Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.68 Billion |

| Market Size (2026) | USD 6.87 Billion |

| Market Size (2031) | USD 8.43 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Paper Packaging Market Analysis by Mordor Intelligence

The Australia paper packaging market size is expected to grow from USD 6.58 billion in 2025 to USD 6.87 billion in 2026 and is forecast to reach USD 8.43 billion by 2031 at 4.18% CAGR over 2026-2031. E-commerce parcel traffic, statewide container-deposit schemes, and retailer circular-economy mandates are the primary forces reshaping business models as converters balance recycled-content targets with pharmaceutical-grade purity demands. Visy’s USD 117.3 million (AUD 175 million) Brisbane plant demonstrates how automation and digital printing are now essential for high-mix, short-lead-time orders, while the 2024 administration of Qenos removed a domestic polyethylene cost reference and accelerated paper substitution in flexible formats. Pulp import volatility and energy-price inflation continue to squeeze margins, yet fresh investments in aqueous and PVOH coatings are unlocking barrier performance that allows fibre to enter meal-kit insulation, aseptic beverages, and premium sauces. Forward-looking players are therefore rewiring supply chains around closed-loop recovery, serialization, and eco-modulation fees that reward low-impact substrates.

Key Report Takeaways

- By product type, corrugated boxes held 48.5% of the Australia paper packaging market share in 2025, whereas flexible paper packaging is projected to expand at a 5.01% CAGR through 2031.

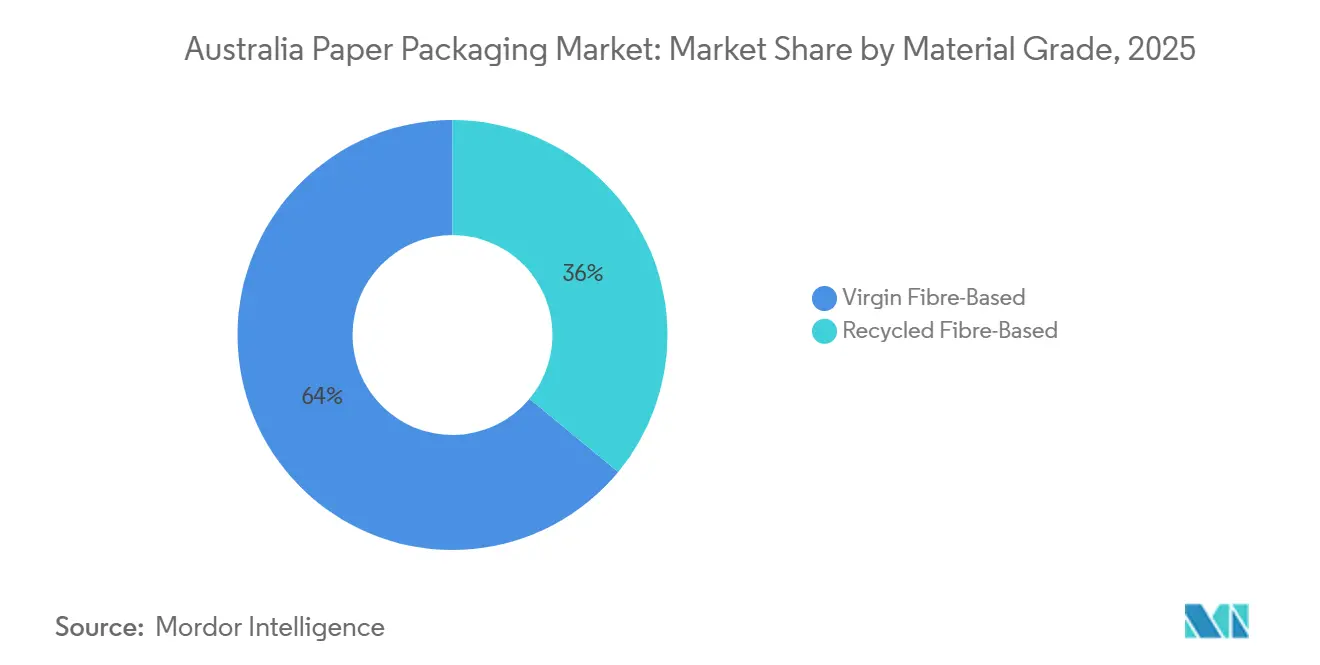

- By material grade, recycled fibre captured 64% of the 2025 Australia paper packaging market size, while virgin fibre is forecast to post the fastest growth at a 4.93% CAGR on rising pharmaceutical and premium-beverage demand.

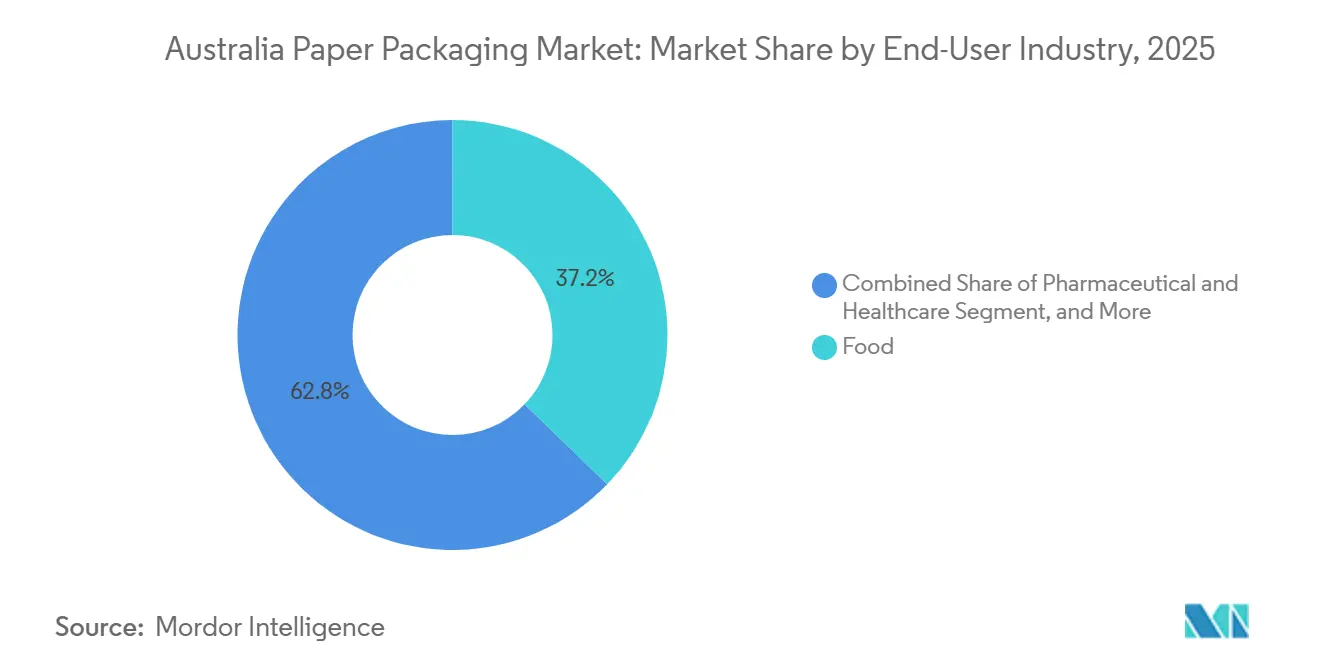

- By end-user industry, food applications accounted for 37.2% of the Australia paper packaging market share in 2025, but pharmaceutical and healthcare end uses are expected to register the highest 5.22% CAGR to 2031.

- By packaging format, secondary formats represented 46.8% of the 2025 Australia paper packaging market size, yet primary packaging is poised to advance at a 4.83% CAGR on carton serialization and fibre bottles.

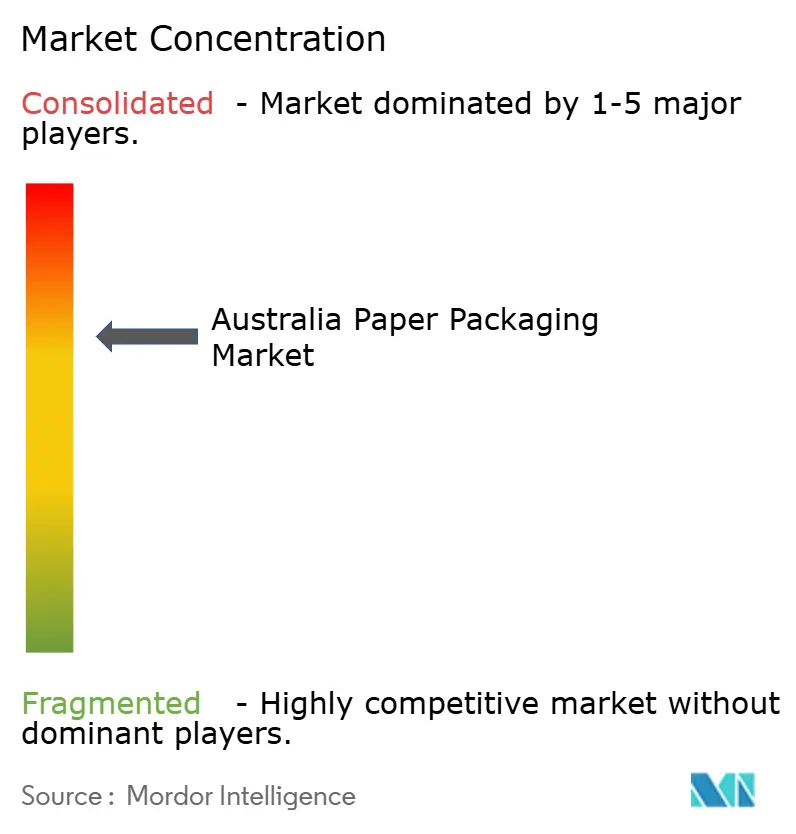

- By company share, Visy, Amcor, Orora, and Pratt Industries together controlled just over half of 2025 revenue, indicating a moderately consolidated structure that still leaves room for niche innovators.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Preference for Sustainable and Recyclable Packaging | +0.90% | National, with stronger uptake in urban centers (Sydney, Melbourne, Brisbane) | Medium term (2-4 years) |

| Booming Australian E-commerce Fulfilment Volumes | +1.10% | National, concentrated in New South Wales and Victoria distribution hubs | Short term (≤ 2 years) |

| Government Single-Use Plastic Bans Fuelling Paper Substitution | +0.80% | National, state-level implementation (New South Wales, Queensland, Victoria lead) | Short term (≤ 2 years) |

| Corporate Circular-Economy Targets Accelerating Fibre-Based Innovation | +0.60% | National, multinational FMCG and retail chains | Medium term (2-4 years) |

| Rapid Growth of Meal-Kit and Food-Delivery Services Increasing Demand for Insulated Paper Packs | +0.40% | National, urban concentration (Sydney, Melbourne, Brisbane) | Short term (≤ 2 years) |

| Retail Private-Label Expansion Requiring Cost-Efficient Shelf-Ready Paper Formats | +0.30% | National, major retailers (Woolworths, Coles, Aldi) | Medium term (2-4 years) |

| State-Level Container-Deposit Schemes Driving Demand for High-Barrier Paper Bottles | +0.20% | National, Tasmania completion mid-2025 | Long term (≥ 4 years) |

| Australia's Remote-Logistics Challenges Increasing Demand for Lightweight Cushioned Corrugated | +0.30% | National, pronounced in Western Australia, Northern Territory, regional Queensland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Sustainable and Recyclable Packaging

Household purchasing data show that packaging displaying the Australasian Recycling Label covered 3.69 million tonnes of product in 2024, with paper and paperboard accounting for more than half of that weight and achieving a 66% recovery rate.[1]Australasian Packaging Covenant Organisation, “APCO Strategic Plan 2030,” apco.org.au Major retailers now leverage nearly universal private-label penetration to dictate packaging specifications, illustrated by Woolworths’ USD 1.34 billion (AUD 2.0-2.2 billion) FY2025 capital program that prioritizes shelf-ready corrugated able to keep produce rejection below 2%. Yet 1.3 million tonnes of fibre still entered landfill, exposing infrastructure gaps that brand owners increasingly view as reputational risk. The result is a pull effect on converters to lift post-consumer content while maintaining food-contact compliance, driving demand for cleaner material streams and certified virgin pulp.

Booming Australian E-commerce Fulfilment Volumes

Parcel volumes continued double-digit expansion through 2025, prompting converters to re-engineer box designs for automated sortation. Visy’s Brisbane plant can output 1 million recycled-content cartons daily, each printable in real time to reflect SKU-level personalization.[2]Visy Industries, “Investment Updates,” visy.com.au The shift is concentrating growth among large, automated sites, while smaller firms are pushed to niche runs or regional accounts. Remote logistics in Western Australia and the Northern Territory further favour micro-flute constructions that lower freight costs per cubic meter, a specification that was rare a decade ago but is now mainstream for national e-commerce accounts.

Government Single-Use Plastic Bans Fuelling Paper Substitution

State regulations banning polystyrene food ware and lightweight bags are converging on paper as the default alternative. Victoria’s CDS Vic processed more than 1 billion containers in its first year, and Queensland’s 2023 decision to include wine and spirits was the first in Australia to apply deposits to premium beverages. Tasmania’s 2025 rollout completes nationwide container-deposit coverage, forcing mills to improve aqueous coatings so cartons remain kerbside-recyclable without polyethylene liners. Early data reveal that liquid paperboard redemption trails glass, highlighting both an opportunity for high-barrier innovation and a need for clearer consumer messaging.

Corporate Circular-Economy Targets Accelerating Fibre-Based Innovation

Global brand pledges for net-zero and plastic reduction translate into procurement standards that reward fibre substrates. Tetra Pak’s 80%-paper aseptic design cuts carbon footprint one-third relative to foil laminates, strengthening the business case for cellulose-based barrier research. Local trials, such as MasterFoods’ paper sauce sachet with 58% less plastic, prove that format migration can reach even high-viscosity condiments. The Australian Packaging Covenant Organisation’s eco-modulation fees reinforce the economic logic by penalizing hard-to-recycle configurations, giving converters a monetary rationale for CAPEX in dispersion-coating and de-inking lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Domestic Pulp and Recovered Paper Prices | -0.70% | National, import-dependent mills in New South Wales, Victoria | Short term (≤ 2 years) |

| Competition from Emerging Bio-Based Plastics | -0.30% | National, food-service and FMCG segments | Medium term (2-4 years) |

| Limited Australian Recycling Infrastructure Capacity | -0.50% | National, pronounced in South Australia, Tasmania, Northern Territory | Medium term (2-4 years) |

| Rising Energy Costs Squeezing Mill Margins | -0.40% | National, energy-intensive mills in Victoria, New South Wales | Short term (≤ 2 years) |

| Chronic Shortage of Skilled Maintenance Staff Limiting Mill Uptime | -0.20% | National, regional mills outside capital cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Domestic Pulp and Recovered Paper Prices

Australian pulp imports dropped 30.2% year-ended February 2024, yet average landed cost rebounded to USD 670 per tonne after strikes in Finland and Chile constrained global supply, exposing mills to currency and commodity risk simultaneously.[3]Australian Bureau of Statistics, “International Trade in Goods and Services,” abs.gov.au Recovered-paper swings are sharper: Victoria’s mixed-paper price collapse in early 2023 reversed only when export-license fees of USD 12,790 per new permit (AUD 19,090) took effect in July 2024. Mills thus face unpredictable input costs that complicate long-term supply contracts and scramble CAPEX planning when margins must absorb de-inking or landfill disposal for contaminated loads.

Limited Australian Recycling Infrastructure Capacity

Export bans on mixed paper diverted volumes into domestic channels already running near capacity, with 1.3 million tonnes of fibre still landfilled in 2024 despite a 66% recovery rate. Visy’s USD 28.5 million (AUD 42.5 million) Coolaroo upgrade added 180,000-tonne pulping capacity in Victoria, yet Tasmania, the Northern Territory, and regional Western Australia remain reliant on long-haul freight to reach processing nodes. Mandatory recycled-content targets of 60% in Year 1 and 75% by 2040 will tighten material supply further, pressuring states to co-invest in sortation and de-inking or risk shortfalls that inflate costs and erode competitiveness.[4]Department of Climate Change Energy the Environment and Water, “National Packaging Targets Consultation,” dcceew.gov.au

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Grade: Virgin Fibre Captures Premium Growth

Virgin pulp substrates represented the minority share in 2025 yet are forecast to grow 4.93% CAGR through 2031 as pharmaceutical and premium-beverage brands demand certified-clean inputs to meet traceability rules set by the Therapeutic Goods Administration. The Australia paper packaging market size for virgin fibre formats is therefore expanding even as eco-modulation fees reward post-consumer content. In response, integrated players are blending higher-quality recovered streams with imported kraft to balance purity and cost.

Recycled fibre still accounted for 64% of 2025 revenue thanks to mature corrugated demand and retailer mandates, but contamination and odor concerns limit use in unit-dose healthcare packaging. Tetra Pak’s foil-free aseptic carton relies on virgin kraft for coating adhesion, while Zipform’s 95%-fibre bottle likewise specifies virgin to achieve burst strength needed for carbonated drinks. Unless domestic recovery infrastructure can lift purity rates, converters will continue to rely on blended solutions that temper virgin growth without displacing it outright.

By Product Type: Flexible Paper Surges on Barrier Wins

Corrugated remained the revenue anchor at 48.5% of the 2025 Australia paper packaging market share, yet flexible formats are projected to expand at 5.01% CAGR, the fastest among product types. Breakthroughs in dispersion-coated liners enabled HelloFresh’s kerbside-recyclable insulation pouch and BioPak’s PFAS-free hot-cup barrier, converting applications once locked into polyethylene laminates.

Folding cartons benefit from serialization mandates but grow more slowly, while liquid cartons face redemption-rate headwinds that spur technical refinements such as 2-4 g m-² aqueous coatings. Meanwhile, e-commerce shifts are steering corrugated design toward lighter grammages and micro-flute profiles that reduce freight cost per delivered item. The net result is a portfolio diversification in which converters balance high-volume board with high-margin barrier pouches.

By End-User Industry: Healthcare Leads Growth Curve

Food maintained a 37.2% revenue share in 2025, yet pharmaceuticals are poised for 5.22% CAGR on the back of unit-level serialization and tamper-evident mandates. The Australia paper packaging market size for healthcare cartons will therefore rise faster than any other end use, creating demand spikes for low-migration virgin substrates and digital print capability for variable data.

Premium spirits, personal care, and household items are also tilting toward paper as retailers enforce single-material shelf-ready guidelines. Coles’ adoption of VektroPack and Woolworths’ multi-year CAPEX on fresh-produce handling underscore how private-label clout translates into supplier compliance, pushing converters to tailor barrier features for moisture or oil resistance while hitting recycled-content thresholds.

By Packaging Format: Primary Rises in a Secondary World

Secondary packaging commanded 46.8% of 2025 revenue, reflecting its dominance in retail and e-commerce logistics. Yet primary formats are forecast to grow 4.83% CAGR as fibre bottles, serialized folding cartons, and kerbside-recyclable pouches displace plastic. Visy’s Brisbane site, geared for one-piece flow and rapid changeover, exemplifies how high-output corrugated remains indispensable even as unit-dose innovations capture headlines.

Tertiary transit solutions expand more modestly given the rise of reusable plastic crates in closed loops. However, demand spikes for pallet-grade sheets still surface in remote mining and agriculture where wood crate alternatives fail cost or sustainability screens. Overall, converters now stage portfolios across three formats, allocating capital to whichever captures the next regulatory or retailer push.

Geography Analysis

New South Wales and Victoria together remained the demand core in 2025, absorbing e-commerce parcels and hosting the densest FMCG hubs. Visy’s Brisbane megasite nonetheless elevates Queensland’s role as a production springboard for eastern-seaboard fulfilment, signalling a northward shift in capacity deployment. South Australia’s 76.4% container-return rate showcases how early policy fosters stable feedstock, while the ACT’s 22% redemption for liquid paperboard flags that multilayer formats still confuse consumers, curtailing fiber recovery.

Tasmania’s mid-2025 container-deposit launch made Australia the first continent with 100% CDS coverage, anchoring demand for high-barrier cartons designed for deposit loops. Western Australia and the Northern Territory continue to wrestle with freight premiums that favour lower-basis-weight corrugated, encouraging mills to adopt micro-flute technology that trims shipping mass without sacrificing compression strength.

Infrastructure gaps remain stark: Victoria gained 180,000 tonnes of new pulping capacity from Visy in 2023, yet Tasmania and northern regions still haul recovered fiber long distances, adding cost and carbon. If mandatory 75% recycled-content rules pass by 2027, states lacking sortation will face material deficits that could inflate converter costs and erode competitiveness until new plants come online.

Competitive Landscape

The market is moderately consolidated, with the top four players holding a bit more than half of 2025 revenue. Visy’s USD 1.34 billion (AUD 2 billion) decade program spans recycling, board, and glass, positioning it to supply closed-loop fiber and capitalize on e-commerce expansion. Amcor’s USD 13 billion Berry Global deal adds rigid plastics globally but leaves Australian fiber films largely untouched, offering little direct challenge to domestic board specialists. Orora’s USD 87.1 million (AUD 130 million) cans expansion underscores a pivot into aluminium, ceding some corrugated share to integrated recyclers and mid-tier converters.

Pratt Industries continues to import know-how from its U.S. plants, focusing on 100% recycled linerboard to meet retailer mandates. Niche innovators such as Zipform and BioPak pursue barrier breakthroughs the former with a 95%-paper bottle and the latter with PHA-lined cups certified for home composting, but scale remains contingent on brand adoption and consumer perception shifts.

The Smurfit Kappa and WestRock merger will raise the bar on global cost efficiency, pushing Australian converters to emphasize short-run agility, high-graphic print, and localized recovery networks to defend margins.

Australia Paper Packaging Industry Leaders

Visy Industries Holdings Pty Ltd

Amcor plc

Orora Limited

Abbe Corrugated Pty Ltd

Pro-Pac Packaging Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Norske Skog completed the sale of Boyer mill to David Marriner for AUD 27 million (USD 17.07 million), transferring 310 employees and 285,000 tonnes per annum of capacity.

- March 2025: Amcor launched paper-based dry beverage packaging, expanding fiber alternatives in drink applications.

- January 2025: Smurfit WestRock introduced paper pallet wrap products after reporting USD 7.5 billion Q4 2024 net sales.

- January 2025: Amcor achieved Dow Jones Sustainability Index recognition for environmental leadership.

Australia Paper Packaging Market Report Scope

The Australia Paper Packaging Market Report is Segmented by Material Grade (Virgin Fibre-Based, Recycled Fibre-Based), Product Type (Folding Cartons, Corrugated Boxes, Flexible Paper Packaging, Liquid Cartons), End-User Industry (Beverage, Food, Pharmaceutical and Healthcare, Personal Care and Household Care, Other End-User Industries), and Packaging Format (Primary Packaging, Secondary Packaging, Tertiary/Transit Packaging). The Market Forecasts are Provided in Terms of Value (USD).

By Material Grade

| Virgin Fibre-Based |

| Recycled Fibre-Based |

By Product Type

| Folding Cartons |

| Corrugated Boxes |

| Flexible Paper Packaging |

| Liquid Cartons |

By End-User Industry

| Beverage |

| Food |

| Pharmaceutical and Healthcare |

| Personal Care and Household Care |

| Other End-User Industries |

By Packaging Format

| Primary Packaging |

| Secondary Packaging |

| Tertiary / Transit Packaging |

| By Material Grade | Virgin Fibre-Based |

| Recycled Fibre-Based | |

| By Product Type | Folding Cartons |

| Corrugated Boxes | |

| Flexible Paper Packaging | |

| Liquid Cartons | |

| By End-User Industry | Beverage |

| Food | |

| Pharmaceutical and Healthcare | |

| Personal Care and Household Care | |

| Other End-User Industries | |

| By Packaging Format | Primary Packaging |

| Secondary Packaging | |

| Tertiary / Transit Packaging |

Key Questions Answered in the Report

What is the forecast value of the Australia paper packaging market by 2031?

It is projected to reach USD 8.43 billion, growing at a 4.18% CAGR between 2026 and 2031.

Which segment will record the fastest growth through 2031?

Pharmaceutical and healthcare applications are expected to expand at a 5.22% CAGR thanks to serialization rules.

How large is the corrugated box share in 2025?

Corrugated boxes commanded 48.5% of total revenue in 2025.

Why are flexible paper formats gaining traction?

Barrier-coating breakthroughs now allow fibre pouches and insulation to replace polyethylene laminates without sacrificing performance.

Which company is investing most heavily in Australian recycling capacity?

Visy is leading with a USD 1.34 billion decade-long program that spans paper, board, and glass recovery assets.

What is the main risk to growth for converters?

Volatile pulp and recovered-paper prices create margin uncertainty that can delay capital projects.

Page last updated on: