Bangladesh Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

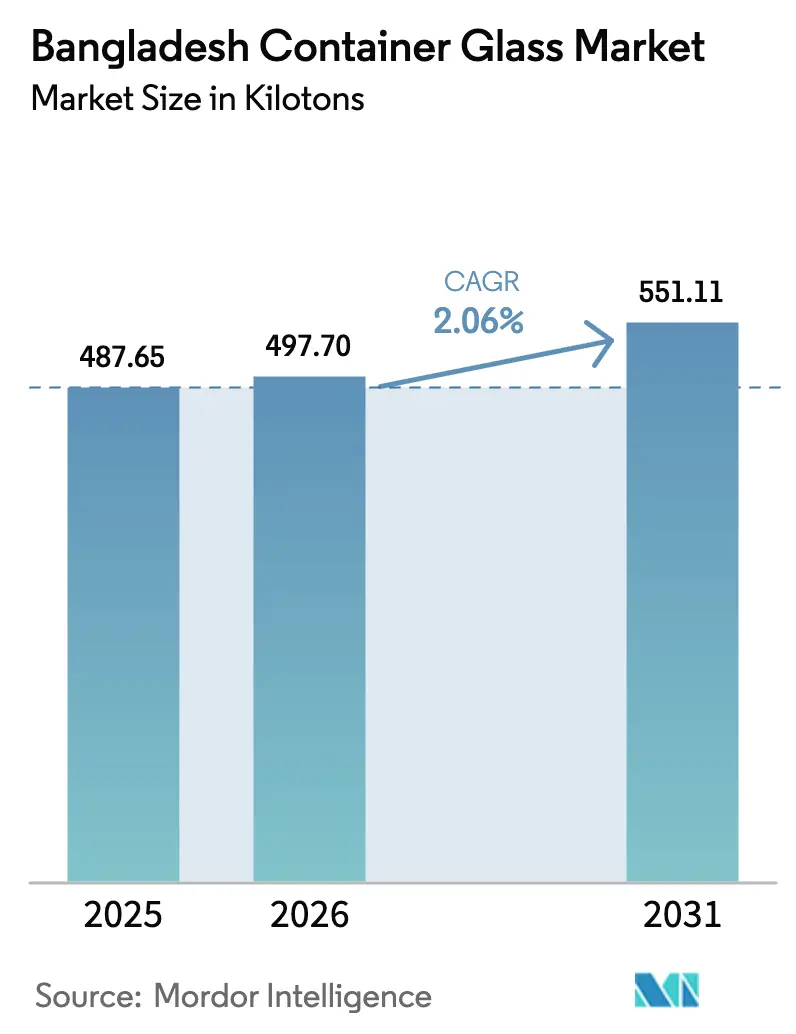

| Base Year Market Size (2025) | 487.65 kilotons |

| Market Volume (2026) | 497.7 kilotons |

| Market Volume (2031) | 551.11 kilotons |

| Growth Rate (2026 - 2031) | 2.06% CAGR |

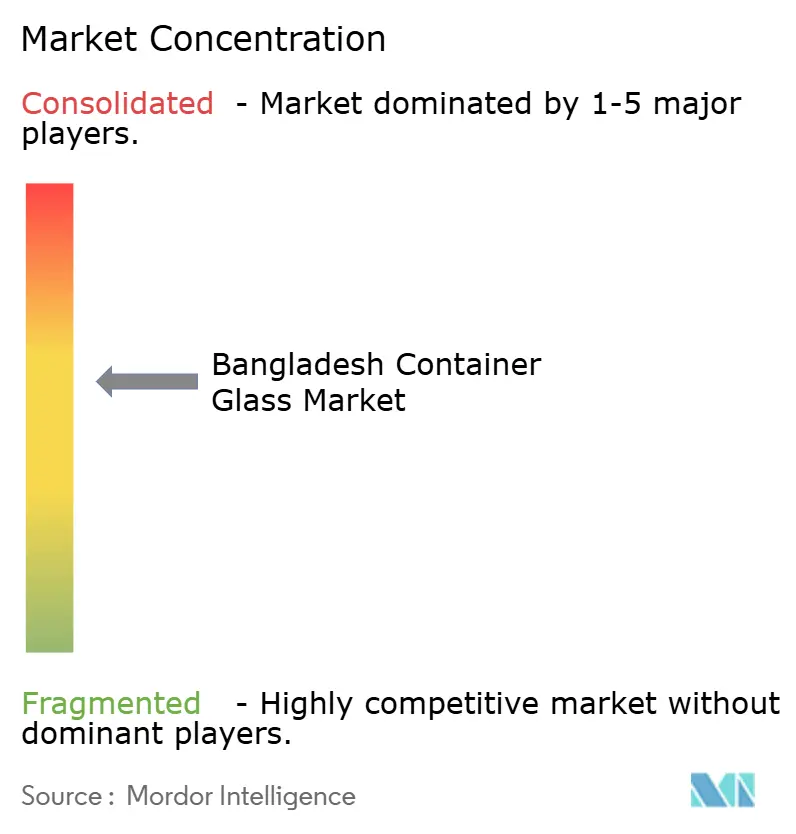

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Container Glass Market Analysis by Mordor Intelligence

The Bangladesh container glass market size is expected to grow from 487.65 kilotons in 2025 to 497.7 kilotons in 2026 and is forecast to reach 551.11 kilotons by 2031 at 2.06% CAGR over 2026-2031. Rising local furnace capacity, favorable plastic-reduction policies, and steady private investments exceeding BDT 10,000 crore have shifted the Bangladesh container glass market from reliance on imports toward near self-sufficiency. Demand is anchored in beverages, processed foods, pharmaceuticals, and fast-growing cosmetics, all of which benefit from the country’s 34 million-strong middle and affluent class, which is expanding at a rate of 10.5% annually. Regulatory momentum, primarily driven by the Ministry of Environment’s ban on 17 categories of single-use plastics, is directing institutional procurement toward glass bottles and jars. Meanwhile, urban consumers associate glass with premium quality and health safety. Domestic silica sand deposits exceeding 5.117 billion tons provide a long-term raw-material hedge, although manufacturers still import high-grade inputs for specialty colors and coatings.[1]Mahmudul Hasan, “Expanding into glass production was a logical step,” The Daily Star, dailystar.net Energy costs and PET substitution remain credible threats; however, process optimization and the adoption of renewable energy have already reduced unit energy consumption across leading plants, thereby cushioning the Bangladesh container glass market against fuel price fluctuations.

Key Report Takeaways

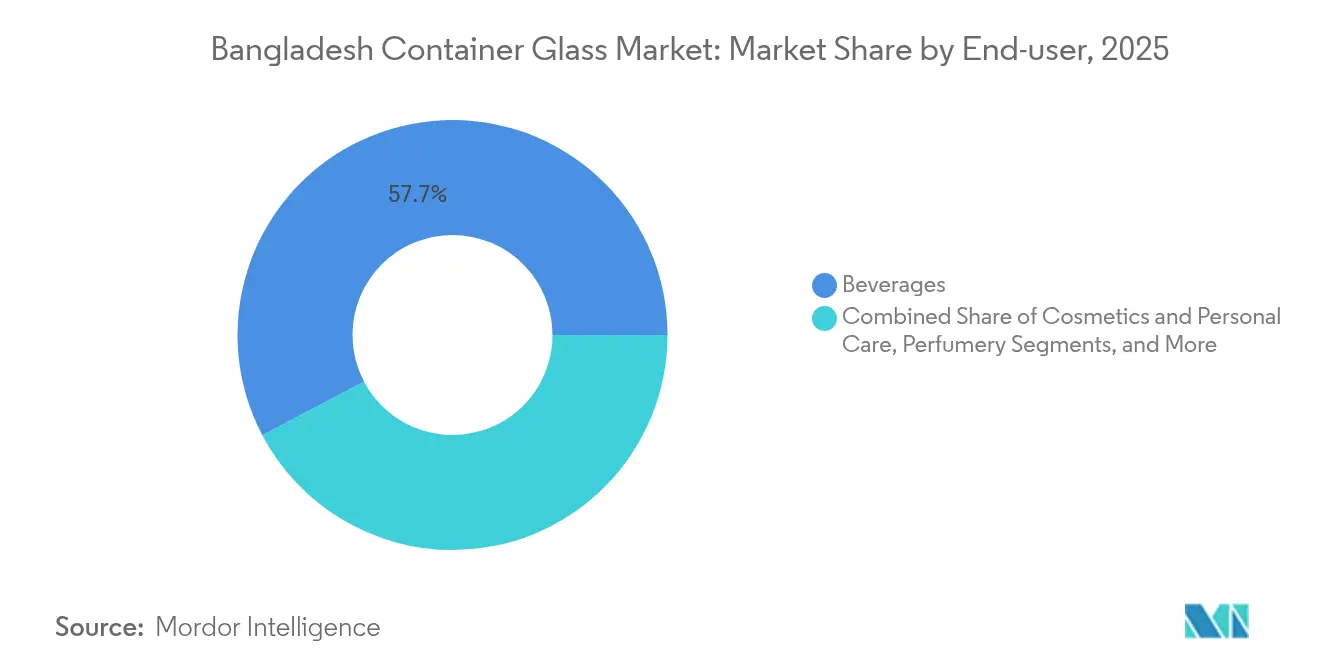

- By end-user, beverages captured 57.72% of the Bangladesh container glass market share in 2025.

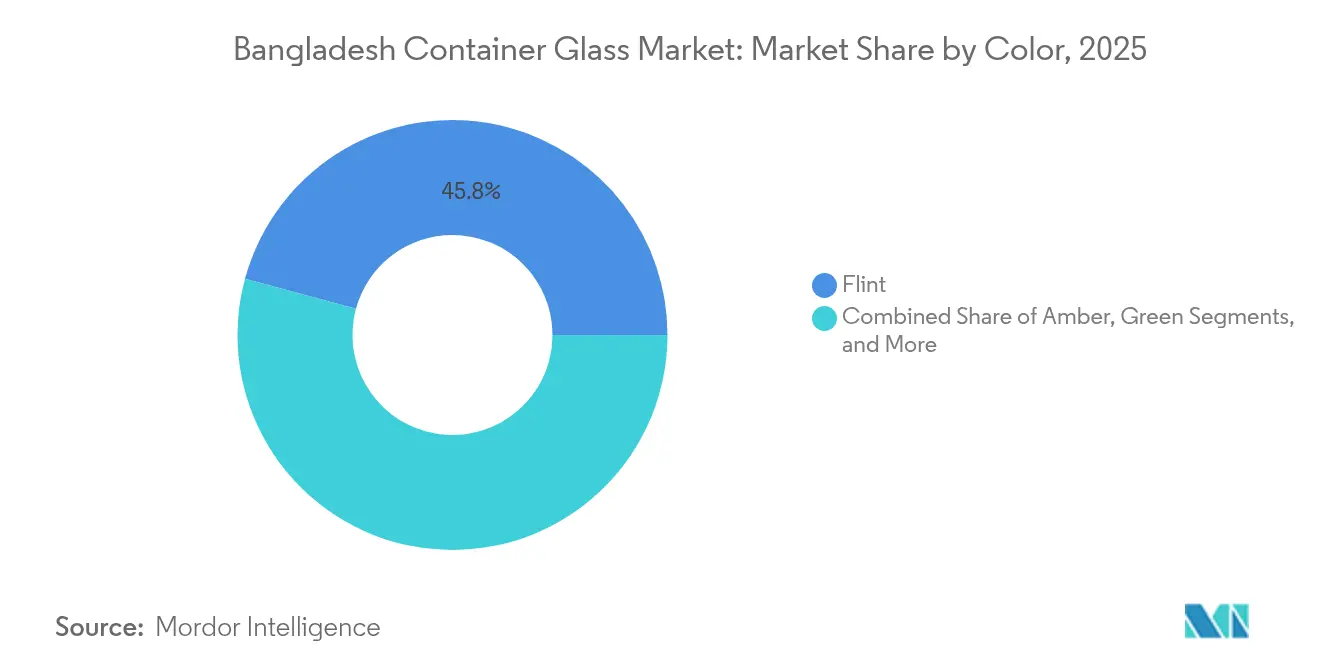

- By color, the Bangladesh container glass market size for the amber segment is projected to grow at a 3.55% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising beverage-packaging demand | +0.8% | Dhaka and Chittagong industrial corridors | Medium term (2-4 years) |

| Eco-friendly consumer preferences | +0.5% | Urban centers and tier-2 cities | Long term (≥ 4 years) |

| Pharmaceutical and cosmetics expansion | +0.4% | Dhaka, Chittagong, Gazipur | Short term (≤ 2 years) |

| Plastic-ban policy stimulus | +0.3% | Nationwide public-sector procurement | Short term (≤ 2 years) |

| Domestic furnace-capacity ramp-up | +0.2% | Gazipur, Narayanganj, Habiganj | Medium term (2-4 years) |

| Export incentives to regional markets | +0.1% | Border economic zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Beverage-Packaging Demand

Soft-drink sales, valued at USD 0.9 billion in 2024, are projected to grow at a 10% annual rate, sustaining a high volume of demand for both returnable and non-returnable glass bottles. Per-capita consumption has more than doubled since 2004 and is projected to keep rising as carbonated drinks, juices, and energy beverages penetrate tier-2 cities.[2]World Health Organization, “Technical assessment of beverage consumption in Bangladesh,” who.int Multinationals such as Coca-Cola, which holds a roughly 45% share, continue to bottle premium SKUs in glass for on-premise and cold-chain channels, reinforcing demand even as PET gains market share in take-home packs. Local challengers, such as Akij’s Mojo, leverage distinctive bottle shapes and embossed branding to differentiate themselves in crowded retail aisles, thereby amplifying unit growth in the Bangladesh container glass market. Capacity additions at Kiam Glassware and AkijBashir have introduced more narrow-neck lines, shortening lead times for beverage fillers and enabling seasonal promotions with specialized embossing and color runs. Although excise-tax shifts momentarily squeeze carbonate pricing, the industry’s 20% employment multiplier ensures supportive lobbying for long-term tax certainty, indirectly stabilizing demand for packaging.

Eco-Friendly Consumer Preferences

Bangladesh’s sweeping single-use plastic phaseout, effective from September 2024, explicitly recommends glass bottles for official purchases, setting a behavioral precedent for private organizations. Consumer surveys in Dhaka indicate that 30% of energy-drink buyers prefer glass over PET and cans, citing perceived purity and recyclability, despite the higher pack weight. Food-delivery aggregators now mandate glass sauce and condiment bottles for premium restaurant listings, raising the visibility of sustainable packaging in daily consumption patterns. Supermarkets have expanded return-and-refill kiosks for cooking oil jars, creating a closed-loop model that improves brand loyalty while reducing unit packaging costs, further expanding the Bangladesh container glass market. Marketing campaigns from cosmetics brands highlight the absence of microplastics in glass containers, cultivating aspirational demand among the 18-35 age cohort that values environmentally sound purchasing. Municipal recycling pilots in Chittagong have expanded color-sorted curbside pickups, nudging households to separate glass waste and reinforcing its recyclability narrative.

Pharmaceutical and Cosmetics Expansion

Local pharmaceutical revenues are on track to double from USD 3 billion in 2024 to USD 6 billion by 2025, driven by export-oriented incentives that offer 10% rebates on finished formulations and 20% on APIs. The pipeline includes 47 units at the upcoming API park near Dhaka, each requiring sterilizable amber glass vials compliant with USP Type III specifications. Pharma Aids’ new ampoule line in Gazipur exemplifies the downstream pull: its 11.38 crore BDT land investment alone signals confidence in a sharply rising demand curve for parenteral packaging. Cosmetic and personal-care labels are also scaling volumes, with glass jars gaining traction in fairness creams and serums that command premium shelf pricing in urban drugstores. Contract fillers have begun sourcing custom shapes locally, rather than importing small batches from Thailand, which shortens product-development cycles and boosts domestic tonnage in the Bangladesh container glass market. Export approvals to 127 countries expand the addressable base for Bangladeshi-made vials, positioning glassmakers for regionwide supply contracts.

Plastic-Ban Policy Stimulus

The Ministry of Environment’s August 2024 listing of 17 generic plastic items slated for elimination created an enforceable procurement baseline for all government agencies. The Cabinet Division mandated the use of glass bottles for official meetings, instantly raising quarterly demand from public-sector buyers across 64 districts. Private conglomerates have adopted these standards in their corporate campuses to signal alignment with national sustainability goals, resulting in institutional orders for glass carafes and canteen tableware. Food-service chains in shopping malls are now advertising plastic-free dining options, swapping PET water bottles for branded glass alternatives, and implementing deposit-return systems to reduce waste handling fees. Trade associations forecast that full enforcement could displace more than 15 kilotons of single-use plastics annually, with glass absorbing a sizable share where material rigidity and chemical inertness are necessary. Packaging converters have responded by commissioning feeder lines for low-weight jars, reducing gram weight by 12% on average, while maintaining breakage resistance through advanced annealing, thereby preserving margins under incoming demand spikes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET and aluminium substitution threat | -0.7% | Nationwide beverage segment | Medium term (2-4 years) |

| High energy intensity of glass melting | -0.5% | Gas-reliant industrial hubs | Short term (≤ 2 years) |

| Limited high-grade silica sand supply | -0.3% | Northern districts | Long term (≥ 4 years) |

| Inland logistics breakage and cost issues | -0.2% | Rural distribution routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PET and Aluminium Substitution Threat

Historically, PET conversions have eroded glass share in low-price carbonates, spotlighted by Partex’s 2000 shift that pioneered plastic bottles in Bangladesh. Current consumer polling indicates that 40% of energy-drink buyers prefer PET for its portability, compared to 30% each for glass and cans. Route-to-market economics amplify this preference: distributors servicing rural kiosks cite 9% lower handling costs when shifting from glass to PET six-packs due to weight efficiencies and reduced breakage. Beverage fillers still incur a refundable deposit of BDT 7-10 per bottle, tying up working capital that could be redeployed to marketing or cold-chain upgrades. Aluminum cans pose a threat to niche segments, such as ready-to-drink coffee, where 200 milliliter formats are easier to chill and stack, putting tactical pressure on the Bangladesh container glass market. Although brand owners recognize glass’s premium value, sustained cost differentials of USD 0.03-0.04 per unit in large-scale runs may favor alternate substrates in purely price-driven channels.

High Energy Intensity of Glass Melting

Glass furnaces consume 3.8-4.2 gigajoules of energy per ton, making profit margins highly sensitive to gas tariffs that tripled between 2020 and 2021 after LNG import hikes.[3]U.S. Geological Survey, “The Mineral Industry of Bangladesh in 2020-2021,” usgs.gov Industrial clusters in Gazipur and Narayanganj periodically face quota-based curtailments that force unplanned hot holding, adding refractory stress and repair costs. AkijBashir’s 71% renewable-energy mix underscores the strategic pivot toward off-grid solar and waste-heat recovery, but industry averages remain below 25% clean-energy penetration. Constrained energy also limits color campaigns because cullet ratio adjustments require stable melt temperatures, compelling manufacturers to lengthen batch runs and inflate working capital tied up in inventory. Smaller plants operating regenerative furnaces often postpone maintenance due to cash flow constraints, leading to 2-3% higher defect rates and up to a 5-kiloton annual yield loss across the market. While government talks of dedicated LNG terminals for industry are ongoing, near-term tariff pass-through to customers would threaten the price competitiveness of the Bangladesh container glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Pharmaceuticals Drive Premium Positioning

Volume dominance remains with beverages, yet pharmaceuticals and personal care anchor value growth in the Bangladesh container glass market. In 2025, beverages accounted for a 57.72% share, while cosmetics and personal care are projected to advance at a 3.18% CAGR through 2031. The sector’s inclination toward unique silhouettes and embossing keeps average selling prices 12-15% above those of flint commodity jars, stabilizing margins even in cost-sensitive non-alcoholic beverages. Carbonated-soft-drink fillers maintain legacy returnable bottles in on-premise channels, but PET’s convenience curtails adoption in suburban retail, an offset partly mitigated by premium craft sodas billed as natural and preservative-free that mandate inert glass packaging. Alcoholic beverages, although limited by excise controls, utilize glass for regulatory compliance purposes, including recyclability and UV protection, which adds incremental tonnage. Food producers contribute to baseline demand with export-oriented sauces and pickles destined for Middle East diaspora shelves, where regulatory import standards favor glass.

Pharmaceuticals contribute higher unit margins owing to stringent USP Type III requirements. Nasir Glass supplies serialized droppers for ophthalmic solutions, and Bengal Glass Works deploys borosilicate upgrades for parenteral packaging, collectively lifting the Bangladesh container glass market size for healthcare applications. Government price caps on essential drugs foster bulk procurement of standardized vial sizes, creating line-of-business predictability for glass converters. Cosmetics capitalize on aspirational purchasing, with color cosmetics pivoting to thick-walled jars that convey luxury. Local brand exports to India and Myanmar exploit duty preferences under SAFTA, broadening their market catchment. Personal-care brands also test silk-screen printing, supported by JMS Glass’s multicolor European presses, which helps tighten value-addition loops within Bangladesh. The cumulative effect is a nuanced product mix where beverage shipments anchor capacity utilization, while pharmaceuticals heighten profitability.

By Color: Amber Glass Captures Pharmaceutical Growth

Clear flint products retained a 45.79% volume share in 2025 because they serve the broadest spectrum from carbonated drinks to honey jars, facilitating quick brand recognition on store shelves. Flint’s mass-market pull sustains economies of scale in continuous furnaces, reducing unit energy by up to 6% due to stable melt chemistry. That said, amber glass is slated to expand at a 3.55% CAGR, eclipsing flint in compounded growth through 2031 thanks to pharmaceutical extensions that require UV-blocking properties. The Bangladesh container glass market size for amber containers is projected to rise concomitantly with domestic API output, as local formulators phase in photostable dosage forms. Beer imports into upper-middle-class neighborhoods often utilize amber long-neck bottles, as duty-free channels emphasize product differentiation. Although volume remains modest, the premium positioning has a strong influence on per-kiloton revenue capture.

Green glass continues to rise moderately within the beer and tonic-water niche, yet its share remains capped by limited domestic hop-based beverage production. Specialty colors such as cobalt blue target the perfume and high-end skincare markets, carrying a tenfold markup over flint due to batch-specific colorants like cobalt oxide. Nasir Glass’s pilot coater line expands possibilities for gradient finishes and metallic sheens, offering domestic fillers a previously import-dependent aesthetic. Simultaneously, recycling campaigns in Chittagong facilitate cullet sorting by color, enhancing furnace efficiency and providing cost-effective feedstock across all shades. The widening of color options reflects the maturing consumer palette and brand-differentiation strategies that collectively advance the Bangladesh container glass market beyond its commodity status.

Geography Analysis

The Bangladesh container glass market is geographically centered in the Dhaka-Gazipur-Narayanganj industrial triangle, where proximity to natural gas pipelines and customer clusters reduces freight overhead. Bengal Glass Works in Demra and JMS Glass in Dilkusha operate at the epicenter of beverage bottling lines, ensuring synchronous delivery schedules that mitigate stock-keeping bottlenecks. Gazipur hosts Nasir Glass Industries, featuring a 73,000-metric-ton float-glass line that co-locates raw-material warehousing, a configuration that lowers inbound silica logistics by 8% compared with legacy Dhaka plants. Habiganj, in the Sylhet division, has emerged as Bangladesh’s newest glass corridor, leveraging abundant silica deposits and a relatively reliable gas grid; AkijBashir’s 600-ton-per-day plant exemplifies this shift. Chittagong’s port proximity offers Asia-wide export gateways and duty-free raw material imports under bonded warehouse schemes, sustaining production aimed at Indian and Nepalese buyers via SAFTA preferences.

Northern districts, including Sylhet, Moulvibazar, and Kurigram, are being evaluated for the commercial extraction of high-purity quartz, following geological surveys that have confirmed resource densities of 50 kg per ton in Brahmaputra sands. While industrial-scale up awaits environmental clearance, these deposits represent a medium-term hedge against imported silica price volatility in the Bangladeshi container glass market. Inland transport challenges persist; double-handling at river ports inflates unit freight cost by 3%-5% for exporters dispatching to West Bengal by truck and rail. Government investment in inland container depots and four-lane highway upgrades aims to reduce lead times by two days, thereby improving on-time delivery metrics that are critical for pharmaceutical clients with strict shelf-life constraints. Coastal economic zones, particularly Matarbari, are slated for cold-chain integrated warehouses, which will add synergies for beverage fillers that rely on temperature-controlled export containers. Collectively, these infrastructural enhancements recalibrate the geographic calculus in favor of diversified capacity deployment across Bangladesh's container glass market clusters.

Competitive Landscape

The Bangladesh container glass market is moderately concentrated, with the top five producers accounting for nearly 65% of the installed capacity. Bengal Glass Works, JMS Glass Industries, and Nasir Glass collectively supply major beverage bottlers and pharmaceutical packers, often under multiyear offtake agreements that safeguard furnace utilization. New entrants, such as Kiam Glassware and AkijBashir Group, intensify competitive rivalry by commissioning European IS machines and high-precision quality-control systems, thereby narrowing historical quality gaps versus imports. Investment cycles are showing a distinct pivot toward green manufacturing; AkijBashir has achieved 71% renewable energy integration through rooftop solar and waste-heat recovery, signaling the pace at which environmental metrics will influence customer preference in the Bangladesh container glass market.

Strategic differentiation now centers on vertical integration and fast design turnaround. Laboratories capable of in-house mold fabrication reduce new-product lead time to 15 days, providing domestic cosmetic brands with agility in seasonal launches. Process digitization, SCADA-based furnace monitoring, and vision inspection for defect detection have reduced rejection rates by 1.8 percentage points since 2024 across top plants. Export ambitions extend beyond South Asia, with exploratory shipments to East African breweries under consideration, supported by government cash incentives under the 2024-27 Export Policy, which favors high-value manufactured goods. Collective bargaining for LNG tariffs through the Bangladesh Glass Manufacturers’ Association may further lower energy cost volatility. While PET and aluminum remain structural substitutes, the orchestrated move toward premium segments and pharmaceutical compliance strengthens the long-term viability of the Bangladesh container glass market.

Bangladesh Container Glass Industry Leaders

J.M.S.Glass Industries Limited

The Bengal Glass Works Limited

Feemio Group Co., Ltd.

Labtex Bangladesh

DK Glass Solutions Pvt Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Kiam Glassware Industries commenced first-phase production at Bangabandhu Sheikh Mujib Shilpa Nagar, adding 70 tons-per-day soda-lime capacity.

- January 2025: Usmania Glass Sheet Factory auctioned multiple raw-material lots to secure silica sand, soda ash, dolomite, limestone, feldspar, and coal.

- September 2024: The Ministry of Environment enforced a nationwide ban on 17 single-use plastics, endorsing glass containers for public-sector procurement.

- May 2024: The National Board of Revenue proposed new duties on capital machinery destined for Export Processing Zones, impacting future furnace installations.

Bangladesh Container Glass Market Report Scope

Glass containers are vessels made from glass used to store and protect products such as food, beverages, pharmaceuticals, cosmetics, and chemicals. Available in diverse shapes and sizes, such as bottles, jars, and vials, these containers provide airtight seals and protect contents from external contaminants. Glass packaging is valued for its non-reactive nature, preservation of product quality, and high recyclability. These attributes make glass containers a preferred choice for packaging across multiple industries.

Bangladesh container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the current volume of the Bangladesh container glass market?

The Bangladesh container glass market size reached 497.7 kilotons in 2026 and is projected to hit 551.11 kilotons by 2031.

Which end-user segment leads demand for glass containers in Bangladesh?

Beverages dominate with 57.72% market share, followed by food, pharmaceuticals, and fast-growing cosmetics.

Why is amber glass gaining popularity in Bangladesh?

Amber glass offers UV protection critical for pharmaceuticals and premium beverages, driving a 3.55% CAGR through 2031.

How are single-use plastic bans affecting glass demand?

Government bans on 17 plastic categories mandate glass in official procurement, triggering wider adoption across food service and retail chains.

Which regions host the majority of Bangladesh’s glass manufacturing capacity?

Dhaka, Gazipur, and Narayanganj form the primary industrial hub, with emerging plants in Habiganj and logistical advantages near Chittagong port.

What challenges do Bangladeshi glass makers face?

Key hurdles include high energy intensity, PET substitution in cost-sensitive segments, and periodic natural-gas supply constraints.

Page last updated on: