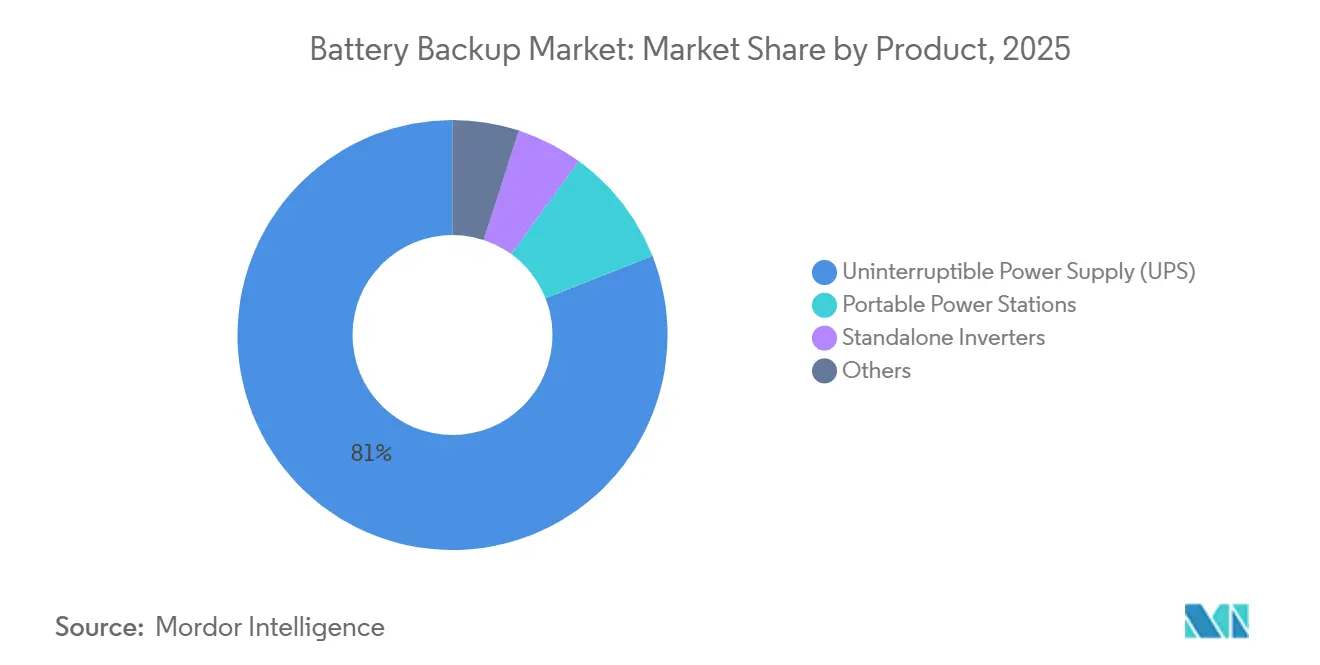

- By product, UPS platforms led with 81.0% revenue share in 2025, whereas standalone inverters are expected to record the strongest 9.4% CAGR outlook to 2031.

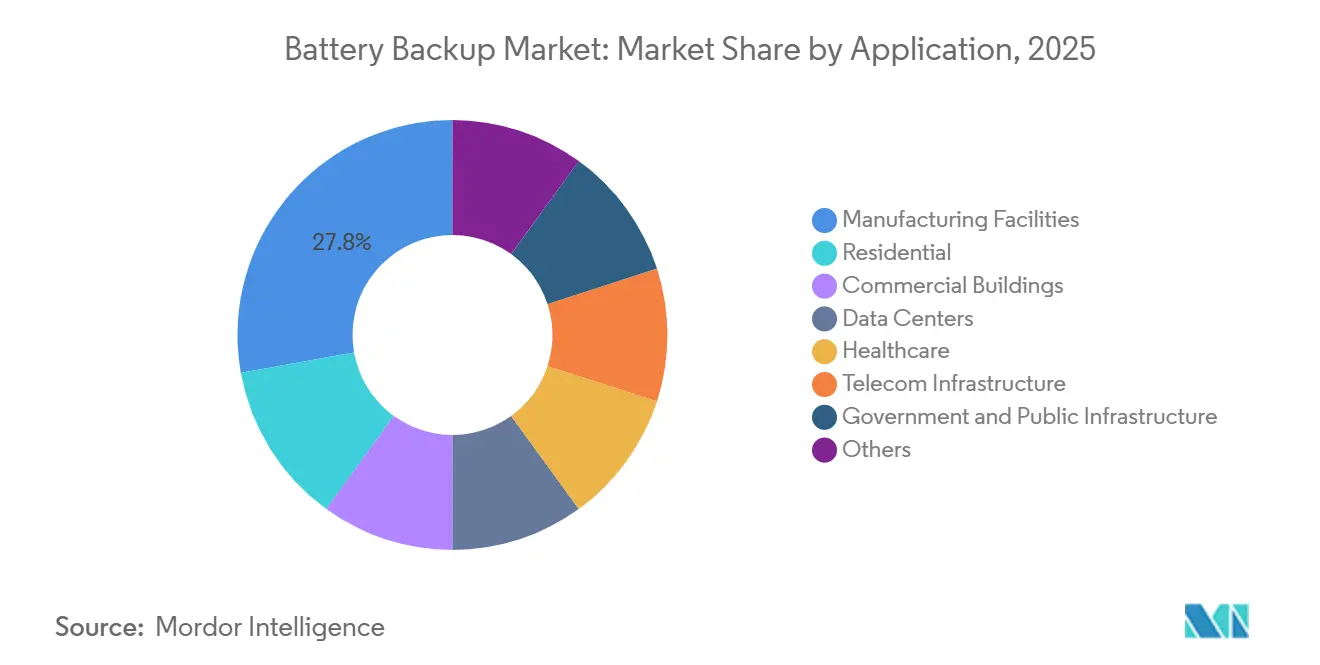

- By application, data centers are projected to record the highest CAGR of 11.3% CAGR, surpassing manufacturing facilities that held 27.8% revenue share in 2025.

- By end-use, commercial enterprises represented 52.2% share in 2025 and are slated for an 8.0% CAGR as Scope-3 reporting reshapes procurement.

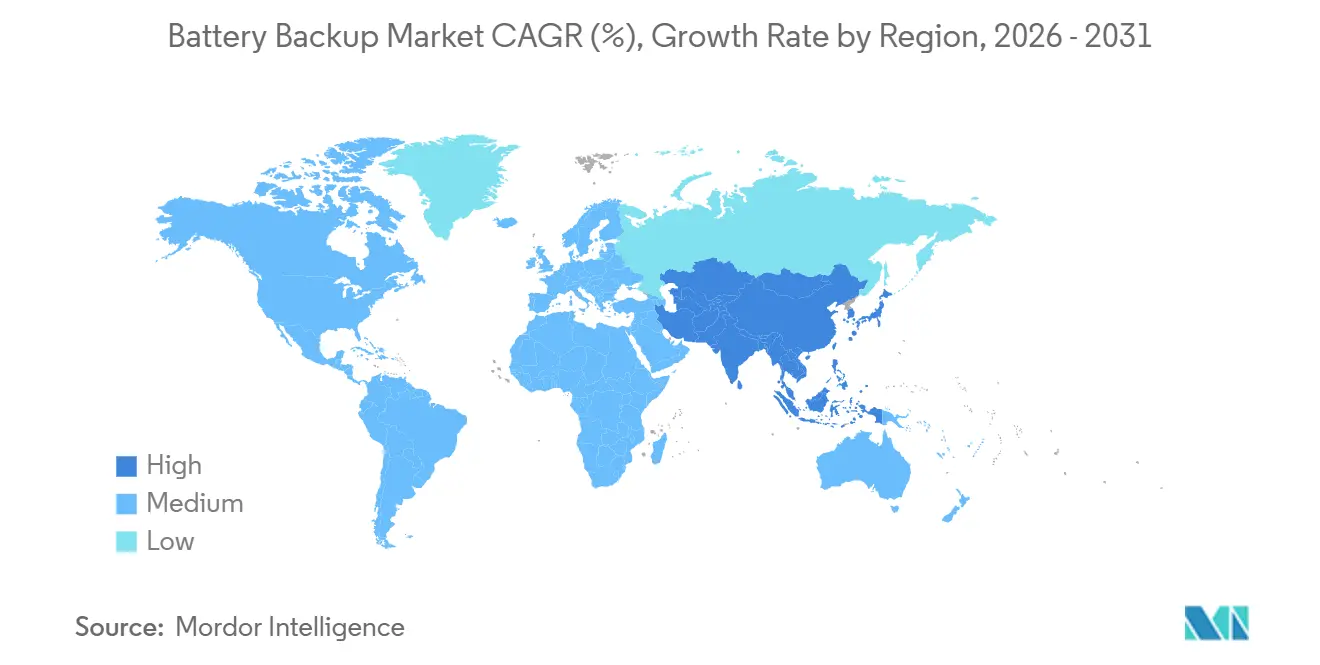

- By geography, North America dominated with 36.1% share in 2025, but Asia-Pacific is expected to show the highest 7.8% CAGR thanks to China’s 180 GW storage target.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Battery Backup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Center Proliferation | +1.8% | North America, Asia-Pacific, Western Europe | Medium term (2-4 years) |

| Rising Grid-Instability Outages | +1.2% | Global, pronounced in Texas, California, India, South Africa | Short term (≤ 2 years) |

| Telecom 5G Roll-Out Densification | +1.0% | China, South Korea, India, North America, Europe | Medium term (2-4 years) |

| AI-Based Predictive BMS Adoption | +0.9% | Early adoption in North America and Europe, global expansion potential | Long term (≥ 4 years) |

| Corporate Scope-3 Supply-Chain Mandates | +0.7% | Europe (CSRD), North America (SEC rules), multinational corporate supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Center Proliferation

Hyperscale operators now require backup systems capable of two- to four-hour support to ensure uninterrupted operation of AI inference clusters, which cannot tolerate even short disruptions. Data center capacity in the United States is projected to reach 7.7 GW by 2025, with Northern Virginia accounting for over 2.8 GW.[1]JLL Research, “U.S. Data Center Market Report Q3 2025,” jll.com Google’s work with Form Energy on a 300 MW iron-air system signals a willingness to diversify beyond lithium-ion for multi-day protection.[2]Form Energy, “Google Partnership on Iron-Air Batteries,” formenergy.comMicrosoft and Meta's capital spending surpassed USD 23 billion during 2024-2025, establishing higher density benchmarks achievable only through lithium-ion or hybrid flow solutions. Downtime costs exceeding USD 10,000 per minute have justified the adoption of premium chemistries, prompting insurance companies to require compliance with NFPA 855 and UL 9540A standards. This compliance adds 8-12% to installation costs. Consequently, the battery backup market has become more robust and resilient, supported by software that enhances cycling efficiency, thermal management, and cell matching.

Rising Grid-Instability Outages

Severe weather conditions and aging transmission infrastructure have led to frequent service interruptions, driving businesses to reevaluate the economic impact of outages. According to ERCOT data, installed battery capacity increased from less than 0.5 GW in 2021 to an expected 17 GW by 2025, accounting for 9% of peak demand during extreme events.[3]ERCOT, “Battery Storage Capacity Report 2025,” ercot.comCalifornia recorded over 25,000 power-quality incidents in 2024, leading to new utility mandates requiring critical sites to maintain self-sufficient battery reserves. Rapid sales growth in India and ongoing load shedding in South Africa highlight the increasing need for reliable backup solutions in emerging markets. Customers are increasingly prioritizing grid-forming and black-start capabilities, driving demand for hybrid inverter-UPS platforms. These requirements broaden the functional scope of the battery backup market and benefit vendors that integrate power electronics, software, and storage chemistry effectively.

Telecom 5G Roll-Out Densification

Small-cell architectures necessitate compact and lightweight batteries that can be installed on poles, rooftops, and concealed street furniture. Starting in 2024, China Tower has mandated the use of lithium-ion batteries in all new 5G installations, achieving a 60% reduction in system footprint compared to lead-acid batteries.[4]China Tower Corp., “5G Lithium-Ion Mandate,” china-tower.comBy the end of 2025, South Korea is expected to have 230,000 base stations equipped with 48-V lithium strings, providing a runtime of 4-8 hours under stringent reliability standards. In North America, carriers are retrofitting existing towers with high-cycle modules to support edge computing. Meanwhile, European operators highlight supply chain vulnerabilities due to reliance on a limited number of cell vendors to meet volume demands. These factors are driving growth in the battery backup market by integrating high-density battery chemistry with telecom expansion strategies.

AI-Based Predictive BMS Adoption

Machine-learning algorithms capable of estimating the state of charge with nearly 1% accuracy can delay battery replacement by up to two years, thereby lowering lifecycle costs and reducing the carbon footprint. Early adopters in the data center and healthcare industries report a 25-30% reduction in unplanned service calls after implementing cloud-connected Battery Management Systems (BMS). Additionally, insurers are offering lower premiums for UL 9540A-certified predictive systems, highlighting the growing integration of software value with hardware in the battery backup market. Manufacturers without digital expertise face the risk of commoditization, as customers increasingly prioritize analytics dashboards over traditional ampere-hour specifications when making purchasing decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility of Lithium Raw Materials | -1.1% | Global, sharp swings in Australia, Chile, and China supply hubs | Short term (≤ 2 years) |

| Lead-Acid Disposal Regulations Tightening | -0.8% | North America, Europe, China | Medium term (2-4 years) |

| Insurance Premium Hikes for Indoor Li-Ion | -0.6% | North America and Europe (NFPA 855 and UL 9540A jurisdictions) | Medium term (2-4 years) |

| Cyber-Risk to Smart-UPS Firmware | -0.5% | Global, concentrated in critical infrastructure sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Lithium Raw Materials

Spot prices for lithium carbonate increased to USD 20-22.50 per kg in February 2026, representing a 264% rise from the June 2025 low. This price surge has driven lithium-ion UPS costs to USD 400-500 per kWh, further widening the cost gap compared to lead-acid batteries and complicating budgets for projects awarded under fixed-price contracts. With futures markets remaining limited, suppliers have incorporated escalation clauses into purchase agreements, transferring the risk to buyers. Utility-scale procurements face the greatest challenges, as they require thousands of modules to be delivered over multiple quarters. While long-term offtake agreements with miners offer cost stability, they also commit manufacturers to volumes that may not align with short-term demand fluctuations.

Lead-Acid Disposal Regulations Tightening

Extended producer responsibility frameworks are becoming increasingly widespread. The European Battery Regulation requires an 85% collection rate and 65% recycling efficiency by 2025, with penalties for non-compliance reaching five-figure euro amounts per violation. In the United States, several states mandate that retailers accept returned units, increasing direct logistics costs. Meanwhile, China’s 2024 regulations require every producer to provide services in all prefecture-level cities. Smaller vendors without established reverse-logistics networks face challenges in meeting these requirements, driving consolidation within the battery backup market. Users are responding by opting for lithium-ion batteries, despite higher initial costs, as they involve less compliance paperwork and reduced future liabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Lithium-Ion Gains Amid Lead-Acid Dominance

In 2025, lead-acid technology accounted for 53.5% of revenue, supported by established supply chains and recycling channels that kept acquisition costs low. Lithium-ion batteries, projected to grow at a CAGR of 10.6% through 2031, are increasingly favored in hyperscale data centers and telecom towers due to their higher energy density and longer cycle life, despite higher initial costs. This trend is driving growth in the battery backup market at the chemistry level. Flow batteries, such as Rongke Power’s 200 MW/1 GWh system commissioned in 2026, address utility requirements for extended durations exceeding four hours, presenting a growing alternative for resilience.

However, battery preferences vary by application. Manufacturing facilities with infrequent power outages continue to opt for lead-acid batteries, as their total cost of ownership remains advantageous with shallow discharge cycles. In contrast, residential solar installers in India increasingly integrate lithium-ion modules, facilitated by ten-year financing options that distribute the higher upfront costs and meet rooftop weight constraints. Emerging technologies like zinc-ion and sodium-ion batteries are under pilot testing, signaling ongoing diversification, though commercial scalability is still several years away. With multiple chemistries competing, the battery backup market accommodates both cost-effective incumbents and high-performance alternatives.

By Power Rating: Sub-10 kVA Units Anchor Edge Deployments

Systems smaller than 10 kVA accounted for a 47.9% value share in 2025 and are projected to grow at a 7.1% CAGR through 2031, driven by the increasing adoption of 5G small cells, retail point-of-sale networks, and micro-branches. These compact systems typically integrate 48-V lithium battery packs with inverter-charger electronics within a single chassis, reducing installation time and simplifying maintenance. In contrast, 10-100 kVA systems cater to mid-size offices and clinics that require higher ride-through capabilities while remaining cost-conscious. Systems above 100 kVA are predominantly used in hyperscale data centers, where hot-swappable power blocks are essential.

Procurement criteria differ based on system ratings. Buyers of sub-10 kVA systems prioritize lightweight designs that comply with pole-mounting load limits, focusing on volumetric density rather than modularity. On the other hand, megawatt-scale purchasers emphasize N+1 redundancy and often use mixed battery chemistries within the same facility to optimize performance for different rack groups. In the mid-tier range, line-interactive topologies compete on efficiency, while double-conversion architectures remain the standard for mission-critical environments. These variations across power bands ensure diverse revenue streams for the battery backup market, reducing dependency on any single segment.

By Product: UPS Systems Retain Primacy While Inverters Accelerate

UPS platforms are projected to account for 81.0% of 2025 revenue, remaining central to the battery backup market due to the critical need for uninterrupted power in data practices, medical regulations, and financial trading activities, where even millisecond transfer delays are unacceptable. Standalone inverters, on the other hand, are expected to grow at a CAGR of 9.4% through 2031, driven by increasing residential solar adoption in regions such as India, Africa, and Latin America, where users are willing to accept up to a minute of switchover time in exchange for cost savings.

The product segmentation reflects differing architectural approaches. Centralized megawatt-scale UPS systems achieve efficiency through economies of scale but pose a risk as a single point of failure. In contrast, distributed rack-level UPS systems localize faults and minimize energy losses in power distribution units. Additionally, portable power stations represent a growing segment targeting outdoor leisure and emergency applications, introducing lithium-iron-phosphate battery technology to the consumer market. All three categories are increasingly integrated with software platforms that enable firmware updates, predictive maintenance, and asset tracking, thereby expanding service revenue opportunities within the battery backup market.

By Application: Data Centers Propel Future Demand

Data centers recorded the highest compound annual growth rate (CAGR) of 11.3%, overtaking manufacturing sites as the primary driver of growth in the battery backup market. Increased AI inference per rack is resulting in higher power density (watts per square meter) and extended runtime requirements. This has led operators to adopt large lithium-ion battery systems or explore hybrid flow battery solutions. Despite this shift, manufacturing continues to account for approximately 27.8% of market revenue, driven by semiconductor fabrication facilities and automotive plants, where unexpected power interruptions can result in significant losses.

In other sectors, healthcare facilities are required to comply with NFPA 99 standards, which mandate 96-hour life support capabilities, typically achieved through UPS-generator hybrid systems. Telecom towers account for 12-15% of expenditures, while commercial campuses rely on modular battery cabinets to protect IT infrastructure, elevators, and building automation systems. Government infrastructure projects demand seismic certification and N+1 redundancy, requiring vendors to meet FEMA guidelines. Each industry vertical imposes unique technical requirements, ensuring that the battery backup market remains less susceptible to commoditization compared to other power-electronics segments.

By End-Use: Commercial Buyers Lead the Sustainability Push

Commercial enterprises accounted for 52.2% of spending in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 8.0%, driven by the influence of Scope-3 reporting on procurement priorities. Environmental, Social, and Governance (ESG) officers now mandate the adoption of lithium-ion batteries due to their lifecycle carbon intensity being 40-50% lower compared to lead-acid batteries. Industrial buyers rank second, utilizing battery backup systems to ensure safe shutdown sequences for process controllers. Residential adoption has been supported by subsidy programs such as Germany’s KfW 442 and California’s SGIP, both of which reduced system payback periods to under seven years in 2025.

Municipal operators extend acquisition cycles across multiple budget years but impose stringent documentation requirements, which smaller suppliers often find challenging to meet. As a result, the commercial segment serves as a key channel for advanced analytics, fire-safety features, and circular-economy certifications. This reinforces the segment's role in driving both volume and innovation within the broader battery backup market.

Geography Analysis

In 2025, North America retained a 36.1% market share and continued to host the largest installed base of hyperscale data centers. However, Asia-Pacific is advancing rapidly with a compound annual growth rate (CAGR) of 7.8%, as Beijing targets 180 GW of storage capacity by 2027. In the United States, federal tax credits now extend to standalone storage systems, further encouraging utility procurement. Meanwhile, Canada’s telecom and mining sectors are investing in ruggedized lithium-ion cabinets designed for sub-zero climates, emphasizing the importance of geographic-specific product adaptations.

In Europe, Germany and the United Kingdom are leading residential battery adoption. German households are projected to add 500,000 battery systems in 2025, supported by KfW subsidies that reduce capital costs by nearly one-third. The European Battery Regulation is increasing compliance costs for lead-acid battery suppliers, indirectly steering buyers toward lithium-ion or flow battery alternatives. In Southern Europe, commercial solar-plus-storage systems are gaining traction as climate-induced heat waves place additional strain on power grids.

Asia-Pacific’s growth is driven by China’s provincial subsidies, South Korea’s 2.22 GW mandate for critical reserves, and India’s 4 GW solar-storage auctions. Domestic cell manufacturers, such as CATL and LG Energy Solution, are reallocating electric vehicle production capacity to stationary storage formats to achieve higher margins. Additionally, Southeast Asian data hubs in Singapore and Indonesia are issuing tenders that reference UL 9540A testing standards, even before local regulatory codes are formalized.

Latin America is experiencing uneven but improving adoption of energy storage solutions. In Brazil, grid volatility in the Northeast is driving demand for residential inverters, while in Argentina, currency fluctuations are prompting businesses to invest in self-generation and storage as a hedge against tariff increases. In the Middle East and Africa, Saudi Arabia’s USD 50 billion Vision 2030 program and the UAE’s 1 GW storage tender are anchoring regional opportunities. South Africa’s ongoing load shedding is acting as a short-term catalyst, accelerating the commercial deployment of lithium-ion hybrid systems designed to operate in extreme thermal conditions.

Competitive Landscape

The battery backup market is moderately concentrated. Schneider Electric’s Galaxy VXL achieves 99% efficiency and a density of 1,042 kW per square meter, highlighting a shift in focus from simple capacity metrics to performance per footprint. Eaton differentiates itself through its Brightlayer analytics, which reduce unplanned downtime by 25-30%, demonstrating how software services can help maintain margins amid hardware price pressures. Vertiv, Huawei, and Delta Electronics emphasize modularity and AI-driven thermal management to appeal to colocation operators requiring rapid deployment solutions.

Asian competitors such as Kstar, Kehua Tech, and CyberPower leverage lower manufacturing costs to offer mid-tier UPS systems at prices 20-25% lower, targeting small businesses and telecom segments. Flow battery specialists Rongke Power and VFlowTech focus on long-duration grid projects, a niche where lithium-ion batteries are less competitive due to cycle-life economics. Meanwhile, Natron Energy and ZincFive promote sodium-ion and nickel-zinc technologies for data center racks, emphasizing inherent fire safety benefits that can reduce insurance costs.

Vertical integration remains a key strategic focus. Vertiv has acquired a battery cell production line in Poland to secure its supply chain, while Huawei integrates power electronics with its NetEco management suite. Patent activity indicates Schneider Electric is exploring liquid-cooled UPS systems, and Eaton is investing in load-prediction models to enhance battery cycle life. Smaller European brands such as Riello and Legrand are scaling manufacturing operations in India to remain cost-competitive. However, their limited R&D budgets for AI-driven features may leave them at a disadvantage as predictive maintenance becomes a standard expectation in the battery backup market.

Battery Backup Industry Leaders

Schneider Electric SE

Eaton Corporation plc

Vertiv Holdings Co.

Huawei Technologies Co., Ltd.

Delta Electronics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Rongke Power commissioned a 200 MW, 1 GWh vanadium redox flow battery in Jimusaer, China, investing CNY 3.8 billion (USD 530 million) to stabilize renewable integration.

- January 2026: LG Energy Solution began domestic production of lithium-iron-phosphate ESS modules, targeting 1 GWh annual capacity.

- October 2025: Schneider Electric unveiled Boost Pro storage, scalable from 200 kWh to 2 MWh for commercial campuses.

- December 2024: Schneider Electric unveiled the Galaxy VXL UPS delivering up to 1.25 MW at 99% eConversion efficiency.

Global Battery Backup Market Report Scope

A battery backup is an emergency power system that supplies electricity to devices immediately when the primary power source fails. Commonly referred to as an Uninterruptible Power Supply (UPS) for electronics, it utilizes stored energy to maintain the operation of equipment such as computers, routers, and alarms, enabling safe shutdown or continued functionality during brief outages.

The Battery Backup Market is segmented into battery type, power rating, product, application, end-use, and geography. By battery type, the market is segmented into lead-acid, lithium-ion, nickel-based, flow battery, and other battery types. By power rating, the market is segmented into below 10 kVA, 10–100 kVA, and above 100 kVA. By product, the market is segmented into UPS, standalone inverters, portable power stations, and other products. By application, the market is segmented into various residential, commercial, industrial, and utility applications. By end-use, the market is segmented into residential, commercial, industrial, telecommunications, healthcare, data centers, and other end-use sectors. The report also covers the market size and forecasts for the battery backup market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Lead-acid Battery |

| Lithium-ion Battery |

| Nickel-based Battery |

| Flow Battery & Other Advanced Batteries |

| Below 10kVA |

| 10 kVA to 100 kVA |

| Above 100 kVA |

| Uninterruptible Power Supply (UPS) |

| Standalone Inverters |

| Portable Power Stations |

| Others |

| Residential |

| Manufacturing Facilities |

| Commercial Buildings |

| Data Centers |

| Healthcare |

| Telecom Infrastructure |

| Government and Public Infrastructure |

| Others |

| Residential |

| Commercial |

| Industrial |

| Municipal/Government |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Type | Lead-acid Battery | |

| Lithium-ion Battery | ||

| Nickel-based Battery | ||

| Flow Battery & Other Advanced Batteries | ||

| By Power Rating | Below 10kVA | |

| 10 kVA to 100 kVA | ||

| Above 100 kVA | ||

| By Product | Uninterruptible Power Supply (UPS) | |

| Standalone Inverters | ||

| Portable Power Stations | ||

| Others | ||

| By Application | Residential | |

| Manufacturing Facilities | ||

| Commercial Buildings | ||

| Data Centers | ||

| Healthcare | ||

| Telecom Infrastructure | ||

| Government and Public Infrastructure | ||

| Others | ||

| By End-Use | Residential | |

| Commercial | ||

| Industrial | ||

| Municipal/Government | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the market size of battery backup market?

The battery backup market size stands at USD 16.43 billion in 2026 and is projected to reach USD 22.3 billion by 2031, growing at a 6.3% CAGR.

Which chemistry will gain the most share by 2031?

Lithium-ion is projected to grow at a 10.6% CAGR, gaining ground over lead-acid in telecom, commercial, and hyperscale data-center deployments.

Why are insurance premiums rising for indoor lithium-ion systems?

Fire-safety rules under NFPA 855 and UL 9540A add detection, suppression, and testing costs, prompting insurers to charge 8-12% higher premiums.

What factors limit lithium-ion adoption in price-sensitive markets?

Volatility in lithium carbonate prices and higher capital expense keep lead-acid attractive for non-critical or infrequently cycled loads.

Which region offers the highest growth potential after 2026?

Asia-Pacific, driven by China's 180 GW storage target and South Korea's 2.22 GW mandate, posts the strongest 7.8% CAGR outlook.

How concentrated is vendor revenue today?

The top five suppliers command about 48% of global sales, placing the market in a moderate-concentration tier that favors incumbents yet still enables new entrants.

Page last updated on: