Fava Bean Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.58 Billion |

| Market Size (2031) | USD 5.71 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fava Bean Market Analysis by Mordor Intelligence

The fava bean market size is projected to grow from USD 4.32 billion in 2025 to USD 4.58 billion in 2026, reaching USD 5.71 billion by 2031, with a CAGR of 4.51% during 2026-2031. Growth is driven by policy-induced acreage expansion in Europe, increased investments in protein fractionation in North America, and rising demand for plant-based products in urban areas of the Asia-Pacific region. While whole beans continue to dominate trade volumes, processors are increasing margins by transitioning from commodity beans to isolates, which command prices 8-12 times higher. Traders are focusing on scale within a bifurcated value chain. European Common Agricultural Policy (CAP) subsidies are directing production toward feed channels, but limited fractionation capacity allows North America to maintain value leadership despite lower harvested volumes. Challenges such as flavor management costs and pest-related crop losses impact profitability. However, investments in enzymatic debittering and blockchain traceability reflect confidence in the market's evolution from an ethnic staple to a functional protein platform.

Key Report Takeaways

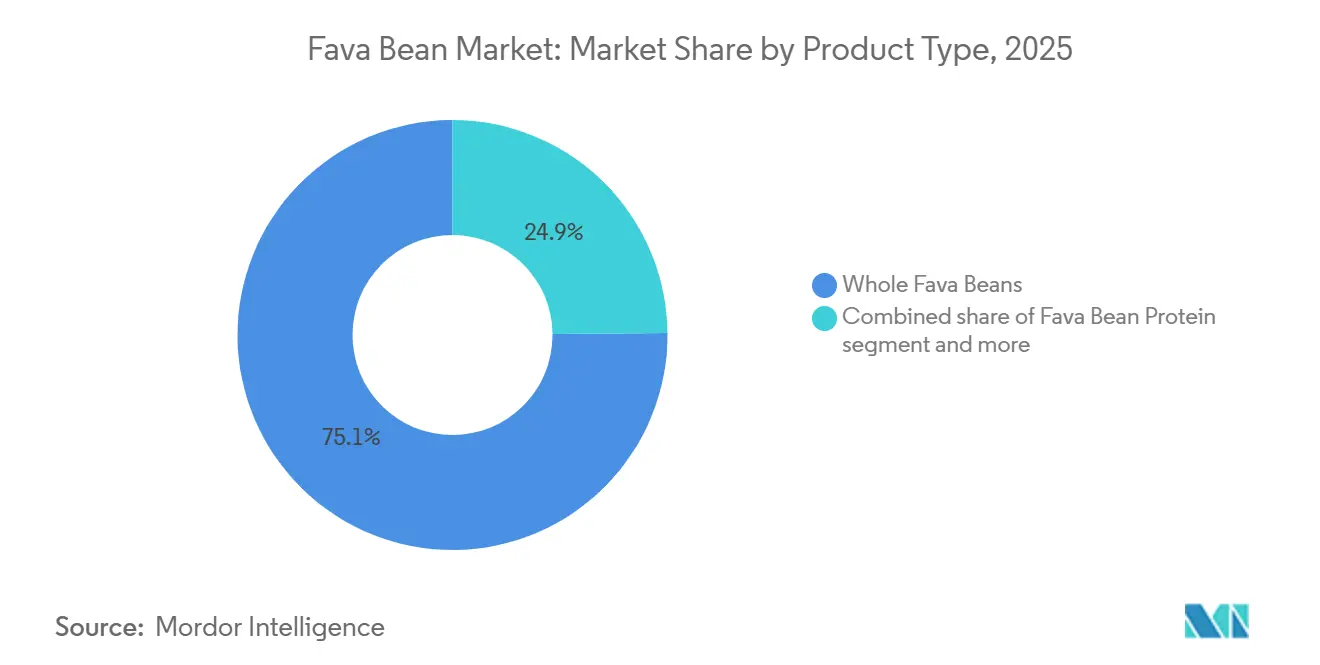

- By product type, whole fava beans led with 75.14% share in 2025, while fava bean protein is advancing at a 5.99% CAGR through 2031.

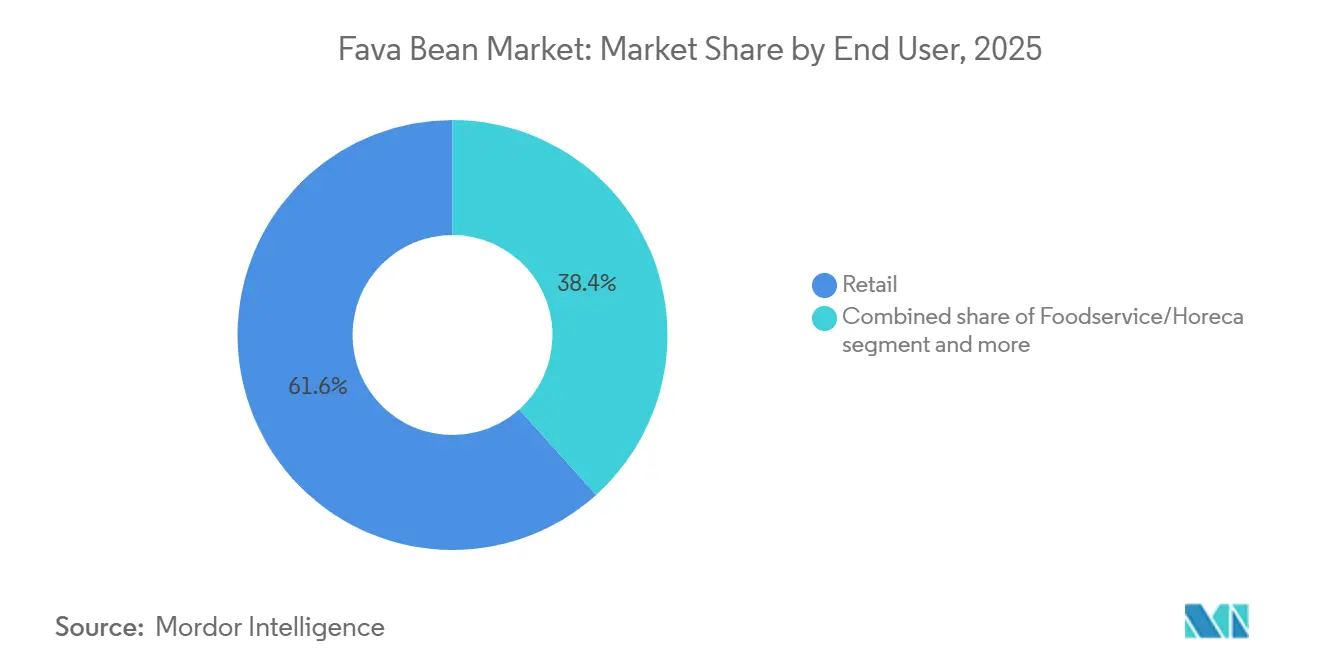

- By end user, retail accounted for 61.65% of sales in 2025, whereas foodservice/horeca is poised for the fastest growth at a 5.17% CAGR to 2031.

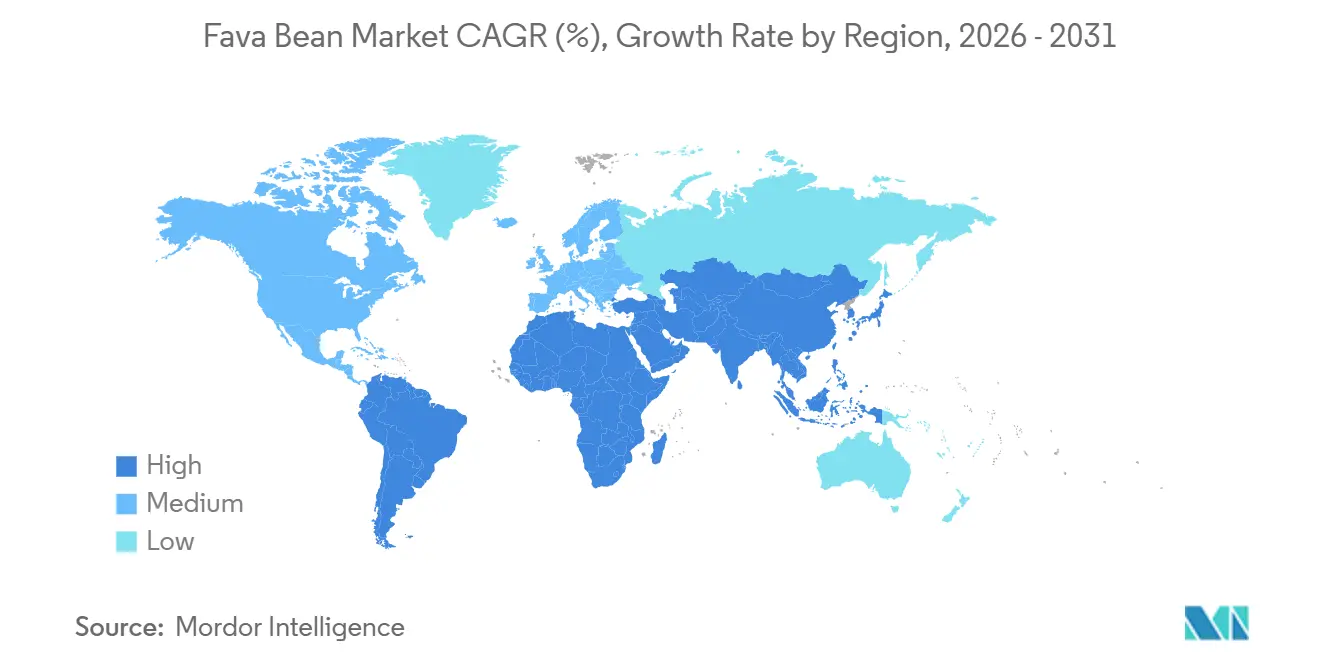

- By geography, North America commanded 33.02% of value in 2025, yet Asia-Pacific is projected to be the fastest region at a 5.11% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fava Bean Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for plant-based protein | +1.2% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Incorporation into meat analogues and dairy substitutes | +0.9% | North America, Europe, Australia; emerging in China and India | Medium term (2-4 years) |

| Commercialization of protein isolates for sports nutrition | +0.7% | North America, Europe, with spillover to Middle East and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Rising consumer awareness of clean labels | +0.6% | Global, led by North America and Western Europe | Long term (≥ 4 years) |

| European CAP subsidies promoting pulse cultivation | +0.5% | Europe (France, Germany, Poland, Spain, Italy), indirect impact on global supply | Long term (≥ 4 years) |

| Growth of gluten-free and allergy-friendly flour alternatives | +0.4% | North America, Europe, Australia, with emerging demand in Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for plant‑based protein

The global fava bean market is experiencing significant growth, driven by the rising demand for plant-based protein as consumers increasingly adopt sustainable and health-conscious dietary habits. This shift represents a structural change in global consumption patterns, influenced by environmental concerns, ethical considerations, and evolving nutritional preferences. Fava beans are gaining prominence within the plant-based protein market due to their high protein content, favorable amino acid profile, and non-GMO status, positioning them as a viable alternative to traditional protein sources such as soy and pea protein. Furthermore, their compatibility with clean-label and allergen-friendly formulations enhances their appeal to both food manufacturers and consumers. The transition toward plant-based diets is evident in both developed and emerging markets, driving demand for alternative protein sources. For instance, in 2024, Statistics Netherlands reported that 25% of meals in the Netherlands were vegetarian, reflecting the widespread adoption of plant-forward eating habits. Similarly, in 2025, data from the Vegan Society indicated that 6% of Polish consumers identified as vegetarian or vegan, with an additional 24% identifying as flexitarian[1]Source: The Vegan Society, "Worldwide growth of veganism", vegansociety.com. The growing number of flexitarian consumers, those who actively reduce meat consumption without fully eliminating it, plays a crucial role in expanding the market for plant-based ingredients like fava beans.

Incorporation into meat analogues and dairy substitutes

The growing incorporation of fava bean ingredients in meat analogues and dairy substitutes is a significant growth driver for the global fava bean market, fueled by advancements in plant-based food innovation. As consumer demand for alternatives to animal-derived products rises, manufacturers face the challenge of creating formulations that replicate the taste, texture, and nutritional attributes of traditional meat and dairy products. Fava beans are emerging as an effective solution in this context. Fava bean protein is increasingly utilized in meat analogues due to its excellent emulsification, water-binding, and texturizing properties, which are critical for replicating the fibrous and juicy characteristics of meat. Additionally, its relatively neutral flavor profile compared to other plant proteins minimizes the need for masking agents, enabling cleaner and more natural product formulations. This makes fava beans particularly suitable for applications such as plant-based burgers, sausages, and minced meat alternatives. In the dairy substitute segment, fava beans are being used in products like plant-based milk, yogurt, and cheese, where they enhance protein content and creaminess. Their functional versatility allows manufacturers to improve both the nutritional profile and mouthfeel of dairy alternatives, addressing common consumer concerns regarding taste and texture in plant-based products.

Commercialization of protein isolates for sports nutrition

The commercialization of protein isolates designed for sports nutrition is emerging as a significant growth driver for the global fava bean market. This trend is supported by the increasing convergence of active lifestyles, performance-oriented nutrition, and plant-based dietary preferences. As consumers place greater emphasis on fitness and physical well-being, the demand for high-quality, digestible, and functional protein ingredients is expanding beyond traditional sources like whey and soy, creating opportunities for alternatives such as fava bean protein isolates. Fava bean protein is gaining prominence in sports nutrition due to its high protein content, balanced amino acid profile, and suitability for clean-label and allergen-free formulations. Unlike some conventional plant proteins, fava bean isolates provide a neutral taste and improved texture, making them ideal for use in protein powders, bars, ready-to-drink beverages, and performance snacks. This functional versatility is driving manufacturers to incorporate fava bean protein isolates into a diverse range of sports nutrition products. The increasing consumer participation in fitness and recreational activities is directly boosting demand for such protein solutions. In 2024, 21.5% of the population in the United States engaged daily in sports, exercise, and recreational activities, up from 21.3% in 2023, reflecting a steady rise in active lifestyle adoption [2]Source: U.S Bureau of Labor Statistics, "Economic News Release", bls.gov. This growing consumer base is fueling consistent demand for convenient and effective protein supplementation, particularly in formats that align with broader health and sustainability values.

Rising consumer awareness of clean labels

The rising consumer demand for clean labels is a key driver for the global fava bean market. Consumers increasingly prefer products made with simple, recognizable ingredients that align with their values of transparency, health, and sustainability. This trend is encouraging manufacturers in the food and beverage industry to adopt clean label formulations, thereby increasing the use of ingredients like fava bean protein, valued for its natural and non-GMO characteristics. As consumers pay closer attention to product contents, there is a growing demand for items free from artificial additives, preservatives, and complex ingredients. Fava beans, with their clean nutritional profile and minimal processing requirements, align well with this trend. They provide a natural source of plant-based protein, making them particularly suitable for products targeting clean label standards, especially in plant-based, gluten-free, and allergen-friendly categories. An important aspect of this trend is consumers' willingness to pay a premium for clean label products. In 2025, 56% of consumers reported being willing to spend more on products with recognizable ingredients, demonstrating a stronger commitment to healthier and more transparent food choices [3]Source: Ingredion, "Clean label ingredients: From buzzword to business driver", ingredion.com. This preference is not only driving changes in product formulations but also influencing packaging strategies, with clean label claims emerging as a significant competitive advantage in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flavor off-notes limit formulation versatility | -0.8% | Global, most acute in North America and Europe where neutral taste is prioritized | Short term (≤ 2 years) |

| Competition from other legumes | -0.6% | Global, with pea protein dominance in North America and Europe; chickpea and lentil growth in Asia-Pacific | Medium term (2-4 years) |

| High cost of value-added product development | -0.5% | North America, Europe, and developed Asia-Pacific markets | Long term (≥ 4 years) |

| Crop losses from broad-bean-weevil outbreaks | -0.3% | Mediterranean Europe (Spain, Italy, Greece), North Africa (Morocco, Egypt) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Flavor off-notes limit formulation versatility

Flavor challenges associated with fava bean ingredients continue to act as a significant restraint in the global fava bean market, particularly in applications where taste neutrality and sensory appeal are critical for consumer acceptance. Despite their strong nutritional and functional profile, fava beans are often linked to beany, bitter, or earthy off-notes, which can restrict their use in various food and beverage formulations. These flavor issues present formulation challenges, especially in product categories such as dairy alternatives, ready-to-drink beverages, and mild-flavored meat analogues, where a subtle and neutral taste profile is essential. To address these challenges, manufacturers frequently use flavor masking agents, sweeteners, or additional processing steps to reduce undesirable flavors. However, these approaches increase formulation costs and may conflict with clean-label objectives, as the inclusion of extra ingredients can compromise product simplicity and transparency. Compared to more established plant proteins like pea or soy, which have undergone extensive optimization to resolve flavor issues, fava bean protein faces greater obstacles. This can lead to slower adoption in mainstream product development, particularly for brands that prioritize minimal formulation complexity and faster time-to-market.

Competition from other legumes

One of the primary restraints affecting the growth of the fava bean market is the intense competition from more established legumes, including soybeans, chickpeas, lentils, peas, and other pulses. These alternatives are more deeply embedded in global food systems, supply chains, and consumer diets, making it challenging for fava beans to significantly increase their market share. A key factor contributing to this challenge is the strong consumer familiarity and acceptance of competing legumes. For instance, soybeans and chickpeas have well-established culinary applications across various cuisines and are widely recognized as staple protein sources. In contrast, fava beans remain relatively niche in many regions, limiting their integration into everyday diets and processed food products. This familiarity advantage enables competing legumes to dominate both retail consumption and foodservice applications. In the plant-based protein market, competition is particularly pronounced. Pea protein and soy protein are widely used in meat alternatives, dairy substitutes, and nutritional products due to their neutral taste profiles, functional properties, and robust innovation pipelines supported by significant investments. As a result, fava beans hold a smaller share of product development activity and face slower adoption in mainstream plant-based formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Fractions Drive Value Migration

Whole fava beans accounted for 75.14% of the market share in 2025, driven by consistent demand from ethnic grocery retailers, bulk foodservice distributors, and animal-feed compounders. This segment's dominance highlights its entrenched role in traditional and bulk markets. However, the revenue contribution of whole fava beans is increasingly diverging from its volume dominance as buyers shift their preferences toward lower-margin commodity grades. This trend reflects changing market dynamics, where cost considerations and evolving consumer preferences are reshaping demand patterns for whole beans.

Fava bean protein, including concentrates and isolates, is projected to grow at a CAGR of 5.99% from 2026 to 2031, surpassing the overall market growth by 148 basis points. This growth is primarily driven by the rising demand for functional ingredients in sports nutrition, meat analogues, and dairy substitutes, which require higher-value products rather than whole pulses. Protein isolates, which deliver 85% to 92% protein on a dry-weight basis, are priced significantly higher at USD 8 to USD 12 per kilogram, compared to USD 0.80 to USD 1.20 for whole beans. This tenfold price differential is reshaping processor investment strategies, as manufacturers increasingly prioritize higher-margin protein products to capitalize on the growing demand for plant-based and functional food ingredients.

By End User: Retail Dominance Masks Foodservice Momentum

Retail channels accounted for 61.65% of the market share in 2025, driven by consumer packaged goods such as canned whole beans, gluten-free flour blends, and plant-based protein powders. However, growth in this segment is slowing as penetration among key demographics, health-conscious millennials and ethnic cuisine enthusiasts, nears saturation in North America and Western Europe. The retail segment has benefited from the increasing consumer preference for convenient and shelf-stable products, but its growth trajectory is now constrained by market maturity in developed regions. Despite this, opportunities remain in emerging markets where awareness of plant-based and gluten-free products is still growing, presenting potential for future expansion. Additionally, innovation in packaging and product formulations could help reinvigorate demand in saturated markets.

The foodservice/horeca segment is expected to grow at a CAGR of 5.17% from 2026 to 2031, making it the fastest-growing end-user category. This growth is fueled by quick-service restaurants and casual dining chains incorporating fava-based patties, dairy-free sauces, and high-protein side dishes to cater to flexitarian consumers and address regulatory pressures on animal-protein sourcing. In September 2025, Nestlé Professional introduced a fava-chickpea burger blend for European foodservice operators, offering a 40% lower carbon footprint compared to beef patties and aligning with EU Green Deal targets for institutional catering. The shift toward foodservice and industrial processing indicates that fava beans are evolving from an ethnic staple to a mainstream functional ingredient. However, this transition relies on processors' ability to ensure consistent quality and neutral flavor profiles at scale. The increasing adoption of fava beans in institutional catering and foodservice highlights their potential to meet sustainability goals while addressing consumer demand for healthier, plant-based options.

Geography Analysis

North America captured 33.02% of the market share in 2025, supported by Canada's position as the world's second-largest fava bean exporter. In 2024, Canada exported 142,000 metric tons, primarily to Egypt, Algeria, and the United Arab Emirates. Additionally, the United States benefits from a concentration of protein-fractionation facilities in Minnesota, North Dakota, and Montana. These facilities enable the region to process fava beans into high-value protein fractions, catering to the growing demand for plant-based proteins in food and beverage applications. The region's ability to integrate production and processing ensures a competitive edge in the global market. Furthermore, North America's well-established infrastructure and focus on innovation in processing technologies allow it to maintain a strong position in the value chain, ensuring profitability and market leadership.

The Asia-Pacific region is expected to grow at a compound annual growth rate (CAGR) of 5.11% from 2026 to 2031, marking the fastest regional growth rate. This growth is driven by China's protein-diversification strategy, which aims to reduce reliance on traditional protein sources, and India's expanding pulse-processing infrastructure, which supports the production of value-added products. The increasing adoption of plant-based diets across the region, coupled with government initiatives to promote pulse cultivation and processing, is further fueling market growth. Additionally, the rising middle-class population and increasing awareness of the health benefits of plant-based proteins are contributing to the region's robust growth prospects, making it a focal point for market expansion.

Europe, despite accounting for significant share of global fava bean production in 2025, lags behind North America in market value. This is primarily because a significant portion of the harvest is directed toward low-margin animal feed rather than human-grade fractions. Structural inefficiencies, such as inadequate cleaning, dehulling, and fractionation infrastructure, limit the region's ability to capitalize on the growing demand for plant-based proteins. CAP subsidies have not yet resolved these challenges, leaving Europe at a disadvantage. However, the region's large production base and increasing focus on improving processing capabilities present opportunities for future growth if these inefficiencies are addressed. Moreover, the growing consumer demand for sustainable and locally sourced plant-based products could drive investments in advanced processing technologies, potentially transforming Europe's fava bean market dynamics in the long term.

Competitive Landscape

The global fava bean market is moderately fragmented, with multinational ingredient suppliers such as Roquette, ADM, Ingredion, and BENEO leading the protein extraction and fractionation segment. These companies leverage advanced processing technologies and extensive global supply chains, establishing themselves as key players in the high-value, plant-based protein market. Meanwhile, regional cooperatives and commodity traders dominate whole-bean distribution, concentrating on large-scale commodity sales within localized markets. Mid-sized processors face challenges in this competitive landscape, struggling to achieve economies of scale and competing with both large suppliers and regional distributors.

Innovative processing technologies, including enzymatic debittering and membrane filtration, present significant opportunities by reducing off-note intensity in fava bean protein while maintaining yield. However, fewer than 10 commercial-scale plants worldwide currently utilize these advanced capabilities. This gap creates potential for specialized processors to enter the market with high-quality, neutral-tasting products. These advancements are expected to drive growth in niche market segments and provide smaller players with a competitive advantage if they can effectively adopt these technologies.

Burcon NutraScience, an emerging player in the market, filed a U.S. patent in 2025 for a pH-shift extraction process that achieves 94% protein purity while reducing water consumption by 30% compared to traditional methods. If successfully implemented, this technology could transform the cost structure of fava bean protein production, making it more sustainable and cost-efficient. As sustainability and efficiency gain importance among consumers and producers, this innovation could offer smaller processors a competitive edge, potentially challenging the dominance of larger multinational companies in the market.

Fava Bean Industry Leaders

-

Goya Foods, Inc.

-

Roquette Frères S.A.

-

Archer Daniels Midland (ADM)

-

Prairie Fava

-

BENEO GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Phytokana Ingredients is spearheading a USD 32.5 million initiative to process Canadian-grown fava beans into plant-based food ingredients, in partnership with Maia Farms and Protein Industries Canada. The project employs a proprietary method that avoids the use of chemicals and heat to produce protein concentrates, flours, and starches. These ingredients are intended for applications such as dairy alternatives and plant-based meats.

- August 2025: Burcon NutraScience has launched FavaPro, a high-purity fava bean protein isolate with over 90% protein content, to address the increasing demand for high-performance plant-based ingredients. The product is manufactured using a proprietary extraction process and is non-GMO, hypoallergenic, and environmentally sustainable. Fava beans, being nitrogen-fixing crops, contribute to improved soil health.

- May 2024: Roquette has introduced its first fava bean protein isolate, NUTRALYS Fava S900M, to expand its plant protein offerings in Europe and North America. This ingredient contains approximately 90% protein and is designed for use in meat alternatives, dairy substitutes, and baked goods. It features a clean taste, light color, and strong functional properties, including gel strength and stability.

Global Fava Bean Market Report Scope

Fava beans are the edible seeds of the legume crop Vicia faba, otherwise known as faba beans, horse beans, or broad beans. The fava bean market includes production analysis (volume), consumption analysis (value and volume), export analysis (value and volume), import analysis (value and volume), and price trend analysis across the globe. The market is segmented by geography into North America, Europe, Asia-Pacific, South America, and Africa. The report offers the market size and forecasts in terms of volume in (metric tons) and value in (USD) for all the above segments.

| Whole Fava Beans | |

| Fava Bean Flour | |

| Fava Bean Protein | Protein Concentrate |

| Protein Isolate | |

| Others |

| Retail |

| Foodservice/Horeca |

| Food Processing |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Whole Fava Beans | |

| Fava Bean Flour | ||

| Fava Bean Protein | Protein Concentrate | |

| Protein Isolate | ||

| Others | ||

| By End User | Retail | |

| Foodservice/Horeca | ||

| Food Processing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the fava bean market?

The sector is valued at USD 4.58 billion in 2026 and is projected to reach USD 5.71 billion by 2031.

How fast is demand for fava protein segment growing?

Fava bean protein is expected to expand at a 5.99% CAGR from 2026 to 2031, outpacing whole-bean growth.

Which region shows the highest growth potential for fava beans?

Asia-Pacific is forecast to post the fastest regional CAGR of 5.11% through 2031, led by China and India.

What challenges limit wider use of fava protein in beverages?

Hexanal-driven off-notes require costly debittering, and calcium fortification can cause protein precipitation.

Page last updated on: