Bambara Beans Market Size and Share

Bambara Beans Market Analysis by Mordor Intelligence

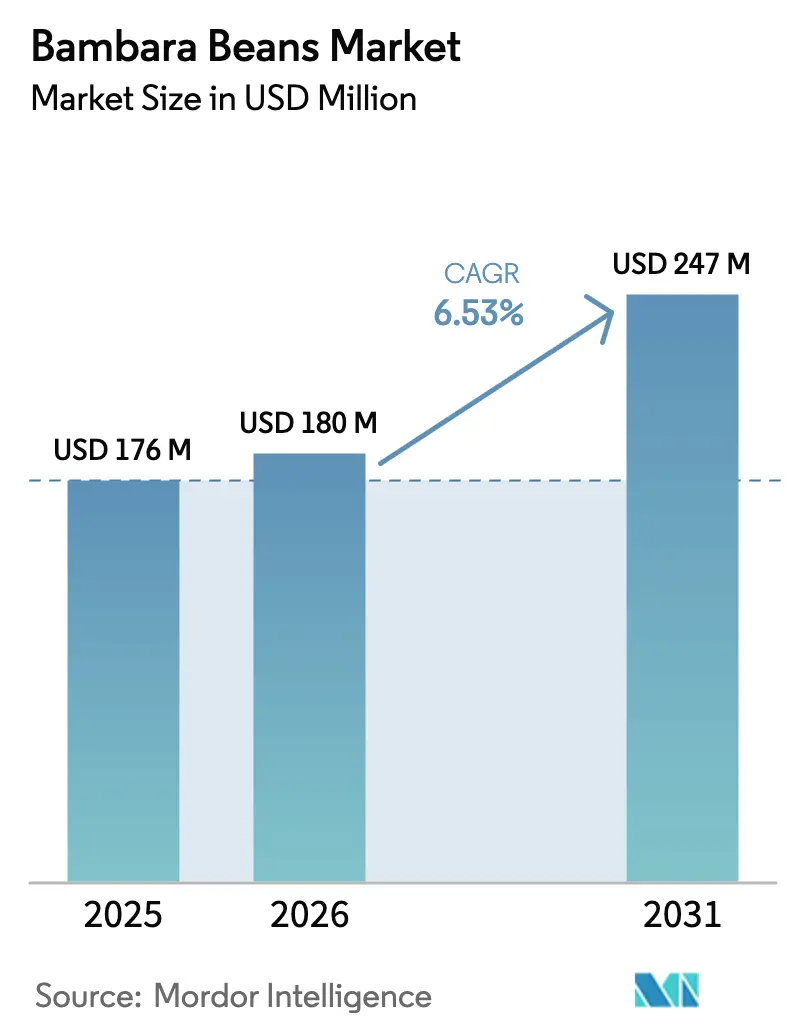

The Bambara beans market size is projected to grow from USD 176.0 million in 2025 to USD 180.0 million in 2026 and is forecast to reach USD 247.0 billion by 2031 at a 6.53% CAGR over 2026-2031, underscoring a decisive pivot in regional protein sourcing. Accelerated investment in drought-tolerant crop genetics, growing demand for clean-label plant proteins, and fresh industrial starch applications are steering steady value growth. Policy incentives that prioritize resilient agriculture in Africa and the Asia-Pacific, coupled with research grants for orphan crops, are expanding commercial cultivation. Processing innovations that shorten cooking time and improve protein extraction efficiency are widening food and industrial use cases, while bioplastic manufacturers trial Bambara starch for high-viscosity films. Market opportunities, however, remain tempered by energy‑intensive cooking profiles and regulatory gaps that elevate transaction costs. The market is moderately consolidated, comprising a mix of established players and smaller participants, which creates scope for further consolidation, particularly as processing technologies advance to address the crop’s inherent cooking challenges.

Key Report Takeaways

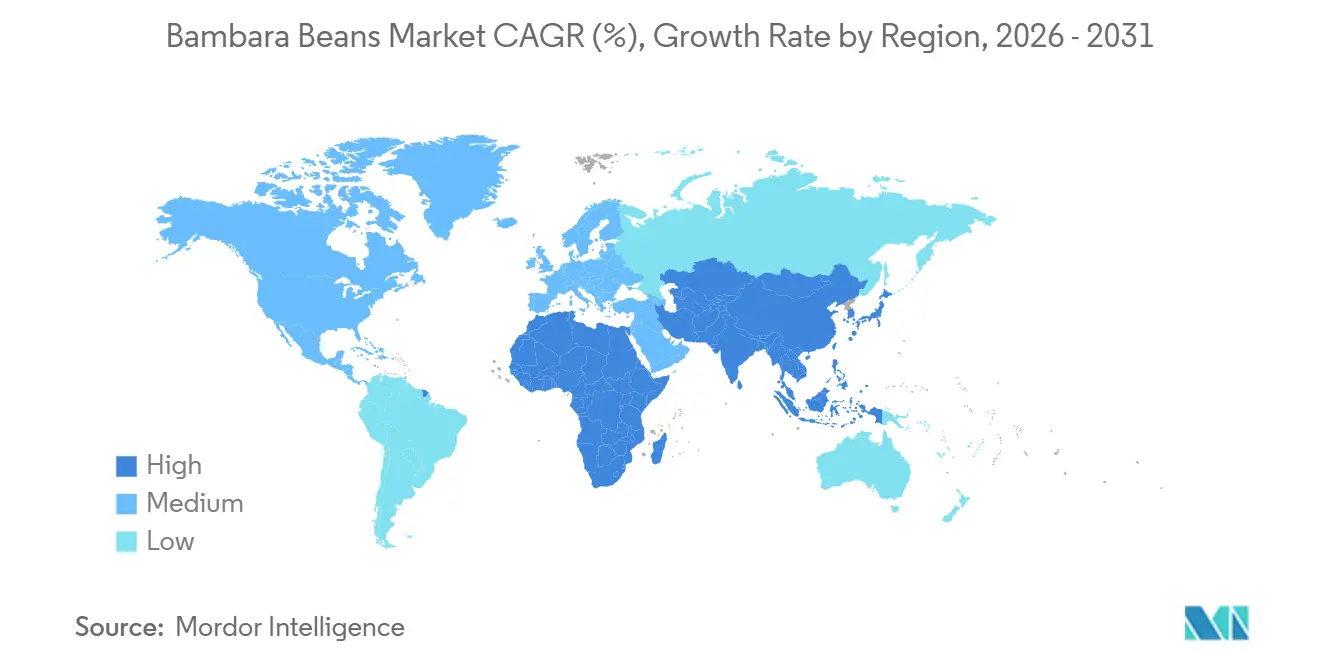

- By geography, Africa led the Bambara beans market with 63% market share in 2025, while Asia-Pacific recorded the highest projected CAGR of 11.7% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bambara Beans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-resilient, drought-tolerant crop genetics | +1.2% | Sub-Saharan Africa, South Asia, Southern Europe | Long term (≥ 4 years) |

| Rising demand for plant-based protein ingredients | +1.0% | Asia-Pacific urban centers, Europe, North America | Medium term (2-4 years) |

| Expanded R&D grants for climate-smart orphan crops | +0.9% | Global, concentrated in Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Emerging industrial starch uses (bioplastics) | +0.7% | Europe, North America, East Asia | Long term (≥ 4 years) |

| Premium positioning in gluten-free pulse category | +0.8% | Europe, North America, Australia, urban Asia | Medium term (2-4 years) |

| Off-season production premiums in Southern Africa | +0.6% | Zimbabwe, Botswana, Zambia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climate-Resilient, Drought-Tolerant Crop Genetics

Bambara beans thrive on as little as 300 mm annual rainfall, sharply contrasting with legumes that require about 550 mm, providing a resilient option for producers in water-stressed areas[1]Source: University of Nottingham Malaysia, “Bambara Groundnut: An Exemplar Underutilised Legume for Resilience Under Climate Change,” springer.com. Climate models published in 2024 forecast an expansion of suitable cultivation zones across the Sahel and South Asia as mean temperatures rise by 1.5 to 2.0 degrees Celsius by 2030. Mapping of 111 drought-associated proteins is guiding breeders toward high-performing lines that hold yield under prolonged stress. National research agencies in Nigeria, South Africa, and India now integrate Bambara beans in climate adaptation portfolios, aligning with USDA findings that endorse resurrection-type stress responses for pulse crops[2]Source: Escuela Superior Politecnica del Litoral, “The Superpower of Beans: Resilient, Nutritious and Ready for Climate Change,” phys.org. As atmospheric models predict wider arid belts, public programs channel subsidy support to encourage farmer uptake, strengthening the long-range outlook for the Bambara beans market.

Rising Demand for Plant-Based Protein Ingredients

Bambara beans contain all essential amino acids, including methionine levels that exceed those in common pulses, allowing formulators to meet complete-protein targets without amino acid fortification. Protein isolates and flour from bambara contain 18 to 24 percent protein and offer lysine and methionine levels attractive to non-soy formulators. Food-tech startups in Europe launched bambara-based bakery and meat analog products in 2024, citing functional benefits such as water-holding capacity and emulsification. The European Union’s protein diversification initiative earmarked EUR 38 million (USD 41 million) to scale under-utilized legumes and is drawing venture capital toward extraction technologies in 2025. These functional benefits accelerate ingredient adoption in sports nutrition, healthy snacks, and fortified beverages.

Expanded R&D Grants for Climate-Smart Orphan Crops

Research and development grants are crucial in transforming Bambara beans from a neglected "orphan crop" into a high-value, climate-resilient commodity. Initiatives such as the Vision for Adapted Crops and Soils (VACS) and the UK-CGIAR AgVACS project have funded genomic research to stabilize yields and enhance disease resistance. This support has reduced investment risks for the private sector, enabling the development of Target Product Profiles that align with the plant-based protein industry's needs and with farmer production. CGIAR’s 2024 strategy identifies orphan crops as key to resilient food systems, unlocking financing for phenotyping and genomic selection. CRISPR-Cas9 protocols have reduced Bambara beans breeding cycles to 4 years, accelerating the release of stress-tolerant varieties. Sustained grant funding ensures a steady pipeline of improved cultivars, supporting long-term market growth.

Emerging Industrial Starch Uses (Bioplastics)

Bambara starch carries double the viscosity of corn starch and forms strong, transparent films that biodegrade within 90 days, meeting European single-use plastic mandates. Polymer engineers exploit this viscosity to create high-barrier pouches for dry foods, opening premium markets where starch prices exceed USD 1,100 per metric ton [3]Source: Kansas State University, “Legume Proteins in Food Products,” mdpi.com. Integrated biorefineries can extract protein concentrates from residual press-cakes, delivering dual revenue streams that strengthen grower margins. European bioplastic firms completed pilot extractions in 2025, while processors in India and Thailand explore retrofitting cassava lines during off-peak seasons. Demand from eco-conscious packaging companies creates a stable offtake channel, allowing processors to hedge food-grade volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hard-to-cook phenomenon raises energy costs | -1.1% | Sub-Saharan Africa and South Asia | Medium term (2-4 years) |

| Weak formal seed systems and cultivar pipelines | -0.9% | Sub-Saharan Africa and emerging Asian zones | Long term (≥ 4 years) |

| Mycotoxin risk in subterranean pods limits exports | -0.7% | West Africa exports to Europe, North America, Asia | Medium term (2-4 years) |

| Low Commercialization & Limited Awareness | -0.5% | Global trade corridors, particularly affecting emerging export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hard-to-Cook Phenomenon Raises Energy Costs

Prolonged storage at 35 °C and 80% humidity can extend Bambara cooking times beyond two hours, curbing appeal among time-pressed consumers. Urban processors face higher steam and electricity bills, undermining margins versus quick-cooking pulses. Alkaline pre-soaks and fermentative treatments cut cooking time by half but require stainless reactors, diverting capital that smallholdings seldom possess[4]Source: Journal of the Science of Food and Agriculture, “Hard-to-Cook Phenomenon in Bambara Groundnut,” wiley.com. Calcium chloride pre-soaking and high-pressure processing mitigate the issue but add 15 to 20% to unit costs, restricting large-scale adoption. Ready-to-eat pouches and dehydrated flakes partially resolve convenience barriers yet shift the value chain toward larger, integrated firms, consolidating the Bambara beans market.

Weak Formal Seed Systems and Cultivar Pipelines

Farmer-saved seed accounts for more than 98% of planted area, leading to genetic drift and slow gains in yield or disease resistance. Inadequate seed systems constrain market expansion by limiting access to improved varieties and maintaining yield gaps that reduce commercial viability compared to established pulse crops. Private breeders hesitate to invest without enforceable intellectual property rights, leaving public entities to shoulder the burden of varietal development. Temperature-controlled seed hubs remain scarce, resulting in viability losses during transit. Yield stagnation dims rural income prospects, slowing acreage expansion despite favorable farm-gate pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Africa accounted for 63% of the Bambara beans market share in 2025, driven by Nigeria, which produces nearly 100,000 metric tons annually, serving as both a food-security buffer and a nitrogen-fixing rotation crop for millet and sorghum. Burkina Faso yields 60,000 to 100,000 metric tons from Sahelian fields, though mechanization gaps limit output to 600 to 800 kilograms per hectare, compared with a potential 1,500 to 2,000 kilograms under optimal practices. South African laboratories that spearhead genetic enhancement programs support the market. This region has centuries of agronomic knowledge, and the crop secures nutrition in lean seasons. The African Continental Free Trade Area's implementation creates opportunities for intra-regional trade expansion, though infrastructure constraints and challenges with quality standardization limit immediate benefits.

Asia-Pacific is climbing at an 11.7% CAGR through 2031, supported by India’s BAMLINK field trials in Rajasthan, Maharashtra, and Karnataka, which aim to reduce dependence on imported pulses, which exceeded 2 million metric tons in 2024. Malaysia’s policy focuses on climate-proof crops, and Singaporean buyers import from Africa for ethnic retail and plant-based manufacturing, while Vietnamese and Thai processors test bambara for gluten-free noodles and snacks. Government support for alternative protein development in countries such as India creates a policy environment favorable to Bambara beans commercialization, particularly for processed food applications. The region’s progression depends on certified seed suited to local photoperiods until then, supply chains face phytosanitary risk and inconsistent quality.

Demand from the African diaspora sustains specialty channels in France, Germany, and the Netherlands, with Rotterdam serving as a re-export hub. Horizon Europe subsidies promote legume diversification, but field trials in Southern France and Spain have yet to achieve consistent commercial yields outside protected cultivation. North America, the Middle East, and South America remain niche markets, driven by health-food segments and diaspora demand, contributing less to global volume growth than Asia-Pacific. The Middle East and North Africa region presents emerging opportunities, driven by food security needs and climate adaptation efforts. Turkey’s role as a regional processing hub for pulses provides infrastructure advantages, while Saudi Arabia’s Vision 2030 agricultural initiatives include investments in drought-tolerant crops. However, consumer acceptance and processing infrastructure development are essential for significant market penetration in these emerging markets.

Competitive Landscape

The bambara beans market remains highly fragmented, with smallholders accounting for major percent of global production. Global commodity houses such as Louis Dreyfus Company and Export Trading Group (ETG Commodities) retain small exposure through diversified pulse desks, supplying specialty food processors on demand. Recent capex by CHS, which processed 68 million pounds of edible beans in 2024, signals broader industry intent to diversify plant protein portfolios. Absent scale leaders, acquisition opportunities abound for firms willing to invest in processing technology that can tame hard-to-cook barriers.

Technological capability is emerging as the chief competitive differentiator. Processors deploying enzymatic tenderization units report 35% shorter cook times and higher throughout, enabling them to capture premium contracts from convenience-meal brands. Cold-chain integrators control aflatoxin by maintaining pod moisture below 12%, securing European Union clearances. Supply-chain digitization from blockchain traceability to mobile agronomy apps strengthens producer loyalty, giving innovators early-mover advantages in an otherwise commoditized pulse landscape.

Sustainability certifications add reputational weight. Buyers increasingly demand proof of regenerative farming practices and fair-trade premiums, pushing exporters to formalize farmer networks. Companies that bundle agronomic advisory services with input financing strengthen their procurement pipelines, paving the way for potential consolidation. Integrated players hold a significant share of the total volume. This may lead to merger controls and antitrust reviews, potentially impacting the competitive landscape.

Recent Industry Developments

- January 2025: Researchers in Ghana, in collaboration with Grow Further, have developed and submitted four new Bambara beans varieties for approval by the National Varietal Release Committee. These high-yield, fast-maturing, protein-rich varieties aim to improve food security and incomes for smallholder farmers, promoting the commercialization of this orphan crop.

- March 2024: The Zero Hunger Coalition is promoting the Bambara beans in Madagascar as a resilience crop to combat food insecurity in drought-prone areas. The initiative trains smallholder farmers in sustainable cultivation and provides high-quality seeds to boost yields. By integrating this nutrient-rich legume into local food systems, the project aims to improve nutrition and economic stability through diversified crop production.

- February 2024: WhatIF Foods introduced BAMnut Milk in Ghana, made entirely from locally sourced Bambara beans, as a sustainable dairy alternative. This launch aims to develop a value chain that supports smallholder farmers while providing consumers with a nutrient-rich option.

Global Bambara Beans Market Report Scope

The Bambara Beans Market Report is Segmented by Geography (North America, Europe, Asia-Pacific, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, Regulatory Framework, List of Key Players, Logistics and Infrastructure, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Europe | France | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Netherlands | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Asia-Pacific | Malaysia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Middle East | Turkey | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Africa | Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Burkina Faso | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Europe | France | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Netherlands | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Asia-Pacific | Malaysia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Middle East | Turkey | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Africa | Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Burkina Faso | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the current Bambara beans market size?

The bambara beans market is valued at USD 180 million in 2026.

How fast is the Bambara beans market growing?

The market is projected to expand at a 6.53% CAGR between 2026 and 2031.

Which region holds the largest Bambara beans market share?

Africa leads with 63% market share, anchored by Nigeria and South Africa.

Why are Bambara beans gaining attention in the plant-based protein space?

They offer a complete amino acid profile and superior emulsification, making them attractive for protein isolates and clean-label products.

What challenges limit wider adoption of Bambara beans?

Extended cooking times, weak formal seed systems and mycotoxin risks are key restraints.

Which new industrial application could boost demand for Bambara beans?

High-viscosity Bambara starch is being tested for biodegradable bioplastic films, opening a growing packaging market.

Page last updated on: