Dry Beans Market Size and Share

Dry Beans Market Analysis by Mordor Intelligence

The dry beans market size was valued at USD 12.81 billion in 2025 and is estimated to reach USD 13.50 billion in 2026. The market is further projected to reach USD 17.40 billion by 2031, registering a CAGR of 5.21% during the forecast period (2026–2031). Strong retail demand for plant proteins, wider crop-rotation benefits for growers, and supportive trade policies keep the growth engine running. Carbon-credit programs that reward nitrogen fixation are turning agronomic advantages into new revenue streams for producers. Food manufacturers are scaling bean-based snacks, pastas, and ready-to-eat meals, while quick-service chains test black-bean and chickpea patties to court younger diners who value sustainability. At the farm level, gene-edited drought-tolerant cultivars are moving from trial plots to commercial seed catalogs, especially in water-scarce regions. These drivers coexist with headwinds such as pest outbreaks, yield swings linked to extreme weather, and labor constraints in smallholder systems, creating a patchwork of opportunities and risks that stakeholders in the dry beans market navigate daily.

Key Report Takeaways

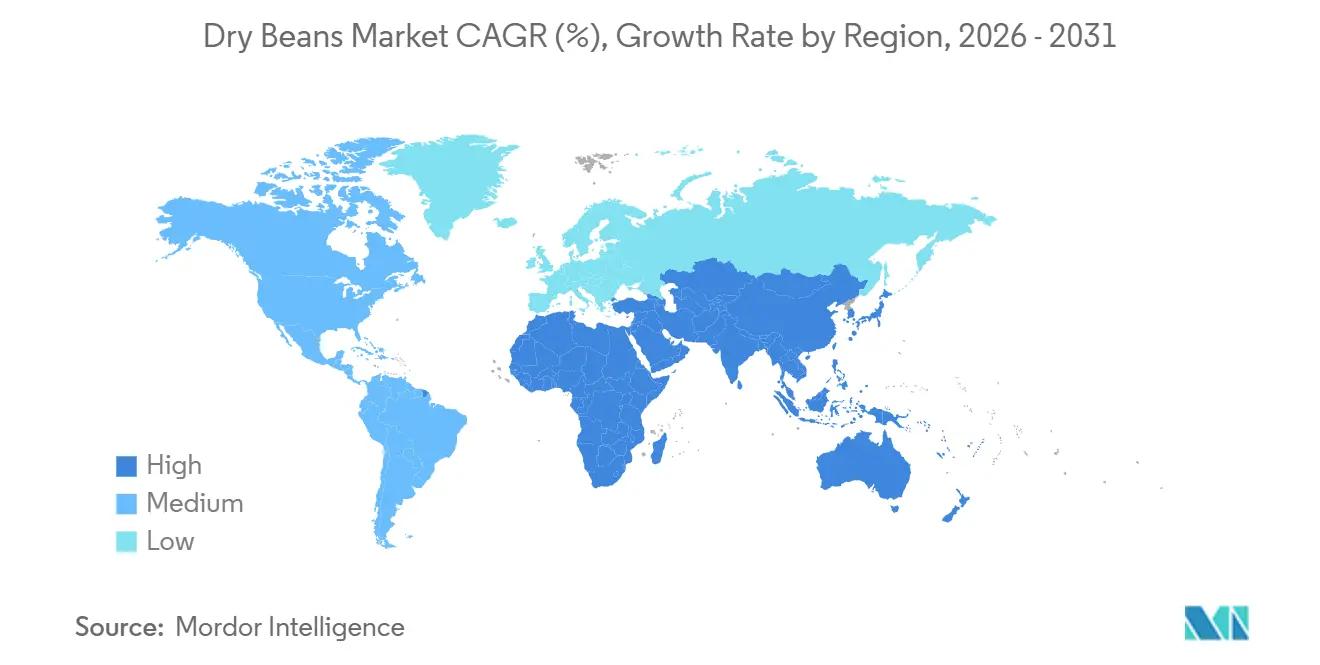

- By geography, the Asia-Pacific region accounted for 41.2% of the dry beans market share in 2025, while the Middle East is projected to register a 6.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dry Beans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global adoption of vegan and flexitarian diets | +1.2% | North America, Europe, and emerging Asia-Pacific urban hubs | Medium term (2 to 4 years) |

| Expanding pulse-crop rotations in cereal-dominant regions | +0.9% | North America, Europe, and Asia-Pacific grain belts | Long term (≥ 4 years) |

| Import tariff cuts on plant proteins in high-income nations | +0.6% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Monetization of on-farm carbon credits for nitrogen-fixing beans | +0.7% | North America, Europe, and pilot sites in South America | Medium term (2 to 4 years) |

| Gene-edited drought-tolerant cultivar commercialization | +0.8% | United States, Australia, Brazil, and research clusters worldwide | Long term (≥ 4 years) |

| Surge in demand for gluten-free staple foods | +1.0% | North America and Europe with global spillover | Medium term (2 to 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Adoption of Vegan and Flexitarian Diets

Consumers reducing animal protein intake are driving higher household purchases of pulses, particularly dried beans. The plant-based retail sector in Europe has nearly doubled in value over the past five years, reflecting strong demand for sustainable alternatives. Shelf space for bean-based snacks, pasta, and ready meals continues to expand, while quick-service restaurants are piloting chickpea and black-bean burgers to appeal to younger diners. Institutional caterers in schools and hospitals are also incorporating more legume dishes to align with health guidelines and carbon reduction targets. Retail data show consistent growth in the consumption of dry beans and other pulses, even when meat prices decline, signaling a structural shift in dietary preferences. Uptake is strongest in metropolitan areas, but similar trends are emerging in secondary cities across North America.

Expanding Pulse-Crop Rotations in Cereal-Dominant Regions

Growers in temperate grain belts are increasingly adopting pulse rotations due to the clear agronomic and economic benefits they offer. United States field trials show that wheat crops grown after legumes experience noticeable yield improvements. This is because legumes naturally enrich the soil by depositing nitrogen and help suppress harmful pathogens[1]Source: United States Department of Agriculture Agricultural Research Service, “Pulse Crop Rotation Benefits,” ars.usda.gov. Incentives from agricultural policies and high fertilizer costs have strengthened the case for rotating beans with barley and wheat. In Australia, pulses are also used as biological break crops to combat herbicide-resistant weeds. Mechanized farms integrate beans quickly, whereas smallholders in South Asia and Africa face challenges due to limited access to seeds and extension services. Rotation benefits remain compelling wherever synthetic fertilizer costs remain elevated, making dry beans and other pulses a valuable complement to cereal systems.

Gene-Edited Drought-Tolerant Cultivar Commercialization

Advances in Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR) technology are accelerating the development of bean cultivars that maintain yields under water stress. Field trials are underway for drought-tolerant lines engineered with deeper roots and improved osmotic balance, building on natural resilience traits. Regulatory frameworks in several countries classify many gene-edited crops as non-transgenic, shortening approval timelines and encouraging private-sector investment. Seed companies anticipate commercial sales later this decade, targeting arid zones where water scarcity limits the production of common beans. Adoption will depend on seed pricing and proven yield stability, but early demonstration plots show promising results. These innovations could reshape production in regions most vulnerable to climate variability.

Surge in Demand for Gluten Free Staple Foods

Growing awareness of celiac disease and non-celiac gluten sensitivity is boosting demand for gluten-free products worldwide. Bean flours are increasingly used as substitutes for wheat in bread, pasta, and snacks, offering protein and fiber without gluten. Food manufacturers capture significant premiums for gluten-free variants, and traditional recipes in countries such as Italy and France are evolving to incorporate more pulses. Public health campaigns encourage higher intake of dry beans, reinforcing their role as nutritious staples. Sensory challenges remain, but research into enzyme treatments and fermentation is improving texture and flavor. These advances are widening consumer acceptance and expanding the market for gluten-free pulse-based foods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pest and disease vulnerability elevating farm-gate losses | -0.7% | North America, South Asia, and East Africa | Short term (≤ 2 years) |

| Yield volatility from extreme weather cycles | -0.9% | Africa, South Asia, and North America | Short term (≤ 2 years) |

| Slow mechanization in smallholder regions | -0.5% | Africa, South Asia, and parts of South America | Long term (≥ 4 years) |

| Rising labor costs in key producing countries | -0.6% | North America, Europe, Brazil, and Asia-Pacific | Medium term (2 to 4 years) |

| Source: Mordor Intelligence | |||

Pest and Disease Vulnerability Elevating Farm-Gate Losses

Diseases such as halo blight and white mold can severely reduce yields, with losses reaching up to half of potential output in affected fields[2]Source: United States Department of Agriculture Agricultural Research Service, “Halo Blight and White Mold Disease Management 2024,” ars.usda.gov. Resistant varieties and fungicides help mitigate damage, but many smallholders lack access to these solutions. Climate change is intensifying risks by allowing pests to overwinter in regions previously protected by frost, expanding outbreaks. Quality downgrades from discoloration or shriveled seeds further erode farm-gate prices, reducing farmer incomes. Breeding programs focused on durable resistance are crucial in countering these threats. Wider access to integrated pest management (IPM) tools will be critical to reducing losses and stabilizing production.

Yield Volatility from Extreme Weather Cycles

Extreme weather events are a major source of yield volatility in pulse production. Droughts during critical growth phases can sharply reduce output, while excessive rainfall encourages fungal diseases and disrupts pollination. Irrigation can triple yields, yet the Food and Agriculture Organization (FAO) estimates show only a small fraction of African farmland is irrigated, leaving millions of farmers exposed[3]Source: Food and Agriculture Organization, “Agricultural Mechanization and Labor Savings in Bean Harvesting 2024,” fao.org. Crop insurance provides protection in developed markets, but similar tools remain scarce in developing regions. This lack of safety nets amplifies income shocks and discourages investment in pulse farming. Addressing weather-related risks will be central to ensuring stable supply and farmer resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

The Asia-Pacific region accounted for 41.2% of the dry beans market share in 2025, underscoring its role as the largest regional base. India anchors this position with substantial output, while China remains a major importer even as it signals greater self-sufficiency. Myanmar and other Southeast Asian countries highlight the region’s export orientation, channeling beans into international markets. Australia contributes through mechanized farms that integrate pulse rotations with cereals, improving soil fertility and supporting export flows. Rising urban incomes and shifts in dietary preferences toward plant-based foods continue to drive consumption growth. Together, these dynamics reinforce the Asia-Pacific region’s dominance in both production and demand, positioning it as the global hub for dry beans.

The Middle East dry beans market size is projected to grow at a CAGR of 6.8% through 2031, making it the fastest-growing region in the dry beans market. Turkey and Iran are expanding domestic acreage to reduce reliance on imports, while broader regional initiatives emphasize food security. Government-backed programs encourage farmers to diversify cropping systems, supporting pulses as a strategic staple. Rising consumer demand for plant proteins is also reshaping dietary preferences, creating opportunities for local producers. The region’s growth trajectory reflects a combination of policy support, shifting consumption habits, and investment in agricultural modernization. As these factors converge, the Middle East is set to become a key driver of global dry bean expansion.

North America remains a critical export hub, with the United States and Mexico contributing significant volumes despite weather-related yield swings. South America is centered on Brazil, where rising domestic consumption absorbs much of the output, while Argentina’s crop-mix shifts add volatility. Europe exhibits diverse trends, with Russia, Italy, and France promoting the consumption of dry beans and other pulses, and Germany importing heavily to meet its plant-protein demand. Africa remains dominated by smallholder systems, where the Food and Agriculture Organization estimates show beans are among the most important food crops. Limited irrigation magnifies weather risks, constraining yield gains relative to irrigated benchmarks. Collectively, these regions balance global supply and demand.

Regulatory Landscape

Regulation of dry beans (HS-0713 scope) is primarily shaped by import food-safety and contaminant-control regimes, as well as pesticide-residue compliance in destination markets. In the European Union, General Food Law traceability requirements apply to imported pulses, while official controls can intensify under Commission Implementing Regulation (EU) 2019/1793 for food of non-animal origin where contaminant risks (including mycotoxins and pesticide residues) are prioritized. Exporters commonly rely on compliance with EU Maximum Residue Levels under Regulation (EC) No 396/2005, including the 0.01 mg/kg default for non-specified substances, to clear market access.

In the United States, imported dry beans are governed under the FDA framework for food imports, including the Food Safety Modernization Act (FSMA) and Foreign Supplier Verification Program (FSVP) expectations for importers of raw agricultural commodities intended for further processing. Internationally, Codex Alimentarius standards and HACCP-based management principles are widely referenced in buyer specifications and quality programs. In January 2026, EFSA published a scientific opinion on plant lectins in food (EFSA Journal 2026;24:9850), which reinforced the public-health importance of adequate soaking and boiling of dried beans and increased focus on consumer-preparation communication and downstream handling practices, even where explicit label mandates are not codified.

Value Chain Analysis

The dry beans value chain starts with seed and input suppliers, then moves through growers, ranging from mechanized farms in North America and Australia to smallholder systems in parts of Africa and South Asia. Primary cleaning, grading, and handling by elevators and processors follow, and then flows typically pass through traders, brokers/indenters, importers, warehousing and shipping providers, and custom brokers before reaching bulk buyers and food manufacturers. Large agribusiness and trading houses, including Archer Daniels Midland Company, Cargill Incorporated, Louis Dreyfus Company B.V., and Olam Agri, play a central role in aggregation, risk management, and global distribution.

Key friction points include uneven access to improved seed, irrigation constraints, long distances between production zones and consumption or export gateways, and post-harvest losses tied to storage and logistics gaps. Market development and trade facilitation programs influence commercialization and export readiness, including USDA Foreign Agricultural Service support via the Market Access Program (MAP), Foreign Market Development (FMD), and Emerging Markets Program (EMP), alongside coordination and information-sharing bodies such as the International Grains Council (IGC) and trade groups such as the India Pulses and Grains Association (IPGA). In the United States, production concentration is visible at the farm gate, with North Dakota, Minnesota, and Michigan accounting for 82% of planted dry bean acreage in 2025, which elevates the importance of regional processing capacity, storage, and outbound logistics from these hubs.

Competitive Landscape

Major multinational agribusinesses, including Archer Daniels Midland Company, Cargill Incorporated, Louis Dreyfus Company B.V., and Olam Agri Holdings Pte Ltd., play a significant role in the dry beans market. Their operations encompass procurement, processing, and global distribution, linking producers with international buyers. These companies utilize economies of scale, advanced logistics infrastructure, and commodity trading expertise to stabilize supply chains and manage price fluctuations. Their strategies often integrate dry beans into broader portfolios of pulses and grains, ensuring consistent availability across various markets. Additionally, they influence production incentives, farmer practices, and sustainability benchmarks, making them essential to the long-term resilience of the dry beans market.

Companies such as Goya Foods Inc., Bonduelle SA, Bush Brothers & Company, and Conagra Brands Inc. are key stakeholders in the dry beans market. These firms process dry beans into packaged, canned, or ready-to-eat products, bridging the gap between agricultural supply and consumer demand. Their contributions include branding, product innovation, and promoting consumption through convenience foods and health-oriented offerings. By investing in marketing and distribution, they shape consumer preferences and drive demand growth in both established and emerging markets. These companies also respond to dietary trends, positioning beans as cost-effective sources of protein and fiber. Their purchasing decisions and quality standards have a significant impact on growers and processors, underscoring their role in shaping the market's trajectory.

Stakeholders such as AGT Food and Ingredients Inc. and J.R. Simplot Company bring specialized expertise and diversified portfolios to the dry beans market. AGT focuses extensively on pulses, including dry beans, offering processing, packaging, and export services that enhance global trade flows. J.R. Simplot, while primarily associated with potatoes, diversifies into beans and other crops, contributing to the resilience of agricultural supply chains. These companies often leverage regional strengths, connecting local producers with international buyers while maintaining flexibility in their product offerings. Their strategies emphasize innovation in processing, sustainability initiatives, and niche market development. Alongside larger agribusinesses and consumer brands, these stakeholders ensure the market remains dynamic, striking a balance between global scale and regional specialization to meet changing demand patterns.

Market Opportunities and Future Outlook

Opportunities in dry beans increasingly show up as farm-level efficiency gains and in supply-chain risk management tied to concentrated production geographies. Research validating lower energy use for strip-planting systems in pinto beans (relative to flat systems) and associated yield improvements points to headroom for equipment, agronomy services, and input packages that reduce cost per ton while stabilizing output under variable weather. On the risk-management side, the market remains sensitive to localized climate and policy shocks because production is concentrated in a limited set of major origins, notably India, Nigeria, and Brazil, which supports diversification in sourcing strategies, origin expansion programs, and investment in post-harvest storage and quality preservation to protect exportable grades.

Institutional support also creates concrete pathways for adoption and differentiation. In Michigan, the Michigan Bean Commission has run a systems-based approach project supported by the USDA Specialty Crop Block Competitive Grant Program to validate alternative agronomic practices and weed control strategies, providing an applied template for scaling similar initiatives in other producing regions. Separately, buyer requirements in import-heavy markets, notably the EU and the United States, lift the value of traceability and residue-compliance capabilities, supporting services in testing, documentation, and identity preservation for premium or specialty lots that compete for shelf space alongside expanding bean-based snacks, pastas, and ready-meal applications.

Recent Industry Developments

- April 2026: Columbia Grain International held the grand opening of a new pulse processing plant in Valley City, North Dakota, focused on black and pinto dry beans. The added processing footprint strengthens a key US origin region that supplies export and domestic channels, supporting tighter quality control and more efficient throughput from farm to buyer.

- March 2026: Melandri Gaudenzio launched a new line of hulled legumes that includes cannellini beans. The launch expands value-added offerings around dry beans, aligning with demand for convenient, differentiated pulse formats in retail and foodservice ingredient channels.

- December 2024: CHS Inc. expanded dry bean processing capacity at its Othello facility in the Pacific Northwest. The expansion increases the region's ability to handle higher volumes and supports CHS in serving customers seeking affordable plant-based protein and consistent supply from a major US growing and logistics corridor.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this methodology, the dry beans market is defined as the traded and consumed value of dried, shelled beans at the primary processing stage, covering domestic use and exports across major producing and importing countries.

Scope exclusions: Fresh green beans, soybeans, chickpeas, and revenue from canned, ready-to-eat, or further processed bean products are excluded.

Segmentation Overview

- By Geography

- North America

- United States

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Mexico

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- United States

- Europe

- Russia

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Italy

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- France

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Germany

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Russia

- Asia-Pacific

- China

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- India

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Myanmar

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Australia

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- China

- South America

- Brazil

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Argentina

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Brazil

- Middle East

- Turkey

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Iran

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Turkey

- Africa

- Tanzania

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Kenya

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- South Africa

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Tanzania

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the supply and trade picture for dried beans using public agriculture and trade statistics, and then aligning it with price signals. We typically reference sources such as FAOSTAT for production and yield, UN Comtrade for HS-coded trade flows (including HS-0713), and national agriculture statistics portals for area harvested and farmgate movements.

To ground pricing and consumption context, we also review sources such as USDA market and PSD style tables, World Bank commodity and macro series for inflation and FX context, and customs or port authority releases where they are available. Company filings, investor presentations, and reputable press are used mainly to understand procurement patterns and processing linkages, while paid subscriptions are used selectively for company financials, shipment-level import and export checks, and patent databases when product handling or storage innovations matter. These examples are illustrative, and many other public sources were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm the real-world links between production, traded volumes, and achievable price levels by region, before final totals are locked. We speak with a mix of growers and aggregators, processors, traders, distributors, and large buyers, and then we re-check assumptions across APAC, EMEA, and the Americas so regional balances and trade directions make sense.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 16% | APAC: 46% |

| Mid tier: 53% | Functional/Unit leaders: 30% | EMEA: 33% |

| Smaller Players: 21% | Managers: 54% | Americas: 21% |

Market-Sizing & Forecasting

The market is sized using a top-down build that reconstructs value from country level production, net trade, and wholesale price trends for dried beans, followed by regional rollups. Where the data is incomplete, we use practical gap handling such as proxying missing prices from nearby reference markets, and then normalizing with inflation and FX movements so values remain comparable.

To keep the model realistic, totals are corroborated with selective bottom-up approximations such as sampled price times volume checks for major corridors, and channel conversations that confirm typical spreads between farmgate, wholesale, and export parity pricing. Inputs that matter most include harvested area and yield movements, export and import volumes under HS-0713, wholesale price seasonality tied to harvest calendars, stock tightness signals reflected in trade swings, and currency conversion timing for key producing nations.

For forecasting, we lean on scenario analysis tied to supply and trade drivers, since weather-linked yields and trade policies can shift availability quickly. Assumptions are then stress-tested with primary feedback on expected acreage intent, price pass-through behavior, and likely trade redirection, and the final CAGR path is adjusted only when the signals line up across regions.

Data Validation & Update Cycle

Validation is done through repeated cross-checks between independent indicators, so production, trade, and pricing do not tell conflicting stories. We run variance checks at country and regional level, review outliers that may come from one-off policy changes or abnormal harvest years, and then re-contact sources when a key assumption shifts beyond a reasonable band.

Before sign-off, the model is reviewed in multiple steps by analysts, with special attention to currency conversions, unit consistency, and year alignment across datasets. Reports are refreshed annually, and interim updates are triggered when material events occur such as major crop shocks, sudden trade restrictions, or sustained price spikes, and then a final pass is completed right before delivery so clients receive the latest view.

Mordor Intelligence's Dry Beans Market Size Compared Against Other Published Estimates

Published market sizes for dry beans can look far apart, even when they seem to cover similar geographies. The gaps usually come from what stage of the value chain is counted, which bean families are included, and how prices and currency conversions are timed across countries.

A refresh-led difference is also common in this market because crop years, harvest-driven price swings, and FX moves can change the USD value quickly, and the spread widens when older price points are carried forward. When wholesale prices are updated with a consistent timing rule and then validated against production and HS-0713 trade movements, the total stays anchored to the same demand and trade pool, which is how Mordor Intelligence keeps its 2025 to 2026 transition and ASP progression logic consistent across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.81 B (2025) | |

| Industry Publisher A | USD 7.50 B (2025) | Uses a broader consumer and packaging-led scope, which can mix primary dry beans with packaged formats and channel margins, and it can apply different pricing bases across countries that are not always aligned to the same crop or trade year. |

| Research Publisher B | USD 4.93 B (2024) | Base year and scope appear more retail and end-user oriented, and the value capture can exclude parts of export-linked trade economics, with less clarity on how FX timing and wholesale-to-retail price steps are converted into a comparable USD series. |

The table shows that the biggest drivers of difference are scope boundaries and price building choices, not just growth expectations. By keeping the count tied to primary-stage dry beans and by checking USD values against trade and production signals, our estimate remains easier to trace, update, and explain when market conditions change year to year.

Key Questions Answered in the Report

What is the estimated current size of the dry beans market, and what is its projected size by 2031?

The dry beans market size is estimated to reach USD 13.50 billion in 2026 and is projected to climb to USD 17.40 billion by 2031.

What is the compound annual growth rate (CAGR) projected for the dry beans market from 2026 to 2031?

The market will advance at a 5.21% CAGR from 2026 to 2031.

Which region held the largest revenue share of the dry beans market in 2025?

Asia-Pacific led with 41.2% share in 2025 due to strong production in India and sizable import demand from China and other economies.

Which geography is projected to record the fastest CAGR through 2031?

The Middle East shows the fastest growth, with a 6.8% CAGR projected through 2031 as Turkey and Iran boost output and consumption.

What are the main growth drivers of the dry beans market projected through 2031?

Rising vegan and flexitarian diets, wider pulse rotations, tariff reductions on plant proteins, carbon credit programs, and gene-edited drought-tolerant seeds all support demand.

Which pests and diseases are projected to pose the greatest threat to dry bean yields through 2031?

Halo blight, white mold, and rust diseases top the list, cutting yields by up to 50% when control measures are lacking.

Page last updated on: