Pakistan Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

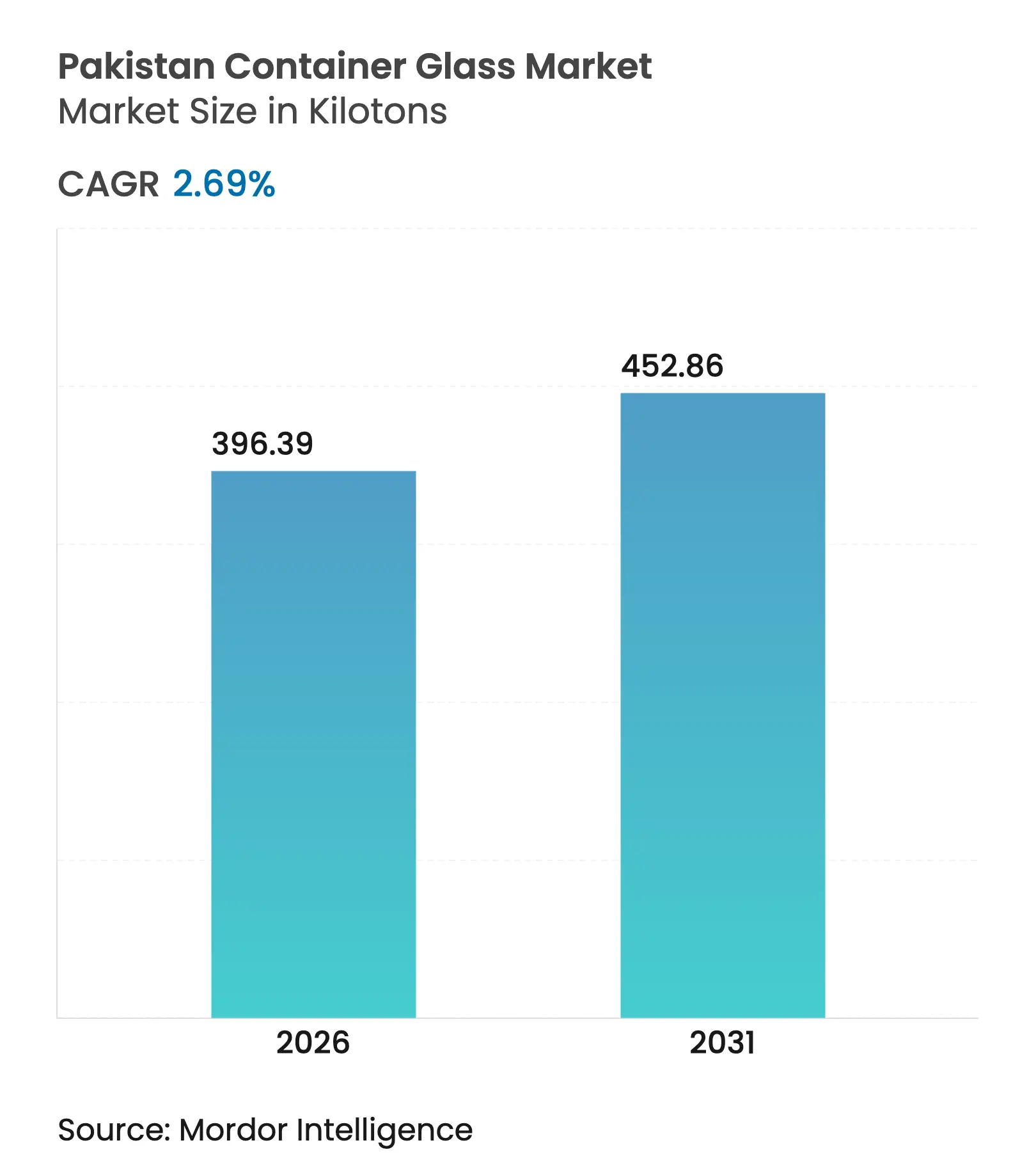

| Market Volume (2026) | 396.39 kilotons |

| Market Volume (2031) | 452.86 kilotons |

| CAGR | 2.69 % |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Pakistan Container Glass Market Analysis by Mordor Intelligence

The Pakistan container glass market size was valued at 386.01 kilotons in 2025 and estimated to grow from 396.39 kilotons in 2026 to reach 452.86 kilotons by 2031, at a CAGR of 2.69% during the forecast period (2026-2031). This steady growth is driven by beverage bottling expansion, pharmaceutical fill-finish investments, and policy incentives that encourage export-oriented manufacturing. Demand momentum is counter-balanced by high energy costs, import compression that limits modernization, and mounting competition from PET and metal packaging. Leading producers are therefore prioritizing furnace retrofits, automation, and halal-certified lines to defend share and unlock premium export opportunities. On balance, the Pakistani container glass market is maturing but still offers headroom through niche applications, sustainability positioning, and untapped demand from the GCC.

Key Report Takeaways

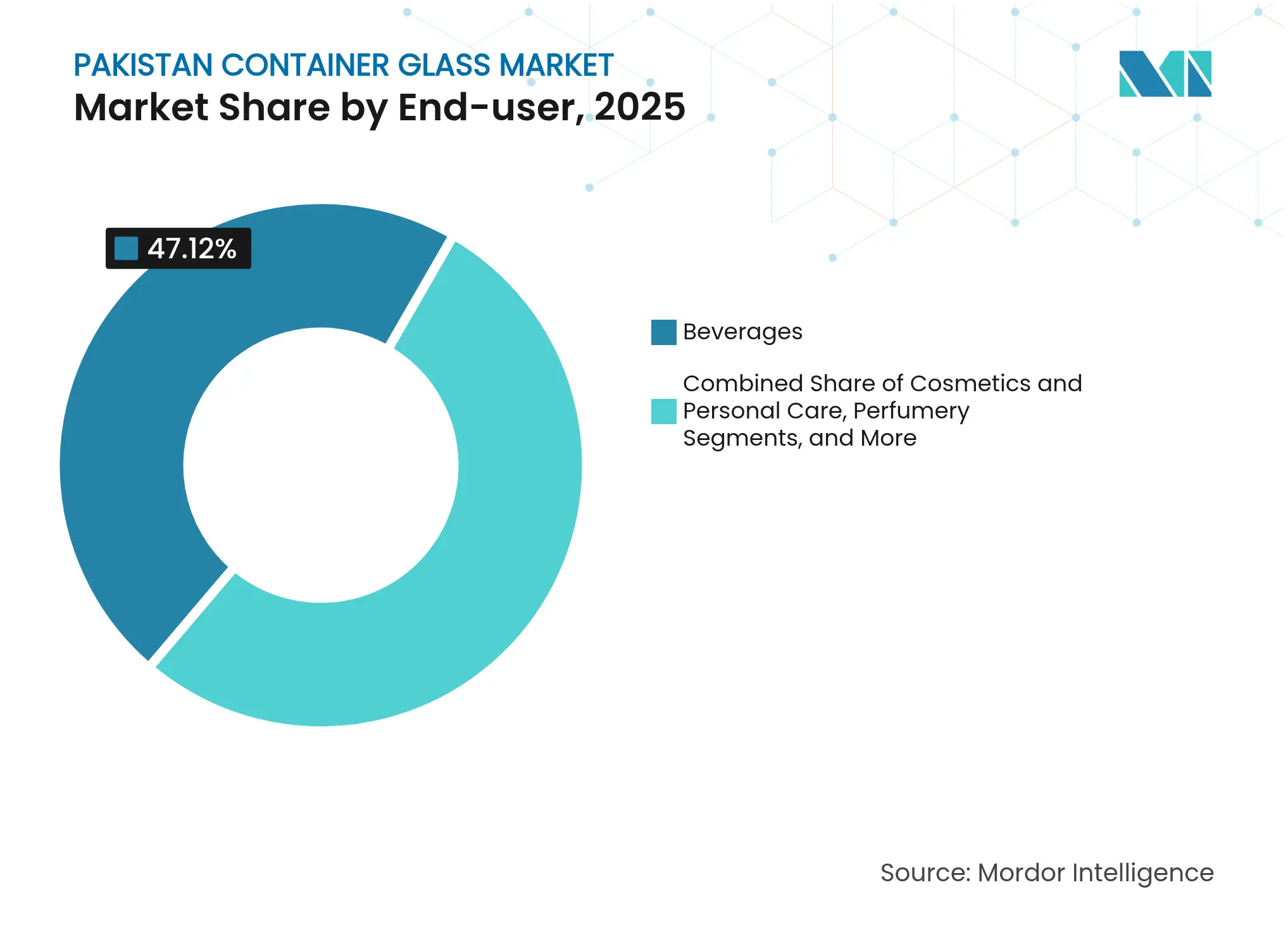

- By end-user, beverages captured 47.12% of the Pakistan container glass market share in 2025.

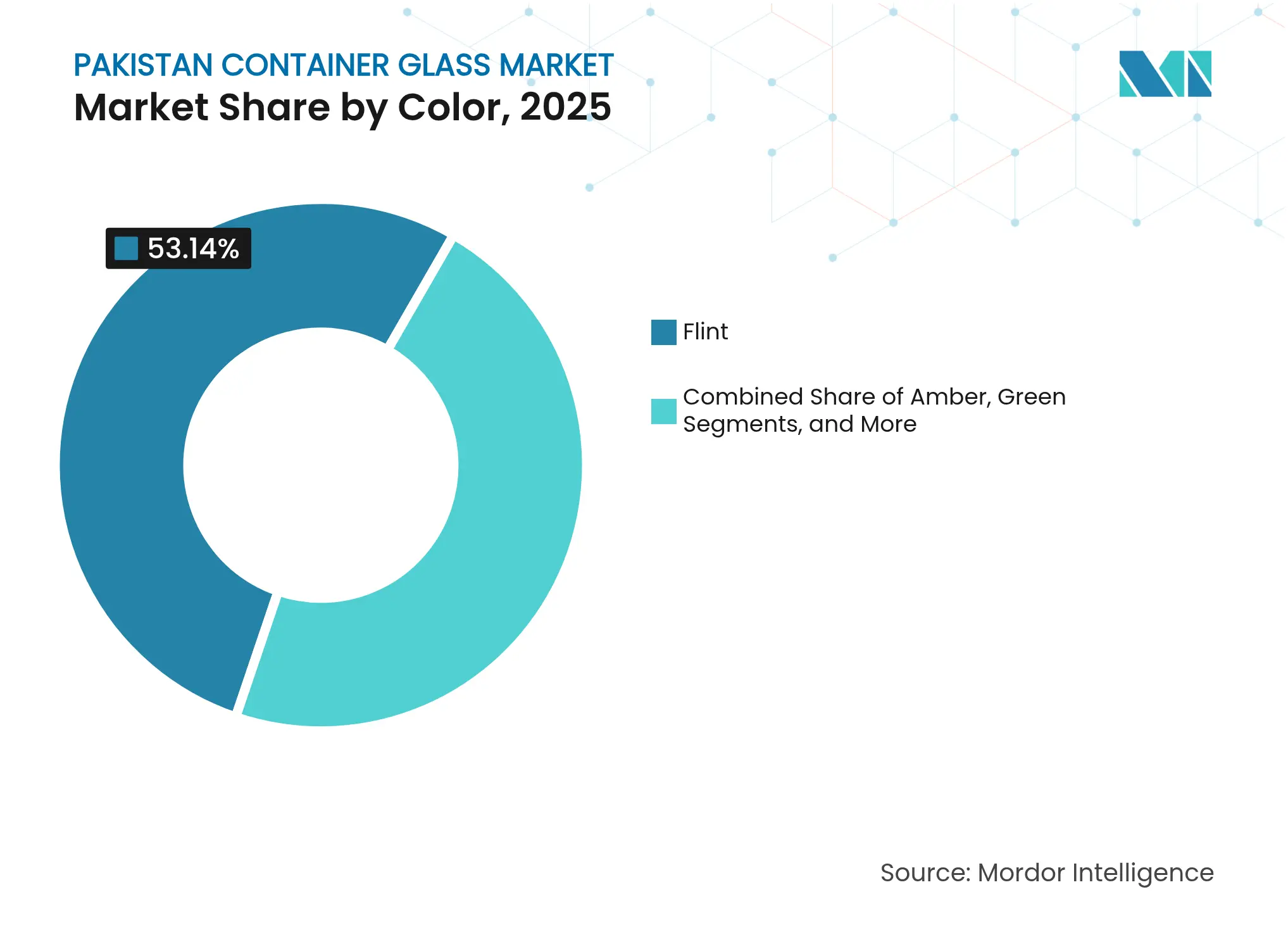

- By color, the Pakistan container glass market for amber glass is projected to grow at a 4.49% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Container Glass Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing food and beverage production Growing food and beverage production | +0.7% | National - Punjab and Sindh industrial zones | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.7% | Geographic Relevance:National - Punjab and Sindh industrial zones | Impact Timeline:Medium term (2-4 years) |

Pharmaceutical fill-finish expansion Pharmaceutical fill-finish expansion | +0.6% | National - clusters in Karachi and Lahore | Long term (≥ 4 years) | |||

Consumer preference for recyclable packaging Consumer preference for recyclable packaging | +0.4% | Urban centers, tier-2 cities | Medium term (2-4 years) | |||

Local manufacturing incentives and export corridors Local manufacturing incentives and export corridors | +0.4% | SEZs and export processing zones | Long term (≥ 4 years) | |||

Halal-certified glass lines targeting GCC markets Halal-certified glass lines targeting GCC markets | +0.2% | Export-oriented coastal facilities | Long term (≥ 4 years) | |||

Govt. gas subsidy for oxy-fuel furnace retrofits Govt. gas subsidy for oxy-fuel furnace retrofits | +0.1% | National | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Growing food and beverage production

Pakistan’s processed food and non-alcoholic beverage output continues to climb, driving incremental glass demand for soft drinks, juices, and condiments. Large-scale manufacturing recorded a 4.7% month-on-month rebound in August 2024, with food and beverages in positive territory, while agricultural exports of rice and fresh produce jumped 77.6% and 17.4% respectively. Higher bottling runs require durable, inert, and premium-looking glass, especially for carbonated beverages, whose household penetration has risen from 25.79% to 37.75% over the past decade. The concentration of beverage plants in Punjab and Sindh keeps freight costs low for suppliers, thereby bolstering the Pakistan container glass market. Continuous capacity additions by Coca-Cola Icecek and other bottlers sustain order books for flint bottles, while niche craft-juice producers adopt textured designs to differentiate on shelves.

Pharmaceutical fill-finish expansion

The rapid scaling of domestic vaccine, syrup, and injectable facilities increases demand for vials, ampules, and narrow-neck bottles. Chemical and pharmaceutical exports grew 9.7% in 3Q 2024. Ghani Global Glass ramped up its ampoule line to 55 million units per month to capitalize on this upswing. Amber glass benefits disproportionately because of ultraviolet-blocking needs in cephalosporin, insulin, and dermatology drugs. Regulatory alignment with GCC and African pharmacopeias positions compliant suppliers to plug regional shortages and fortify the Pakistan container glass market.

Consumer preference for recyclable packaging

Urban households are increasingly aware of their recyclable footprints. Glass’s infinite recyclability without quality loss supports brand sustainability claims, particularly in premium beverages, skincare, and fragrance products. Advocacy by the CoRe Alliance for circular-economy tax incentives and duty-free recycling machinery signals policy backing. Brands such as National Foods and Tapal Tea have transitioned their flagship SKUs to clear jars, citing product visibility and waste reduction as key goals.[1]Khan et al., “Marble Production and Environmental Pressure,” Research Square, researchsquare.com The resulting demand cluster enhances the value proposition of the Pakistani container glass market compared to single-use PET.

Local manufacturing incentives and export corridors

The Export Facilitation Scheme 2021, National Tariff Policy 2025-30, and targeted SEZ perks lower input duties, fast-track utilities, and streamline customs for exporters. Foreign direct investment surged 48.2% year-over-year to USD 771 million in 1Q FY2025, with Chinese capital accounting for 52% of the inflow. Container glass firms co-located in Rashakai and Allama Iqbal Industrial Cities can leverage common effluent plants and rail spurs to fulfill GCC orders. These incentives help offset Pakistan’s high logistics bill and expand the regional reach of the Pakistan container glass market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High energy cost and power outages High energy cost and power outages | -1.0% | National - acute in industrial zones | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.0% | Geographic Relevance:National - acute in industrial zones | Impact Timeline:Short term (≤ 2 years) |

PET and metal packaging substitution PET and metal packaging substitution | -0.6% | Urban markets, rural spillover | Medium term (2-4 years) | |||

Volatile domestic soda-ash supply Volatile domestic soda-ash supply | -0.4% | National | Medium term (2-4 years) | |||

Fragmented return-logistics network Fragmented return-logistics network | -0.2% | National | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High energy cost and power outages

Continuous furnaces operate above 1,500 °C and cannot tolerate unplanned shutdowns without the buildup of glassy cullet, which destroys refractories. Pakistan’s industrial electricity tariff jumped 29% in 2024, while unannounced load-shedding persisted in key clusters. Producers responded by installing captive LNG generators and embracing oxy-fuel conversions, partially cushioned by a temporary gas subsidy. Nonetheless, elevated unit energy costs trim margins and curb furnace rebuilds, moderating near-term growth of the Pakistan container glass market.

PET and metal packaging substitution

Lightweight PET bottles and aluminum cans erode glass’s share in carbonated soft drinks and edible oil. Domestic PET capacity additions benefited from easier import of resin technology relative to heavy furnace equipment. Lower freight charges and reduced breakage appeal to high-volume beverage fillers distributing beyond tier-1 cities. Unless glass manufacturers reinforce premium branding and recyclability messaging, substitution could erode volume growth in the Pakistani container glass market.

Segment Analysis

By End-user: Beverage Dominance and Cosmetics Upswing

The beverage segment accounted for 47.12% of the Pakistan container glass market share in 2025, as bottlers expanded their filling lines for carbonated drinks, juices, and isotonic beverages. Continuous investments by multinational beverage firms drove the uptake of lightweight flint bottles, sustaining production runs across Punjab and Sindh. Forecasts indicate steady 2.05% annual volume gains as per-capita consumption edges higher. In parallel, artisanal juice and cold-brew tea players favor distinctive embossed bottles that lift brand recall and retail margins, further reinforcing the Pakistan container glass market.

Cosmetics and personal care, although currently smaller, are projected to chart a 4.68% CAGR and outpace all other consumer segments. Rising disposable income among urban Gen Z shoppers fuels demand for serums, fragrances, and color cosmetics packed in colored and frosted glass. Independent beauty labels outsource small-batch jars to flexible converters, while multinationals localize production to avoid duties and shorten lead times. Premiumization trends align with higher unit prices, driving disproportionate revenue capture relative to tonnage in the Pakistan container glass market size for this segment.

Note: Segment shares of all individual segments available upon report purchase

By Color: Flint Leadership, Amber Momentum

Flint glass captured 53.14% of 2025 demand, underpinning its status as the default choice for beverages, jams, and cosmetics that rely on product visibility to build consumer trust. Standardized flint bottles also enable high recycled cullet content, improving sustainability metrics. Competitive kilns have achieved wall thickness reduction without compromising top-load strength, which helps curb freight expenses in the Pakistani container glass market.

Amber glass is forecast to expand at a 4.49% CAGR, supported by pharmaceutical fill-finish growth and UV-sensitive nutraceuticals. Drug regulators in the GCC and African Union openly prefer amber for light-sensitive antibiotics and vitamins, prompting local converters to install amber-capable forehearths. Capacity investments respond to this shift, with Ghani Glass dedicating a furnace channel exclusively to amber bottles. Green glass remains a specialty around premium mineral water and craft beverages, leveraging its association with heritage brands.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Punjab and Sindh together house over 80% of installed furnace capacity, clustering near beverage bottlers, pharma hubs, and port logistics. The Lahore-Sheikhupura and Karachi-Hub corridors offer rail and motorway links that reduce inbound raw material and outbound finished goods costs. However, rolling blackouts in both provinces and gas rationing during winter expose producers to unplanned downtime. Government-led industrial estates, such as Faisalabad’s Allama Iqbal Industrial City, offer captive power and effluent-treatment plants, thereby mitigating compliance and utility hurdles for new entrants.

Khyber Pakhtunkhwa’s Hayatabad Industrial Estate illustrates how shared utilities and clusters enable smaller converters to scale operations swiftly. Yet, remoteness from deep-water ports inflates export freight, dampening cross-border competitiveness. Balochistan’s emerging SEZ near Gwadar port promises future cost relief once rail links mature, potentially reshaping the Pakistan container glass market’s geographic footprint.

Export flows remain thin relative to potential. SAARC intraregional trade faces a tariff-equivalent cost of 161%. Digitizing customs and adopting cross-border paperless trade could shave 11% off logistics expenses and stimulate shipments to GCC, Central Asia, and East Africa. Coastal Karachi plants already dispatch small amber-vial consignments to Oman and the United Arab Emirates, but high back-haul imbalance and container shortages limit scale.

Competitive Landscape

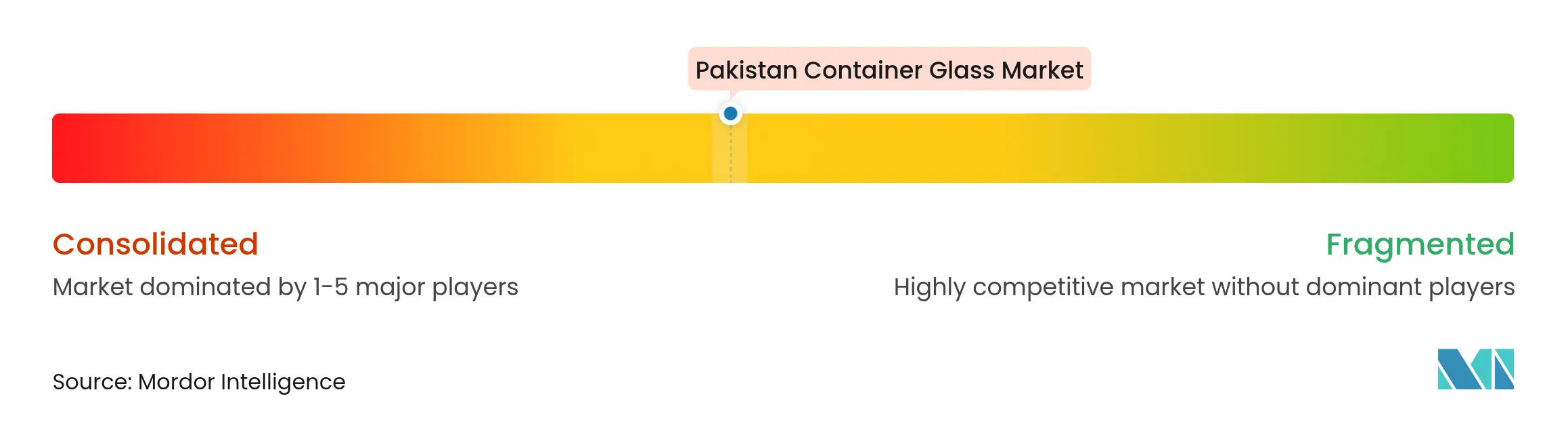

Market Concentration

Domestic incumbents, such as Ghani Glass, Tariq Glass Industries, and Balochistan Glass, dominate the installed capacity. Ghani commissioned a float line and overhauled its main furnace in January 2025 to restore throughput after a maintenance outage, signaling a commitment to technological upgrades. Tariq Glass had doubled its profits in FY 2024, only to experience a drop in early FY 2025, highlighting its sensitivity to energy tariffs and currency fluctuations. Newer entrants are leveraging government incentives to install oxy-fuel burners, which can reduce gas use by up to 20%, thereby enhancing their competitiveness.

Strategic focus is shifting toward higher-margin niches: pharmaceutical amber vials, cosmetics jars with complex shapes, and halal-certified export bottles. Automation, quality control, and lean warehousing are being deployed to counteract energy volatility. Compliance with the Pakistan Environmental Protection Act 1997 and the National Environmental Quality Standards raises entry barriers and favors incumbents that have invested in emission scrubbers and wastewater recycling.[3]Ministry of Climate Change, “Pak EPA Acts,” mocc.gov.pk

Chinese giants such as Fuyao Glass, fresh from a 2024 expansion, exert price pressure in generic flint bottles by offering large-volume exports, forcing local producers to specialize. Domestic firms are therefore partnering with European mold designers and investing in hot-end coating lines to lift durability and aesthetics. Given that the top five players control roughly 65% of domestic capacity, market rivalry is intense but not oligopolistic, leaving room for regional specialists to capture share within the Pakistan container glass market.

Pakistan Container Glass Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ghani Glass Limited restarted its primary furnace after upgrades, restoring capacity lost to an earlier shutdown.

- May 2024: Balochistan Glass Limited began operating a new 110-ton-per-day furnace, the largest single addition in recent years, aimed at beverage and food packaging demand.

- March 2024: Fuyao Glass Industry Group completed its Fuqing export expansion, adding float capacity that intensifies regional competition.

- March 2024: Pakistan secured a USD 1.03 billion IMF tranche that stabilized macro conditions.

Table of Contents for Pakistan Container Glass Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing food and beverage production

- 4.2.2Pharmaceutical fill-finish expansion

- 4.2.3Consumer preference for recyclable packaging

- 4.2.4Local manufacturing incentives and export corridors

- 4.2.5Halal-certified glass lines targeting GCC markets

- 4.2.6Govt. gas subsidy for oxy-fuel furnace retrofits

- 4.3Market Restraints

- 4.3.1High energy cost and power outages

- 4.3.2PET and metal packaging substitution

- 4.3.3Volatile domestic soda-ash supply

- 4.3.4Fragmented return-logistics network

- 4.4PESTEL Analysis

- 4.5Industry Supply-Chain Analysis

- 4.6Container Glass Furnace Capacity and Locations in Pakistan

- 4.6.1Plant Locations and Year of Commencement

- 4.6.2Production Capacities

- 4.6.3Types of Furnaces

- 4.6.4Color of Glass Produced

- 4.7Export-Import Data of Container Glass - Covering Key Import and Export Destinations

- 4.7.1Import Volume and Value, 2021-2024

- 4.7.2Export Volume and Value, 2021-2024

- 4.8Porter’s Five Forces Analysis

- 4.8.1Threat of New Entrants

- 4.8.2Bargaining Power of Suppliers

- 4.8.3Bargaining Power of Buyers

- 4.8.4Threat of Substitutes

- 4.8.5Competitive Rivalry

- 4.9Raw Material Analysis

- 4.10Recycling Trends for Glass Packaging

- 4.11Demand vs Supply Analysis for Glass Packaging

5. MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1By End-user

- 5.1.1Beverages

- 5.1.1.1Alcoholic

- 5.1.1.1.1Beer

- 5.1.1.1.2Wine

- 5.1.1.1.3Spirits

- 5.1.1.1.4Other Alcoholic Beverages (Cider and Other Fermented Drinks)

- 5.1.1.2Non-Alcoholic

- 5.1.1.2.1Juices

- 5.1.1.2.2Carbonated Drinks (CSDs)

- 5.1.1.2.3Dairy Product Based Drinks

- 5.1.1.2.4Other Non-Alcoholic Beverages

- 5.1.2Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles)

- 5.1.3Cosmetics and Personal Care

- 5.1.4Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.5Perfumery

- 5.2By Color

- 5.2.1Green

- 5.2.2Amber

- 5.2.3Flint

- 5.2.4Other Colors

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves and Developments

- 6.3Company Market Share Analysis, (Based on Latest Production Capacity)

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Ghani Glass Limited

- 6.4.2Tariq Glass Industries Limited

- 6.4.3Balochistan Glass Limited

- 6.4.4Feemio Group Co., Ltd.

- 6.4.5ZSons Group of Pakistan

- 6.4.6Kary packaging

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Pakistan Container Glass Market Report Scope

Container glass is designed for manufacturing glass containers, including bottles, jars, drinkware, and bowls. Its key attributes include chemical inertness, sterility, and non-permeability, rendering it especially sought after in the beverage, food, pharmaceutical, and cosmetic sectors. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

Pakistan container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.