Cowpeas Market Size and Share

Cowpeas Market Analysis by Mordor Intelligence

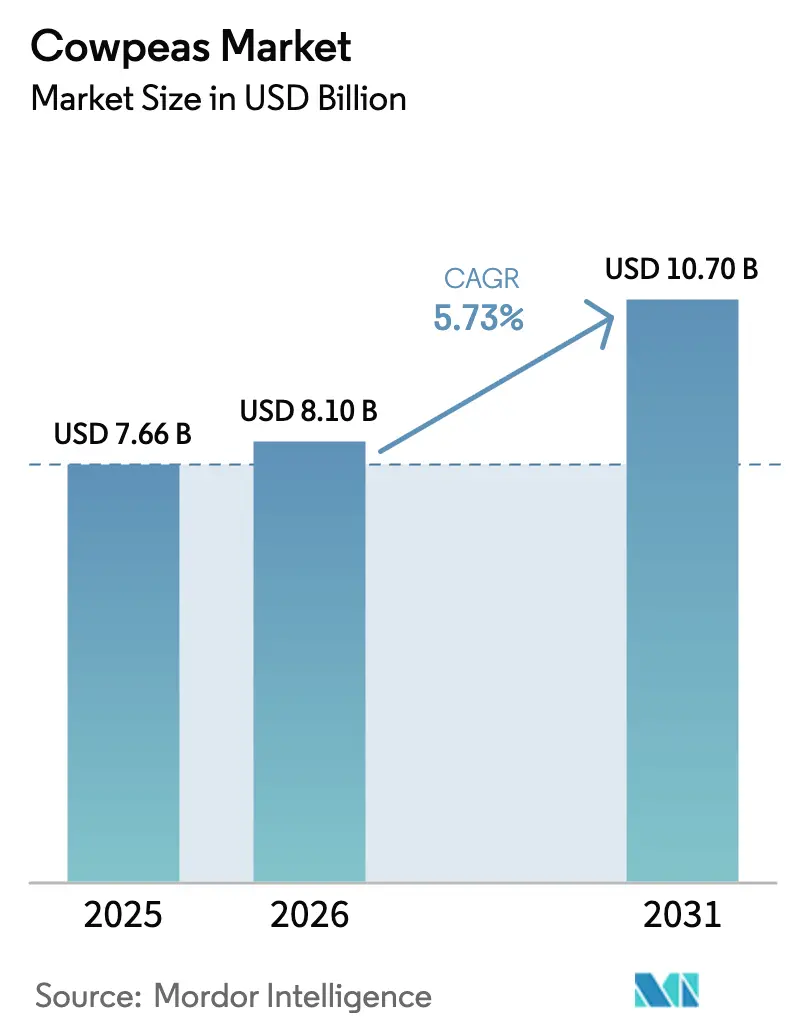

The cowpeas market was valued at USD 7.66 billion in 2025 and is estimated to grow from USD 8.10 billion in 2026 to reach USD 10.70 billion by 2031, advancing at a 5.73% CAGR during the forecast period (2026-2031). The shift toward pulse-based diets, tariff-free intra-African trade, and rising demand for ruminant forage in China keep global consumption on a steady climb. Africa accounts for a significant share of global consumption, followed by the Asia-Pacific region. This highlights the geographic dynamic, with supply concentrated in West Africa and demand driven by South and East Asia. The dual-market structure facilitates resilient trade flows, supported by advancements in storage infrastructure and regional processing capacity, which improve supply efficiency and minimize post-harvest losses. While staple food retail continues to dominate, the adoption of plant-based meat applications is growing, with manufacturers increasingly substituting soy with cowpea protein. Additionally, blockchain traceability, carbon-credit income, and climate-smart seeds are driving the emergence of new revenue streams. However, pest outbreaks and currency volatility pose challenges, limiting short-term price gains.

Key Report Takeaways

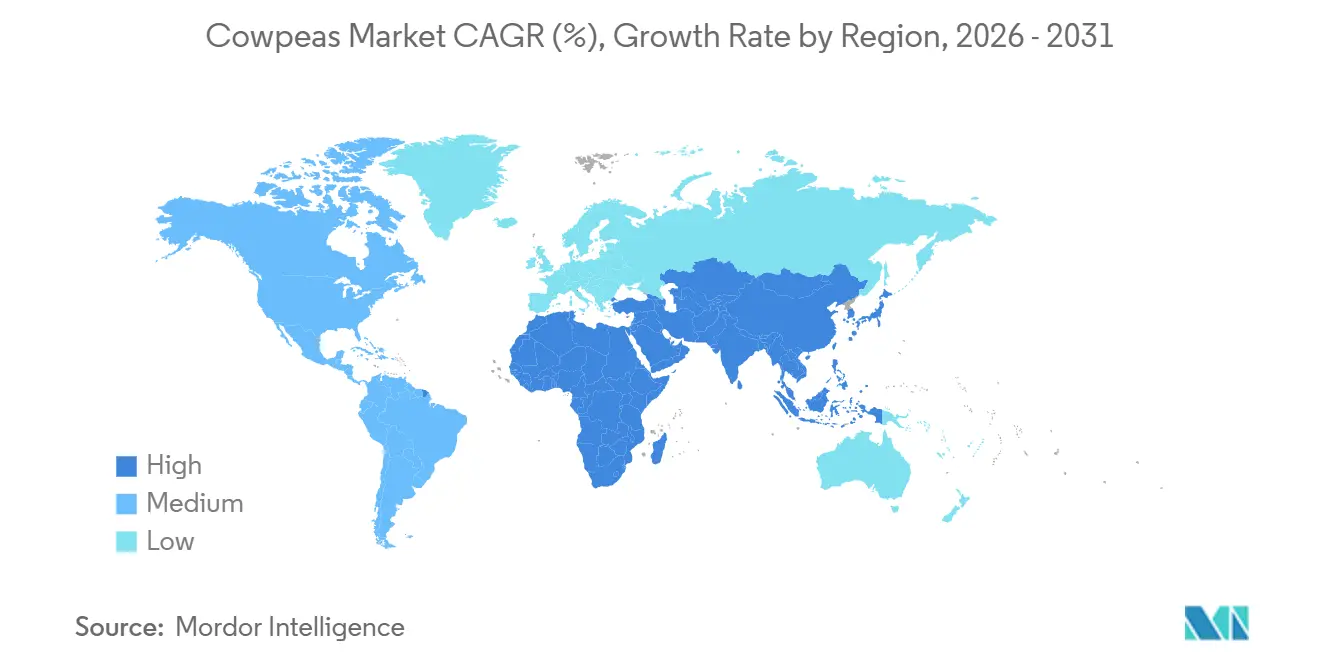

- By geography, Africa held 38.7% of the cowpeas market share in 2025, while Asia-Pacific is on track to log the fastest 6.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cowpeas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to pulse-based proteins among flexitarian consumers | +1.20% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Recovery of Sahelian export corridors after African Continental Free Trade Area (AfCFTA) tariff cuts | +0.90% | Nigeria, Niger, Burkina Faso, Mali, spill-over to Middle East and Asia-Pacific | Short term (≤ 2 years) |

| Chinese feed compounders blending cowpea haulms in ruminant rations | +0.70% | China, India, and emerging Southeast Asia | Medium term (2-4 years) |

| Climate-smart seed subsidies in Economic Community of West African States (ECOWAS) drought-hotspots | +0.60% | Nigeria, Niger, Burkina Faso, Senegal, and Mali | Long term (≥ 4 years) |

| Blockchain traceability premiums from European retailers | +0.40% | United Kingdom, Netherlands, Spain, Portugal, and expanding North America | Short term (≤ 2 years) |

| Carbon-credit income from inter-cropped cowpea-millet systems | +0.30% | Sahel belt, and pilot South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Pulse-Based Proteins Among Flexitarian Consumers

North American and European food makers doubled cowpea flour and isolate use between 2024 and 2025 as flexitarian shoppers sought non-soy protein options. Cowpea’s 23-25% protein and mild flavor ease formulation in meat analogs, dairy alternatives, and snack bars. Surveys in 2025 showed that 57% of European adults eat legumes weekly and that more than half want a larger pulse assortment [1]Source: European Food Safety Authority, “Consumer Pulse Consumption Survey 2025,” EFSA.europa.eu. The United States' acreage in California and Texas rose 22% in 2025 after crop insurance expansion [2]Source: USDA Foreign Agricultural Service, “Global Agricultural Trade Data,” FAS.usda.gov. Urban consumers in India and China are also raising pulse intake to manage metabolic diseases, supporting long-run demand growth.

Recovery of Sahelian Export Corridors After African Continental Free Trade Area (AfCFTA) Tariff Cuts

The African Continental Free Trade Area (AfCFTA) removed tariffs on intra-African pulses in 2024, trimming landed costs by 12-18% on the Niger–Nigeria route [3]Source: African Union, “African Continental Free Trade Area,” AU.int. Formal Nigerian imports from Niger have grown substantially in recent years. Similarly, Burkina Faso and Mali have increased exports to Côte d’Ivoire and Ghana, supported by reinvestments in cleaning and grading processes. However, despite improvements in customs clearance times, congestion at the Maradi-Katsina corridor continues to cause delays, adding several transit days during peak harvest periods.

Chinese Feed Compounders Blending Cowpea Haulms in Ruminant Rations

Facing high alfalfa prices of USD 385 per metric ton CIF (Cost, Insurance, and Freight) in 2025, Chinese dairies used cowpea haulms for up to 15% of forage dry matter, cutting feed bills by 9-11% while holding milk yields steady [4]Source: Kansas State University, “Cowpea Protein Properties and Applications,” K-state.edu. Feed makers in Shandong and Hebei now contract growers in Myanmar and India, where haulm yields top 4 metric tons per hectare [5]Source: China Feed Industry Association, “Feed Industry Statistics and Trends,” Chinafeed.org.cn. This contracting model enhances feed cost predictability, ensures supply security, and promotes improved post-harvest handling and consistent quality. Cooperatives in Gujarat and Rajasthan, India, have initiated silage pilot projects to reduce reliance on maize stover, fostering more resilient and diversified forage strategies.

Blockchain Traceability Premiums from European Retailers

United Kingdom-based retailers Tesco and Sainsbury’s launched blockchain-tracking pilots in late 2024. By 2025, the 12–15% premium for verified shipments to the Netherlands and Spain extended. This development led to a one-third reduction in documentation disputes and shortened customs delays by two days, enhancing shipment reliability and boosting buyer confidence across retail supply chains. The European Union’s due diligence law, set to take effect in 2027, will require digital traceability as a standard. However, the associated upfront technology and compliance costs continue to pose challenges for smaller African cooperatives, which often lack access to digital infrastructure and financial support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thrips-driven yield crashes in South Asian spring crop | -0.80% | India, Bangladesh, Myanmar, and localized West Africa | Short term (≤ 2 years) |

| Price suppression from record Brazilian common-bean harvests | -0.60% | Brazil, Argentina, and global pulse markets | Short term (≤ 2 years) |

| Post-harvest fungal losses in humid coastal Africa | -0.50% | Nigeria, Ghana, Benin, and Cameroon | Medium term (2-4 years) |

| Tight credit and foreign-exchange restrictions for Nigerian exporters | -0.40% | Nigeria, spill-over Niger and Burkina Faso | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Thrips-Driven Yield Crashes in South Asian Spring Crop

Flower thrips cut yields by up to 18% in India and Bangladesh during 2025, forcing imports from Myanmar and West Africa [6]Source: International Crops Research Institute for the Semi-Arid Tropics, “Cowpea Production and Pest Management,” Icrisat.org. Integrated pest management reduced losses by approximately 25% in controlled trials. However, adoption remained below 15% of the planted area due to weak extension services, limited farmer awareness, and higher upfront implementation costs. Additionally, export rejections in Europe increased as pesticide residues exceeded regulatory limits, escalating compliance risks and creating quality-related barriers for affected growers.

Price Suppression from Record Brazilian Common-Bean Harvests

Brazil harvested 3.2 million metric tons of common beans in 2025, the highest since 2019, driving cowpea farm-gate prices down 8-11% [7]Source: National Supply Company of Brazil, “Brazilian Pulse Production Statistics 2025,” Conab.gov.br. Wholesale Carioca beans were priced at BRL 180 (USD 30) per 60-kilogram bag, compared to BRL 210 (USD 35) for cowpeas. This narrowing price premium has prompted Northeastern farmers to allocate more acreage to common beans. Meanwhile, West African buyers have further reduced imports from Brazil, taking advantage of the African Continental Free Trade Area, which has exacerbated oversupply in export markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Africa accounted for 38.7% of the cowpea market in 2025. Nigeria’s Kano, Katsina, and Jigawa states anchor production, yet high coastal humidity invites fungal losses that can erase up to 12% of stored beans. African Continental Free Trade Area (AfCFTA) tariff removal has already boosted Niger–Nigeria flows and stimulated investment in cleaning and grading units near Maradi. Tanzania and Mozambique are gaining share as donor-funded seed programs raise output and diversify origin risk for European and Middle Eastern buyers.

The Asia-Pacific region accounted for a substantial share of demand and is projected to be the fastest-growing, with a 6.5% CAGR during the forecast period (2026-2031). This growth is driven by structural deficits in pulse availability in India and increasing forage requirements in China. Crop disruptions caused by thrips in parts of India and Southeast Asia during 2025 tightened regional supply, leading to greater reliance on imports from West Africa. China continues to procure imported materials through structured haulm contracts to manage dairy feed costs, while Bangladesh remains reliant on imports to address ongoing domestic production shortfalls.

South America accounts for a smaller share of global demand, and recent price pressure from strong Carioca and black-bean harvests has led to reduced cowpea plantings for the upcoming season. In North America, demand is concentrated primarily in Texas and California, where improved insurance conditions have encouraged acreage expansion. Europe’s market is driven by migrant-led retail consumption and by blockchain-based traceability premiums that support verified supply chains. Middle Eastern demand remains limited but strategic, with countries such as the United Arab Emirates and Saudi Arabia maintaining pulse stocks as part of broader food-security initiatives.

Competitive Landscape

The cowpea market remains moderately fragmented, with no single entity dominating the trading landscape. A select group of large international merchants accounts for a significant portion of traded volumes, while regional aggregators and origin-focused traders continue to find opportunities for growth. Major exporters have established integrated sourcing and logistics hubs in key producing regions, particularly in Africa and parts of Asia. These hubs enable efficient supply aggregation and investment in post-harvest handling. Additionally, exporters are increasingly enhancing their cleaning, grading, and processing capabilities to meet the rising quality standards of import-dependent markets, thereby strengthening their position in the value chain while maintaining operational flexibility across various origins.

Leading agribusiness firms are expanding downstream applications to diversify cowpea demand beyond traditional food and feed uses. In Africa and Asia, platforms are being scaled to improve farmer aggregation, traceability, and processing efficiency. Concurrently, investments in protein innovation are facilitating the use of cowpeas as an ingredient in plant-based food products. These developments underscore the growing recognition of cowpeas as a sustainable protein source and aim to support commercial-scale supply for food manufacturers. Consequently, value addition is increasingly occurring closer to production origins, fostering tighter integration between sourcing, processing, and end-use markets.

In addition to large multinational players, smaller mission-driven organizations are contributing significantly by supporting farmer cooperatives. These organizations provide bundled services, including access to improved seeds, risk mitigation tools, and structured financing models, which help stabilize farmer incomes and reduce the need for forced selling during periods of price volatility. Meanwhile, competitive advantages in the cowpea market are shifting toward firms adept at managing traceability, currency risks, and sustainability compliance. Stricter due-diligence requirements and carbon accountability standards, particularly in Europe, are raising entry barriers. This trend is gradually driving market consolidation, favoring traders with robust financial resources, advanced digital infrastructure, and strong compliance capabilities.

Recent Industry Developments

- November 2024: Ghana’s Council for Scientific and Industrial Research - Savanna Agricultural Research Institute (CSIR-SARI) introduced two drought-tolerant cowpea varieties, Awudu Benga and Kanton Bongdaa, for smallholder farmers in the Mion District. Supported by the United States Agency for International Development (USAID) through the Legume Systems Innovation Lab.

- October 2024: Indonesia introduced new advanced-notice quarantine rules for agricultural imports, influencing cowpea exporters seeking Southeast Asian market entry.

- September 2024: Cargill, Incorporated and HarvestPlus initiated the 36-month NutriHarvest project to support over 119,000 farmers with nutrition-enhancing crops, including cowpea.

Global Cowpeas Market Report Scope

The Cowpeas Market Report is Segmented by Geography (North America, Europe, Asia-Pacific, Africa, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, Regulatory Framework, Logistics and Infrastructure, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Europe | United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Netherlands | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Spain | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Portugal | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Asia-Pacific | India | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| China | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Myanmar | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Bangladesh | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Middle East | United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Africa | Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Niger | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Europe | United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Netherlands | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Spain | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Portugal | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Asia-Pacific | India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| China | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Myanmar | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Bangladesh | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Middle East | United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Africa | Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Niger | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the projected value of the cowpeas market in 2031?

The cowpeas market is forecast to reach USD 10.70 billion by 2031.

Which region is expanding fastest in cowpea demand?

Asia-Pacific leads with a projected 6.5% CAGR from 2026 to 2031, driven by India’s pulse gap and China’s forage needs.

Why are European retailers paying premiums for cowpeas?

They offer 12-15% premiums for blockchain-verified lots that prove origin, pesticide compliance, and carbon footprint.

How do pesticide-residue rules affect exports?

Stricter limits in Europe and North America elevate compliance costs and raise rejection risks, slightly dampening export growth in the short term.

Page last updated on: