Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 21.20 Billion |

| Market Size (2031) | USD 30.22 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

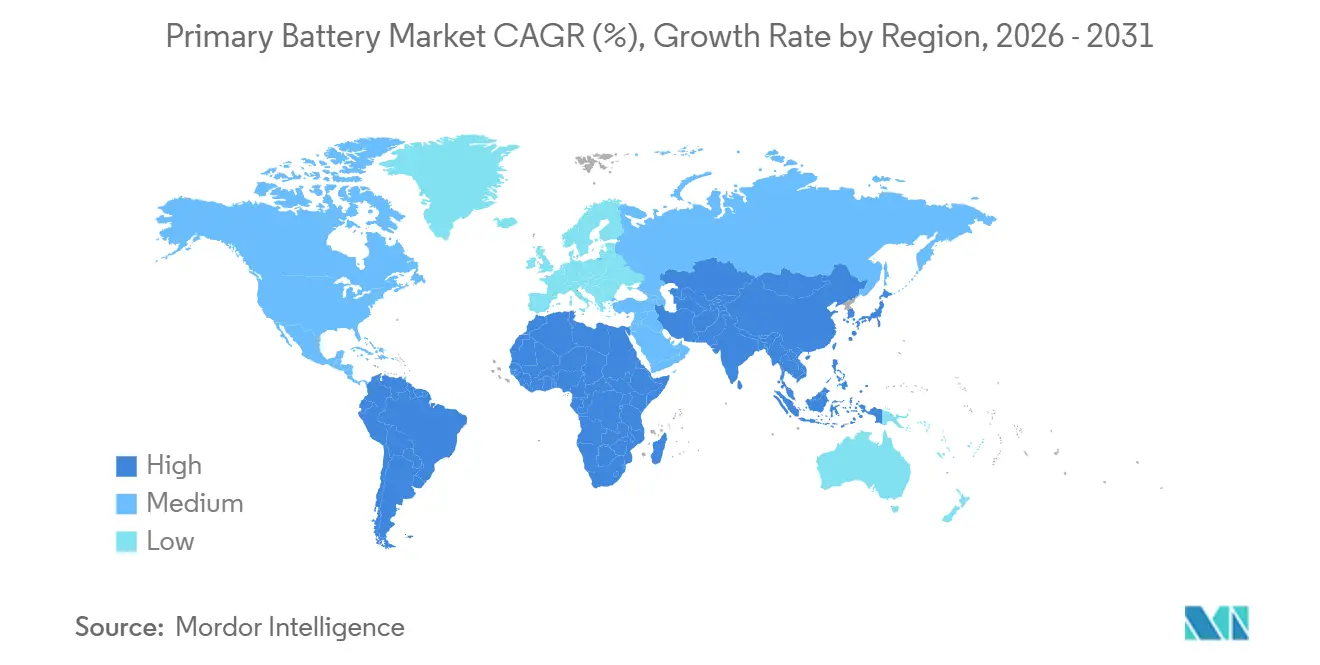

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

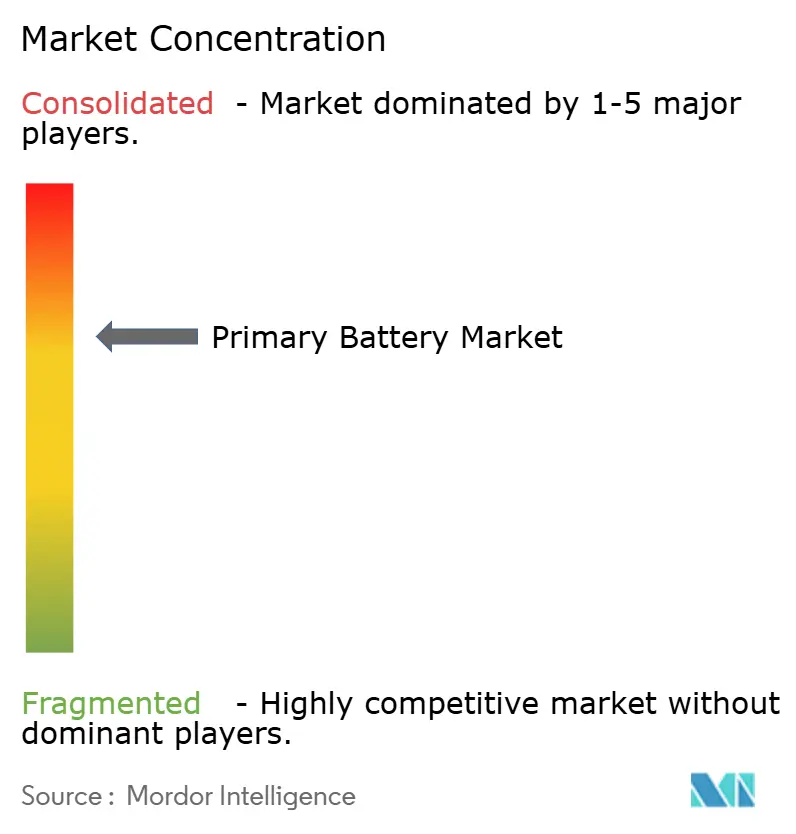

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Primary Battery Market Analysis by Mordor Intelligence

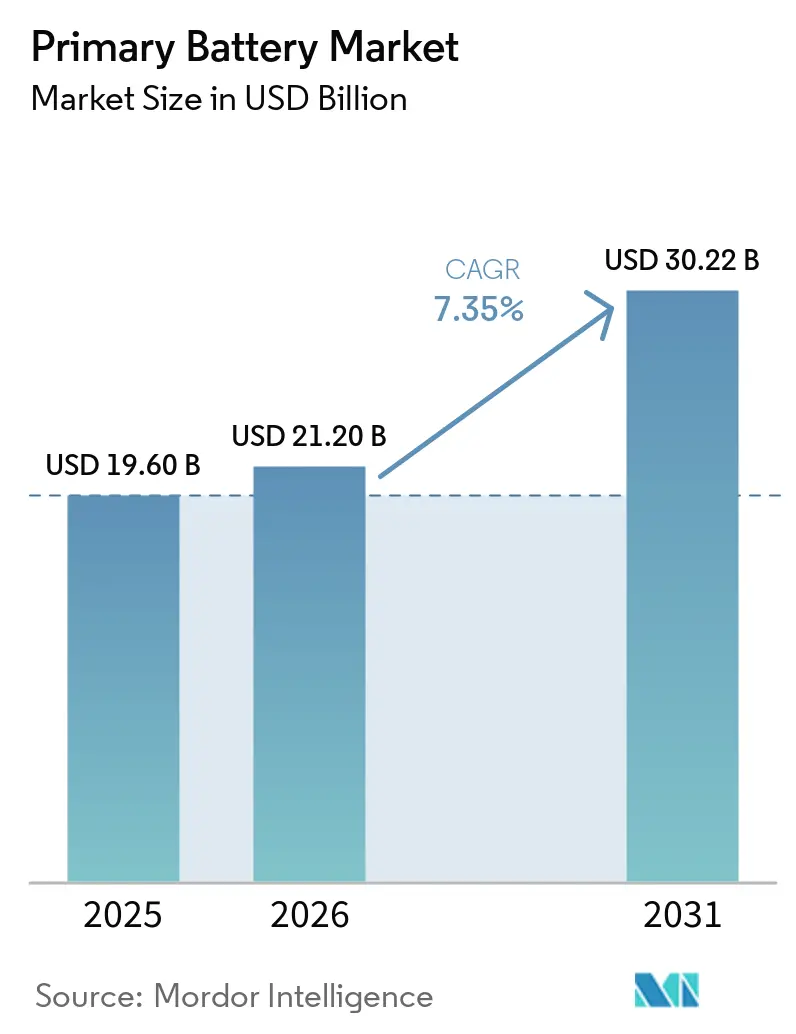

The Primary Battery Market size is estimated at USD 21.20 billion in 2026, and is expected to reach USD 30.22 billion by 2031, at a CAGR of 7.35% during the forecast period (2026-2031).

Structural growth now stretches beyond routine replacement purchases as the primary battery market expands into IoT sensor networks, off-grid medical diagnostics, and defense-portable electronics, where recharging is impractical or cost-prohibitive. Rapid deployment of low-power wide-area networks, stringent green-procurement rules that favor mercury-free chemistries, and policy incentives such as U.S. Section 45X production tax credits are broadening demand while improving profitability for domestic producers. Yet, counterfeit inflows and raw-material volatility continue to strain margins, and secondary lithium-ion packs are capturing share in applications that tolerate frequent charging.

Key Report Takeaways

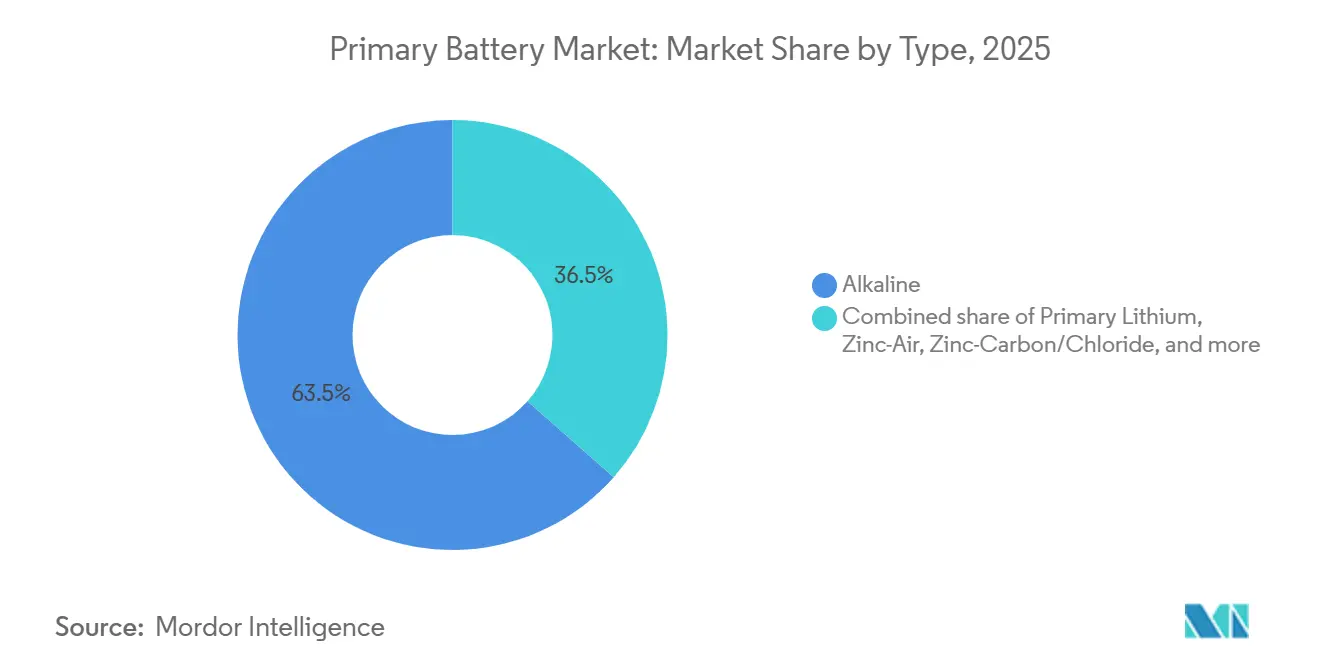

- By chemistry, alkaline claimed 63.5% of the primary battery market share in 2025, while primary lithium variants are forecast to advance at a 9.5% CAGR through 2031.

- By form factor, cylindrical cells led with 52.9% revenue share in 2025, whereas coin and button cells are projected to expand at a 9.9% CAGR through 2031.

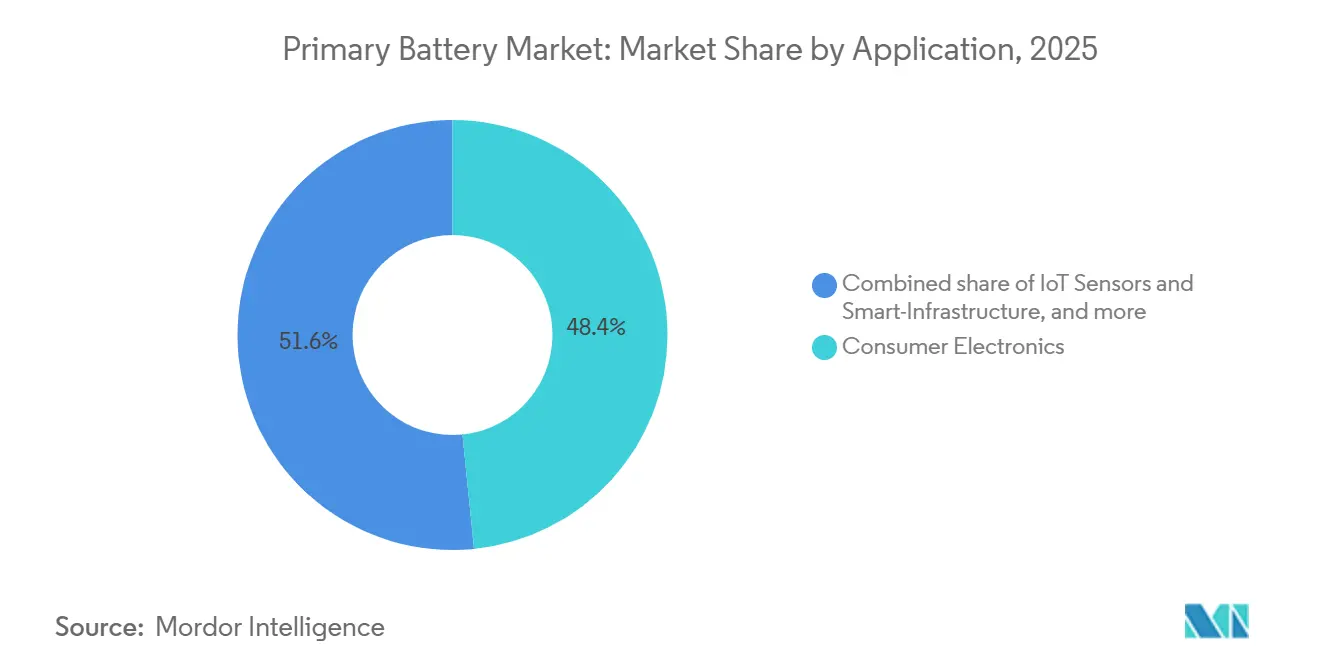

- By application, consumer electronics accounted for 48.4% of revenue in 2025, but IoT sensors and smart infrastructure are poised to grow at a 10.1% CAGR to 2031.

- By geography, Asia-Pacific held 46.1% of global revenue in 2025, while the Middle East & Africa region is set to post the fastest 9.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Primary Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from smart-home & IoT single-use sensors | 1.8% | Global, with APAC and North America leading deployment | Medium term (2-4 years) |

| Rapid growth of off-grid medical devices in emerging markets | 1.5% | Middle East & Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Expansion of defence portable electronics budgets | 1.2% | North America, Europe, Asia-Pacific (South Korea, Japan) | Short term (≤ 2 years) |

| Shift toward mercury-free chemistries & green purchasing mandates | 0.9% | Europe, North America, with spillover to APAC | Medium term (2-4 years) |

| Mainstream consumer-electronics replacement cycle | 0.8% | Global, peaking in Asia-Pacific and North America | Short term (≤ 2 years) |

| E-commerce penetration widening retail reach | 0.5% | Global, fastest in North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Smart-Home & IoT Single-Use Sensors

LoRaWAN networks surpassed 125 million connected devices in 2024, growing 25% year over year, and most of these endpoints, such as door, leak, and occupancy sensors, are engineered for up to 10 years of operation on a single AA or coin-cell. Deployers avoid the USD 15–30 per node expense of adding recharging infrastructure, keeping the total cost of ownership low. Wi-Fi HaLow chipsets from multiple vendors promise a decade of runtime on two AA alkaline cells, which enables retrofits in commercial buildings without wiring for power. Although the GSM Association expects 1.1 billion ambient IoT devices by 2030, roughly 473 million units will still rely on primary batteries in locations that lack sufficient light for energy harvesting.[1]The Mobile Economy 2026,” GSM Association, gsma.com Supercapacitors specified in ITU-T L.1310 offer hundreds of thousands of cycles but only fleeting backup time, confirming their complementary, not substitutive, role against long-duration primary chemistries.

Rapid Growth of Off-Grid Medical Devices in Emerging Markets

The World Health Organization reported in 2024 that facilities serving 1 billion people in sub-Saharan Africa and South Asia still lack reliable electricity, spurring adoption of pulse oximeters, portable ultrasound units, and vaccine monitors powered by primary lithium cells that deliver a decade-long shelf life.[2]Global Atlas of Medical Devices 2024,” WHO, who.int Solar-plus-storage microgrids financed by multilateral banks often reserve these cells for low-drain instrumentation where the cost of battery-management systems outweighs the price of periodic replacement. Global shipments of wearable medical devices reached 556.5 million units in mid-2025, 18% of which require silver-oxide or lithium coin cells to meet strict volumetric-energy-density needs. Zinc-air button cells remain dominant in hearing aids because they deliver 1.4 V and up to 650 mAh in tiny housings that rechargeable options cannot match without sacrificing comfort.

Expansion of Defense Portable Electronics Budgets

The U.S. defense budget topped USD 850 billion in fiscal 2024, channeling funds into radios, GPS receivers, and night-vision systems that specify BA-5590 or BA-5390 primary lithium packs for 72-hour missions. NATO’s 2%-of-GDP spending pledge is pushing procurement toward platforms that remain functional from −40 °C to +60 °C without active thermal management, a specification rechargeable lithium-ion often fails to meet. South Korea’s 2025 infantry-gear contract and Japan’s 16% defense-budget increase both mandate primary lithium cells with 15-year storage life. These requirements highlight the continuing relevance of non-rechargeable chemistries in logistics-constrained environments.

Shift Toward Mercury-Free Chemistries & Green Purchasing Mandates

EU Regulation 2023/1542 sets 63% collection by 2027 and 73% by 2030, elevating compliance costs and accelerating conversion to mercury- and cadmium-free formulations. Energizer cited these fees as shaving 2.1 percentage points off gross margin in fiscal 2025. Panasonic’s EVOLTA NEO range achieves 1.3 times the runtime of standard alkaline cells while meeting RoHS and REACH rules after retooling at its Nishikinohama factory. U.S. federal procurement rules now prioritize batteries with recognized ecolabels, steering demand toward incumbents with compliant supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from secondary batteries & supercapacitors | -1.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Extended Producer Responsibility (EPR) fees inflating costs | -0.7% | Europe, North America, with emerging adoption in APAC | Short term (≤ 2 years) |

| Raw-material price volatility (zinc, lithium, manganese) | -0.5% | Global, supply concentrated in China, Chile, Australia | Short term (≤ 2 years) |

| Counterfeit battery inflow in Asia & Africa | -0.4% | Asia-Pacific, Middle East & Africa, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Secondary Batteries & Super-Capacitors

Rechargeable lithium-ion captured 83% of global battery capacity in 2025, pushing pack prices below USD 100 per kWh and eroding primary share in peripherals, speakers, and grooming devices.[3]Global EV Outlook 2025,” International Energy Agency, iea.org Despite energy-density limits, supercapacitors boasting 500,000-plus cycles are gaining ground in telecom backup, though they cannot supply multi-year, low-drain power. Nickel-metal-hydride AA cells continue to replace alkaline primaries in mid-drain consumer gear, while counterfeit alkaline imports further depress prices and compromise safety.

Extended Producer Responsibility Fees Inflating Costs

EU and U.S. EPR schemes add EUR 0.02–0.05 per cell to compliance costs, a burden Energizer flagged as material in its 2025 annual report. Counterfeit cells avoid these fees outright, amplifying cost disadvantages for legitimate brands. At the same time, electrolytic manganese dioxide fetched USD 2,062.92 per metric ton in April 2025, about 2.8 times the price of battery-grade manganese sulfate, underscoring persistent raw-material pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Lithium Chemistries Gain on Cold-Chain Demand

Primary lithium variants are projected to post a 9.5% CAGR between 2026 and 2031, the quickest within the primary battery market, as industrial metering and defense communications migrate to cells that operate from −40 °C to +85 °C at 3.0–3.6 V per cell.[4]Technical Data Sheets—LSP Series,” Saft, saftbatteries.com Conversely, alkaline held 63.5% revenue share in 2025 thanks to ubiquitous retail distribution. Zinc-air dominates hearing aids with 1.4-V output and up to 650 mAh capacity, while silver-oxide button cells sustain premium pricing in precision watches and glucose monitors. Recent U.S. import data show manganese-ore volumes escalating as manufacturers hedge against Chinese refining dominance.

Alkaline incumbents defend share through materials science: Panasonic’s EVOLTA NEO uses high-purity manganese dioxide with titanium additives to deliver 1.3 times longer runtime. Meanwhile, nickel-zinc variants remain niche due to limited shelf life. Zinc-carbon cells persist in price-sensitive segments but are losing ground as alkaline approaches price parity, reinforcing the gradual premiumization of the primary battery market.

By Form Factor: Coin Cells Ride Wearables Wave

Coin and button cells are forecast to expand at a 9.9% CAGR through 2031, buoyed by wearable medical devices and miniature IoT modules that demand compact energy sources. Cylindrical AA and AAA formats retained a 52.9% share in 2025, supported by standardized dimensions and widespread retail placement. Prismatic cells cater to OEMs seeking custom footprints but face higher tooling hurdles. Genuine CR2032 cells provide 220–240 mAh at 3.0 V in 3-g packages, whereas counterfeits deliver less than half that capacity, prompting device shutdowns and warranty claims.

The LoRa Alliance’s 125 million-device milestone intensifies demand for CR2032 and CR123A cells designed for five-to-ten-year lifecycles. Hearing-aid OEMs continue to rely on zinc-air size 10, 13, 312, and 675 buttons, underscoring the irreplaceability of specialized chemistries for ultra-small devices within the primary battery market size benchmarks.

By Application: IoT Sensors Outpace Consumer Electronics

IoT sensors and smart-infrastructure deployments are projected to rise at a 10.1% CAGR, becoming the fastest-growing slice of the primary battery market. Consumer electronics still led with 48.4% revenue in 2025, but are gradually ceding ground to rechargeable packs as costs fall. Industrial OEM segments require Li-SOCl₂ cells to guarantee decade-long service in extreme temperatures, a niche where rechargeable alternatives falter without costly thermal controls.

Medical wearables depend on silver-oxide and lithium coin cells to maintain a steady voltage across body-temperature variations. Defense and aerospace specify BA-series lithium packs for extended autonomy, further sustaining high-margin niches. Wi-Fi HaLow sensor retrofits in commercial real estate highlight the economic advantage of primary cells when maintenance labor eclipses battery cost.

Geography Analysis

Asia-Pacific commanded 46.1% of revenue in 2025, reflecting China’s vertically integrated cost leadership across manganese dioxide refining, zinc powder production, and cell assembly. India’s Production-Linked Incentive scheme earmarked 18 GWh of battery capacity, largely for lithium-ion EV packs, leaving primary cell output concentrated in smaller domestic plants. Japan’s Nishikinohama factory, ramped up in late 2023, produces 48 million alkaline cells monthly, providing a non-Chinese source for premium EVOLTA NEO products. Emerging ASEAN hubs, Thailand, Vietnam, and Indonesia, are attracting coin-cell assembly for hearing aids, leveraging low labor costs and supply-chain proximity.

The Middle East & Africa region is expected to post a 9.0% CAGR to 2031, driven by decentralized-energy programs. The World Bank estimates 640–650 million people in sub-Saharan Africa still lack grid power, prompting solar-plus-microgrid deployments that reserve primary batteries for low-drain monitoring. South Africa’s 360 MW battery tender in 2024, and its 1,200 MW pipeline, principally features rechargeable chemistries for long-duration discharge, leaving primary cells in peripheral telemetry roles. Counterfeit batteries remain pervasive, undermining safety and eroding legitimate brand share.

North America and Europe are consolidating around premium niches. Energizer received USD 112.4 million in Section 45X credits in fiscal 2025, underpinning domestic production. Its May 2025 purchase of Advanced Power Solutions NV added Polish capacity, albeit at a short-term margin cost. EU EPR mandates continue to lift compliance expenses, which established players can absorb more readily than new entrants. South American growth centers on Brazil and Argentina as e-commerce unlocks rural demand, though logistics obstacles in the Amazon and Patagonia impede deeper penetration.

Competitive Landscape

The primary battery market exhibits moderate concentration. Duracell, Energizer, and Panasonic Energy jointly control about 55–60% of global alkaline revenue through strong branding, shelf dominance, and vertical integration. Energizer’s APS acquisition expands European output and diversifies supply chains, while Panasonic pushes performance boundaries with titanium-enhanced cathodes that deliver 1.3 times longer runtime. Saft, Ultralife, and FDK specialize in industrial primary lithium cells with 10-year shelf lives, positioning themselves for metering and defense contracts where alkaline incumbents are less active.

Chinese challengers, EVE Energy, Zhejiang Mustang, Xiamen 3-Circle, undercut Western pricing by 15–20%, but lack strong consumer brands. Counterfeit inflows, largely sourced from China and Hong Kong, amount to 24% of seized dangerous goods and compress legitimate margins. U.S. policy incentives may temper import reliance, yet the scheduled phase-down of Section 45X credits after 2032 leaves future competitiveness uncertain for domestic manufacturers.

Primary Battery Industry Leaders

Duracell

Energizer

Panasonic Energy

GP Batteries

Varta AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Panasonic has announced plans to commence mass production of battery cells for data center backup power systems at its Kansas facility in the United States by fiscal year 2028.

- June 2025: Murata Manufacturing Co., Ltd. has announced that its Board of Directors has approved the transfer of its micro primary battery business, currently operated by Murata and its wholly owned subsidiary, Tohoku Murata Manufacturing Co., Ltd., to Maxell, Ltd. The company has also finalized a share transfer agreement with Maxell.

- January 2025: Nordic Semiconductor, a global leader in low-power wireless connectivity solutions, has introduced the nPM2100 PMIC, the latest addition to its nPM Power Management IC family.

- July 2024: Maxell unveiled its latest manganese battery series, named Super Power Ace and Power Ace. The revamped packaging now mirrors the aesthetics of the alkaline (GD) batteries, boosting its visibility.

Global Primary Battery Market Report Scope

Primary batteries refer to portable batteries designed to be used once and discarded. Primary batteries are non-rechargeable as the electrochemical reactions in the cell are irreversible.

The global primary battery market is segmented by type, form factor, application, and geography. By type, the market is segmented into alkaline, primary lithium, zinc-air, zinc-carbon/chloride, and silver-oxide and others. By form factor, the market is segmented into cylindrical, coin and button cells, prismatic/packaged, and others. By application, the market is segmented into consumer electronics, industrial and OEM, medical and healthcare, defence and aerospace, IoT sensors, and smart infrastructure. The report also covers market size and forecasts for the primary battery market across major regions. The market sizing and forecasts have been projected in revenue (USD) for each segment.

By Type

| Alkaline |

| Primary Lithium (Li-MnO₂, Li-SOCl₂, Li-CFx) |

| Zinc-Air |

| Zinc-Carbon/Chloride |

| Silver-Oxide and Others |

By Form Factor

| Cylindrical (AA, AAA, C, D) |

| Coin and Button Cells |

| Prismatic/Packaged |

| Others (Special shapes) |

By Application

| Consumer Electronics |

| Industrial and OEM |

| Medical and Healthcare |

| Defence and Aerospace |

| IoT Sensors and Smart-Infrastructure |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Alkaline | |

| Primary Lithium (Li-MnO₂, Li-SOCl₂, Li-CFx) | ||

| Zinc-Air | ||

| Zinc-Carbon/Chloride | ||

| Silver-Oxide and Others | ||

| By Form Factor | Cylindrical (AA, AAA, C, D) | |

| Coin and Button Cells | ||

| Prismatic/Packaged | ||

| Others (Special shapes) | ||

| By Application | Consumer Electronics | |

| Industrial and OEM | ||

| Medical and Healthcare | ||

| Defence and Aerospace | ||

| IoT Sensors and Smart-Infrastructure | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the primary battery market?

The primary battery market size stood at USD 21.20 billion in 2026.

How fast is the primary battery market expected to grow?

The market is forecast to post a 7.35% CAGR, reaching USD 30.22 billion by 2031.

Which chemistry is growing fastest?

Primary lithium variants are projected to expand at a 9.5% CAGR through 2031.

Which region leads revenue generation?

Asia-Pacific held 46.1% of global revenue in 2025 due to China’s manufacturing dominance.

Which application segment will outpace others?

IoT sensors and smart-infrastructure deployments are set to grow at a 10.1% CAGR to 2031.

Page last updated on: