Okra Seeds Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

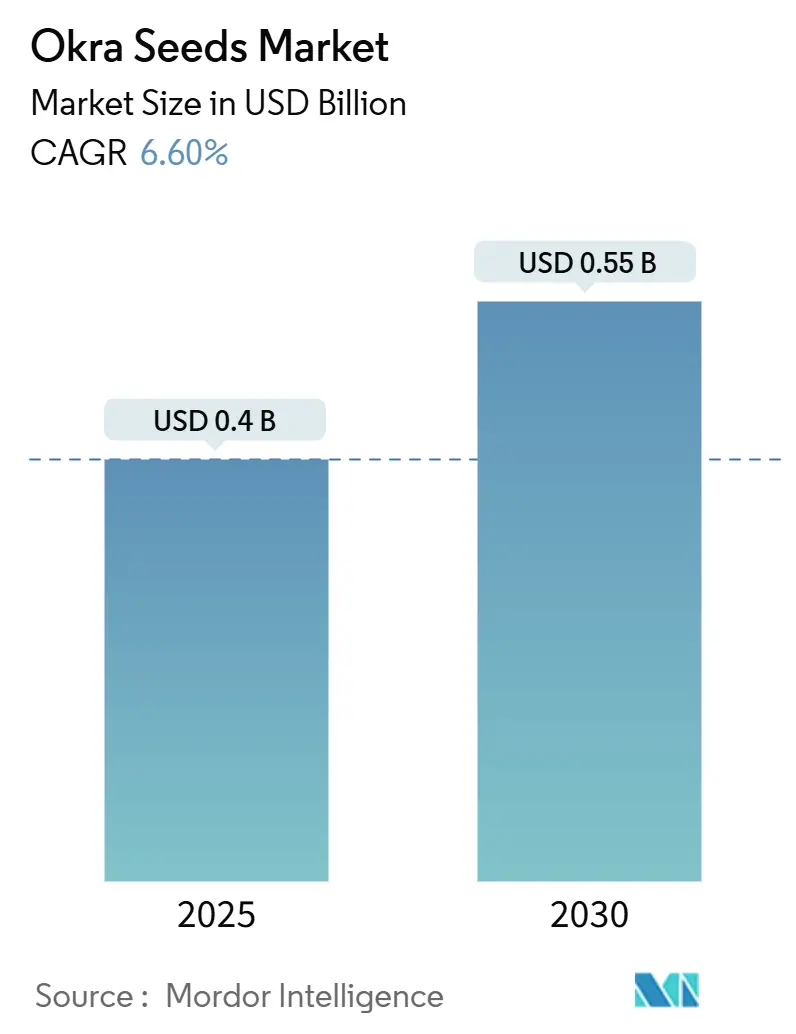

| Market Size (2025) | USD 0.4 Billion |

| Market Size (2030) | USD 0.55 Billion |

| Growth Rate (2025 - 2030) | 6.60% CAGR |

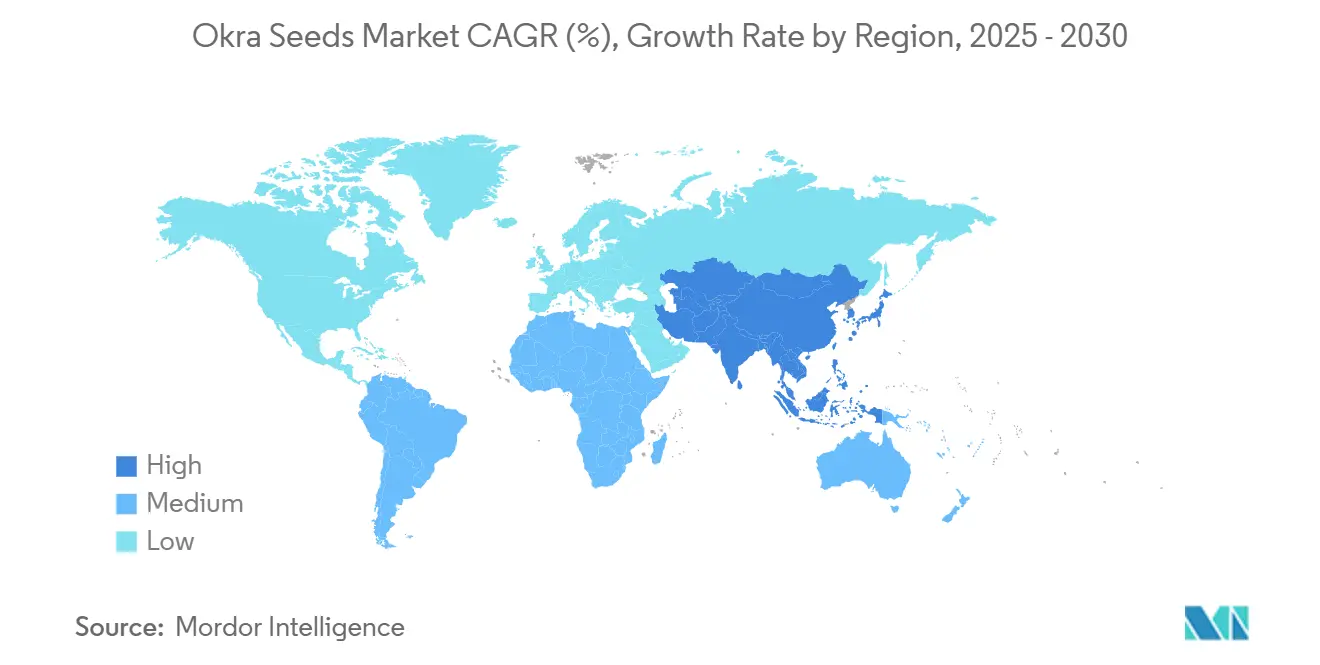

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Okra Seeds Market Analysis by Mordor Intelligence

The okra seeds market size is valued at USD 0.40 billion in 2025 and is forecast to reach USD 0.55 billion by 2030, advancing at a 6.60% CAGR. Demand is driven by the steady shift from open-pollinated cultivars toward disease-resistant hybrids, wider adoption of seed treatment technologies, and government seed-replacement programs that lower cost barriers for smallholder farmers. The penetration of protected cultivation, especially in the Asia-Pacific and the Middle East, widens seasonal planting windows and increases per-crop seed requirements. The competitive landscape is moderately concentrated, with the top five suppliers controlling a significant share of revenue and leveraging marker-assisted breeding and precision coating to capture value across the supply chain[1]United States Patent and Trademark Office, “Seed Industry Patent Filings Analysis,” uspto.gov . Supply-side risks center on Yellow Vein Mosaic Virus (YVMV) outbreaks and cold-chain gaps in emerging markets, yet advances in near-infrared (NIR) quality screening and diversified production geographies help stabilize distribution.

Key Report Takeaways

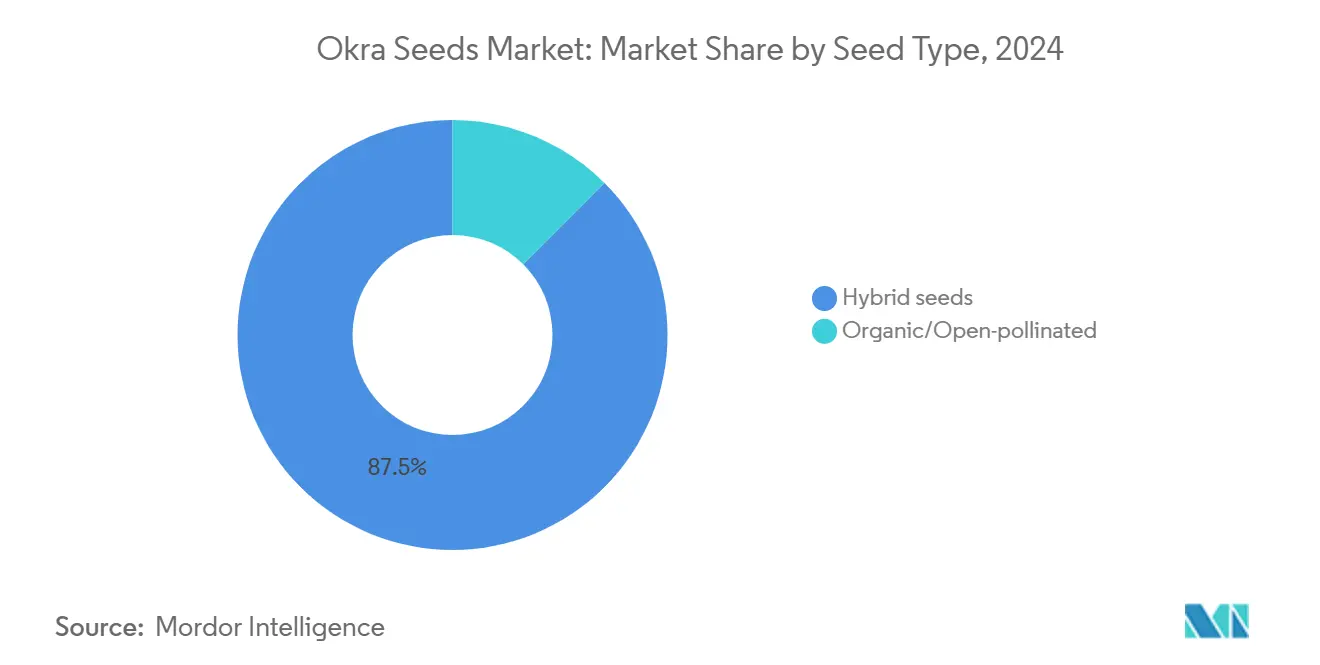

- By seed type, hybrids led with 87.5% of the okra seeds market share in 2024, while organic/open-pollinated seeds are projected to expand at a 10.95% CAGR through 2030.

- By seed form, treated seeds accounted for 67% of the okra seeds market size in 2024, and untreated seeds recorded the fastest 9.75% CAGR to 2030 as organic farming expands.

- By end use, commercial farming held 76% of the okra seeds market size in 2024, whereas home gardening is set to progress at a 9.15% CAGR on the back of urban agriculture.

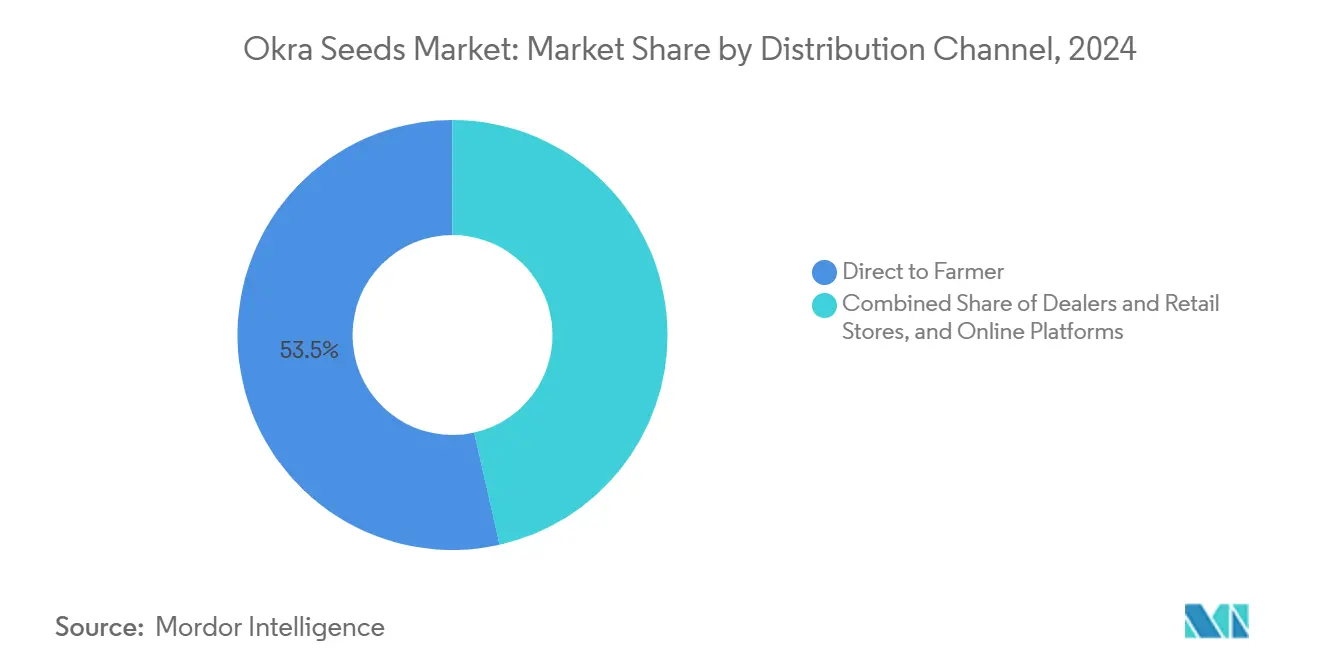

- By distribution channel, dealer and retail outlets maintained a 53.5% share of the okra seeds market size in 2024, yet online platforms posted an 11.85% CAGR through 2030.

- Asia-Pacific leads the market with 52% of the okra seeds market size and registers an 8.5% CAGR through 2030.

Global Okra Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in hybrid seed adoption among commercial growers | +1.8% | Global, strongest in Asia-Pacific and Africa | Medium term (2-4 years) |

| Growth in demand for disease-resistant cultivars | +1.5% | Global, critical in Yellow Vein Mosaic Virus endemic regions | Long term (≥ 4 years) |

| Expansion of protected cultivation acreage worldwide | +1.2% | Asia-Pacific core, spill-over to Middle East | Medium term (2-4 years) |

| Government programs promoting vegetable seed replacement | +0.9% | Asia-Pacific and Africa | Long term (≥ 4 years) |

| Emergence of near-infrared seed screening technologies | +0.6% | North America and Europe early adoption | Long term (≥ 4 years) |

| Seed-grade okra oil demand in nutraceuticals | +0.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Hybrid Seed Adoption among Commercial Growers

Hybrid adoption is accelerating because the yield advantage can surpass 50% under optimum field conditions. Commercial farms exceeding 5 hectares exhibit 85% hybrid use compared with 45% among smallholder plots, indicating that scale economics favor premium genetics. Subsidized access through public extension programs in India and Ghana reinforces confidence in certified seed purchases. Seed companies stress multi-trait hybrids such as ADV 842 that stack Yellow Vein Mosaic Virus (YVMV) and Enation Leaf Curl tolerance, helping stabilize harvests when virus pressure spikes. Widespread demonstration trials build local proof of concept and pull hybrids deeper into rural markets.

Growth in Demand for Disease-Resistant Cultivars

Shielding crops from Yellow Vein Mosaic Virus (YVMV) is now the top breeding goal because outbreaks can wipe out entire plantings within weeks. Robust lines that pyramid resistance genes curb pesticide use and unlock residue-free export channels. Varieties like Navya lengthen shelf life while defending against evolving viral strains. Continuous gene introgression and marker-assisted selection require sizable R&D budgets, tilting competitive advantage toward firms with global breeding networks. Durable resistance also lowers farmer risk perception, partly offsetting higher seed costs and spurring re-purchase rates.

Expansion of Protected Cultivation Acreage Worldwide

Greenhouse and net-house acreage in the Asia-Pacific region has increased in recent years, turning okra into a year-round crop that commands premium off-season pricing.[2]University of Cape Coast, “Drought and Heat Tolerance Assessment in African Okra Genotypes,” ucc.edu.gh Protected systems need determinate plant architecture and compact nodes that suit dense spacing. Farmers willingly pay 200-300% more for seeds optimized for these conditions because higher output per square foot shortens payback on capital structures. As extreme weather intensifies, protected cultivation moves beyond export-oriented farms to domestic supply chains intent on buffering climate risk.

Seed-Grade Okra Oil Demand in Nutraceuticals

Okra seeds contain 15-20% oil rich in unsaturated fatty acids and antioxidants that appeal to functional food formulators. Dual-purpose cultivars could supply fresh pods and oilseed stock, turning by-products into new revenue lines. Seed companies are exploring vertical integration to capture this margin, though balancing horticultural yield with oil content demands sophisticated breeding. Nutraceutical pull may justify premium price tiers in developed markets where dietary supplements scale quickly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Vulnerability of Seed Supply to Yellow Vein Mosaic Virus Outbreaks | −1.2% | Global, most severe in Asia-Pacific and Africa | Short term (≤ 2 years) |

| Limited cold-chain infrastructure in emerging markets | −0.8% | Africa, rural Asia-Pacific, South America | Medium term (2-4 years) |

| Price sensitivity among smallholder farmers | −0.6% | Global, concentrated in developing regions | Long term (≥ 4 years) |

| Regulatory uncertainty around Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR)-edited okra varieties | −0.4% | Global, varies by jurisdiction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Vulnerability of Seed Supply to Yellow Vein Mosaic Virus Outbreaks

The 2024 Yellow Vein Mosaic Virus (YVMV) surge in northern India destroyed 30% of foundation seed beds, forcing emergency sourcing at inflated prices. Supply shortfalls ripple through planting seasons, driving retail prices beyond smallholder reach. Concentrated seed production zones heighten systemic exposure, prompting firms to diversify geography and build insect-proof screen houses. These measures lift overhead in the short term yet remain vital to safeguarding consistent supply.

Limited Cold-Chain Infrastructure in Emerging Markets

Treated seeds lose vigor rapidly when exposed to humidity and heat during transport. In sub-Saharan Africa, post-harvest seed losses exceed 25% because rural distributors lack refrigerated storage[3]International Food Policy Research Institute, “Cold Chain Infrastructure in Developing Countries,” ifpri.org. The resulting shrink forces companies either to absorb inventory write-offs or restrict distribution to well-served corridors. Solar-powered micro cold rooms offer promise, but adoption suffers from capital costs and maintenance skill gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Seed Type: Hybrid Dominance Drives Premium Positioning

Hybrid seeds captured 87.5% of the okra seeds market in 2024, underlining growers’ need for uniform yield and virus protection. The hybrid segment yields 15-22 metric tons per hectare versus 8-12 metric tons from traditional varieties, a difference that often offsets higher input costs during the first harvest cycle. Commercial farm consolidation and contract farming models amplify demand for proprietary hybrids because large buyers insist on consistent pod size and supply. Open-pollinated and organic lines retain cultural importance and niche appeal, expanding at a 10.9% CAGR to 2030 as health-conscious consumers embrace heritage produce. Community seed banks and regional seed festivals further bolster visibility for these varieties, creating micro-markets that reward biodiversity.

Across the Asia-Pacific, public institutes co-develop hybrids with private firms, allowing rapid dissemination through subsidized channels. In Africa, hybrid adoption is accelerating as vegetable exports to the Middle East rise, spurring quality specifications that local landraces struggle to meet. The okra seeds market size for organic/open-pollinated types remains modest but shows upside as e-commerce platforms curate specialty seed packets for urban gardeners. Hybrid seed pricing strategies now include smaller pack sizes to reach cash-constrained growers, ensuring continual infusion of new genetics into subsistence plots and sustaining overall okra seeds market growth.

By Seed Form: Treatment Technologies Expand Value Proposition

Treated seeds command 67% of the okra seeds market and deliver superior emergence and early vigor. Modern coatings embed biological inoculants alongside fungicides, creating a protective micro-environment around the radicle. Precision coaters adjust payload per kernel, reducing environmental run-off and enhancing field stand uniformity. Untreated seeds, compliant with organic certification, maintain a loyal base among specialty growers and record a 9.7% CAGR as eco-labeled produce gains shelf space.

Seed issuers often bundle treatment and advisory services, transforming simple product sales into integrated crop solutions. The okra seeds market share for novel film coatings that release micronutrients gradually during germination is projected to widen once cost curves fall. In regions with strict pesticide residue rules, biological seed treatments offer a regulatory workaround, keeping treated seeds attractive across diverse geographies.

By End Use: Commercial Scale Drives Volume Growth

Commercial farming commands 76% of seed demand because large holdings exploit hybrid vigor across broad acreage. Mechanized harvesting systems favor erect, uniform plants achievable only through controlled genetics, further cementing commercial dominance. Home gardening, though smaller, posts a 9.1% CAGR due to rooftop and balcony cultivation trends in densely populated cities. Seed firms market compact varieties with prolonged harvest windows and tender pods that suit kitchen gardens.

As disposable incomes rise, more urban dwellers prioritize fresh, pesticide-free vegetables, stimulating do-it-yourself cultivation. This behavioral shift anchors a resilient demand pillar that shields the overall okra seeds market from cyclical swings in commercial produce prices. Conversely, commercial farms anchor seed volume even during lean retail periods because supply contracts obligate planting schedules.

By Distribution Channel: Digital Platforms Reshape Access

Dealer and retail networks retained a 53.5% share in 2024 owing to long-standing credit facilities and agronomic advisory services. Direct-to-farmer sales hold a moderate share as multinationals build village-level depots to bypass intermediaries and secure brand loyalty. Online platforms only represent a minimal share but clock an 11.8% CAGR, propelled by smartphone penetration and reliable courier services.

Hybrid models are emerging in which farmers order via mobile apps and collect from local depots that provide planting guidance. Such schemas marry digital convenience with the human advisory layer crucial for complex products like treated hybrids. Seasonal demand spikes drive flash promotions on e-commerce sites, introducing price transparency into traditionally opaque markets and forcing brick-and-mortar dealers to refine service levels.

Geography Analysis

Asia-Pacific leads the okra seeds market with 52% of the market size and registers an 8.5% CAGR through 2030, underpinned by India’s good annual harvest and aggressive seed-replacement targets. Regional governments subsidize protected cultivation structures and drip irrigation, lifting seed turnover rates as growers experiment with densified planting systems. China and Japan contribute technology transfer and advanced breeding, while Vietnam and Indonesia bring emerging commercial acreage that opens new customer segments. Import-exempt status for vegetable seed in several Association of Southeast Asian Nations (ASEAN) economies speeds hybrid influx and stimulates local replication.

Africa posts a medium growth rate, driven by Nigeria’s rising urban demand and Kenya’s export corridors to Gulf markets. Development projects funded by multilateral agencies supply starter packs of hybrid seed and train extension officers, building technical literacy. Constraints revolve around limited refrigerated storage and uneven rural roads that inflate seed distribution costs. Nonetheless, expanding mobile money networks eases payment friction and facilitates direct-to-farmer deliveries, keeping the okra seeds market on a firm upward trajectory.

The Middle East also secured a medium growth rate, powered by national food-security plans and widespread adoption of climate-controlled greenhouses. High ambient temperatures compel growers to invest in specialized varieties that withstand heat and salinity, which in turn raises acceptable seed price bands. North America and Europe showcase the minimal growth rates, reflecting mature markets where incremental gains come from niche organic and ethnic-cuisine demand. South America is steered by Brazil’s expanding fresh-vegetable exports and protected niches in the Andean highlands suited for year-round production.

Competitive Landscape

The okra seeds market exhibits moderate concentration. The top five companies hold a significant combined market share. Advanta Seeds tops the chart owing to its broad hybrid lineup and entrenched distribution in India and Southeast Asia. Syngenta Group and Bayer Crop Science capture the following market shares, respectively, leveraging global research and development pipelines and strong dealer networks. Namdhari Seeds strengthened its footprint via the 2025 acquisition of Axia’s open-field vegetable division, expanding germplasm access across four complementary brands.

Technology is the central battlefront. Market leaders deploy genomics, doubled-haploid technology, and speed breeding to slash development cycles. Investments in Near-Infrared Spectroscopy (NIRS)-enabled quality control help guarantee purity and vigor, buttressing brand credibility. Smaller firms defend turf through localized adaptation, releasing cultivars tuned to microclimates and taste preferences. Joint ventures between multinationals and regional institutes proliferate, marrying global analytics with indigenous genetic diversity.

Consolidation momentum persists as firms seek scale to absorb rising regulatory costs for trait approvals and biosecurity compliance. Strategic partnerships extend beyond seed into crop-protection integration and post-harvest solutions, positioning companies for bundled product offerings. White-space opportunities remain in organic seed production and dual-use cultivars for nutraceutical oil extraction, where first movers can lock in premium positions.

Okra Seeds Industry Leaders

Advanta Seeds (UPL Limited)

Syngenta Group

Bayer AG

Sakata Seed Corporation

East-West Seed Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kaveri Seeds acquired the remaining 30% equity shares of Aditya Agritech Private Limited, where it previously held a 70% stake. Following this transaction, Kaveri Seed Company Limited now owns 100% of Aditya Agritech Private Limited, making it a wholly owned subsidiary. The acquisition aims to enhance operational synergies and expand market reach. Complete ownership enables Kaveri Seed Company Limited to streamline decision-making, improve efficiency, and accelerate product development and innovation.

- July 2023: Syngenta Vegetable Seeds has completed the acquisition of Feltrin Sementes, a Brazilian vegetable seed company that serves smallholder growers and home gardeners in more than 40 countries. The acquisition of Feltrin Sementes expands Syngenta's portfolio, enabling the company to provide comprehensive seed offerings to growers worldwide.

Global Okra Seeds Market Report Scope

| Conventional/Hybrid |

| Organic/Open-pollinated |

| Treated |

| Untreated |

| Commercial Farming |

| Home Gardening |

| Direct to Farmer (Company/Co-op) |

| Dealers and Retail Stores |

| Online Platforms |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | Nigeria |

| Kenya | |

| Rest of Africa |

| By Seed Type | Conventional/Hybrid | |

| Organic/Open-pollinated | ||

| By Seed Form | Treated | |

| Untreated | ||

| By End Use | Commercial Farming | |

| Home Gardening | ||

| By Distribution Channel | Direct to Farmer (Company/Co-op) | |

| Dealers and Retail Stores | ||

| Online Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the okra seeds market?

The okra seeds market size stands at USD 0.40 billion in 2025 and is projected to grow to USD 0.55 billion by 2030.

Which region leads demand for okra seeds?

Asia-Pacific is the largest regional consumer, supported by India’s dominant okra production and strong government seed-replacement schemes.

Why are hybrid okra seeds gaining traction?

Hybrids deliver higher yields and built-in disease resistance, making them attractive despite their premium price for commercial farms focused on consistent output.

How significant is online seed distribution?

Although online sales hold only a 7.5% share today, they are the fastest-growing channel at an 11.85% CAGR due to improved logistics and smartphone adoption.

What major constraint could affect market expansion?

Yellow Vein Mosaic Virus outbreaks pose the greatest immediate threat by disrupting seed supply chains and inflating prices.

Which technology is improving seed quality assurance?

Near-infrared hyperspectral imaging allows non-destructive testing for vigor and purity, reducing batch rejection and boosting field performance.

Page last updated on: