Energy Storage Battery For Microgrids Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

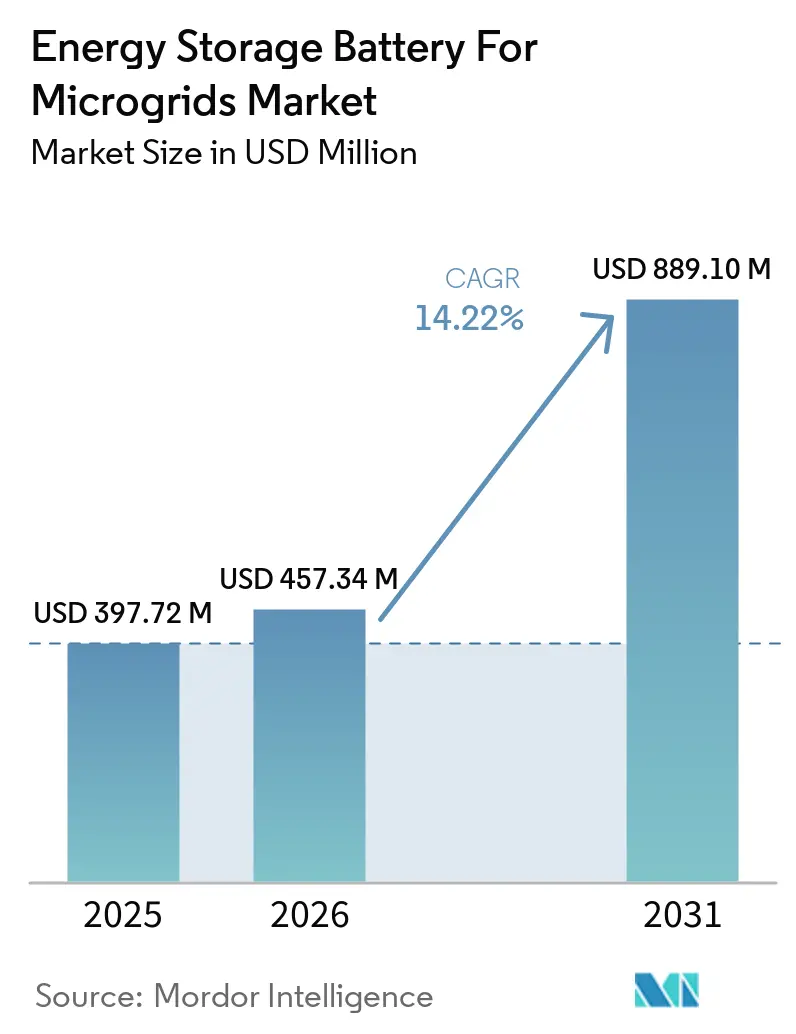

| Market Size (2026) | USD 457.34 Million |

| Market Size (2031) | USD 889.10 Million |

| Growth Rate (2026 - 2031) | 14.22% CAGR |

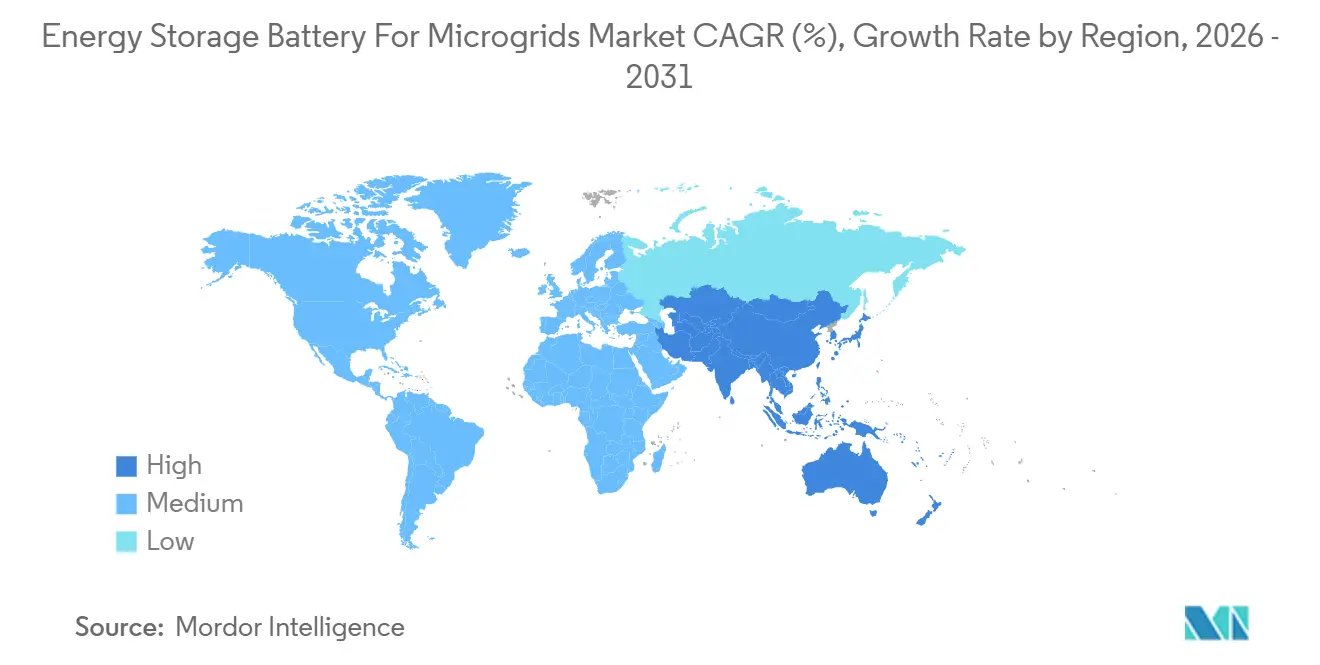

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

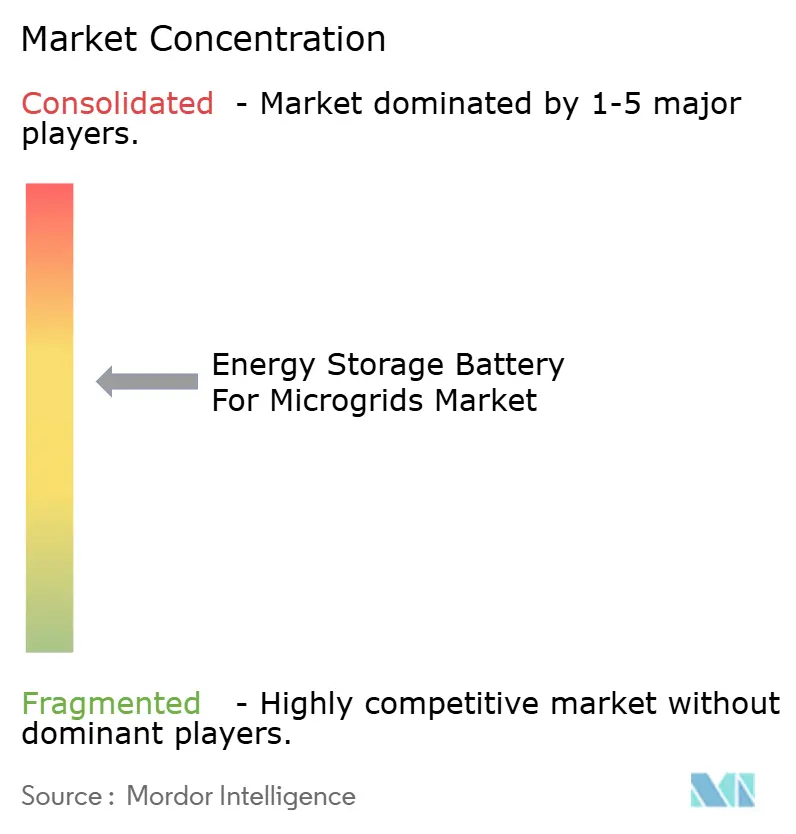

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Energy Storage Battery For Microgrids Market Analysis by Mordor Intelligence

The Energy Storage Battery For Microgrids Market size was valued at USD 397.72 million in 2025 and is estimated to grow from USD 457.34 million in 2026 to reach USD 889.10 million by 2031, at a CAGR of 14.22% during the forecast period (2026-2031). Falling lithium-iron-phosphate (LFP) cell costs, rising microgrid-specific incentives, and more frequent extreme-weather events are lifting global demand for resilient distributed systems. Lithium-ion technologies remain the performance benchmark, yet sodium variants are closing the gap in cost-sensitive, long-duration roles. Utilities in hurricane- and wildfire-prone zones are front-loading procurement schedules as regulators classify microgrids as critical infrastructure. Open-source controller standards are lowering integration expenses, while hybrid solar-storage-diesel architectures are displacing single-fuel backup schemes, especially in regions with volatile diesel logistics.

Key Report Takeaways

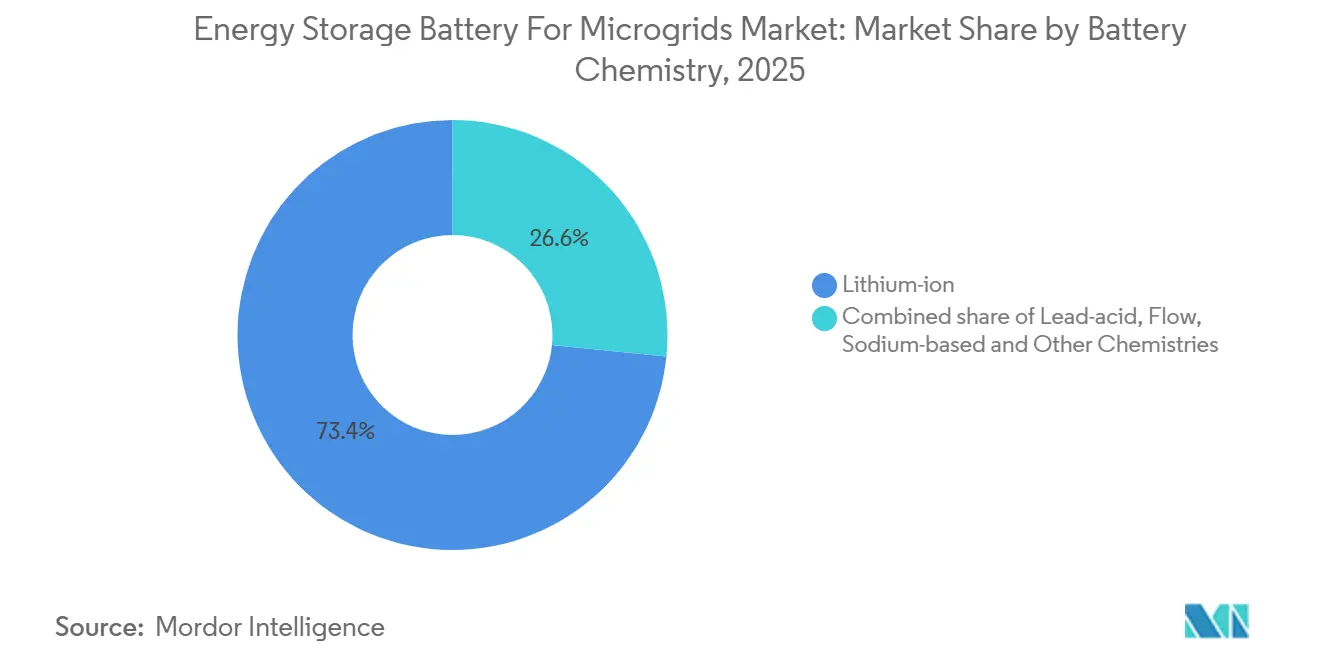

- By battery chemistry, lithium-ion led with 73.4% of the Energy Storage Battery for Microgrids market share in 2025, while sodium batteries are projected to advance at a 31.9% CAGR through 2031.

- By power rating, systems above 500 kW commanded 55.1% revenue share in 2025 and are expected to grow at a 15.2% CAGR during 2026-2031.

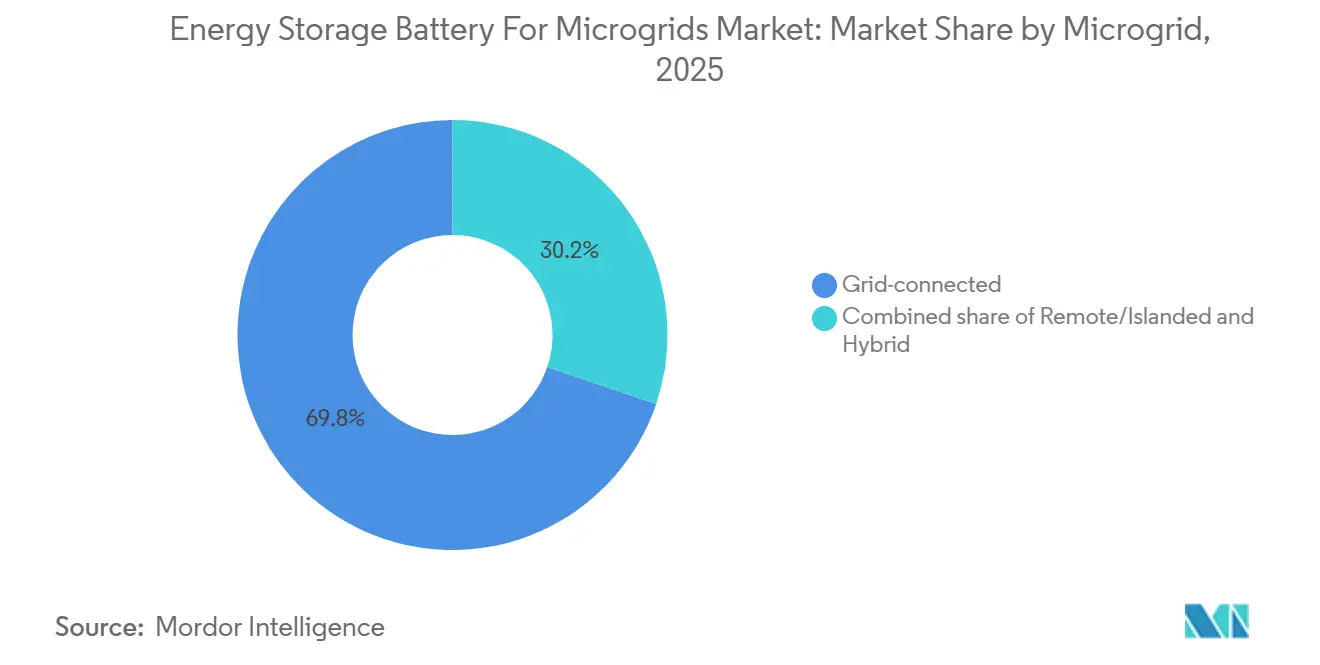

- By microgrid type, grid-connected configurations held 69.8% of 2025 installations; hybrid microgrids are forecast to expand at 20.6% CAGR over the same horizon.

- By end-user, commercial and industrial sites accounted for 44.6% revenue share in 2025, whereas residential deployments exhibit the fastest growth at 23.8% CAGR to 2031.

- By geography, North America captured 34.7% revenue in 2025, yet Asia-Pacific is the fastest-growing region with a 19.5% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Energy Storage Battery For Microgrids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling lithium-ion battery pack costs | +3.2% | Global, with steepest declines in China and North America | Short term (≤ 2 years) |

| Rising microgrid-specific incentives & tariff reforms | +2.8% | North America, Europe, India | Medium term (2-4 years) |

| Growing demand for energy resilience in extreme-weather zones | +2.5% | North America (hurricanes, wildfires), Asia-Pacific (typhoons), Europe (heatwaves) | Medium term (2-4 years) |

| Rapid decline in LFP cell degradation rates | +1.9% | Global, with early adoption in China and utility-scale projects | Long term (≥ 4 years) |

| Open-source microgrid controllers enabling standardisation | +1.4% | North America, Europe, Australia | Long term (≥ 4 years) |

| Emerging green-hydrogen hybrid microgrids | +1.1% | Europe, Middle East, pilot projects in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Falling Lithium-Ion Battery Pack Costs

Stationary storage pack prices dropped to USD 70 per kWh in 2025 after a surge in Chinese LFP output, compressing project paybacks from eight to five years and accelerating utility procurements. Nearly half of the cost decline stems from the substitution of cobalt-rich NMC cathodes with cobalt-free LFP, which also simplifies recycling. BloombergNEF estimates show price reductions moderating toward USD 60 per kWh by 2028 as cell-plant capex plateaus and raw-material logistics hit scale limits. Developers are responding with multi-year offtake contracts that hedge spot volatility and underwrite more aggressive bid prices in competitive tenders. Lower pack prices directly boost the Energy Storage Battery for Microgrids market by expanding the addressable base of projects that clear internal hurdle rates.

Rising Microgrid-Specific Incentives & Tariff Reforms

The United States’ Inflation Reduction Act provides a 30% standalone storage tax credit, unlocking USD 2.1 billion in new projects across 18 states in 2025. California and New York layered performance-based tariffs on top, paying microgrids for grid services rather than kilowatt-hour throughput. India’s 60% capital subsidy for rural microgrids spurred 1.2 GW of pipeline capacity by mid-2025. Tariff shifts in Hawaii and California reduced export credits by 40-75%, incentivizing self-consumption and lifting residential attachment rates. Collectively, these measures shave soft-cost risk, standardize interconnection, and add 2.8 % to the baseline CAGR for the Energy Storage Battery for Microgrids market.

Rapid Decline in LFP Cell Degradation Rates

Peer-reviewed data show modern LFP cells retaining 92% capacity after 6,000 cycles at 25 °C, aided by electrolyte additives and silicon-doped graphite anodes [1]Nature Energy Editors, “Extended Lifetimes for LFP Cells,” Nature Energy, nature.com. CATL’s 587 Ah LFP cell, launched in 2025, embeds real-time impedance spectroscopy, supporting 15-year warranties. Longer lifetimes reduce mid-life augmentation events and bring total cost of ownership to parity with diesel gensets whenever local fuel prices exceed USD 1.20 per liter. High round-trip efficiencies from products like Tesla’s Megapack 2XL eliminate inverter oversizing, trim balance-of-system costs, and lift the Energy Storage Battery for Microgrids market size in cost-sensitive projects.

Open-Source Microgrid Controllers Enabling Standardisation

IEEE 2030.7-2024 mandates interoperable protocols for systems above 100 kW, curbing vendor lock-in and halving controller engineering budgets to 9% of total project cost [2]IEEE Standards Association, “IEEE 2030.7-2024 Standard Finalized,” IEEE, standards.ieee.org. NREL’s OpenMicroGrid 3.0, adopted by 14 utilities, allows third-party battery swaps without firmware rewrites, fostering competitive re-bidding for augmentation contracts REUTERS.COM. Cost savings redirect capital toward additional storage capacity and extend addressable markets. Software-defined architectures thus reinforce the Energy Storage Battery for Microgrids market trajectory by converting proprietary ecosystems into open platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-mineral supply-chain volatility | -2.1% | Global, acute in lithium (Australia, Chile) and cobalt (DRC) | Short term (≤ 2 years) |

| Fire-safety & thermal-runaway concerns | -1.6% | North America, Europe (UL 9540A, NFPA 855 compliance zones) | Medium term (2-4 years) |

| High Balance of System (BOS) costs for <100 kW rural systems | -1.3% | Asia-Pacific, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Slow permitting in legacy grid codes | -1.0% | Europe, parts of North America with outdated interconnection standards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Supply-Chain Volatility

Lithium carbonate spot prices swung 50% during 2025, peaking at USD 18,500 per metric ton in January before sliding to USD 9,200 by December, which forced battery makers to reopen contracts and delayed 8 GWh of planned microgrid capacity in North America and Europe. The Democratic Republic of Congo’s artisanal-mining ban cut global cobalt supply by 12% and drove a 40% price jump for cobalt sulfate, adding unbudgeted augmentation costs for legacy NMC systems. Indonesia tightened nickel-ore export restrictions, stretching procurement cycles for high-nickel cathodes by up to nine months and disadvantaging suppliers without integrated refining. Vanadium pentoxide prices ranged between USD 8 and USD 14 per kilogram, preventing flow-battery vendors from locking in 25-year fixed-price bids that many utilities now demand. The International Energy Agency projects a 15% lithium-refining deficit by 2028, which could redirect material toward electric vehicles and compress Energy Storage Battery for Microgrids market growth by 2.1 % each year [3]International Energy Agency Analysts, “Critical Minerals Outlook 2025,” IEA, iea.org.

Fire-Safety and Thermal-Runaway Concerns

UL 9540A propagation tests became mandatory in 13 U.S. states during 2025, adding USD 0.2 million to USD 0.5 million per project and extending schedules by up to twelve weeks. NFPA 855 now requires aerosol suppression for enclosures above 600 kWh, which has lifted balance-of-system costs 7% to 11% and pushed some developers to subdivide large sites into smaller modules. A 22 MWh lithium fire in South Korea in April 2024 prompted a nationwide review that stalled 400 MW of pipeline capacity and highlighted how single incidents ripple across permitting agencies. Tesla’s Bouldercombe Megapack recall paused global shipments for four months and cost an estimated USD 120 million in lost revenue, eroding customer confidence in turnkey lithium solutions. Insurers have reacted with 15%–25% premium hikes for projects lacking UL 9540A certification, which raises levelized storage costs by up to USD 0.04 per kWh and narrows the economic edge over diesel gensets in unpriced-carbon regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Sodium Variants Erode Lithium’s Lead

Lithium-ion technologies controlled 73.4% of the Energy Storage Battery for Microgrids market share in 2025, underpinned by proven supply chains and high-power capability. Sodium chemistries, however, are set to expand at 31.9% CAGR through 2031, the fastest pace among all options. CATL’s USD 50 per kWh sodium-ion cells remove cobalt and nickel risk, redirecting cost savings toward balance-of-system upgrades. In Japan, sodium-sulfur systems meet 6-hour discharge needs within island grids, bridging the duration gap left by mainstream lithium products. Flow batteries occupy a niche in the market, offering long-duration energy storage with consistent performance over operating lifetimes exceeding 25 years and minimal capacity degradation.

Lead-acid batteries continue to support sub-50 kW rural microgrid projects due to their widespread familiarity in servicing and ease of repair. However, their shorter lifecycle performance limits their broader long-term adoption. Lithium titanate batteries remain primarily utilized in specialized transit and military applications, where ultra-long cycle life and high durability are prioritized over energy density. Alternative battery chemistries are expected to see steady adoption through 2031 as microgrid deployments expand across various use cases and operating conditions. Consequently, competitive positioning increasingly relies on aligning battery chemistry with specific application requirements rather than depending on a single dominant technology. Manufacturers with diversified chemistry portfolios are better equipped to address the evolving and fragmented demand landscape.

By Power Rating: Utility-Scale Projects Sustain Revenue Momentum

Systems above 500 kW held 55.1% of Energy Storage Battery for Microgrids market size in 2025 and exhibit a 15.2% CAGR through 2031, buoyed by utility procurements such as the 2.2 GWh Arizona Copia installation [4]Financial Times Reporters, “CATL Commercializes Sodium-Ion at USD 50/kWh,” Financial Times, ft.com. Configurations in the 100-500 kW range constitute 28% of deployments, serving hospitals, data centers, and light-industrial loads that need two-to-three-hour back-up at manageable capex.

High balance-of-system costs still impede rural sub-100 kW roll-outs, although containerized kits from Schneider Electric cut installation time by 80% and shrink BOS premiums. IEEE 1547‐2024 further accelerates 100-500 kW approvals by halving interconnection queues, pulling capital cycles forward. Utility-scale orders remain sticky because revenue stacking capacity payments, frequency response buffers margin risk. Conversely, small projects rely on donor finance and concessional loans, slowing scale. Suppliers that package standardized hardware plus remote monitoring stand to capture this underserved volume market.

By Microgrid Type: Hybrid Configurations Accelerate

Grid-connected designs made up 69.8% of 2025 installations, leveraging dual revenue streams and simplified O&M. Hybrid microgrids, combining renewables, storage, and diesel or gas peakers, are on track for a 20.6% CAGR, outpacing every other configuration. Fluence’s 1.2 GWh Arizona Pioneer project illustrates how solar, batteries, and quick-start gas together achieve 95% renewable penetration while meeting N-1 reliability.

Remote microgrids remain essential for mines, islands, and military bases where grid extension costs exceed USD 50,000 per km. Open-source controllers enable seamless mode-shifting between grid-parallel and islanded operation, blurring historical distinctions. The Energy Storage Battery for Microgrids market size tied to hybrids is forecast to double by 2031 as climate risks challenge single-fuel systems. This shift forces suppliers to optimize total cost across multi-asset portfolios, making software orchestration as valuable as additional kilowatt-hours.

By End-User: Residential Uptake Surges Amid Net-Metering Reform

Commercial and industrial facilities commanded 44.6% of 2025 revenue, using microgrids to hedge demand charges and ensure uptime. Residential systems are growing fastest with a 23.8% CAGR after Hawaii and California slashed export tariffs, making self-consumption vital.

Utility deployments in the Energy Storage Battery for Microgrids market often exceed 10 MW and are increasingly supported by capacity payments through grid-support and peak-shaving programs. Enphase Energy’s IQ Battery 5P streamlines residential installations to approximately three hours, significantly reducing labor requirements while offering standardized 10–15 kWh storage packages. Commercial and industrial projects demonstrate varied requirements, including hospital-grade compliance standards and data-center five-nines uptime expectations, which limit the potential for commoditization. Residential customers prioritize aesthetics, seamless backup automation, and ease of use. Vendors that adapt their products, service models, and sales channels to meet the specific needs of these customer segments are better positioned to enhance customer retention and reduce acquisition costs.

Geography Analysis

North America held 34.7% of 2025 revenue. ERCOT’s energy-only market and federal tax credits sustain a 13.8% regional CAGR despite growing interconnection backlogs. Texas and California each announced more than 1 GW of new projects after weather-driven outages. Canada’s 80 MW Oneida installation exemplifies indigenous energy sovereignty plus grid-service monetization.

The Asia-Pacific region is expected to be the fastest-growing energy storage market, with a projected CAGR of 19.5% during the forecast period. This growth is driven by strong policy support, industrial decarbonization efforts, and grid modernization initiatives. In India, a 60% capital subsidy for battery energy storage projects has facilitated the development of approximately 1.2 GW of pipeline capacity, boosting deployment in both utility-scale and distributed applications. In China, the requirement for on-site microgrids in newly developed industrial parks has created an estimated 3 GW of additional energy storage demand. Japan is focusing on sodium-sulfur (NaS) battery systems to improve energy security and resilience, particularly for remote islands and disaster-prone areas. In Australia, the 500 MW Tomago Energy Hub project underscores the growing adoption of large-scale energy storage solutions by energy-intensive industries, further solidifying the region's position in advanced storage deployment and grid flexibility.

In Europe, Germany’s hydrogen-battery hybrid at Energiepark Mainz validates multi-day balancing, yet permitting queues averaging 38 months suppresses market velocity. Nordic nations deploy microgrids for remote villages and data centers, whereas Spain and Italy struggle with legacy grid codes. South America, the Middle East, and Africa add opportunistic growth via mining corridors and solar campuses where grid extension is uneconomic.

Competitive Landscape

The Energy Storage Battery for Microgrids Market is semi-consolidated. Integrated system providers monetize uptime guarantees and software, earning higher gross margins than cell-only peers. Tesla’s Megapack backlog surpassed 2.2 GWh on the strength of 20-year warranties and GridOS-compatible controls. Flow specialists ESS Tech and Eos Energy secured 200 MWh of 25-year iron-flow contracts, filling a long-duration niche that lithium rivals. Sodium-ion entrants such as Peak Energy undercut lithium by 30%, targeting cost-sensitive rural microgrids. Open-source standards diminish lock-in, and UL 9540A compliance expenses raise entry barriers. M&A picked up in 2025. Aqua Metals bought Lion Energy, and Zenobē consolidated 1.3 GW of German assets, signaling portfolio-scale competition grounded in balance-sheet strength.

Energy Storage Battery For Microgrids Industry Leaders

-

ESS Tech, Inc.

-

Panasonic Energy Co., Ltd.

-

Tesla, Inc.

-

Fluence Energy, Inc.,

-

LG Energy Solution Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Redwood Materials has expanded the deployment of microgrids utilizing repurposed EV batteries. Its Nevada installation provides 12 MW / 63 MWh of capacity using second-life batteries, making it one of the largest microgrid projects globally. This initiative demonstrates a cost-efficient approach to microgrid storage by leveraging battery reuse and circular economy principles.

- July 2025: Panasonic opened its cylindrical lithium-ion battery factory in De Soto, Kansas, achieving 32 GWh annual production capacity as one of North America's largest gigafactories, with USD 4 billion total investment creating 8,000 jobs and supporting domestic battery supply chain development.

- June 2025: AMEA Power reached financial close for Egypt's first utility-scale battery energy storage system project, marking Africa's largest solar PV development with an integrated storage solution that advances renewable energy adoption across the continent.

- March 2025: Hopi Nation secured USD 4.63 million Department of Energy funding for a solar and battery storage microgrid serving 230 residential and 14 commercial customers, demonstrating federal support for tribal energy sovereignty and rural electrification initiatives.

Global Energy Storage Battery For Microgrids Market Report Scope

An energy storage battery for microgrids is a system designed to store electricity, typically in chemical form, and supply it as needed to support a localized power network known as a microgrid. A microgrid is a small-scale energy system that can function independently or in conjunction with the main grid, often incorporating renewable energy sources such as solar or wind. These batteries, which commonly utilize technologies like lithium-ion, flow batteries, or lead-acid, play a critical role in balancing supply and demand. They store surplus energy generated during periods of low demand and release it during peak demand or power outages. Additionally, they enhance reliability, stabilize voltage and frequency, facilitate renewable energy integration, and provide backup power in remote or off-grid locations.

The Energy Storage Battery for Microgrids market is segmented by battery chemistry, power rating, microgrid type, end-user, and geography. By battery chemistry, the market is segmented into lithium-ion, lead-acid, flow batteries, sodium-based batteries, and other chemistries. By power rating, the market is segmented into below 100 kW, 100 to 500 kW, and above 500 kW. By microgrid type, the market is segmented into remote/islanded, grid-connected, and hybrid systems. By end-user, the market is segmented into residential, commercial, industrial, and utility sectors. The report also covers market size and forecasts for the global energy storage battery for microgrids market across major countries in key regions. For each segment, market sizing and forecasts are provided based on value (USD).

| Lithium-ion (NMC, LFP, LTO) |

| Lead-acid (VRLA, Flooded) |

| Flow (Vanadium, Zinc, Iron, Others) |

| Sodium-based (Na-ion, NaS) |

| Other Chemistries (NiCd, Zn-Br, etc.) |

| Below 100 kW |

| 100 to 500 kW |

| Above 500 kW |

| Remote/Islanded |

| Grid-connected |

| Hybrid (PV-Diesel-Storage, etc.) |

| Residential |

| Commercial and Industrial |

| Utility |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Chemistry | Lithium-ion (NMC, LFP, LTO) | |

| Lead-acid (VRLA, Flooded) | ||

| Flow (Vanadium, Zinc, Iron, Others) | ||

| Sodium-based (Na-ion, NaS) | ||

| Other Chemistries (NiCd, Zn-Br, etc.) | ||

| By Power Rating | Below 100 kW | |

| 100 to 500 kW | ||

| Above 500 kW | ||

| By Microgrid Type | Remote/Islanded | |

| Grid-connected | ||

| Hybrid (PV-Diesel-Storage, etc.) | ||

| By End-user | Residential | |

| Commercial and Industrial | ||

| Utility | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected global value of energy-storage batteries deployed in microgrids by 2031?

The market is forecast to reach about USD 889.10 million by 2031.

What compound annual growth rate is expected for microgrid battery revenue between 2026 and 2031?

Revenue is projected to rise at roughly 14.22% CAGR over that period.

Which region will register the fastest uptake of microgrid batteries through 2031?

Asia-Pacific is anticipated to expand the fastest, at around 19.5% CAGR.

Which battery chemistry is gaining share most rapidly within microgrid applications?

Sodium-based chemistries are slated to grow the quickest, at nearly 31.9% per year.

How are recent U.S. tax credits and resilience grants influencing project paybacks?

The 30% standalone storage credit and state incentives have shortened typical paybacks from eight years to about five years.

Page last updated on: