Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

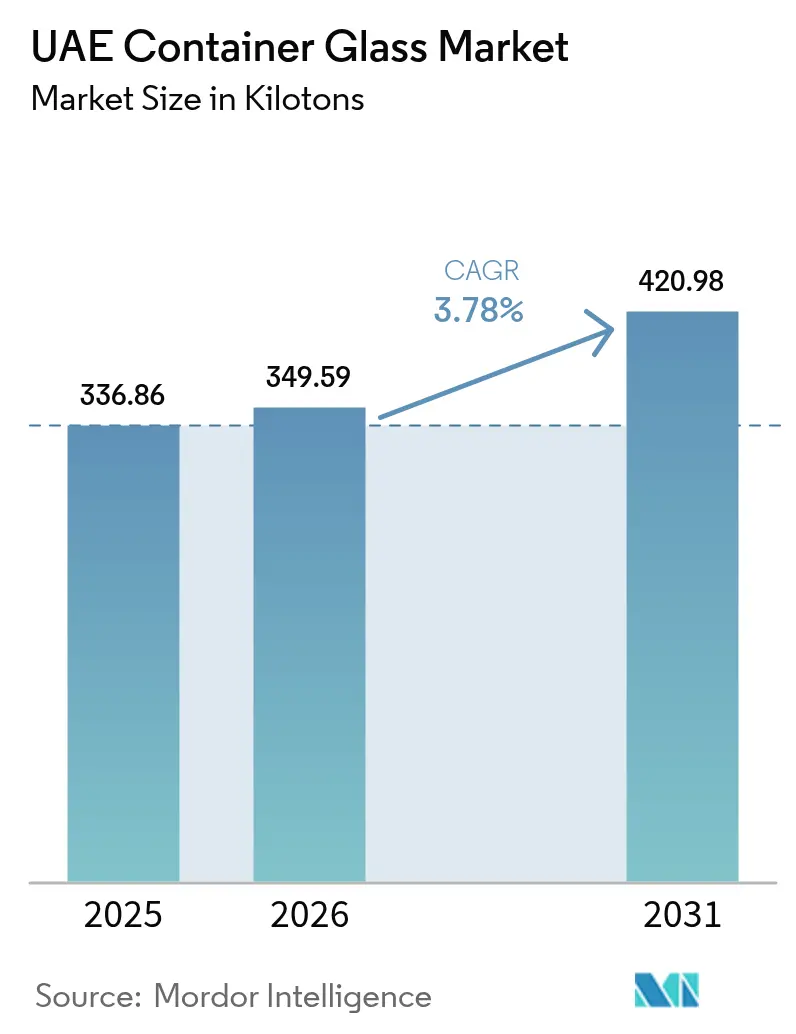

| Base Year Market Size (2025) | 336.86 kilotons |

| Market Volume (2026) | 349.59 kilotons |

| Market Volume (2031) | 420.98 kilotons |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

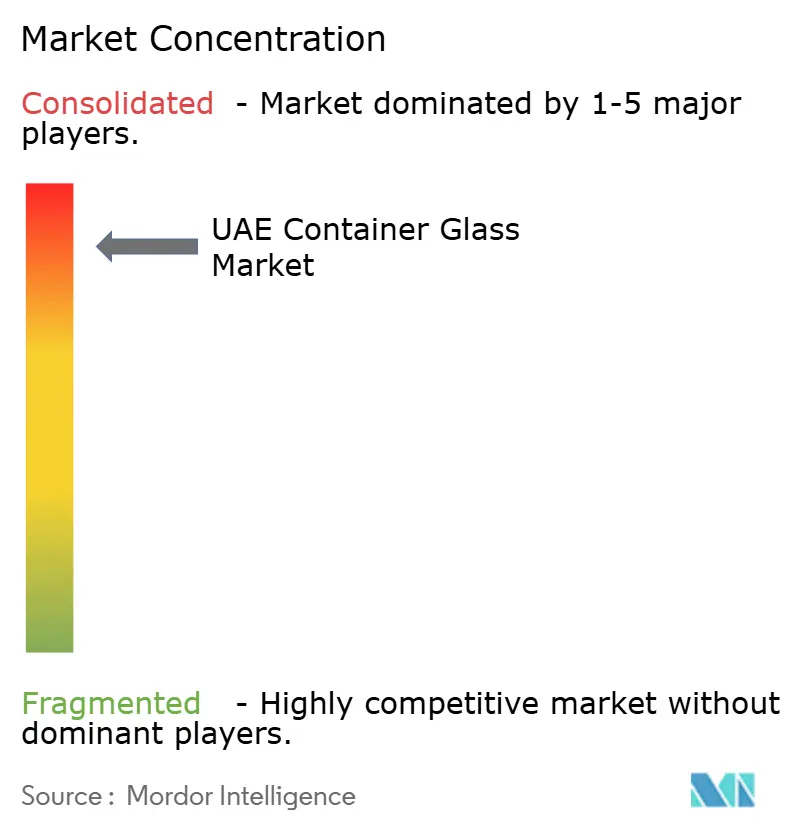

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Container Glass Market Analysis by Mordor Intelligence

The UAE container glass market size was valued at 336.86 kilotons in 2025 and is estimated to grow from 349.59 kilotons in 2026 to reach 420.94 kilotons by 2031, at a CAGR of 3.78% during the forecast period (2026-2031). Robust demand from beverages, pharmaceuticals, and perfumery, along with fresh foreign direct investment in Ras Al Khaimah and Dubai, and policy-backed circular-economy targets are combining to push volumes higher, even as lightweight plastic alternatives and elevated energy tariffs curb momentum. Growing export corridors into Saudi Arabia, Oman, Qatar, and East Africa amplify the UAE’s role as a re-export hub for regional fast-moving consumer goods that specify glass for premium positioning. Container glass also benefits from a rising preference for refillable formats in premium bottled-water hospitality programs and from fragrance brands that require heavy flacons to signal luxury. At the same time, elevated industrial electricity prices of 36.6 fils per kilowatt-hour during the 2025 summer peaks inflate furnace operating costs.

Key Report Takeaways

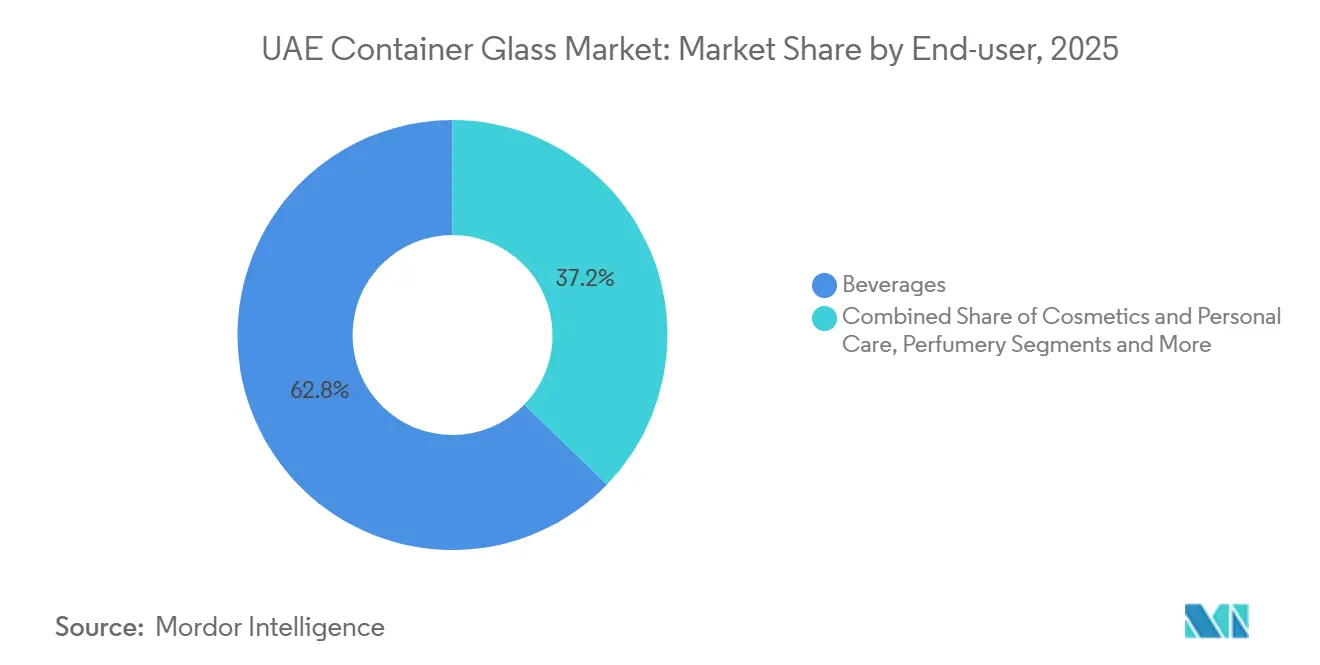

- By end-user, beverages led with 62.76% of the UAE container glass market share in 2025. Perfumery is projected to advance at a 4.74% CAGR through 2031.

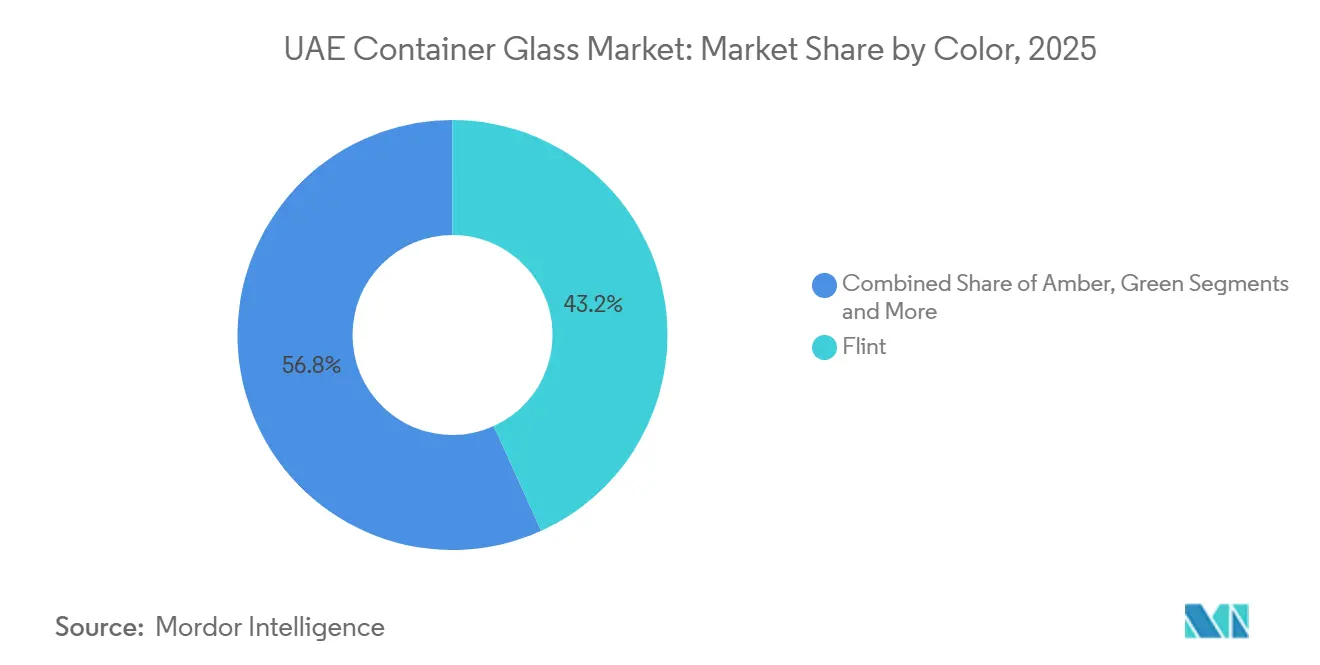

- By color, flint captured 43.23% of the UAE container glass market in 2025. Amber glass is forecast to expand at a 4.59% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmaceutical Manufacturing Expansion in Ras Al Khaimah and Dubai | +0.8% | Ras Al Khaimah, Dubai | Medium term (2-4 years) |

| Government Incentives for Sustainable Packaging Solutions | +0.6% | Dubai, Abu Dhabi, national rollout | Short term (≤2 years) |

| Growth of E-Commerce and Export-Oriented FMCG | +0.7% | National, GCC spillover | Medium term (2-4 years) |

| Strategic FDI and Local Furnace Investments | +0.9% | Dubai, Abu Dhabi, Ras Al Khaimah | Long term (≥4 years) |

| Booming Beverage Sector Including Water and Juices | +1.0% | National | Short term (≤2 years) |

| Rising Demand for Premium Packaging in Cosmetics and Perfumery | +0.5% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pharmaceutical Manufacturing Expansion in Ras Al Khaimah and Dubai

Ras Al Khaimah’s life-sciences cluster supplies validated amber and flint bottles that satisfy USP Type I and II standards, enabling Julphar and other drug makers to scale insulin, syrup, and supplement lines for regional export.[1]FoodTechBiz, “Sidel introduces EvoBLOW Laser,” foodtechbiz.com RAK Ghani Glass operates a 43,800-tonne plant that outputs more than 600 million pharmaceutical containers a year, securing dependable local feedstock and shortening approval timelines for new formulations. RAKEZ confirmed 13,141 new company registrations in 2024, 66% above 2023, broadening the base of potential buyers of pharmaceutical glass. Policy alignment with World Health Organization good-manufacturing-practice rules further hardens entry barriers, channeling demand toward suppliers with certified clean-room operations. As clinical pipelines mature, validated glass suppliers enjoy mid-term volume upside concentrated in Ras Al Khaimah and Dubai.

Government Incentives for Sustainable Packaging Solutions

A six-month Extended Producer Responsibility pilot launched in July 2025 obliges brand owners to fund the collection and recycling of post-consumer packaging, thereby narrowing the price gap between glass and single-use plastics.[2]UAE Ministry of Climate Change and Environment, “Extended Producer Responsibility Pilot,” moccae.gov.ae The national Circular Economy Policy Framework also targets 75% landfill diversion by 2030, while the new Tahweel secondary-raw-materials marketplace encourages cullet trading, creating a financial rationale for higher glass recollection rates. Although Random Global’s automated plant in Dubai processes 100 million bottles annually, only 10% of them re-enter container production, so cullet supply still lags furnace demand. Near-term, producers that pre-fund collection infrastructure or invest in color-sorted cullet will meet emerging thresholds and secure supply, providing a measurable advantage in public tenders and retailer procurement.

Growth of E-Commerce and Export-Oriented FMCG

E-commerce grew faster than any other channel in 2025, as Noon, Amazon.ae, and Carrefour online amplified consumer access to premium jams, honeys, and specialty oils often packed in glass jars for shelf-life extension and gifting appeal. Bottlers use the UAE’s duty-free zones to consolidate, label, and dispatch goods into Oman and Saudi Arabia, leveraging Jebel Ali’s bonded warehousing to cut clearance times. Ghana imported USD 0.76 million in glass jars from the UAE in 2023, underscoring African demand for re-exports. Online platforms bundle fragile-item insurance and offer reusable outer cartons, mitigating breakage and increasing merchant willingness to select heavier packaging. Over the medium term, combined digital-commerce growth and free-zone incentives sustain incremental demand across all emirates.

Strategic FDI and Local Furnace Investments

Dubai Investments broke ground on a USD 163.35 million second float line at Khalifa Industrial Zone in October 2025, doubling capacity to 1,200 tonnes per day and showcasing global appetite for large-scale glass assets in the UAE.[3]“Dubai Investments to double float-glass capacity,” albawaba.com Source: Saverglass, “Saverglass RAK Facility,” saverglass.com Although the project targets architectural glass, the financing structure, preferential land rents, and HORN Glass’s energy-efficient technology create a replicable template for container-glass furnaces once domestic demand crosses critical mass. RAKEZ road-shows in Mumbai and Hyderabad in 2025 highlighted 100% foreign ownership and zero corporate tax for industrial clusters, stimulating enquiries from packaging investors. Long gestation cycles mean capacity will surface after 2029, but early land banking and engineering procurement drive a visible pipeline that underpins long-term CAGR support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Lightweight Plastic and Flexible Packaging | -0.5% | National | Short term (≤2 years) |

| High Energy Consumption and Carbon Emissions in Glass Melting | -0.4% | National | Medium term (2-4 years) |

| Logistics and Breakage Risks in Regional Distribution | -0.2% | GCC export corridors | Short term (≤2 years) |

| Limited Local Cullet Collection and Recycling Infrastructure | -0.2% | National | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Competition from Lightweight Plastic and Flexible Packaging

Polyethylene terephthalate producers showcased a laser-based heating system at Gulfood Manufacturing 2025 that trims preform waste by 50%, improving cost structures and encouraging beverage fillers to stay with plastic.[4]FoodTechBiz, “Sidel introduces EvoBLOW Laser,” foodtechbiz.com Lifecycle studies indicate that glass must be reused 35 times to outperform single-use PET on carbon metrics, a hurdle that many retail supply chains have not yet met. Brand owners of mass-market water and soft drinks still default to PET for its lighter freight weight and lower shelf price, keeping glass volumes confined to premium tiers. Near-term, campaigns that bundle carbon-offset certificates with PET may widen the cost-to-benefit gap, temporarily tempering demand for the UAE container glass market.

High Energy Consumption and Carbon Emissions in Glass Melting

Continuous furnaces exceed 1,500 °C and rely heavily on electricity, the second-largest expense after raw materials. Abu Dhabi’s 2025 tariff schedule showed 36.6 fils per kilowatt-hour at peak, squeezing margins during the hottest months when cooling loads also rise ADDC.AE. While Union Cement captured 25 megawatts from waste-heat recovery, container-glass operators have yet to install similar modules, so energy-intensity remains higher than aluminum and PET alternatives. As voluntary carbon disclosure spreads among GCC retailers, glass makers face pressure to demonstrate absolute emission cuts, not just recycling claims. Mid-term, plants that deploy oxy-fuel firing or hybrid-electric melting will preserve competitiveness, yet substantial capital outlays may slow adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Dominant Beverage Volumes, Accelerating Perfumery Upside

In 2025 beverages represented 62.76% of UAE container glass market size, driven by non-alcoholic juices, carbonated drinks and refillable premium water products that rely on strong barrier properties and visual clarity. The share stayed resilient as hotels upgraded to in-house bottling and regional FMCG exporters shifted to glass for differentiated shelf appeal ZAWYA. Alcoholic segments remain niche due to licensing constraints, yet imported premium spirits utilize bespoke flint bottles that elevate duty-free sales. Dairy-based probiotic drinks added incremental tonnage by adopting small returnable glass formats for health-positioned cold chains.

Cosmetics and personal care, though smaller in tonnage, emerge as the fastest-growing slot with a 4.68% CAGR between 2026 and 2031. Dubai’s position as a regional beauty-retail showcase fosters mini-series launches that value tactile closure systems and embossed logos achievable only in glass. Niche perfumers exploit laser-etched extra-white bottles and colored sprays produced in Ras Al Khaimah to elevate shelf impact, while e-commerce channels carry refill schemes that further legitimize heavier yet refillable formats. The UAE container glass industry also captures incremental orders from pharmaceutical health-and-beauty crossovers where therapeutic positioning demands inert, non-permeable containers. Collectively, these tendencies reinforce revenue diversity and insulate the supply chain from beverage-centric cyclicality.

By Color: Flint Retains Leadership while Amber Accelerates with Pharma Demand

Flint commanded 43.23% of the UAE container glass market share in 2025 because luxury spirits, cosmetics, and nutraceuticals require ultra-clear transparency to spotlight product color and purity. Extra-white variants produced in Ras Al Khaimah achieve low-iron clarity prized by perfume houses, helping sustain premium price realization and buttress factory margins.

Amber glass is forecast to outpace all colors at a 4.59% CAGR through 2031, shielded by Ras Al Khaimah’s expanding pharmaceutical cluster that specifies UV-blocking containers for photosensitive active ingredients. Rising nutraceutical intake and fortified syrup lines multiply bottle counts per production batch. Green glass lags because domestic beer and wine volumes are muted, yet bespoke olive oil exporters order limited runs to tap into Mediterranean aesthetic cues. Custom blues and blacks address niche cosmetics, keeping color diversity vibrant while keeping it small.

Geography Analysis

The first production-centered cluster lies in Ras Al Khaimah, where RAK Ghani Glass and Saverglass rely on Saqr Port to land low-iron sand and to ship finished bottles across the Gulf and East Africa. Both factories are located within RAKEZ, which offers 100% foreign ownership, zero import duties, and on-site customs clearance that compresses working capital cycles for exporters. RAKEZ reported 13,141 new company registrations in 2024, a 66% jump that broadened the local customer pool for glass bottles and jars. Julphar’s insulin plant, RAK Hospital’s clinical-trials hub, and a growing nutraceutical base amplify amber-glass pull as each new drug line needs validated primary packaging. The emirate’s furnace output also serves premium spirits bottlers in Oman and luxury fragrance houses in Bahrain, reinforcing Ras Al Khaimah’s role as the UAE’s manufacturing spine for container glass.

Dubai serves as the commercial and logistics hub of the UAE container glass market. Jebel Ali Free Zone centralizes bonded warehousing, shared decorating lines, and consolidated trucking, cutting cross-border lead times for Saudi and Omani deliveries. Beautyworld Middle East and Gulfood Manufacturing convene design teams and purchasing managers, accelerating the diffusion of European styles into Gulf brands and locking in flint-glass demand for limited-edition launches. Random Global’s automated recycling plant in Al Quoz processes 100 million bottles a year, yet only 10% re-enters container production, leaving cullet tight and forcing Dubai distributors to supplement with virgin raw material. Importantly, the city’s hospitality sector has begun installing in-house bottling lines that refill glass water bottles, raising urban-loop reuse rates and keeping empty bottles within metro boundaries for faster recollection.

Abu Dhabi rounds out the geographic picture by providing heavy-industry infrastructure, energy policy levers and new float-glass investments that could spill over into bottle production. Khalifa Industrial Zone houses the USD 163.35 million Emirates Float Glass expansion scheduled to start by 2028, a signal that capital and skills for high-temperature melting are welcome in the capital. Industrial electricity tariffs sit at 36.6 fils per kilowatt-hour during summer peaks, pressuring furnace margins but also motivating trials of oxy-fuel firing and photovoltaic offsets. Tadweer’s integrated waste-management network, aligned with the Cabinet’s national framework, is piloting color-sorted cullet streams for possible direct feed into container furnaces. Sharjah and the Northern Emirates contribute demand through retail chains and landfill-diversion mandates; Bee'ah’s 90% diversion milestone in 2023 positions the emirate to supply incremental cullet once sorting lines for glass scale. Together, the three leading emirates create a compact yet functionally diverse ecosystem that underpins the UAE container glass market size and export reach.

Competitive Landscape

Market share is concentrated in two furnace operators, yet competitive dynamics remain fluid because distributors, recyclers, and technology suppliers influence value capture along the chain. RAK Ghani Glass targets regulated life-science buyers by maintaining a Class 100,000 clean room and USP Type I and II validation, giving pharmaceutical firms confidence in leachables compliance. Saverglass emphasizes aesthetics, offering extra-white flint, heavy punts, and intricate embossing that allow perfume and spirits brands to justify double-digit retail price premiums at. Each player leans on Ras Al Khaimah’s free-zone tax incentives and Saqr Port’s bulk-sand import berths, but their customer mixes only partially overlap, which tempers direct price wars and keeps list prices stable.

Secondary competition comes from packaging distributors such as Global Packaging and Hotpack that aggregate overseas supply when local furnaces run at capacity or when clients need exotic colors in small lots. These traders maintain inventory in Jebel Ali and Sharjah to guarantee 48-hour regional delivery, a service level difficult for furnace makers to match for niche SKUs. Random Global, though not a bottle producer, wields influence by supplying color-sorted cullet, enabling glassmakers to raise recycled content and meet retailer sustainability scorecards. Technology vendors wield additional power; HORN Glass sells low-energy furnaces, and Sidel promotes PET systems that chip away at beverage-glass volume, prompting glass producers to invest in lighter-weight bottle designs to defend territory.

Strategic white space persists in high-value niches such as pharmaceutical vials, ampoules and color-sorted cullet systems. No UAE player currently melts borosilicate glass at scale, so hospitals import vials from Europe, presenting a USD-denominated gap that could entice new entrants with GMP credentials. Likewise, the absence of a national producer-funded recycling cooperative leaves each company to arrange its own take-back loops, inflating cash costs and limiting recycled-content claims. Should a third furnace operator enter, possibly via a joint venture between a global major and a local energy investor, the two-player equilibrium would shift, but high capital intensity and 24-7 energy tariffs still act as formidable barriers. For now, RAK Ghani and Saverglass command a combined share in the mid-60s percent range, sustaining a moderately concentrated UAE container glass market.

UAE Container Glass Industry Leaders

RAK Ghani Glass LLC

Saverglass LLC

Hotpack Packaging Industries LLC

Global Packaging FZC

Al Wara Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Dubai Investments began building a second float-glass line worth USD 163.35 million at Khalifa Industrial Zone, doubling capacity to 1,200 tonnes per day.

- October 2025: Hilton Abu Dhabi Yas Island opened an automated in-house water bottling plant with MYWATER, able to refill up to 2,500 glass bottles daily.

- July 2025: The UAE Ministry of Climate Change and Environment commenced a six-month Extended Producer Responsibility pilot in Dubai and Abu Dhabi.

- May 2025: RAKEZ signed a AED 1.1 billion park development to attract advanced-technology manufacturers and packaging converters.

- January 2024: SGD Pharma detailed a Corning joint venture for Velocity Vials, underscoring global supply-chain realignment around premium pharma glass.

UAE Container Glass Market Report Scope

The UAE Container Glass Market Report is Segmented by End-User (Beverages, Food, Cosmetics and Personal Care, Pharmaceuticals, Perfumery), Color (Green, Amber, Flint, Other Colors), and Geography (Dubai, Abu Dhabi, Ras Al Khaimah, Other Emirates). The Market Forecasts are Provided in Terms of Volume (Kilotons).

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large will UAE container-glass demand be by 2031?

The UAE container glass market is projected to reach 420.94 kilotons by 2031, growing at a 3.78% CAGR from 2026.

Which segment is expanding fastest?

Perfumery is forecast to register the quickest growth, advancing at a 4.74% CAGR through 2031, thanks to Dubai’s status as a regional fragrance hub.

Why does amber glass usage rise in the UAE?

Pharmaceutical production in Ras Al Khaimah specifies amber bottles for UV protection of photosensitive drugs, lifting amber volume at a 4.59% CAGR.

What policy changes favor glass over plastic?

A July 2025 Extended Producer Responsibility pilot in Dubai and Abu Dhabi shifts collection-cost liability to producers, narrowing the price gap between glass and single-use plastics.

Who are the main container-glass manufacturers in the UAE?

RAK Ghani Glass focuses on pharmaceutical bottles, while Saverglass supplies extra-white and colored flacons for luxury spirits and perfumes.

Page last updated on: